Deck 13: The Us Taxation of Multinational Transactions

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

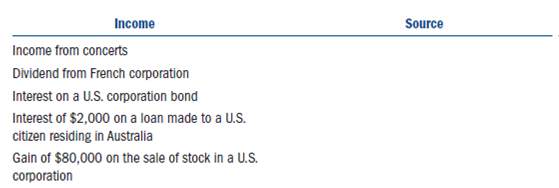

John Elton is a citizen and bona fide resident of Great Britain (United Kingdom). During 2011, John received the following income:

• Compensation of $30 million from performing concerts in the United States.

• Cash dividends of $10,000 from a French corporation stock.

• Interest of $6,000 on a U.S. corporation bond.• Interest of $2,000 on a loan made to a U.S. citizen residing in Australia.• Gain of $80,000 on the sale of stock in a U.S. corporation.

• Determine the source (U.S. or foreign) of each item of income John received in 2011.

• Compensation of $30 million from performing concerts in the United States.

• Cash dividends of $10,000 from a French corporation stock.

• Interest of $6,000 on a U.S. corporation bond.• Interest of $2,000 on a loan made to a U.S. citizen residing in Australia.• Gain of $80,000 on the sale of stock in a U.S. corporation.

• Determine the source (U.S. or foreign) of each item of income John received in 2011.

Question

Question

Question

Question

Question

Question

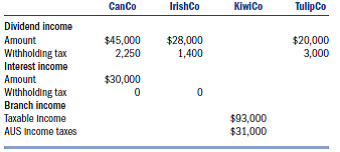

Windmill Corporation manufactures products in its plants in Iowa, Canada, Ireland, and Australia. Windmill conducts its operations in Canada through a 50 percent owned joint venture, CanCo. CanCo is treated as a corporation for U.S. and Canadian tax purposes. An unrelated Canadian investor owns the remaining 50 percent. Windmill conducts its operations in Ireland through a wholly owned subsidiary, IrishCo. IrishCo is a controlled foreign corporation for U.S. tax purposes. Windmill conducts its operations in Australia through a wholly owned hybrid entity (KiwiCo) treated as a branch for U.S. tax purposes and a corporation for Australian tax purposes. Windmill also owns a 5 percent interest in a Dutch corporation (TulipCo). During 2011, Windmill reported the following foreign source income from its international operations and investments.

Notes to the table:

1. CanCo and KiwiCo derive all of their earnings from active business operations.

2. The dividend from CanCo carries with it a deemed paid credit (§78 gross-up) of $30,000.

3. The dividend from IrishCo carries with it a deemed paid credit (§78 gross-up) of $4,000.

a. Classify the income received by Windmill and any associated §78 gross-up into the appropriate FTC baskets.

b. Windmill has $1,250,000 of U.S. source gross income. Windmill also incurred SG A of $300,000 that is apportioned between U.S. and foreign source income based on the gross income in each basket. Assume KiwiCo's gross income is $93,000. Compute the FTC limitation for each basket of foreign source income. The corporate tax rate is 35 percent.

Notes to the table:

1. CanCo and KiwiCo derive all of their earnings from active business operations.

2. The dividend from CanCo carries with it a deemed paid credit (§78 gross-up) of $30,000.

3. The dividend from IrishCo carries with it a deemed paid credit (§78 gross-up) of $4,000.

a. Classify the income received by Windmill and any associated §78 gross-up into the appropriate FTC baskets.

b. Windmill has $1,250,000 of U.S. source gross income. Windmill also incurred SG A of $300,000 that is apportioned between U.S. and foreign source income based on the gross income in each basket. Assume KiwiCo's gross income is $93,000. Compute the FTC limitation for each basket of foreign source income. The corporate tax rate is 35 percent.

Question

Question

Question

Question

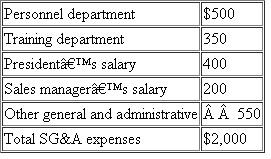

Falmouth Kettle Company, a U.S. corporation, sells its products in the United States and Europe. During 2011, selling, general, and administrative (SG A) expenses included:

Falmouth had $12,000 of gross sales to U.S. customers and $3,000 of gross sales to European customers. Gross profit (sales minus cost of goods sold) from domestic sales was $3,000 and gross profit from foreign sales was $1,000. ApportionFalmouth's's SG A expenses to foreign source income using the following methods:

Falmouth had $12,000 of gross sales to U.S. customers and $3,000 of gross sales to European customers. Gross profit (sales minus cost of goods sold) from domestic sales was $3,000 and gross profit from foreign sales was $1,000. ApportionFalmouth's's SG A expenses to foreign source income using the following methods:

a. Gross sales.

b. Gross income.

c. If Falmouth wants to maximize its foreign tax credit limitation, whichmethod produces the better outcome

Falmouth had $12,000 of gross sales to U.S. customers and $3,000 of gross sales to European customers. Gross profit (sales minus cost of goods sold) from domestic sales was $3,000 and gross profit from foreign sales was $1,000. ApportionFalmouth's's SG A expenses to foreign source income using the following methods:a. Gross sales.

b. Gross income.

c. If Falmouth wants to maximize its foreign tax credit limitation, whichmethod produces the better outcome

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

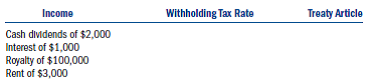

Colleen is a citizen and bona fide resident of Ireland. During 2011, she received the following income:

• Cash dividends of $2,000 from a U.S. corporation's stock.

• Interest of $1,000 on a U.S. corporation bond.• Royalty of $100,000 from a U.S. corporation for use of a patent she developed.• Rent of $3,000 from U.S. individuals renting her cottage in Maine.

Identify the U.S. withholding tax rate on the payment of each item of income under the U.S.-Ireland income tax treaty and cite the appropriate treaty article. You can access the 1997 U.S.-Ireland income tax treaty on the IRS Web site, www.irs.gov

• Cash dividends of $2,000 from a U.S. corporation's stock.

• Interest of $1,000 on a U.S. corporation bond.• Royalty of $100,000 from a U.S. corporation for use of a patent she developed.• Rent of $3,000 from U.S. individuals renting her cottage in Maine.

Identify the U.S. withholding tax rate on the payment of each item of income under the U.S.-Ireland income tax treaty and cite the appropriate treaty article. You can access the 1997 U.S.-Ireland income tax treaty on the IRS Web site, www.irs.gov

Question

Question

Question

Question

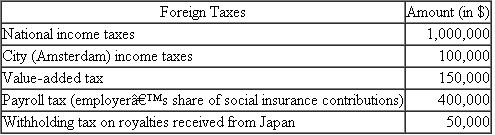

Gameco, a U.S. corporation, operates gambling machines in the United States and abroad. Gameco conducts its operations in Europe through a Dutch B.V., which is treated as a branch for U.S. tax purposes. Gameco also licenses game machines to an unrelated company in Japan. During the current year, Gameco paid the following foreign taxes, translated into U.S. dollars at the appropriate exchange rate:

Identify Gameco's creditable foreign taxes.

Identify Gameco's creditable foreign taxes.

Identify Gameco's creditable foreign taxes. Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/67

Play

Full screen (f)

Deck 13: The Us Taxation of Multinational Transactions

1

Natasha is not a citizen of the United States, but she spends 200 days per year in the United States on business. She does not have a green card. True or false. Natasha will always be considered a resident of the United States for U.S. tax purposes because of her physical presence in the United States. Explain.

Inbound and outbound transaction

An outbound transaction happens when a person from USA gets in a transaction outside the USA or with a person not resident of USA.An inbound transaction happens when a person not of USA gets into a transaction with resident of United States.

Discussion and analysis

Under following conditions Natasha will be considered a resident of the United States for U.S.tax purposes if she fulfills any of the below two conditions:

• If she holds a green card for any part of the calendar year

• If she meets the substantial presence test as prescribed by US tax laws.As per them, Maria needs to be physically present for more at least 31 days during the calendar year in USA and the sum of 1/3 times of days present in USA in preceding year and 1/6 times of days present in USA in second preceding year must be at least 183 days.

Since Natasha does not hold green card but has clears she would be qualified as resident for the tax purposes.However, it is not the blanket rule and she may still be unqualified if she meets any of the exception mentioned in the tax treaty between USA and the country where Natasha is resident.

An outbound transaction happens when a person from USA gets in a transaction outside the USA or with a person not resident of USA.An inbound transaction happens when a person not of USA gets into a transaction with resident of United States.

Discussion and analysis

Under following conditions Natasha will be considered a resident of the United States for U.S.tax purposes if she fulfills any of the below two conditions:

• If she holds a green card for any part of the calendar year

• If she meets the substantial presence test as prescribed by US tax laws.As per them, Maria needs to be physically present for more at least 31 days during the calendar year in USA and the sum of 1/3 times of days present in USA in preceding year and 1/6 times of days present in USA in second preceding year must be at least 183 days.

Since Natasha does not hold green card but has clears she would be qualified as resident for the tax purposes.However, it is not the blanket rule and she may still be unqualified if she meets any of the exception mentioned in the tax treaty between USA and the country where Natasha is resident.

2

Why is a treaty important to a nonresident investor in U.S. stocks and bonds

Inbound and outbound transaction

An outbound transaction happens when a person from USA gets in a transaction outside the USA or with a person not resident of USA.An inbound transaction happens when a person not of USA gets into a transaction with resident of United States.

Discussion and analysis

When a non resident of USA for tax purposes earns income from source in USA then it can be classified as

• Effectively connected income (ECI)

• Or fixed and determinable, Annual or periodic income (FDAP).

ECI income is taxed at graduated tax rates of USA on Gross Income minus Deductions.On the other hand FDAP is subject to withholding taxes on gross income.For investors, a treaty can often lead to reduction in withholding tax rates which can be up to 30% or total exemption from them as well.

An outbound transaction happens when a person from USA gets in a transaction outside the USA or with a person not resident of USA.An inbound transaction happens when a person not of USA gets into a transaction with resident of United States.

Discussion and analysis

When a non resident of USA for tax purposes earns income from source in USA then it can be classified as

• Effectively connected income (ECI)

• Or fixed and determinable, Annual or periodic income (FDAP).

ECI income is taxed at graduated tax rates of USA on Gross Income minus Deductions.On the other hand FDAP is subject to withholding taxes on gross income.For investors, a treaty can often lead to reduction in withholding tax rates which can be up to 30% or total exemption from them as well.

3

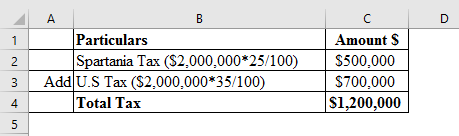

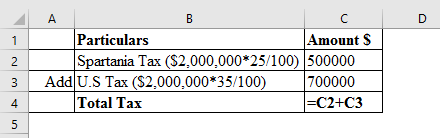

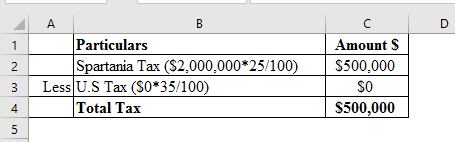

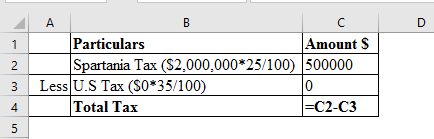

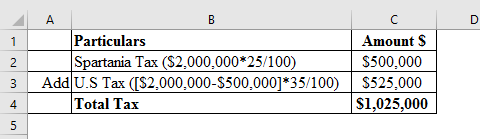

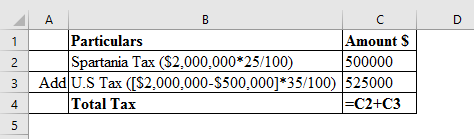

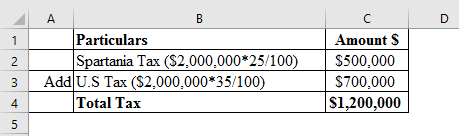

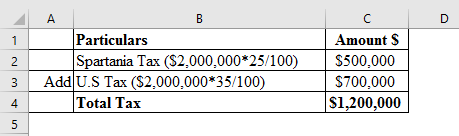

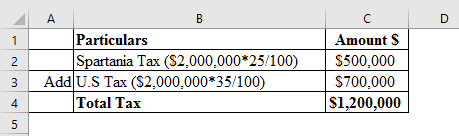

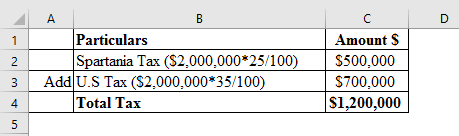

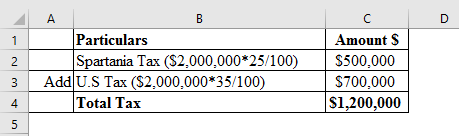

Spartan Corporation, a U.S. corporation, reported $2 million of pretax income from its business operations in Spartania, which were conducted through a foreign branch. Spartania taxes branch income at 25 percent, and the United States taxes corporate income at 35 percent.

a. If the United States provided no mechanism for mitigating double taxation, what would be the total tax (U.S. and foreign) on the $2 million of branch profits

b. Assume the United States allows U.S. corporations to exclude foreign source income from U.S. taxation. What would be the total tax on the $2 million of branch profits

c. Assume the United States allows U.S. corporations to claim a deduction for foreign income taxes. What would be the total tax on the $2 million of branch profits

d. Assume the United States allows U.S. corporations to claim a credit for foreign income taxes paid on foreign source income. What would be the total tax on the $2 million of branch profits What would be your answer if Spartania taxed branch profits at 40 percent

a. If the United States provided no mechanism for mitigating double taxation, what would be the total tax (U.S. and foreign) on the $2 million of branch profits

b. Assume the United States allows U.S. corporations to exclude foreign source income from U.S. taxation. What would be the total tax on the $2 million of branch profits

c. Assume the United States allows U.S. corporations to claim a deduction for foreign income taxes. What would be the total tax on the $2 million of branch profits

d. Assume the United States allows U.S. corporations to claim a credit for foreign income taxes paid on foreign source income. What would be the total tax on the $2 million of branch profits What would be your answer if Spartania taxed branch profits at 40 percent

Inside Outside Basis Partnership

Outside basis of partnership is defined as tax basis of each partner of a partnership and inside basis of partnership refers to the tax basis of partnership in each partners asset.

The distributive share generated from partnership including both taxable non-taxable income is added, which increases inside basis of partnership.

Share in partnership is a capital asset, when any partner sells his/her share it, loss/gain arising is recognised as capital gain/loss.

Gain/ loss arising out of hot assets is recognised as ordinary gain/loss.

a.Calculation of total tax if US provide no mechanism for mitigating double taxation

Thus, total tax if US provides no mechanism for mitigating double taxation is

Thus, total tax if US provides no mechanism for mitigating double taxation is

b.Calculation of total tax if United States allows U.S.corporations to exclude foreign source income

b.Calculation of total tax if United States allows U.S.corporations to exclude foreign source income

Total tax would be $500,000 which is illustrated as under

Thus, total tax if United States allows U.S.corporations to exclude foreign source income is

Thus, total tax if United States allows U.S.corporations to exclude foreign source income is

c.Calculation of total tax if United States allow U.S.corporations to claim a deduction for foreign income taxes.

c.Calculation of total tax if United States allow U.S.corporations to claim a deduction for foreign income taxes.

Thus, total tax if United States allows U.S.corporations to claim a deduction for foreign income taxes would be of

Thus, total tax if United States allows U.S.corporations to claim a deduction for foreign income taxes would be of

4.Calculation of total tax if United States allows U.S.corporations to claim a credit for foreign income taxes paid on foreign source income

4.Calculation of total tax if United States allows U.S.corporations to claim a credit for foreign income taxes paid on foreign source income

0

0

1

1

Thus, total tax if United States allows U.S.corporations to claim a credit for foreign income taxes paid on foreign source income is

2

2

Calculation of total tax if Spartania taxed branch profits at 40 percent

3

3

Thus, total tax if Spartania taxed branch profits at 40 percent is

4

4

.

Outside basis of partnership is defined as tax basis of each partner of a partnership and inside basis of partnership refers to the tax basis of partnership in each partners asset.

The distributive share generated from partnership including both taxable non-taxable income is added, which increases inside basis of partnership.

Share in partnership is a capital asset, when any partner sells his/her share it, loss/gain arising is recognised as capital gain/loss.

Gain/ loss arising out of hot assets is recognised as ordinary gain/loss.

a.Calculation of total tax if US provide no mechanism for mitigating double taxation

Thus, total tax if US provides no mechanism for mitigating double taxation is b.Calculation of total tax if United States allows U.S.corporations to exclude foreign source incomeTotal tax would be $500,000 which is illustrated as under

Thus, total tax if United States allows U.S.corporations to exclude foreign source income is c.Calculation of total tax if United States allow U.S.corporations to claim a deduction for foreign income taxes. Thus, total tax if United States allows U.S.corporations to claim a deduction for foreign income taxes would be of 4.Calculation of total tax if United States allows U.S.corporations to claim a credit for foreign income taxes paid on foreign source income 0 1Thus, total tax if United States allows U.S.corporations to claim a credit for foreign income taxes paid on foreign source income is

2Calculation of total tax if Spartania taxed branch profits at 40 percent

3Thus, total tax if Spartania taxed branch profits at 40 percent is

4.

4

Chapeau Company, a U.S. corporation, operates through a branch in Champagnia. The source rules used by Champagnia are identical to those used by the United States. For 2011, Chapeau has $2,000 of gross income, $1,200 from U.S. sources and $800 from sources within Champagnia. The $1,200 of U.S. source income and $700 of the foreign source income are attributable to manufacturing activities in Champagnia (general category income). The remaining $100 of foreign source income is passive category interest income. Chapeau had $500 of expenses other than taxes, all of which are allocated directly to manufacturing income ($200 of which is apportioned to foreign sources). Chapeau paid $150 of income taxes to Champagnia on its manufacturing income. The interest income was subject to a 10 percent withholding tax of $10. Assume the U.S. tax rate is 35%. Compute Chapeau's allowable foreign tax credit in 2011.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

5

Why does the United States allow U.S. taxpayers to claim a credit against their precredit U.S. tax for foreign income taxes paid

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

6

Why is a treaty important to a nonresident worker in the United States

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

7

Guido is a citizen and resident of Belgium. He has a full-time job in Belgium and has lived there with his family for the past 10 years. In 2009, Guido came to the United States for the first time. The sole purpose of his trip was business. He intended to stay in the United States for only 180 days, but he ended up staying for 210 days because of unforeseen problems with his business. Guido came to the United States again on business in 2010 and stayed for 180 days. In 2011 he came back to the United States on business and stayed for 70 days. Determine if Guido meets the U.S. statutory definition of a resident alien in 2009, 2010, and 2011 under the substantial presence test.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

8

Paton Corporation, a U.S. corporation, owns 100 percent of the stock of Tappan Ltd, a British corporation, and 100 percent of the stock of Monroe N.V., a Dutch corporation. Monroe has post-1986 undistributed earnings of €600 and post-1986 foreign income taxes of $400. Tappan has post-1986 undistributed earnings of £800 and post-1986 foreign income taxes of $200. During the current year, Tappan paid Paton a dividend of £100, and Monroe paid Paton a dividend of €100. The dividends were exempt from withholding tax under the U.S.-UK and U.S.-Netherlands income tax treaties. The exchange rates are as follows: €1:$1.50 and £1:$2.00.

a. Compute Paton's deemed paid credit on the dividends it received from Tappan and Monroe.

b. Assume this is Paton's only income and compute the company's net U.S. tax after allowance of any foreign tax credits.

a. Compute Paton's deemed paid credit on the dividends it received from Tappan and Monroe.

b. Assume this is Paton's only income and compute the company's net U.S. tax after allowance of any foreign tax credits.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

9

What role does the foreign tax credit limitation play in U.S. tax policy

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

10

Why does the United States use a "basket" approach in the foreign tax credit limitation computation

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

11

{ research } Use the facts in Problem 41. If Guido meets the statutory requirements to be considered a resident of both the United States and Belgium, what criteria does the U.S.-Belgium treaty use to "break the tie" and determine Guido's country of residence Look at Article 4 of the 2006 U.S.-Belgium income tax treaty, which you can find on the IRS website, http://www.irs.gov.

Problem 41

Guido is a citizen and resident of Belgium. He has a full-time job in Belgium and has lived there with his family for the past 10 years. In 2007, Guido came to the United States for the first time. The sole purpose of his trip was business. He intended to stay in the United States for only 180 days, but he ended up staying for 210 days because of unforeseen problems with his business. Guido came to the United States again on business in 2008 and stayed for 180 days. In 2009 he came back to the United States on business and stayed for 70 days. Determine if Guido meets the U.S. statutory definition of a resident alien in 2007, 2008, and 2009 under the substantial presence test.

Problem 41

Guido is a citizen and resident of Belgium. He has a full-time job in Belgium and has lived there with his family for the past 10 years. In 2007, Guido came to the United States for the first time. The sole purpose of his trip was business. He intended to stay in the United States for only 180 days, but he ended up staying for 210 days because of unforeseen problems with his business. Guido came to the United States again on business in 2008 and stayed for 180 days. In 2009 he came back to the United States on business and stayed for 70 days. Determine if Guido meets the U.S. statutory definition of a resident alien in 2007, 2008, and 2009 under the substantial presence test.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

12

Hannah Corporation, a U.S. corporation, owns 100 percent of the stock of its two foreign corporations, Red S

a. and Cedar A.G. Red and Cedar derive all of their income from active foreign business operations. Red operates in a low-tax jurisdiction (20 percent tax rate), and Cedar operates in a high-tax jurisdiction (50 percent tax rate). Red has post-1986 foreign income taxes of $200 and post-1986 undistributed earnings of 800u. Cedar has post-1986 foreign income taxes of $500 and post-1986 undistributed earnings of 500q. No withholding taxes are imposed on any dividends that Hannah receives from Red or Cedar. The exchange rate between all three currencies is 1:1. Assume a U.S. corporate tax rate of 35 percent. Under the look-through rules, all dividend income is treated as general category income.

a. Compute the effect of an 80u dividend from Red on Hannah's net U.S. tax liability.

b. Can you offer Hannah any suggestions regarding how it might eliminate the residual U.S. tax due on an 80u dividend from Red Be specific in terms of the exact amounts involved in any planning opportunities you identify.

a. and Cedar A.G. Red and Cedar derive all of their income from active foreign business operations. Red operates in a low-tax jurisdiction (20 percent tax rate), and Cedar operates in a high-tax jurisdiction (50 percent tax rate). Red has post-1986 foreign income taxes of $200 and post-1986 undistributed earnings of 800u. Cedar has post-1986 foreign income taxes of $500 and post-1986 undistributed earnings of 500q. No withholding taxes are imposed on any dividends that Hannah receives from Red or Cedar. The exchange rate between all three currencies is 1:1. Assume a U.S. corporate tax rate of 35 percent. Under the look-through rules, all dividend income is treated as general category income.

a. Compute the effect of an 80u dividend from Red on Hannah's net U.S. tax liability.

b. Can you offer Hannah any suggestions regarding how it might eliminate the residual U.S. tax due on an 80u dividend from Red Be specific in terms of the exact amounts involved in any planning opportunities you identify.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

13

Why are the income source rules important to a U.S. citizen or resident

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

14

True or False. All dividend income received by a U.S. taxpayer is classified as passive category income for foreign tax credit limitation purposes. Explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

15

{ research } How does the U.S.-Belgium treaty define a permanent establishment for determining nexus Look at Article 5 of the 2006 U.S.-Belgium income tax treaty, which you can find on the IRS website, http://www.irs.gov.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

16

Identify the "per se" companies for which a check-the-box election cannot be made for U.S. tax purposes in the countries listed below. Consult the Instructions to Form 8832, which can be found on the "Forms and Instructions" site on the IRS Web site, www.irs.gov.

a. Japan

b. Germany

c. Netherlands

d. United Kingdom

e. People's Republic of China

a. Japan

b. Germany

c. Netherlands

d. United Kingdom

e. People's Republic of China

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

17

Why are the income source rules important to a U.S. nonresident

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

18

True or False. All foreign taxes are creditable for U.S. tax purposes. Explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

19

Mackinac Corporation, a U.S. corporation, reported total taxable income of $5 million in 2011. Taxable income included $1.5 million of foreign source taxable income from the company's branch operations in Canada. All of the branch income is general category income. Mackinac paid Canadian income taxes of $600,000 on its branch income. Compute Mackinac's allowable foreign tax credit for 2011. Assume a U.S. corporate tax rate of 34%.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

20

Eagle Inc., a U.S. corporation, intends to create a limitada in Brazil in 2011 to manufacture pitching machines. The company expects the operation to generate losses of US$2,500,000 during its first three years of operations. Eagle would like the losses to flow through to its U.S. tax return and offset its U.S. profits.

a. Can Eagle "check the box" and treat the limitada as a disregarded entity (branch) for U.S. tax purposes Consult the Instructions to Form 8832, which can be found on the "Forms and Instructions" site on the IRS Web site, www.irs.gov.

b. Assume management's projections were accurate and Eagle deducted $75,000 of branch losses on its U.S. tax return from 2011-2013. At 01/01/14, the fair market value of the limitada's net assets exceeded Eagle's tax basis in the assets by US$5 million. What are the U.S. tax consequences of checking the box on Form 8832 and converting the limitada to a corporation for U.S. tax purposes

a. Can Eagle "check the box" and treat the limitada as a disregarded entity (branch) for U.S. tax purposes Consult the Instructions to Form 8832, which can be found on the "Forms and Instructions" site on the IRS Web site, www.irs.gov.

b. Assume management's projections were accurate and Eagle deducted $75,000 of branch losses on its U.S. tax return from 2011-2013. At 01/01/14, the fair market value of the limitada's net assets exceeded Eagle's tax basis in the assets by US$5 million. What are the U.S. tax consequences of checking the box on Form 8832 and converting the limitada to a corporation for U.S. tax purposes

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

21

Carol receives $500 of dividend income from Microsoft, Inc., a U.S. company. True or False. Absent any treaty provisions, Carol will be subject to U.S. tax on the dividend regardless of whether she is a resident or nonresident. Explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

22

What is an indirect credit for foreign tax credit purposes What is the tax policy reason for allowing such a credit

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

23

Waco Leather, Inc., a U.S. corporation, reported total taxable income of $5 million in 2011. Taxable income included 1.5 million of foreign source taxable income from the company's branch operations in Mexico. All of the branch income is general category income. Waco paid Mexican income taxes of $420,000 on its branch income. Compute Waco's allowable foreign tax credit for 2011. Assume a U.S. corporate tax rate of 34%.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

24

Identify whether the corporations described below are controlled foreign corporations.

a. Shetland PLC, a UK corporation, has two classes of stock outstanding, 75 shares of class AA stock and 25 shares of class A stock. Each class of stock has equal voting power. Angus owns 35 shares of class AA stock and 20 shares of class A stock. Angus is a U.S. citizen who resides in England.b. Tony and Gina, both U.S. citizens, own 5 percent and 10 percent, respectively, of the voting stock of DaVinci S

a., an Italian corporation. Tony and Gina are also equal partners in Roma Corporation, an Italian corporation that owns 50 percent of the DaVinci stock.

c. Pierre, a U.S. citizen, owns 45 of the 100 shares outstanding in Vino S

a., a French corporation. Pierre's father, Pepe, owns 8 shares in Vino. Pepe also is a U.S. citizen. The remaining 47 shares are owned by non-U.S. individuals.

a. Shetland PLC, a UK corporation, has two classes of stock outstanding, 75 shares of class AA stock and 25 shares of class A stock. Each class of stock has equal voting power. Angus owns 35 shares of class AA stock and 20 shares of class A stock. Angus is a U.S. citizen who resides in England.b. Tony and Gina, both U.S. citizens, own 5 percent and 10 percent, respectively, of the voting stock of DaVinci S

a., an Italian corporation. Tony and Gina are also equal partners in Roma Corporation, an Italian corporation that owns 50 percent of the DaVinci stock.

c. Pierre, a U.S. citizen, owns 45 of the 100 shares outstanding in Vino S

a., a French corporation. Pierre's father, Pepe, owns 8 shares in Vino. Pepe also is a U.S. citizen. The remaining 47 shares are owned by non-U.S. individuals.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

25

Pavel, a citizen and resident of Russia, spent 100 days in the United States working for his employer, Yukos Oil, a Russian corporation. Under what conditions will Pavel be subject to U.S. tax on the portion of his compensation earned while working in the United States

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

26

What is a functional currency What role does it play in the computation of an indirect credit for foreign tax credit purposes

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

27

Petoskey Stone Inc., a U.S. corporation, received the following sources of income during 2011. Identify the source of each item as either U.S. or foreign.

a. Interest income from a loan to its German subsidiary.

b. Dividend income from Granite Corporation, a U.S. corporation.

c. Royalty income from its Irish subsidiary for use of a trademark.

d. Rent income from its Canadian subsidiary of a warehouse located in Wisconsin.

a. Interest income from a loan to its German subsidiary.

b. Dividend income from Granite Corporation, a U.S. corporation.

c. Royalty income from its Irish subsidiary for use of a trademark.

d. Rent income from its Canadian subsidiary of a warehouse located in Wisconsin.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

28

USCo owns 100 percent of the following corporations: Dutch N.V., Germany A.G., Australia PLC, Japan Corporation, and Brazil S

a. During the year, the following transactions took place:

a. Germany A.G. owns an office building that it leases to unrelated persons. Germany A.G. engaged an independent managing agent to manage and maintain the office building and performs no activities with respect to the property.

b. Dutch N.V. leased office machines to unrelated persons. Dutch N.V. performed only incidental activities and incurred nominal expenses in leasing and servicing the machines. Dutch N.V. is not engaged in the manufacture or production of the machines and does not add substantial value to the machines.

c. Dutch N.V. purchased goods manufactured in France from an unrelated contract manufacturer and sold them to Germany A.G. for consumption in Germany.

d. Australia PLC purchased goods manufactured in Australia from an unrelated person and sold them to Japan Corporation for use in Japan. Determine whether the above transactions result in subpart F income to USCo.

a. During the year, the following transactions took place:

a. Germany A.G. owns an office building that it leases to unrelated persons. Germany A.G. engaged an independent managing agent to manage and maintain the office building and performs no activities with respect to the property.

b. Dutch N.V. leased office machines to unrelated persons. Dutch N.V. performed only incidental activities and incurred nominal expenses in leasing and servicing the machines. Dutch N.V. is not engaged in the manufacture or production of the machines and does not add substantial value to the machines.

c. Dutch N.V. purchased goods manufactured in France from an unrelated contract manufacturer and sold them to Germany A.G. for consumption in Germany.

d. Australia PLC purchased goods manufactured in Australia from an unrelated person and sold them to Japan Corporation for use in Japan. Determine whether the above transactions result in subpart F income to USCo.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

29

What are the potential U.S. tax benefits from engaging in a §863 sale

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

30

What is a hybrid entity for U.S. tax purposes Why is it a popular organizational form for a U.S. company expanding its international operations What are the potential drawbacks to using a hybrid entity

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

31

Carmen SanDiego, a U.S. citizen, is employed by General Motors Corporation, a U.S. corporation. On April 1, 2011, GM relocated Carmen to its Brazilian operations for the remainder of 2011. Carmen was paid a salary of $120,000 and was employed on a 5-day week basis. As part of her compensation package for moving to Brazil, Carmen also received a housing allowance of $25,000. Carmen's salary was earned ratably over the twelve month period. During 2011 Carmen worked 260 days, 195 of which were in Brazil and 65 of which were in Michigan. How much of Carmen's total compensation is treated as foreign source income for 2011 Why might Carmen want to maximize her foreign source income in 2011

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

32

USCo manufactures and markets electrical components. USCo operates outside the United States through a number of CFCs, each of which is organized in a different country. These CFCs derived the following income for the current year:

a. F1 has gross income of $5 million, including $200,000 of foreign personal holding company interest and $4.8 million of gross income from the sale of inventory that F1 manufactured at a factory located within its home country.

b. F2 has gross income of $5 million, including $4 million of foreign personal holding company interest and $1 million of gross income from the sale of inventory that F2 manufactured at a factory located within its home country.

Determine the amount of income that USCo must report as a deemed dividend under subpart F in each scenario.

a. F1 has gross income of $5 million, including $200,000 of foreign personal holding company interest and $4.8 million of gross income from the sale of inventory that F1 manufactured at a factory located within its home country.

b. F2 has gross income of $5 million, including $4 million of foreign personal holding company interest and $1 million of gross income from the sale of inventory that F2 manufactured at a factory located within its home country.

Determine the amount of income that USCo must report as a deemed dividend under subpart F in each scenario.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

33

True or False. A taxpayer will always prefer deducting an expense against U.S. source income and not foreign source income when filing a tax return in the United States. Explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

34

What is a per se entity under the check-the-box rules

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

35

John Elton is a citizen and bona fide resident of Great Britain (United Kingdom). During 2011, John received the following income:

• Compensation of $30 million from performing concerts in the United States.

• Cash dividends of $10,000 from a French corporation stock.

• Interest of $6,000 on a U.S. corporation bond.• Interest of $2,000 on a loan made to a U.S. citizen residing in Australia.• Gain of $80,000 on the sale of stock in a U.S. corporation.

• Determine the source (U.S. or foreign) of each item of income John received in 2011.

• Compensation of $30 million from performing concerts in the United States.

• Cash dividends of $10,000 from a French corporation stock.

• Interest of $6,000 on a U.S. corporation bond.• Interest of $2,000 on a loan made to a U.S. citizen residing in Australia.• Gain of $80,000 on the sale of stock in a U.S. corporation.

• Determine the source (U.S. or foreign) of each item of income John received in 2011.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

36

Spartan Corporation manufactures quidgets at its plant in Sparta, Michigan. Spartan sells its quidgets to customers in the United States, Canada, England, and Australia.Spartan markets its products in Canada and England through branches in Toronto and London, respectively. Title transfers in the United States on all sales to U.S. customers and abroad (FOB: destination) on all sales to Canadian and English customers. Spartan reported total gross income on U.S. sales of $15,000,000 and total gross income on Canadian and U.K. sales of $5,000,000, split equally between the two countries. Spartan paid Canadian income taxes of $600,000 on its branch profits in Canada and U.K. income taxes of $700,000 on its branch profits in the U.K. Spartan financed its Canadian operations through a $10 million capital contribution, which Spartan financed through a loan from Bank of America. During the current year, Spartan paid $600,000 in interest on the loan. Spartan sells its quidgets to Australian customers through its wholly owned Australian subsidiary. Title passes in the United States (FOB: shipping) on all sales to the subsidiary. Spartan reported gross income of $3,000,000 on sales to its subsidiary during the year. The subsidiary paid Spartan a dividend of $670,000 on December 31 (the withholding tax is 0 percent under the U.S.- Australia treaty). Spartan was deemed to have paid Australian income taxes of $330,000 on the income repatriated as a dividend

a. Compute Spartan's foreign source gross income and foreign tax (direct and withholding) for the current year.

b. Assume 20 percent of the interest paid to Bank of America is allocated to the numerator of Spartan's FTC limitation calculation. Compute Spartan Corporation's FTC limitation using your calculation from question a and any excess FTC or excess FTC limitation (all of the foreign source income is put in the general category FTC basket).

a. Compute Spartan's foreign source gross income and foreign tax (direct and withholding) for the current year.

b. Assume 20 percent of the interest paid to Bank of America is allocated to the numerator of Spartan's FTC limitation calculation. Compute Spartan Corporation's FTC limitation using your calculation from question a and any excess FTC or excess FTC limitation (all of the foreign source income is put in the general category FTC basket).

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

37

Distinguish between an outbound transaction and an inbound transaction from a U.S. tax perspective.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

38

Distinguish between allocation and apportionment in sourcing deductions in computing the foreign tax credit limitation.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

39

What are the requirements for a foreign corporation to be a controlled foreign corporation for U.S. tax purposes

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

40

Spartan Corporation, a U.S. company, manufactures green eyeshades for sale in the United States and Europe. All manufacturing activities take place in Michigan. During the current year, Spartan sold 10,000 green eyeshades to European customers at a price of $10 each. Each eyeshade costs $4 to produce.

All of Spartan's production assets are located in the United States. For each independent scenario, determine the source of the gross income from sale of the green eyeshades.

a. Spartan ships its eyeshades F.O.B., place of destination.

b. Spartan ships its eyeshades F.O.B., place of shipment.

All of Spartan's production assets are located in the United States. For each independent scenario, determine the source of the gross income from sale of the green eyeshades.

a. Spartan ships its eyeshades F.O.B., place of destination.

b. Spartan ships its eyeshades F.O.B., place of shipment.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

41

Windmill Corporation manufactures products in its plants in Iowa, Canada, Ireland, and Australia. Windmill conducts its operations in Canada through a 50 percent owned joint venture, CanCo. CanCo is treated as a corporation for U.S. and Canadian tax purposes. An unrelated Canadian investor owns the remaining 50 percent. Windmill conducts its operations in Ireland through a wholly owned subsidiary, IrishCo. IrishCo is a controlled foreign corporation for U.S. tax purposes. Windmill conducts its operations in Australia through a wholly owned hybrid entity (KiwiCo) treated as a branch for U.S. tax purposes and a corporation for Australian tax purposes. Windmill also owns a 5 percent interest in a Dutch corporation (TulipCo). During 2011, Windmill reported the following foreign source income from its international operations and investments.

Notes to the table:

1. CanCo and KiwiCo derive all of their earnings from active business operations.

2. The dividend from CanCo carries with it a deemed paid credit (§78 gross-up) of $30,000.

3. The dividend from IrishCo carries with it a deemed paid credit (§78 gross-up) of $4,000.

a. Classify the income received by Windmill and any associated §78 gross-up into the appropriate FTC baskets.

b. Windmill has $1,250,000 of U.S. source gross income. Windmill also incurred SG A of $300,000 that is apportioned between U.S. and foreign source income based on the gross income in each basket. Assume KiwiCo's gross income is $93,000. Compute the FTC limitation for each basket of foreign source income. The corporate tax rate is 35 percent.

Notes to the table:

1. CanCo and KiwiCo derive all of their earnings from active business operations.

2. The dividend from CanCo carries with it a deemed paid credit (§78 gross-up) of $30,000.

3. The dividend from IrishCo carries with it a deemed paid credit (§78 gross-up) of $4,000.

a. Classify the income received by Windmill and any associated §78 gross-up into the appropriate FTC baskets.

b. Windmill has $1,250,000 of U.S. source gross income. Windmill also incurred SG A of $300,000 that is apportioned between U.S. and foreign source income based on the gross income in each basket. Assume KiwiCo's gross income is $93,000. Compute the FTC limitation for each basket of foreign source income. The corporate tax rate is 35 percent.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

42

What are the major U.S. tax issues that apply to an inbound transaction

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

43

Distinguish between a definitely related deduction and a not definitely related deduction in the allocation and apportionment of deductions to foreign source taxable income.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

44

Why does the United States not allow deferral on all foreign source income earned by a controlled foreign corporation

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

45

Falmouth Kettle Company, a U.S. corporation, sells its products in the United States and Europe. During 2011, selling, general, and administrative (SG A) expenses included:

Falmouth had $12,000 of gross sales to U.S. customers and $3,000 of gross sales to European customers. Gross profit (sales minus cost of goods sold) from domestic sales was $3,000 and gross profit from foreign sales was $1,000. ApportionFalmouth's's SG A expenses to foreign source income using the following methods:

a. Gross sales.

b. Gross income.

c. If Falmouth wants to maximize its foreign tax credit limitation, whichmethod produces the better outcome

Falmouth had $12,000 of gross sales to U.S. customers and $3,000 of gross sales to European customers. Gross profit (sales minus cost of goods sold) from domestic sales was $3,000 and gross profit from foreign sales was $1,000. ApportionFalmouth's's SG A expenses to foreign source income using the following methods:a. Gross sales.

b. Gross income.

c. If Falmouth wants to maximize its foreign tax credit limitation, whichmethod produces the better outcome

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

46

Euro Corporation, a U.S. corporation, operates through a branch in Germany. During 2011 the branch reported taxable income of $1,000,000 and paid German income taxes of $300,000. In addition, Shamrock received $50,000 of dividends from its 5% investment in the stock of Maple Leaf Company, a Canadian corporation. The dividend was subject to a withholding tax of $5,000. Euro reported U.S. taxable income from its manufacturing operations of $950,000. Total taxable income was $2,000,000. Precredit U.S. taxes on the taxable income were $680,000. Included in the computation of Euro's taxable income were "definitely allocable" expenses of $500,000, 50% of which were related to the German branch taxable income.

Complete pages 1 and 2 of Form 1118 for just the general category income reported by Euro. You can use the "fill-in" form available on the IRS website, http://www.irs.gov.

Complete pages 1 and 2 of Form 1118 for just the general category income reported by Euro. You can use the "fill-in" form available on the IRS website, http://www.irs.gov.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

47

What are the major U.S. tax issues that apply to an outbound transaction

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

48

Briefly describe the two different methods for apportioning interest expense to foreign source taxable income in the computation of the foreign tax credit limitation.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

49

True or False. A foreign corporation owned equally by 11 U.S. individuals can never be a controlled foreign corporation Explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

50

Owl Vision Corporation (OVC) is a North Carolina corporation engaged in the manufacture and sale of contact lenses and other optical equipment. The company handles its export sales through sales branches in Belgium and Singapore. The average tax book value of OVC's assets for the year was $200 million, of which $160 million generated U.S. source income and $40 million generated foreign source income. The average fair market value of OVC's assets was $240 million, of which $180 million generated U.S. source income and $60 million generated foreign source income. OVC's total interest expense was $20 million.

a. What amount of the interest expense will be apportioned to foreign source income under the tax book value method

b. What amount of the interest expense will be apportioned to foreign source income under the fair market value method

c. If OVC wants to maximize its foreign tax credit limitation, which method produces the better outcome

a. What amount of the interest expense will be apportioned to foreign source income under the tax book value method

b. What amount of the interest expense will be apportioned to foreign source income under the fair market value method

c. If OVC wants to maximize its foreign tax credit limitation, which method produces the better outcome

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

51

USCo, a U.S. corporation, has decided to set up a headquarters subsidiary in Europe. Management has narrowed its location choice to either Spain, Ireland, or Switzerland. The company has asked you to research some of the income tax implications of setting up a corporation in these three countries. In particular, management wants to know what tax rate will be imposed on corporate income earned in the country and the withholding rates applied to interest, dividends, and royalty payments from the subsidiary to USCo.

To answer the tax rate question, consult KPMG's Corporate and Indirect Tax Rate Survey 2010 , which you can access at http://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/Documents/Corp-and-Indirect-Tax-Oct12-2010.pdf. To answer the withholding tax questions, consult the treaties between the United States and Spain, Ireland, and Switzerland, which you can access at http://www.irs.gov (type in "treaties" as your searchword).

To answer the tax rate question, consult KPMG's Corporate and Indirect Tax Rate Survey 2010 , which you can access at http://www.kpmg.com/Global/en/IssuesAndInsights/ArticlesPublications/Documents/Corp-and-Indirect-Tax-Oct12-2010.pdf. To answer the withholding tax questions, consult the treaties between the United States and Spain, Ireland, and Switzerland, which you can access at http://www.irs.gov (type in "treaties" as your searchword).

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

52

How does a residence-based approach to taxing worldwide income differ from a source-based approach to taxing the same income.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

53

Briefly describe the two different methods for apportioning R E to foreign source taxable income in the computation of the foreign tax credit limitation.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

54

What is foreign base company sales income Why does the United States include this income in its definition of subpart F income

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

55

Freon Corporation, a U.S. corporation, manufactures air-conditioning and warm air heating equipment. Freon reported gross sales from this product group of $50,000,000, of which $10,000,000 was foreign source. The gross profit percentage for domestic sales was 15 percent, and the gross profit percentage from non-U.S. sales was 20 percent. Freon incurred R E expenses of $6,000,000, all of which were conducted in the United States.

a. What amount of the R E expense will be apportioned to foreign source income under the sales method

b. What amount of the R E expense will be apportioned to foreign source income under the gross income method

c. If Freon wants to maximize its foreign tax credit limitation, which method produces the better outcome

a. What amount of the R E expense will be apportioned to foreign source income under the sales method

b. What amount of the R E expense will be apportioned to foreign source income under the gross income method

c. If Freon wants to maximize its foreign tax credit limitation, which method produces the better outcome

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

56

Henri is a resident of the United States for U.S. tax purposes and earns $10,000 from an investment in a French company. Will Henri be subject to U.S. tax under a residence-based approach to taxation A source-based approach

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

57

IBM incurs $250 million of R E in the United States. How does the "exclusive apportionment" of this deduction differ depending on the R E apportionment method chosen in the computation of the foreign tax credit limitation

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

58

True or False. Subpart F income is always treated as a deemed dividend to the U.S. shareholders of a controlled foreign corporation. Explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

59

Colleen is a citizen and bona fide resident of Ireland. During 2011, she received the following income:

• Cash dividends of $2,000 from a U.S. corporation's stock.

• Interest of $1,000 on a U.S. corporation bond.• Royalty of $100,000 from a U.S. corporation for use of a patent she developed.• Rent of $3,000 from U.S. individuals renting her cottage in Maine.

Identify the U.S. withholding tax rate on the payment of each item of income under the U.S.-Ireland income tax treaty and cite the appropriate treaty article. You can access the 1997 U.S.-Ireland income tax treaty on the IRS Web site, www.irs.gov

• Cash dividends of $2,000 from a U.S. corporation's stock.

• Interest of $1,000 on a U.S. corporation bond.• Royalty of $100,000 from a U.S. corporation for use of a patent she developed.• Rent of $3,000 from U.S. individuals renting her cottage in Maine.

Identify the U.S. withholding tax rate on the payment of each item of income under the U.S.-Ireland income tax treaty and cite the appropriate treaty article. You can access the 1997 U.S.-Ireland income tax treaty on the IRS Web site, www.irs.gov

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

60

What are the two categories of income that can be taxed by the United States when earned by a nonresident How does the United States tax each category of income

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

61

What is the primary goal of the United States in negotiating income tax treaties with other countries

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

62

True or False. Non subpart F income always qualifies for tax deferral until it is repatriated back to the United States. Explain.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

63

Gameco, a U.S. corporation, operates gambling machines in the United States and abroad. Gameco conducts its operations in Europe through a Dutch B.V., which is treated as a branch for U.S. tax purposes. Gameco also licenses game machines to an unrelated company in Japan. During the current year, Gameco paid the following foreign taxes, translated into U.S. dollars at the appropriate exchange rate:

Identify Gameco's creditable foreign taxes.

Identify Gameco's creditable foreign taxes. Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

64

Maria is not a citizen of the United States, but she spends 180 days per year in the United States on business-related activities. Under what conditions will Maria be considered a resident of the United States for U.S. tax purposes

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

65

What is a permanent establishment and why is it an important part of most income tax treaties

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

66

Camille, a citizen and resident of Country A, received a $1,000 dividend from a corporation organized in Country B. Which statement best describes the taxation of this income under the two different approaches to taxing foreign income

a. Country B will not tax this income under a residence-based jurisdiction approach but will tax this income under a source-based jurisdiction approach.

b. Country B will tax this income under a residence-based jurisdiction approach but will not tax this income under a source-based jurisdiction approach.

c. Country B will tax this income under both a residence-based jurisdiction approach and a source-based jurisdiction approach.

d. Country B will not tax this income under either a residence-based jurisdiction approach or a source-based jurisdiction approach.

a. Country B will not tax this income under a residence-based jurisdiction approach but will tax this income under a source-based jurisdiction approach.

b. Country B will tax this income under a residence-based jurisdiction approach but will not tax this income under a source-based jurisdiction approach.

c. Country B will tax this income under both a residence-based jurisdiction approach and a source-based jurisdiction approach.

d. Country B will not tax this income under either a residence-based jurisdiction approach or a source-based jurisdiction approach.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

67

Sombrero Corporation, a U.S. corporation, operates through a branch in Espania. Management projects that the company's pretax income in the next taxable year will be $100,000, $80,000 from U.S. operations and $20,000 from the branch. Espania taxes corporate income at a rate of 45 percent. The U.S. corporate tax rate is 35 percent.

a. If management's projections are accurate, what will be Sombrero's excess foreign tax credit in the next taxable year Assume all of the income is general category income.

b. Management plans to establish a second branch in Italia. Italia taxes corporate income at a rate of 30 percent. What amount of income will the branch in Italia have to generate to eliminate the excess credit generated by the branch in Espania

a. If management's projections are accurate, what will be Sombrero's excess foreign tax credit in the next taxable year Assume all of the income is general category income.

b. Management plans to establish a second branch in Italia. Italia taxes corporate income at a rate of 30 percent. What amount of income will the branch in Italia have to generate to eliminate the excess credit generated by the branch in Espania

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 67 flashcards in this deck.