Deck 18: Food Marketing: From Stable to Table

Full screen (f)

Question

Processors of FCOJ face price risks that the price of oranges may go up because of a freeze or a bad crop. In a table similar to Figure 17-6, show the steps a processor would go through to hedge this risk.

Question

Question

Question

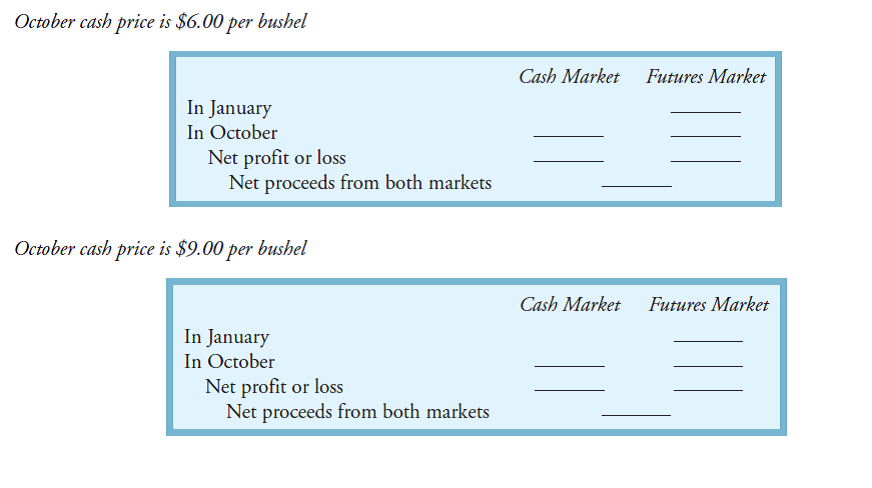

In order to hedge effectively, the hedger must have knowledge about expected bases. Traders and brokers have tables that show what a typical basis is in any given month for a particular contract. Sam is a soybean farmer. In October he will harvest 5,000 bushels of soybeans(one contract.) Based on past experience he expects the basis on the December contract to be $0.08 in October. Tha is, December futures contract will trade in October for $0.08 more than the cash price in October.

In January (a slow time for soybean farmers), Sam notes that a December contract is trading at $7.80 per bushel. Sam figures his cost of production and returns to land to be $6.80 per bushel. SO, in January he hedges his crop. Show in the following how the hedge will work assuming two alternative October cash prices ($6.00 and $9.00 per bushel) and an October basis $0.08.

In January (a slow time for soybean farmers), Sam notes that a December contract is trading at $7.80 per bushel. Sam figures his cost of production and returns to land to be $6.80 per bushel. SO, in January he hedges his crop. Show in the following how the hedge will work assuming two alternative October cash prices ($6.00 and $9.00 per bushel) and an October basis $0.08.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/5

Play

Full screen (f)

Deck 18: Food Marketing: From Stable to Table

1

Processors of FCOJ face price risks that the price of oranges may go up because of a freeze or a bad crop. In a table similar to Figure 17-6, show the steps a processor would go through to hedge this risk.

The basic notion of future market entails to the agreement of price upon the present time but promising the delivery is stated for a future period of time. The hedger in the futures market will always work toward to minimize the price risk.

The hedger in this case is the processor of FCOJ in the future markets. The processor has come in the market in order to buy an insurance to protect against the volatility in the prices market of oranges due to bad weather or crop failure.

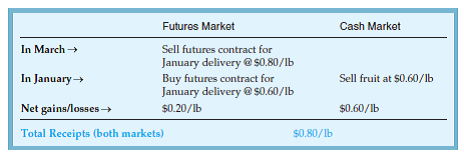

The processor A of FCOJ can also use this future market in order to hedge his crop of orange in the market. In the month of March the person A has finished the harvest and now looks forward for another year. So considering an option of hedging at a future contract that matures in January next year, it is quoted at around $0.70 per ponds. He uses it for around $6 pounds per box that is equal to $4.2 per box. The person A estimates its production cost at around approximately $3.2 per box, so the processor will be pleased with the price that has been locked in to around $4.2 per box for the crop in next year.

But the problem lies in the contract as there are still around 9 months away from the actual harvest and there can be possibility of a freeze or crop failure in future. Because of this inherent risk, A will decide to hedge the next year crop of oranges in the month of March.

So the person a will open up the hedge with a price equal to $0.70 per pound by selling the January future contracts equal to the amount that is equal to his expected level of production. On the March day, the person a is making a promise of delivery in January according to the terms of the FCOJ contract at the price equal to $0.70 as expected in present context. By selling a contract equal to $0.70, A has assured himself a minimum price no matter what happens in January. So by opening up the bid, A has been protected against any significant future variations in price.

By selling the contract in March, A has put himself in a situation where a can buy the future contracts in January to close his futures position at the time he sells its fruits in the cash market. Since there is close interaction of cash and futures and they both move in same way, any losses that are incurred in one market in January will be covered by gains in the other.

By selling a contract in March for delivery in FCOJ in January, A is selling something that he never intends to have or able to deliver. Being no future contracts on fruit, A trades FCOJ contract because the person knows that prices of fruit as well as FCOJ move in tandem. There is certainty that if fruit prices fall, FCOJ as well as prices of FCOJ contract will also fall. The success lies in the price variation of these two markets only. So the person A is relaxed as he is insured for any future calamity.

Now if the price of FCOJ contract in March was only $0.63 as compared to $3.2 per pounds, a will not hedge because the price offered in market is much below its production cost. A can also close out before the due date as there are only few contracts that result in actual delivery as scheduled. There is inherent advantage of closing a hedge due to convenience.

There can be possibility where a will close out his future position in January and sell oranges in fruit market. In the month of March, A set the hedge by selling the contract at $0.8 per pound. In January, he buys the futures contract to close his open position in the futures market and sell oranges in fruit market.

In the situation of hedging without physical delivery, A assumed the cash price of FCOJ in January to be $0.60 per box. A sold the futures contract in March for around $0.70 per pound that he now buys back at $0.60 per pound in January. As it is known that the contract nearing the maturity date, the storage costs will be zero and contract price is equal to the current cash price.

Therefore A gains $0.10 per pound on the future contract and is also able to sell its fruit for only the FCOJ that equals to $0.60 per pound. So the total gain that has been incurred to A and sales in cash market equals to $0.70 per pound, the price locked in by A in March.

The hedger in this case is the processor of FCOJ in the future markets. The processor has come in the market in order to buy an insurance to protect against the volatility in the prices market of oranges due to bad weather or crop failure.

The processor A of FCOJ can also use this future market in order to hedge his crop of orange in the market. In the month of March the person A has finished the harvest and now looks forward for another year. So considering an option of hedging at a future contract that matures in January next year, it is quoted at around $0.70 per ponds. He uses it for around $6 pounds per box that is equal to $4.2 per box. The person A estimates its production cost at around approximately $3.2 per box, so the processor will be pleased with the price that has been locked in to around $4.2 per box for the crop in next year.

But the problem lies in the contract as there are still around 9 months away from the actual harvest and there can be possibility of a freeze or crop failure in future. Because of this inherent risk, A will decide to hedge the next year crop of oranges in the month of March.

So the person a will open up the hedge with a price equal to $0.70 per pound by selling the January future contracts equal to the amount that is equal to his expected level of production. On the March day, the person a is making a promise of delivery in January according to the terms of the FCOJ contract at the price equal to $0.70 as expected in present context. By selling a contract equal to $0.70, A has assured himself a minimum price no matter what happens in January. So by opening up the bid, A has been protected against any significant future variations in price.

By selling the contract in March, A has put himself in a situation where a can buy the future contracts in January to close his futures position at the time he sells its fruits in the cash market. Since there is close interaction of cash and futures and they both move in same way, any losses that are incurred in one market in January will be covered by gains in the other.

By selling a contract in March for delivery in FCOJ in January, A is selling something that he never intends to have or able to deliver. Being no future contracts on fruit, A trades FCOJ contract because the person knows that prices of fruit as well as FCOJ move in tandem. There is certainty that if fruit prices fall, FCOJ as well as prices of FCOJ contract will also fall. The success lies in the price variation of these two markets only. So the person A is relaxed as he is insured for any future calamity.

Now if the price of FCOJ contract in March was only $0.63 as compared to $3.2 per pounds, a will not hedge because the price offered in market is much below its production cost. A can also close out before the due date as there are only few contracts that result in actual delivery as scheduled. There is inherent advantage of closing a hedge due to convenience.

There can be possibility where a will close out his future position in January and sell oranges in fruit market. In the month of March, A set the hedge by selling the contract at $0.8 per pound. In January, he buys the futures contract to close his open position in the futures market and sell oranges in fruit market.

In the situation of hedging without physical delivery, A assumed the cash price of FCOJ in January to be $0.60 per box. A sold the futures contract in March for around $0.70 per pound that he now buys back at $0.60 per pound in January. As it is known that the contract nearing the maturity date, the storage costs will be zero and contract price is equal to the current cash price.

Therefore A gains $0.10 per pound on the future contract and is also able to sell its fruit for only the FCOJ that equals to $0.60 per pound. So the total gain that has been incurred to A and sales in cash market equals to $0.70 per pound, the price locked in by A in March.

2

Clearly distinguish between the objectives of the speculator and the hedger. Which is more likely to closely follow prices of futures contracts after a position has been opened?

Speculators and hedgers both are the players of the future market. Future market is a market where buying and selling activities are not done by the buyer and seller simultaneously, in future market buyer and seller trade standardized future contracts.

The difference between the objectives of speculator and hedger is the bearing of risk.

Speculators are those who do not want to avoid the risk involved in the buying and selling of futures contracts. They want to grasp the profits from the risk involved in trading in future markets, and for that they want to buy the contract at less price and sell it at a higher price. They buy future contracts with the purpose to sale it in higher prices and not for the delivery purpose.

Hedgers are those who want to avoid risk of price variation while trading in future contracts. Their motive is to make profit by their actual business and not by the transaction in the future markets. Hedgers in the future market come to future market to protect themselves from the risk of price variation.

Speculators follows the price variation more closely than the hedgers because they are doing business in variation of price.they have to keep a check on price and have to look for the opportunity with their speculation skills to get higher profits. Hedgers by hedging avoid themselves form the risk involved but speculators have to deal with the risk to achieve higher profits and for that following price more closely is very important.

The difference between the objectives of speculator and hedger is the bearing of risk.

Speculators are those who do not want to avoid the risk involved in the buying and selling of futures contracts. They want to grasp the profits from the risk involved in trading in future markets, and for that they want to buy the contract at less price and sell it at a higher price. They buy future contracts with the purpose to sale it in higher prices and not for the delivery purpose.

Hedgers are those who want to avoid risk of price variation while trading in future contracts. Their motive is to make profit by their actual business and not by the transaction in the future markets. Hedgers in the future market come to future market to protect themselves from the risk of price variation.

Speculators follows the price variation more closely than the hedgers because they are doing business in variation of price.they have to keep a check on price and have to look for the opportunity with their speculation skills to get higher profits. Hedgers by hedging avoid themselves form the risk involved but speculators have to deal with the risk to achieve higher profits and for that following price more closely is very important.

3

One of the important things that makes futures markets work is the use of arbitrage by specula-tors. For wheat contracts within a single crop year the difference in prices for different maturity dates is equal to the carrying (i.e., storage) costs. A speculator knows that the usual carrying cost of wheat is about $0.02 per bushel per month plus a $0.02 per bushel placement fee. Therefore, one would expect the December wheat contract to be priced at the September contract plus $0.08. At present (in June), both contracts are trading at the exact same price, $3.75 per bushel. This presents an opportunity for temporal (i.e., across time) arbitrage.

a. Given this price abnormality, there is an opportunity for the speculator to profit from temporal arbitrage. The arbitrager would simultaneously make trades in the September and the December wheat futures markets. What position would be taken in each market?

b. What is the effect of these trades (and those of similar speculators) on the prices of the two contracts?

c. Assume that by August, the usual $0.08 spread between the September and December con-tracts has returned. If the price of the September contract has fallen to $3.50 per bushel and the speculator doses out both positions, what has he or she gained? d. Assume that by August, the usual $0.08 spread between the September and December con-tracts has returned. If the price of the September contract has risen to $3.90 per bushel and the speculator closes out both positions, what has he or she gained? Note that in this example, the speculator is speculating not on the price of wheat but on the price differential between the two different delivery months. Thus, the speculator makes markets efficient.

a. Given this price abnormality, there is an opportunity for the speculator to profit from temporal arbitrage. The arbitrager would simultaneously make trades in the September and the December wheat futures markets. What position would be taken in each market?

b. What is the effect of these trades (and those of similar speculators) on the prices of the two contracts?

c. Assume that by August, the usual $0.08 spread between the September and December con-tracts has returned. If the price of the September contract has fallen to $3.50 per bushel and the speculator doses out both positions, what has he or she gained? d. Assume that by August, the usual $0.08 spread between the September and December con-tracts has returned. If the price of the September contract has risen to $3.90 per bushel and the speculator closes out both positions, what has he or she gained? Note that in this example, the speculator is speculating not on the price of wheat but on the price differential between the two different delivery months. Thus, the speculator makes markets efficient.

Unlock Deck

Unlock for access to all 5 flashcards in this deck.

Unlock Deck

k this deck

4

In order to hedge effectively, the hedger must have knowledge about expected bases. Traders and brokers have tables that show what a typical basis is in any given month for a particular contract. Sam is a soybean farmer. In October he will harvest 5,000 bushels of soybeans(one contract.) Based on past experience he expects the basis on the December contract to be $0.08 in October. Tha is, December futures contract will trade in October for $0.08 more than the cash price in October.

In January (a slow time for soybean farmers), Sam notes that a December contract is trading at $7.80 per bushel. Sam figures his cost of production and returns to land to be $6.80 per bushel. SO, in January he hedges his crop. Show in the following how the hedge will work assuming two alternative October cash prices ($6.00 and $9.00 per bushel) and an October basis $0.08.

In January (a slow time for soybean farmers), Sam notes that a December contract is trading at $7.80 per bushel. Sam figures his cost of production and returns to land to be $6.80 per bushel. SO, in January he hedges his crop. Show in the following how the hedge will work assuming two alternative October cash prices ($6.00 and $9.00 per bushel) and an October basis $0.08.

Unlock Deck

Unlock for access to all 5 flashcards in this deck.

Unlock Deck

k this deck

5

(Note: this problem is a little more complicated than the examples given in the text because it includes the realities of basis in options valuation.) It is January, and the cash market price of corn is $6.00 per bushel. A futures contract for December delivery is $6.40, indicating a basis of $0.40. In checking prices on his computer, Edlef finds that he can buy a put option on a December futures contract with a strike price of $6.50 for a $0.35 per bushel premium. Now further assume that when Edlef harvests his corn in late October, the basis on the December futures contract has fallen to $0.10 per bushel.

a. Suppose that by harvest time, the cash price of corn has fallen to $4.00 per bushel. What are Edlef's total receipts from sales in the cash market and transactions in the options and futures markets? (Hint: the price of the December futures contract will be $4.10-Why?)

b. In the previous case, would Edlef have been better off if he had hedged than he was with a put option strategy? Why?

c. Suppose that by harvest time, the cash price of corn has risen to $8.00 per bushel. What are Edlef's total receipts from sales in the cash market and transactions in the options and futures markets?

d. In the previous case, would Edlef have been better off if he had hedged than he was with a put option strategy? Why?

a. Suppose that by harvest time, the cash price of corn has fallen to $4.00 per bushel. What are Edlef's total receipts from sales in the cash market and transactions in the options and futures markets? (Hint: the price of the December futures contract will be $4.10-Why?)

b. In the previous case, would Edlef have been better off if he had hedged than he was with a put option strategy? Why?

c. Suppose that by harvest time, the cash price of corn has risen to $8.00 per bushel. What are Edlef's total receipts from sales in the cash market and transactions in the options and futures markets?

d. In the previous case, would Edlef have been better off if he had hedged than he was with a put option strategy? Why?

Unlock Deck

Unlock for access to all 5 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 5 flashcards in this deck.