Deck 6: Accounting for General Long-Term Liabilities and Debt Service

Full screen (f)

Question

Question

Question

Question

Question

Question

Multiple Choice.Choose the best answer. 1.Which of the following would not be considered a general long-term liability

A)The estimated liability to clean up the fuel and hazard waste storage sites of the city's Public Works Department.

B)Capitalized equipment leases of the water utility fund.

C)Compensated absences for the city's Police Department.

D)Five-year notes payable used to acquire computer equipment for the city library.

2)Proceeds from bonds issued to construct a new county jail would most likely be recorded in the journal of the:

A)Capital projects fund.

B)Debt service fund.

C)General Fund.

D)Enterprise fund.

3)The long-term liability for a bond issue used to construct a new city recreation center should be recorded in the:

A)Capital projects fund general journal.

B)Debt service fund general journal.

C)Governmental activities general journal.

D)Both b and c.

Items 4 and 5 are based on the following information:

On March 2, 2010, 20-year, 6 percent, general obligation serial bonds were issued at the face amount of $3,000,000.Interest of 6 percent per annum is due semiannually on March 1 and September 1.The first payment of $150,000 for redemption of principal is due on March 1, 2011.Fiscal year-end occurs on December 31.

4)What is the interest expense for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

5)What is the interest expenditure for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

6)Debt service funds may be used to account for all of the following except:

A)Repayment of debt principal.

B)Lease payments under capital leases.

C)Amortization of premiums on bonds payable.

D)The proceeds of refunding bond issues.

7)Expenditures for redemption of principal of tax-supported bonds payable should be recorded in a debt service fund:

A)When the bonds are issued.

B)When the bond principal is legally due.

C)When the redemption checks are written.

D)Any of the above, if consistently followed.

8)Which of the following items would be reported in the Governmental Activities column of the government-wide financial statements

9.Interest on general long-term debt would be recorded as an expenditure in which of the following financial statements

9.Interest on general long-term debt would be recorded as an expenditure in which of the following financial statements

A)Statement of revenues, expenditures, and changes in fund balances- governmental funds.

B)Statement of activities.

C)Both a and b are correct.

D)None of the above; interest is recorded as an expense, not an expenditure.

10)Which of the following accounts is unlikely to appear in a debt service fund ledger

A)Estimated Revenue.

B)Appropriations.

C)Estimated Other Financing Sources.

D)Encumbrances.

A)The estimated liability to clean up the fuel and hazard waste storage sites of the city's Public Works Department.

B)Capitalized equipment leases of the water utility fund.

C)Compensated absences for the city's Police Department.

D)Five-year notes payable used to acquire computer equipment for the city library.

2)Proceeds from bonds issued to construct a new county jail would most likely be recorded in the journal of the:

A)Capital projects fund.

B)Debt service fund.

C)General Fund.

D)Enterprise fund.

3)The long-term liability for a bond issue used to construct a new city recreation center should be recorded in the:

A)Capital projects fund general journal.

B)Debt service fund general journal.

C)Governmental activities general journal.

D)Both b and c.

Items 4 and 5 are based on the following information:

On March 2, 2010, 20-year, 6 percent, general obligation serial bonds were issued at the face amount of $3,000,000.Interest of 6 percent per annum is due semiannually on March 1 and September 1.The first payment of $150,000 for redemption of principal is due on March 1, 2011.Fiscal year-end occurs on December 31.

4)What is the interest expense for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

5)What is the interest expenditure for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

6)Debt service funds may be used to account for all of the following except:

A)Repayment of debt principal.

B)Lease payments under capital leases.

C)Amortization of premiums on bonds payable.

D)The proceeds of refunding bond issues.

7)Expenditures for redemption of principal of tax-supported bonds payable should be recorded in a debt service fund:

A)When the bonds are issued.

B)When the bond principal is legally due.

C)When the redemption checks are written.

D)Any of the above, if consistently followed.

8)Which of the following items would be reported in the Governmental Activities column of the government-wide financial statements

9.Interest on general long-term debt would be recorded as an expenditure in which of the following financial statementsA)Statement of revenues, expenditures, and changes in fund balances- governmental funds.

B)Statement of activities.

C)Both a and b are correct.

D)None of the above; interest is recorded as an expense, not an expenditure.

10)Which of the following accounts is unlikely to appear in a debt service fund ledger

A)Estimated Revenue.

B)Appropriations.

C)Estimated Other Financing Sources.

D)Encumbrances.

Question

Question

Question

Question

Question

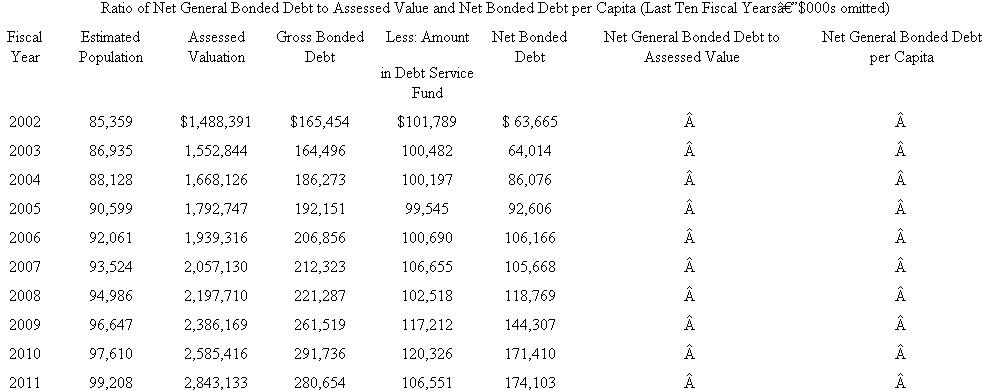

Assessing General Obligation Debt Burden.This case focuses on the analysis of a city's general obligation debt burden.After examining the accompanying table that shows a city's general obligation (tax-supported) debt for the last ten fiscal years, answer the following questions.

Required

a.What is your initial assessment of the trend of the city's general obligation debt burden

b.Complete the table by calculating the ratio of Net General Bonded Debt to Assessed Value of taxable property and the ratio of Net General Bonded Debt per Capita.In addition, you learn that the average ratio of Net General Bonded Debt to Assessed Value for comparable-size cities in 2011 was 2.13 percent, and the average net general bonded debt per capita was $1,256.Based on time series analysis of the ratios you have calculated and the benchmark information provided in this paragraph, is your assessment of the city's general obli-gation still the same as it was in part a, or has it changed Explain.

Source: Adapted from City of Fargo, North Dakota, Comprehensive Annual Financial Report, 2006.

Source: Adapted from City of Fargo, North Dakota, Comprehensive Annual Financial Report, 2006.

Required

a.What is your initial assessment of the trend of the city's general obligation debt burden

b.Complete the table by calculating the ratio of Net General Bonded Debt to Assessed Value of taxable property and the ratio of Net General Bonded Debt per Capita.In addition, you learn that the average ratio of Net General Bonded Debt to Assessed Value for comparable-size cities in 2011 was 2.13 percent, and the average net general bonded debt per capita was $1,256.Based on time series analysis of the ratios you have calculated and the benchmark information provided in this paragraph, is your assessment of the city's general obli-gation still the same as it was in part a, or has it changed Explain.

Source: Adapted from City of Fargo, North Dakota, Comprehensive Annual Financial Report, 2006. Question

Question

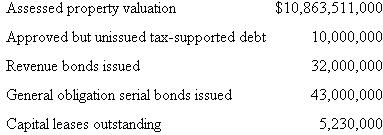

The debt limit for general obligation debt for Milos City is 1 percent of the assessed property valuation for the city.Using the following information, calculate the city's debt margin.

Question

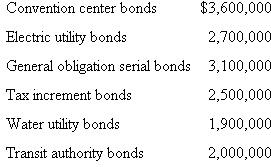

Statement of Legal Debt Margin.In preparation for a proposed bond sale, the city manager of the City of Appleton requested that you prepare a statement of legal debt margin for the city as of December 31, 2010.You ascertain that the following bond issues are outstanding on that date:

You obtain other information that includes the following items:

You obtain other information that includes the following items:

1.Assessed valuation of real and taxable personal property in the city totaled $240,000,000.

2.The rate of debt limitation applicable to the City of Appleton was 8 percent of total real and taxable personal property valuation.

3.Electric utility, water utility, and transit authority bonds were all serviced by enterprise revenues, but each carries a full-faith-and-credit contingency provision.By law, such self-supporting debt is not subject to debt limitation.

4.The convention center bonds and tax increment bonds are subject to debt limitation.

5.The amount of assets segregated for debt retirement at December 31, 2010, is $1,800,000.

You obtain other information that includes the following items:1.Assessed valuation of real and taxable personal property in the city totaled $240,000,000.

2.The rate of debt limitation applicable to the City of Appleton was 8 percent of total real and taxable personal property valuation.

3.Electric utility, water utility, and transit authority bonds were all serviced by enterprise revenues, but each carries a full-faith-and-credit contingency provision.By law, such self-supporting debt is not subject to debt limitation.

4.The convention center bonds and tax increment bonds are subject to debt limitation.

5.The amount of assets segregated for debt retirement at December 31, 2010, is $1,800,000.

Question

Question

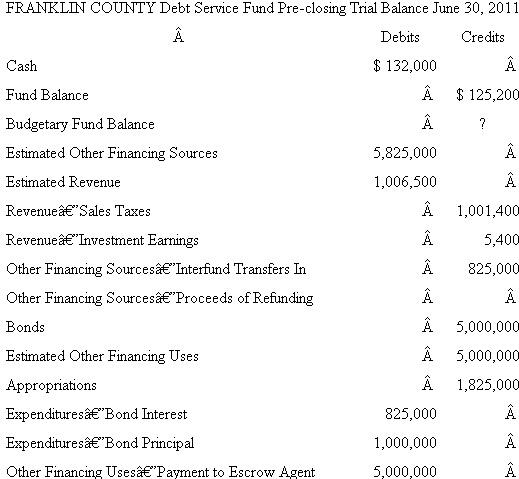

Debt Service Fund Trial Balance.Following is Franklin County's debt service fund pre-closing trial balance for the fiscal year ended June 30, 2011.

Required

Required

Using information provided by the trial balance, answer the following.

a.Assuming the budget was not amended, what was the budgetary journal entry recorded at the beginning of the fiscal year

b.What is the budgetary fund balance

c.Did the debt service fund pay debt obligations related to capital leases Explain.

d.Did the debt service fund perform a debt refunding Explain.

e.Prepare a statement of revenues, expenditures, and changes in fund balance for the debt service fund for the year ended June 30, 2011.

Required Using information provided by the trial balance, answer the following.

a.Assuming the budget was not amended, what was the budgetary journal entry recorded at the beginning of the fiscal year

b.What is the budgetary fund balance

c.Did the debt service fund pay debt obligations related to capital leases Explain.

d.Did the debt service fund perform a debt refunding Explain.

e.Prepare a statement of revenues, expenditures, and changes in fund balance for the debt service fund for the year ended June 30, 2011.

Question

Question

Question

Question

Question

Question

Question

Question

Comprehensive Capital Assets/Serial Bond Problem.Transaction data related to the City of Chambers's issuance of serial bonds to finance street and park improvements follow.Utilizing worksheets formatted as shown at the end of the problem, prepare all necessary journal entries for these transactions in the city's capital projects fund, debt service fund, and governmental activities at the government-wide level.You may ignore related entries in the General Fund.Round all amounts to the nearest whole dollar.

a.On July 1, 2010, the first day of its fiscal year, the City of Chambers issued serial bonds with a face value totaling $5,000,000 and having maturities ranging from one to 20 years to make certain street and park improvements.The bonds were issued at 102 and bear interest of 5 percent per annum, payable semiannually on January 1 and July 1, with the first payment due on January 1, 2011.The first installment of principal in the amount of $250,000 is due on July 1, 2011.Premiums on bonds issued must be deposited directly in the debt service fund and be used for payment of bond interest.Premiums are amortized using the straight-line method in the governmental activities journal but are not amortized in the debt service fund.Debt service for the serial bonds will be provided by a one-quarter-cent city sales tax imposed on every dollar of sales in the city.

(1) Record the FY 2011 budget for the Serial Bond Debt Service Fund, utilizing worksheets formatted as shown at the end of this problem.The city estimates that the sales tax will generate $440,000 in FY 2011.An appropriation needs to be provided only for the interest payment due on January 1, 2011.

(2) Record the issuance of the bonds, again utilizing your worksheets.

b.On August 2, 2010, the city entered into a $4,800,000 contract with Central Paving and Construction.Work on street and park improvement projects is expected to begin immediately and continue until August 2011.

c.On August 10, 2010, the capital project fund paid the city's Utility Fund $42,000 for relocating power lines and poles to facilitate street widening.No encumbrance had been recorded for this service.

d.On August 20, 2010, the city's Public Works Department billed the capital projects fund $30,000 for engineering and other design assistance.This amount was paid.

e.Street and park improvement sales taxes for debt service of $248,000 were collected in the six months ending December 31, 2010.

f.On January 1, 2011, the city mailed checks to bondholders for semiannual interest on the bonds.

g.On January 15, 2011, Central Paving and Construction submitted a billing to the city for $2,500,000.The city's public works inspector agrees that all milestones have been met for this portion of the work.

h.On February 2, 2011, the city paid Central Paving and Construction the amount it had billed, except for 4 percent that was withheld as a retained percentage per terms of the contract.

i.During the six months ended June 30, 2011, sales tax collections for debt service amounted to $194,600.

j.Make all appropriate adjusting and closing entries at June 30, 2011, the end of the fiscal year.Based on authorization from the Public Works Department, $1,650,000 of construction work in progress was reclassified as infrastructure and another $250,000 was reclassified as improvements other than buildings.(Ignore closing entry for governmental activities.)k.Reestablish the Encumbrances account balance in the capital projects fund effective July 1, 2011.

l.Record the FY 2012 budget for the debt service fund, assuming sales revenues are estimated at $492,000.m.

m.On July 1, 2011, the city mailed checks totaling $125,000 to all bondholders for semiannual interest and $250,000 to holders of record for bonds being redeemed.

n.On August 14, 2011, Central Paving and Construction submitted a final billing to the city for $2,300,000.o.

o.On August 23, 2011, the city paid the August 14 billing, except for a 4 percent retained percentage.

p.Upon final inspection by the Public Works Department, it was discovered that the contractor had failed to provide all required landscaping and certain other work for the street and park improvements.Public works employees completed this work at a total cost of $210,000.This amount was transferred to the General Fund using all retained cash and other cash of the capital projects fund.

q.The balance of the Construction Work in Progress account was reclassified as $150,000 to Improvements Other Than Buildings and the remainder to Infrastructure.

r.All remaining cash in the capital projects fund was transferred to the debt service fund and all accounts of the capital projects fund were closed.

a.On July 1, 2010, the first day of its fiscal year, the City of Chambers issued serial bonds with a face value totaling $5,000,000 and having maturities ranging from one to 20 years to make certain street and park improvements.The bonds were issued at 102 and bear interest of 5 percent per annum, payable semiannually on January 1 and July 1, with the first payment due on January 1, 2011.The first installment of principal in the amount of $250,000 is due on July 1, 2011.Premiums on bonds issued must be deposited directly in the debt service fund and be used for payment of bond interest.Premiums are amortized using the straight-line method in the governmental activities journal but are not amortized in the debt service fund.Debt service for the serial bonds will be provided by a one-quarter-cent city sales tax imposed on every dollar of sales in the city.

(1) Record the FY 2011 budget for the Serial Bond Debt Service Fund, utilizing worksheets formatted as shown at the end of this problem.The city estimates that the sales tax will generate $440,000 in FY 2011.An appropriation needs to be provided only for the interest payment due on January 1, 2011.

(2) Record the issuance of the bonds, again utilizing your worksheets.

b.On August 2, 2010, the city entered into a $4,800,000 contract with Central Paving and Construction.Work on street and park improvement projects is expected to begin immediately and continue until August 2011.

c.On August 10, 2010, the capital project fund paid the city's Utility Fund $42,000 for relocating power lines and poles to facilitate street widening.No encumbrance had been recorded for this service.

d.On August 20, 2010, the city's Public Works Department billed the capital projects fund $30,000 for engineering and other design assistance.This amount was paid.

e.Street and park improvement sales taxes for debt service of $248,000 were collected in the six months ending December 31, 2010.

f.On January 1, 2011, the city mailed checks to bondholders for semiannual interest on the bonds.

g.On January 15, 2011, Central Paving and Construction submitted a billing to the city for $2,500,000.The city's public works inspector agrees that all milestones have been met for this portion of the work.

h.On February 2, 2011, the city paid Central Paving and Construction the amount it had billed, except for 4 percent that was withheld as a retained percentage per terms of the contract.

i.During the six months ended June 30, 2011, sales tax collections for debt service amounted to $194,600.

j.Make all appropriate adjusting and closing entries at June 30, 2011, the end of the fiscal year.Based on authorization from the Public Works Department, $1,650,000 of construction work in progress was reclassified as infrastructure and another $250,000 was reclassified as improvements other than buildings.(Ignore closing entry for governmental activities.)k.Reestablish the Encumbrances account balance in the capital projects fund effective July 1, 2011.

l.Record the FY 2012 budget for the debt service fund, assuming sales revenues are estimated at $492,000.m.

m.On July 1, 2011, the city mailed checks totaling $125,000 to all bondholders for semiannual interest and $250,000 to holders of record for bonds being redeemed.

n.On August 14, 2011, Central Paving and Construction submitted a final billing to the city for $2,300,000.o.

o.On August 23, 2011, the city paid the August 14 billing, except for a 4 percent retained percentage.

p.Upon final inspection by the Public Works Department, it was discovered that the contractor had failed to provide all required landscaping and certain other work for the street and park improvements.Public works employees completed this work at a total cost of $210,000.This amount was transferred to the General Fund using all retained cash and other cash of the capital projects fund.

q.The balance of the Construction Work in Progress account was reclassified as $150,000 to Improvements Other Than Buildings and the remainder to Infrastructure.

r.All remaining cash in the capital projects fund was transferred to the debt service fund and all accounts of the capital projects fund were closed.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/24

Play

Full screen (f)

Deck 6: Accounting for General Long-Term Liabilities and Debt Service

1

How are general long-term liabilities distinguished from other long-term liabilities of the government How does the financial reporting of general long-term liabilities differ from the financial reporting of other long-term liabilities

General long-term liabilities arise from activities of the General Fund or some other governmental fund. These liabilities are distinguished from "fund" long-term liabilities that are incurred by a proprietary or fiduciary fund and for which debt service will be paid from that fund. General long-term liabilities are reported only in the Governmental Activities column of the government-wide financial statements and not in any fund.

2

Policy Issue: Who Should Pay for Neighborhood Improvements Related Accounting Issues.

Facts: Pursuant to its capital improvement plan, the City of Kirkland decided to make certain improvements to Oak Ridge Street, a residential thoroughfare located in the northern part of the city.Specifically, the project entailed purchasing 20 feet at the front of all private properties fronting the street to facilitate widening of the street from two to four lanes and adding sidewalks.The project was expected to cost $5 million.

After extensive and often contentious hearing presentations involving property owners, the public works director, city planners, and the city attorney, the city council decided that property owners fronting on Oak Ridge Street would be the primary beneficiaries of the street-widening project.Accordingly, as permitted by state law, the city council formed the Oak Ridge Special Improvement District and approved the issuance of $5 million in special assessment bonds to be repaid from special assessment levies on the Oak Ridge Street property owners.To reduce interest rates on the debt, the city agreed to make the bonds general obligations of the city should property owners default on debt service payments.

After the bonds had been issued and the project was well under way, all Oak Ridge Street property owners retained a local law firm and sued the City of Kirk-land to make the street-widening project a publicly funded project of the city rather than a special assessment project.Attorneys for property owners argued in briefs filed with the court that (1) the property owners will not benefit from the street improvements and, in fact, had fought the project for years since they would lose valuable property and the street would be transformed from a quiet, low-density, mainly local traffic street to a noisy, high-density public thoroughfare, and (2) the property owners were not adequately informed about the special assessment financing for the project before the financing was approved and the bonds were issued.

The city attorney filed a brief with the court laying out the city's reasoning for financing the street-widening project with special assessment bonds, essentially arguing that the Oak Ridge Street Project is no different from many past city neighborhood improvement projects that have been financed with special assessments.According to the city attorney, there is strong legal precedent for requiring property owners who receive private benefit to pay for such improvements.

Required

a.Assume you are the judge in this case.After analyzing the facts of this case, decide what remedies, if any, you will order for the plaintiffs (the property owners).Prepare a written brief explaining your reasoning and verdict.

b.How would accounting for the bond issuance, street construction, and debt service differ if you (the judge) were to rule for the plaintiffs and thus require the city to repay the project bonds from tax revenues rather than from special assessments How would accounting differ if you were to rule against the plaintiffs (assuming the city had not pledged to be secondarily liable for the bonds)

Facts: Pursuant to its capital improvement plan, the City of Kirkland decided to make certain improvements to Oak Ridge Street, a residential thoroughfare located in the northern part of the city.Specifically, the project entailed purchasing 20 feet at the front of all private properties fronting the street to facilitate widening of the street from two to four lanes and adding sidewalks.The project was expected to cost $5 million.

After extensive and often contentious hearing presentations involving property owners, the public works director, city planners, and the city attorney, the city council decided that property owners fronting on Oak Ridge Street would be the primary beneficiaries of the street-widening project.Accordingly, as permitted by state law, the city council formed the Oak Ridge Special Improvement District and approved the issuance of $5 million in special assessment bonds to be repaid from special assessment levies on the Oak Ridge Street property owners.To reduce interest rates on the debt, the city agreed to make the bonds general obligations of the city should property owners default on debt service payments.

After the bonds had been issued and the project was well under way, all Oak Ridge Street property owners retained a local law firm and sued the City of Kirk-land to make the street-widening project a publicly funded project of the city rather than a special assessment project.Attorneys for property owners argued in briefs filed with the court that (1) the property owners will not benefit from the street improvements and, in fact, had fought the project for years since they would lose valuable property and the street would be transformed from a quiet, low-density, mainly local traffic street to a noisy, high-density public thoroughfare, and (2) the property owners were not adequately informed about the special assessment financing for the project before the financing was approved and the bonds were issued.

The city attorney filed a brief with the court laying out the city's reasoning for financing the street-widening project with special assessment bonds, essentially arguing that the Oak Ridge Street Project is no different from many past city neighborhood improvement projects that have been financed with special assessments.According to the city attorney, there is strong legal precedent for requiring property owners who receive private benefit to pay for such improvements.

Required

a.Assume you are the judge in this case.After analyzing the facts of this case, decide what remedies, if any, you will order for the plaintiffs (the property owners).Prepare a written brief explaining your reasoning and verdict.

b.How would accounting for the bond issuance, street construction, and debt service differ if you (the judge) were to rule for the plaintiffs and thus require the city to repay the project bonds from tax revenues rather than from special assessments How would accounting differ if you were to rule against the plaintiffs (assuming the city had not pledged to be secondarily liable for the bonds)

a.We recommend that the substance of a student's brief be emphasized more than its form. The key issues that students should identify in this case are: (1) Should property owners have to bear the full cost burden for improvements that have public as well as private benefit (2) Should the government have the power to create a special improvement district without approval of a majority of affected property owners As in any ambiguous situation involving subjective evaluation, students' may reach different verdicts. So, each student's work should be assessed on the quality of analysis and how well he or she supports his/her verdict, rather than on the verdict itself.

Verdict: In the verdict on which this case is based, the court ruled for the plaintiffs on the grounds that the city failed to show that property owners benefited substantially from the street widening project. Further, the project was found to have significant public benefit; therefore, the judge ordered the city to use public taxes to pay a majority of the cost of the project.

As a result of this case, the city adopted a new and, many would argue, fairer policy for financing future capital projects that provide both public and private benefit. Further, the revised city ordinance requires a public hearing for all special assessment and other public improvement projects, as well as public notification in local newspapers.

b.If, as in this case, the government provides secondary backing for special assessment bonds, then accounting and financial reporting are not affected by who pays the debt service on the project. Issuance of the bonds is recorded as an other financing source in the capital projects fund and as general long-term liabilities at the government-wide level, regardless of who pays debt service on the bonds. Moreover, capital projects fund accounting and reporting for street construction would not be affected by the verdict.

Even debt service fund accounting is unaffected by the verdict since the city had agreed to make the bonds general obligations of the city should property owners default on special assessments. If, however, the special assessment bonds did not have the secondary backing of the city and the court did not rule for the plaintiffs, then accounting and reporting would be very different. In the capital projects fund, the change would be minor-titling the other financing source as "Contributions from Property Owners" rather than "Proceeds of Bonds." In this changed scenario, the liability for the bond issue would not be recorded at the government-wide level as the city has no obligation for the debt. In addition, all debt service activities would be reported in an agency fund (see Chapter 8 for more discussion.) All of this is academic, however, since the court did rule for the plaintiffs, which essentially converts the project into a normal capital project, accounted for and reported as described in this chapter.

Verdict: In the verdict on which this case is based, the court ruled for the plaintiffs on the grounds that the city failed to show that property owners benefited substantially from the street widening project. Further, the project was found to have significant public benefit; therefore, the judge ordered the city to use public taxes to pay a majority of the cost of the project.

As a result of this case, the city adopted a new and, many would argue, fairer policy for financing future capital projects that provide both public and private benefit. Further, the revised city ordinance requires a public hearing for all special assessment and other public improvement projects, as well as public notification in local newspapers.

b.If, as in this case, the government provides secondary backing for special assessment bonds, then accounting and financial reporting are not affected by who pays the debt service on the project. Issuance of the bonds is recorded as an other financing source in the capital projects fund and as general long-term liabilities at the government-wide level, regardless of who pays debt service on the bonds. Moreover, capital projects fund accounting and reporting for street construction would not be affected by the verdict.

Even debt service fund accounting is unaffected by the verdict since the city had agreed to make the bonds general obligations of the city should property owners default on special assessments. If, however, the special assessment bonds did not have the secondary backing of the city and the court did not rule for the plaintiffs, then accounting and reporting would be very different. In the capital projects fund, the change would be minor-titling the other financing source as "Contributions from Property Owners" rather than "Proceeds of Bonds." In this changed scenario, the liability for the bond issue would not be recorded at the government-wide level as the city has no obligation for the debt. In addition, all debt service activities would be reported in an agency fund (see Chapter 8 for more discussion.) All of this is academic, however, since the court did rule for the plaintiffs, which essentially converts the project into a normal capital project, accounted for and reported as described in this chapter.

3

Examine the CAFR.Utilizing the comprehensive annual financial report (CAFR) obtained for Exercise 1-1, follow the instructions below.

a.General Long-term Liabilities.

(1) Disclosure of Long-term Debt.Does the report contain evidence that the government has general long-term liabilities What evidence is there Does the report specify that no such debt is outstanding, or does it include a list of outstanding tax-supported debt issues; capital lease obligations; claims, judgments, and compensated absence payments to be made in future years; and unfunded pension obligations

Refer to the enterprise funds statement of net assets as well as note disclosures for long-term liabilities.Are any enterprise debt issues backed by the full faith and credit of the general government If so, how are the primary liability and the contingent liability disclosed

(2) Changes in Long-term Liabilities.How are changes in long-term liabilities during the year disclosed Is there a disclosure schedule for long-term liabilities similar to Illustration 6-1 Does the information in that schedule agree with the statements presented for capital projects funds and debt service funds and the government-wide financial statements

Are interest payments and principal payments due in future years disclosed If so, does the report relate these future payments with resources to be made available under existing debt service laws and covenants

(3) Debt Limitations.Does the report contain information as to legal debt limit and legal debt margin If so, is the information contained in the report explained in enough detail so that an intelligent reader (you) can understand how the limit is set, what debt is subject to it, and how much debt the government might legally issue in the year following the date of the report

(4) Overlapping Debt.Does the report disclose direct debt and overlapping debt of the reporting entity What disclosures of debt of the primary government are made in distinction to debt of component units Is debt of component units reported as "direct" debt of the reporting entity or as "overlapping debt"

b.Debt Service Funds.

(1) Debt Service Function.How is the debt service function for tax-supported debt and special assessment debt handled-by the General Fund, by a special revenue fund, or by one or more debt service funds If there is more than one debt service fund, what kinds of bond issues or other debt instruments are serviced by each fund Is debt service for bonds to be retired from enterprise revenues reported by enterprise funds

Does the report state the basis of accounting used for debt service funds If so, is the financial statement presentation consistent with the stated basis If the basis of accounting is not stated, analyze the statements to determine which basis is used-full accrual, modified accrual, or cash basis.Is the basis used consistent with the standards discussed in this chapter

(2) Investment Activity.Compare the net assets reserved for debt service, if any, in the Governmental Activities column of the government-wide statement of net assets and the fund balance of each debt service fund at balance sheet date with the amount of interest and the amount of debt principal the fund will be required to pay early in the following year (you may find debt service requirements in the notes to the financial statements or in supplementary schedules following the individual fund statements in the Financial Section of the CAFR).If debt service funds have accumulated assets in excess of amounts needed within a few days after the end of the fiscal year, are the excess assets invested Does the CAFR contain a schedule or list of investments of debt service funds Does the report disclose increases or decreases in the fair value of investments realized during the year Does the report disclose net earnings on investments during the year What percentage of revenue of each debt service fund is derived from earnings on investments What percentage of the revenue of each debt service fund is derived from taxes levied directly for the debt service fund What percentage is derived from transfers from other funds List any other sources of debt service revenue and other financing sources, and indicate the relative importance of each source.

Are estimated revenues for term bond debt service budgeted on an actuarial basis If so, are revenues received as required by the actuarial computations

(3) Management.Considering the debt maturity dates as well as the amount of debt and apparent quality of debt service fund investments, does the debt service activity appear to be properly managed Does the report disclose whether investments are managed by a corporate fiduciary, another outside investment manager, or governmental employees If outside investment managers are employed, is the basis of their fees disclosed Are the fees accounted for as additions to the cost of investments or as expenditures

Is one or more paying agents, or fiscal agents, employed If so, does the report disclose whether the agents keep track of the ownership of registered bonds, write checks to bondholders for interest payments and matured bonds or, in the case of coupon bonds, pay matured coupons and matured bonds presented through banking channels If agents are employed, do the balance sheet or the notes to the financial statements disclose the amount of cash in their possession If so, does this amount appear reasonable in relation to interest payable and matured bonds payable Do the statements, schedules, or narratives disclose for how long a period of time debt service funds carry a liability for unpresented checks for interest on registered bonds, for matured but unpresented interest coupons, and for matured but unpresented bonds

(4) Capital Lease Rental Payments.If general capital assets are being acquired under capital lease agreements, are periodic lease rental payments accounted for as expenditures of a debt service fund (or by another governmental fund) If so, does the report disclose that the provisions of SFAS No.13 are being followed (see the "Use of Debt Service Funds to Record Capital Lease Payments" section of this chapter) to determine the portion of each capital lease payment considered as interest and the portion considered as payment on the principal.

a.General Long-term Liabilities.

(1) Disclosure of Long-term Debt.Does the report contain evidence that the government has general long-term liabilities What evidence is there Does the report specify that no such debt is outstanding, or does it include a list of outstanding tax-supported debt issues; capital lease obligations; claims, judgments, and compensated absence payments to be made in future years; and unfunded pension obligations

Refer to the enterprise funds statement of net assets as well as note disclosures for long-term liabilities.Are any enterprise debt issues backed by the full faith and credit of the general government If so, how are the primary liability and the contingent liability disclosed

(2) Changes in Long-term Liabilities.How are changes in long-term liabilities during the year disclosed Is there a disclosure schedule for long-term liabilities similar to Illustration 6-1 Does the information in that schedule agree with the statements presented for capital projects funds and debt service funds and the government-wide financial statements

Are interest payments and principal payments due in future years disclosed If so, does the report relate these future payments with resources to be made available under existing debt service laws and covenants

(3) Debt Limitations.Does the report contain information as to legal debt limit and legal debt margin If so, is the information contained in the report explained in enough detail so that an intelligent reader (you) can understand how the limit is set, what debt is subject to it, and how much debt the government might legally issue in the year following the date of the report

(4) Overlapping Debt.Does the report disclose direct debt and overlapping debt of the reporting entity What disclosures of debt of the primary government are made in distinction to debt of component units Is debt of component units reported as "direct" debt of the reporting entity or as "overlapping debt"

b.Debt Service Funds.

(1) Debt Service Function.How is the debt service function for tax-supported debt and special assessment debt handled-by the General Fund, by a special revenue fund, or by one or more debt service funds If there is more than one debt service fund, what kinds of bond issues or other debt instruments are serviced by each fund Is debt service for bonds to be retired from enterprise revenues reported by enterprise funds

Does the report state the basis of accounting used for debt service funds If so, is the financial statement presentation consistent with the stated basis If the basis of accounting is not stated, analyze the statements to determine which basis is used-full accrual, modified accrual, or cash basis.Is the basis used consistent with the standards discussed in this chapter

(2) Investment Activity.Compare the net assets reserved for debt service, if any, in the Governmental Activities column of the government-wide statement of net assets and the fund balance of each debt service fund at balance sheet date with the amount of interest and the amount of debt principal the fund will be required to pay early in the following year (you may find debt service requirements in the notes to the financial statements or in supplementary schedules following the individual fund statements in the Financial Section of the CAFR).If debt service funds have accumulated assets in excess of amounts needed within a few days after the end of the fiscal year, are the excess assets invested Does the CAFR contain a schedule or list of investments of debt service funds Does the report disclose increases or decreases in the fair value of investments realized during the year Does the report disclose net earnings on investments during the year What percentage of revenue of each debt service fund is derived from earnings on investments What percentage of the revenue of each debt service fund is derived from taxes levied directly for the debt service fund What percentage is derived from transfers from other funds List any other sources of debt service revenue and other financing sources, and indicate the relative importance of each source.

Are estimated revenues for term bond debt service budgeted on an actuarial basis If so, are revenues received as required by the actuarial computations

(3) Management.Considering the debt maturity dates as well as the amount of debt and apparent quality of debt service fund investments, does the debt service activity appear to be properly managed Does the report disclose whether investments are managed by a corporate fiduciary, another outside investment manager, or governmental employees If outside investment managers are employed, is the basis of their fees disclosed Are the fees accounted for as additions to the cost of investments or as expenditures

Is one or more paying agents, or fiscal agents, employed If so, does the report disclose whether the agents keep track of the ownership of registered bonds, write checks to bondholders for interest payments and matured bonds or, in the case of coupon bonds, pay matured coupons and matured bonds presented through banking channels If agents are employed, do the balance sheet or the notes to the financial statements disclose the amount of cash in their possession If so, does this amount appear reasonable in relation to interest payable and matured bonds payable Do the statements, schedules, or narratives disclose for how long a period of time debt service funds carry a liability for unpresented checks for interest on registered bonds, for matured but unpresented interest coupons, and for matured but unpresented bonds

(4) Capital Lease Rental Payments.If general capital assets are being acquired under capital lease agreements, are periodic lease rental payments accounted for as expenditures of a debt service fund (or by another governmental fund) If so, does the report disclose that the provisions of SFAS No.13 are being followed (see the "Use of Debt Service Funds to Record Capital Lease Payments" section of this chapter) to determine the portion of each capital lease payment considered as interest and the portion considered as payment on the principal.

Each student will have a different annual report; therefore, there is no single set of answers to the question asked. Asking students to compare their answers to various questions is an effective active learning in-class technique.

4

What disclosures about long-term liabilities are required in the notes to the financial statements

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

5

Financial Statement Impact of Incurring General Long-term Debt on Behalf of Other Governments.

Facts: The Bates County government issued $2.5 million of tax-supported bonds to finance a major addition to the Bates County Hospital, a legally separate organization reported as a discretely presented component unit of the county.At the end of the fiscal year in which the debt was issued and the project completed, the county commission was shocked to see a deficit of more than $2 million reported for unrestricted net assets in the Governmental Activities column of the government-wide statement of net assets, compared with a surplus of over $400,000 the preceding year.The commission is quite concerned about how creditors and citizens will react to this large deficit and have asked you, in your role as county finance director, to explain how the deficit occurred and what actions should be taken to eliminate it.

Required

a.Write a brief memo to the county commission explaining how the $2.5 million bond issue for the addition to the Bates County Hospital resulted in the large and apparently unexpected deficit in unrestricted net assets.

( Hint: Refer to Illustration A 1-1, the City and County of Denver statement of net assets, and evaluate whether the bonds issued by Bates County would affect net assets-invested in capital assets, net of related debt or net assets- unrestricted.For additional insight, you may also wish to read the portion of Chapter 9 of this text that relates to preparation of government-wide financial statements for the Town of Brighton.)b.In your memo, explain what actions can be taken, if any, to eliminate the deficit in governmental activities unrestricted net assets, or at least make it less objectionable.

Facts: The Bates County government issued $2.5 million of tax-supported bonds to finance a major addition to the Bates County Hospital, a legally separate organization reported as a discretely presented component unit of the county.At the end of the fiscal year in which the debt was issued and the project completed, the county commission was shocked to see a deficit of more than $2 million reported for unrestricted net assets in the Governmental Activities column of the government-wide statement of net assets, compared with a surplus of over $400,000 the preceding year.The commission is quite concerned about how creditors and citizens will react to this large deficit and have asked you, in your role as county finance director, to explain how the deficit occurred and what actions should be taken to eliminate it.

Required

a.Write a brief memo to the county commission explaining how the $2.5 million bond issue for the addition to the Bates County Hospital resulted in the large and apparently unexpected deficit in unrestricted net assets.

( Hint: Refer to Illustration A 1-1, the City and County of Denver statement of net assets, and evaluate whether the bonds issued by Bates County would affect net assets-invested in capital assets, net of related debt or net assets- unrestricted.For additional insight, you may also wish to read the portion of Chapter 9 of this text that relates to preparation of government-wide financial statements for the Town of Brighton.)b.In your memo, explain what actions can be taken, if any, to eliminate the deficit in governmental activities unrestricted net assets, or at least make it less objectionable.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

6

Multiple Choice.Choose the best answer. 1.Which of the following would not be considered a general long-term liability

A)The estimated liability to clean up the fuel and hazard waste storage sites of the city's Public Works Department.

B)Capitalized equipment leases of the water utility fund.

C)Compensated absences for the city's Police Department.

D)Five-year notes payable used to acquire computer equipment for the city library.

2)Proceeds from bonds issued to construct a new county jail would most likely be recorded in the journal of the:

A)Capital projects fund.

B)Debt service fund.

C)General Fund.

D)Enterprise fund.

3)The long-term liability for a bond issue used to construct a new city recreation center should be recorded in the:

A)Capital projects fund general journal.

B)Debt service fund general journal.

C)Governmental activities general journal.

D)Both b and c.

Items 4 and 5 are based on the following information:

On March 2, 2010, 20-year, 6 percent, general obligation serial bonds were issued at the face amount of $3,000,000.Interest of 6 percent per annum is due semiannually on March 1 and September 1.The first payment of $150,000 for redemption of principal is due on March 1, 2011.Fiscal year-end occurs on December 31.

4)What is the interest expense for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

5)What is the interest expenditure for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

6)Debt service funds may be used to account for all of the following except:

A)Repayment of debt principal.

B)Lease payments under capital leases.

C)Amortization of premiums on bonds payable.

D)The proceeds of refunding bond issues.

7)Expenditures for redemption of principal of tax-supported bonds payable should be recorded in a debt service fund:

A)When the bonds are issued.

B)When the bond principal is legally due.

C)When the redemption checks are written.

D)Any of the above, if consistently followed.

8)Which of the following items would be reported in the Governmental Activities column of the government-wide financial statements

9.Interest on general long-term debt would be recorded as an expenditure in which of the following financial statements

A)Statement of revenues, expenditures, and changes in fund balances- governmental funds.

B)Statement of activities.

C)Both a and b are correct.

D)None of the above; interest is recorded as an expense, not an expenditure.

10)Which of the following accounts is unlikely to appear in a debt service fund ledger

A)Estimated Revenue.

B)Appropriations.

C)Estimated Other Financing Sources.

D)Encumbrances.

A)The estimated liability to clean up the fuel and hazard waste storage sites of the city's Public Works Department.

B)Capitalized equipment leases of the water utility fund.

C)Compensated absences for the city's Police Department.

D)Five-year notes payable used to acquire computer equipment for the city library.

2)Proceeds from bonds issued to construct a new county jail would most likely be recorded in the journal of the:

A)Capital projects fund.

B)Debt service fund.

C)General Fund.

D)Enterprise fund.

3)The long-term liability for a bond issue used to construct a new city recreation center should be recorded in the:

A)Capital projects fund general journal.

B)Debt service fund general journal.

C)Governmental activities general journal.

D)Both b and c.

Items 4 and 5 are based on the following information:

On March 2, 2010, 20-year, 6 percent, general obligation serial bonds were issued at the face amount of $3,000,000.Interest of 6 percent per annum is due semiannually on March 1 and September 1.The first payment of $150,000 for redemption of principal is due on March 1, 2011.Fiscal year-end occurs on December 31.

4)What is the interest expense for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

5)What is the interest expenditure for the fiscal year ending December 31, 2010

A)$90,000.

B)$135,000.

C)$150,000.

D)None of the above.

6)Debt service funds may be used to account for all of the following except:

A)Repayment of debt principal.

B)Lease payments under capital leases.

C)Amortization of premiums on bonds payable.

D)The proceeds of refunding bond issues.

7)Expenditures for redemption of principal of tax-supported bonds payable should be recorded in a debt service fund:

A)When the bonds are issued.

B)When the bond principal is legally due.

C)When the redemption checks are written.

D)Any of the above, if consistently followed.

8)Which of the following items would be reported in the Governmental Activities column of the government-wide financial statements

9.Interest on general long-term debt would be recorded as an expenditure in which of the following financial statementsA)Statement of revenues, expenditures, and changes in fund balances- governmental funds.

B)Statement of activities.

C)Both a and b are correct.

D)None of the above; interest is recorded as an expense, not an expenditure.

10)Which of the following accounts is unlikely to appear in a debt service fund ledger

A)Estimated Revenue.

B)Appropriations.

C)Estimated Other Financing Sources.

D)Encumbrances.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

7

In the current fiscal year, St.George County issued $3,000,000 in general obligation term bonds for 102.The county is required to use any accrued interest or premiums for servicing the debt issue.

a.How would the bond issue be recorded at the fund and government-wide level

b.How would the bond issue be reported in the fund financial statements and the government-wide financial statements

c.What effect, if any, do interest payments have on the carrying value of the bond issue as reported in the financial statements

a.How would the bond issue be recorded at the fund and government-wide level

b.How would the bond issue be reported in the fund financial statements and the government-wide financial statements

c.What effect, if any, do interest payments have on the carrying value of the bond issue as reported in the financial statements

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

8

The Case of the Vanishing Debt.

Facts: A county government and a legally separate organization-the Sports Stadium Authority-entered into an agreement under which the authority issued revenue bonds to construct a new stadium.Although the intent is to make debt service payments on the bonds from a surcharge on ticket sales, the county agreed to annually advance the Sports Stadium Authority the required amounts to make up any debt service shortfalls and has done so for several years.Accordingly, the county has recorded a receivable from the authority and the authority has recorded a liability to the county for all advances made under the agreement.

Ticket surcharge revenues that exceed $1,500,000 are to be paid to the county and to be applied first toward interest and then toward principal repayment of advances.Both par ties acknowledge, however, that annual ticket surcharge revenues may never exceed $1,500,000, since to reach that level would require an annual paid attendance of 3,000,000.Considering that season ticket holders and luxury suite renters are not included in the attendance count, it is quite uncertain if the required trigger level will ever be reached.

The authority has twice proposed to raise the ticket surcharge amount, but the county in both cases vetoed the proposal.Thus, the lender in this transaction (the county) has imposed limits that appear to make it infeasible for the borrower (the authority) to repay the advances.Consequently, the authority's legal counsel has taken the position that the authority is essentially a pass-through agency with respect to the advances in that the authority merely receives the advances and passes them on to a fiscal agent for debt service payments.Moreover, they note that the bonds could never have been issued in the first place without the county's irrevocable guarantee of repayment, since all parties knew from the beginning that the authority likely would not have the resources to make full debt service payments.

Based on the foregoing considerations, the authority's legal counsel has rendered an opinion that the liability for the advances can be removed from the authority's accounts.The county tacitly agrees that the loans (advances) are worthless, since it records an allowance for doubtful loans equal to the total amount of the advances.Still, the county board of commissioners refuses to remove the receivable from its accounts because of its ongoing rights under the original agreement for repayment.

Required

a.Assume you are the independent auditor for the authority, and provide a written analysis of the facts of this case, indicating whether or not you concur with the authority's decision to no longer report the liability to the county for debt service advances.

b.Alternatively, assume you are the independent auditor for the county and, based on the same analysis you conducted for requirement a, indicate whether or not you concur with the county continuing to report a receivable for debt service advances on its General Fund balance sheet and government-wide statement of net assets.

Facts: A county government and a legally separate organization-the Sports Stadium Authority-entered into an agreement under which the authority issued revenue bonds to construct a new stadium.Although the intent is to make debt service payments on the bonds from a surcharge on ticket sales, the county agreed to annually advance the Sports Stadium Authority the required amounts to make up any debt service shortfalls and has done so for several years.Accordingly, the county has recorded a receivable from the authority and the authority has recorded a liability to the county for all advances made under the agreement.

Ticket surcharge revenues that exceed $1,500,000 are to be paid to the county and to be applied first toward interest and then toward principal repayment of advances.Both par ties acknowledge, however, that annual ticket surcharge revenues may never exceed $1,500,000, since to reach that level would require an annual paid attendance of 3,000,000.Considering that season ticket holders and luxury suite renters are not included in the attendance count, it is quite uncertain if the required trigger level will ever be reached.

The authority has twice proposed to raise the ticket surcharge amount, but the county in both cases vetoed the proposal.Thus, the lender in this transaction (the county) has imposed limits that appear to make it infeasible for the borrower (the authority) to repay the advances.Consequently, the authority's legal counsel has taken the position that the authority is essentially a pass-through agency with respect to the advances in that the authority merely receives the advances and passes them on to a fiscal agent for debt service payments.Moreover, they note that the bonds could never have been issued in the first place without the county's irrevocable guarantee of repayment, since all parties knew from the beginning that the authority likely would not have the resources to make full debt service payments.

Based on the foregoing considerations, the authority's legal counsel has rendered an opinion that the liability for the advances can be removed from the authority's accounts.The county tacitly agrees that the loans (advances) are worthless, since it records an allowance for doubtful loans equal to the total amount of the advances.Still, the county board of commissioners refuses to remove the receivable from its accounts because of its ongoing rights under the original agreement for repayment.

Required

a.Assume you are the independent auditor for the authority, and provide a written analysis of the facts of this case, indicating whether or not you concur with the authority's decision to no longer report the liability to the county for debt service advances.

b.Alternatively, assume you are the independent auditor for the county and, based on the same analysis you conducted for requirement a, indicate whether or not you concur with the county continuing to report a receivable for debt service advances on its General Fund balance sheet and government-wide statement of net assets.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

9

Long-term Liability Transactions.Following are a number of unrelated transactions for K-Town, some of which affect governmental activities at the government-wide level.None of the transactions has been recorded yet.

1.The General Fund collected $825,000 in accrued taxes, which was transferred to the debt service fund; $600,000 of this amount was used to retire outstanding serial bonds and the remainder was used to make the interest payment on the outstanding serial bonds.

2.A $5,000,000 issue of serial bonds to finance a capital project was sold at 102 plus accrued interest in the amount of $50,000.The accrued interest and the premium were recorded in the debt service fund.Accrued interest on bonds sold must be used for interest payments; the premium is designated by state law for eventual payment of bond principal.

3.The debt service fund made a $110,000 capital lease payment, of which $15,809 was interest.Funds used to make the lease payment came from a capital grant received by the special revenue fund.

4.Tax-supported serial bonds with a $2,800,000 par value were issued in cash to permit partial refunding of a $3,500,000 par value issue of term bonds.The difference was settled with $700,000 that had been accumulated in prior years in a debt service fund.Assume that the term bonds had been issued several years earlier at par.

Required

Prepare in general journal form the necessary entries in the governmental activities and appropriate fund journals for each transaction.Explanations may be omitted.For each entry you prepare, name the fund in which the entry should be made.

1.The General Fund collected $825,000 in accrued taxes, which was transferred to the debt service fund; $600,000 of this amount was used to retire outstanding serial bonds and the remainder was used to make the interest payment on the outstanding serial bonds.

2.A $5,000,000 issue of serial bonds to finance a capital project was sold at 102 plus accrued interest in the amount of $50,000.The accrued interest and the premium were recorded in the debt service fund.Accrued interest on bonds sold must be used for interest payments; the premium is designated by state law for eventual payment of bond principal.

3.The debt service fund made a $110,000 capital lease payment, of which $15,809 was interest.Funds used to make the lease payment came from a capital grant received by the special revenue fund.

4.Tax-supported serial bonds with a $2,800,000 par value were issued in cash to permit partial refunding of a $3,500,000 par value issue of term bonds.The difference was settled with $700,000 that had been accumulated in prior years in a debt service fund.Assume that the term bonds had been issued several years earlier at par.

Required

Prepare in general journal form the necessary entries in the governmental activities and appropriate fund journals for each transaction.Explanations may be omitted.For each entry you prepare, name the fund in which the entry should be made.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

10

If a bond ordinance provides for regular and recurring payments of interest and principal payments on a general obligation bond issue of a certain government to be made from earnings of an enterprise fund and these payments are being made by the enterprise fund, how should the bond liability be disclosed in the comprehensive annual financial report of the government

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

11

Assessing General Obligation Debt Burden.This case focuses on the analysis of a city's general obligation debt burden.After examining the accompanying table that shows a city's general obligation (tax-supported) debt for the last ten fiscal years, answer the following questions.

Required

a.What is your initial assessment of the trend of the city's general obligation debt burden

b.Complete the table by calculating the ratio of Net General Bonded Debt to Assessed Value of taxable property and the ratio of Net General Bonded Debt per Capita.In addition, you learn that the average ratio of Net General Bonded Debt to Assessed Value for comparable-size cities in 2011 was 2.13 percent, and the average net general bonded debt per capita was $1,256.Based on time series analysis of the ratios you have calculated and the benchmark information provided in this paragraph, is your assessment of the city's general obli-gation still the same as it was in part a, or has it changed Explain.

Source: Adapted from City of Fargo, North Dakota, Comprehensive Annual Financial Report, 2006.

Required

a.What is your initial assessment of the trend of the city's general obligation debt burden

b.Complete the table by calculating the ratio of Net General Bonded Debt to Assessed Value of taxable property and the ratio of Net General Bonded Debt per Capita.In addition, you learn that the average ratio of Net General Bonded Debt to Assessed Value for comparable-size cities in 2011 was 2.13 percent, and the average net general bonded debt per capita was $1,256.Based on time series analysis of the ratios you have calculated and the benchmark information provided in this paragraph, is your assessment of the city's general obli-gation still the same as it was in part a, or has it changed Explain.

Source: Adapted from City of Fargo, North Dakota, Comprehensive Annual Financial Report, 2006. Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

12

Budgetary Transactions.Fleck County issued $5,500,000, 3 percent serial bonds, paying interest on January 1 and July 1.The bonds were sold on June 1 for 101.The county is required to use all accrued interest and premiums to service the debt.Any additional resources needed to service the debt are to come from the General Fund.The county's fiscal year-end is December 31.

Required

Prepare in general journal form the budgetary entry the debt service fund would make to account for this serial bond issue.What, if any, adjustment would need to be made to the General Fund budget to account for this serial bond issue

Required

Prepare in general journal form the budgetary entry the debt service fund would make to account for this serial bond issue.What, if any, adjustment would need to be made to the General Fund budget to account for this serial bond issue

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

13

The debt limit for general obligation debt for Milos City is 1 percent of the assessed property valuation for the city.Using the following information, calculate the city's debt margin.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

14

Statement of Legal Debt Margin.In preparation for a proposed bond sale, the city manager of the City of Appleton requested that you prepare a statement of legal debt margin for the city as of December 31, 2010.You ascertain that the following bond issues are outstanding on that date:

You obtain other information that includes the following items:

1.Assessed valuation of real and taxable personal property in the city totaled $240,000,000.

2.The rate of debt limitation applicable to the City of Appleton was 8 percent of total real and taxable personal property valuation.

3.Electric utility, water utility, and transit authority bonds were all serviced by enterprise revenues, but each carries a full-faith-and-credit contingency provision.By law, such self-supporting debt is not subject to debt limitation.

4.The convention center bonds and tax increment bonds are subject to debt limitation.

5.The amount of assets segregated for debt retirement at December 31, 2010, is $1,800,000.

You obtain other information that includes the following items:1.Assessed valuation of real and taxable personal property in the city totaled $240,000,000.

2.The rate of debt limitation applicable to the City of Appleton was 8 percent of total real and taxable personal property valuation.

3.Electric utility, water utility, and transit authority bonds were all serviced by enterprise revenues, but each carries a full-faith-and-credit contingency provision.By law, such self-supporting debt is not subject to debt limitation.

4.The convention center bonds and tax increment bonds are subject to debt limitation.

5.The amount of assets segregated for debt retirement at December 31, 2010, is $1,800,000.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

15

What is overlapping debt Why would a citizen care about the amount of overlapping debt reported Why would a government care about the amount of overlapping debt reported

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

16

Debt Service Fund Trial Balance.Following is Franklin County's debt service fund pre-closing trial balance for the fiscal year ended June 30, 2011.

Required

Using information provided by the trial balance, answer the following.

a.Assuming the budget was not amended, what was the budgetary journal entry recorded at the beginning of the fiscal year

b.What is the budgetary fund balance

c.Did the debt service fund pay debt obligations related to capital leases Explain.

d.Did the debt service fund perform a debt refunding Explain.

e.Prepare a statement of revenues, expenditures, and changes in fund balance for the debt service fund for the year ended June 30, 2011.

Required Using information provided by the trial balance, answer the following.

a.Assuming the budget was not amended, what was the budgetary journal entry recorded at the beginning of the fiscal year

b.What is the budgetary fund balance

c.Did the debt service fund pay debt obligations related to capital leases Explain.

d.Did the debt service fund perform a debt refunding Explain.

e.Prepare a statement of revenues, expenditures, and changes in fund balance for the debt service fund for the year ended June 30, 2011.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

17

"If a certain city had six tax-supported bond issues and three special assessment bond issues outstanding, it would be preferable to operate nine separate debt service funds or, at a minimum, one debt service fund for tax-supported bonds and one for special assessment bonds." Do you agree Explain.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

18

Capital Lease.The City of Jamestown has agreed to acquire a new city maintenance building under a capital lease agreement.At the inception of the lease, a payment of $100,000 is to be made; nine annual lease payments, each in the amount of $100,000, are to be made at the end of each year after the inception of the lease.The total amount to be paid under this lease, therefore, is $1,000,000.The town could borrow this amount for nine years at the annual rate of 8 percent; therefore, the present value of the lease at inception, including the initial payment, is $724,689.Assume that the fair value of the building at the inception of the lease is $750,000.

a.Show the entry that should be made in a capital projects fund at the inception of the lease after the initial payment has been made.

b.Show the entry that should be made at the inception of the lease in the government activities journal.

c.Show the entry that should be made in the debt service fund and governmental activities journal to record the second lease payment.

a.Show the entry that should be made in a capital projects fund at the inception of the lease after the initial payment has been made.

b.Show the entry that should be made at the inception of the lease in the government activities journal.

c.Show the entry that should be made in the debt service fund and governmental activities journal to record the second lease payment.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

19

Explain the essential differences between regular serial bonds and term bonds and how debt service fund accounting differs for the two types of bonds.

Unlock Deck

Unlock for access to all 24 flashcards in this deck.

Unlock Deck

k this deck

20

Serial Bond Debt Service Fund Journal Entries and Financial Statements.

As of December 31, 2010, New Town had $9,500,000 in 4.5 percent serial bonds outstanding.Cash of $509,000 is the debt service fund's only asset as of December 31, 2010, and there are no liabilities.The serial bonds pay interest semiannually on January 1 and July 1, with $500,000 in bonds being retired on each interest payment date.Resources for payment of interest are transferred from the General Fund and the debt service fund levies property taxes in an amount sufficient to cover principal payments.

Required

a.Prepare debt service fund and government-wide entries in general journal form to reflect, as necessary, the following information and transactions for FY 2011.

(1) The operating budget for FY 2011 consists of estimated revenues of $1,020,000 and estimated other financing sources equal to the amount of interest to be paid in FY 2011.Appropriations must be provided for interest payments and bond redemptions on January 1 and July 1.

(2) Cash was received from the General Fund and checks were written and mailed for the January 1 principal and interest payments.

(3) Property taxes in the amount of $1,020,000 were levied (no estimate for uncollectible accounts has been made).

(4) Property taxes in the amount of $1,019,000 were collected.

(5) Cash was received from the General Fund and checks were written and mailed for the July 1 principal and interest payments.

(6) Adjusting entries were made and uncollected taxes receivable were reclassified as delinquent.At the fund level, entries were also made to close budgetary and operating statement accounts.(Ignore closing entries in the government activities journal.)b.Prepare a statement of revenues, expenditures, and changes in fund balances for the debt service fund for the year ended December 31, 2011.

c.Prepare a balance sheet for the debt service fund as of December 31, 2011.

As of December 31, 2010, New Town had $9,500,000 in 4.5 percent serial bonds outstanding.Cash of $509,000 is the debt service fund's only asset as of December 31, 2010, and there are no liabilities.The serial bonds pay interest semiannually on January 1 and July 1, with $500,000 in bonds being retired on each interest payment date.Resources for payment of interest are transferred from the General Fund and the debt service fund levies property taxes in an amount sufficient to cover principal payments.

Required

a.Prepare debt service fund and government-wide entries in general journal form to reflect, as necessary, the following information and transactions for FY 2011.

(1) The operating budget for FY 2011 consists of estimated revenues of $1,020,000 and estimated other financing sources equal to the amount of interest to be paid in FY 2011.Appropriations must be provided for interest payments and bond redemptions on January 1 and July 1.

(2) Cash was received from the General Fund and checks were written and mailed for the January 1 principal and interest payments.

(3) Property taxes in the amount of $1,020,000 were levied (no estimate for uncollectible accounts has been made).

(4) Property taxes in the amount of $1,019,000 were collected.

(5) Cash was received from the General Fund and checks were written and mailed for the July 1 principal and interest payments.