Deck 22: Estates and Trusts: Their Nature and the Accountants Role

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

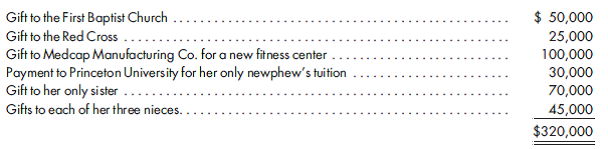

Calculation of gift and estate tax. Early in 2011, Nancy Fable was diagnosed with a terminal illness, and doctors gave her one more year to live. Aside from a 2010 $1,000,000 gift to the University of Georgia, she had not done any other gifting prior to 2011. She made the following gifts during 2011:

Early in 2012, she made gifts of $25,000 each to her sister, three nieces, and a nephew. In the spring of 2012, Nancy passed away, leaving an estate consisting of the following at her date of death:

a. One thousand shares of Google stock valued at $900 per share.

b. Real estate inMacon County, Georgia, valued at $3,250,000.

c. Household effects valued at $21,000.

d. Bank accounts totaling $780,000 and gold coins valued at $310,000.

e. Loan against the Macon County real estate consisting of $300,000 plus accrued interest of $7,200.

Funeral and other estate administrative expenses totaled $45,000. Property taxes of $4,000 on the real estate and income taxes of $27,000 were paid by the personal representative. In addition to the above insurance policy, Medcap Manufacturing owned an insurance policy on Nancy's life that had a death benefit of $150,000.

Subsequent to Nancy's death, but within the 6-month alternative valuation date, the following occurred:

a. Two months after Nancy's death, theMacon County land was sold for $3,050,000, and the principal amount of the real estate loan was paid off along with revised accrued interest of $8,300.

b. Three months after Nancy's death, the gold market began to collapse, and the coins were sold for $250,000.

c. ExxonMobil stock was discovered. The stock had a value of $22,000 at Nancy's date of death and was subsequently sold for $23,000.

d. The bubble burst and four months after Nancy's death, the Google stock was sold for $780 per share.

e. The household effects were distributed to family and friends and are excluded from estate assets.

f. All remaining cash, including $21,000 of interest since Nancy's date of death, was distributed as follows: one-third to immediate family and the balance to the University of Georgia to endow a chaired professorship in the Theatre Department. Determine the total amount to be paid for both estate and gift taxes over the 3-year period of 2010 through 2012 by year.

Early in 2012, she made gifts of $25,000 each to her sister, three nieces, and a nephew. In the spring of 2012, Nancy passed away, leaving an estate consisting of the following at her date of death:

a. One thousand shares of Google stock valued at $900 per share.

b. Real estate inMacon County, Georgia, valued at $3,250,000.

c. Household effects valued at $21,000.

d. Bank accounts totaling $780,000 and gold coins valued at $310,000.

e. Loan against the Macon County real estate consisting of $300,000 plus accrued interest of $7,200.

Funeral and other estate administrative expenses totaled $45,000. Property taxes of $4,000 on the real estate and income taxes of $27,000 were paid by the personal representative. In addition to the above insurance policy, Medcap Manufacturing owned an insurance policy on Nancy's life that had a death benefit of $150,000.

Subsequent to Nancy's death, but within the 6-month alternative valuation date, the following occurred:

a. Two months after Nancy's death, theMacon County land was sold for $3,050,000, and the principal amount of the real estate loan was paid off along with revised accrued interest of $8,300.

b. Three months after Nancy's death, the gold market began to collapse, and the coins were sold for $250,000.

c. ExxonMobil stock was discovered. The stock had a value of $22,000 at Nancy's date of death and was subsequently sold for $23,000.

d. The bubble burst and four months after Nancy's death, the Google stock was sold for $780 per share.

e. The household effects were distributed to family and friends and are excluded from estate assets.

f. All remaining cash, including $21,000 of interest since Nancy's date of death, was distributed as follows: one-third to immediate family and the balance to the University of Georgia to endow a chaired professorship in the Theatre Department. Determine the total amount to be paid for both estate and gift taxes over the 3-year period of 2010 through 2012 by year.

Question

Question

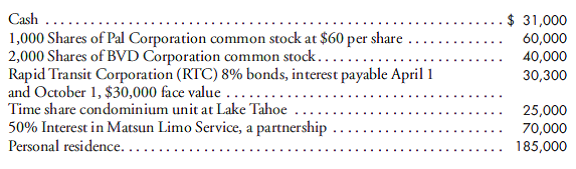

Preparation of a charge and discharge statement. Eleanor Matsun died on June 1 of the current year, leaving a valid will with JamesMadison being named as her personal representative. All of the following occurred in the year of her death:

a. The personal representative prepared the following inventory of assets at fair market value as of the date of death:.

b. Subsequent to filing the above inventory with the court, the personal representative discovered the decedent's gold coin collection valued at $18,000.

c. On June 20, $2,500 was received from Pal Corporation for dividends declared onMay 10 to shareholders of record on May 31.

d. On July 7, the time share condominium was sold for $30,000.

e. The following items were paid during the period from June 2 through July 31:

f. On July 5, a check for $15,000 was received for the decedent's portion of Matsun Limo Service income earned during the quarter ended June 30. Income is assumed to be earned evenly over the quarter.

g. The decedent's partner in the limo service offered the personal representative $65,000 for the decedent's interest in the partnership. After much negotiation, the interest was sold for $80,000.

h. In mid-September, the decedent's personal residence was sold for $162,000, net of brokerage and closing costs totaling $15,000. The outstanding mortgage and accrued interest were promptly paid in the amount of $82,800. At the date of death, the mortgage balance along with accrued interest was $81,100.

i. On October 1, a check was received for interest on the RTC bonds.

j. On November 5, the decedent's income tax return for the year of death was filed and $6,400 of additional taxes was sent in with the return.

Prepare a charge and discharge statement as of December 31 of the current year.

a. The personal representative prepared the following inventory of assets at fair market value as of the date of death:.

b. Subsequent to filing the above inventory with the court, the personal representative discovered the decedent's gold coin collection valued at $18,000.

c. On June 20, $2,500 was received from Pal Corporation for dividends declared onMay 10 to shareholders of record on May 31.

d. On July 7, the time share condominium was sold for $30,000.

e. The following items were paid during the period from June 2 through July 31:

f. On July 5, a check for $15,000 was received for the decedent's portion of Matsun Limo Service income earned during the quarter ended June 30. Income is assumed to be earned evenly over the quarter.

g. The decedent's partner in the limo service offered the personal representative $65,000 for the decedent's interest in the partnership. After much negotiation, the interest was sold for $80,000.

h. In mid-September, the decedent's personal residence was sold for $162,000, net of brokerage and closing costs totaling $15,000. The outstanding mortgage and accrued interest were promptly paid in the amount of $82,800. At the date of death, the mortgage balance along with accrued interest was $81,100.

i. On October 1, a check was received for interest on the RTC bonds.

j. On November 5, the decedent's income tax return for the year of death was filed and $6,400 of additional taxes was sent in with the return.

Prepare a charge and discharge statement as of December 31 of the current year.

Question

Question

Question

Question

Question

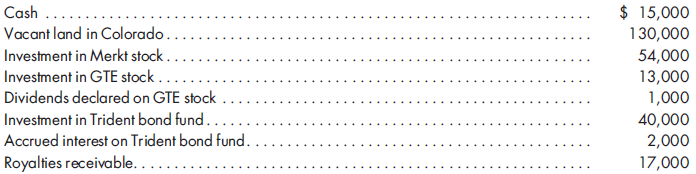

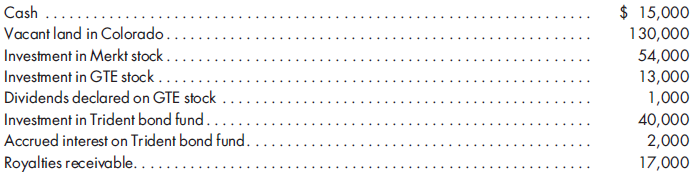

Accounting for estate principal and income. Jason Jackson was killed in a mountain-climbing accident in British Columbia. As Jason's trusted friend and CPA, you have been named executor of his estate and guardian to his minor child, Cody Jackson. Jason's estate consists of the following assets subject to probate:

Prepare journal entries to record the above inventory and the following events related to the estate principal and income:

1. Final medical and funeral expenses of $22,000 are paid.

2. An individual retirement account (IRA) naming Jackson's estate as beneficiary and having a value of $37,000 subsequently is discovered.

3. Cash dividends of $1,000 on the GTE stock and $2,700 on theMerkt stock are received.

4. The vacant land in Colorado is sold for $150,000 less accrued property taxes of $2,000 and a broker's commission of $8,000.

5. Interest of $2,400 is received on the Trident bond fund, and the royalty receivable is also collected.

6. Income taxes of $4,000 on the decedent's final tax return are paid, along with $24,000 of other claims against the estate.

7. A legacy of $15,000 is paid to the High Adventure Climbing School.

8. Administrative expenses of $3,200 are paid, of which $100 is traceable to income.

Prepare journal entries to record the above inventory and the following events related to the estate principal and income:

1. Final medical and funeral expenses of $22,000 are paid.

2. An individual retirement account (IRA) naming Jackson's estate as beneficiary and having a value of $37,000 subsequently is discovered.

3. Cash dividends of $1,000 on the GTE stock and $2,700 on theMerkt stock are received.

4. The vacant land in Colorado is sold for $150,000 less accrued property taxes of $2,000 and a broker's commission of $8,000.

5. Interest of $2,400 is received on the Trident bond fund, and the royalty receivable is also collected.

6. Income taxes of $4,000 on the decedent's final tax return are paid, along with $24,000 of other claims against the estate.

7. A legacy of $15,000 is paid to the High Adventure Climbing School.

8. Administrative expenses of $3,200 are paid, of which $100 is traceable to income.

Question

Question

Charge and discharge statement. Given the facts of Exercise 8, (1) prepare the charge and discharge statement that would have resulted from the above events and (2) prepare the entries to transfer all estate principal and income amounts to a trust for the benefit of Cody Jackson.

REFERENCE:

Accounting for estate principal and income. Jason Jackson was killed in a mountain-climbing accident in British Columbia. As Jason's trusted friend and CPA, you have been named executor of his estate and guardian to his minor child, Cody Jackson. Jason's estate consists of the following assets subject to probate:

Prepare journal entries to record the above inventory and the following events related to the estate principal and income:

1. Final medical and funeral expenses of $22,000 are paid.

2. An individual retirement account (IRA) naming Jackson's estate as beneficiary and having a value of $37,000 subsequently is discovered.

3. Cash dividends of $1,000 on the GTE stock and $2,700 on theMerkt stock are received.

4. The vacant land in Colorado is sold for $150,000 less accrued property taxes of $2,000 and a broker's commission of $8,000.

5. Interest of $2,400 is received on the Trident bond fund, and the royalty receivable is also collected.

6. Income taxes of $4,000 on the decedent's final tax return are paid, along with $24,000 of other claims against the estate.

7. A legacy of $15,000 is paid to the High Adventure Climbing School.

8. Administrative expenses of $3,200 are paid, of which $100 is traceable to income.

REFERENCE:

Accounting for estate principal and income. Jason Jackson was killed in a mountain-climbing accident in British Columbia. As Jason's trusted friend and CPA, you have been named executor of his estate and guardian to his minor child, Cody Jackson. Jason's estate consists of the following assets subject to probate:

Prepare journal entries to record the above inventory and the following events related to the estate principal and income:

1. Final medical and funeral expenses of $22,000 are paid.

2. An individual retirement account (IRA) naming Jackson's estate as beneficiary and having a value of $37,000 subsequently is discovered.

3. Cash dividends of $1,000 on the GTE stock and $2,700 on theMerkt stock are received.

4. The vacant land in Colorado is sold for $150,000 less accrued property taxes of $2,000 and a broker's commission of $8,000.

5. Interest of $2,400 is received on the Trident bond fund, and the royalty receivable is also collected.

6. Income taxes of $4,000 on the decedent's final tax return are paid, along with $24,000 of other claims against the estate.

7. A legacy of $15,000 is paid to the High Adventure Climbing School.

8. Administrative expenses of $3,200 are paid, of which $100 is traceable to income.

Question

Question

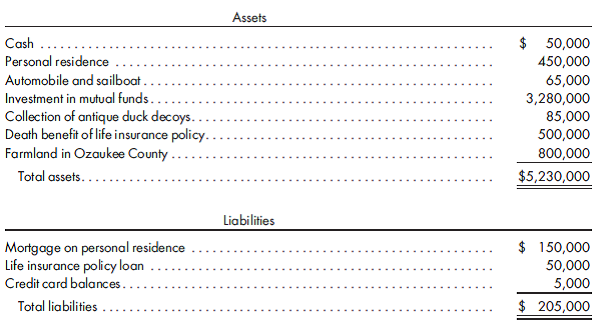

Recording activities for an estate and a trust. At the time of Robert Granger's death, his estate consisted of the following assets and liabilities measured at fair market value:

The following information is relevant to the administration of Robert's estate:

a. Robert is a single person and has two minor children from a previous marriage. After satisfying the other provisions of his will, the balance of Robert's estate is to be transferred to a trust for the benefit of his minor children. Annual trust income in the amount of $15,000 is to be transferred to the children. Upon attaining the age of 21, each child would receive corpus of $25,000. The remaining corpus of the trust and any undistributed income is to be paid out to the children when they both have attained the age of 25.

b. Title to the personal residence, subject to the mortgage, will be transferred to Robert's sister who is to serve as the guardian for his minor children.

c. The collection of antique duck decoys is to be given to Ducks Unlimited which is a qualifying charitable organization.

d. Robert's sailboat, valued at $35,000, is to be given as a charitable contribution to the Milwaukee Community Sailing Center. The automobile will be given to his nephew Roger Stevens.

e. Funeral and administrative expenses of the estate are $25,000.

f. Investments in mutual funds with an estate value of $170,000 were sold for $180,000 to provide necessary liquidity.

Subsequent to the settlement of Robert's estate, the following activity occurred in the children's trust during the first month:

a. The farmland was rented for $25,000. Property taxes and other operating expenses associated with the farmland were incurred in the amount of $8,000.

b. Mutual funds with an estate value of $120,000 were sold for $132,000. Mutual funds with an estate value of $50,000 were sold for $45,000.

c. Income on the mutual fund investments was $22,000.

d. The trustee made a payment of corpus to Robert's daughter upon her turning 21 years of age.

e. After distributing the required amount of trust income, all available cash with the exception of $5,000 of income cash was invested in mutual funds.

Prepare all necessary entries to record the activities of the estate and the trust. Unified transfer tax rates and the exclusion amount as set forth in the text should be used.

The following information is relevant to the administration of Robert's estate:

a. Robert is a single person and has two minor children from a previous marriage. After satisfying the other provisions of his will, the balance of Robert's estate is to be transferred to a trust for the benefit of his minor children. Annual trust income in the amount of $15,000 is to be transferred to the children. Upon attaining the age of 21, each child would receive corpus of $25,000. The remaining corpus of the trust and any undistributed income is to be paid out to the children when they both have attained the age of 25.

b. Title to the personal residence, subject to the mortgage, will be transferred to Robert's sister who is to serve as the guardian for his minor children.

c. The collection of antique duck decoys is to be given to Ducks Unlimited which is a qualifying charitable organization.

d. Robert's sailboat, valued at $35,000, is to be given as a charitable contribution to the Milwaukee Community Sailing Center. The automobile will be given to his nephew Roger Stevens.

e. Funeral and administrative expenses of the estate are $25,000.

f. Investments in mutual funds with an estate value of $170,000 were sold for $180,000 to provide necessary liquidity.

Subsequent to the settlement of Robert's estate, the following activity occurred in the children's trust during the first month:

a. The farmland was rented for $25,000. Property taxes and other operating expenses associated with the farmland were incurred in the amount of $8,000.

b. Mutual funds with an estate value of $120,000 were sold for $132,000. Mutual funds with an estate value of $50,000 were sold for $45,000.

c. Income on the mutual fund investments was $22,000.

d. The trustee made a payment of corpus to Robert's daughter upon her turning 21 years of age.

e. After distributing the required amount of trust income, all available cash with the exception of $5,000 of income cash was invested in mutual funds.

Prepare all necessary entries to record the activities of the estate and the trust. Unified transfer tax rates and the exclusion amount as set forth in the text should be used.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/19

Play

Full screen (f)

Deck 22: Estates and Trusts: Their Nature and the Accountants Role

1

Taxation of gifts. Determine the correct value for each of the following questions:

1. Assume that an individual gives cash to the following parties: $25,000 to a charitable organization, $15,000 to her grandson for his college tuition, $8,000 to her granddaughter to buy a car, and $14,000 to her spouse for a trip to France. What amount of gifts is considered taxable?

2. Assume that an individual has given $25,000 to each of his four grandchildren for each of the past three years and $50,000 to a charitable organization. If he wants to make a single gift to each of his four grandchildren, what would the maximum gift per grandchild be in order to avoid all gift tax?

3. Your client made the following gifts last year: $200,000 to each of her three children, $50,000 to her brother, and $10,000 to each of her eight grandchildren. Prior to that, your client made a single gift of $50,000 to each of her two nieces. If she made a gift of $500,000 to her sister in the current year, what amount of gift tax would be due?

4. Assume the same facts as in item (3) above except that your client married during the current year prior to making the gift to her sister. Furthermore, assume that her spouse is a consenting spouse for purposes of gifting to the sister and they both gave the gift to the sister. The new spouse had prior taxable gifts of $100,000. What amount of gift tax would be due?

5. Assume that an individual and his consenting spouse hadmade no gifts prior to last year.However, last year, they gave $50,000, $32,000, and $72,000, to their daughter, son, and neighbor, respectively. This year, they want to do significant gifting to the same three individuals but do not want the cumulative net tax on gifts to exceed $61,500 per spouse. Assuming a minimum gift of $30,000 to each party, what is the sum of all gifts that could be made this year?

1. Assume that an individual gives cash to the following parties: $25,000 to a charitable organization, $15,000 to her grandson for his college tuition, $8,000 to her granddaughter to buy a car, and $14,000 to her spouse for a trip to France. What amount of gifts is considered taxable?

2. Assume that an individual has given $25,000 to each of his four grandchildren for each of the past three years and $50,000 to a charitable organization. If he wants to make a single gift to each of his four grandchildren, what would the maximum gift per grandchild be in order to avoid all gift tax?

3. Your client made the following gifts last year: $200,000 to each of her three children, $50,000 to her brother, and $10,000 to each of her eight grandchildren. Prior to that, your client made a single gift of $50,000 to each of her two nieces. If she made a gift of $500,000 to her sister in the current year, what amount of gift tax would be due?

4. Assume the same facts as in item (3) above except that your client married during the current year prior to making the gift to her sister. Furthermore, assume that her spouse is a consenting spouse for purposes of gifting to the sister and they both gave the gift to the sister. The new spouse had prior taxable gifts of $100,000. What amount of gift tax would be due?

5. Assume that an individual and his consenting spouse hadmade no gifts prior to last year.However, last year, they gave $50,000, $32,000, and $72,000, to their daughter, son, and neighbor, respectively. This year, they want to do significant gifting to the same three individuals but do not want the cumulative net tax on gifts to exceed $61,500 per spouse. Assuming a minimum gift of $30,000 to each party, what is the sum of all gifts that could be made this year?

Compute the taxable amount on gift as follows:

• $25,000 paid to a charitable organization is exempted under gift tax.

• $15,000 to her grandson for his college tuition is taxable under gift taxation.

Hence, the amount of tax as for the tax rate of 2009 (mentioned in Exhibit 2o-1) is 20% of the gift amount. That is,

.

.

• $8,000 to her granddaughter to buy a car is below the annual exclusion amount of $10,000.

• $14,000 to her spouses for a trip to France. Gift to spouse is exempted under gift taxation.

Total gift tax is

Therefore, the person has to pay $3,000 as gift tax.

Therefore, the person has to pay $3,000 as gift tax.

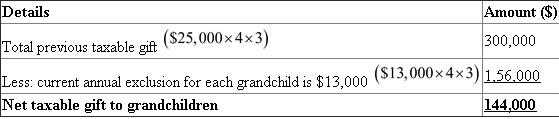

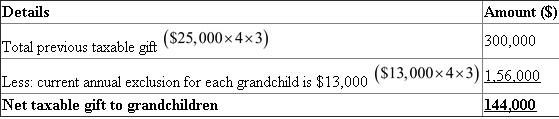

2. An individual has given $25,000 to each of his 4 grandchildren for the past 3 years, and $50,000 to a charitable organization.

Calculate the maximum amount of gift to each grandchild in order to avoid gift tax.

Calculate the amount of previous taxable gift to the grandchildren as follows:

Taxable gift to each grandchild is $25,000.

Number of grandchildren is 4.

Number of previous years is 3 years.

Calculate the maximum gift per grandchild as follows:

Calculate the maximum gift per grandchild as follows:

Therefore, the maximum gift per grandchild to avoid all gift tax is

.

3. Calculate the cumulative taxable gift as follows:

The gift list of the client for the last year is as follows:

• $200,000 to each of her three children.

• $50,000 to her brother.

• $10,000 to her eight grandchildren.

• Prior to these, the client had made a single gift of $50,000 to each of her two nieces.

Compute the amount of gift tax that would be due if she made a gift of $500,000 to her sister in the current year, as follows:

The annual exclusion for each person is $13,000.

Note 1: Gift to all grandchildren is less than $13,000.

Note 2: Calculation of tax on total gift:

Total taxable gift: $1,159,000.

Hence, tax on total taxable gift is tax on gift up to $1,000,000 as per 2009 tax rate (exhibit 21-1). That is: is $345,800 plus 41% 0f

. That is: 65,190.

. That is: 65,190.

Hence, total tax on gift is

Therefore, the net tax on gift for the current year is

Therefore, the net tax on gift for the current year is

.

.

4. Calculate the amount of gift tax that would be due as follows:

• The client is married in the current year prior to making a gift to her sister.

• Her spouse is a consenting spouse; for the purpose of gifting to her sister, they both gifted to her sister. So, the amount of gift given by the client to her sister is

.

.

• The new spouse had a prior taxable gift of $100,000.

Calculate the tax, considering the total gift made in item 3:

Note 3: Calculation of tax on total gift:

Note 3: Calculation of tax on total gift:

Total amount of taxable gift: $909,000.

Hence, tax on total taxable gift is tax on gift up to $750,000 as per 2009 tax rate (exhibit 20-1). That is: is $155,800 plus 39% of

. That is: 62,010.

. That is: 62,010.

Hence, total tax on gift is

.

.

Note 4: The lifetime exclusion amount exceeds the tax on total gift. Therefore, no tax would be due.

Calculate the tax on gift, considering the new spouse:

Note 3: Calculation of tax on total gift:

Note 3: Calculation of tax on total gift:

Total amount of taxable gift: $337,000.

Hence, tax on total taxable gift is tax on gift up to $250,000 as per 2009 tax rate (exhibit 20-1). That is: is $38,800 plus 34% 0f

. That is: 29,580.

. That is: 29,580.

Hence, total tax on gift is

.

.

Note 4: The lifetime exclusion amount exceeds the tax on total gift. Therefore, no tax would be due.

5. Calculate the sum of all gifts made in the current year as follows:

The individual and his consenting spouse had not made any gift prior to last year.

Last year, they gave $50,000, $32,000, and $72,000, to their daughter, son, and neighbor, respectively.

The maximum amount of cumulative gift tax is $61,500.

So, the maximum tax before lifetime exclusion should be $407,300. That is, Net tax on gift of $61,500 plus lifetime exclusion.

Calculate the amount of taxable gift on a tax amount of $457,300 as follows:

Calculate the total of all gifts that could be made in the current year as follows:

Calculate the total of all gifts that could be made in the current year as follows:

For spouse 1:

Note: Annual exclusion for 2 spouses is $26,000. That is,

Note: Annual exclusion for 2 spouses is $26,000. That is,

Calculate the total of all gifts that could be made in the current year as follows:

Calculate the total of all gifts that could be made in the current year as follows:

For spouse 2:

Note: Annual exclusion for 2 spouses is $26,000. That is,

Note: Annual exclusion for 2 spouses is $26,000. That is,

Therefore, the total of all gifts that could be made in the current year is

Therefore, the total of all gifts that could be made in the current year is

.

.

• $25,000 paid to a charitable organization is exempted under gift tax.

• $15,000 to her grandson for his college tuition is taxable under gift taxation.

Hence, the amount of tax as for the tax rate of 2009 (mentioned in Exhibit 2o-1) is 20% of the gift amount. That is,

.• $8,000 to her granddaughter to buy a car is below the annual exclusion amount of $10,000.

• $14,000 to her spouses for a trip to France. Gift to spouse is exempted under gift taxation.

Total gift tax is

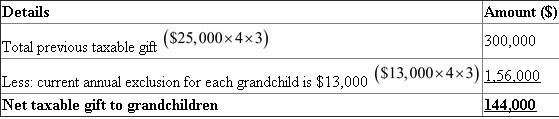

Therefore, the person has to pay $3,000 as gift tax.2. An individual has given $25,000 to each of his 4 grandchildren for the past 3 years, and $50,000 to a charitable organization.

Calculate the maximum amount of gift to each grandchild in order to avoid gift tax.

Calculate the amount of previous taxable gift to the grandchildren as follows:

Taxable gift to each grandchild is $25,000.

Number of grandchildren is 4.

Number of previous years is 3 years.

Calculate the maximum gift per grandchild as follows: Therefore, the maximum gift per grandchild to avoid all gift tax is

.

3. Calculate the cumulative taxable gift as follows:

The gift list of the client for the last year is as follows:

• $200,000 to each of her three children.

• $50,000 to her brother.

• $10,000 to her eight grandchildren.

• Prior to these, the client had made a single gift of $50,000 to each of her two nieces.

Compute the amount of gift tax that would be due if she made a gift of $500,000 to her sister in the current year, as follows:

The annual exclusion for each person is $13,000.

Note 1: Gift to all grandchildren is less than $13,000.

Note 2: Calculation of tax on total gift:

Total taxable gift: $1,159,000.

Hence, tax on total taxable gift is tax on gift up to $1,000,000 as per 2009 tax rate (exhibit 21-1). That is: is $345,800 plus 41% 0f

. That is: 65,190.Hence, total tax on gift is

Therefore, the net tax on gift for the current year is .4. Calculate the amount of gift tax that would be due as follows:

• The client is married in the current year prior to making a gift to her sister.

• Her spouse is a consenting spouse; for the purpose of gifting to her sister, they both gifted to her sister. So, the amount of gift given by the client to her sister is

.• The new spouse had a prior taxable gift of $100,000.

Calculate the tax, considering the total gift made in item 3:

Note 3: Calculation of tax on total gift:Total amount of taxable gift: $909,000.

Hence, tax on total taxable gift is tax on gift up to $750,000 as per 2009 tax rate (exhibit 20-1). That is: is $155,800 plus 39% of

. That is: 62,010.Hence, total tax on gift is

.Note 4: The lifetime exclusion amount exceeds the tax on total gift. Therefore, no tax would be due.

Calculate the tax on gift, considering the new spouse:

Note 3: Calculation of tax on total gift:Total amount of taxable gift: $337,000.

Hence, tax on total taxable gift is tax on gift up to $250,000 as per 2009 tax rate (exhibit 20-1). That is: is $38,800 plus 34% 0f

. That is: 29,580.Hence, total tax on gift is

.Note 4: The lifetime exclusion amount exceeds the tax on total gift. Therefore, no tax would be due.

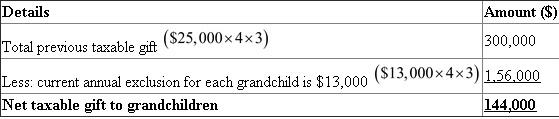

5. Calculate the sum of all gifts made in the current year as follows:

The individual and his consenting spouse had not made any gift prior to last year.

Last year, they gave $50,000, $32,000, and $72,000, to their daughter, son, and neighbor, respectively.

The maximum amount of cumulative gift tax is $61,500.

So, the maximum tax before lifetime exclusion should be $407,300. That is, Net tax on gift of $61,500 plus lifetime exclusion.

Calculate the amount of taxable gift on a tax amount of $457,300 as follows:

Calculate the total of all gifts that could be made in the current year as follows: For spouse 1:

Note: Annual exclusion for 2 spouses is $26,000. That is, Calculate the total of all gifts that could be made in the current year as follows: For spouse 2:

Note: Annual exclusion for 2 spouses is $26,000. That is, Therefore, the total of all gifts that could be made in the current year is . 2

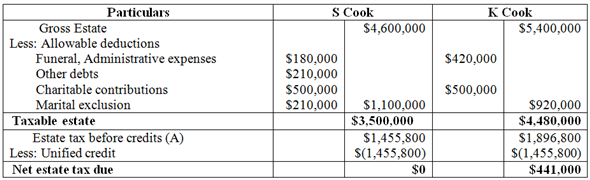

Determining and minimizing estate tax. Spencer Cook died on July 18 of the current year, leaving a gross estate of $4,600,000. Claims to be settled against that estate included funeral, administrative, and medical expenses of $180,000 and other debts of $210,000. Spencer's wife Sara has a considerable estate of her own, and she and Spencer have each agreed to leave $500,000 of their personal estate to charity. One year after Spencer's death, Sara passed away. Allowable expenses against Sara's estate totaled $420,000 excluding charitable bequests.

Using the estate tax rates and unified credit in the text:

1. Determine the estate tax to be paid by both Spencer and Sara assuming that no credit shelter trusts are employed and that Sara's gross estate is $7,300,000 including the assets inherited from Spencer.

2. Assume that prior to death Spencer and Sara both created a credit shelter trust calling for the surviving spouse to be the income beneficiary and their children to be the recipient of the principal. The principal of the trust is equal to the applicable exclusion amount. Determine the estate tax to be paid by both Spencer and Sara assuming that Sara's gross estate at the date of her death was $5,400,000 including the assets inherited from Spencer.

Using the estate tax rates and unified credit in the text:

1. Determine the estate tax to be paid by both Spencer and Sara assuming that no credit shelter trusts are employed and that Sara's gross estate is $7,300,000 including the assets inherited from Spencer.

2. Assume that prior to death Spencer and Sara both created a credit shelter trust calling for the surviving spouse to be the income beneficiary and their children to be the recipient of the principal. The principal of the trust is equal to the applicable exclusion amount. Determine the estate tax to be paid by both Spencer and Sara assuming that Sara's gross estate at the date of her death was $5,400,000 including the assets inherited from Spencer.

a.

The estate tax before credits is $780,800 plus 45% on balance of the taxable estate over $2,000,000. Therefore, the tax is $2,751,800.

The estate tax before credits is $780,800 plus 45% on balance of the taxable estate over $2,000,000. Therefore, the tax is $2,751,800.

2.

Determine the estate tax to be paid to S and K Cook:

Condition: Assuming a credit shelter trust is employed.

b.

b.

The estate tax before credits is $780,800 plus 45% on the balance of the taxable estate over $2,000,000. Therefore, the tax is $1,896,800.

The estate tax before credits is $780,800 plus 45% on the balance of the taxable estate over $2,000,000. Therefore, the tax is $1,896,800.

The estate tax before credits is $780,800 plus 45% on balance of the taxable estate over $2,000,000. Therefore, the tax is $2,751,800.2.

Determine the estate tax to be paid to S and K Cook:

Condition: Assuming a credit shelter trust is employed.

b. The estate tax before credits is $780,800 plus 45% on the balance of the taxable estate over $2,000,000. Therefore, the tax is $1,896,800. 3

Explain why it is important to separately account for the principal and income of an estate and what happens if such assets are not adequate to satisfy demonstrative or general legacies.

If the principal assets and income of the deceased person are not adequate to satisfy the demonstrative and the general legacies, then a process of abatement is followed.

The abatement method states that the available funds are to be distributed as per the order of legacies.

In such a situation, where the assets are not adequate to satisfy the demonstrative legacy, the inadequate amount of the demonstrative legacy becomes a general legacy. Again, if the general legacy is not satisfied, the available funds are to be distributed proportionately among the persons mentioned in the will of the deceased person.

The following is an example to explain how an abatement process is applied if there are inadequate assets to satisfy the legacies.

Mr. A mentioned in his will that the $100,000 income from insurance policies is to be distributed equally between his two sons in the ratio of 3:2 as demonstrative legacy and $40,000 of the available funds is to be distributed equally between his two grandchildren as general legacy.

After the death of Mr. A, its fiduciary found that the income derived from the insurance policy proceeds is $80,000 and the available funds are $30,000.

From the above situation, it is found that $80,000 is to be paid proportionately between the two sons. But there remains a deficiency of $20,000 ($100,000 - $80,000) which is yet to be paid.

As per the order of the legacies of abatement process, the inadequate amount of $20,000 as a demonstrative legacy now becomes general legacy.

Now, the total general legacy to be distributed becomes $60,000 ($20,000+$40,000).

As the available funds are only $30,000, it is to be divided equally between the original general legacy and the converted general legacy; that is, the first $15,000 is to be distributed between the two sons in the ratio of 3:2 and the rest $15,000 is to be distributed equally between the two grandchildren.

Therefore, the first son would receive $9,000 ($15,000×3/5) and the second son would receive $6,000 ($15,000×2/5). However, the two grandchildren would receive each $7,500 ($15,000/2).

The abatement method states that the available funds are to be distributed as per the order of legacies.

In such a situation, where the assets are not adequate to satisfy the demonstrative legacy, the inadequate amount of the demonstrative legacy becomes a general legacy. Again, if the general legacy is not satisfied, the available funds are to be distributed proportionately among the persons mentioned in the will of the deceased person.

The following is an example to explain how an abatement process is applied if there are inadequate assets to satisfy the legacies.

Mr. A mentioned in his will that the $100,000 income from insurance policies is to be distributed equally between his two sons in the ratio of 3:2 as demonstrative legacy and $40,000 of the available funds is to be distributed equally between his two grandchildren as general legacy.

After the death of Mr. A, its fiduciary found that the income derived from the insurance policy proceeds is $80,000 and the available funds are $30,000.

From the above situation, it is found that $80,000 is to be paid proportionately between the two sons. But there remains a deficiency of $20,000 ($100,000 - $80,000) which is yet to be paid.

As per the order of the legacies of abatement process, the inadequate amount of $20,000 as a demonstrative legacy now becomes general legacy.

Now, the total general legacy to be distributed becomes $60,000 ($20,000+$40,000).

As the available funds are only $30,000, it is to be divided equally between the original general legacy and the converted general legacy; that is, the first $15,000 is to be distributed between the two sons in the ratio of 3:2 and the rest $15,000 is to be distributed equally between the two grandchildren.

Therefore, the first son would receive $9,000 ($15,000×3/5) and the second son would receive $6,000 ($15,000×2/5). However, the two grandchildren would receive each $7,500 ($15,000/2).

4

Distinguishing between principal and income. Roger Kramer's wife Sarah passed away five years ago, and she made Roger promise to continue to provide care for Sarah's sister Margaret Smith and let her live in their residence for a period of time. Roger and Sarah had no children, and Margaret Smith was like a daughter to them. Roger passed away, and his will contained the following provisions:

a. $200,000 of estate principal should be donated to the Sierra Club and the balance, less appropriate expenses, should be placed in theMargaret Smith trust.

b. The Margaret Smith trust calls for 80% of periodic net income to be paid out to Margaret Smith with the balance to be considered trust corpus.

c. The trust is to be terminated two years after Roger's death at which time 60% of the corpus will be given to Margaret Smith and the balance to the Milwaukee Foundation to be placed in a fund to support environmental issues dealing with alternative energy sources.

The following events occurred within one year of Roger's death:

1. In addition to the personal residence (valued at $350,000), the inventory at fair value of Roger's estate consisted of $230,000 cash, securities worth $210,000, personal effects worth $12,000, and a sailboat worth $8,000.

2. Mortgage payments on the residence were paid in the amount of $24,000, of which $8,000 was interest ($2,000 of which had accrued as of Roger's date of death).

3. Funeral and attorney fees to administer the estate were $27,000. Medical expenses incurred up to Roger's death were $21,000. Income taxes of $13,000 were due on Roger's final personal tax return.

4. Securities existing at the date of death with a cost of $130,000 and a market value of $178,000 were subsequently sold for $164,000. The proceeds upon sale were reinvested into bonds. Interest of $4,000 was received on the bonds.

5. A delinquency notice was received indicating that real estate taxes on the residence from last year remained unpaid in the amount of $12,000 plus interest and penalties of $2,000.

6. Dividends on the securities were received in the amount of $27,000, of which $7,000 were declared as of Roger's death.

7. Utilities and normal repairs and maintenance on the residence were $7,200, of which $1,200 had remained unpaid as of the date of death.

8. Out of estate assets, $15,000 was spent to replace the roof on the residence and $3,000 was paid for lawn care.

9. A bill was received from the Yacht Club indicating that Roger had unpaid dues and charges of $1,400. Margaret decided to continue membership in the club and paid additional dues and charges of $2,800.

Assuming that the trustee of the trust has approved all of the above, prepare a schedule to determine the principal and income balances after periodic distributions have been made to Margaret.

a. $200,000 of estate principal should be donated to the Sierra Club and the balance, less appropriate expenses, should be placed in theMargaret Smith trust.

b. The Margaret Smith trust calls for 80% of periodic net income to be paid out to Margaret Smith with the balance to be considered trust corpus.

c. The trust is to be terminated two years after Roger's death at which time 60% of the corpus will be given to Margaret Smith and the balance to the Milwaukee Foundation to be placed in a fund to support environmental issues dealing with alternative energy sources.

The following events occurred within one year of Roger's death:

1. In addition to the personal residence (valued at $350,000), the inventory at fair value of Roger's estate consisted of $230,000 cash, securities worth $210,000, personal effects worth $12,000, and a sailboat worth $8,000.

2. Mortgage payments on the residence were paid in the amount of $24,000, of which $8,000 was interest ($2,000 of which had accrued as of Roger's date of death).

3. Funeral and attorney fees to administer the estate were $27,000. Medical expenses incurred up to Roger's death were $21,000. Income taxes of $13,000 were due on Roger's final personal tax return.

4. Securities existing at the date of death with a cost of $130,000 and a market value of $178,000 were subsequently sold for $164,000. The proceeds upon sale were reinvested into bonds. Interest of $4,000 was received on the bonds.

5. A delinquency notice was received indicating that real estate taxes on the residence from last year remained unpaid in the amount of $12,000 plus interest and penalties of $2,000.

6. Dividends on the securities were received in the amount of $27,000, of which $7,000 were declared as of Roger's death.

7. Utilities and normal repairs and maintenance on the residence were $7,200, of which $1,200 had remained unpaid as of the date of death.

8. Out of estate assets, $15,000 was spent to replace the roof on the residence and $3,000 was paid for lawn care.

9. A bill was received from the Yacht Club indicating that Roger had unpaid dues and charges of $1,400. Margaret decided to continue membership in the club and paid additional dues and charges of $2,800.

Assuming that the trustee of the trust has approved all of the above, prepare a schedule to determine the principal and income balances after periodic distributions have been made to Margaret.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

5

Determining estate tax and general legacies. Walter Campbell was a very giving person all of his life. His surviving children speak frequently of his generosity not only toward his deceased wife but also to many beyond his immediate family. Unfortunately, Walter's will proved to be more generous than his estate was able to support. Provisions ofWalter's will included the following:

a. My entire collection of Navajo rugs and Acoma pottery (fair value at date of death is $120,000) is to be given to the Museum of Northern New Mexico, a charitable organization.

b. My residence (fair value at date of death is $550,000) is to be given to my younger brother Thomas along with $2,500,000 from my brokerage account at Wachovia Securities (fair value at date of death is $2,200,000).

c. My brokerage account at Schmidt Investment Services (fair value at date of death is $900,000) is to be liquidated with $500,000 going to each of my two sisters.

d. My collection of antique pistols (fair value at date of death is $85,000) is to be given to my son-in-law Eric Jacobsen.

e. My hunting land in Buffalo County, Wisconsin (fair value at date of death is $750,000), is to be sold and my uncle is to receive $700,000 of the proceeds.

f. Of the proceeds from my life insurance policies (fair value at date of death is $250,000), $200,000 is to be given to First Church of Brookfield, a charitable organization.

g. Each of my eight grandchildren is to receive $50,000, and each of my three children is to receive $400,000.

h. The balance of my assets is to be divided equally between the Kohler Arts Center in Kohler, Wisconsin, and the WisconsinMaritimeMuseum inManitowoc, Wisconsin.

In addition to the above listed items, all other assets of Walter's estate were liquidated for a total amount of $1,500,000 cash. Allowable deductions, excluding charitable donations, against his gross estate amounted to $235,000. All calculations of estate tax should use the rates and unified credit set forth in the text.

Prepare a schedule to determine who will receive a general legacy from Walter's estate and the amount of each legacy.

a. My entire collection of Navajo rugs and Acoma pottery (fair value at date of death is $120,000) is to be given to the Museum of Northern New Mexico, a charitable organization.

b. My residence (fair value at date of death is $550,000) is to be given to my younger brother Thomas along with $2,500,000 from my brokerage account at Wachovia Securities (fair value at date of death is $2,200,000).

c. My brokerage account at Schmidt Investment Services (fair value at date of death is $900,000) is to be liquidated with $500,000 going to each of my two sisters.

d. My collection of antique pistols (fair value at date of death is $85,000) is to be given to my son-in-law Eric Jacobsen.

e. My hunting land in Buffalo County, Wisconsin (fair value at date of death is $750,000), is to be sold and my uncle is to receive $700,000 of the proceeds.

f. Of the proceeds from my life insurance policies (fair value at date of death is $250,000), $200,000 is to be given to First Church of Brookfield, a charitable organization.

g. Each of my eight grandchildren is to receive $50,000, and each of my three children is to receive $400,000.

h. The balance of my assets is to be divided equally between the Kohler Arts Center in Kohler, Wisconsin, and the WisconsinMaritimeMuseum inManitowoc, Wisconsin.

In addition to the above listed items, all other assets of Walter's estate were liquidated for a total amount of $1,500,000 cash. Allowable deductions, excluding charitable donations, against his gross estate amounted to $235,000. All calculations of estate tax should use the rates and unified credit set forth in the text.

Prepare a schedule to determine who will receive a general legacy from Walter's estate and the amount of each legacy.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

6

Determination of estate tax. Charles Kamp, a divorced person, died in February of the current year with an estate consisting of assets valued at $7,008,000 and liabilities of $380,000. Charles's will contained the following provisions:

a. Robert Sullivan would serve as executor of the estate and trustee for the Kamp Children Trust.

b. Timberland with a market value of $560,000 would be placed in a charitable remainder trust. The income from the trust would accrue to the benefit of his sister Marsha Kamp Rodriquez. Income would be reduced by the depletion charge associated with the number of board feet of lumber harvested.

c. Securities with a value of $25,000 would be given to the Milwaukee Art Museum, recognized as a charitable organization.

d. Securities with a value of $600,000 would be given to his married daughter, Maria Kamp Wilson.

e. Each of his three best hunting friends would be paid $180,000 from the proceeds of the sale of Charles's investment in hunting land in Alaska. The hunting land was valued at $475,000 and subsequently sold for $480,000.

f. His long-time friend Ernest Kampmeyer would be given $3,940,000.

g. Proceeds from the life insurance policy with a death benefit of $1,200,000 would be placed in a trust for the benefit of Charles's two minor children.

Administrative and funeral expenses associated with Charles's estate totaled $30,000. Charles's income tax returns for the year of death reported unpaid federal and state income taxes of $13,000.

1. Assuming the unified transfer tax rates and unified credit as set forth in the text, determine the amount of estate tax due on Charles Kamp's estate.

2. Prepare a schedule showing the amounts and recipients of general legacies.

a. Robert Sullivan would serve as executor of the estate and trustee for the Kamp Children Trust.

b. Timberland with a market value of $560,000 would be placed in a charitable remainder trust. The income from the trust would accrue to the benefit of his sister Marsha Kamp Rodriquez. Income would be reduced by the depletion charge associated with the number of board feet of lumber harvested.

c. Securities with a value of $25,000 would be given to the Milwaukee Art Museum, recognized as a charitable organization.

d. Securities with a value of $600,000 would be given to his married daughter, Maria Kamp Wilson.

e. Each of his three best hunting friends would be paid $180,000 from the proceeds of the sale of Charles's investment in hunting land in Alaska. The hunting land was valued at $475,000 and subsequently sold for $480,000.

f. His long-time friend Ernest Kampmeyer would be given $3,940,000.

g. Proceeds from the life insurance policy with a death benefit of $1,200,000 would be placed in a trust for the benefit of Charles's two minor children.

Administrative and funeral expenses associated with Charles's estate totaled $30,000. Charles's income tax returns for the year of death reported unpaid federal and state income taxes of $13,000.

1. Assuming the unified transfer tax rates and unified credit as set forth in the text, determine the amount of estate tax due on Charles Kamp's estate.

2. Prepare a schedule showing the amounts and recipients of general legacies.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

7

Calculation of gift and estate tax. Early in 2011, Nancy Fable was diagnosed with a terminal illness, and doctors gave her one more year to live. Aside from a 2010 $1,000,000 gift to the University of Georgia, she had not done any other gifting prior to 2011. She made the following gifts during 2011:

Early in 2012, she made gifts of $25,000 each to her sister, three nieces, and a nephew. In the spring of 2012, Nancy passed away, leaving an estate consisting of the following at her date of death:

a. One thousand shares of Google stock valued at $900 per share.

b. Real estate inMacon County, Georgia, valued at $3,250,000.

c. Household effects valued at $21,000.

d. Bank accounts totaling $780,000 and gold coins valued at $310,000.

e. Loan against the Macon County real estate consisting of $300,000 plus accrued interest of $7,200.

Funeral and other estate administrative expenses totaled $45,000. Property taxes of $4,000 on the real estate and income taxes of $27,000 were paid by the personal representative. In addition to the above insurance policy, Medcap Manufacturing owned an insurance policy on Nancy's life that had a death benefit of $150,000.

Subsequent to Nancy's death, but within the 6-month alternative valuation date, the following occurred:

a. Two months after Nancy's death, theMacon County land was sold for $3,050,000, and the principal amount of the real estate loan was paid off along with revised accrued interest of $8,300.

b. Three months after Nancy's death, the gold market began to collapse, and the coins were sold for $250,000.

c. ExxonMobil stock was discovered. The stock had a value of $22,000 at Nancy's date of death and was subsequently sold for $23,000.

d. The bubble burst and four months after Nancy's death, the Google stock was sold for $780 per share.

e. The household effects were distributed to family and friends and are excluded from estate assets.

f. All remaining cash, including $21,000 of interest since Nancy's date of death, was distributed as follows: one-third to immediate family and the balance to the University of Georgia to endow a chaired professorship in the Theatre Department. Determine the total amount to be paid for both estate and gift taxes over the 3-year period of 2010 through 2012 by year.

Early in 2012, she made gifts of $25,000 each to her sister, three nieces, and a nephew. In the spring of 2012, Nancy passed away, leaving an estate consisting of the following at her date of death:

a. One thousand shares of Google stock valued at $900 per share.

b. Real estate inMacon County, Georgia, valued at $3,250,000.

c. Household effects valued at $21,000.

d. Bank accounts totaling $780,000 and gold coins valued at $310,000.

e. Loan against the Macon County real estate consisting of $300,000 plus accrued interest of $7,200.

Funeral and other estate administrative expenses totaled $45,000. Property taxes of $4,000 on the real estate and income taxes of $27,000 were paid by the personal representative. In addition to the above insurance policy, Medcap Manufacturing owned an insurance policy on Nancy's life that had a death benefit of $150,000.

Subsequent to Nancy's death, but within the 6-month alternative valuation date, the following occurred:

a. Two months after Nancy's death, theMacon County land was sold for $3,050,000, and the principal amount of the real estate loan was paid off along with revised accrued interest of $8,300.

b. Three months after Nancy's death, the gold market began to collapse, and the coins were sold for $250,000.

c. ExxonMobil stock was discovered. The stock had a value of $22,000 at Nancy's date of death and was subsequently sold for $23,000.

d. The bubble burst and four months after Nancy's death, the Google stock was sold for $780 per share.

e. The household effects were distributed to family and friends and are excluded from estate assets.

f. All remaining cash, including $21,000 of interest since Nancy's date of death, was distributed as follows: one-third to immediate family and the balance to the University of Georgia to endow a chaired professorship in the Theatre Department. Determine the total amount to be paid for both estate and gift taxes over the 3-year period of 2010 through 2012 by year.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

8

Strategies to minimize estate taxes. Edith Leppert and her husband, Gerald Leppert, have net assets with market values of $4,300,000 and $2,400,000, respectively. The Lepperts have begun to do some estate tax planning and are developing various strategies based on the following assumptions:

a. Due to preexisting health conditions, it is assumed that Edith will precede her husband in death and Gerald will survive Edith by three years.

b. Gerald's net assets, including those assets received upon Edith's death, are expected to appreciate at an annual compound rate of 5% per year.

c. Administrative and funeral expenses are estimated to be $25,000 per person.

d. Both Edith and Gerald have each earmarked $150,000 of their net assets to be donated to charitable organizations.

Based on the above information, determine the amount of estate tax that both Edith and Gerald Leppert would be exposed to given: (1) that no trusts were established and (2) that a credit shelter trust is created by each person for the benefit of their children in the amount of $3,500,000. Unified transfer tax rates and the unified credit as set forth in the text should be used.

a. Due to preexisting health conditions, it is assumed that Edith will precede her husband in death and Gerald will survive Edith by three years.

b. Gerald's net assets, including those assets received upon Edith's death, are expected to appreciate at an annual compound rate of 5% per year.

c. Administrative and funeral expenses are estimated to be $25,000 per person.

d. Both Edith and Gerald have each earmarked $150,000 of their net assets to be donated to charitable organizations.

Based on the above information, determine the amount of estate tax that both Edith and Gerald Leppert would be exposed to given: (1) that no trusts were established and (2) that a credit shelter trust is created by each person for the benefit of their children in the amount of $3,500,000. Unified transfer tax rates and the unified credit as set forth in the text should be used.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

9

Preparation of a charge and discharge statement. Eleanor Matsun died on June 1 of the current year, leaving a valid will with JamesMadison being named as her personal representative. All of the following occurred in the year of her death:

a. The personal representative prepared the following inventory of assets at fair market value as of the date of death:.

b. Subsequent to filing the above inventory with the court, the personal representative discovered the decedent's gold coin collection valued at $18,000.

c. On June 20, $2,500 was received from Pal Corporation for dividends declared onMay 10 to shareholders of record on May 31.

d. On July 7, the time share condominium was sold for $30,000.

e. The following items were paid during the period from June 2 through July 31:

f. On July 5, a check for $15,000 was received for the decedent's portion of Matsun Limo Service income earned during the quarter ended June 30. Income is assumed to be earned evenly over the quarter.

g. The decedent's partner in the limo service offered the personal representative $65,000 for the decedent's interest in the partnership. After much negotiation, the interest was sold for $80,000.

h. In mid-September, the decedent's personal residence was sold for $162,000, net of brokerage and closing costs totaling $15,000. The outstanding mortgage and accrued interest were promptly paid in the amount of $82,800. At the date of death, the mortgage balance along with accrued interest was $81,100.

i. On October 1, a check was received for interest on the RTC bonds.

j. On November 5, the decedent's income tax return for the year of death was filed and $6,400 of additional taxes was sent in with the return.

Prepare a charge and discharge statement as of December 31 of the current year.

a. The personal representative prepared the following inventory of assets at fair market value as of the date of death:.

b. Subsequent to filing the above inventory with the court, the personal representative discovered the decedent's gold coin collection valued at $18,000.

c. On June 20, $2,500 was received from Pal Corporation for dividends declared onMay 10 to shareholders of record on May 31.

d. On July 7, the time share condominium was sold for $30,000.

e. The following items were paid during the period from June 2 through July 31:

f. On July 5, a check for $15,000 was received for the decedent's portion of Matsun Limo Service income earned during the quarter ended June 30. Income is assumed to be earned evenly over the quarter.

g. The decedent's partner in the limo service offered the personal representative $65,000 for the decedent's interest in the partnership. After much negotiation, the interest was sold for $80,000.

h. In mid-September, the decedent's personal residence was sold for $162,000, net of brokerage and closing costs totaling $15,000. The outstanding mortgage and accrued interest were promptly paid in the amount of $82,800. At the date of death, the mortgage balance along with accrued interest was $81,100.

i. On October 1, a check was received for interest on the RTC bonds.

j. On November 5, the decedent's income tax return for the year of death was filed and $6,400 of additional taxes was sent in with the return.

Prepare a charge and discharge statement as of December 31 of the current year.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

10

Analysis of trust activity. Jack Mason is a single parent with three minor children. His will provides for the creation of a trust for the benefit of his three children. His entire net estate is to be placed into the trust, and the trustee is authorized to approve disbursements to the children until they reach the age of 25. Upon reaching the age of 25, each child is to receive their proportionate share of the trust principal and income. For example, the first child to reach age 25 will receive one-third of the trust principal and income. The next child to reach age 25 will receive one-half of the trust principal and income at that time. The following facts relate to the trust between the time of Mason's death and the first child's 25th birthday.

a. The following assets were transferred to the trust after the settlement of Jack Mason's estate: Cash, $100,000; stock in IBM, $150,000; investment in real estate partnership, $400,000; and forest land, $200,000.

b. Subsequent to Mason's death, an investment in a limited partnership was discovered. The investment was valued at $40,000.

c. One-half of the investment in the real estate partnership was sold for $220,000.

d. Dividends on the IBM stock were received in the amount of $20,000. The dividend was declared prior to Mason's death.

e. All cash balances were invested in a short-term interest-bearing account, and the trust received $5,000 in interest.

f. The trustee for the benefit of the children approved disbursements in the amount of $32,000. Disbursements are first considered to be a distribution of available trust income and then as a distribution of trust principal.

g. Trustee's fees in the amount of $10,000 were paid. All such fees are to be allocated equally between principal and income.

h. Eight percent bonds with a face value of $80,000 were purchased for $84,000. The bonds have a remaining life of five years, and any premium is to be amortized.

i. Income from the harvest of timber in the amount of $22,000 was received. The trust document calls for a charge against income for depletion. Depletion is calculated based on a unitsof- output method that is based on board feet of timber harvested. Approximately 11% of the total board feet is represented by this harvest. The land is expected to have a residual value of $60,000 after removal of the timber.

j. Real estate taxes on the land in the amount of $6,000 were paid. Such taxes are considered a component of trust income.

k. The real estate partnership made a distribution of income in the amount of $22,000 to the trust.

l. A semiannual interest payment on the bonds was received by the trust.

m. The trustee paid $6,000 of taxes on trust income.

n. IBM stock with a basis of $60,000 was sold for $80,100.

Prepare a schedule to determine the amount of trust principal to be received by the first child to reach the age of 25. The schedule should show the cash balance available at any point in time.

a. The following assets were transferred to the trust after the settlement of Jack Mason's estate: Cash, $100,000; stock in IBM, $150,000; investment in real estate partnership, $400,000; and forest land, $200,000.

b. Subsequent to Mason's death, an investment in a limited partnership was discovered. The investment was valued at $40,000.

c. One-half of the investment in the real estate partnership was sold for $220,000.

d. Dividends on the IBM stock were received in the amount of $20,000. The dividend was declared prior to Mason's death.

e. All cash balances were invested in a short-term interest-bearing account, and the trust received $5,000 in interest.

f. The trustee for the benefit of the children approved disbursements in the amount of $32,000. Disbursements are first considered to be a distribution of available trust income and then as a distribution of trust principal.

g. Trustee's fees in the amount of $10,000 were paid. All such fees are to be allocated equally between principal and income.

h. Eight percent bonds with a face value of $80,000 were purchased for $84,000. The bonds have a remaining life of five years, and any premium is to be amortized.

i. Income from the harvest of timber in the amount of $22,000 was received. The trust document calls for a charge against income for depletion. Depletion is calculated based on a unitsof- output method that is based on board feet of timber harvested. Approximately 11% of the total board feet is represented by this harvest. The land is expected to have a residual value of $60,000 after removal of the timber.

j. Real estate taxes on the land in the amount of $6,000 were paid. Such taxes are considered a component of trust income.

k. The real estate partnership made a distribution of income in the amount of $22,000 to the trust.

l. A semiannual interest payment on the bonds was received by the trust.

m. The trustee paid $6,000 of taxes on trust income.

n. IBM stock with a basis of $60,000 was sold for $80,100.

Prepare a schedule to determine the amount of trust principal to be received by the first child to reach the age of 25. The schedule should show the cash balance available at any point in time.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

11

Allocating legacies. Calvin Hughes's will provided for the following distributions:

a. The 40-acre parcel in Leona, Wisconsin, is to be given to The Nature Conservancy along with $50,000.

b. My 1970 GTO Pontiac convertible along with my 1937 Chevrolet pickup truck are to be given to the ''Piston Auto Club'' located in Slinger, Wisconsin.

c. The collection of Zuni Kachina dolls is to be given to my nephew William Hughes.

d. My Northwestern Mutual insurance policy number 14378 has named my son Calvin, Jr., as beneficiary. Policy number 48002 has named the estate as beneficiary. However, I want my sister Roberta and my brother Roger to each receive $30,000 from the policy proceeds.

e. My residence at 110 Hillcrest Road is to be given to the Riveredge Nature Center located in Newburg, Wisconsin, provided that the center has not already grown to include more than 500 acres.

f. My grandchildren, Riley, Corey and Toby, are to receive $50,000 each for the purpose of hopefully funding their college education. This bequest is not contingent upon their going to college or having already finished college.

g. The balance of my estate is to be divided equally between my son Calvin, Jr., and my daughter, Susan.

Determine the amount of cash to be received by the decedent's grandchild Riley and his son Calvin Hughes, Jr., under each of the following scenarios:

Scenario A: The following additional information is available at the date of death: the estate only consisted of $40,000 cash, William Hughes was deceased, the Kachina collection was sold for $45,000, insurance policy number 14378 had a death benefit of $50,000, insurance policy number 48002 had a death benefit of $40,000, Riveredge Nature Center consisted of 560 acres, and the residence at 110 Hillcrest Road was sold for $220,000.

Scenario B: The following additional information is available at the date of death: the estate only consisted of $15,000 cash, William Hughes was thrilled to receive the Kachina collection which was valued at $45,000, insurance policy number 14378 had a death benefit of $50,000, insurance policy number 48002 had a death benefit of $40,000, Riveredge Nature Center consisted of 160 acres, and the residence at 110 Hillcrest Road was sold for $220,000.

a. The 40-acre parcel in Leona, Wisconsin, is to be given to The Nature Conservancy along with $50,000.

b. My 1970 GTO Pontiac convertible along with my 1937 Chevrolet pickup truck are to be given to the ''Piston Auto Club'' located in Slinger, Wisconsin.

c. The collection of Zuni Kachina dolls is to be given to my nephew William Hughes.

d. My Northwestern Mutual insurance policy number 14378 has named my son Calvin, Jr., as beneficiary. Policy number 48002 has named the estate as beneficiary. However, I want my sister Roberta and my brother Roger to each receive $30,000 from the policy proceeds.

e. My residence at 110 Hillcrest Road is to be given to the Riveredge Nature Center located in Newburg, Wisconsin, provided that the center has not already grown to include more than 500 acres.

f. My grandchildren, Riley, Corey and Toby, are to receive $50,000 each for the purpose of hopefully funding their college education. This bequest is not contingent upon their going to college or having already finished college.

g. The balance of my estate is to be divided equally between my son Calvin, Jr., and my daughter, Susan.

Determine the amount of cash to be received by the decedent's grandchild Riley and his son Calvin Hughes, Jr., under each of the following scenarios:

Scenario A: The following additional information is available at the date of death: the estate only consisted of $40,000 cash, William Hughes was deceased, the Kachina collection was sold for $45,000, insurance policy number 14378 had a death benefit of $50,000, insurance policy number 48002 had a death benefit of $40,000, Riveredge Nature Center consisted of 560 acres, and the residence at 110 Hillcrest Road was sold for $220,000.

Scenario B: The following additional information is available at the date of death: the estate only consisted of $15,000 cash, William Hughes was thrilled to receive the Kachina collection which was valued at $45,000, insurance policy number 14378 had a death benefit of $50,000, insurance policy number 48002 had a death benefit of $40,000, Riveredge Nature Center consisted of 160 acres, and the residence at 110 Hillcrest Road was sold for $220,000.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

12

Recording estate principal and income. Laurel Rose has been the personal representative of her brother's estate since his death on February 1, 2016. The following events occurred during her administration:

1. Included in the principal assets were 40, $1,000, 8% city of Pittsburgh bonds paying interest on January 1 and July 1. The bonds had a fair value of 101 on February 1, 2016. Laurel sold the bonds at 103, plus accrued interest, onMarch 1, 2016.

2. On March 1, 2016, Laurel purchased 50, $1,000, 5% city of Detroit bonds at 98, plus accrued interest. The bonds pay interest on April 1 and October 1. The bonds mature on April 1, 2018.

3. On March 1, 2016, she also purchased $10,000 (face value), 7% city of Newark bonds at 102 plus accrued interest. The bonds pay interest on June 1 and December 1. The bonds mature on December 1, 2017.

4. On April 1, 2016, she received a check for the interest on the Detroit bonds.

5. On June 1, 2016, she received a check for the interest on the Newark bonds.

6. On September 1, 2016, she sold the Detroit bonds at 101, plus accrued interest.

Prepare journal entries to record each of these events. Use the straight-line method of amortization where applicable.

1. Included in the principal assets were 40, $1,000, 8% city of Pittsburgh bonds paying interest on January 1 and July 1. The bonds had a fair value of 101 on February 1, 2016. Laurel sold the bonds at 103, plus accrued interest, onMarch 1, 2016.

2. On March 1, 2016, Laurel purchased 50, $1,000, 5% city of Detroit bonds at 98, plus accrued interest. The bonds pay interest on April 1 and October 1. The bonds mature on April 1, 2018.

3. On March 1, 2016, she also purchased $10,000 (face value), 7% city of Newark bonds at 102 plus accrued interest. The bonds pay interest on June 1 and December 1. The bonds mature on December 1, 2017.

4. On April 1, 2016, she received a check for the interest on the Detroit bonds.

5. On June 1, 2016, she received a check for the interest on the Newark bonds.

6. On September 1, 2016, she sold the Detroit bonds at 101, plus accrued interest.

Prepare journal entries to record each of these events. Use the straight-line method of amortization where applicable.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

13

Strategies to minimize estate tax. James and SusanWagner have assets with fair market values of $5,700,000 and $1,800,000, respectively. James has been diagnosed with a terminal illness and is expected to pass away within the current year 2015. James wants to minimize his estate taxes, and any appropriate planning should consider the following factors:

a. JamesWagner has debts of $210,000 against the assets in his estate.

b. It is estimated that administrative and funeral expenses will be $25,000 each for James and Susan.

c. It is estimated that Susan would be able to live comfortably for the balance of her life if she had an estate of $3,000,000 at the time of her husband's death. Susan will make charitable contributions to the extent that her estate exceeds $3,000,000 as a result of her husband's death.

d. Assume that Susan will live for three years after the death of her husband.

e. It is anticipated that at the time of Susan's death her estate would have appreciated by $150,000 per year for years 2015 through 2017.

f. Neither James nor Susan has made any gifts during the current year 2015.

g. The couple has two children and three grandchildren. One of the grandchildren is attending the University of Wisconsin and is expected to graduate in 2017. Annual tuition costs are $10,000 per year.

h. James has agreed to make a $200,000 charitable contribution to the Sierra Club out of his estate.

i. If any trusts are created, the income from the trust will benefit the surviving spouse, and any corpus will ultimately pass to the children.

Develop an estate plan for the Wagners that would minimize estate taxes and incorporate the above factors. The unified transfer tax rates and exclusion amounts set forth in the text should be used. Assume that annual nontaxable gifts up to $13,000 per donor will be made to all children and grandchildren to whatever extent possible.

a. JamesWagner has debts of $210,000 against the assets in his estate.

b. It is estimated that administrative and funeral expenses will be $25,000 each for James and Susan.

c. It is estimated that Susan would be able to live comfortably for the balance of her life if she had an estate of $3,000,000 at the time of her husband's death. Susan will make charitable contributions to the extent that her estate exceeds $3,000,000 as a result of her husband's death.

d. Assume that Susan will live for three years after the death of her husband.

e. It is anticipated that at the time of Susan's death her estate would have appreciated by $150,000 per year for years 2015 through 2017.

f. Neither James nor Susan has made any gifts during the current year 2015.

g. The couple has two children and three grandchildren. One of the grandchildren is attending the University of Wisconsin and is expected to graduate in 2017. Annual tuition costs are $10,000 per year.

h. James has agreed to make a $200,000 charitable contribution to the Sierra Club out of his estate.

i. If any trusts are created, the income from the trust will benefit the surviving spouse, and any corpus will ultimately pass to the children.

Develop an estate plan for the Wagners that would minimize estate taxes and incorporate the above factors. The unified transfer tax rates and exclusion amounts set forth in the text should be used. Assume that annual nontaxable gifts up to $13,000 per donor will be made to all children and grandchildren to whatever extent possible.

Unlock Deck

Unlock for access to all 19 flashcards in this deck.

Unlock Deck

k this deck

14

Accounting for estate principal and income. Jason Jackson was killed in a mountain-climbing accident in British Columbia. As Jason's trusted friend and CPA, you have been named executor of his estate and guardian to his minor child, Cody Jackson. Jason's estate consists of the following assets subject to probate:

Prepare journal entries to record the above inventory and the following events related to the estate principal and income:

1. Final medical and funeral expenses of $22,000 are paid.

2. An individual retirement account (IRA) naming Jackson's estate as beneficiary and having a value of $37,000 subsequently is discovered.

3. Cash dividends of $1,000 on the GTE stock and $2,700 on theMerkt stock are received.

4. The vacant land in Colorado is sold for $150,000 less accrued property taxes of $2,000 and a broker's commission of $8,000.

5. Interest of $2,400 is received on the Trident bond fund, and the royalty receivable is also collected.

6. Income taxes of $4,000 on the decedent's final tax return are paid, along with $24,000 of other claims against the estate.

7. A legacy of $15,000 is paid to the High Adventure Climbing School.

8. Administrative expenses of $3,200 are paid, of which $100 is traceable to income.