Deck 23: Debt Restructuring, Corporate Reorganizations, and Liquidations

Full screen (f)

Question

Question

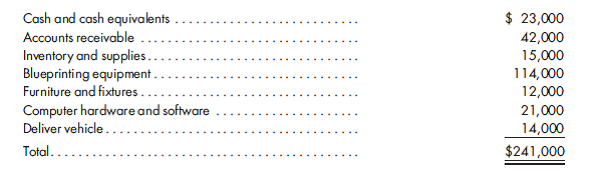

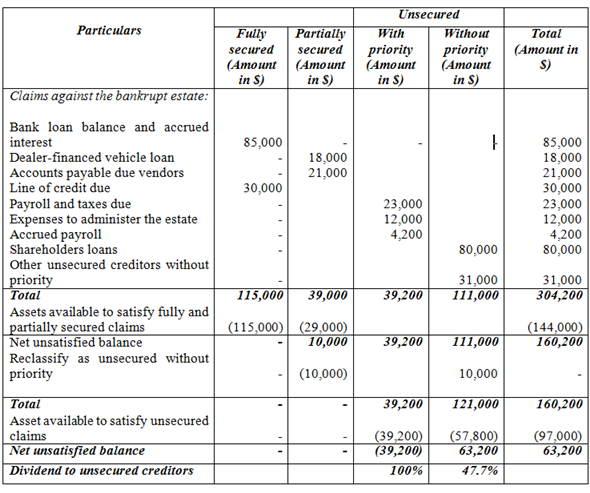

Amounts to be received by creditors under Chapter 7. Casper Blueprinting, Inc., has filed under Chapter 7 of the Bankruptcy Code. The estimated net realizable value of its assets is as follows:

Creditors' claims are summarized as follows:

a. Bank loan balance of $82,000 plus accrued interest of $3,000 with a first lien against blueprinting equipment.

b. Dealer-financed vehicle loan with an outstanding balance of $18,000, which is secured by the delivery vehicle.

c. Accounts payable due vendors in the amount of $21,000 and secured by the inventory and supplies.

d. A line of credit balance due of $30,000 secured by the accounts receivable.

e. Unpaid payroll and income taxes of $23,000.

f. Accounting and legal fees due in the amount of $12,000 in connection with the administration of the bankrupt estate.

g. Unpaid wages to employees totaling $4,200 ($700 represents the largest amount due any one employee).

h. Loans due shareholders of the corporation totaling $80,000.

i. Other unsecured creditors without priority in the amount of $31,000.

Prepare a schedule to show the estimated amount to be received by each major category of creditor.

Creditors' claims are summarized as follows:

a. Bank loan balance of $82,000 plus accrued interest of $3,000 with a first lien against blueprinting equipment.

b. Dealer-financed vehicle loan with an outstanding balance of $18,000, which is secured by the delivery vehicle.

c. Accounts payable due vendors in the amount of $21,000 and secured by the inventory and supplies.

d. A line of credit balance due of $30,000 secured by the accounts receivable.

e. Unpaid payroll and income taxes of $23,000.

f. Accounting and legal fees due in the amount of $12,000 in connection with the administration of the bankrupt estate.

g. Unpaid wages to employees totaling $4,200 ($700 represents the largest amount due any one employee).

h. Loans due shareholders of the corporation totaling $80,000.

i. Other unsecured creditors without priority in the amount of $31,000.

Prepare a schedule to show the estimated amount to be received by each major category of creditor.

Question

Question

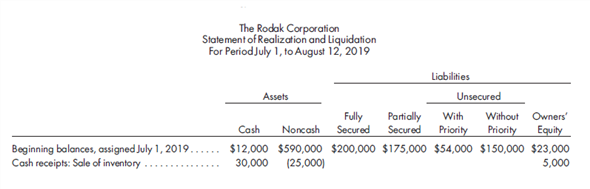

Statement of realization and liquidation, dividend to unsecured creditors without priority. A partially completed statement of realization and liquidation is as follows:

The following additional transactions have occurred through August 12, 2019:

a. Receivables collected amounted to $39,000. Receivables with a book value of $15,000 that were not allowed for were written off.

b. A $12,000 loan that was fully secured was paid off.

c. A valid claim was received from a leasing company seeking payment of $15,000 for equipment rentals.

d. Securities costing $18,000 were sold for $23,000, minus a brokerage fee of $500.

e. Depreciation on machinery was $3,200.

f. Payments on accounts payable totaled $25,000, of which the entire amount was secured by the inventory sold.

g. Machinery that originally cost $85,000 and had a book value of $45,000 sold for $36,000.

h. Proceeds from the sale of machinery in (g) were remitted to the bank, which holds a $50,000 loan on the machinery.

1. Update the statement of realization and liquidation to properly reflect transactions (a) through (h).

2. Assuming the remaining noncash assets can be realized for $410,000, determine the estimated dividend to be received by unsecured creditors without priority.

The following additional transactions have occurred through August 12, 2019:

a. Receivables collected amounted to $39,000. Receivables with a book value of $15,000 that were not allowed for were written off.

b. A $12,000 loan that was fully secured was paid off.

c. A valid claim was received from a leasing company seeking payment of $15,000 for equipment rentals.

d. Securities costing $18,000 were sold for $23,000, minus a brokerage fee of $500.

e. Depreciation on machinery was $3,200.

f. Payments on accounts payable totaled $25,000, of which the entire amount was secured by the inventory sold.

g. Machinery that originally cost $85,000 and had a book value of $45,000 sold for $36,000.

h. Proceeds from the sale of machinery in (g) were remitted to the bank, which holds a $50,000 loan on the machinery.

1. Update the statement of realization and liquidation to properly reflect transactions (a) through (h).

2. Assuming the remaining noncash assets can be realized for $410,000, determine the estimated dividend to be received by unsecured creditors without priority.

Question

Question

Question

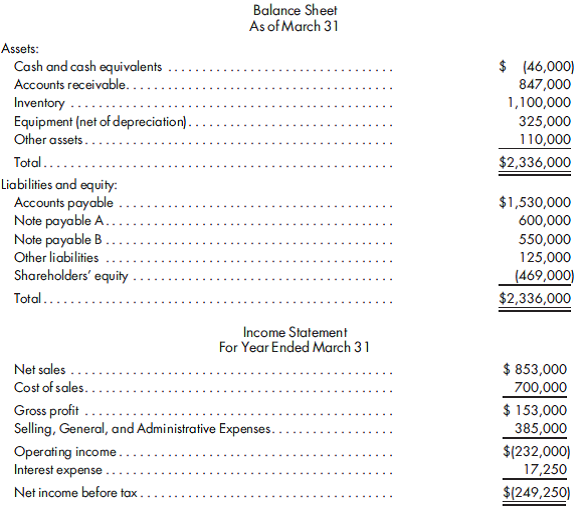

Effect of a quasi-reorganization. Marshall Tool and Die Company has been experiencing significant foreign competition and a declining market. Annual net losses from operations have averaged $250,000 over the last three years. The company's balance sheet as of December 31, 2017, is as follows:

After analyzing accounts receivable and inventory, it has been determined that the allowance for uncollectibles should be increased by $75,000 and the inventory should be written down by $20,000. Based on recent appraisals, it is estimated that the plant and equipment have a market value of $1,285,000. The goodwill is traceable to the purchase of a small tooling company in 2013. Based on an analysis of cash flows associated with that acquisition, it is estimated that the goodwill has an impaired value of $0. Other assets represent a note receivable from officers of the corporation. The note calls for five annual payments of $8,309 including interest at the rate of 6%.

In response to the current situation, the company has decided to take the following actions:

a. Record the suggested impairment in all assets.

b. Restructure the note receivable from the officers to reflect four annual payments and an interest rate of 7.5%.

c. Restructure the note payable, which was due in 2019, to provide for 12 semiannual payments of $120,000 including interest at the annual rate of 6%.

d. Engage in a quasi-reorganization to eliminate the deficit in retained earnings.

1. Prepare a revised classified balance sheet to reflect the effect of management's actions.

2. Compute the following ratios before and after management's actions: current ratio and debt-to-equity ratio.

3. Given the above ratio analysis, if the ratios do not suggest an improvement, discuss the benefits of management's actions.

After analyzing accounts receivable and inventory, it has been determined that the allowance for uncollectibles should be increased by $75,000 and the inventory should be written down by $20,000. Based on recent appraisals, it is estimated that the plant and equipment have a market value of $1,285,000. The goodwill is traceable to the purchase of a small tooling company in 2013. Based on an analysis of cash flows associated with that acquisition, it is estimated that the goodwill has an impaired value of $0. Other assets represent a note receivable from officers of the corporation. The note calls for five annual payments of $8,309 including interest at the rate of 6%.

In response to the current situation, the company has decided to take the following actions:

a. Record the suggested impairment in all assets.

b. Restructure the note receivable from the officers to reflect four annual payments and an interest rate of 7.5%.

c. Restructure the note payable, which was due in 2019, to provide for 12 semiannual payments of $120,000 including interest at the annual rate of 6%.

d. Engage in a quasi-reorganization to eliminate the deficit in retained earnings.

1. Prepare a revised classified balance sheet to reflect the effect of management's actions.

2. Compute the following ratios before and after management's actions: current ratio and debt-to-equity ratio.

3. Given the above ratio analysis, if the ratios do not suggest an improvement, discuss the benefits of management's actions.

Question

Question

Troubled debt restructurings, impact on earnings. Ridgeway Builders, Inc., is in the residential construction industry and has been experiencing a business downturn. As a result of these economic conditions, the company is having difficulty serving its outstanding debt and is seeking relief outside of the bankruptcy courts. The following summarizes outstanding debt and management's proposed restructuring:

Question

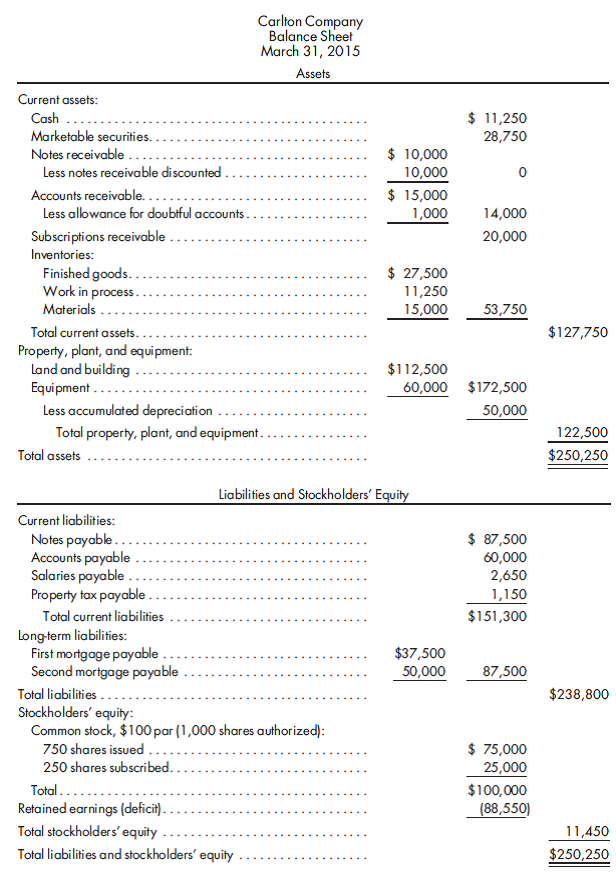

Statement of affairs. A creditor's committee of Carlton Company has obtained the March 31, 2015, balance sheet shown below.

An analysis of the company's accounts disclosed the following activities through April 30, 2015:

a. Carlton Company started business on April 1, 2010, with authorized stock of $100 par. Of the 1,000 authorized shares, 750 were paid for in full at par, and 250 were subscribed at par, with a required 20% down payment and the balance payable upon call. All the subscriptions receivable are due fromW. Krueger, president of the company, and are fully collectible.

b. Marketable securities include the $25,000 cost of U.S. Treasury bonds valued at $23,200 and 25 shares of Groves Company common stock, costing $3,750, with a fair value of $3,300.

c. The land originally cost $10,000, and the building was erected at a cost of $102,500. Of the accumulated depreciation, $30,000 is applicable to the building. The realizable value of the real estate is $75,000.

d. Notes receivable were endorsed with recourse when discounted and are expected to be dishonored. Of the accounts receivable, $3,000 are considered collectible.

e. Inventories are shown at cost. Any finished goods are expected to yield 110% of cost. If scrapped, goods in process have a realizable value of only $2,200. It is estimated, however, that the work in process can be completed by the addition of $3,000 of present materials and an expenditure of $3,500 for labor. The materials deteriorate rapidly and will realize only 20% of cost. (Use the cost completion method illustrated in the text.)

f. Equipment is estimated to have a realizable value of $12,000.

g. Notes payable include a $25,000 note to Aerotex Company and a $62,500 note to B. Williams. Aerotex holds the U.S. Treasury bonds as security for its loans. It also holds the first mortgage of $37,500 on the company's real estate, interest on which is paid throughMarch 31, 2015. The note payable toWilliams is secured by a chattelmortgage on factory equipment. Interest on the note has been paid throughMarch 31, 2015. Williams also holds the secondmortgage on the real estate.

h. Any expenses not specifically mentioned need not be considered. All salaries qualify for priority, including labor to complete the work in process.

Prepare a statement of affairs for Carlton Company.

An analysis of the company's accounts disclosed the following activities through April 30, 2015:

a. Carlton Company started business on April 1, 2010, with authorized stock of $100 par. Of the 1,000 authorized shares, 750 were paid for in full at par, and 250 were subscribed at par, with a required 20% down payment and the balance payable upon call. All the subscriptions receivable are due fromW. Krueger, president of the company, and are fully collectible.

b. Marketable securities include the $25,000 cost of U.S. Treasury bonds valued at $23,200 and 25 shares of Groves Company common stock, costing $3,750, with a fair value of $3,300.

c. The land originally cost $10,000, and the building was erected at a cost of $102,500. Of the accumulated depreciation, $30,000 is applicable to the building. The realizable value of the real estate is $75,000.

d. Notes receivable were endorsed with recourse when discounted and are expected to be dishonored. Of the accounts receivable, $3,000 are considered collectible.

e. Inventories are shown at cost. Any finished goods are expected to yield 110% of cost. If scrapped, goods in process have a realizable value of only $2,200. It is estimated, however, that the work in process can be completed by the addition of $3,000 of present materials and an expenditure of $3,500 for labor. The materials deteriorate rapidly and will realize only 20% of cost. (Use the cost completion method illustrated in the text.)

f. Equipment is estimated to have a realizable value of $12,000.

g. Notes payable include a $25,000 note to Aerotex Company and a $62,500 note to B. Williams. Aerotex holds the U.S. Treasury bonds as security for its loans. It also holds the first mortgage of $37,500 on the company's real estate, interest on which is paid throughMarch 31, 2015. The note payable toWilliams is secured by a chattelmortgage on factory equipment. Interest on the note has been paid throughMarch 31, 2015. Williams also holds the secondmortgage on the real estate.

h. Any expenses not specifically mentioned need not be considered. All salaries qualify for priority, including labor to complete the work in process.

Prepare a statement of affairs for Carlton Company.

Question

Question

Question

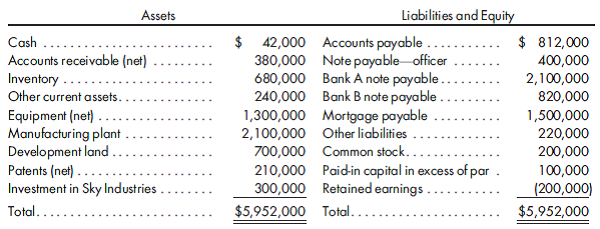

Recording restructuring transactions. St. John Corporation is barely solvent and has been seeking an equity investor that would be interested in making a capital contribution so that the company would hopefully return to performance levels it had experienced in the past. The company's year-end 2015 balance sheet is presented below.

Selected transactions occurring during the first six months of 2016 were as follows:

a. Patents with a fair value of $230,000 were transferred to the officer in partial satisfaction of their note. The remaining balance on the note would be paid over five quarters with the first payment of $35,026.77 due on June 30, 2016.

b. The mortgage payable was restructured with 40 quarterly payments of $51,178.05, beginning on June 30, 2016, in addition to an immediate lump sum payment of $100,000.

c. The bank A note payable was restructured as follows: the development land with a net realizable value of $980,000 was conveyed along with marketable securities having a book value of $80,000 and a market value of $95,000. The balance of the note was to be over 10 quarters with payments of $111,145.03 beginning on June 30, 2016.

d. The bank B note payable was partially secured by equipment which had a book value of $240,000 and a net realizable value of $220,000. The equipment was seized by the bank and the company agreed to settle the balance of the note by making 10 quarterly payments of $55,000 beginning on June 30, 2016.

e. On June 30, 2016 all payments required by item (a) through (d) above were paid.

f. Common shareholders approved a reduction in par value from $10 per share to $5 per share and the deficit was eliminated.

Prepare all necessary entries to record the above transactions (a) through (f ).

Selected transactions occurring during the first six months of 2016 were as follows:

a. Patents with a fair value of $230,000 were transferred to the officer in partial satisfaction of their note. The remaining balance on the note would be paid over five quarters with the first payment of $35,026.77 due on June 30, 2016.

b. The mortgage payable was restructured with 40 quarterly payments of $51,178.05, beginning on June 30, 2016, in addition to an immediate lump sum payment of $100,000.

c. The bank A note payable was restructured as follows: the development land with a net realizable value of $980,000 was conveyed along with marketable securities having a book value of $80,000 and a market value of $95,000. The balance of the note was to be over 10 quarters with payments of $111,145.03 beginning on June 30, 2016.

d. The bank B note payable was partially secured by equipment which had a book value of $240,000 and a net realizable value of $220,000. The equipment was seized by the bank and the company agreed to settle the balance of the note by making 10 quarterly payments of $55,000 beginning on June 30, 2016.

e. On June 30, 2016 all payments required by item (a) through (d) above were paid.

f. Common shareholders approved a reduction in par value from $10 per share to $5 per share and the deficit was eliminated.

Prepare all necessary entries to record the above transactions (a) through (f ).

Question

Question

Question

Question

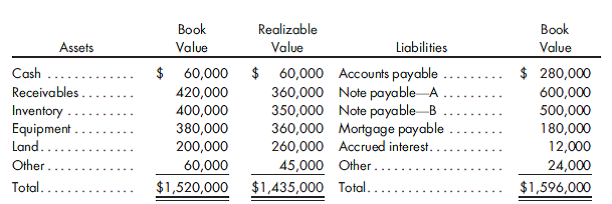

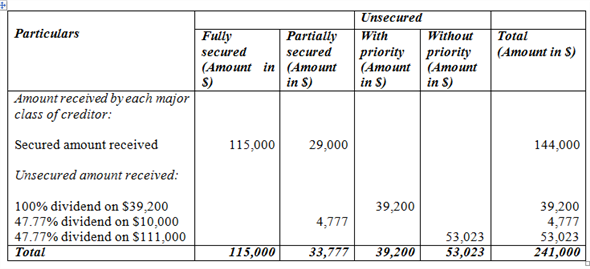

Determining proceeds to various classes of claims. Tebon Manufacturing is considering seeking relief under Chapter 7 of the Bankruptcy Code. However, the company would prefer to engage in out-of-court activities that would allow for a restructuring of debts in an orderly manner. Before approaching its creditors, the company is attempting to estimate the amount of consideration that would be received by various classes of creditors if the company did liquidate. The company's assets and liabilities are as follows:

Of the accounts payable, $130,000 is secured by inventory which has a net realizable value of $150,000. Note A is secured by the balance of the inventory and receivables. Note B is secured by equipment with a net realizable value of $300,000, and the mortgage payable and accrued interest are secured by the land. All of the other liabilities are unsecured, although $10,000 is unsecured with priority over the balance.

Prepare a schedule that sets forth the classes of claims (fully secured, partially secured, unsecured) and the assets that satisfy each class. For each class, compute the dividend and determine the total amount of consideration to be received in satisfaction of Note Payable-B.

Of the accounts payable, $130,000 is secured by inventory which has a net realizable value of $150,000. Note A is secured by the balance of the inventory and receivables. Note B is secured by equipment with a net realizable value of $300,000, and the mortgage payable and accrued interest are secured by the land. All of the other liabilities are unsecured, although $10,000 is unsecured with priority over the balance.

Prepare a schedule that sets forth the classes of claims (fully secured, partially secured, unsecured) and the assets that satisfy each class. For each class, compute the dividend and determine the total amount of consideration to be received in satisfaction of Note Payable-B.

Question

Restructuring versus liquidation. Atoyo Fabricating, Inc., has not been able to service its debts adequately. The company is a family business that has been in existence for 35 years. The shareholders want to avoid liquidating the business and are seeking your help in formulating a plan of reorganization which:

a. Provides creditors with at least as much consideration as, if not more than, they would receive if the company were liquidated.

b. Does not require monthly debt service in excess of $75,000.

Information regarding the various creditor claims and possible restructuring parameters is as follows:

a. Accounts payable due vendors total $134,000. Terms are generally 2/10 net 30, and virtually all accounts are past due. Vendors with balances of $40,000 due have indicated that in satisfaction of the amount due, they would accept equal monthly installment payments bearing no less than 12% and not exceeding three months in duration. These vendors have secured their claims with inventory that has a book value and net realizable value of $55,000 and $42,000, respectively. Vendors with a balance due of $74,000 have a secured interest in inventory with a book value of $60,000 and a net realizable value of $46,000. These vendors would accept three monthly installment payments of $20,000 including interest at the rate of 12% in satisfaction of the amount due. The remaining payables represent unsecured amounts that would be paid $3,000 per month for the next five months including interest at 12%.

b. The equipment note has a balance due of $320,000 plus accrued interest of $18,000. Equipment with a book value of $280,000 and a net realizable value of $325,000 serves as collateral for this loan. The original loan had an interest rate of 11% and a remaining term of 30 months. The creditor will not agree to a change in the interest rate but will accept a revised term of 36 to 42 months in exchange for a personal guarantee of the amount due by each of the shareholders of record.

c. The note due a shareholder in the amount of $20,000 is secured by the cash surrender value of an insurance policy in the amount of $15,000 and is payable on demand. The shareholder would accept four semiannual payments, including interest at 12%, if the present value of these payments is equal to 120% of what would have been received if the company had been liquidated.

d. The mortgage payable of $420,000 plus accrued interest of $28,000 is fully secured by real estate with a book value of $310,000 and a net realizable value of $460,000. The original mortgage has a remaining term of 334 months and an interest rate of 9%. The mortgage company would agree to a restructuring of 360 months and an interest rate of 11%.

e. All other creditors totaling $160,000 are unsecured without priority. Management would like to propose that these creditors receive monthly payments over the next eight months with interest at 12%. The net present value of these payments should equal 110% of what would have been received had the company been liquidated.

The book values and net realizable values of the company's assets are as follows:

a. Provides creditors with at least as much consideration as, if not more than, they would receive if the company were liquidated.

b. Does not require monthly debt service in excess of $75,000.

Information regarding the various creditor claims and possible restructuring parameters is as follows:

a. Accounts payable due vendors total $134,000. Terms are generally 2/10 net 30, and virtually all accounts are past due. Vendors with balances of $40,000 due have indicated that in satisfaction of the amount due, they would accept equal monthly installment payments bearing no less than 12% and not exceeding three months in duration. These vendors have secured their claims with inventory that has a book value and net realizable value of $55,000 and $42,000, respectively. Vendors with a balance due of $74,000 have a secured interest in inventory with a book value of $60,000 and a net realizable value of $46,000. These vendors would accept three monthly installment payments of $20,000 including interest at the rate of 12% in satisfaction of the amount due. The remaining payables represent unsecured amounts that would be paid $3,000 per month for the next five months including interest at 12%.

b. The equipment note has a balance due of $320,000 plus accrued interest of $18,000. Equipment with a book value of $280,000 and a net realizable value of $325,000 serves as collateral for this loan. The original loan had an interest rate of 11% and a remaining term of 30 months. The creditor will not agree to a change in the interest rate but will accept a revised term of 36 to 42 months in exchange for a personal guarantee of the amount due by each of the shareholders of record.

c. The note due a shareholder in the amount of $20,000 is secured by the cash surrender value of an insurance policy in the amount of $15,000 and is payable on demand. The shareholder would accept four semiannual payments, including interest at 12%, if the present value of these payments is equal to 120% of what would have been received if the company had been liquidated.

d. The mortgage payable of $420,000 plus accrued interest of $28,000 is fully secured by real estate with a book value of $310,000 and a net realizable value of $460,000. The original mortgage has a remaining term of 334 months and an interest rate of 9%. The mortgage company would agree to a restructuring of 360 months and an interest rate of 11%.

e. All other creditors totaling $160,000 are unsecured without priority. Management would like to propose that these creditors receive monthly payments over the next eight months with interest at 12%. The net present value of these payments should equal 110% of what would have been received had the company been liquidated.

The book values and net realizable values of the company's assets are as follows:

Question

Financial statements after a reorganization. Crawford Distributors, Inc., is a distributor of industrial cleaning supplies throughout the Midwest. Unfortunately, the company has experienced a downturn in sales due to plant closings and relocations throughout its Midwest market. The company is seeking protection under Chapter 11 of the Bankruptcy Code. Condensed financial statements for the year-to-date period ending March 31 of the current year are as follows:

During the next three months, the company engaged in the following activities regarding its reorganization:

a. Net sales of $600,000 have occurred with a gross profit margin of 15.00%. Eighty percent of these sales has been collected in full, and 5.00% of the remaining balance is deemed to be uncollectible.

b. Of the receivables existing at March 31, 90.00% has been collected. Of the remaining balance, 5.00% is deemed to be uncollectible.

c. In an attempt to reduce inventory levels, only $230,000 of inventory was purchased on account. Payments against accounts payable were $800,000.

d. Accounts payable of $135,000 were satisfied by returning the inventory that was purchased. The inventory was carried at its market value of $120,000. Based on current interest rates, another $360,000 of accounts payable was restructured as a note beginning onMay 1 calling for 15 monthly payments of $24,971.17.

e. Note A was restructured by a conveyance of assets and a modification of terms. A vacant lot with a book value of $60,000 and a market value of $116,000 was conveyed to the creditor. As of May 1, the remaining balance of the note, along with accrued interest of $6,000 as of April 30, is to be satisfied by making 30 payments of $16,000 bearing a market interest rate of 6.12%.

f. Note B was restructured on June 30 by forgiving $50,000 of debt and making 48 equal monthly payments of $11,000 based on a market interest rate of 6.30%.

g. Included in other liabilities is a short-term note with a book value of $15,000. Based on current interest rates, the note has a present value of $14,704. Common stock of the company has been issued to the creditor in full satisfaction of the note.

Given the above information, prepare the company's trial balance for the 6-month period ending June 30 of the current year. It may be helpful to prepare a worksheet with the following column headings: Account, Trial Balance as of March 31 (Debit and Credit columns), Second Quarter Activities/Adjustments (Debit and Credit columns), and Trial Balance as of June 30 (Debit and Credit columns). The use of Excel or some other computer spreadsheet is highly recommended.

During the next three months, the company engaged in the following activities regarding its reorganization:

a. Net sales of $600,000 have occurred with a gross profit margin of 15.00%. Eighty percent of these sales has been collected in full, and 5.00% of the remaining balance is deemed to be uncollectible.

b. Of the receivables existing at March 31, 90.00% has been collected. Of the remaining balance, 5.00% is deemed to be uncollectible.

c. In an attempt to reduce inventory levels, only $230,000 of inventory was purchased on account. Payments against accounts payable were $800,000.

d. Accounts payable of $135,000 were satisfied by returning the inventory that was purchased. The inventory was carried at its market value of $120,000. Based on current interest rates, another $360,000 of accounts payable was restructured as a note beginning onMay 1 calling for 15 monthly payments of $24,971.17.

e. Note A was restructured by a conveyance of assets and a modification of terms. A vacant lot with a book value of $60,000 and a market value of $116,000 was conveyed to the creditor. As of May 1, the remaining balance of the note, along with accrued interest of $6,000 as of April 30, is to be satisfied by making 30 payments of $16,000 bearing a market interest rate of 6.12%.

f. Note B was restructured on June 30 by forgiving $50,000 of debt and making 48 equal monthly payments of $11,000 based on a market interest rate of 6.30%.

g. Included in other liabilities is a short-term note with a book value of $15,000. Based on current interest rates, the note has a present value of $14,704. Common stock of the company has been issued to the creditor in full satisfaction of the note.

Given the above information, prepare the company's trial balance for the 6-month period ending June 30 of the current year. It may be helpful to prepare a worksheet with the following column headings: Account, Trial Balance as of March 31 (Debit and Credit columns), Second Quarter Activities/Adjustments (Debit and Credit columns), and Trial Balance as of June 30 (Debit and Credit columns). The use of Excel or some other computer spreadsheet is highly recommended.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/21

Play

Full screen (f)

Deck 23: Debt Restructuring, Corporate Reorganizations, and Liquidations

1

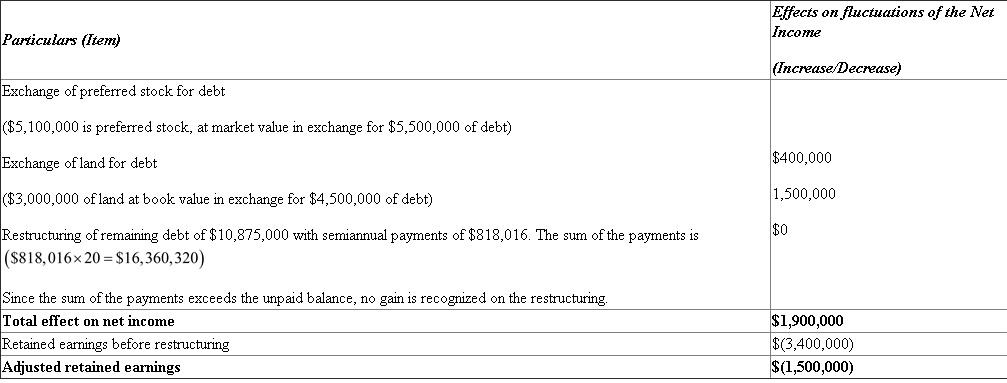

Effect of a quasi-reorganization. For the last several years, Manion Corporation has encountered a declining market for its major product line. Attempts to diversify have led to additional disappointments. This unfortunate set of circumstances has left the company with significant debt and an inability to service its debt. The existing debt consists of $20,000,000 of principal and $875,000 of accrued interest. Discussions with the creditors have resulted in a proposed restructuring of debt. The restructuring would consist of the following actions:

a. Exchanging preferred stock with a fair value of $5,100,000 and a par value of $5,000,000 in exchange for full settlement of $5,500,000 of principal debt.

b. Exchanging land with a value of $4,000,000 and a book value of $3,000,000 in exchange for $4,500,000 of principal debt.

c. The remaining debt and accrued interest would be repaid over the next 10 years with semiannual payments due every six months. The annual stated rate would be 8.5%.

Past operating losses have resulted in a deficit in retained earnings of $3,400,000. In addition to the deficit, the company's equity includes common stock at par value of $6,000,000 and contributed capital in excess of par value in the amount of $1,000,000.

Prepare a schedule that determines the effect on current income of the debt restructuring and the reduction in par value of the common stock necessary to eliminate any deficit in retained earnings. Assume that the restructuring is not part of a formal bankruptcy filing.

a. Exchanging preferred stock with a fair value of $5,100,000 and a par value of $5,000,000 in exchange for full settlement of $5,500,000 of principal debt.

b. Exchanging land with a value of $4,000,000 and a book value of $3,000,000 in exchange for $4,500,000 of principal debt.

c. The remaining debt and accrued interest would be repaid over the next 10 years with semiannual payments due every six months. The annual stated rate would be 8.5%.

Past operating losses have resulted in a deficit in retained earnings of $3,400,000. In addition to the deficit, the company's equity includes common stock at par value of $6,000,000 and contributed capital in excess of par value in the amount of $1,000,000.

Prepare a schedule that determines the effect on current income of the debt restructuring and the reduction in par value of the common stock necessary to eliminate any deficit in retained earnings. Assume that the restructuring is not part of a formal bankruptcy filing.

A quasi reorganization is the " fresh start " of accounting that allows companies to eliminate accumulated deficits in the retained earnings account on their balance sheets. It allows small or large businesses to continue operating after reset of an accounting reorganization of its assets, liabilities, and net worth without the time and expenses normally associated with a legal reorganization.

Statement showing the effect on the current income of debt restructuring

Hence, for eliminating the deficit in retained earnings, the contributed capital in excess of par value would be reduced to zero, and the par value of the common stock would have to be reduced by $500,000.

Hence, for eliminating the deficit in retained earnings, the contributed capital in excess of par value would be reduced to zero, and the par value of the common stock would have to be reduced by $500,000.

Statement showing the effect on the current income of debt restructuring

Hence, for eliminating the deficit in retained earnings, the contributed capital in excess of par value would be reduced to zero, and the par value of the common stock would have to be reduced by $500,000. 2

Amounts to be received by creditors under Chapter 7. Casper Blueprinting, Inc., has filed under Chapter 7 of the Bankruptcy Code. The estimated net realizable value of its assets is as follows:

Creditors' claims are summarized as follows:

a. Bank loan balance of $82,000 plus accrued interest of $3,000 with a first lien against blueprinting equipment.

b. Dealer-financed vehicle loan with an outstanding balance of $18,000, which is secured by the delivery vehicle.

c. Accounts payable due vendors in the amount of $21,000 and secured by the inventory and supplies.

d. A line of credit balance due of $30,000 secured by the accounts receivable.

e. Unpaid payroll and income taxes of $23,000.

f. Accounting and legal fees due in the amount of $12,000 in connection with the administration of the bankrupt estate.

g. Unpaid wages to employees totaling $4,200 ($700 represents the largest amount due any one employee).

h. Loans due shareholders of the corporation totaling $80,000.

i. Other unsecured creditors without priority in the amount of $31,000.

Prepare a schedule to show the estimated amount to be received by each major category of creditor.

Creditors' claims are summarized as follows:

a. Bank loan balance of $82,000 plus accrued interest of $3,000 with a first lien against blueprinting equipment.

b. Dealer-financed vehicle loan with an outstanding balance of $18,000, which is secured by the delivery vehicle.

c. Accounts payable due vendors in the amount of $21,000 and secured by the inventory and supplies.

d. A line of credit balance due of $30,000 secured by the accounts receivable.

e. Unpaid payroll and income taxes of $23,000.

f. Accounting and legal fees due in the amount of $12,000 in connection with the administration of the bankrupt estate.

g. Unpaid wages to employees totaling $4,200 ($700 represents the largest amount due any one employee).

h. Loans due shareholders of the corporation totaling $80,000.

i. Other unsecured creditors without priority in the amount of $31,000.

Prepare a schedule to show the estimated amount to be received by each major category of creditor.

Prepare a schedule to show estimate amount to be received by each category of creditor

Working notes:

Working notes:

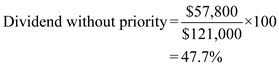

Calculation of dividend to unsecured creditors:

Calculation of unsecured amount received by each creditor:

Calculation of unsecured amount received by each creditor:

The calculated unsecured dividend with priority is 100%, and dividend without priority is 47.77% (refer above calculation).

Now, calculate unsecured amount received by each creditor as follows:

Working notes: Calculation of dividend to unsecured creditors:

Calculation of unsecured amount received by each creditor: The calculated unsecured dividend with priority is 100%, and dividend without priority is 47.77% (refer above calculation).

Now, calculate unsecured amount received by each creditor as follows:

3

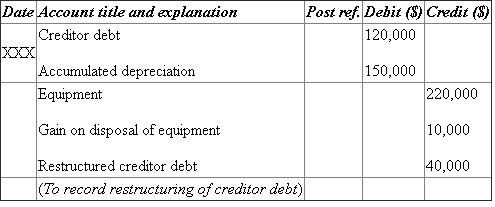

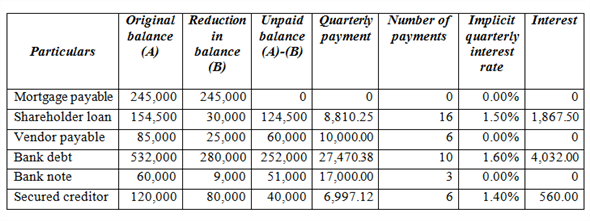

Entries to record restructuring of debt. Rose Corporation was unable to service its outstanding debt. In an attempt to avoid filing for bankruptcy, it took the following measures:

a. Patents with book value of $140,000 and accumulated amortization of $115,000 were sold for $20,000.

b. Goodwill with a book value of $150,000 resulted from the acquisition of a small manufacturing firm in Indiana. The goodwill was tested for impairment, and it was concluded that $100,000 of the goodwill was impaired.

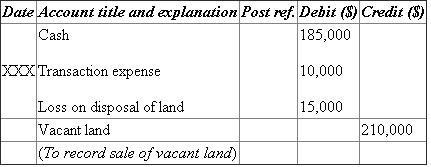

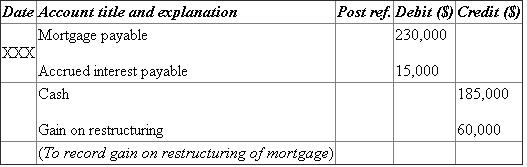

c. A mortgage on a parcel of vacant land had a book value of $230,000. The land with a book value of $210,000 was sold for net proceeds of $185,000 after payment of $10,000 of transaction costs. The mortgage holder accepted the proceeds in full settlement of the mortgage and related accrued interest of $15,000.

d. A loan from a major shareholder/employee had a remaining principal amount of $150,000 plus accrued interest of $4,500 based on the stated rate of 12% payable quarterly. Given significantly lower current market rates, the shareholder agreed to restructure the debt as follows: 6% interest, 16 quarterly payments of principal and interest in the amount of $8,810.25, and receipt of a cash bonus of $30,000 in satisfaction of any remaining debt.

e. A major vendor had a payable balance of $85,000, which had remained unpaid for over five months. In satisfaction of the payable, the vendor agreed to receive an immediate cash payment of $15,000 plus six monthly payments of $10,000 each.

f. Bank debt with an outstanding balance of $532,000 including accrued interest of $22,000 was reduced by $80,000 in exchange for investment securities that were recorded at their market value of $62,000. Another $200,000 of debt was exchanged for treasury stock of the company that had a par value of $50,000 and an original cost of $150,000. The balance of the debt was restructured calling for 10 quarterly payments of $27,470.38.

g. A bank note payable with a balance of $60,000 was restructured by making three quarterly payments of $17,000.

h. A partially secured creditor with a debt balance of $120,000 repossessed equipment that served as collateral. The equipment had a book value of $220,000 and accumulated depreciation of $150,000. The remaining $40,000 of debt was to be paid over the next six quarters in equal payments bearing interest at 5.6%.

Prepare all of the necessary entries to record the above events (a) through (h). Determine the total amount of interest expense to be recognized in connection with the first quarterly payment associated with the restructured debts.

a. Patents with book value of $140,000 and accumulated amortization of $115,000 were sold for $20,000.

b. Goodwill with a book value of $150,000 resulted from the acquisition of a small manufacturing firm in Indiana. The goodwill was tested for impairment, and it was concluded that $100,000 of the goodwill was impaired.

c. A mortgage on a parcel of vacant land had a book value of $230,000. The land with a book value of $210,000 was sold for net proceeds of $185,000 after payment of $10,000 of transaction costs. The mortgage holder accepted the proceeds in full settlement of the mortgage and related accrued interest of $15,000.

d. A loan from a major shareholder/employee had a remaining principal amount of $150,000 plus accrued interest of $4,500 based on the stated rate of 12% payable quarterly. Given significantly lower current market rates, the shareholder agreed to restructure the debt as follows: 6% interest, 16 quarterly payments of principal and interest in the amount of $8,810.25, and receipt of a cash bonus of $30,000 in satisfaction of any remaining debt.

e. A major vendor had a payable balance of $85,000, which had remained unpaid for over five months. In satisfaction of the payable, the vendor agreed to receive an immediate cash payment of $15,000 plus six monthly payments of $10,000 each.

f. Bank debt with an outstanding balance of $532,000 including accrued interest of $22,000 was reduced by $80,000 in exchange for investment securities that were recorded at their market value of $62,000. Another $200,000 of debt was exchanged for treasury stock of the company that had a par value of $50,000 and an original cost of $150,000. The balance of the debt was restructured calling for 10 quarterly payments of $27,470.38.

g. A bank note payable with a balance of $60,000 was restructured by making three quarterly payments of $17,000.

h. A partially secured creditor with a debt balance of $120,000 repossessed equipment that served as collateral. The equipment had a book value of $220,000 and accumulated depreciation of $150,000. The remaining $40,000 of debt was to be paid over the next six quarters in equal payments bearing interest at 5.6%.

Prepare all of the necessary entries to record the above events (a) through (h). Determine the total amount of interest expense to be recognized in connection with the first quarterly payment associated with the restructured debts.

(c)  • Cash is an income and increases the value of asset. Therefore, it is debited.

• Cash is an income and increases the value of asset. Therefore, it is debited.

• Transaction expense decreases the value of liability. Therefore, it is debited.

• Loss on disposal of land decreases the value of liability. Therefore, it is credited.

• Vacant land decreases the value of asset. Therefore, it is credited.

• Mortgage payable and accrued interest payable decrease the value of asset. Therefore, they are debited.

• Mortgage payable and accrued interest payable decrease the value of asset. Therefore, they are debited.

• Cash decreases the value of asset. Therefore, it is credited.

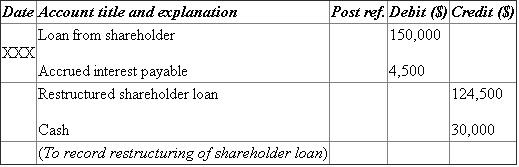

(d) • Loan from shareholder and accrued interest payable decrease the value of asset. Therefore, they are debited.

• Loan from shareholder and accrued interest payable decrease the value of asset. Therefore, they are debited.

• Restructured shareholder loan increases the value of liability. Therefore, it is credited.

• Cash decreases the value of asset. Therefore, it is credited.

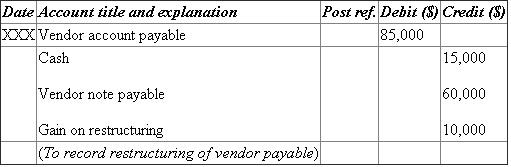

(e) • Vendor account payable increases the value of liability. Therefore, it is debited.

• Vendor account payable increases the value of liability. Therefore, it is debited.

• Cash decreases the value of asset. Therefore, it is credited.

• Vendor note payable increases the value of liability. Therefore, it is credited.

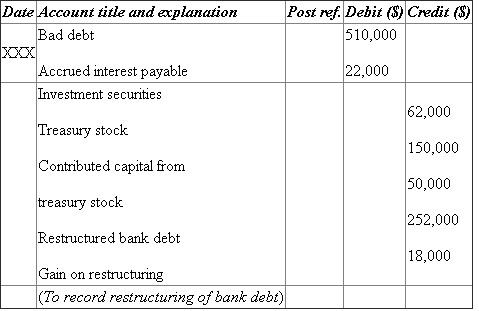

(f) • Accrued interest payable decreases the value of liability. Therefore, it is debited.

• Accrued interest payable decreases the value of liability. Therefore, it is debited.

• Investment and treasury stock increase the value of asset. Therefore, they are credited.

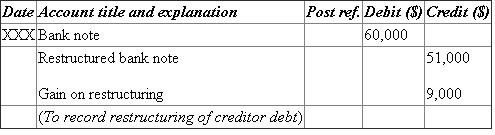

(g) • Bank note decreases the value of liability. Therefore, it is debited.

• Bank note decreases the value of liability. Therefore, it is debited.

• Gain on restructuring increases the value of liability. Therefore, it is credited.

(h) • Accumulated depreciation decreases the value of liability. Therefore, it is debited.

• Accumulated depreciation decreases the value of liability. Therefore, it is debited.

• Equipment decreases the value of asset. Therefore, it is credited.

• Gain on disposal of equipment increases the value of liability. Therefore, it is credited.

Calculation of total interest expense with first quarterly payment:

Note:

Note:

• Cash is an income and increases the value of asset. Therefore, it is debited.• Transaction expense decreases the value of liability. Therefore, it is debited.

• Loss on disposal of land decreases the value of liability. Therefore, it is credited.

• Vacant land decreases the value of asset. Therefore, it is credited.

• Mortgage payable and accrued interest payable decrease the value of asset. Therefore, they are debited.• Cash decreases the value of asset. Therefore, it is credited.

(d)

• Loan from shareholder and accrued interest payable decrease the value of asset. Therefore, they are debited.• Restructured shareholder loan increases the value of liability. Therefore, it is credited.

• Cash decreases the value of asset. Therefore, it is credited.

(e)

• Vendor account payable increases the value of liability. Therefore, it is debited.• Cash decreases the value of asset. Therefore, it is credited.

• Vendor note payable increases the value of liability. Therefore, it is credited.

(f)

• Accrued interest payable decreases the value of liability. Therefore, it is debited.• Investment and treasury stock increase the value of asset. Therefore, they are credited.

(g)

• Bank note decreases the value of liability. Therefore, it is debited.• Gain on restructuring increases the value of liability. Therefore, it is credited.

(h)

• Accumulated depreciation decreases the value of liability. Therefore, it is debited.• Equipment decreases the value of asset. Therefore, it is credited.

• Gain on disposal of equipment increases the value of liability. Therefore, it is credited.

Calculation of total interest expense with first quarterly payment:

Note: 4

Statement of realization and liquidation, dividend to unsecured creditors without priority. A partially completed statement of realization and liquidation is as follows:

The following additional transactions have occurred through August 12, 2019:

a. Receivables collected amounted to $39,000. Receivables with a book value of $15,000 that were not allowed for were written off.

b. A $12,000 loan that was fully secured was paid off.

c. A valid claim was received from a leasing company seeking payment of $15,000 for equipment rentals.

d. Securities costing $18,000 were sold for $23,000, minus a brokerage fee of $500.

e. Depreciation on machinery was $3,200.

f. Payments on accounts payable totaled $25,000, of which the entire amount was secured by the inventory sold.

g. Machinery that originally cost $85,000 and had a book value of $45,000 sold for $36,000.

h. Proceeds from the sale of machinery in (g) were remitted to the bank, which holds a $50,000 loan on the machinery.

1. Update the statement of realization and liquidation to properly reflect transactions (a) through (h).

2. Assuming the remaining noncash assets can be realized for $410,000, determine the estimated dividend to be received by unsecured creditors without priority.

The following additional transactions have occurred through August 12, 2019:

a. Receivables collected amounted to $39,000. Receivables with a book value of $15,000 that were not allowed for were written off.

b. A $12,000 loan that was fully secured was paid off.

c. A valid claim was received from a leasing company seeking payment of $15,000 for equipment rentals.

d. Securities costing $18,000 were sold for $23,000, minus a brokerage fee of $500.

e. Depreciation on machinery was $3,200.

f. Payments on accounts payable totaled $25,000, of which the entire amount was secured by the inventory sold.

g. Machinery that originally cost $85,000 and had a book value of $45,000 sold for $36,000.

h. Proceeds from the sale of machinery in (g) were remitted to the bank, which holds a $50,000 loan on the machinery.

1. Update the statement of realization and liquidation to properly reflect transactions (a) through (h).

2. Assuming the remaining noncash assets can be realized for $410,000, determine the estimated dividend to be received by unsecured creditors without priority.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

5

Distinguish between a corporate reorganization and a liquidation as provided for under bankruptcy law.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

6

Benefits of a quasi-reorganization. Barber Technologies designs and develops software to be used for the management of inventory by both retailers and manufacturing firms. Over the past three years, the company has experienced significant competition and a declining market resulting in a significant deficit in retained earnings. In response to this condition, you have suggested that management consider the following:

a. Recognize all asset impairments.

b. Restructure the long-term debt by committing to make future payments that are less than the basis of the original debt.

c. Adjust the par value of common stock to eliminate the deficit in retained earnings.

Discuss how the above actions will likely affect:

1. The current ratio, debt-to-equity ratio, and return on equity.

2. The determination of net income in subsequent periods.

a. Recognize all asset impairments.

b. Restructure the long-term debt by committing to make future payments that are less than the basis of the original debt.

c. Adjust the par value of common stock to eliminate the deficit in retained earnings.

Discuss how the above actions will likely affect:

1. The current ratio, debt-to-equity ratio, and return on equity.

2. The determination of net income in subsequent periods.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

7

Effect of a quasi-reorganization. Marshall Tool and Die Company has been experiencing significant foreign competition and a declining market. Annual net losses from operations have averaged $250,000 over the last three years. The company's balance sheet as of December 31, 2017, is as follows:

After analyzing accounts receivable and inventory, it has been determined that the allowance for uncollectibles should be increased by $75,000 and the inventory should be written down by $20,000. Based on recent appraisals, it is estimated that the plant and equipment have a market value of $1,285,000. The goodwill is traceable to the purchase of a small tooling company in 2013. Based on an analysis of cash flows associated with that acquisition, it is estimated that the goodwill has an impaired value of $0. Other assets represent a note receivable from officers of the corporation. The note calls for five annual payments of $8,309 including interest at the rate of 6%.

In response to the current situation, the company has decided to take the following actions:

a. Record the suggested impairment in all assets.

b. Restructure the note receivable from the officers to reflect four annual payments and an interest rate of 7.5%.

c. Restructure the note payable, which was due in 2019, to provide for 12 semiannual payments of $120,000 including interest at the annual rate of 6%.

d. Engage in a quasi-reorganization to eliminate the deficit in retained earnings.

1. Prepare a revised classified balance sheet to reflect the effect of management's actions.

2. Compute the following ratios before and after management's actions: current ratio and debt-to-equity ratio.

3. Given the above ratio analysis, if the ratios do not suggest an improvement, discuss the benefits of management's actions.

After analyzing accounts receivable and inventory, it has been determined that the allowance for uncollectibles should be increased by $75,000 and the inventory should be written down by $20,000. Based on recent appraisals, it is estimated that the plant and equipment have a market value of $1,285,000. The goodwill is traceable to the purchase of a small tooling company in 2013. Based on an analysis of cash flows associated with that acquisition, it is estimated that the goodwill has an impaired value of $0. Other assets represent a note receivable from officers of the corporation. The note calls for five annual payments of $8,309 including interest at the rate of 6%.

In response to the current situation, the company has decided to take the following actions:

a. Record the suggested impairment in all assets.

b. Restructure the note receivable from the officers to reflect four annual payments and an interest rate of 7.5%.

c. Restructure the note payable, which was due in 2019, to provide for 12 semiannual payments of $120,000 including interest at the annual rate of 6%.

d. Engage in a quasi-reorganization to eliminate the deficit in retained earnings.

1. Prepare a revised classified balance sheet to reflect the effect of management's actions.

2. Compute the following ratios before and after management's actions: current ratio and debt-to-equity ratio.

3. Given the above ratio analysis, if the ratios do not suggest an improvement, discuss the benefits of management's actions.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

8

Explain how the claims of fully secured and partially secured creditors affect the dividend that may be received by unsecured creditors.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

9

Troubled debt restructurings, impact on earnings. Ridgeway Builders, Inc., is in the residential construction industry and has been experiencing a business downturn. As a result of these economic conditions, the company is having difficulty serving its outstanding debt and is seeking relief outside of the bankruptcy courts. The following summarizes outstanding debt and management's proposed restructuring:

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

10

Statement of affairs. A creditor's committee of Carlton Company has obtained the March 31, 2015, balance sheet shown below.

An analysis of the company's accounts disclosed the following activities through April 30, 2015:

a. Carlton Company started business on April 1, 2010, with authorized stock of $100 par. Of the 1,000 authorized shares, 750 were paid for in full at par, and 250 were subscribed at par, with a required 20% down payment and the balance payable upon call. All the subscriptions receivable are due fromW. Krueger, president of the company, and are fully collectible.

b. Marketable securities include the $25,000 cost of U.S. Treasury bonds valued at $23,200 and 25 shares of Groves Company common stock, costing $3,750, with a fair value of $3,300.

c. The land originally cost $10,000, and the building was erected at a cost of $102,500. Of the accumulated depreciation, $30,000 is applicable to the building. The realizable value of the real estate is $75,000.

d. Notes receivable were endorsed with recourse when discounted and are expected to be dishonored. Of the accounts receivable, $3,000 are considered collectible.

e. Inventories are shown at cost. Any finished goods are expected to yield 110% of cost. If scrapped, goods in process have a realizable value of only $2,200. It is estimated, however, that the work in process can be completed by the addition of $3,000 of present materials and an expenditure of $3,500 for labor. The materials deteriorate rapidly and will realize only 20% of cost. (Use the cost completion method illustrated in the text.)

f. Equipment is estimated to have a realizable value of $12,000.

g. Notes payable include a $25,000 note to Aerotex Company and a $62,500 note to B. Williams. Aerotex holds the U.S. Treasury bonds as security for its loans. It also holds the first mortgage of $37,500 on the company's real estate, interest on which is paid throughMarch 31, 2015. The note payable toWilliams is secured by a chattelmortgage on factory equipment. Interest on the note has been paid throughMarch 31, 2015. Williams also holds the secondmortgage on the real estate.

h. Any expenses not specifically mentioned need not be considered. All salaries qualify for priority, including labor to complete the work in process.

Prepare a statement of affairs for Carlton Company.

An analysis of the company's accounts disclosed the following activities through April 30, 2015:

a. Carlton Company started business on April 1, 2010, with authorized stock of $100 par. Of the 1,000 authorized shares, 750 were paid for in full at par, and 250 were subscribed at par, with a required 20% down payment and the balance payable upon call. All the subscriptions receivable are due fromW. Krueger, president of the company, and are fully collectible.

b. Marketable securities include the $25,000 cost of U.S. Treasury bonds valued at $23,200 and 25 shares of Groves Company common stock, costing $3,750, with a fair value of $3,300.

c. The land originally cost $10,000, and the building was erected at a cost of $102,500. Of the accumulated depreciation, $30,000 is applicable to the building. The realizable value of the real estate is $75,000.

d. Notes receivable were endorsed with recourse when discounted and are expected to be dishonored. Of the accounts receivable, $3,000 are considered collectible.

e. Inventories are shown at cost. Any finished goods are expected to yield 110% of cost. If scrapped, goods in process have a realizable value of only $2,200. It is estimated, however, that the work in process can be completed by the addition of $3,000 of present materials and an expenditure of $3,500 for labor. The materials deteriorate rapidly and will realize only 20% of cost. (Use the cost completion method illustrated in the text.)

f. Equipment is estimated to have a realizable value of $12,000.

g. Notes payable include a $25,000 note to Aerotex Company and a $62,500 note to B. Williams. Aerotex holds the U.S. Treasury bonds as security for its loans. It also holds the first mortgage of $37,500 on the company's real estate, interest on which is paid throughMarch 31, 2015. The note payable toWilliams is secured by a chattelmortgage on factory equipment. Interest on the note has been paid throughMarch 31, 2015. Williams also holds the secondmortgage on the real estate.

h. Any expenses not specifically mentioned need not be considered. All salaries qualify for priority, including labor to complete the work in process.

Prepare a statement of affairs for Carlton Company.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

11

Explain what purpose the statement of realization and liquidation serves.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

12

Cash flows, debt restructuring, effect on income under bankruptcy and nonbankruptcy law. In an attempt to avoid liquidating the company, the management of Carter, Inc., is considering a reorganization that calls for the restructuring of $2,100,000 of debt maturing in three years and related accrued interest payable of $72,737. The restructuring agreement calls for monthly payments over the next 60 months, a reduction in the interest rate to 8%, and the cancellation of $200,000 of debt. The market rate of interest for such a refinancing would be 13%. In addition to the debt restructuring, management is proposing to reduce the par value of its common stock in order to generate enough paid-in capital in excess of par value to absorb a $500,000 deficit in retained earnings. The present balance of paid-in capital in excess of par value is $80,000.

1. Prepare a schedule to determine the total gain resulting from the forgiveness and restructuring of debt and the amount of future interest expense assuming (a) a nonbankruptcy approach and (b) a bankruptcy approach to the reorganization.

2. Determine by how much the par value of common stock would have to be reduced in order to absorb the deficit in retained earnings assuming (a) a nonbankruptcy approach and (b) a bankruptcy approach.

1. Prepare a schedule to determine the total gain resulting from the forgiveness and restructuring of debt and the amount of future interest expense assuming (a) a nonbankruptcy approach and (b) a bankruptcy approach to the reorganization.

2. Determine by how much the par value of common stock would have to be reduced in order to absorb the deficit in retained earnings assuming (a) a nonbankruptcy approach and (b) a bankruptcy approach.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

13

Recording restructuring transactions. St. John Corporation is barely solvent and has been seeking an equity investor that would be interested in making a capital contribution so that the company would hopefully return to performance levels it had experienced in the past. The company's year-end 2015 balance sheet is presented below.

Selected transactions occurring during the first six months of 2016 were as follows:

a. Patents with a fair value of $230,000 were transferred to the officer in partial satisfaction of their note. The remaining balance on the note would be paid over five quarters with the first payment of $35,026.77 due on June 30, 2016.

b. The mortgage payable was restructured with 40 quarterly payments of $51,178.05, beginning on June 30, 2016, in addition to an immediate lump sum payment of $100,000.

c. The bank A note payable was restructured as follows: the development land with a net realizable value of $980,000 was conveyed along with marketable securities having a book value of $80,000 and a market value of $95,000. The balance of the note was to be over 10 quarters with payments of $111,145.03 beginning on June 30, 2016.

d. The bank B note payable was partially secured by equipment which had a book value of $240,000 and a net realizable value of $220,000. The equipment was seized by the bank and the company agreed to settle the balance of the note by making 10 quarterly payments of $55,000 beginning on June 30, 2016.

e. On June 30, 2016 all payments required by item (a) through (d) above were paid.

f. Common shareholders approved a reduction in par value from $10 per share to $5 per share and the deficit was eliminated.

Prepare all necessary entries to record the above transactions (a) through (f ).

Selected transactions occurring during the first six months of 2016 were as follows:

a. Patents with a fair value of $230,000 were transferred to the officer in partial satisfaction of their note. The remaining balance on the note would be paid over five quarters with the first payment of $35,026.77 due on June 30, 2016.

b. The mortgage payable was restructured with 40 quarterly payments of $51,178.05, beginning on June 30, 2016, in addition to an immediate lump sum payment of $100,000.

c. The bank A note payable was restructured as follows: the development land with a net realizable value of $980,000 was conveyed along with marketable securities having a book value of $80,000 and a market value of $95,000. The balance of the note was to be over 10 quarters with payments of $111,145.03 beginning on June 30, 2016.

d. The bank B note payable was partially secured by equipment which had a book value of $240,000 and a net realizable value of $220,000. The equipment was seized by the bank and the company agreed to settle the balance of the note by making 10 quarterly payments of $55,000 beginning on June 30, 2016.

e. On June 30, 2016 all payments required by item (a) through (d) above were paid.

f. Common shareholders approved a reduction in par value from $10 per share to $5 per share and the deficit was eliminated.

Prepare all necessary entries to record the above transactions (a) through (f ).

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

14

Cash flows, debt restructuring, effect on income under bankruptcy and nonbankruptcy law. Rather than entering into a lengthy bankruptcy proceeding, Peltzer Manufacturing has reached agreement with its long-term creditors to restructure various loans. The restructured loans are described below.

Loan A-This debt has a principal balance of $4,000,000 and accrued interest of $80,000. Under the restructuring agreement, $500,000 of debt would be forgiven, and the balance of the amounts due would be refinanced at a rate of 10% with monthly installment payments of $50,000 and a term of eight years. Assets with a net realizable value of $2,500,000 would also be pledged as additional security against the restructured loan.

Loan B-This debt has a principal balance of $1,000,000 and accrued interest of $25,000. Under the restructuring agreement, the accrued interest would be forgiven, and the principal amount would be exchanged for preferred stock with a par value of $500,000 and a fair value of $900,000.

Loan C-This debt has a principal balance of $2,000,000 and accrued interest of $37,500. Under the restructuring agreement, the creditor would receive a parcel of land with a book value of $200,000 and a net realizable value of $250,000. The remaining unpaid balance would be refinanced over five years at a 9% interest rate. Installment payments would be on a quarterly basis.

1. Determine the total quarterly cash outflows that will be required by Peltzer's debt restructuring.

2. Covering the first quarter subsequent to restructuring, prepare a schedule that compares the effect on Peltzer's net income of accounting for the restructuring as part of a formal bankruptcy filing versus it not being part of such a filing.

Loan A-This debt has a principal balance of $4,000,000 and accrued interest of $80,000. Under the restructuring agreement, $500,000 of debt would be forgiven, and the balance of the amounts due would be refinanced at a rate of 10% with monthly installment payments of $50,000 and a term of eight years. Assets with a net realizable value of $2,500,000 would also be pledged as additional security against the restructured loan.

Loan B-This debt has a principal balance of $1,000,000 and accrued interest of $25,000. Under the restructuring agreement, the accrued interest would be forgiven, and the principal amount would be exchanged for preferred stock with a par value of $500,000 and a fair value of $900,000.

Loan C-This debt has a principal balance of $2,000,000 and accrued interest of $37,500. Under the restructuring agreement, the creditor would receive a parcel of land with a book value of $200,000 and a net realizable value of $250,000. The remaining unpaid balance would be refinanced over five years at a 9% interest rate. Installment payments would be on a quarterly basis.

1. Determine the total quarterly cash outflows that will be required by Peltzer's debt restructuring.

2. Covering the first quarter subsequent to restructuring, prepare a schedule that compares the effect on Peltzer's net income of accounting for the restructuring as part of a formal bankruptcy filing versus it not being part of such a filing.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

15

Preparation of a statement of realization and liquidation. Problem 21-5 presents the balance sheet of St. John Corporation as of year-end 2015. Assume that the company is not able to service its debts and is unable to secure any significant restructuring arrangements from its primary lenders. As a result, St. John has decided to liquidate the corporation and has submitted a plan for liquidation. The plan has received all necessary approvals, and the liabilities affected by the plan are described as follows:

Accounts payable: Of these accounts, $400,000 is fully secured by claims against inventory with a book value of $430,000. The inventory was completed at an additional cost of $25,000, it was sold for $480,000, and the secured payables were paid. Another $320,000 of the payables is secured by the remaining inventory which is estimated to have a net realizable value of $200,000. The balance of the payables is unsecured.

Note payable-officer: This note is secured by the investment in Sky Industries which has a net realizable value of $320,000.

Bank A note payable: This note is secured by all of the equipment and the patent. Equipment with a book value of $800,000 has been sold for $700,000 by a broker who was paid a fee of $10,000. It is estimated that the balance of the equipment will have a net realizable value of $400,000. The patent was sold to an officer of the corporation for $250,000. Net proceeds from the collateral were paid to Bank A.

Bank B note payable: This note is secured by the development land. The land consists of two separate parcels with book values of $400,000 and $300,000. The $300,000 parcel was sold for $360,000 and it is estimated that the remaining parcel will have a net realizable value of $500,000.

Mortgage payable: This mortgage is secured by the manufacturing plant and other current assets with a book value of $130,000. The plant is currently listed for sale with an asking price of $1,800,000. Realistically, it is estimated that the plant could sell for $1,500,000 before commissions of $90,000. The other current assets securing the mortgage were sold for $100,000.

Other liabilities: $90,000 of these liabilities is secured by all receivables of the company. Receivables with a book value of $150,000 have been collected, and an additional $40,000 of allowance for uncollectible accounts has been established on the balance of the accounts. The $90,000 of other liabilities was paid. Of the remaining other liabilities, $95,000 is unsecured without priority, and the balance is unsecured with priority. Since year-end, $20,000 of the unsecured liabilities with priority has been paid out of available assets.

Since year-end 2016, additional assets with a net realizable value of $15,000 have been discovered, and administrative/legal expenses of $20,000 in connection with the liquidation have been incurred of which half have been paid.

Assuming that all of the above activity occurred within the first six months of 2016, prepare a statement of realization and liquidation to reflect the above activity and information.

Accounts payable: Of these accounts, $400,000 is fully secured by claims against inventory with a book value of $430,000. The inventory was completed at an additional cost of $25,000, it was sold for $480,000, and the secured payables were paid. Another $320,000 of the payables is secured by the remaining inventory which is estimated to have a net realizable value of $200,000. The balance of the payables is unsecured.

Note payable-officer: This note is secured by the investment in Sky Industries which has a net realizable value of $320,000.

Bank A note payable: This note is secured by all of the equipment and the patent. Equipment with a book value of $800,000 has been sold for $700,000 by a broker who was paid a fee of $10,000. It is estimated that the balance of the equipment will have a net realizable value of $400,000. The patent was sold to an officer of the corporation for $250,000. Net proceeds from the collateral were paid to Bank A.

Bank B note payable: This note is secured by the development land. The land consists of two separate parcels with book values of $400,000 and $300,000. The $300,000 parcel was sold for $360,000 and it is estimated that the remaining parcel will have a net realizable value of $500,000.

Mortgage payable: This mortgage is secured by the manufacturing plant and other current assets with a book value of $130,000. The plant is currently listed for sale with an asking price of $1,800,000. Realistically, it is estimated that the plant could sell for $1,500,000 before commissions of $90,000. The other current assets securing the mortgage were sold for $100,000.

Other liabilities: $90,000 of these liabilities is secured by all receivables of the company. Receivables with a book value of $150,000 have been collected, and an additional $40,000 of allowance for uncollectible accounts has been established on the balance of the accounts. The $90,000 of other liabilities was paid. Of the remaining other liabilities, $95,000 is unsecured without priority, and the balance is unsecured with priority. Since year-end, $20,000 of the unsecured liabilities with priority has been paid out of available assets.

Since year-end 2016, additional assets with a net realizable value of $15,000 have been discovered, and administrative/legal expenses of $20,000 in connection with the liquidation have been incurred of which half have been paid.

Assuming that all of the above activity occurred within the first six months of 2016, prepare a statement of realization and liquidation to reflect the above activity and information.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

16

Impact of restructuring on the income statement. Cutler Manufacturing manufactures and distributes specialty piping used in the construction industry. Due to the recent contraction in the commercial construction market, Cutler has had difficulty servicing its outstanding debt. In particular, debt bearing interest at a stated rate of 6.00% with 42 remaining payments of $15,000 per month is being considered for restructuring. The creditor and Cutler have identified the following two alternatives:

a. Alternative A: Convey vacant land with a fair market value of $380,000 and a book value of $260,000 to the creditor along with a commitment to make 40 monthly payments of $5,067.60 each. The market rate of interest for a loan with similar characteristics is 6.24%.

b. Alternative B: Convey vacant land with a fair market value of $380,000 and a book value of $260,000 to the creditor along with a commitment to make 60 monthly payments of $3,000 each. The market rate of interest for a loan with similar characteristics is 6.60%.

For each of the above restructuring alternatives, determine the impact on Cutler's income statement for the first two months of the restructuring period.

a. Alternative A: Convey vacant land with a fair market value of $380,000 and a book value of $260,000 to the creditor along with a commitment to make 40 monthly payments of $5,067.60 each. The market rate of interest for a loan with similar characteristics is 6.24%.

b. Alternative B: Convey vacant land with a fair market value of $380,000 and a book value of $260,000 to the creditor along with a commitment to make 60 monthly payments of $3,000 each. The market rate of interest for a loan with similar characteristics is 6.60%.

For each of the above restructuring alternatives, determine the impact on Cutler's income statement for the first two months of the restructuring period.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

17

Determining proceeds to various classes of claims. Tebon Manufacturing is considering seeking relief under Chapter 7 of the Bankruptcy Code. However, the company would prefer to engage in out-of-court activities that would allow for a restructuring of debts in an orderly manner. Before approaching its creditors, the company is attempting to estimate the amount of consideration that would be received by various classes of creditors if the company did liquidate. The company's assets and liabilities are as follows:

Of the accounts payable, $130,000 is secured by inventory which has a net realizable value of $150,000. Note A is secured by the balance of the inventory and receivables. Note B is secured by equipment with a net realizable value of $300,000, and the mortgage payable and accrued interest are secured by the land. All of the other liabilities are unsecured, although $10,000 is unsecured with priority over the balance.

Prepare a schedule that sets forth the classes of claims (fully secured, partially secured, unsecured) and the assets that satisfy each class. For each class, compute the dividend and determine the total amount of consideration to be received in satisfaction of Note Payable-B.

Of the accounts payable, $130,000 is secured by inventory which has a net realizable value of $150,000. Note A is secured by the balance of the inventory and receivables. Note B is secured by equipment with a net realizable value of $300,000, and the mortgage payable and accrued interest are secured by the land. All of the other liabilities are unsecured, although $10,000 is unsecured with priority over the balance.

Prepare a schedule that sets forth the classes of claims (fully secured, partially secured, unsecured) and the assets that satisfy each class. For each class, compute the dividend and determine the total amount of consideration to be received in satisfaction of Note Payable-B.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

18

Restructuring versus liquidation. Atoyo Fabricating, Inc., has not been able to service its debts adequately. The company is a family business that has been in existence for 35 years. The shareholders want to avoid liquidating the business and are seeking your help in formulating a plan of reorganization which:

a. Provides creditors with at least as much consideration as, if not more than, they would receive if the company were liquidated.

b. Does not require monthly debt service in excess of $75,000.

Information regarding the various creditor claims and possible restructuring parameters is as follows:

a. Accounts payable due vendors total $134,000. Terms are generally 2/10 net 30, and virtually all accounts are past due. Vendors with balances of $40,000 due have indicated that in satisfaction of the amount due, they would accept equal monthly installment payments bearing no less than 12% and not exceeding three months in duration. These vendors have secured their claims with inventory that has a book value and net realizable value of $55,000 and $42,000, respectively. Vendors with a balance due of $74,000 have a secured interest in inventory with a book value of $60,000 and a net realizable value of $46,000. These vendors would accept three monthly installment payments of $20,000 including interest at the rate of 12% in satisfaction of the amount due. The remaining payables represent unsecured amounts that would be paid $3,000 per month for the next five months including interest at 12%.