Deck 5: The Market for Foreign Exchange

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

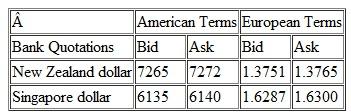

Given the following information, what are the NZD/SGD currency against currency bid-ask quotations

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Restate the following one-, three-, and six-month outright forward European term bid-ask quotes in forward points.

Question

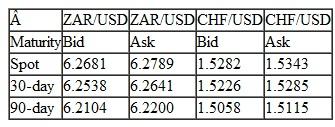

Omni Advisors, an international pension fund manager, plans to sell equities denominated in Swiss Francs (CHF) and purchase an equivalent amount of equities denominated in South African rands (ZAR).

Omni will realize net proceeds of 3 million CHF at the end of 30 days and wants to eliminate the risk that the ZAR will appreciate relative to the CHF during this 30-day period. The following exhibit shows current exchange rates between the ZAR, CHF, and the U.S. dollar (USD).

Currency Exchange Rates a.Describe the currency transaction that Omni should undertake to eliminate currency risk over the 30-day period.

a.Describe the currency transaction that Omni should undertake to eliminate currency risk over the 30-day period.

b.Calculate the following:

• The CHF/ZAR cross-currency rate Omni would use in valuing the Swiss equity portfolio.

• The current value of Omni's Swiss equity portfolio in ZAR.

• The annualized forward premium or discount at which the ZAR is trading versus the CHF.

Omni will realize net proceeds of 3 million CHF at the end of 30 days and wants to eliminate the risk that the ZAR will appreciate relative to the CHF during this 30-day period. The following exhibit shows current exchange rates between the ZAR, CHF, and the U.S. dollar (USD).

Currency Exchange Rates

a.Describe the currency transaction that Omni should undertake to eliminate currency risk over the 30-day period.b.Calculate the following:

• The CHF/ZAR cross-currency rate Omni would use in valuing the Swiss equity portfolio.

• The current value of Omni's Swiss equity portfolio in ZAR.

• The annualized forward premium or discount at which the ZAR is trading versus the CHF.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/23

Play

Full screen (f)

Deck 5: The Market for Foreign Exchange

1

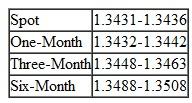

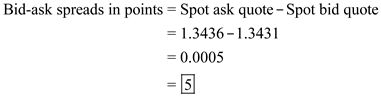

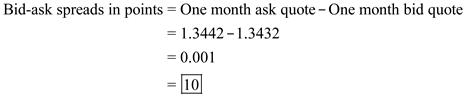

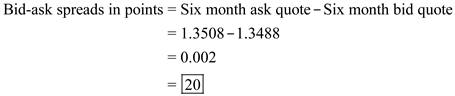

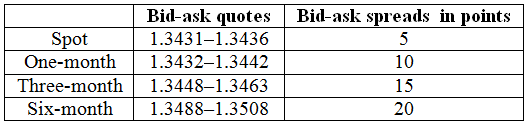

Using the spot and outright forward quotes in problem 4, determine the corresponding bid-ask spreads in points.

The spot bid-ask quote is 1.3431-1.3436. The one-month bid-ask quote is 1.3432-1.3442; three-month bid-ask quote is 1.3448-1.3463 and six-month bid-ask quote is 1.3488-1.3508.

The bid-ask spread is the difference between ask and bid quote. Calculate the bid-ask spreads in points as follows:

Calculate the bid-ask spreads in points for spot bid-ask quote as follows: Calculate the bid-ask spreads in points for one-month bid-ask quote as follows:

Calculate the bid-ask spreads in points for one-month bid-ask quote as follows:  Calculate the bid-ask spreads in points for three-month bid-ask quote as follows:

Calculate the bid-ask spreads in points for three-month bid-ask quote as follows:  Calculate the bid-ask spreads in points for six-month bid-ask quote as follows:

Calculate the bid-ask spreads in points for six-month bid-ask quote as follows:  Therefore, the bid-ask spread is as follows:

Therefore, the bid-ask spread is as follows:

The bid-ask spread is the difference between ask and bid quote. Calculate the bid-ask spreads in points as follows:

Calculate the bid-ask spreads in points for spot bid-ask quote as follows:

Calculate the bid-ask spreads in points for one-month bid-ask quote as follows: Calculate the bid-ask spreads in points for three-month bid-ask quote as follows: Calculate the bid-ask spreads in points for six-month bid-ask quote as follows: Therefore, the bid-ask spread is as follows: 2

What is meant by a currency trading at a discount or at a premium in the forward market

Market for foreign exchange

It is one of the biggest financial market in the world which operates 24 x 7. Turnover of the market increases with increase in transactions by other financial institutions which includes central banks, mutual funds, insurance companies, hedge funds etc. This market covers multiple operations like conversion of purchasing power of one currency into another, trading in foreign currency, foreign trade financing etc.

Forward exchange market

This market deals with the contracts done today to buy or sell foreign exchange in future.

Forward exchange price may be higher or lower than the spot prices. Forward exchange quotes are provided for various currencies and time frames or maturity periods.

Currency trading at premium or discount in forward market

Currency trading at discount means when in future the value of a currency depreciates in comparison to another currency. For example, it means that if Euro is trading in forward market at discount, then more Euro currency is needed to buy another currency CD.

Currency trading at premium means when in future the value of a currency appreciates in comparison to another currency. For example, it means that if Euro is trading in forward market at premium, then less Euro currency is needed to buy another currency CD.

It is one of the biggest financial market in the world which operates 24 x 7. Turnover of the market increases with increase in transactions by other financial institutions which includes central banks, mutual funds, insurance companies, hedge funds etc. This market covers multiple operations like conversion of purchasing power of one currency into another, trading in foreign currency, foreign trade financing etc.

Forward exchange market

This market deals with the contracts done today to buy or sell foreign exchange in future.

Forward exchange price may be higher or lower than the spot prices. Forward exchange quotes are provided for various currencies and time frames or maturity periods.

Currency trading at premium or discount in forward market

Currency trading at discount means when in future the value of a currency depreciates in comparison to another currency. For example, it means that if Euro is trading in forward market at discount, then more Euro currency is needed to buy another currency CD.

Currency trading at premium means when in future the value of a currency appreciates in comparison to another currency. For example, it means that if Euro is trading in forward market at premium, then less Euro currency is needed to buy another currency CD.

3

Using Exhibit 5.4, calculate the one-, three-, and six-month forward premium or discount for the Canadian dollar versus the U.S. dollar using American term quotations. For simplicity, assume each month has 30 days. What is the interpretation of your results

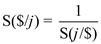

When a currency is to be traded with another currency, two general conventions are used, one the European terms in which an US Dollar ($) is expressed in terms of a foreign currency. This is given by  , where S is a function which expresses US Dollar in terms of the foreign currency ' j '. Similarly, in the second notation the foreign currency is expressed in term of US Dollar, known as the American terms, and is given by

, where S is a function which expresses US Dollar in terms of the foreign currency ' j '. Similarly, in the second notation the foreign currency is expressed in term of US Dollar, known as the American terms, and is given by  . The relation between these terms is given by

. The relation between these terms is given by  These are traded in money markets or foreign exchange markets and there is forward contract in which we get into a contract today for selling or buying a currency in the future. This forward rate could vary with the spot rate of the currency on the due date and is usually either higher or lower than the spot price. The forward rate for a currency ' j ' in terms of a currency ' k ', for a given duration ' N' is given by

These are traded in money markets or foreign exchange markets and there is forward contract in which we get into a contract today for selling or buying a currency in the future. This forward rate could vary with the spot rate of the currency on the due date and is usually either higher or lower than the spot price. The forward rate for a currency ' j ' in terms of a currency ' k ', for a given duration ' N' is given by  and can be calculated using the American terms as

and can be calculated using the American terms as  Or using the European terms as

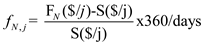

Or using the European terms as  The Premium or the discount for the forward contract is calculated using the formula

The Premium or the discount for the forward contract is calculated using the formula  From exhibit 5.4, we know that a 1-month forward cross exchange rate of a Canadian Dollar (CD) in terms of US Dollar is 0.9628 and the spot exchange rate is 0.9629. That is

From exhibit 5.4, we know that a 1-month forward cross exchange rate of a Canadian Dollar (CD) in terms of US Dollar is 0.9628 and the spot exchange rate is 0.9629. That is  and

and  . Therefore, the 1-month forward premium or discount for Canadian Dollar is given as:

. Therefore, the 1-month forward premium or discount for Canadian Dollar is given as:  0

0  1

1

From exhibit 5.4, we know that a 3-month forward cross exchange rate of a Canadian Dollar (CD) in terms of US Dollar is 0.9624 and the spot exchange rate is 0.9629. That is 2

2

and 3

3

. Therefore, the 3-month forward premium or discount for Canadian Dollar is given as: 4

4  5

5

From exhibit 5.4, we know that a 6-month forward cross exchange rate of a Canadian Dollar (CD) in terms of US Dollar is 0.9614 and the spot exchange rate is 0.9629. That is 6

6

and 7

7

. Therefore, the 1-month forward premium or discount for Canadian Dollar is given as: 8

8  9

9

Therefore, from the above calculations, the discount for the forward contracts is increasing with the duration of the contract. So, we can interpret that the longer the duration of the contract, higher is the discount on the contract.

, where S is a function which expresses US Dollar in terms of the foreign currency ' j '. Similarly, in the second notation the foreign currency is expressed in term of US Dollar, known as the American terms, and is given by . The relation between these terms is given by These are traded in money markets or foreign exchange markets and there is forward contract in which we get into a contract today for selling or buying a currency in the future. This forward rate could vary with the spot rate of the currency on the due date and is usually either higher or lower than the spot price. The forward rate for a currency ' j ' in terms of a currency ' k ', for a given duration ' N' is given by and can be calculated using the American terms as Or using the European terms as The Premium or the discount for the forward contract is calculated using the formula From exhibit 5.4, we know that a 1-month forward cross exchange rate of a Canadian Dollar (CD) in terms of US Dollar is 0.9628 and the spot exchange rate is 0.9629. That is and . Therefore, the 1-month forward premium or discount for Canadian Dollar is given as: 0 1From exhibit 5.4, we know that a 3-month forward cross exchange rate of a Canadian Dollar (CD) in terms of US Dollar is 0.9624 and the spot exchange rate is 0.9629. That is

2and

3. Therefore, the 3-month forward premium or discount for Canadian Dollar is given as:

4 5From exhibit 5.4, we know that a 6-month forward cross exchange rate of a Canadian Dollar (CD) in terms of US Dollar is 0.9614 and the spot exchange rate is 0.9629. That is

6and

7. Therefore, the 1-month forward premium or discount for Canadian Dollar is given as:

8 9Therefore, from the above calculations, the discount for the forward contracts is increasing with the duration of the contract. So, we can interpret that the longer the duration of the contract, higher is the discount on the contract.

4

Why does most interbank currency trading worldwide involve the U.S. dollar

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

5

Using Exhibit 5.4, calculate the one-, three-, and six-month forward premium or discount for the U.S. dollar versus the British pound using European term quotations. For simplicity, assume each month has 30 days. What is the interpretation of your results

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

6

Banks find it necessary to accommodate their clients' needs to buy or sell FX forward, in many instances for hedging purposes. How can the bank eliminate the currency exposure it has created for itself by accommodating a client's forward transaction

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

7

A bank is quoting the following exchange rates against the dollar for the Swiss franc and the Australian dollar:

SFr/$ = 1.5960--70

A$/$ = 1.7225--35

An Australian firm asks the bank for an A$/SFr quote. What cross-rate would the bank quote

SFr/$ = 1.5960--70

A$/$ = 1.7225--35

An Australian firm asks the bank for an A$/SFr quote. What cross-rate would the bank quote

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

8

A CD/$ bank trader is currently quoting a small figure bid-ask of 35-40, when the rest of the market is trading at CD1.3436-CD1.3441. What is implied about the trader's beliefs by his prices

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

9

Using the American term quotes from Exhibit 5.4, calculate a cross-rate matrix for the euro, Swiss franc, Japanese yen, and the British pound so that the resulting triangular matrix is similar to the portion above the diagonal in Exhibit 5.6.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

10

Given the following information, what are the NZD/SGD currency against currency bid-ask quotations

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

11

Give a full definition of the market for foreign exchange.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

12

What is triangular arbitrage What is a condition that will give rise to a triangular arbitrage opportunity

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

13

Using the American term quotes from Exhibit 5.4, calculate the one-, three-, and six-month forward cross-exchange rates between the Canadian dollar and the Swiss franc. State the forward cross-rates in "Canadian" terms.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

14

Doug Bernard specializes in cross-rate arbitrage. He notices the following quotes:

Swiss franc/dollar = SFr1.5971$

Australian dollar/U.S. dollar = A$1.8215/$

Australian dollar/Swiss franc = A$1.1440/SFr

Ignoring transaction costs, does Doug Bernard have an arbitrage opportunity based on these quotes If there is an arbitrage opportunity, what steps would he take to make an arbitrage profit, and how would he profit if he has $1,000,000 available for this purpose.

Swiss franc/dollar = SFr1.5971$

Australian dollar/U.S. dollar = A$1.8215/$

Australian dollar/Swiss franc = A$1.1440/SFr

Ignoring transaction costs, does Doug Bernard have an arbitrage opportunity based on these quotes If there is an arbitrage opportunity, what steps would he take to make an arbitrage profit, and how would he profit if he has $1,000,000 available for this purpose.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

15

What is the difference between the retail or client market and the wholesale or interbank market for foreign exchange

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

16

Over the past five years, the exchange rate between British pound and U.S. dollar, $/£, has changed from about 1.90 to about 1.45. Would you agree that over this five-year period that British goods have become cheaper for buyers in the United States

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

17

A foreign exchange trader with a U.S. bank took a short position of £5,000,000 when the $/£ exchange rate was 1.55. Subsequently, the exchange rate has changed to 1.61. Is this movement in the exchange rate good from the point of view of the position taken by the trader By how much has the bank's liability changed because of the change in the exchange rate

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

18

Assume you are a trader with Deutsche Bank. From the quote screen on your computer terminal, you notice that Dresdner Bank is quoting €0.7627/$1.00 and Credit Suisse is offering SF1.1806/$1.00. You learn that UBS is making a direct market between the Swiss franc and the euro, with a current €/SF quote of.6395. Show how you can make a triangular arbitrage profit by trading at these prices. (Ignore bid-ask spreads for this problem.) Assume you have $5,000,000 with which to conduct the arbitrage. What happens if you initially sell dollars for Swiss francs What €/SF price will eliminate triangular arbitrage

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

19

Who are the market participants in the foreign exchange market

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

20

The current spot exchange rate is $1.95/£ and the three-month forward rate is $1.90/£. Based on your analysis of the exchange rate, you are pretty confident that the spot exchange rate will be $1.92/£ in three months. Assume that you would like to buy or sell £1,000,000.

a.What actions do you need to take to speculate in the forward market What is the expected dollar profit from speculation

b.What would be your speculative profit in dollar terms if the spot exchange rate actually turns out to be $1.86/£.

a.What actions do you need to take to speculate in the forward market What is the expected dollar profit from speculation

b.What would be your speculative profit in dollar terms if the spot exchange rate actually turns out to be $1.86/£.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

21

Restate the following one-, three-, and six-month outright forward European term bid-ask quotes in forward points.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

22

Omni Advisors, an international pension fund manager, plans to sell equities denominated in Swiss Francs (CHF) and purchase an equivalent amount of equities denominated in South African rands (ZAR).

Omni will realize net proceeds of 3 million CHF at the end of 30 days and wants to eliminate the risk that the ZAR will appreciate relative to the CHF during this 30-day period. The following exhibit shows current exchange rates between the ZAR, CHF, and the U.S. dollar (USD).

Currency Exchange Rates a.Describe the currency transaction that Omni should undertake to eliminate currency risk over the 30-day period.

b.Calculate the following:

• The CHF/ZAR cross-currency rate Omni would use in valuing the Swiss equity portfolio.

• The current value of Omni's Swiss equity portfolio in ZAR.

• The annualized forward premium or discount at which the ZAR is trading versus the CHF.

Omni will realize net proceeds of 3 million CHF at the end of 30 days and wants to eliminate the risk that the ZAR will appreciate relative to the CHF during this 30-day period. The following exhibit shows current exchange rates between the ZAR, CHF, and the U.S. dollar (USD).

Currency Exchange Rates

a.Describe the currency transaction that Omni should undertake to eliminate currency risk over the 30-day period.b.Calculate the following:

• The CHF/ZAR cross-currency rate Omni would use in valuing the Swiss equity portfolio.

• The current value of Omni's Swiss equity portfolio in ZAR.

• The annualized forward premium or discount at which the ZAR is trading versus the CHF.

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

23

How are foreign exchange transactions between international banks settled

Unlock Deck

Unlock for access to all 23 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 23 flashcards in this deck.