Deck 13: Overhead and Marketing Variances

Full screen (f)

Question

Betterton Corporation

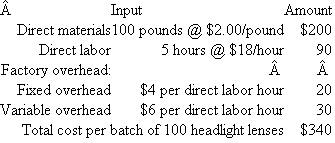

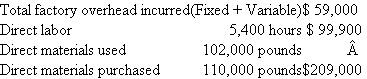

Betterton Corporation manufactures automobile headlight lenses and uses a standard cost system. At the beginning of the year, the following standards were established per 100 lenses (a single batch). Expected volume per month is 5,000 direct labor hours for January, and 105,000 headlight lenses were produced. There were no beginning inventories. The following costs were incurred in January:

Expected volume per month is 5,000 direct labor hours for January, and 105,000 headlight lenses were produced. There were no beginning inventories. The following costs were incurred in January:  Required:

Required:

a. Calculate the following variances:

(1) Overhead spending variance.

(2) Volume variance.

(3) Over/underabsorbed overhead.

(4) Direct materials price variance at purchase.

(5) Direct labor efficiency variance.

(6) Direct materials quantity variance.

b. Discuss how the direct materials price variance computed at purchase differs from the direct materials price variance computed at use. What are the advantages and disadvantages of each?

Betterton Corporation manufactures automobile headlight lenses and uses a standard cost system. At the beginning of the year, the following standards were established per 100 lenses (a single batch).

Expected volume per month is 5,000 direct labor hours for January, and 105,000 headlight lenses were produced. There were no beginning inventories. The following costs were incurred in January: Required: a. Calculate the following variances:

(1) Overhead spending variance.

(2) Volume variance.

(3) Over/underabsorbed overhead.

(4) Direct materials price variance at purchase.

(5) Direct labor efficiency variance.

(6) Direct materials quantity variance.

b. Discuss how the direct materials price variance computed at purchase differs from the direct materials price variance computed at use. What are the advantages and disadvantages of each?

Question

Question

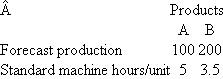

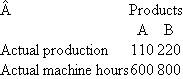

UOP

UOP is a manufacturing firm that has depreciation as its only overhead expense (i.e., there are no indirect labor, indirect materials, property taxes, factory insurance, etc.). UOP uses a flexible budget at the beginning of the year to forecast overhead in calculating the overhead rate. Overhead is assigned to products based on machine hours.

UOP uses units-of-production depreciation to calculate depreciation. A single machine manufactures all products. Its original cost is $600,000 and it has an estimated useful life of 10,000 machine hours.

UOP manufactures two products: A and B. Units-of-production depreciation is based on standard machine hours used. UOP assigns overhead to products based on standard machine hours, not actual machine hours.

The following budgeted data were produced at the beginning of the year: Actual operating data for the year are as follows:

Actual operating data for the year are as follows:  Required:

Required:

a. Calculate the overhead rate per machine hour and the amount of budgeted overhead for the year.

b. Calculate the total overhead absorbed to products during the year.

c. Calculate the over/underabsorbed overhead for the year.

d. Suppose UOP still assigns overhead to products based on standard machine hours, but now calculates units-of-production depreciation using actual machine hours. How much is the over/underabsorbed overhead?

e. Explain any difference between your answers to parts ( c ) and ( d ) above. What causes the difference? Why might UOP prefer the accounting treatment described in part ( d ) over that in part ( c ) ?

UOP is a manufacturing firm that has depreciation as its only overhead expense (i.e., there are no indirect labor, indirect materials, property taxes, factory insurance, etc.). UOP uses a flexible budget at the beginning of the year to forecast overhead in calculating the overhead rate. Overhead is assigned to products based on machine hours.

UOP uses units-of-production depreciation to calculate depreciation. A single machine manufactures all products. Its original cost is $600,000 and it has an estimated useful life of 10,000 machine hours.

UOP manufactures two products: A and B. Units-of-production depreciation is based on standard machine hours used. UOP assigns overhead to products based on standard machine hours, not actual machine hours.

The following budgeted data were produced at the beginning of the year:

Actual operating data for the year are as follows: Required: a. Calculate the overhead rate per machine hour and the amount of budgeted overhead for the year.

b. Calculate the total overhead absorbed to products during the year.

c. Calculate the over/underabsorbed overhead for the year.

d. Suppose UOP still assigns overhead to products based on standard machine hours, but now calculates units-of-production depreciation using actual machine hours. How much is the over/underabsorbed overhead?

e. Explain any difference between your answers to parts ( c ) and ( d ) above. What causes the difference? Why might UOP prefer the accounting treatment described in part ( d ) over that in part ( c ) ?

Question

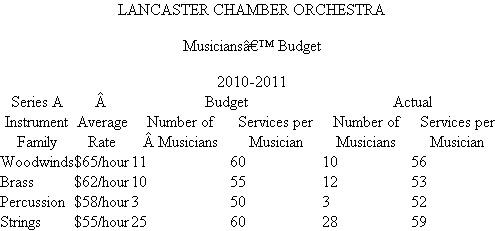

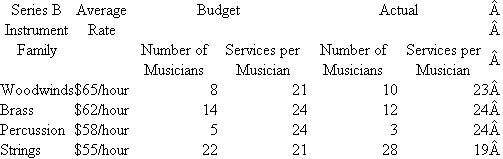

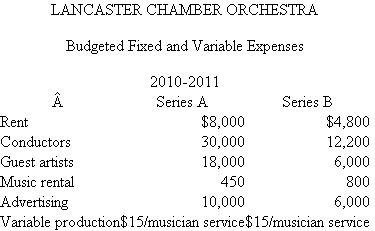

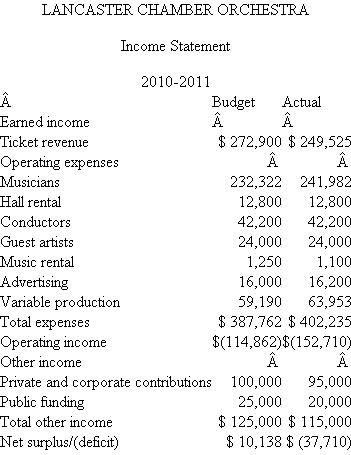

Lancaster Chamber Orchestra

The Lancaster Chamber Orchestra is a small community orchestra that offers two distinct concert series for its patrons. Series A is devoted entirely to the performance of a classical repertoire and offers 10 concerts throughout the year, while Series B consists of six pops concerts and serves to broaden the audience base of the ensemble.

Since programming needs change from concert to concert, musicians are hired on a per- service basis. (A service is either a rehearsal or a concert.) They are paid at differential average rates due to instrumental doubling requirements and also due to solo pay for woodwinds, percussion, and brass players. After the budget has been set, variances in musician costs are the result of changes in programming and rehearsal scheduling. Programming changes can cause different numbers of musicians to be needed for a particular series of rehearsals and concerts or can change the doubling requirements. Changes in rehearsal scheduling can alter needs for certain families of instruments at some rehearsals. For example, one Series A concert usually consists of six services, but not all instruments are required at each service. Programming and rehearsal scheduling are decided by the music director, Maestro Fritz Junger, but musician cost constraints are imposed by the director of production, Candice Wrightway. Budgeted and actual musician costs for the 2010-2011 season follow.

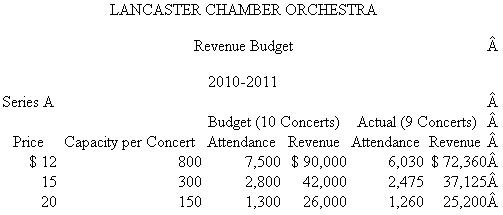

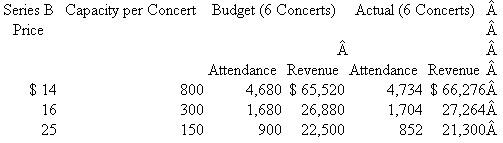

When the budget was prepared at the beginning of the year, Alan Voit, director of marketing, admitted that projected ticket sales for the two series were optimistic, but he believed that his innovative advertising campaign would help the orchestra meet its goal. Although pops sales came in almost exactly on target, a devastating ice storm caused the cancellation of one of the classical concerts. Unfortunately, rehearsals had already been held and the musicians had been paid for their services. Series sales figures for the three levels of ticket prices follow.

When the budget was prepared at the beginning of the year, Alan Voit, director of marketing, admitted that projected ticket sales for the two series were optimistic, but he believed that his innovative advertising campaign would help the orchestra meet its goal. Although pops sales came in almost exactly on target, a devastating ice storm caused the cancellation of one of the classical concerts. Unfortunately, rehearsals had already been held and the musicians had been paid for their services. Series sales figures for the three levels of ticket prices follow.

As with any orchestra, ticket sales alone are never enough to totally cover expenses, so the director of development, Lydia Givme, is responsible for the coordination of fundraising in the community. Unfortunately, the goals set at the beginning of the year did not anticipate an extended recession, with potential private, corporate, and government contributors tightening their fiscal belts.

As with any orchestra, ticket sales alone are never enough to totally cover expenses, so the director of development, Lydia Givme, is responsible for the coordination of fundraising in the community. Unfortunately, the goals set at the beginning of the year did not anticipate an extended recession, with potential private, corporate, and government contributors tightening their fiscal belts.

Additional expenses include a long-term rental agreement for the hall, a permanent conductor, guest artists, music rental and advertising costs, and variable production costs based on total services. Music rental and advertising are treated as fixed expenses even though their cost may vary during the course of the season. Here are budgeted fixed and variable expenses for 2010-2011. The income statement for 2010-2011 follows.

The income statement for 2010-2011 follows.  Required:

Required:

a. Calculate a flexible budget for the Lancaster Chamber Orchestra's 2010-2011 season.

b. After calculating the flexible budget, Randall Nobucs, director of finance, found a total unfavorable variance in net income of $53,158. Account for this unfavorable variance by calculating

(1) Revenue variances.

(2) Labor efficiency variances.

(3) Overhead efficiency and overhead spending variances.

c. Nobucs is concerned that if the orchestra faces similar problems in the next season, the accumulated deficit will cause bankruptcy. He argues with Alan Voit that a 15 percent increase in ticket prices would ensure a balanced budget for the 2010-2011 season. Discuss the feasibility of this strategy.

d. In examining the income statement, CEO Peter Morris is puzzled. He believes that all of his senior staff members are superb and is not sure where to lay the blame for the orchestra's dismal financial performance. Discuss the areas of specialized knowledge involved in the operation. Which person should be held accountable for each variance?

SOURCE: M Ames, J Dallas, R Krebs, W Perdue, and J Ricker.

The Lancaster Chamber Orchestra is a small community orchestra that offers two distinct concert series for its patrons. Series A is devoted entirely to the performance of a classical repertoire and offers 10 concerts throughout the year, while Series B consists of six pops concerts and serves to broaden the audience base of the ensemble.

Since programming needs change from concert to concert, musicians are hired on a per- service basis. (A service is either a rehearsal or a concert.) They are paid at differential average rates due to instrumental doubling requirements and also due to solo pay for woodwinds, percussion, and brass players. After the budget has been set, variances in musician costs are the result of changes in programming and rehearsal scheduling. Programming changes can cause different numbers of musicians to be needed for a particular series of rehearsals and concerts or can change the doubling requirements. Changes in rehearsal scheduling can alter needs for certain families of instruments at some rehearsals. For example, one Series A concert usually consists of six services, but not all instruments are required at each service. Programming and rehearsal scheduling are decided by the music director, Maestro Fritz Junger, but musician cost constraints are imposed by the director of production, Candice Wrightway. Budgeted and actual musician costs for the 2010-2011 season follow.

When the budget was prepared at the beginning of the year, Alan Voit, director of marketing, admitted that projected ticket sales for the two series were optimistic, but he believed that his innovative advertising campaign would help the orchestra meet its goal. Although pops sales came in almost exactly on target, a devastating ice storm caused the cancellation of one of the classical concerts. Unfortunately, rehearsals had already been held and the musicians had been paid for their services. Series sales figures for the three levels of ticket prices follow. As with any orchestra, ticket sales alone are never enough to totally cover expenses, so the director of development, Lydia Givme, is responsible for the coordination of fundraising in the community. Unfortunately, the goals set at the beginning of the year did not anticipate an extended recession, with potential private, corporate, and government contributors tightening their fiscal belts.Additional expenses include a long-term rental agreement for the hall, a permanent conductor, guest artists, music rental and advertising costs, and variable production costs based on total services. Music rental and advertising are treated as fixed expenses even though their cost may vary during the course of the season. Here are budgeted fixed and variable expenses for 2010-2011.

The income statement for 2010-2011 follows. Required: a. Calculate a flexible budget for the Lancaster Chamber Orchestra's 2010-2011 season.

b. After calculating the flexible budget, Randall Nobucs, director of finance, found a total unfavorable variance in net income of $53,158. Account for this unfavorable variance by calculating

(1) Revenue variances.

(2) Labor efficiency variances.

(3) Overhead efficiency and overhead spending variances.

c. Nobucs is concerned that if the orchestra faces similar problems in the next season, the accumulated deficit will cause bankruptcy. He argues with Alan Voit that a 15 percent increase in ticket prices would ensure a balanced budget for the 2010-2011 season. Discuss the feasibility of this strategy.

d. In examining the income statement, CEO Peter Morris is puzzled. He believes that all of his senior staff members are superb and is not sure where to lay the blame for the orchestra's dismal financial performance. Discuss the areas of specialized knowledge involved in the operation. Which person should be held accountable for each variance?

SOURCE: M Ames, J Dallas, R Krebs, W Perdue, and J Ricker.

Question

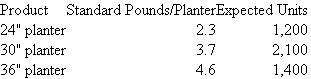

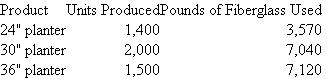

Artco Planters

Artco manufactures fiberglass home and office planters in a variety of decorator colors. These planters, in three sizes, are used to hold indoor plants. Overhead is allocated based on the standard pounds of fiberglass per planter. Here are standards for the three planters: Artco uses a flexible budget to calculate overhead rates at the beginning of the year. Fixed overhead for the year is budgeted at $593,950, and variable overhead is budgeted at $2.10 per pound of fiberglass. Actual overhead incurred is $633,805. The accompanying table summarizes the actual results for the year.

Artco uses a flexible budget to calculate overhead rates at the beginning of the year. Fixed overhead for the year is budgeted at $593,950, and variable overhead is budgeted at $2.10 per pound of fiberglass. Actual overhead incurred is $633,805. The accompanying table summarizes the actual results for the year.  Required:

Required:

a. Calculate the total variance (over/underabsorbed) if standard pounds are used to assign overhead to products.

b. Calculate the total overhead variance (over/underabsorbed) if actual pounds are used to assign overhead to products.

c. Explain why the answers differ in parts ( a ) and ( b ).

Artco manufactures fiberglass home and office planters in a variety of decorator colors. These planters, in three sizes, are used to hold indoor plants. Overhead is allocated based on the standard pounds of fiberglass per planter. Here are standards for the three planters:

Artco uses a flexible budget to calculate overhead rates at the beginning of the year. Fixed overhead for the year is budgeted at $593,950, and variable overhead is budgeted at $2.10 per pound of fiberglass. Actual overhead incurred is $633,805. The accompanying table summarizes the actual results for the year. Required: a. Calculate the total variance (over/underabsorbed) if standard pounds are used to assign overhead to products.

b. Calculate the total overhead variance (over/underabsorbed) if actual pounds are used to assign overhead to products.

c. Explain why the answers differ in parts ( a ) and ( b ).

Question

Question

Shady Tree Manufacturing

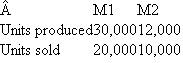

Shady Tree produces two products: M1 and M2. There are no beginning inventories or ending work- in-process inventories of either M1 or M2. A single plantwide overhead rate is used to allocate overhead to products using standard direct labor hours. This overhead rate is set at the beginning of the year based on the following flexible budget: Fixed factory overhead is forecast to be $3 million and variable overhead is projected to be $20 per direct labor hour. Management expects plant volume to be 200,000 standard direct labor hours. Here are the standard direct labor hours for each product: The efficiency and spending overhead variances for the year were zero. The following table summarizes operations for the year.

The efficiency and spending overhead variances for the year were zero. The following table summarizes operations for the year.  Required:

Required:

a. Calculate the plantwide overhead rate computed at the beginning of the year.

b. Calculate the volume variance for the year.

c. What is the dollar impact on accounting earnings if the volume variance is written off to cost of goods sold?

d. What is the dollar impact on accounting earnings of prorating the volume variance to inventories and cost of goods sold compared with writing it off to cost of sales?

Shady Tree produces two products: M1 and M2. There are no beginning inventories or ending work- in-process inventories of either M1 or M2. A single plantwide overhead rate is used to allocate overhead to products using standard direct labor hours. This overhead rate is set at the beginning of the year based on the following flexible budget: Fixed factory overhead is forecast to be $3 million and variable overhead is projected to be $20 per direct labor hour. Management expects plant volume to be 200,000 standard direct labor hours. Here are the standard direct labor hours for each product:

The efficiency and spending overhead variances for the year were zero. The following table summarizes operations for the year. Required: a. Calculate the plantwide overhead rate computed at the beginning of the year.

b. Calculate the volume variance for the year.

c. What is the dollar impact on accounting earnings if the volume variance is written off to cost of goods sold?

d. What is the dollar impact on accounting earnings of prorating the volume variance to inventories and cost of goods sold compared with writing it off to cost of sales?

Question

Spectra Inc.

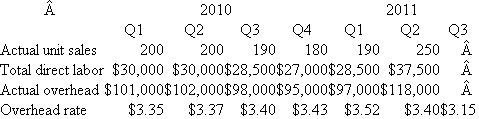

Spectra Inc. produces color monitors for personal computers. The firm makes 19-inch monitors with the following cost structure: Because of the rapidly changing market for computer monitors, standard costs, overhead rates, and prices are revised quarterly. While the direct labor component of standard cost has been relatively constant over time, direct materials costs, especially the cost of the circuit boards, fluctuate widely. Therefore, for pricing purposes, management reviews costs each quarter and forecasts next quarter's costs using the current quarter's cost structure. It also uses this method for revising overhead costs each quarter. Overhead is absorbed to products using direct labor cost. Fixed overhead is incurred fairly uniformly over the year. The overhead rate next quarter is the actual overhead costs incurred this quarter divided by this quarter's direct labor cost. Data for the last six quarters are shown.

Because of the rapidly changing market for computer monitors, standard costs, overhead rates, and prices are revised quarterly. While the direct labor component of standard cost has been relatively constant over time, direct materials costs, especially the cost of the circuit boards, fluctuate widely. Therefore, for pricing purposes, management reviews costs each quarter and forecasts next quarter's costs using the current quarter's cost structure. It also uses this method for revising overhead costs each quarter. Overhead is absorbed to products using direct labor cost. Fixed overhead is incurred fairly uniformly over the year. The overhead rate next quarter is the actual overhead costs incurred this quarter divided by this quarter's direct labor cost. Data for the last six quarters are shown.  The president of the company, responding to the auditor's suggestion that Spectra set standard costs on an annual basis, replied, "Annual budgeting is fine for more static companies like automobiles. But the computer industry, especially peripherals, changes day by day. We have to be ahead of our competitors in terms of changing our product price in response to cost changes. If we waited eight months to react to cost changes, we'd be out of business."

The president of the company, responding to the auditor's suggestion that Spectra set standard costs on an annual basis, replied, "Annual budgeting is fine for more static companies like automobiles. But the computer industry, especially peripherals, changes day by day. We have to be ahead of our competitors in terms of changing our product price in response to cost changes. If we waited eight months to react to cost changes, we'd be out of business."

Required:

Do you agree with the president or the auditor? Critically evaluate Spectra's costing system. What changes would you suggest, and how would you justify them to the president?

Spectra Inc. produces color monitors for personal computers. The firm makes 19-inch monitors with the following cost structure:

Because of the rapidly changing market for computer monitors, standard costs, overhead rates, and prices are revised quarterly. While the direct labor component of standard cost has been relatively constant over time, direct materials costs, especially the cost of the circuit boards, fluctuate widely. Therefore, for pricing purposes, management reviews costs each quarter and forecasts next quarter's costs using the current quarter's cost structure. It also uses this method for revising overhead costs each quarter. Overhead is absorbed to products using direct labor cost. Fixed overhead is incurred fairly uniformly over the year. The overhead rate next quarter is the actual overhead costs incurred this quarter divided by this quarter's direct labor cost. Data for the last six quarters are shown. The president of the company, responding to the auditor's suggestion that Spectra set standard costs on an annual basis, replied, "Annual budgeting is fine for more static companies like automobiles. But the computer industry, especially peripherals, changes day by day. We have to be ahead of our competitors in terms of changing our product price in response to cost changes. If we waited eight months to react to cost changes, we'd be out of business."Required:

Do you agree with the president or the auditor? Critically evaluate Spectra's costing system. What changes would you suggest, and how would you justify them to the president?

Question

Ultrasonic

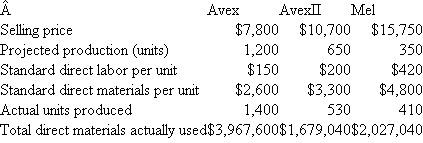

Ultrasonic manufactures three ultrasound imaging systems: Avex, AvexII, and Mel. Overhead is allocated to each system based on standard direct material dollars in each system. The firm uses a flexible overhead budget to calculate the overhead rate for the coming year, where budgeted volume is based on expected (projected) direct material dollars. The following table summarizes operations for the year: Fixed manufacturing overhead was budgeted at $7.5 million and variable overhead was budgeted at $0.30 per direct material dollar. In other words, each dollar spent on direct materials is expected to generate $0.30 of variable manufacturing overhead. Actual overhead incurred during the year was $10.280 million.

Fixed manufacturing overhead was budgeted at $7.5 million and variable overhead was budgeted at $0.30 per direct material dollar. In other words, each dollar spent on direct materials is expected to generate $0.30 of variable manufacturing overhead. Actual overhead incurred during the year was $10.280 million.

Required:

a. Calculate the budgeted overhead rate Ultrasonic will use to absorb overhead to products. Round the overhead rate to two significant digits.

b. Calculate the total amount of over-or underabsorbed overhead Ultrasonic reports for the year.

c. Compute the overhead spending variance, the overhead volume variance, and the overhead efficiency variance.

Ultrasonic manufactures three ultrasound imaging systems: Avex, AvexII, and Mel. Overhead is allocated to each system based on standard direct material dollars in each system. The firm uses a flexible overhead budget to calculate the overhead rate for the coming year, where budgeted volume is based on expected (projected) direct material dollars. The following table summarizes operations for the year:

Fixed manufacturing overhead was budgeted at $7.5 million and variable overhead was budgeted at $0.30 per direct material dollar. In other words, each dollar spent on direct materials is expected to generate $0.30 of variable manufacturing overhead. Actual overhead incurred during the year was $10.280 million.Required:

a. Calculate the budgeted overhead rate Ultrasonic will use to absorb overhead to products. Round the overhead rate to two significant digits.

b. Calculate the total amount of over-or underabsorbed overhead Ultrasonic reports for the year.

c. Compute the overhead spending variance, the overhead volume variance, and the overhead efficiency variance.

Question

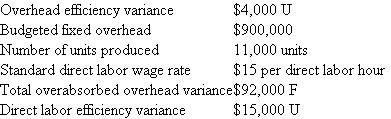

Logical Solutions

Logical Solutions reports the following overhead variances for 2010: In addition, actual overhead incurred in 2010 was $1 million. Overhead is absorbed to products using standard direct labor hours. 2010 volume was budgeted to be 40,000 direct labor hours and fixed overhead was budgeted to be $600,000.

In addition, actual overhead incurred in 2010 was $1 million. Overhead is absorbed to products using standard direct labor hours. 2010 volume was budgeted to be 40,000 direct labor hours and fixed overhead was budgeted to be $600,000.

Required:

What were actual volume, standard volume, and budgeted variable overhead for 2010?

Logical Solutions reports the following overhead variances for 2010:

In addition, actual overhead incurred in 2010 was $1 million. Overhead is absorbed to products using standard direct labor hours. 2010 volume was budgeted to be 40,000 direct labor hours and fixed overhead was budgeted to be $600,000.Required:

What were actual volume, standard volume, and budgeted variable overhead for 2010?

Question

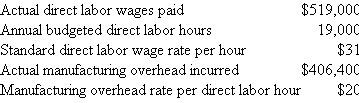

Megan Corp.

The following data are available for the Megan Corp. finishing department for the current year. The department makes a single product that requires three hours of labor per unit of finished product. Budgeted volume for the year was 30,000 direct labor hours. Required:

Required:

a. Calculate

(1) Actual overhead incurred.

(2) Overhead spending variance.

(3) Actual number of direct labor hours.

(4) Budgeted variable overhead rate per direct labor hour.

(5) Overhead rate per direct labor hour.

(6) Overhead volume variance.

(7) Actual direct labor wage rate.

b. Write a one-paragraph report summarizing the results of operations.

The following data are available for the Megan Corp. finishing department for the current year. The department makes a single product that requires three hours of labor per unit of finished product. Budgeted volume for the year was 30,000 direct labor hours.

Required: a. Calculate

(1) Actual overhead incurred.

(2) Overhead spending variance.

(3) Actual number of direct labor hours.

(4) Budgeted variable overhead rate per direct labor hour.

(5) Overhead rate per direct labor hour.

(6) Overhead volume variance.

(7) Actual direct labor wage rate.

b. Write a one-paragraph report summarizing the results of operations.

Question

Oneida Metal

Oneida Metal manufactures stainless steel boxes to house sophisticated communications integrated circuit boards for the defense industry. Oneida cuts the metal, bends it to form the chassis and top, punches holes, and drills and taps holes for screws. Oneida uses a standard cost system. Manufacturing overhead is assigned to jobs using standard direct labor hours. Before the year begins, Oneida uses a flexible manufacturing overhead budget and estimates the annual fixed manufacturing overhead and the budgeted variable overhead rate per direct labor hour. In the current year, Oneida started and completed four jobs. The following table summarizes the four jobs started and completed this year. There were no beginning or ending work-in-process inventories. Budgeted variable overhead was estimated to be $8 per direct labor hour. The following table summarizes the operating results and standards for the year:

There were no beginning or ending work-in-process inventories. Budgeted variable overhead was estimated to be $8 per direct labor hour. The following table summarizes the operating results and standards for the year:  Required:

Required:

Calculate the following:

a. Total direct labor efficiency variance (sum over the four jobs).

b. Total direct labor wage rate variance (aggregate over the four jobs).

c. Budgeted annual fixed manufacturing overhead.

d. Manufacturing overhead spending variance.

e. Manufacturing overhead efficiency variance.

f. Manufacturing overhead volume variance.

Oneida Metal manufactures stainless steel boxes to house sophisticated communications integrated circuit boards for the defense industry. Oneida cuts the metal, bends it to form the chassis and top, punches holes, and drills and taps holes for screws. Oneida uses a standard cost system. Manufacturing overhead is assigned to jobs using standard direct labor hours. Before the year begins, Oneida uses a flexible manufacturing overhead budget and estimates the annual fixed manufacturing overhead and the budgeted variable overhead rate per direct labor hour. In the current year, Oneida started and completed four jobs. The following table summarizes the four jobs started and completed this year.

There were no beginning or ending work-in-process inventories. Budgeted variable overhead was estimated to be $8 per direct labor hour. The following table summarizes the operating results and standards for the year: Required: Calculate the following:

a. Total direct labor efficiency variance (sum over the four jobs).

b. Total direct labor wage rate variance (aggregate over the four jobs).

c. Budgeted annual fixed manufacturing overhead.

d. Manufacturing overhead spending variance.

e. Manufacturing overhead efficiency variance.

f. Manufacturing overhead volume variance.

Question

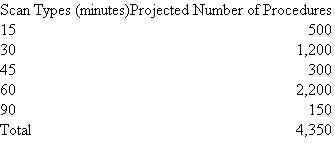

MRI Department

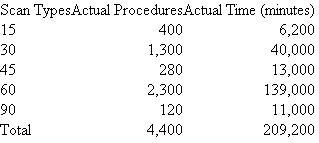

The MRI department at Community Hospital, a large urban health center, performs magnetic resonance imaging for heart disease, brain disorders, and total body scans for the various patient care units (neurology, cardiovascular, OB/GYN, oncology, and so forth). The fixed costs of the MRI department (MRI lease, space costs, personnel, overhead, and utilities) are budgeted to be $700,000 next year. The variable costs of the MRI department (supplies, fees, maintenance) are budgeted to be $300 per MRI hour. (An MRI hour is the total time needed to position the patient, set up the MRI for the scan, perform the scan, remove the patient, and prepare the MRI for the next patient.) The MRI is scheduled in 15-minute blocks. Some simple scans can be performed in 15 minutes, including the time to position the patient, set up the MRI, perform the scan, and prepare the machine for the next patient. Most scans take 30 minutes or 60 minutes. Each patient unit (neurology, cardiovascular, etc.) sending patients for an MRI is charged the expected, not the actual, time of the scan. If a patient requires a 30-minute scan but actually takes 35 minutes, the patient care unit is charged 30 minutes at the predetermined cost per minute. The predetermined cost per minute is calculated at the beginning of the year based on (1) the expected fixed costs, (2) the expected variable cost per minute, and (3) the expected number of minutes from the projected number of scans of various types.

The following table projects the number of various types of scans the MRI Department expects to perform next year. At the end of the year the MRI Department performed the following number of scans and the actual time spent on each scan:

At the end of the year the MRI Department performed the following number of scans and the actual time spent on each scan:  The total cost of operating the MRI Department (fixed and variable costs) was $1,750,000. Required:

The total cost of operating the MRI Department (fixed and variable costs) was $1,750,000. Required:

a. Calculate the predetermined cost per minute of MRI scan time.

b. Based on the predetermined cost per minute calculated in ( a ) , what are the total MRI charges to the patient care units?

c. Prepare a report that analyzes the financial performance of the MRI Department.

d. Write a short report that succinctly summarizes the key findings of your performance analysis in part ( c ).

The MRI department at Community Hospital, a large urban health center, performs magnetic resonance imaging for heart disease, brain disorders, and total body scans for the various patient care units (neurology, cardiovascular, OB/GYN, oncology, and so forth). The fixed costs of the MRI department (MRI lease, space costs, personnel, overhead, and utilities) are budgeted to be $700,000 next year. The variable costs of the MRI department (supplies, fees, maintenance) are budgeted to be $300 per MRI hour. (An MRI hour is the total time needed to position the patient, set up the MRI for the scan, perform the scan, remove the patient, and prepare the MRI for the next patient.) The MRI is scheduled in 15-minute blocks. Some simple scans can be performed in 15 minutes, including the time to position the patient, set up the MRI, perform the scan, and prepare the machine for the next patient. Most scans take 30 minutes or 60 minutes. Each patient unit (neurology, cardiovascular, etc.) sending patients for an MRI is charged the expected, not the actual, time of the scan. If a patient requires a 30-minute scan but actually takes 35 minutes, the patient care unit is charged 30 minutes at the predetermined cost per minute. The predetermined cost per minute is calculated at the beginning of the year based on (1) the expected fixed costs, (2) the expected variable cost per minute, and (3) the expected number of minutes from the projected number of scans of various types.

The following table projects the number of various types of scans the MRI Department expects to perform next year.

At the end of the year the MRI Department performed the following number of scans and the actual time spent on each scan: The total cost of operating the MRI Department (fixed and variable costs) was $1,750,000. Required: a. Calculate the predetermined cost per minute of MRI scan time.

b. Based on the predetermined cost per minute calculated in ( a ) , what are the total MRI charges to the patient care units?

c. Prepare a report that analyzes the financial performance of the MRI Department.

d. Write a short report that succinctly summarizes the key findings of your performance analysis in part ( c ).

Question

Question

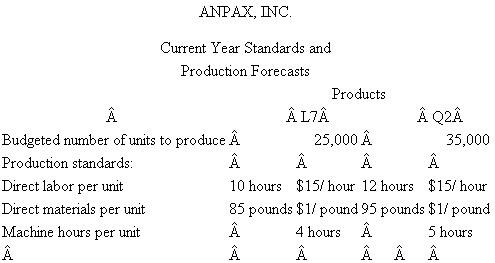

Anpax, Inc.

Anpax, Inc., manufactures two products: L7 and Q2. Overhead is allocated to products based on machine hours. Management uses a flexible budget to forecast overhead. For the current year, fixed factory overhead is projected to be $2.75 million and variable factory overhead is budgeted at $20 per machine hour. At the beginning of the year, management developed the following standards for each product and made the following production forecasts for the year: There were no beginning or ending inventories. Actual production for the year was 20,000 units of L7 and 40,000 units of Q2. Other data summarizing actual operations for the year are:

There were no beginning or ending inventories. Actual production for the year was 20,000 units of L7 and 40,000 units of Q2. Other data summarizing actual operations for the year are:  Required:

Required:

a. Calculate the overhead rate for the current year.

b. Calculate materials and labor variances. Report quantity (efficiency) variances and price variances.

c. Calculate the volume, spending, and efficiency overhead variances.

d. Your boss (a nonaccountant) asks you to explain in nontechnical terms the meaning of each overhead variance.

Anpax, Inc., manufactures two products: L7 and Q2. Overhead is allocated to products based on machine hours. Management uses a flexible budget to forecast overhead. For the current year, fixed factory overhead is projected to be $2.75 million and variable factory overhead is budgeted at $20 per machine hour. At the beginning of the year, management developed the following standards for each product and made the following production forecasts for the year:

There were no beginning or ending inventories. Actual production for the year was 20,000 units of L7 and 40,000 units of Q2. Other data summarizing actual operations for the year are: Required: a. Calculate the overhead rate for the current year.

b. Calculate materials and labor variances. Report quantity (efficiency) variances and price variances.

c. Calculate the volume, spending, and efficiency overhead variances.

d. Your boss (a nonaccountant) asks you to explain in nontechnical terms the meaning of each overhead variance.

Question

Question

Mopart Division

The Mopart Division produces a single product. Its standard cost system uses a flexible budget to assign indirect costs on the basis of standard direct labor hours. At the budgeted volume of 4,000 direct labor hours, the standard cost per unit is as follows: For the month of March, the following actual data were reported:

For the month of March, the following actual data were reported:  There was no beginning inventory.

There was no beginning inventory.

Required:

a. Analyze the results of operations for March. Support your analysis.

b. Present two income statements in good format using absorption costing and variable costing net income.

c. Reconcile any difference in net income between the two statements.

d. What is the opportunity cost of the unused normal capacity?

The Mopart Division produces a single product. Its standard cost system uses a flexible budget to assign indirect costs on the basis of standard direct labor hours. At the budgeted volume of 4,000 direct labor hours, the standard cost per unit is as follows:

For the month of March, the following actual data were reported: There was no beginning inventory.Required:

a. Analyze the results of operations for March. Support your analysis.

b. Present two income statements in good format using absorption costing and variable costing net income.

c. Reconcile any difference in net income between the two statements.

d. What is the opportunity cost of the unused normal capacity?

Question

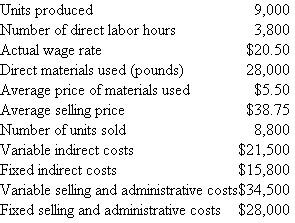

Galt Electric Motors

Galt Electric Motors (GEM) produces two types of motors, small and large. Standard machine time to make one small motor is 20 minutes; standard machine time to make one large motor is 30 minutes. GEM plans to make 30,000 small motors and 20,000 large motors during the year. Budgeted manufacturing overhead (fixed and variable) for GEM is $1,800,000. During the year, Galt used 21,600 machine hours to make 27,000 small motors and 24,000 large motors. Actual overhead incurred during the year was $1,900,000.

a. What is GEM's standard overhead rate per machine hour? How much overhead is reflected in the standard cost of each type of motor?

b. Use your answers in part ( a ) to verify that GEM's total overhead variance during the year was $10,000. Is this variance favorable or unfavorable?

c. The table below decomposes the $10,000 overhead variance into spending, efficiency, and volume variances assuming that (1) all overhead is variable and (2) all overhead is fixed. Verify the variances and determine which variances are favorable and which are unfavorable. d. Explain the economic intuition behind these variances. In particular, explain why even though in each case the expenditures, inputs, and outputs are the same, (1) the spending variances are different, (2) there is no efficiency variance in the "fixed overhead" case, and (3) there is no volume variance in the "variable overhead" case.

d. Explain the economic intuition behind these variances. In particular, explain why even though in each case the expenditures, inputs, and outputs are the same, (1) the spending variances are different, (2) there is no efficiency variance in the "fixed overhead" case, and (3) there is no volume variance in the "variable overhead" case.

SOURCE: R Sansing.

Galt Electric Motors (GEM) produces two types of motors, small and large. Standard machine time to make one small motor is 20 minutes; standard machine time to make one large motor is 30 minutes. GEM plans to make 30,000 small motors and 20,000 large motors during the year. Budgeted manufacturing overhead (fixed and variable) for GEM is $1,800,000. During the year, Galt used 21,600 machine hours to make 27,000 small motors and 24,000 large motors. Actual overhead incurred during the year was $1,900,000.

a. What is GEM's standard overhead rate per machine hour? How much overhead is reflected in the standard cost of each type of motor?

b. Use your answers in part ( a ) to verify that GEM's total overhead variance during the year was $10,000. Is this variance favorable or unfavorable?

c. The table below decomposes the $10,000 overhead variance into spending, efficiency, and volume variances assuming that (1) all overhead is variable and (2) all overhead is fixed. Verify the variances and determine which variances are favorable and which are unfavorable.

d. Explain the economic intuition behind these variances. In particular, explain why even though in each case the expenditures, inputs, and outputs are the same, (1) the spending variances are different, (2) there is no efficiency variance in the "fixed overhead" case, and (3) there is no volume variance in the "variable overhead" case.SOURCE: R Sansing.

Question

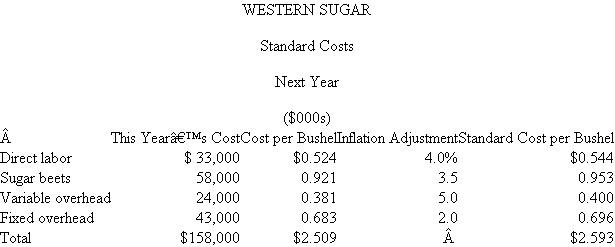

Western Sugar

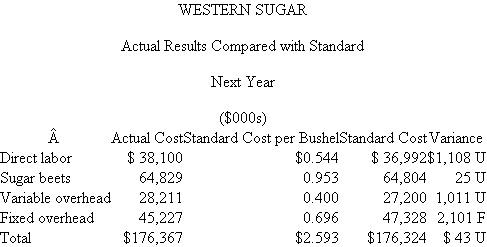

Western Sugar processes sugar beets into granulated sugar that is sold to food companies. It uses a standard cost system to aid in cost control and performance evaluation. To compute the standards for next year, the actual expense incurred by expense category is divided by the bushels of sugar beets processed to arrive at a standard cost per bushel. These per-bushel standards are then increased by the expected amount of inflation forecast for that expense category. This year, Western Sugar processed 63 million bushels of beets. The accompanying table calculates next year's standard costs. Next year, actual production is 68 million bushels. At the end of next year, the following report is prepared:

Next year, actual production is 68 million bushels. At the end of next year, the following report is prepared:  Senior management was not surprised at the small variances for labor and sugar beets. The processing plant has very good operating controls and there had been no surprises in the sugar beet market or in the labor market. Initial forecasts proved to be good. Management was delighted to see the favorable total overhead variance ($1,090F = $1,011U + $2,101F). Although variable overhead was over budget, fixed overhead more than offset it. There was no major change in the plant's production technology to explain this shift (such as increased automation), so senior management was prepared to attribute the favorable total overhead variance to better internal control by the plant manager.

Senior management was not surprised at the small variances for labor and sugar beets. The processing plant has very good operating controls and there had been no surprises in the sugar beet market or in the labor market. Initial forecasts proved to be good. Management was delighted to see the favorable total overhead variance ($1,090F = $1,011U + $2,101F). Although variable overhead was over budget, fixed overhead more than offset it. There was no major change in the plant's production technology to explain this shift (such as increased automation), so senior management was prepared to attribute the favorable total overhead variance to better internal control by the plant manager.

Required:

a. What do you think is the reason for the overhead variances?

b. Is it appropriate to base next year's standards on last year's costs?

Western Sugar processes sugar beets into granulated sugar that is sold to food companies. It uses a standard cost system to aid in cost control and performance evaluation. To compute the standards for next year, the actual expense incurred by expense category is divided by the bushels of sugar beets processed to arrive at a standard cost per bushel. These per-bushel standards are then increased by the expected amount of inflation forecast for that expense category. This year, Western Sugar processed 63 million bushels of beets. The accompanying table calculates next year's standard costs.

Next year, actual production is 68 million bushels. At the end of next year, the following report is prepared: Senior management was not surprised at the small variances for labor and sugar beets. The processing plant has very good operating controls and there had been no surprises in the sugar beet market or in the labor market. Initial forecasts proved to be good. Management was delighted to see the favorable total overhead variance ($1,090F = $1,011U + $2,101F). Although variable overhead was over budget, fixed overhead more than offset it. There was no major change in the plant's production technology to explain this shift (such as increased automation), so senior management was prepared to attribute the favorable total overhead variance to better internal control by the plant manager.Required:

a. What do you think is the reason for the overhead variances?

b. Is it appropriate to base next year's standards on last year's costs?

Question

Soldering Department

The soldering department of Xtel Circuits solders integrated circuits onto circuit boards. The department is highly automated. The existing machinery is state of the art, having been installed only 15 months ago.

Overhead in the department is allocated based on machine hours. Normal volume is 2,000 machine hours per month. Fixed overhead averages $160,000 per month, and variable overhead is $110 per machine hour. Actual volume for the month of March (which just ended) was 2,400 machine hours, and standard volume was 2,200 machine hours.

The accompanying table summarizes the overhead efficiency and volume variances in the soldering department for the last 14 months since the new equipment was installed: Required:

Required:

a. Calculate the overhead rate in the soldering department.

b. Calculate the overhead efficiency and volume variances in the soldering department for March of this year.

c. Comment on any apparent patterns in the overhead variances in the soldering department. What might be causing the patterns?

The soldering department of Xtel Circuits solders integrated circuits onto circuit boards. The department is highly automated. The existing machinery is state of the art, having been installed only 15 months ago.

Overhead in the department is allocated based on machine hours. Normal volume is 2,000 machine hours per month. Fixed overhead averages $160,000 per month, and variable overhead is $110 per machine hour. Actual volume for the month of March (which just ended) was 2,400 machine hours, and standard volume was 2,200 machine hours.

The accompanying table summarizes the overhead efficiency and volume variances in the soldering department for the last 14 months since the new equipment was installed:

Required: a. Calculate the overhead rate in the soldering department.

b. Calculate the overhead efficiency and volume variances in the soldering department for March of this year.

c. Comment on any apparent patterns in the overhead variances in the soldering department. What might be causing the patterns?

Question

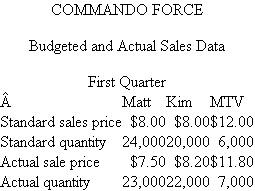

Commando Force

Commando Force is a new set of children's action toys consisting of three separately sold pieces: Matt, Kim, and the multi-terrain vehicle (MTV). The MTV can be used by itself or it can hold either Matt or Kim or both. With male and female action figures, Commando Force toys are targeted at both boys and girls aged 7 to 11. Commando Force is sold to wholesalers who sell to toy stores, chains, and discount stores.

The first calendar quarter (January-March) tends to be very slow because it follows the holidays. Here are budgeted and actual sales data for the first quarter. Required:

Required:

a. Calculate the price and quantity variances for each separately sold toy and all the toys.

b. Calculate the mix and sales variances for each separately sold toy and all the toys.

c. Write a short memo interpreting to management the variances in ( a ) and ( b ).

Commando Force is a new set of children's action toys consisting of three separately sold pieces: Matt, Kim, and the multi-terrain vehicle (MTV). The MTV can be used by itself or it can hold either Matt or Kim or both. With male and female action figures, Commando Force toys are targeted at both boys and girls aged 7 to 11. Commando Force is sold to wholesalers who sell to toy stores, chains, and discount stores.

The first calendar quarter (January-March) tends to be very slow because it follows the holidays. Here are budgeted and actual sales data for the first quarter.

Required: a. Calculate the price and quantity variances for each separately sold toy and all the toys.

b. Calculate the mix and sales variances for each separately sold toy and all the toys.

c. Write a short memo interpreting to management the variances in ( a ) and ( b ).

Question

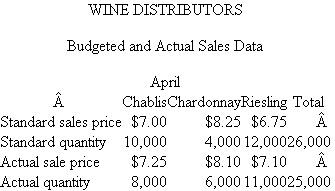

Wine Distributors

Wine Distributors is a wholesaler of wine, buying from wineries and selling to wine stores. Three different white wines are sold: Chablis, Chardonnay, and Riesling. Here are budgeted and actual sales data for the month of April. Required:

Required:

Write a short memo to management analyzing the operating performance for April.

Wine Distributors is a wholesaler of wine, buying from wineries and selling to wine stores. Three different white wines are sold: Chablis, Chardonnay, and Riesling. Here are budgeted and actual sales data for the month of April.

Required: Write a short memo to management analyzing the operating performance for April.

Question

Auden Manufacturing

Auden Manufacturing produces a single product with the following standards: FIFO inventory costing is used. Normal volume is used as budgeted volume. Actual production, sales, and costs for the year were as follows:

FIFO inventory costing is used. Normal volume is used as budgeted volume. Actual production, sales, and costs for the year were as follows:  Required:

Required:

a. Compute the overhead rate used to apply overhead to the product.

b. Calculate all variances.

c. Calculate net income under absorption costing. (All variances are taken to cost of goods sold.)

d. Calculate net income under variable costing. (All variances are taken to cost of goods sold.)

e. Reconcile the difference in income between variable costing and absorption costing.

Auden Manufacturing produces a single product with the following standards:

FIFO inventory costing is used. Normal volume is used as budgeted volume. Actual production, sales, and costs for the year were as follows: Required: a. Compute the overhead rate used to apply overhead to the product.

b. Calculate all variances.

c. Calculate net income under absorption costing. (All variances are taken to cost of goods sold.)

d. Calculate net income under variable costing. (All variances are taken to cost of goods sold.)

e. Reconcile the difference in income between variable costing and absorption costing.

Question

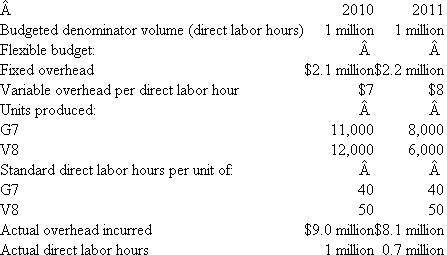

Turow Trailers

Turow Trailers assembles horse trailers. Two models are manufactured: G7 and V8. While laborintensive, the production process is not very complicated. The single plant produces all the trailers with 48 work teams of two or three workers. Sixteen supervisors oversee the work teams. Materials handlers deliver all the parts needed for each trailer to the work team. Human resources, accounting, inspection, purchasing, and tools are the other major overhead departments. Some operating statistics for 2010 and 2011 follow. Required:

Required:

a. Calculate all the overhead variances for both 2010 and 2011.

b. Discuss who in the plant should be held responsible for each overhead variance.

Turow Trailers assembles horse trailers. Two models are manufactured: G7 and V8. While laborintensive, the production process is not very complicated. The single plant produces all the trailers with 48 work teams of two or three workers. Sixteen supervisors oversee the work teams. Materials handlers deliver all the parts needed for each trailer to the work team. Human resources, accounting, inspection, purchasing, and tools are the other major overhead departments. Some operating statistics for 2010 and 2011 follow.

Required: a. Calculate all the overhead variances for both 2010 and 2011.

b. Discuss who in the plant should be held responsible for each overhead variance.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/24

Play

Full screen (f)

Deck 13: Overhead and Marketing Variances

1

Betterton Corporation

Betterton Corporation manufactures automobile headlight lenses and uses a standard cost system. At the beginning of the year, the following standards were established per 100 lenses (a single batch). Expected volume per month is 5,000 direct labor hours for January, and 105,000 headlight lenses were produced. There were no beginning inventories. The following costs were incurred in January: Required:

a. Calculate the following variances:

(1) Overhead spending variance.

(2) Volume variance.

(3) Over/underabsorbed overhead.

(4) Direct materials price variance at purchase.

(5) Direct labor efficiency variance.

(6) Direct materials quantity variance.

b. Discuss how the direct materials price variance computed at purchase differs from the direct materials price variance computed at use. What are the advantages and disadvantages of each?

Betterton Corporation manufactures automobile headlight lenses and uses a standard cost system. At the beginning of the year, the following standards were established per 100 lenses (a single batch).

Expected volume per month is 5,000 direct labor hours for January, and 105,000 headlight lenses were produced. There were no beginning inventories. The following costs were incurred in January: Required: a. Calculate the following variances:

(1) Overhead spending variance.

(2) Volume variance.

(3) Over/underabsorbed overhead.

(4) Direct materials price variance at purchase.

(5) Direct labor efficiency variance.

(6) Direct materials quantity variance.

b. Discuss how the direct materials price variance computed at purchase differs from the direct materials price variance computed at use. What are the advantages and disadvantages of each?

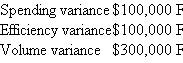

a.The following data are used in calculating the variances:

105,000 lens = 1,050 batches

Standard (earned) volume = 1,050 batches × 5 hours/batch

= 5,250 direct labor hours

Ws=$18/ hour

Wa=$99,900/5,400 = $18.50 / hour

Ha=5,400 direct labor hours

Hs=1,050 × 5 = 5,250 direct labor hours

Qa=102,000 lbs.

Qs=1,050 × 100 = 105,000 lbs.

Qb=110,000 lbs.

Ps=$2/lb

Pa=$209,000/110,000 = $1.90/lb

Fixed overhead = $4/hour × 5,000 hours = $20,000 month

Flexible overhead budget = $20,000 + $6/direct labor hour

Overhead rate = ($20,000 + $6 × 5,000hours)/5,000 hours = $10/ direct labor hour

Flexible budget @ standard volume = $20,000 + $6 × (1,050 × 5) = $51,500

Overhead absorbed = 1,050 × $10 × 5 hours = $52,500

(i)Overhead spending variance = Actual overhead - flexible budget @ actual volume = $59,000 - ($20,000 + $6 × 5,400 hours) = $6,600 U

(ii)Volume variance = flexible budget @ standard - overhead absorbed = ($20,000 + $6 × 5,250 hours) - $52,500 = 1,000 F

(iii)Over/underabsorbed overhead = overhead incurred - overhead absorbed

= $59,000 - $52,500 = $6,500 underabsorbed

(iv)Direct materials price variance at purchase = (Pa - Ps) × Qb = ($1.90 -$2.00) × 110,000 lbs = $11,000 F

(v)Direct labor efficiency variance = (Ha - Hs) × Ws = (5,400 - 5,250) × $18

= $2,700 U

(vi)Direct materials quantity variance = (Qa - Qs) × Ps = (102,000 - 105,000)

× $2 = $6,000 F

b.The price variance at purchase includes all the raw materials purchased, not just those used in production. Thus, it is a more timely and accurate measure of the purchasing department's performance this period. Raw material inventories are stated at standard cost and as they are used, work-in-process is charged at standard cost. Removing all the price variance at the time of purchase simplifies having to keep the raw materials at different actual costs.

105,000 lens = 1,050 batches

Standard (earned) volume = 1,050 batches × 5 hours/batch

= 5,250 direct labor hours

Ws=$18/ hour

Wa=$99,900/5,400 = $18.50 / hour

Ha=5,400 direct labor hours

Hs=1,050 × 5 = 5,250 direct labor hours

Qa=102,000 lbs.

Qs=1,050 × 100 = 105,000 lbs.

Qb=110,000 lbs.

Ps=$2/lb

Pa=$209,000/110,000 = $1.90/lb

Fixed overhead = $4/hour × 5,000 hours = $20,000 month

Flexible overhead budget = $20,000 + $6/direct labor hour

Overhead rate = ($20,000 + $6 × 5,000hours)/5,000 hours = $10/ direct labor hour

Flexible budget @ standard volume = $20,000 + $6 × (1,050 × 5) = $51,500

Overhead absorbed = 1,050 × $10 × 5 hours = $52,500

(i)Overhead spending variance = Actual overhead - flexible budget @ actual volume = $59,000 - ($20,000 + $6 × 5,400 hours) = $6,600 U

(ii)Volume variance = flexible budget @ standard - overhead absorbed = ($20,000 + $6 × 5,250 hours) - $52,500 = 1,000 F

(iii)Over/underabsorbed overhead = overhead incurred - overhead absorbed

= $59,000 - $52,500 = $6,500 underabsorbed

(iv)Direct materials price variance at purchase = (Pa - Ps) × Qb = ($1.90 -$2.00) × 110,000 lbs = $11,000 F

(v)Direct labor efficiency variance = (Ha - Hs) × Ws = (5,400 - 5,250) × $18

= $2,700 U

(vi)Direct materials quantity variance = (Qa - Qs) × Ps = (102,000 - 105,000)

× $2 = $6,000 F

b.The price variance at purchase includes all the raw materials purchased, not just those used in production. Thus, it is a more timely and accurate measure of the purchasing department's performance this period. Raw material inventories are stated at standard cost and as they are used, work-in-process is charged at standard cost. Removing all the price variance at the time of purchase simplifies having to keep the raw materials at different actual costs.

2

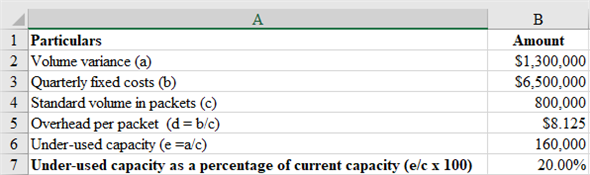

On-Call

You work in the Strategy Analysis department of On-Call, a worldwide paging firm offering satellitebased digital communications through sophisticated pagers. On-Call is analyzing the possibility of acquiring AtlantiCom, an East Coast paging firm in Maine.

AtlantiCom's latest quarterly report disclosed an unfavorable volume variance of $1.3 million. The engineering staff of On-Call, familiar with AtlantiCom's network, estimates that AtlantiCom has quarterly fixed overhead costs of $6.5 million that can deliver 800,000 message packets per quarter. A message packet is the industry standard of delivering a fixed amount of digital information within a given time period.

In valuing AtlantiCom, senior management at On-Call wants to know whether AtlantiCom has excess capacity, and, if so, how much.

Required:

As a percentage of AtlantiCom's current capacity of 800,000 message packets, estimate AtlantiCom's over-or undercapacity last quarter. Assume that the quarterly fixed overhead costs of $6.5 million approximate budgeted fixed overhead and that actual and standard volumes are the same.

You work in the Strategy Analysis department of On-Call, a worldwide paging firm offering satellitebased digital communications through sophisticated pagers. On-Call is analyzing the possibility of acquiring AtlantiCom, an East Coast paging firm in Maine.

AtlantiCom's latest quarterly report disclosed an unfavorable volume variance of $1.3 million. The engineering staff of On-Call, familiar with AtlantiCom's network, estimates that AtlantiCom has quarterly fixed overhead costs of $6.5 million that can deliver 800,000 message packets per quarter. A message packet is the industry standard of delivering a fixed amount of digital information within a given time period.

In valuing AtlantiCom, senior management at On-Call wants to know whether AtlantiCom has excess capacity, and, if so, how much.

Required:

As a percentage of AtlantiCom's current capacity of 800,000 message packets, estimate AtlantiCom's over-or undercapacity last quarter. Assume that the quarterly fixed overhead costs of $6.5 million approximate budgeted fixed overhead and that actual and standard volumes are the same.

Variance analysis

When a company establishes a standard costing system, it compares actual results with the standards set and computes variances that help the management of the company to control operations after identifying the causes of the variances.

Volume variance

This is the difference between budgeted and actual revenue due purely to a difference between the budgeted volume and the actual volume of production.

Estimate over (under) used capacity as follows: - Therefore, the company has an under-used capacity which is 20% of the standard capacity.

Therefore, the company has an under-used capacity which is 20% of the standard capacity.

Explanation:

Under-used units have been found out by dividing the volume variance by standard overhead rate per unit. The percentage of under-used capacity has been found out by dividing the under-used capacity by the standard volume as 20%.

When a company establishes a standard costing system, it compares actual results with the standards set and computes variances that help the management of the company to control operations after identifying the causes of the variances.

Volume variance

This is the difference between budgeted and actual revenue due purely to a difference between the budgeted volume and the actual volume of production.

Estimate over (under) used capacity as follows: -

Therefore, the company has an under-used capacity which is 20% of the standard capacity.Explanation:

Under-used units have been found out by dividing the volume variance by standard overhead rate per unit. The percentage of under-used capacity has been found out by dividing the under-used capacity by the standard volume as 20%.

3

UOP

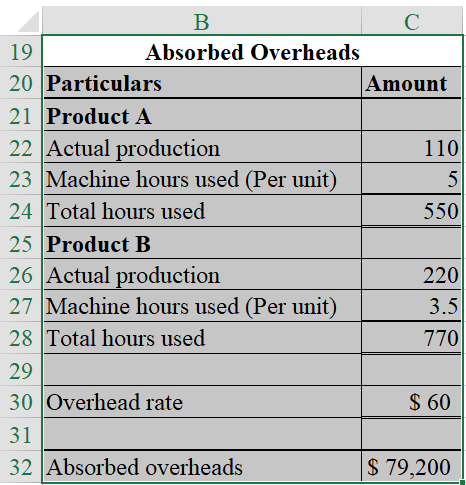

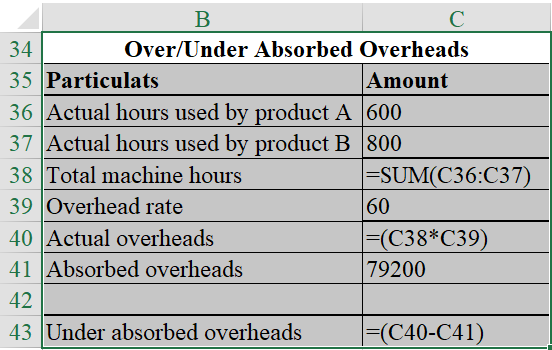

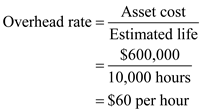

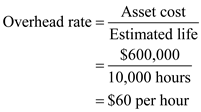

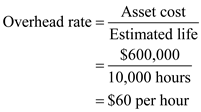

UOP is a manufacturing firm that has depreciation as its only overhead expense (i.e., there are no indirect labor, indirect materials, property taxes, factory insurance, etc.). UOP uses a flexible budget at the beginning of the year to forecast overhead in calculating the overhead rate. Overhead is assigned to products based on machine hours.

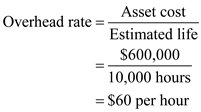

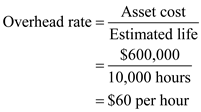

UOP uses units-of-production depreciation to calculate depreciation. A single machine manufactures all products. Its original cost is $600,000 and it has an estimated useful life of 10,000 machine hours.

UOP manufactures two products: A and B. Units-of-production depreciation is based on standard machine hours used. UOP assigns overhead to products based on standard machine hours, not actual machine hours.

The following budgeted data were produced at the beginning of the year: Actual operating data for the year are as follows: Required:

a. Calculate the overhead rate per machine hour and the amount of budgeted overhead for the year.

b. Calculate the total overhead absorbed to products during the year.

c. Calculate the over/underabsorbed overhead for the year.

d. Suppose UOP still assigns overhead to products based on standard machine hours, but now calculates units-of-production depreciation using actual machine hours. How much is the over/underabsorbed overhead?

e. Explain any difference between your answers to parts ( c ) and ( d ) above. What causes the difference? Why might UOP prefer the accounting treatment described in part ( d ) over that in part ( c ) ?

UOP is a manufacturing firm that has depreciation as its only overhead expense (i.e., there are no indirect labor, indirect materials, property taxes, factory insurance, etc.). UOP uses a flexible budget at the beginning of the year to forecast overhead in calculating the overhead rate. Overhead is assigned to products based on machine hours.

UOP uses units-of-production depreciation to calculate depreciation. A single machine manufactures all products. Its original cost is $600,000 and it has an estimated useful life of 10,000 machine hours.

UOP manufactures two products: A and B. Units-of-production depreciation is based on standard machine hours used. UOP assigns overhead to products based on standard machine hours, not actual machine hours.

The following budgeted data were produced at the beginning of the year:

Actual operating data for the year are as follows: Required: a. Calculate the overhead rate per machine hour and the amount of budgeted overhead for the year.

b. Calculate the total overhead absorbed to products during the year.

c. Calculate the over/underabsorbed overhead for the year.

d. Suppose UOP still assigns overhead to products based on standard machine hours, but now calculates units-of-production depreciation using actual machine hours. How much is the over/underabsorbed overhead?

e. Explain any difference between your answers to parts ( c ) and ( d ) above. What causes the difference? Why might UOP prefer the accounting treatment described in part ( d ) over that in part ( c ) ?

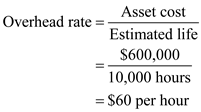

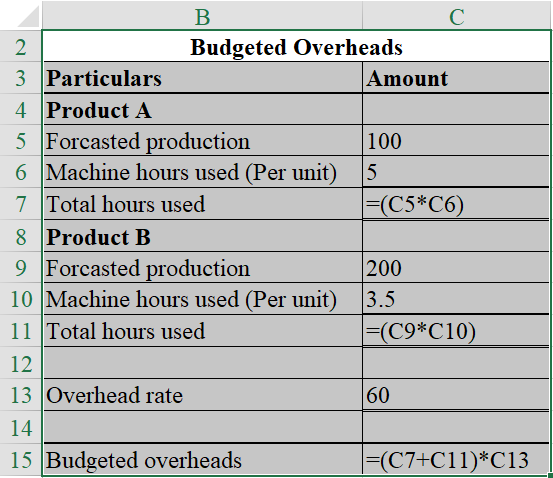

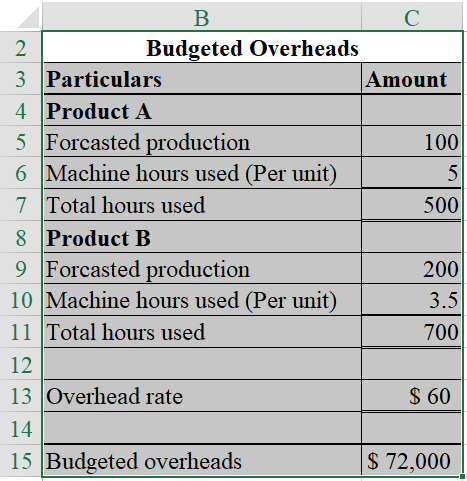

Overhead Cost:

It can be referred to as an accounting term which states all the indirect expenses incurred by an organization for operating a business. These expenses are not directly related to the manufacturing of a product or rendering of a service.

Over/Under Applied Overhead:

The overheads are absorbed based on some predetermined factor that may be machine hours or labor hours. These are called the budgeted overheads. These overheads and are then matched with the actual overheads. In case the actual overheads are more than the budgeted then that situation is called under-applied overhead and vice-versa.

a. Compute the overhead rate per machine hour, using the equation as shown below: Hence, the overhead rate is

Hence, the overhead rate is  Compute the budgeted overheads for the year, using MS-excel as shown below:

Compute the budgeted overheads for the year, using MS-excel as shown below:  The result of the above-excel table is as follows:

The result of the above-excel table is as follows:  Hence, the budgeted overheads are

Hence, the budgeted overheads are  b. Compute the total overheads absorbed, using MS-excel as shown below:

b. Compute the total overheads absorbed, using MS-excel as shown below:  The result of the above excel table is as follows:

The result of the above excel table is as follows:  Hence, the total overheads absorbed is

Hence, the total overheads absorbed is  c. Compute the over/under absorbed overheads, using the MS-excel as shown below:

c. Compute the over/under absorbed overheads, using the MS-excel as shown below:  The result of the above-excel table is as follows:

The result of the above-excel table is as follows:  0

0

Hence, the under absorbed overheads is 1

1

d. Compute the over/under absorbed overheads, using the MS-excel as shown below: 2

2

The result of the above-excel table is as follows: 3

3

Hence, the under absorbed overheads is 4

4

e. In part (c), the company allocates the overheads on the basis of standard hours and in part (d), the company allocates the overheads on the basis of actual machine hours. The difference in under absorbed overheads was arise due to the changes in the allocation policy of the company.

The treatment described in part (d) easily allocates the overheads on the basis of actual hours. Under this method, under/over absorbed overheads are just the difference between the budgeted overheads and the actual overheads.

It can be referred to as an accounting term which states all the indirect expenses incurred by an organization for operating a business. These expenses are not directly related to the manufacturing of a product or rendering of a service.

Over/Under Applied Overhead:

The overheads are absorbed based on some predetermined factor that may be machine hours or labor hours. These are called the budgeted overheads. These overheads and are then matched with the actual overheads. In case the actual overheads are more than the budgeted then that situation is called under-applied overhead and vice-versa.

a. Compute the overhead rate per machine hour, using the equation as shown below:

Hence, the overhead rate is Compute the budgeted overheads for the year, using MS-excel as shown below: The result of the above-excel table is as follows: Hence, the budgeted overheads are b. Compute the total overheads absorbed, using MS-excel as shown below: The result of the above excel table is as follows: Hence, the total overheads absorbed is c. Compute the over/under absorbed overheads, using the MS-excel as shown below: The result of the above-excel table is as follows: 0Hence, the under absorbed overheads is

1d. Compute the over/under absorbed overheads, using the MS-excel as shown below:

2The result of the above-excel table is as follows:

3Hence, the under absorbed overheads is

4e. In part (c), the company allocates the overheads on the basis of standard hours and in part (d), the company allocates the overheads on the basis of actual machine hours. The difference in under absorbed overheads was arise due to the changes in the allocation policy of the company.

The treatment described in part (d) easily allocates the overheads on the basis of actual hours. Under this method, under/over absorbed overheads are just the difference between the budgeted overheads and the actual overheads.

4

Lancaster Chamber Orchestra

The Lancaster Chamber Orchestra is a small community orchestra that offers two distinct concert series for its patrons. Series A is devoted entirely to the performance of a classical repertoire and offers 10 concerts throughout the year, while Series B consists of six pops concerts and serves to broaden the audience base of the ensemble.

Since programming needs change from concert to concert, musicians are hired on a per- service basis. (A service is either a rehearsal or a concert.) They are paid at differential average rates due to instrumental doubling requirements and also due to solo pay for woodwinds, percussion, and brass players. After the budget has been set, variances in musician costs are the result of changes in programming and rehearsal scheduling. Programming changes can cause different numbers of musicians to be needed for a particular series of rehearsals and concerts or can change the doubling requirements. Changes in rehearsal scheduling can alter needs for certain families of instruments at some rehearsals. For example, one Series A concert usually consists of six services, but not all instruments are required at each service. Programming and rehearsal scheduling are decided by the music director, Maestro Fritz Junger, but musician cost constraints are imposed by the director of production, Candice Wrightway. Budgeted and actual musician costs for the 2010-2011 season follow. When the budget was prepared at the beginning of the year, Alan Voit, director of marketing, admitted that projected ticket sales for the two series were optimistic, but he believed that his innovative advertising campaign would help the orchestra meet its goal. Although pops sales came in almost exactly on target, a devastating ice storm caused the cancellation of one of the classical concerts. Unfortunately, rehearsals had already been held and the musicians had been paid for their services. Series sales figures for the three levels of ticket prices follow. As with any orchestra, ticket sales alone are never enough to totally cover expenses, so the director of development, Lydia Givme, is responsible for the coordination of fundraising in the community. Unfortunately, the goals set at the beginning of the year did not anticipate an extended recession, with potential private, corporate, and government contributors tightening their fiscal belts.

Additional expenses include a long-term rental agreement for the hall, a permanent conductor, guest artists, music rental and advertising costs, and variable production costs based on total services. Music rental and advertising are treated as fixed expenses even though their cost may vary during the course of the season. Here are budgeted fixed and variable expenses for 2010-2011. The income statement for 2010-2011 follows. Required:

a. Calculate a flexible budget for the Lancaster Chamber Orchestra's 2010-2011 season.

b. After calculating the flexible budget, Randall Nobucs, director of finance, found a total unfavorable variance in net income of $53,158. Account for this unfavorable variance by calculating

(1) Revenue variances.

(2) Labor efficiency variances.

(3) Overhead efficiency and overhead spending variances.

c. Nobucs is concerned that if the orchestra faces similar problems in the next season, the accumulated deficit will cause bankruptcy. He argues with Alan Voit that a 15 percent increase in ticket prices would ensure a balanced budget for the 2010-2011 season. Discuss the feasibility of this strategy.

d. In examining the income statement, CEO Peter Morris is puzzled. He believes that all of his senior staff members are superb and is not sure where to lay the blame for the orchestra's dismal financial performance. Discuss the areas of specialized knowledge involved in the operation. Which person should be held accountable for each variance?

SOURCE: M Ames, J Dallas, R Krebs, W Perdue, and J Ricker.

The Lancaster Chamber Orchestra is a small community orchestra that offers two distinct concert series for its patrons. Series A is devoted entirely to the performance of a classical repertoire and offers 10 concerts throughout the year, while Series B consists of six pops concerts and serves to broaden the audience base of the ensemble.

Since programming needs change from concert to concert, musicians are hired on a per- service basis. (A service is either a rehearsal or a concert.) They are paid at differential average rates due to instrumental doubling requirements and also due to solo pay for woodwinds, percussion, and brass players. After the budget has been set, variances in musician costs are the result of changes in programming and rehearsal scheduling. Programming changes can cause different numbers of musicians to be needed for a particular series of rehearsals and concerts or can change the doubling requirements. Changes in rehearsal scheduling can alter needs for certain families of instruments at some rehearsals. For example, one Series A concert usually consists of six services, but not all instruments are required at each service. Programming and rehearsal scheduling are decided by the music director, Maestro Fritz Junger, but musician cost constraints are imposed by the director of production, Candice Wrightway. Budgeted and actual musician costs for the 2010-2011 season follow.

When the budget was prepared at the beginning of the year, Alan Voit, director of marketing, admitted that projected ticket sales for the two series were optimistic, but he believed that his innovative advertising campaign would help the orchestra meet its goal. Although pops sales came in almost exactly on target, a devastating ice storm caused the cancellation of one of the classical concerts. Unfortunately, rehearsals had already been held and the musicians had been paid for their services. Series sales figures for the three levels of ticket prices follow. As with any orchestra, ticket sales alone are never enough to totally cover expenses, so the director of development, Lydia Givme, is responsible for the coordination of fundraising in the community. Unfortunately, the goals set at the beginning of the year did not anticipate an extended recession, with potential private, corporate, and government contributors tightening their fiscal belts.Additional expenses include a long-term rental agreement for the hall, a permanent conductor, guest artists, music rental and advertising costs, and variable production costs based on total services. Music rental and advertising are treated as fixed expenses even though their cost may vary during the course of the season. Here are budgeted fixed and variable expenses for 2010-2011.

The income statement for 2010-2011 follows. Required: a. Calculate a flexible budget for the Lancaster Chamber Orchestra's 2010-2011 season.

b. After calculating the flexible budget, Randall Nobucs, director of finance, found a total unfavorable variance in net income of $53,158. Account for this unfavorable variance by calculating