Deck 11: Costs and Profit Maximization Under Competition

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

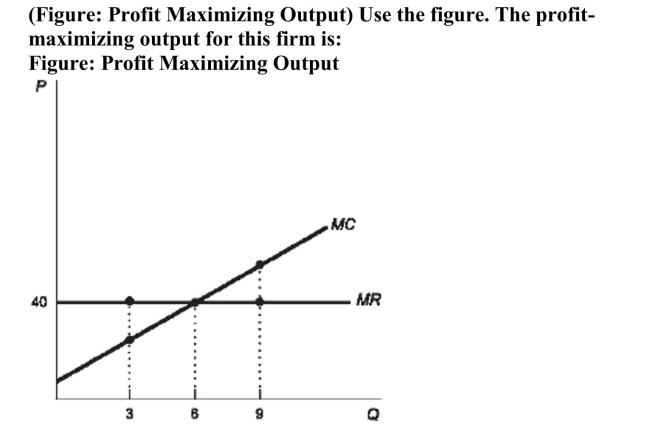

Question

Question

A) 40.

B) 3.

C) 6.

D) 9.

Question

Question

Question

Question

Question

Question

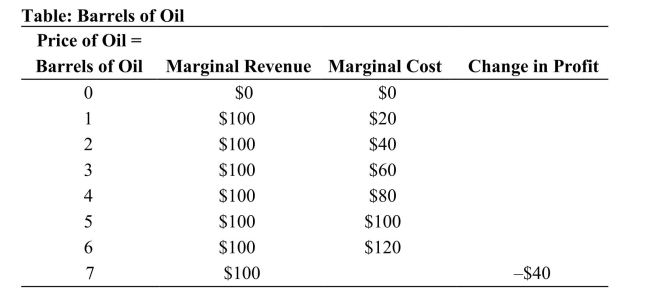

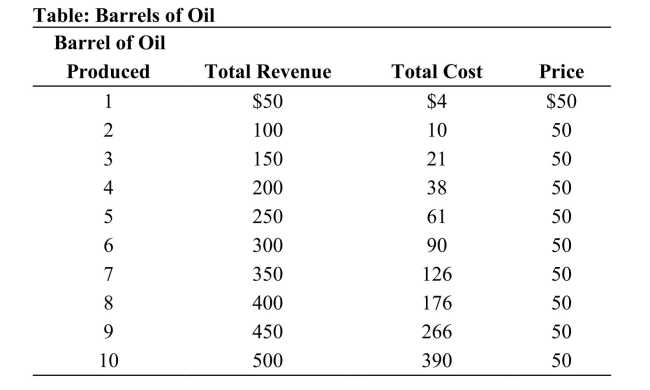

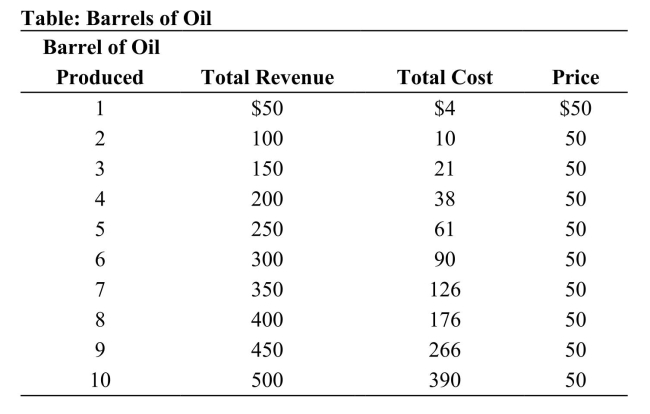

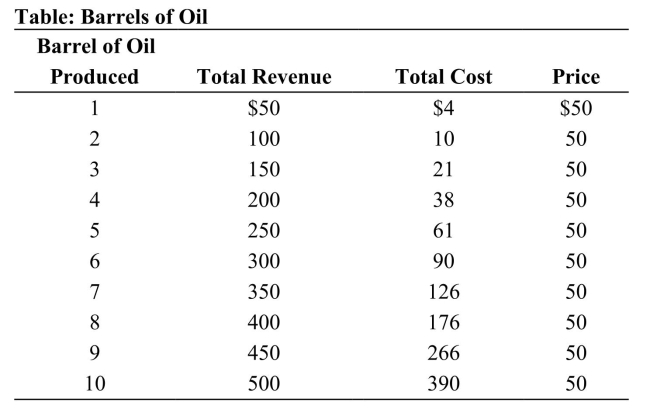

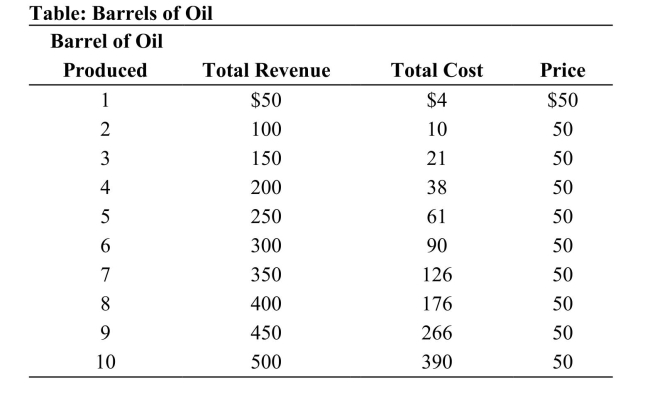

Reference: Ref 11-1 (Table: Barrels of Oil) Refer to the table. The change in profit from producing the second barrel of oil is ________, and the marginal cost from producing the seventh barrel of oil is ________.

Reference: Ref 11-1 (Table: Barrels of Oil) Refer to the table. The change in profit from producing the second barrel of oil is ________, and the marginal cost from producing the seventh barrel of oil is ________.A) $140; $140

B) $100; $20

C) $60; $140

D) $140; $20

Question

Question

Question

Reference: Ref 11-1 (Table: Barrels of Oil) Refer to the table. The profit-maximizing level of output is ________ barrels of oil.

Reference: Ref 11-1 (Table: Barrels of Oil) Refer to the table. The profit-maximizing level of output is ________ barrels of oil.A) 1

B) 3

C) 5

D) 7

Question

Question

Question

Question

Question

Question

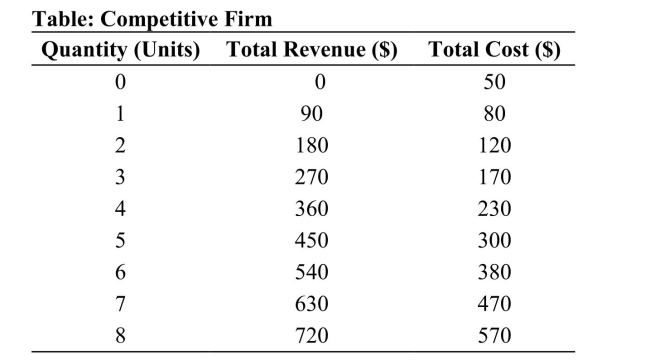

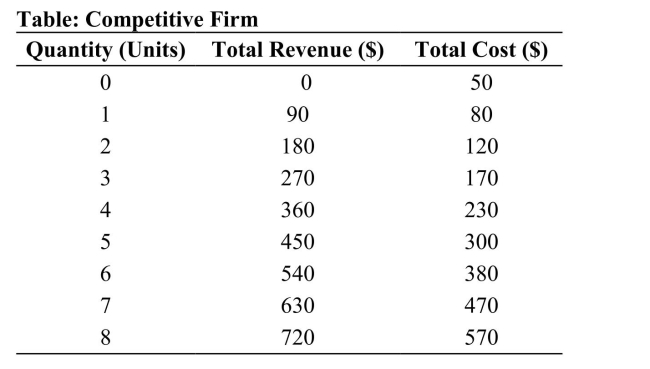

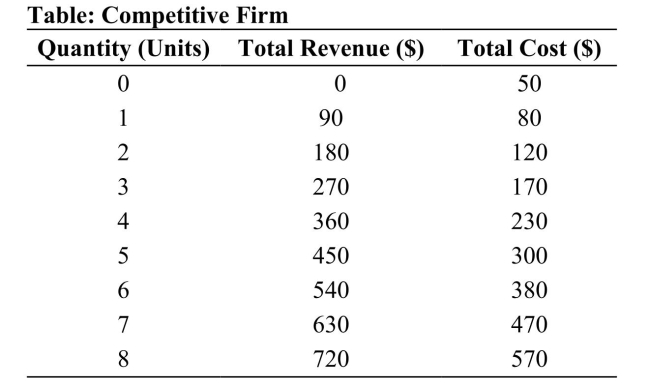

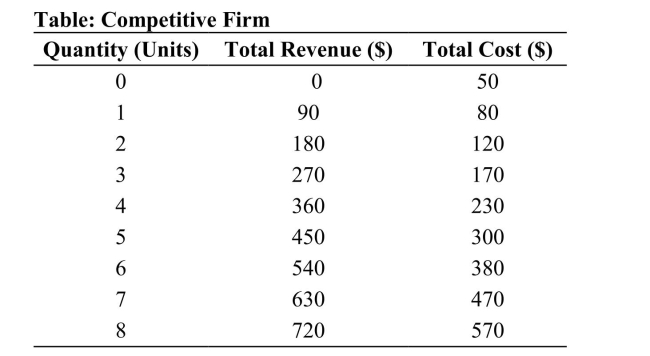

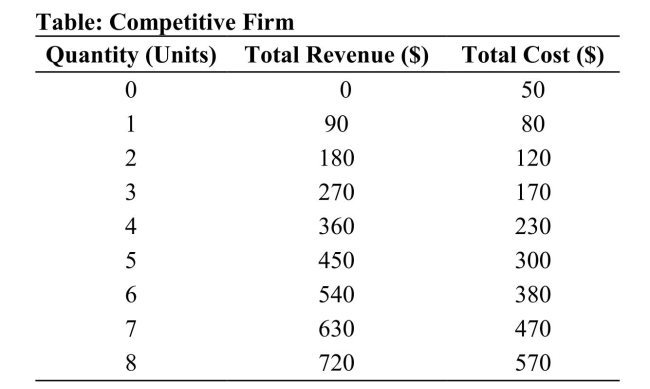

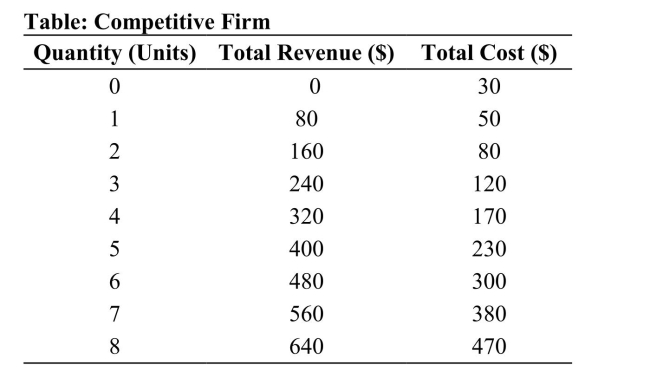

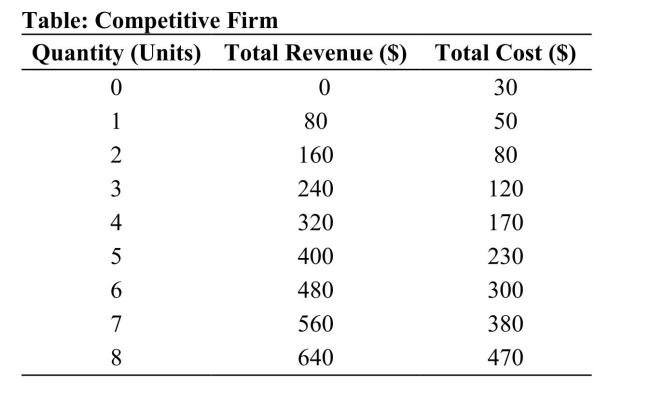

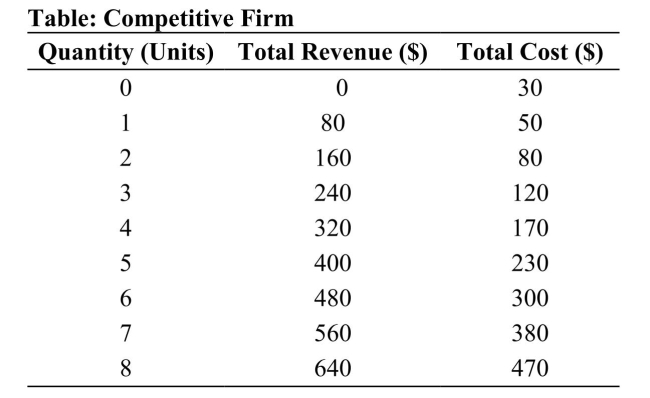

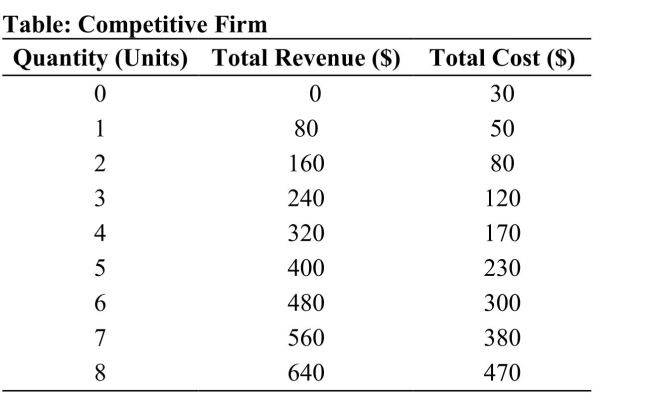

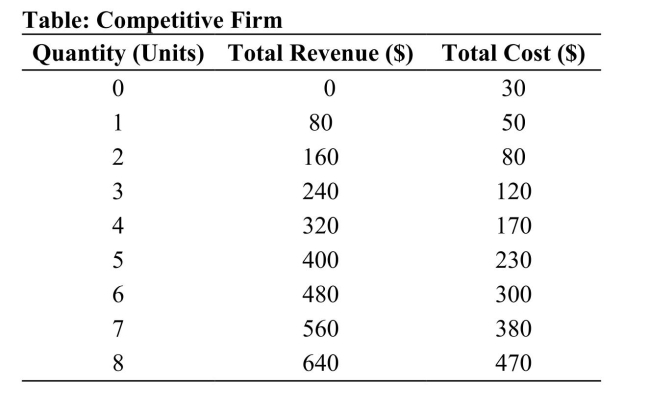

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The profit maximizing output for this firm is:

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The profit maximizing output for this firm is:A) 5.

B) 6.

C) 7.

D) 8.

Question

Question

Reference: Ref 11-3 (Table: Competitive Firm) The marginal revenue for the fifth unit of output is:

Reference: Ref 11-3 (Table: Competitive Firm) The marginal revenue for the fifth unit of output is:A) $70.

B) $90.

C) $450.

D) $20.

Question

Question

Reference: Ref 11-3 (Table: Competitive Firm) The marginal cost of the fifth unit of output is:

Reference: Ref 11-3 (Table: Competitive Firm) The marginal cost of the fifth unit of output is:A) $70.

B) $90.

C) $450.

D) $300.

Question

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. The maximum profit available to the company is:

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. The maximum profit available to the company is:A) $184.

B) $210.

C) $224.

D) $266.

Question

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The market price for the product is:

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The market price for the product is:A) $90.

B) $80.

C) $100.

D) A dollar amount, but it cannot be determined from the information in the table.

Question

Question

Question

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The fixed cost for this firm is:

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The fixed cost for this firm is:A) $80.

B) $90.

C) $50.

D) $100.

Question

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. For the seventh unit of output, total profit is:

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. For the seventh unit of output, total profit is:A) $630.

B) $90.

C) $160.

D) $470.

Question

Question

Question

Question

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. What is the marginal cost of producing the seventh barrel of oil?

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. What is the marginal cost of producing the seventh barrel of oil?A) 36

B) 50

C) 90

D) 126

Question

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. What is the marginal revenue of producing the fifth barrel of oil?

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. What is the marginal revenue of producing the fifth barrel of oil?A) 61

B) 50

C) 200

D) 250

Question

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. How many barrels of oil should the company produce to maximize profit?

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. How many barrels of oil should the company produce to maximize profit?A) 6

B) 7

C) 8

D) 9

Question

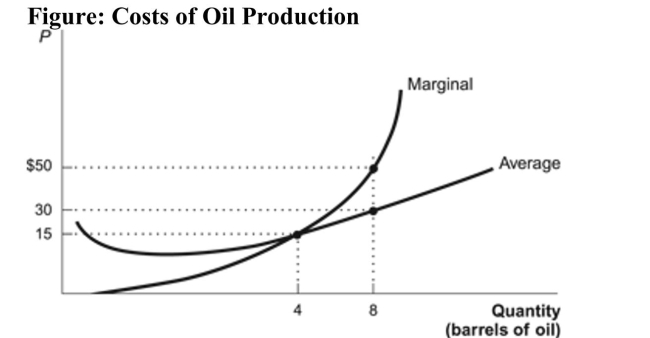

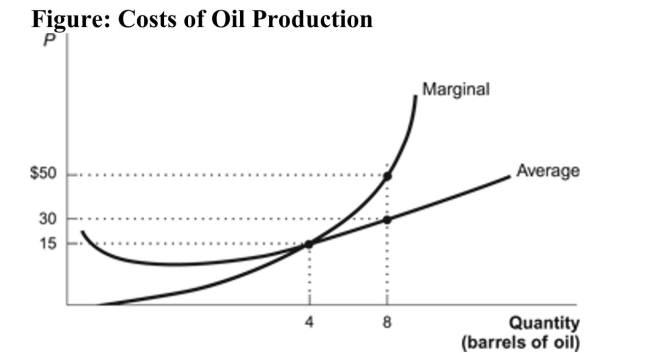

Reference: Ref 11-4 (Figure: Costs of Oil Production) Refer to the figure. Assuming that price equals marginal cost, the total cost of producing eight barrels of oil is:

Reference: Ref 11-4 (Figure: Costs of Oil Production) Refer to the figure. Assuming that price equals marginal cost, the total cost of producing eight barrels of oil is:A) $60.

B) $240.

C) $400.

D) It cannot be determined from the information given.

Question

Question

Question

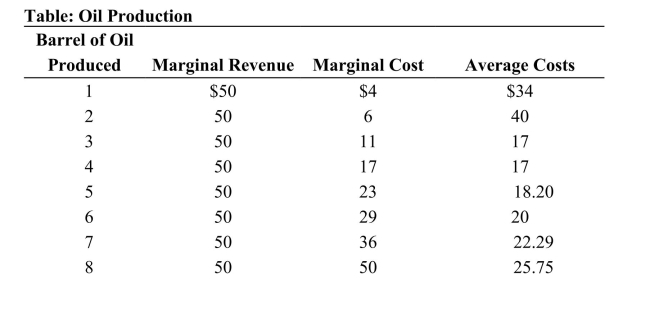

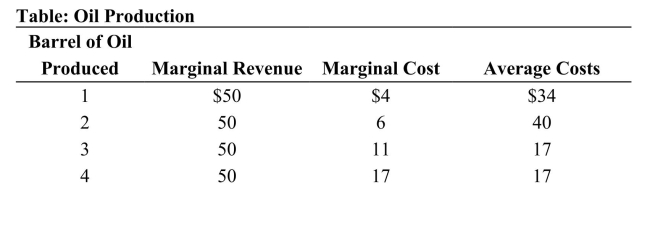

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What is the total cost of producing eight barrels of oil?

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What is the total cost of producing eight barrels of oil?A) $50

B) $206

C) $178

D) $336

Question

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows revenue and cost schedules for a competitive firm. At the profit-maximizing quantity, which of the following is TRUE? I. MR = MC II. Producer surplus is maximized. III. Profits are equal to $180.

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows revenue and cost schedules for a competitive firm. At the profit-maximizing quantity, which of the following is TRUE? I. MR = MC II. Producer surplus is maximized. III. Profits are equal to $180.A) I only

B) I and II only

C) I and III only

D) I, II, and III

Question

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What are the fixed costs of production for this firm?

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What are the fixed costs of production for this firm?A) $34

B) $4

C) $30

D) $50

Question

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What is the profit of producing ten barrels of oil?

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What is the profit of producing ten barrels of oil?A) $80

B) $154

C) $180

D) $194

Question

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the average fixed cost at the profit maximizing quantity?

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the average fixed cost at the profit maximizing quantity?A) $54.30

B) $4.28

C) $50

D) $80

Question

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the marginal cost at the profit maximizing quantity?

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the marginal cost at the profit maximizing quantity?A) $50

B) $80

C) $230

D) $300

Question

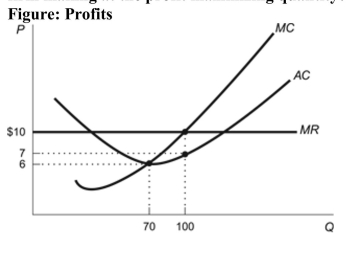

(Figure: Profits) Refer to the figure. How much profit is the firm making at the profit maximizing quantity?

A) a profit of $300

B) a profit of $70

C) The firm is not making a profit-it is making a loss of $300.

D) The firm is not making a profit-it is making a loss of $70.

A) a profit of $300

B) a profit of $70

C) The firm is not making a profit-it is making a loss of $300.

D) The firm is not making a profit-it is making a loss of $70.

Question

Reference: Ref 11-4 (Figure: Costs of Oil Production) Refer to the figure. Assuming that price equals marginal cost, the profit of producing eight barrels of oil is:

Reference: Ref 11-4 (Figure: Costs of Oil Production) Refer to the figure. Assuming that price equals marginal cost, the profit of producing eight barrels of oil is:A) $160.

B) $240.

C) $400

D) It cannot be determined from the information given.

Question

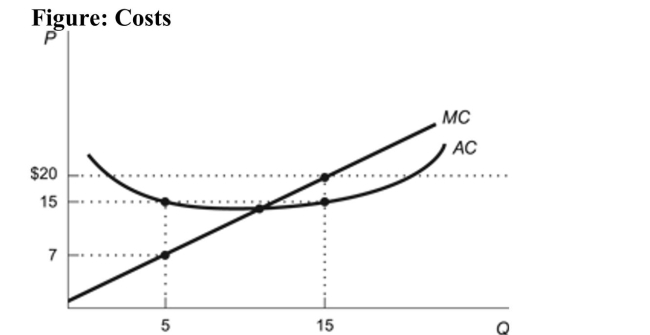

Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20, the firm earns profit of:

Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20, the firm earns profit of:A) $75.

B) $300.

C) $225.

D) $0, because P = MC at P = $20.

Question

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the average cost at the profit maximizing quantity?

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the average cost at the profit maximizing quantity?A) $54.30

B) $58.75

C) $50

D) $80

Question

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the profit maximizing quantity?

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the profit maximizing quantity?A) 5

B) 6

C) 7

D) 8

Question

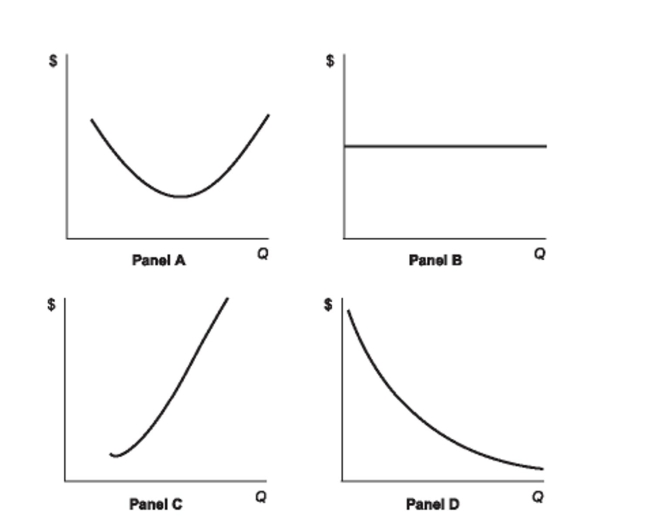

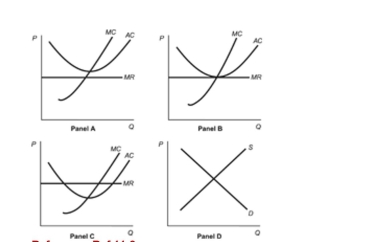

(Figure: AC) Refer to the set of four panels in the figure. Which of the panels shows the typical shape of the average cost curve in a competitive market? Figure: AC

A) Panel A

B) Panel B

C) Panel C

D) Panel D

A) Panel A

B) Panel B

C) Panel C

D) Panel D

Question

Question

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. How much profit will this firm earn?

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. How much profit will this firm earn?A) $0; this firm is making a loss

B) $50

C) $170

D) $180

Question

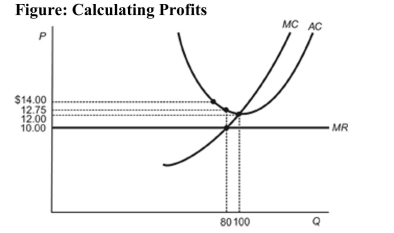

(Figure: Calculating Profits) Refer to the figure. How much profit is the firm making at the profit maximizing quantity?

A) a profit of $200

B) The firm is not making a profit-it is making a loss of $220.

C) The firm is not making a profit-it is making a loss of $200.

D) The firm is not making a profit-it is making a loss of $320.

A) a profit of $200

B) The firm is not making a profit-it is making a loss of $220.

C) The firm is not making a profit-it is making a loss of $200.

D) The firm is not making a profit-it is making a loss of $320.

Question

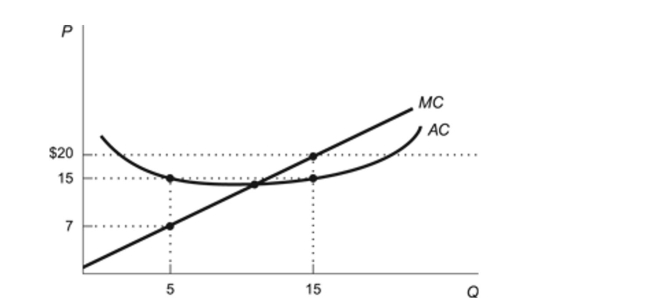

Figure: Costs  Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20 which of the following statements is FALSE?

Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20 which of the following statements is FALSE?

A) AC = $15

B) Profit = (20 - 15)15

C) Average profit = $5

D) MC < AC

Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20 which of the following statements is FALSE?A) AC = $15

B) Profit = (20 - 15)15

C) Average profit = $5

D) MC < AC

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

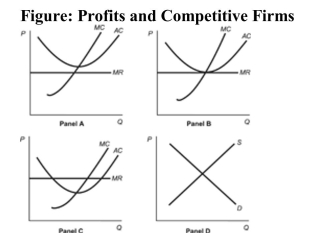

Figure: Profits and Competitive Firms Reference: Ref 11-8  (Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making positive economic profits?

(Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making positive economic profits?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

(Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making positive economic profits?A) Panel A

B) Panel B

C) Panel C

D) Panel D

Question

(Table: Oil Production Costs) Refer to the table. If seven barrels of oil are produced, this firm is making:

A) a profit, because P >AC.

B) a loss, because MC > AC.

C) a profit, because MR > MC.

D) a loss, because TR < TC.

A) a profit, because P >AC.

B) a loss, because MC > AC.

C) a profit, because MR > MC.

D) a loss, because TR < TC.

Question

Figure: Profits and Competitive Firms Reference: Ref 11-8  (Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making an economic loss?

(Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making an economic loss?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

(Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making an economic loss?A) Panel A

B) Panel B

C) Panel C

D) Panel D

Question

Reference: Ref 11-8 (Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making zero economic profits?

Reference: Ref 11-8 (Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making zero economic profits?A) Panel A

B) Panel B

C) Panel C

D) Panel D

Question

Question

Question

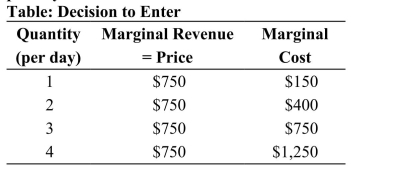

(Table: Decision to Enter) Use the table. A firm is considering whether to enter an industry, with the conditions upon entry set forth in the table. Entering the industry would require the firm to pay $800 per day in fixed costs. This firm should ________ the industry because its profits would be ________ per day.

A) not enter; -$1,350

B) not enter; -$800

C) enter; $700

D) enter; $150

A) not enter; -$1,350

B) not enter; -$800

C) enter; $700

D) enter; $150

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/126

Play

Full screen (f)

Deck 11: Costs and Profit Maximization Under Competition

1

In the small town of Wellsville, there is only one grocery store. Given that everyone needs food, we would expect that:

A) this grocery store is a monopoly and hence highly profitable.

B) this grocery store charges exorbitant prices.

C) this grocery store prices competitively.

D) this grocery store faces a perfectly inelastic demand.

A) this grocery store is a monopoly and hence highly profitable.

B) this grocery store charges exorbitant prices.

C) this grocery store prices competitively.

D) this grocery store faces a perfectly inelastic demand.

C

2

At a ski resort located over one hour from the nearest large town, there is only one grocery store and it charges prices more than 200 percent above the typical retail prices. In the long run, we would expect that:

A) another store will open that will charge equally high prices since competition is low.

B) the store will continue to earn high profits even in the long run since the size of the market is small.

C) demand will decrease since people will not want to pay the high prices.

D) another store will open that will charge lower prices.

A) another store will open that will charge equally high prices since competition is low.

B) the store will continue to earn high profits even in the long run since the size of the market is small.

C) demand will decrease since people will not want to pay the high prices.

D) another store will open that will charge lower prices.

D

3

Marginal cost is:

A) the change in total cost from producing one more unit of output.

B) total cost divided by the change in total output.

C) the change in total output divided by the change in total cost.

D) average cost times output.

A) the change in total cost from producing one more unit of output.

B) total cost divided by the change in total output.

C) the change in total output divided by the change in total cost.

D) average cost times output.

A

4

When there are many buyers and sellers of a good, and the product sold is identical across firms:

A) the demand curve for each firm's output is perfectly elastic.

B) the industry demand curve is perfectly elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic

A) the demand curve for each firm's output is perfectly elastic.

B) the industry demand curve is perfectly elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

5

Profit is defined as:

A) net revenue minus depreciation.

B) average revenue minus average total cost.

C) marginal revenue minus marginal cost.

D) total revenue minus total cost.

A) net revenue minus depreciation.

B) average revenue minus average total cost.

C) marginal revenue minus marginal cost.

D) total revenue minus total cost.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

6

When there are many buyers and sellers of a good, and the product sold is identical across firms:

A) the demand curve for each firm's output is perfectly elastic.

B) the industry demand curve is perfectly elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic.

A) the demand curve for each firm's output is perfectly elastic.

B) the industry demand curve is perfectly elastic.

C) the demand curve for each firm's output is perfectly inelastic.

D) the industry demand curve is perfectly inelastic.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

7

If Homer operates a small bakery and sells donuts for $4/dozen, he should:

A) sell an additional dozen donuts as long as the marginal cost of producing an additional dozen donuts is less than $4.

B) sell an additional dozen donuts as long as the total cost of producing an additional dozen donuts is less than $4.

C) only sell more donuts if his total revenue is greater than his total cost.

D) sell an additional dozen donuts so long as the fixed cost of production is greater than $4.

A) sell an additional dozen donuts as long as the marginal cost of producing an additional dozen donuts is less than $4.

B) sell an additional dozen donuts as long as the total cost of producing an additional dozen donuts is less than $4.

C) only sell more donuts if his total revenue is greater than his total cost.

D) sell an additional dozen donuts so long as the fixed cost of production is greater than $4.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

8

When a firm expands output from 10 to 11 units and total revenue increases from $100 to $110, marginal revenue of the 11th unit is:

A) $110.

B) $11.

C) $10.

D) $210.

A) $110.

B) $11.

C) $10.

D) $210.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

9

A) 40.

B) 3.

C) 6.

D) 9.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

10

A perfectly competitive industry exists under which of the following conditions? I. The product sold is similar across firms. II. There are many sellers, each small relative to the total market. III. There are many sellers, each with total assets less than $2 million. IV. The threat of competition exists from potential sellers that have not yet entered the market.

A) I and II only

B) I, II, and III only

C) I, III, and IV only

D) I, II, and IV only

A) I and II only

B) I, II, and III only

C) I, III, and IV only

D) I, II, and IV only

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

11

The amount of money that the firm pays for its inputs is called:

A) marginal cost.

B) total cost.

C) variable cost.

D) fixed cost.

A) marginal cost.

B) total cost.

C) variable cost.

D) fixed cost.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

12

The total amount of money that a firm receives from sales of its output is called:

A) gross profit.

B) net profit.

C) total revenue.

D) net revenue.

A) gross profit.

B) net profit.

C) total revenue.

D) net revenue.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

13

Firms in a perfectly competitive industry maximize profits by:

A) eliminating the competition.

B) producing a higher quality good and setting a price higher than the competition.

C) setting a price equal to the market price.

D) setting a price less than the market price and undercutting the competition.

A) eliminating the competition.

B) producing a higher quality good and setting a price higher than the competition.

C) setting a price equal to the market price.

D) setting a price less than the market price and undercutting the competition.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

14

The marginal revenue (MR) for a firm is a constant $45, and the firm's marginal cost (MC) is given by MC = 1.5Q (where Q is quantity of output). What is the firm's profit-maximizing level of output?

A) 67.5

B) 30

C) 45

D) 15

A) 67.5

B) 30

C) 45

D) 15

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

15

Reference: Ref 11-1 (Table: Barrels of Oil) Refer to the table. The change in profit from producing the second barrel of oil is ________, and the marginal cost from producing the seventh barrel of oil is ________.A) $140; $140

B) $100; $20

C) $60; $140

D) $140; $20

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

16

Firms in competitive industries: I. can only charge a price equal to the market price. II. cannot charge any more than the market price. III. will earn less profit if they charge less than the market price.

A) I only

B) I and III only

C) II only

D) I, II, and III

A) I only

B) I and III only

C) II only

D) I, II, and III

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is NOT a key decision that a firm must make?

A) what price to set

B) what quantity to produce

C) where to produce

D) when to enter and exit an industry

A) what price to set

B) what quantity to produce

C) where to produce

D) when to enter and exit an industry

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

18

Reference: Ref 11-1 (Table: Barrels of Oil) Refer to the table. The profit-maximizing level of output is ________ barrels of oil.A) 1

B) 3

C) 5

D) 7

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

19

An industry is said to be perfectly competitive when:

A) demand in the industry is high.

B) each firm has virtually no influence over the price of its product.

C) there are many buyers and sellers, and each is large relative to the total market.

D) supply in the industry is highly elastic.

A) demand in the industry is high.

B) each firm has virtually no influence over the price of its product.

C) there are many buyers and sellers, and each is large relative to the total market.

D) supply in the industry is highly elastic.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following statements is TRUE? Economists normally assume that the goal of the firm is to: I. sell as much of their product as possible. II. set the price of their product as high as possible III. maximize profit.

A) I and II only

B) II and III only

C) I and III only

D) III only

A) I and II only

B) II and III only

C) I and III only

D) III only

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

21

For a small firm in an extremely competitive industry, marginal revenue is always equal to price because:

A) the firm has no ability to influence the market price.

B) each firm has large economies of scale.

C) each firm has large fixed costs.

D) if consumers increase their demand for the product, producer surplus falls.

A) the firm has no ability to influence the market price.

B) each firm has large economies of scale.

C) each firm has large fixed costs.

D) if consumers increase their demand for the product, producer surplus falls.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

22

As the price of a good fluctuates, a profit-maximizing firm will expand or contract production along its:

A) average cost curve.

B) average product curve.

C) marginal cost curve.

D) marginal product curve.

A) average cost curve.

B) average product curve.

C) marginal cost curve.

D) marginal product curve.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

23

To maximize profit firms should keep producing as long as marginal revenue is:

A) greater than marginal cost.

B) equal to marginal cost.

C) less than marginal cost.

D) greater than total cost.

A) greater than marginal cost.

B) equal to marginal cost.

C) less than marginal cost.

D) greater than total cost.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

24

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The profit maximizing output for this firm is:A) 5.

B) 6.

C) 7.

D) 8.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

25

Total profit for a given quantity of output can be calculated as:

A) Total Revenue - Total Costs.

B) Marginal Revenue - Marginal Cost.

C) Total Revenue - Marginal Revenue.

D) Marginal Profit + Marginal Revenue.

A) Total Revenue - Total Costs.

B) Marginal Revenue - Marginal Cost.

C) Total Revenue - Marginal Revenue.

D) Marginal Profit + Marginal Revenue.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

26

Reference: Ref 11-3 (Table: Competitive Firm) The marginal revenue for the fifth unit of output is:A) $70.

B) $90.

C) $450.

D) $20.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

27

In their calculation of profit, accountants typically do not take into account:

A) variable costs.

B) fixed costs.

C) opportunity costs.

D) explicit costs.

A) variable costs.

B) fixed costs.

C) opportunity costs.

D) explicit costs.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

28

Reference: Ref 11-3 (Table: Competitive Firm) The marginal cost of the fifth unit of output is:A) $70.

B) $90.

C) $450.

D) $300.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

29

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. The maximum profit available to the company is:A) $184.

B) $210.

C) $224.

D) $266.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

30

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The market price for the product is:A) $90.

B) $80.

C) $100.

D) A dollar amount, but it cannot be determined from the information in the table.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

31

Economic profit differs from accounting profits because of its inclusion of:

A) explicit costs.

B) incidental costs.

C) potential costs.

D) implicit costs.

A) explicit costs.

B) incidental costs.

C) potential costs.

D) implicit costs.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

32

To maximize profit a firm in a competitive market increases output until:

A) P = TC.

B) P = AR.

C) P = MC.

D) P = AC.

A) P = TC.

B) P = AR.

C) P = MC.

D) P = AC.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

33

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. The fixed cost for this firm is:A) $80.

B) $90.

C) $50.

D) $100.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

34

Reference: Ref 11-3 (Table: Competitive Firm) Refer to the table. For the seventh unit of output, total profit is:A) $630.

B) $90.

C) $160.

D) $470.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

35

Damien produces 400 gallons of milk a day in a very competitive industry. The market price for a gallon of milk is $2. Damien's marginal revenue per gallon of milk is:

A) $200.

B) $800.

C) $2.

D) There is not enough information to answer the question.

A) $200.

B) $800.

C) $2.

D) There is not enough information to answer the question.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following statements is FALSE?

A) AC = TC/Q

B) A firm that produces 100 units at a total cost of $500, has an average cost of $5 per unit.

C) Firms will earn positive profits if price exceeds average cost.

D) When marginal cost is below average cost, average cost is rising.

A) AC = TC/Q

B) A firm that produces 100 units at a total cost of $500, has an average cost of $5 per unit.

C) Firms will earn positive profits if price exceeds average cost.

D) When marginal cost is below average cost, average cost is rising.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

37

Profit can be shown graphically by depicting a firm's costs and revenues, and is determined mathematically by calculating the:

A) distance from price to average cost.

B) area of the box that is price times quantity.

C) area of the box that is (price minus average cost) times the quantity.

D) area of the box that is average cost times quantity.

A) distance from price to average cost.

B) area of the box that is price times quantity.

C) area of the box that is (price minus average cost) times the quantity.

D) area of the box that is average cost times quantity.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

38

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. What is the marginal cost of producing the seventh barrel of oil?A) 36

B) 50

C) 90

D) 126

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

39

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. What is the marginal revenue of producing the fifth barrel of oil?A) 61

B) 50

C) 200

D) 250

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

40

Reference: Ref 11-2 (Table: Barrels of Oil) Refer to the table. How many barrels of oil should the company produce to maximize profit?A) 6

B) 7

C) 8

D) 9

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

41

Reference: Ref 11-4 (Figure: Costs of Oil Production) Refer to the figure. Assuming that price equals marginal cost, the total cost of producing eight barrels of oil is:A) $60.

B) $240.

C) $400.

D) It cannot be determined from the information given.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

42

Profit is positive whenever price is greater than:

A) total cost.

B) average cost.

C) fixed cost.

D) marginal cost.

A) total cost.

B) average cost.

C) fixed cost.

D) marginal cost.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

43

Which of the following is TRUE?

A) Price times quantity equals profit.

B) Profit equals marginal revenue minus marginal cost.

C) Profit equals total revenue minus average cost.

D) Profit equals (price minus average cost) times quantity.

A) Price times quantity equals profit.

B) Profit equals marginal revenue minus marginal cost.

C) Profit equals total revenue minus average cost.

D) Profit equals (price minus average cost) times quantity.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

44

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What is the total cost of producing eight barrels of oil?A) $50

B) $206

C) $178

D) $336

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

45

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows revenue and cost schedules for a competitive firm. At the profit-maximizing quantity, which of the following is TRUE? I. MR = MC II. Producer surplus is maximized. III. Profits are equal to $180.A) I only

B) I and II only

C) I and III only

D) I, II, and III

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

46

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What are the fixed costs of production for this firm?A) $34

B) $4

C) $30

D) $50

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

47

Reference: Ref 11-5 (Table: Oil Production) Refer to the table. What is the profit of producing ten barrels of oil?A) $80

B) $154

C) $180

D) $194

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

48

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the average fixed cost at the profit maximizing quantity?A) $54.30

B) $4.28

C) $50

D) $80

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

49

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the marginal cost at the profit maximizing quantity?A) $50

B) $80

C) $230

D) $300

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

50

(Figure: Profits) Refer to the figure. How much profit is the firm making at the profit maximizing quantity?

A) a profit of $300

B) a profit of $70

C) The firm is not making a profit-it is making a loss of $300.

D) The firm is not making a profit-it is making a loss of $70.

A) a profit of $300

B) a profit of $70

C) The firm is not making a profit-it is making a loss of $300.

D) The firm is not making a profit-it is making a loss of $70.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

51

Reference: Ref 11-4 (Figure: Costs of Oil Production) Refer to the figure. Assuming that price equals marginal cost, the profit of producing eight barrels of oil is:A) $160.

B) $240.

C) $400

D) It cannot be determined from the information given.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

52

Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20, the firm earns profit of:A) $75.

B) $300.

C) $225.

D) $0, because P = MC at P = $20.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

53

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the average cost at the profit maximizing quantity?A) $54.30

B) $58.75

C) $50

D) $80

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

54

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. What is the profit maximizing quantity?A) 5

B) 6

C) 7

D) 8

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

55

(Figure: AC) Refer to the set of four panels in the figure. Which of the panels shows the typical shape of the average cost curve in a competitive market? Figure: AC

A) Panel A

B) Panel B

C) Panel C

D) Panel D

A) Panel A

B) Panel B

C) Panel C

D) Panel D

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

56

Stating that TR = TC is equivalent to stating that:

A) MR = MC.

B) P = AC.

C) P = Average fixed cost.

D) MR = P.

A) MR = MC.

B) P = AC.

C) P = Average fixed cost.

D) MR = P.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

57

Reference: Ref 11-7 (Table: Competitive Firm) Refer to the table that shows the revenue and cost schedules for a competitive firm. How much profit will this firm earn?A) $0; this firm is making a loss

B) $50

C) $170

D) $180

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

58

(Figure: Calculating Profits) Refer to the figure. How much profit is the firm making at the profit maximizing quantity?

A) a profit of $200

B) The firm is not making a profit-it is making a loss of $220.

C) The firm is not making a profit-it is making a loss of $200.

D) The firm is not making a profit-it is making a loss of $320.

A) a profit of $200

B) The firm is not making a profit-it is making a loss of $220.

C) The firm is not making a profit-it is making a loss of $200.

D) The firm is not making a profit-it is making a loss of $320.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

59

Figure: Costs Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20 which of the following statements is FALSE?

A) AC = $15

B) Profit = (20 - 15)15

C) Average profit = $5

D) MC < AC

Reference: Ref 11-6 (Figure: Costs) Use the figure. At a price of $20 which of the following statements is FALSE?A) AC = $15

B) Profit = (20 - 15)15

C) Average profit = $5

D) MC < AC

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

60

When the level of production is relatively low, the average cost per unit of output would ________ if output increased.

A) increase

B) decrease

C) either increase or decrease depending on marginal cost

D) remain constant

A) increase

B) decrease

C) either increase or decrease depending on marginal cost

D) remain constant

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following statements is TRUE?

A) Entry and exit from an industry depend on the firm's market share.

B) Fixed costs fall as firms produce more output, the so-called ―spreading of the costs.‖

C) High profits in an industry give entrepreneurs an incentive to enter that industry.

D) A firm should enter an industry if average costs are less than producer surplus.

A) Entry and exit from an industry depend on the firm's market share.

B) Fixed costs fall as firms produce more output, the so-called ―spreading of the costs.‖

C) High profits in an industry give entrepreneurs an incentive to enter that industry.

D) A firm should enter an industry if average costs are less than producer surplus.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

62

Firms should exit the market if:

A) sunk costs are a significant portion of the total cost.

B) producer surplus is just equivalent to recoverable costs.

C) price falls below the average cost.

D) marginal cost exceeds the average cost.

A) sunk costs are a significant portion of the total cost.

B) producer surplus is just equivalent to recoverable costs.

C) price falls below the average cost.

D) marginal cost exceeds the average cost.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following statements are TRUE? A firm's entry/exit decision is about: I. whether profits are positive or negative now. II. whether the stream of future profits is positive or negative. III. government regulations.

A) I, II, and III

B) I only

C) I and II only

D) II and III only

A) I, II, and III

B) I only

C) I and II only

D) II and III only

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

64

Whenever marginal cost is greater than the average total cost:

A) marginal cost is falling.

B) average cost is falling.

C) average cost is constant.

D) average cost is rising.

A) marginal cost is falling.

B) average cost is falling.

C) average cost is constant.

D) average cost is rising.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

65

A baker wants to establish a pie factory. The cost of leasing the factory is $1,000 per day. The profit maximizing quantity of pies is 1,000 pies a day. Each pie sells for $3 and costs only $2.10 to make. Which of the following is a correct conclusion based on this data?

A) The baker will enjoy profits of $900 per day.

B) The baker should not enter the industry.

C) At the profit maximizing quantity, the baker's producer surplus is -$200.

D) The baker will enjoy profits of $3,000 per day.

A) The baker will enjoy profits of $900 per day.

B) The baker should not enter the industry.

C) At the profit maximizing quantity, the baker's producer surplus is -$200.

D) The baker will enjoy profits of $3,000 per day.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following statements about cost is correct?

A) Marginal cost is constant.

B) Marginal cost is always falling.

C) Average total cost is U-shaped.

D) Average total cost always declines.

A) Marginal cost is constant.

B) Marginal cost is always falling.

C) Average total cost is U-shaped.

D) Average total cost always declines.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

67

A firm pays a monthly lease of $10,000 and generates $8,000 of revenue a month. Which of the following is true?

A) Firms will enter the industry.

B) This firm will exit the industry in the long run.

C) The recoverable costs are less than the difference between revenues and variable costs.

D) The recoverable costs are less than operating profit.

A) Firms will enter the industry.

B) This firm will exit the industry in the long run.

C) The recoverable costs are less than the difference between revenues and variable costs.

D) The recoverable costs are less than operating profit.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

68

Profit is positive whenever:

A) P < AC.

B) P < MC.

C) P > MC.

D) P > AC.

A) P < AC.

B) P < MC.

C) P > MC.

D) P > AC.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

69

When marginal cost is rising, the average total costs:

A) could be rising or falling.

B) must be rising.

C) must be falling.

D) must be constant.

A) could be rising or falling.

B) must be rising.

C) must be falling.

D) must be constant.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

70

A firm should exit the industry if which of the following conditions apply?

A) TR > TC

B) P < AC

C) Lifetime expected profit is positive.

D) Prices are low now but expected to rise.

A) TR > TC

B) P < AC

C) Lifetime expected profit is positive.

D) Prices are low now but expected to rise.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

71

Figure: Profits and Competitive Firms Reference: Ref 11-8 (Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making positive economic profits?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

(Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making positive economic profits?A) Panel A

B) Panel B

C) Panel C

D) Panel D

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

72

(Table: Oil Production Costs) Refer to the table. If seven barrels of oil are produced, this firm is making:

A) a profit, because P >AC.

B) a loss, because MC > AC.

C) a profit, because MR > MC.

D) a loss, because TR < TC.

A) a profit, because P >AC.

B) a loss, because MC > AC.

C) a profit, because MR > MC.

D) a loss, because TR < TC.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

73

Figure: Profits and Competitive Firms Reference: Ref 11-8 (Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making an economic loss?

A) Panel A

B) Panel B

C) Panel C

D) Panel D

(Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making an economic loss?A) Panel A

B) Panel B

C) Panel C

D) Panel D

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

74

Reference: Ref 11-8 (Figure: Profits and Competitive Firms) Refer to the four panels in the figure. Which of the panels shows a competitive firm making zero economic profits?A) Panel A

B) Panel B

C) Panel C

D) Panel D

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

75

The typical average cost curve in a competitive market is:

A) an upward sloping straight line because fixed costs are constant, and variable costs are increasing with the level of output.

B) U-shaped because the firm's fixed costs are first spread over greater quantities, but then increasingly greater quantities will create production capacity constraints.

C) downward sloping until fixed costs are eliminated and then it becomes a horizontal line.

D) U-shaped because increasing quantities of output cause a decrease in fixed costs but an offsetting increase in variable costs.

A) an upward sloping straight line because fixed costs are constant, and variable costs are increasing with the level of output.

B) U-shaped because the firm's fixed costs are first spread over greater quantities, but then increasingly greater quantities will create production capacity constraints.

C) downward sloping until fixed costs are eliminated and then it becomes a horizontal line.

D) U-shaped because increasing quantities of output cause a decrease in fixed costs but an offsetting increase in variable costs.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

76

Firms will enter an industry when the:

A) price rises above the minimum of the marginal cost curve.

B) price rises above the minimum of the average total cost curve.

C) marginal cost rises above the minimum of the average total cost curve.

D) average cost rises above the minimum of the marginal cost curve.

A) price rises above the minimum of the marginal cost curve.

B) price rises above the minimum of the average total cost curve.

C) marginal cost rises above the minimum of the average total cost curve.

D) average cost rises above the minimum of the marginal cost curve.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

77

(Table: Decision to Enter) Use the table. A firm is considering whether to enter an industry, with the conditions upon entry set forth in the table. Entering the industry would require the firm to pay $800 per day in fixed costs. This firm should ________ the industry because its profits would be ________ per day.

A) not enter; -$1,350

B) not enter; -$800

C) enter; $700

D) enter; $150

A) not enter; -$1,350

B) not enter; -$800

C) enter; $700

D) enter; $150

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following statements is correct?

A) When the marginal cost curve is above the average cost curve, the average cost curve must be rising.

B) When the marginal cost curve is below the average cost curve, the average cost curve must be rising.

C) When MR = MC, the average cost curve is at its minimum point.

D) When MR = P, the average cost curve is at its minimum point.

A) When the marginal cost curve is above the average cost curve, the average cost curve must be rising.

B) When the marginal cost curve is below the average cost curve, the average cost curve must be rising.

C) When MR = MC, the average cost curve is at its minimum point.

D) When MR = P, the average cost curve is at its minimum point.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

79

A firm should exit an industry if:

A) P < MC.

B) P - AC > 0.

C) P - AC < 0.

D) P - AC = 0.

A) P < MC.

B) P - AC > 0.

C) P - AC < 0.

D) P - AC = 0.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

80

With fluctuating prices in an industry, firms are likely to:

A) immediately exit any time profits are negative.

B) enter any time profits are positive.

C) consider lifetime profits of entering or exiting the industry.

D) act risk averse by producing only where (2 × MR) > MC.

A) immediately exit any time profits are negative.

B) enter any time profits are positive.

C) consider lifetime profits of entering or exiting the industry.

D) act risk averse by producing only where (2 × MR) > MC.

Unlock Deck

Unlock for access to all 126 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 126 flashcards in this deck.