Deck 12: Property Transactions: Treatment of Capital and Section 1231 Assets

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

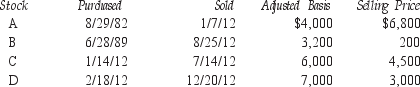

For 2012, Steven Sutton had taxable income of $40,000. His stock transactions in 2012 were as follows:  What is Steve's net capital loss for 2012 and his carryover to 2013?

What is Steve's net capital loss for 2012 and his carryover to 2013?

A) Deduction: $3,000; carryover: $2,700

B) Deduction: $3,000; carryover: $3,000

C) Deduction: $5,700; carryover: $3,000

D) Deduction: $5,700; carryover: $2,700

What is Steve's net capital loss for 2012 and his carryover to 2013?A) Deduction: $3,000; carryover: $2,700

B) Deduction: $3,000; carryover: $3,000

C) Deduction: $5,700; carryover: $3,000

D) Deduction: $5,700; carryover: $2,700

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

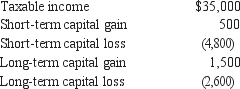

For 2012, Joyce Jacobson's books and records reflected the following:  What is the amount of Joyce's capital loss carryover to 2013?

What is the amount of Joyce's capital loss carryover to 2013?

A) $2,400 short-term; $0 long-term

B) $1,300 short-term; $1,100 long-term

C) $1,900 short-term; $3,500 long-term

D) $4,300 short-term; $1,100 long-term

What is the amount of Joyce's capital loss carryover to 2013?A) $2,400 short-term; $0 long-term

B) $1,300 short-term; $1,100 long-term

C) $1,900 short-term; $3,500 long-term

D) $4,300 short-term; $1,100 long-term

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/111

Play

Full screen (f)

Deck 12: Property Transactions: Treatment of Capital and Section 1231 Assets

1

Regardless of the length of the holding period, nonbusiness bad debts are considered short-term capital losses in the year they become completely worthless.

True

2

Section 1231 property includes depreciable or real property used in a trade or business (for example, machinery, equipment, buildings, and land).

True

3

fte ordinary loss provisions on small business stock (Code Sec. 1244) are available only to the original owner of the stock.

True

To claim the deduction under Section 1244, the individual must have continuously held the stock from the date of issuance

Section 1244(a) provides that an individual is entitled to an ordinary loss deduction on the sale of Section 1244 stock issued to such individual.

To claim the deduction under Section 1244, the individual must have continuously held the stock from the date of issuance

Section 1244(a) provides that an individual is entitled to an ordinary loss deduction on the sale of Section 1244 stock issued to such individual.

4

For property to be held long-term, it must be held for one year.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

5

For purposes of determining the holding period for property, the holding period begins on the day the property is acquired and ends on the day before the sale of the property.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

6

If a taxpayer's stock in a corporation becomes worthless as a result of the corporation's insolvency during the tax year, the taxpayer's loss is a capital loss as if it occurred on the last day of the year.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

7

In March 2011, Jim Jorges formed a small business corporation and issued Section 1244 small business stock. In November 2012, the company went bankrupt and Jim incurred a $75,000 loss for amounts invested in the common stock of the small business corporation. If Jim files a joint return, he should report a $50,000 ordinary loss and a $25,000 long-term capital loss.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

8

A "sale or exchange" must occur in order to recognize capital gains and losses.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

9

Doug Draper's capital losses exceeded the $3,000 capital loss limitation. He may elect to carry the unused capital loss back to an earlier year.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

10

On February 9, 2011, Ed Earlson purchased a rare gem as an investment. On August 26, 2011, he exchanged it for another rare gem in a nontaxable exchange. On February 10, 2012, he sold it for cash. Any gain or loss on the sale is a long-term capital gain or loss.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

11

fte maximum capital loss deductible in any one year by a taxpayer is generally $3,000 with an indefinite carryover period.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

12

If the sale or exchange of a patent qualifies for capital gain treatment, the holding period of the inventor determines whether the gain is long-term or short-term.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

13

Some examples of capital assets are stocks and bonds held in a personal account, a personal residence, and household furnishings.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

14

Securities held by a brokerage firm are capital assets.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

15

Real property used in a trade or business is a capital asset.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

16

Payments made to a taxpayer for a franchise that are based upon the profitability of the franchise are considered to be a capital gain.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

17

Fully depreciated property used in a trade or business is a capital asset.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

18

Capital assets do not include inventory, depreciable property, copyrights, accounts receivable, or literary, musical or artistic compositions.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

19

On receipt of a gift of property purchased by the donor in 2007 the basis is determined by the donor's basis. fte holding period begins on the day the gift is received.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

20

Ned Newell transferred all substantial rights to a trade secret to an unrelated third party for $25,000. Ned must report the entire proceeds as ordinary income.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

21

Section 1245 and 1250 recapture rules apply to both gain and loss realized situations.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

22

If business casualty losses exceed business casualty gains, the gains are ordinary income and the losses are deductible for adjusted gross income.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

23

When the basis of the taxpayer's property is determined in whole or in part by reference to another asset, the holding period of the taxpayer's property includes the holding period of the other asset.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

24

Section 1245 recapture rules do not apply to nonresidential real property if its cost is recovered under the ACRS statutory (accelerated) method.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

25

Personal casualty losses are determined and considered in their netting before considering the $100 reduction.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

26

Section 1245 property includes depreciable machinery and equipment and amortizable patents and leaseholds of machinery and equipment.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

27

For individuals, the deduction for capital losses is limited to the capital gains included in gross income plus

$3,000; any unused capital losses are carried forward five years.

$3,000; any unused capital losses are carried forward five years.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

28

Section 1231 property includes inventory, copyrights, and literary compositions.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

29

fte recapture potential as ordinary income under Sections 1245 and 1250 reduces the amount of charitable contribution deduction allowed.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

30

Section 1245 requires that all realized gain from the sale of Section 1245 property be recaptured as ordinary income.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

31

For the individual taxpayer, all gain recognized is 15-percent gain if 15-year, 18-year, or 19-year real property under ACRS is depreciated on a straight-line basis.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

32

Section 1250 recapture rules apply to all depreciable real property.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

33

If Section 1231 gains exceed Section 1231 losses, the excess of the gains over the losses is added to long-term capital gains, assuming there are no prior years' net Section 1231 losses to recapture.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

34

If Section 1231 losses exceed Section 1231 gains, losses are netted with long-term capital losses and gains are netted with long-term capital gains.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

35

Section 1231 gains in one year are used to offset Section 1231 losses in the next year.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

36

Gain is recaptured as ordinary income to the extent of total depreciation taken when residential real property depreciated under ACRS is sold.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

37

In making a charitable transfer of Section 1245 property, the recapture that would have occurred had the property been sold has no effect on the amount of the charitable contribution deduction.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

38

If business casualty gains exceed business casualty losses, the excess of the gains over the losses is netted with Section 1231 gains and losses.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

39

fte recapture rules under Section 1245 depend on the depreciation method used.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

40

Although the recapture provisions of Sections 1245 and 1250 do not apply to the act of giving a gift, the recapture potential carries over to the donee.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

41

Ralph Robinson has a long-term capital loss of $3,000, a short-term capital loss of $2,000, a short-term capital gain of $1,000 and taxable income of $12,500. His deductible capital loss is $2,500.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

42

For 2012, Steven Sutton had taxable income of $40,000. His stock transactions in 2012 were as follows: What is Steve's net capital loss for 2012 and his carryover to 2013?

A) Deduction: $3,000; carryover: $2,700

B) Deduction: $3,000; carryover: $3,000

C) Deduction: $5,700; carryover: $3,000

D) Deduction: $5,700; carryover: $2,700

What is Steve's net capital loss for 2012 and his carryover to 2013?A) Deduction: $3,000; carryover: $2,700

B) Deduction: $3,000; carryover: $3,000

C) Deduction: $5,700; carryover: $3,000

D) Deduction: $5,700; carryover: $2,700

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

43

Individuals are entitled to a 50% capital gains deduction.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

44

Gain on the sale of 19-year real property for which the straight-line ACRS election is made is not subject to Code Sec. 1250 depreciation recapture (taxed as ordinary income) unless it is held for one year or less.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

45

Capital gains and losses generally do not result unless there is a sale or exchange. An exception to this rule occurs when an investor holds corporate stock that becomes worthless.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

46

A real estate dealer who holds property as part of his stock-in-trade is not subject to capital gains treatment of gains and losses on the sale of the property.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

47

Oscar Orsen is an officer of Atlas Company. He loaned the company $10,000 but was unable to collect it because the company went bankrupt a year after the loan was made. Oscar did not own any stock in the company and the loan was not a condition of employment. How should Oscar report this loss?

A) Nondeductible gift

B) Short-term capital loss

C) Long-term capital loss

D) Miscellaneous itemized deduction

E) Business bad debt

A) Nondeductible gift

B) Short-term capital loss

C) Long-term capital loss

D) Miscellaneous itemized deduction

E) Business bad debt

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

48

An individual taxpayer with $10,000 of surviving short-term capital loss may deduct no more than $3,000 of the loss against ordinary income during any single tax year.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following is a capital asset?

A) Property held primarily for sale to customers

B) Accounts or notes receivable acquired in the ordinary course of business

C) Machinery and equipment used in a trade or business

D) Temporary investment of idle business cash in marketable corporate securities

E) Real property used in a trade or business

A) Property held primarily for sale to customers

B) Accounts or notes receivable acquired in the ordinary course of business

C) Machinery and equipment used in a trade or business

D) Temporary investment of idle business cash in marketable corporate securities

E) Real property used in a trade or business

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

50

Susan Short had net long-term capital losses that exceeded the $3,000 capital loss limitation. fte unused portion may be carried over as a short-term capital loss.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

51

Becky Best received a long-term capital gain distribution of $350 from her stock in MXM Corporation. She also had a $4,000 short-term capital gain, a $3,000 long-term capital loss and a short-term capital loss carryover from 2011 of $1,200. What is Becky's net capital gain or (loss)?

A) $150

B) $4,000

C) ($3,000)

D) ($4,200)

A) $150

B) $4,000

C) ($3,000)

D) ($4,200)

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

52

Even though a husband and wife file a joint return, each spouse's capital gains and losses are separately calculated.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

53

If a business elected or was required to use straight-line depreciation under the alternative depreciation system for personal property, only a percentage of straight-line depreciation taken is subject to recapture as ordinary income.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

54

Henry Hoover operates a freight line which delivers a substantial number of boats made by Walter Company. During 2012, Henry made a loan of $45,000 to Walter Company in order to maintain their business. Walter Company went bankrupt in 2012 and did not repay Henry's loan. Henry is entitled to which of the following in 2012?

A) $0 loss

B) $3,000 short-term capital loss

C) $27,000 long-term capital loss

D) $45,000 ordinary loss

E) $45,000 short-term capital loss

A) $0 loss

B) $3,000 short-term capital loss

C) $27,000 long-term capital loss

D) $45,000 ordinary loss

E) $45,000 short-term capital loss

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

55

In the case of an individual taxpayer, unused capital losses may be carried forward for an unlimited number of years.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

56

fte disposition of inherited property results in long- or short-term gain or loss, depending on the actual time the taxpayer holds the property or the decedent had held the property.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

57

fte tax laws require that net Section 1231 gain be recaptured as ordinary income to the extent that the taxpayer has nonrecaptured Section 1231 losses from the previous five tax years.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

58

For 2012, Greg Grammer had a short-term capital loss of $4,000, a short-term capital gain of $1,900, a short- term capital loss carryover from 2011 of $700, a long-term capital gain of $800, and a long-term capital loss of $1,000. What is Greg's deductible loss in 2012?

A) $0

B) $2,560

C) $2,800

D) $2,900

E) $3,000

A) $0

B) $2,560

C) $2,800

D) $2,900

E) $3,000

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

59

If the property sold in an installment sale is subject to depreciation recapture, the tax law requires that a portion of the amount of depreciation recapture be recognized as ordinary income in the year of sale, depending on the amount of cash the taxpayer receives during the year.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

60

George Grant runs a hot dog stand. During the year, he sells an oven and a refrigerator that were used in his business and held for five years. He had a gain of $500 on the oven and a loss of $1,000 on the refrigerator. If these are his only sales or exchanges during the tax year, George will treat the gain as long-term capital gain and the loss as long-term capital loss.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

61

Tom Truman sells a business machine which he has owned for four years for $27,000. Tom purchased the machine for $42,000 and has taken $18,000 in depreciation. How much and what type of gain will result from this sale?

A) $3,000 long-term capital gain

B) $3,000 ordinary income

C) $18,000 ordinary income; $3,000 long-term capital gain

D) $3,000 Section 1231 gain

A) $3,000 long-term capital gain

B) $3,000 ordinary income

C) $18,000 ordinary income; $3,000 long-term capital gain

D) $3,000 Section 1231 gain

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

62

Karen Kirbey grants Pamela Prentiss a franchise to sell handcrafted gifts. Pamela pays Karen 15 percent of all revenue. Sales for 2012 were $550,000. How will Pamela treat her payment to Karen on her tax return?

A) $82,500 short-term capital loss

B) $82,500 long-term capital loss

C) $82,500 nonbusiness deduction

D) $82,500 business expense deduction

A) $82,500 short-term capital loss

B) $82,500 long-term capital loss

C) $82,500 nonbusiness deduction

D) $82,500 business expense deduction

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

63

All of the following property is used in a trade or business and has been held in excess of one year. Which property will not qualify for gains or losses from Section 1231 property upon its disposition by sale or exchange?

A) Property includible in inventory

B) Business property condemned for public use

C) Property held for production of rent and royalties

D) Depreciable property used in a trade or business

A) Property includible in inventory

B) Business property condemned for public use

C) Property held for production of rent and royalties

D) Depreciable property used in a trade or business

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

64

Sam Shoeman, a calendar year taxpayer, purchased stock in Eaton Corporation on July 12, 2012, for $2,500. On December 12, 2012, Eaton went bankrupt. What is Sam's 2012 loss?

A) $2,500 long-term capital loss

B) $2,500 ordinary loss

C) $2,500 short-term capital loss

D) No loss

A) $2,500 long-term capital loss

B) $2,500 ordinary loss

C) $2,500 short-term capital loss

D) No loss

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

65

Wade Woodruff purchased a factory building on January 1, 1980 for $375,000. At the time of Wade's death in 2012, he had taken $20,000 in excess depreciation. fte factory building was transferred to his son John at the time of Wade's death and John sold it immediately after receiving it at a gain of $30,000. What amount of depreciation needs to be recaptured by Wade's estate and what amount by John?

A) $0/$0

B) $20,000/$0

C) $0/$20,000

D) $10,000/$10,000

A) $0/$0

B) $20,000/$0

C) $0/$20,000

D) $10,000/$10,000

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

66

Milton Manse, who has a salary of $50,000 during 2012, has a net long-term capital loss of $2,000 and a net short-term capital loss of $3,000 in 2012. What are his 2012 capital loss deduction and carryover?

A) $3,000 deduction; $2,000 LTCL carryover

B) $3,000 deduction; $1,000 LTCL carryover

C) $5,000 deduction; no carryover

D) $2,500 deduction; no carryover

A) $3,000 deduction; $2,000 LTCL carryover

B) $3,000 deduction; $1,000 LTCL carryover

C) $5,000 deduction; no carryover

D) $2,500 deduction; no carryover

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

67

All of the following are considered in the first or second netting except:

A) Fire loss on a business office building owned five years.

B) Gain from insurance recovery on vandalism to a business truck owned two years.

C) Loss on condemnation of business land held for 13 months.

D) fteft of uninsured jewelry owned for 11 months.

A) Fire loss on a business office building owned five years.

B) Gain from insurance recovery on vandalism to a business truck owned two years.

C) Loss on condemnation of business land held for 13 months.

D) fteft of uninsured jewelry owned for 11 months.

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

68

If the fair market value of Section 1245 property is greater than its basis, which of the following events would give rise to Section 1245 recapture as ordinary income?

A) Disposition at death

B) Disposition by gift

C) Like-kind exchange where boot is received

D) All of the above

E) None of the above

A) Disposition at death

B) Disposition by gift

C) Like-kind exchange where boot is received

D) All of the above

E) None of the above

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

69

Ed Evans, who files a single return, sold qualifying small business stock for $30,000 in 2012. He paid $140,000 for the stock in 2004. What is the maximum amount of ordinary loss Ed may deduct on his 2012 return?

A) $0

B) $50,000

C) $100,000

D) $110,000

A) $0

B) $50,000

C) $100,000

D) $110,000

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

70

Which of the following is not Section 1245 property?

A) Intangible personal property

B) Machinery used in a business

C) An office building depreciated using the regular MACRS method

D) An amortized certified pollution control facility

A) Intangible personal property

B) Machinery used in a business

C) An office building depreciated using the regular MACRS method

D) An amortized certified pollution control facility

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

71

Jennifer Judd gives her son, Jim, Section 1245 property. fte property has an adjusted basis of $11,000 to Jennifer, who has taken $2,000 in depreciation expense. Jim uses the property for three years, takes depreciation of $3,000 and then sells it for $14,000. What amount of gain must Jennifer recognize and what amount of gain must Jim recognize?

A) $2,000 Section 1231 gain; $3,000 Section 1231 gain

B) $0; $5,000 ordinary income and $1,000 Section 1231 gain

C) $2,000 ordinary income; $6,000 Section 1231 gain

D) $0; $3,000 ordinary income and $3,000 Section 1231 gain

A) $2,000 Section 1231 gain; $3,000 Section 1231 gain

B) $0; $5,000 ordinary income and $1,000 Section 1231 gain

C) $2,000 ordinary income; $6,000 Section 1231 gain

D) $0; $3,000 ordinary income and $3,000 Section 1231 gain

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

72

Which of the following qualify for capital gain treatment?

A) Inventors with patents

B) Authors of books

C) Composers of music

D) Artists

A) Inventors with patents

B) Authors of books

C) Composers of music

D) Artists

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

73

Ralph Rodgers, a calendar year taxpayer, purchased stock on June 18, 2011, for $8,000. fte stock became worthless on June 4, 2012. What is Ralph's loss in 2012?

A) $8,000 short-term capital loss

B) $8,000 long-term capital loss

C) No loss

D) $8,000 itemized deduction

A) $8,000 short-term capital loss

B) $8,000 long-term capital loss

C) No loss

D) $8,000 itemized deduction

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

74

Karen Kirbey grants Pamela Prentiss a franchise to sell handcrafted gifts. Pamela pays Karen 15 percent of all revenue. Sales for 2012 were $550,000. How will Karen treat the payment she receives on her 2012 return?

A) $82,500 short-term capital gain

B) $82,500 long-term capital gain

C) $82,500 ordinary income

D) No gain or income

A) $82,500 short-term capital gain

B) $82,500 long-term capital gain

C) $82,500 ordinary income

D) No gain or income

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

75

On January 5, 2012, Ernest Earner sells his patent (basis of $0) for a machine to a company which will manufacture the machine. He receives $150,000 plus $15 for each machine manufactured. In 2012, 10,000 machines were manufactured. What amount(s) must Ernest report on his 2012 tax return?

A) $150,000 long-term capital gain; $150,000 ordinary income

B) $150,000 short-term capital gain; $150,000 ordinary income

C) $300,000 short-term capital gain

D) $300,000 long-term capital gain

A) $150,000 long-term capital gain; $150,000 ordinary income

B) $150,000 short-term capital gain; $150,000 ordinary income

C) $300,000 short-term capital gain

D) $300,000 long-term capital gain

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

76

Valerie Villane incurred the following gains and losses during 2012: Loss resulting from theft of a diamond ring held two years ($1,000) Loss on the sale of a typewriter used in her business for five years ($250)

Gain on the sale of an adding machine used in her business for

Two years (in addition to recapture)

What is Valerie's net Section 1231 gain or loss for 2012?

$500

A) $750 loss

B) $1,250 loss

C) $0

D) $250 gain

Gain on the sale of an adding machine used in her business for

Two years (in addition to recapture)

What is Valerie's net Section 1231 gain or loss for 2012?

$500

A) $750 loss

B) $1,250 loss

C) $0

D) $250 gain

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

77

On January 4, 1980, Rita Racksaw purchased a warehouse for $200,000 with an estimated life of 40 years to be used in her business. On January 5, 2012, she sold the warehouse for $150,000. She used an accelerated depreciation method resulting in $170,000 depreciation. Straight-line depreciation would have been $160,000. How much and what type of gain will Rita have on the sale?

A) $10,000 ordinary income; $110,000 taxed at 25 percent

B) $10,000 Section 1231 gain; $110,000 ordinary income

C) $120,000 long-term capital gain

D) $120,000 ordinary income

A) $10,000 ordinary income; $110,000 taxed at 25 percent

B) $10,000 Section 1231 gain; $110,000 ordinary income

C) $120,000 long-term capital gain

D) $120,000 ordinary income

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

78

All of the following assets are Section 1245 property except:

A) Intangible personal property

B) Tangible personal property

C) Oil and gas storage tanks

D) Warehouse holding sorted and boxed oranges

A) Intangible personal property

B) Tangible personal property

C) Oil and gas storage tanks

D) Warehouse holding sorted and boxed oranges

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

79

Susan Songbird sold a word processor used in her business for $550. She had purchased the word processor three years ago for $950 and has taken $300 in depreciation. How much and what type of gain or loss will Susan have on the sale?

A) $300 ordinary income

B) $100 Section 1231 loss

C) $300 Section 1231 gain

D) $100 ordinary loss

A) $300 ordinary income

B) $100 Section 1231 loss

C) $300 Section 1231 gain

D) $100 ordinary loss

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

80

For 2012, Joyce Jacobson's books and records reflected the following: What is the amount of Joyce's capital loss carryover to 2013?

A) $2,400 short-term; $0 long-term

B) $1,300 short-term; $1,100 long-term

C) $1,900 short-term; $3,500 long-term

D) $4,300 short-term; $1,100 long-term

What is the amount of Joyce's capital loss carryover to 2013?A) $2,400 short-term; $0 long-term

B) $1,300 short-term; $1,100 long-term

C) $1,900 short-term; $3,500 long-term

D) $4,300 short-term; $1,100 long-term

Unlock Deck

Unlock for access to all 111 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 111 flashcards in this deck.