Deck 9: Production Cycle 394

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

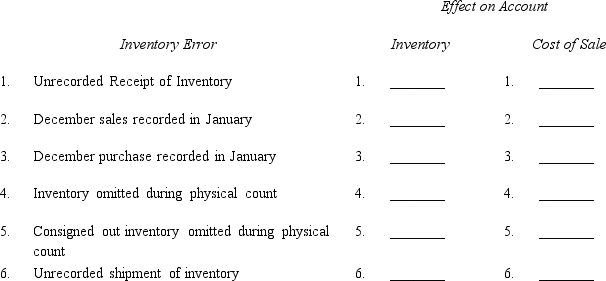

Audit planning requires that the auditor consider possible inventory errors or frauds that might occur that could affect the financial statements. For each of the types of inventory errors listed in the following table, indicate what would be the possible effect in the inventory and cost of sales accounts: overstated, understated, or no effect.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/78

Play

Full screen (f)

Deck 9: Production Cycle 394

1

Your client plans to count inventory at several locations on the same day. No location is material in amount, but the total of inventory is quite material. How is an auditor likely to plan to observe?

A)Observe all counts at all locations by using the required number of auditors.

B)Insist the inventory be counted on separate days so the auditor can be present at all locations.

C)Work with the client to determine which locations to observe.

D)Observe a sample of locations on a surprise basis.

A)Observe all counts at all locations by using the required number of auditors.

B)Insist the inventory be counted on separate days so the auditor can be present at all locations.

C)Work with the client to determine which locations to observe.

D)Observe a sample of locations on a surprise basis.

D

2

Generally accepted accounting principles (GAAP) require that inventory be recorded at

A)the lower of cost or fair market value.

B)the lower of cost or net realizable value.

C)the higher of cost or net realizable value less a normal profit (floor).

D)None of the choices are correct.

A)the lower of cost or fair market value.

B)the lower of cost or net realizable value.

C)the higher of cost or net realizable value less a normal profit (floor).

D)None of the choices are correct.

D

3

A client's physical count of inventories was higher than the inventory quantities shown in the perpetual records. This situation could be the result of the failure to record

A)sales.

B)sales discounts.

C)purchases.

D)purchase discounts.

A)sales.

B)sales discounts.

C)purchases.

D)purchase discounts.

C

4

Selecting a sample of cost accounting reports for labor and vouching it to time records is a procedure designed to test the ASB transaction assertion of

A)occurrence.

B)valuation.

C)completeness.

D)presentation and disclosure.

A)occurrence.

B)valuation.

C)completeness.

D)presentation and disclosure.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

5

L. Martinez, CPA, was auditing a client, Marvelous Retail Company and selected a sample of inventory items from the perpetual records and vouched additions to receiving reports. This procedure was intended to satisfy which PCAOB assertion?

A)Rights and obligations.

B)Completeness.

C)Existence or occurrence.

D)Valuation or allocation.

A)Rights and obligations.

B)Completeness.

C)Existence or occurrence.

D)Valuation or allocation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

6

Periodic or cycle counts of selected inventory items are made at various times during the year rather than during a single inventory count at year-end. Which of the following is necessary if the auditor plans to observe inventories at interim dates?

A)Complete recounts by independent teams are performed.

B)Perpetual inventory records are maintained.

C)Unit cost records are integrated with production accounting records.

D)Inventory balances are rarely at low levels.

A)Complete recounts by independent teams are performed.

B)Perpetual inventory records are maintained.

C)Unit cost records are integrated with production accounting records.

D)Inventory balances are rarely at low levels.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

7

A company's cost accountant periodically reconciles job cost sheets to the work-in-process inventory accounts. This reconciliation is most likely performed to provide assurance that

A)recorded production transactions are valid and documented.

B)valid production transactions are recorded and none omitted.

C)production accounting and posting is complete.

D)production transactions are recorded in the proper period.

A)recorded production transactions are valid and documented.

B)valid production transactions are recorded and none omitted.

C)production accounting and posting is complete.

D)production transactions are recorded in the proper period.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

8

To gain assurance that all inventory items in a client's inventory listing schedule are valid, an auditor most likely would trace

A)inventory tags noted during the auditor's observation to items in the inventory listing schedule.

B)inventory tags noted during the auditor's observation to items listed in receiving reports and vendors' invoices.

C)items in the inventory listing schedule to inventory tags and the auditor's recorded count sheets.

D)items in receiving reports and vendors' invoices to the inventory listing schedule.

A)inventory tags noted during the auditor's observation to items in the inventory listing schedule.

B)inventory tags noted during the auditor's observation to items listed in receiving reports and vendors' invoices.

C)items in the inventory listing schedule to inventory tags and the auditor's recorded count sheets.

D)items in receiving reports and vendors' invoices to the inventory listing schedule.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

9

An auditor selected a product maintained in the finished goods warehouse. The auditor counted the product and compared this amount with the amount in the finished goods perpetual inventory subsidiary account. Which ASB balance assertion is the auditor most likely testing?

A)Existence

B)Completeness

C)Rights and obligations

D)Valuation

A)Existence

B)Completeness

C)Rights and obligations

D)Valuation

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

10

To test the control assertion of completeness in the area of work-in-process inventory, the auditor most likely would

A)select a sample of open and closed production cost reports and recalculate all costs entered.

B)select a sample of issue slips from the raw materials stores file and trace materials-used reports to production cost reports.

C)select a sample of open and closed production cost reports and vouch overhead charges to overhead analysis schedules.

D)select a sample of production orders and determine whether the production orders were authorized.

A)select a sample of open and closed production cost reports and recalculate all costs entered.

B)select a sample of issue slips from the raw materials stores file and trace materials-used reports to production cost reports.

C)select a sample of open and closed production cost reports and vouch overhead charges to overhead analysis schedules.

D)select a sample of production orders and determine whether the production orders were authorized.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

11

Counting different parts of inventory at different times of the year is called

A)LIFO inventory.

B)inventory cutoff.

C)cycle counting.

D)just-in-time inventory.

A)LIFO inventory.

B)inventory cutoff.

C)cycle counting.

D)just-in-time inventory.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

12

Mary Monitor, CPA, noted that ABC Co. received goods prior to year-end that were included in physical inventory but had not been recorded. In this case, which of the following adjustments should be made?

A)Debit purchases/credit cost of goods sold.

B)Debit cost of goods sold/credit accounts payable.

C)Debit inventory/credit accounts payable.

D)None.

A)Debit purchases/credit cost of goods sold.

B)Debit cost of goods sold/credit accounts payable.

C)Debit inventory/credit accounts payable.

D)None.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

13

While observing a client's annual physical inventory, an auditor recorded test counts for several items and noticed that certain test counts were higher than the recorded quantities in the client's perpetual records. This situation could be the result of the client's failure to record

A)purchase discounts.

B)purchase returns.

C)sales.

D)sales returns.

A)purchase discounts.

B)purchase returns.

C)sales.

D)sales returns.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

14

An auditor selected a product recorded in the finished goods perpetual inventory subsidiary account. The auditor went to the warehouse and counted the product and compared this amount with the amount in the finished goods perpetual inventory subsidiary account. Which ASB balance assertion is the auditor most likely testing?

A)Existence

B)Completeness

C)Rights and obligations

D)Valuation

A)Existence

B)Completeness

C)Rights and obligations

D)Valuation

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

15

An auditor selected an invoice for a large inventory purchase and vouched the invoice to the receiving report. Which ASB transaction assertion is the auditor most likely testing?

A)Occurrence

B)Completeness

C)Rights and obligations

D)Valuation

A)Occurrence

B)Completeness

C)Rights and obligations

D)Valuation

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

16

The audit procedures used in an observation of the client's physical inventory taking are designed primarily to

A)test and observe the client's physical count of inventory.

B)verify independently the physical counts obtained by the client.

C)assist the client in taking test counts of year-end inventory.

D)determine whether inventory contains obsolete goods.

A)test and observe the client's physical count of inventory.

B)verify independently the physical counts obtained by the client.

C)assist the client in taking test counts of year-end inventory.

D)determine whether inventory contains obsolete goods.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

17

If overhead is miscalculated so that it is underabsorbed, the result if the error is not corrected will be that

A)inventory will be understated and net income will be overstated.

B)inventory and net income will be overstated.

C)inventory will be overstated and net income will be understated.

D)inventory and net income will be understated.

A)inventory will be understated and net income will be overstated.

B)inventory and net income will be overstated.

C)inventory will be overstated and net income will be understated.

D)inventory and net income will be understated.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following steps would not normally be included in a program for a physical inventory observation?

A)Vouch unit prices to vendors' invoices or other cost records.

B)Obtain the client's inventory counting instructions and review them for completeness.

C)Inspect the tags used and unused and record the tag numbers used.

D)Obtain the numbers of the last five receiving reports and last five shipping documents.

A)Vouch unit prices to vendors' invoices or other cost records.

B)Obtain the client's inventory counting instructions and review them for completeness.

C)Inspect the tags used and unused and record the tag numbers used.

D)Obtain the numbers of the last five receiving reports and last five shipping documents.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

19

An auditor who wished to test for the existence or occurrence of inventory would most likely select a sample of inventory items from the perpetual records and

A)trace additions to the general ledger.

B)vouch additions to receiving reports.

C)vouch additions to sales invoices.

D)trace receipts to receiving reports.

A)trace additions to the general ledger.

B)vouch additions to receiving reports.

C)vouch additions to sales invoices.

D)trace receipts to receiving reports.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

20

An auditor selected an inventory item on the warehouse floor, test counted it, and traced the count to the final inventory compilation. The auditor most likely was testing the PCAOB assertion of

A)existence.

B)valuation.

C)completeness.

D)rights and obligations.

A)existence.

B)valuation.

C)completeness.

D)rights and obligations.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

21

An auditor's tests of controls over the issuance of raw materials to production would most likely include

A)reconciling raw materials and work-in-process perpetual inventory records to general ledger balances.

B)inquiring of the custodian about the procedures followed when defective materials are received from vendors.

C)observing that raw materials are stored in secure areas and that storeroom security is supervised by a responsible individual.

D)examining material requisitions and reperforming client controls designed to process and record issuances.

A)reconciling raw materials and work-in-process perpetual inventory records to general ledger balances.

B)inquiring of the custodian about the procedures followed when defective materials are received from vendors.

C)observing that raw materials are stored in secure areas and that storeroom security is supervised by a responsible individual.

D)examining material requisitions and reperforming client controls designed to process and record issuances.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following is not an acceptable method of determining inventory cost under GAAP?

A)FIFO.

B)LIFO.

C)Average cost.

D)All of the choices are acceptable.

A)FIFO.

B)LIFO.

C)Average cost.

D)All of the choices are acceptable.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

23

Auditors record the last bill of lading used at the time of the inventory count to

A)search for unrecorded sales.

B)test cutoff.

C)verify ownership.

D)All of the choices.

A)search for unrecorded sales.

B)test cutoff.

C)verify ownership.

D)All of the choices.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following methods for determining inventory cost is not allowed by GAAP?

A)Average cost.

B)FIFO.

C)LIFO.

D)Standard cost.

A)Average cost.

B)FIFO.

C)LIFO.

D)Standard cost.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

25

An auditor most likely would make inquiries of production and sales personnel concerning possible obsolete or slow-moving inventory to support management's financial statement (PCAOB) assertion of

A)valuation or allocation.

B)rights and obligations.

C)existence or occurrence.

D)presentation and disclosure.

A)valuation or allocation.

B)rights and obligations.

C)existence or occurrence.

D)presentation and disclosure.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

26

A client maintains perpetual inventory records in quantities and in dollars. If the assessed control risk is high, an auditor would probably

A)apply gross profit tests to ascertain the reasonableness of the physical counts.

B)increase the extent of tests of controls relevant to the inventory cycle.

C)request the client to schedule the physical inventory count at the end of the year.

D)insist that the client perform physical counts of inventory items several times during the year.

A)apply gross profit tests to ascertain the reasonableness of the physical counts.

B)increase the extent of tests of controls relevant to the inventory cycle.

C)request the client to schedule the physical inventory count at the end of the year.

D)insist that the client perform physical counts of inventory items several times during the year.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

27

An auditor reviews job cost sheets to test which transaction assertion?

A)Occurrence.

B)Completeness.

C)Accuracy.

D)Classification.

A)Occurrence.

B)Completeness.

C)Accuracy.

D)Classification.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

28

To make a year-to-year comparison of inventory turnover most meaningful, the auditor will perform the analysis

A)for the company as a whole.

B)by division.

C)by product.

D)All of the choices are correct.

A)for the company as a whole.

B)by division.

C)by product.

D)All of the choices are correct.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

29

A retailer's physical count of inventory was higher than that shown by the perpetual records. Which of the following could explain the difference?

A)Inventory items had been counted but the tags placed on the items had not been taken off and added to the inventory accumulation sheets.

B)Credit memos for several items returned by customers had not been recorded.

C)No journal entry had been made on the retailer's books for several items returned to its suppliers.

D)An item purchased FOB shipping point had not arrived at the date of the inventory count and had not been reflected in the perpetual records.

A)Inventory items had been counted but the tags placed on the items had not been taken off and added to the inventory accumulation sheets.

B)Credit memos for several items returned by customers had not been recorded.

C)No journal entry had been made on the retailer's books for several items returned to its suppliers.

D)An item purchased FOB shipping point had not arrived at the date of the inventory count and had not been reflected in the perpetual records.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

30

An auditor will usually trace the details of the test counts made during the observation of physical inventory counts to a final inventory compilation. This audit procedure is undertaken to provide evidence that items physically present and observed by the auditor at the time of the physical inventory count are

A)owned by the client.

B)not obsolete.

C)physically present at the time of the preparation of the final inventory schedule.

D)included in the final inventory schedule.

A)owned by the client.

B)not obsolete.

C)physically present at the time of the preparation of the final inventory schedule.

D)included in the final inventory schedule.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

31

To determine the client's planned amount and timing of production of a product, the auditor will review the

A)sales forecast.

B)inventory reports.

C)production plan.

D)purchases journal.

A)sales forecast.

B)inventory reports.

C)production plan.

D)purchases journal.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following procedures would best prevent or detect the theft of valuable items from an inventory that consists of hundreds of different items selling for $1 to $10 and a few items selling for hundreds of dollars?

A)Maintain a perpetual inventory of only the more valuable items with frequent periodic verification of the accuracy of the perpetual inventory record.

B)Have an independent accounting firm prepare an internal control report on the effectiveness of the controls over inventory.

C)Have separate warehouse space for the more valuable items with frequent periodic physical counts and comparison to perpetual inventory records.

D)Require a manager's signature for the removal of any inventory item with a value above $50.

A)Maintain a perpetual inventory of only the more valuable items with frequent periodic verification of the accuracy of the perpetual inventory record.

B)Have an independent accounting firm prepare an internal control report on the effectiveness of the controls over inventory.

C)Have separate warehouse space for the more valuable items with frequent periodic physical counts and comparison to perpetual inventory records.

D)Require a manager's signature for the removal of any inventory item with a value above $50.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

33

When auditing inventories, an auditor would least likely verify that

A)all inventory owned by the client is on hand at the time of the count.

B)the client has used proper inventory pricing.

C)the financial statement presentation of inventories is appropriate.

D)damaged goods and obsolete items have been properly accounted for.

A)all inventory owned by the client is on hand at the time of the count.

B)the client has used proper inventory pricing.

C)the financial statement presentation of inventories is appropriate.

D)damaged goods and obsolete items have been properly accounted for.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

34

Inventory count tags are controlled

A)to prevent counting errors.

B)to test cutoff.

C)to prevent subsequent addition of goods to the inventory.

D)for reasons specified in all of the choices.

A)to prevent counting errors.

B)to test cutoff.

C)to prevent subsequent addition of goods to the inventory.

D)for reasons specified in all of the choices.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

35

Counting inventory on the warehouse floor and tracing the count to the inventory compilation provides evidence to support which management (PCAOB) assertion?

A)Existence or occurrence.

B)Completeness.

C)Rights and obligations.

D)Valuation or allocation.

A)Existence or occurrence.

B)Completeness.

C)Rights and obligations.

D)Valuation or allocation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

36

Which cycle is not directly linked to the production cycle?

A)Acquisition and expenditure cycle.

B)Payroll cycle.

C)Revenue and collection cycle.

D)Finance and investment cycle.

A)Acquisition and expenditure cycle.

B)Payroll cycle.

C)Revenue and collection cycle.

D)Finance and investment cycle.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following internal control activities most likely addresses the completeness assertion for inventory?

A)The work-in-process account is periodically reconciled with subsidiary inventory records.

B)Employees responsible for custody of finished goods do not perform the receiving function.

C)Receiving reports are prenumbered and the numbering sequence is checked periodically.

D)There is a separation of duties between the payroll department and inventory accounting personnel.

A)The work-in-process account is periodically reconciled with subsidiary inventory records.

B)Employees responsible for custody of finished goods do not perform the receiving function.

C)Receiving reports are prenumbered and the numbering sequence is checked periodically.

D)There is a separation of duties between the payroll department and inventory accounting personnel.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

38

From the auditors' point of view, inventory counts are more acceptable prior to the year end when

A)internal control is weak.

B)accurate perpetual inventory records are maintained.

C)inventory is slow moving.

D)significant amounts of inventory are held on a consignment basis.

A)internal control is weak.

B)accurate perpetual inventory records are maintained.

C)inventory is slow moving.

D)significant amounts of inventory are held on a consignment basis.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

39

Which of the following is an internal control weakness for a company whose inventory of supplies consists of a large number of individual items?

A)Supplies of relatively little value are expensed when purchased.

B)The cycle basis is used for physical counts.

C)The warehouse manager is responsible for maintenance of perpetual inventory records.

D)Perpetual inventory records are maintained only for items of significant value.

A)Supplies of relatively little value are expensed when purchased.

B)The cycle basis is used for physical counts.

C)The warehouse manager is responsible for maintenance of perpetual inventory records.

D)Perpetual inventory records are maintained only for items of significant value.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

40

An auditor selected items for test counts while observing a client's physical inventory. The auditor then traced the test counts to the client's inventory listing. This procedure most likely obtained evidence concerning management's balance assertion of

A)rights and obligations.

B)completeness.

C)existence.

D)accuracy and valuation.

A)rights and obligations.

B)completeness.

C)existence.

D)accuracy and valuation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

41

The production planner determines what inventory is need for future production using

A)finished goods inventory status report for the product being produced.

B)bill of materials for the product being produced.

C)standard costs for the product being produced.

D)manpower availability report from human resources.

A)finished goods inventory status report for the product being produced.

B)bill of materials for the product being produced.

C)standard costs for the product being produced.

D)manpower availability report from human resources.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

42

Vouching a sample of items from the perpetual inventory records to the receiving reports achieves the specific ASB balance assertion of

A)completeness.

B)occurrence.

C)presentation.

D)valuation.

A)completeness.

B)occurrence.

C)presentation.

D)valuation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

43

The typical functions of the production and conversion includes

A)cash payments for raw materials purchased.

B)inventory planning and control.

C)purchase requisitioning and purchase ordering for inventory.

D)receiving of inventory shipments from vendors.

A)cash payments for raw materials purchased.

B)inventory planning and control.

C)purchase requisitioning and purchase ordering for inventory.

D)receiving of inventory shipments from vendors.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

44

An auditor's observation procedures for inventory may be performed during or after the end of the period under audit under which of the following conditions?

A)When the client maintains periodic inventory records.

B)When the auditor finds minimal variations in client records and test counts in prior periods.

C)When total inventory has not varied more than 5% in the last five years.

D)When well-kept perpetual inventory records are checked by the client periodically by comparisons with physical counts.

A)When the client maintains periodic inventory records.

B)When the auditor finds minimal variations in client records and test counts in prior periods.

C)When total inventory has not varied more than 5% in the last five years.

D)When well-kept perpetual inventory records are checked by the client periodically by comparisons with physical counts.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

45

A production order usually includes a _______.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

46

An auditor would vouch inventory on the inventory status report to the vendor's invoice to obtain evidence concerning management's balance assertions about

A)existence.

B)rights and obligations.

C)completeness.

D)valuation.

A)existence.

B)rights and obligations.

C)completeness.

D)valuation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

47

Maple Company has an increase in purchases from specific vendors and an increase in raw materials inventory for the items purchased from these vendors. Sales for the company have not increased and are not forecast to increase. From this information an auditor might suspect

A)an increase in obsolete raw material inventory.

B)theft of raw material inventory.

C)kickbacks from vendors.

D)poor security over raw material inventory.

A)an increase in obsolete raw material inventory.

B)theft of raw material inventory.

C)kickbacks from vendors.

D)poor security over raw material inventory.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

48

Which of the following auditing procedures probably would provide the most reliable evidence concerning the entity's assertion of rights and obligations related to inventories?

A)Trace test counts noted during the entity's physical count to the entity's summarization of quantities.

B)Inspect agreements to determine whether any inventory is pledged as collateral or subject to any liens.

C)Select the last few shipping documents used before the physical count and determine whether the shipments were recorded as sales.

D)Inspect the open purchase order file for significant commitments that should be considered for disclosure.

A)Trace test counts noted during the entity's physical count to the entity's summarization of quantities.

B)Inspect agreements to determine whether any inventory is pledged as collateral or subject to any liens.

C)Select the last few shipping documents used before the physical count and determine whether the shipments were recorded as sales.

D)Inspect the open purchase order file for significant commitments that should be considered for disclosure.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

49

Your client counts inventory three months before the end of the fiscal year. Internal controls over inventory are excellent. Which procedure is not necessary for the inventory roll-forward?

A)Check that shipping documents for the last three months agree with perpetual records.

B)Tracing receiving reports for the last three months to perpetual records.

C)Compare gross margin percentages for the last three months.

D)Request the client to recount inventory at the end of the year.

A)Check that shipping documents for the last three months agree with perpetual records.

B)Tracing receiving reports for the last three months to perpetual records.

C)Compare gross margin percentages for the last three months.

D)Request the client to recount inventory at the end of the year.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

50

When testing a company's cost accounting system, the auditor uses procedures that are primarily designed to determine that

A)quantities on hand have been computed based on acceptable cost accounting techniques that reasonably approximate actual quantities on hand.

B)physical inventories agree substantially with book inventories.

C)the system is in accordance with generally accepted accounting principles and is functioning as planned.

D)costs have been properly assigned to finished goods, work-in-process, and cost of goods sold.

A)quantities on hand have been computed based on acceptable cost accounting techniques that reasonably approximate actual quantities on hand.

B)physical inventories agree substantially with book inventories.

C)the system is in accordance with generally accepted accounting principles and is functioning as planned.

D)costs have been properly assigned to finished goods, work-in-process, and cost of goods sold.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

51

An auditor is examining a nonpublic company's inventory procurement system and has decided to perform tests of controls. Under which of the following conditions should the auditor perform tests of controls?

A)Significant weaknesses were found in the company's internal control.

B)The auditor hopes to reduce the amount of work to be done in assessing inherent risk.

C)The auditor believes that testing the controls could lead to a reduction in overall audit time and cost.

D)Tests of controls are always performed when the auditor begins to assess control risk.

A)Significant weaknesses were found in the company's internal control.

B)The auditor hopes to reduce the amount of work to be done in assessing inherent risk.

C)The auditor believes that testing the controls could lead to a reduction in overall audit time and cost.

D)Tests of controls are always performed when the auditor begins to assess control risk.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

52

When a production plan is complete the production planner needs to determine

A)what raw materials need to be ordered.

B)labor rates for the jobs are needed to produce the orders.

C)which vendors need to supply raw materials.

D)what equipment needs to be purchased to meet production quotas.

A)what raw materials need to be ordered.

B)labor rates for the jobs are needed to produce the orders.

C)which vendors need to supply raw materials.

D)what equipment needs to be purchased to meet production quotas.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

53

An auditor most likely would analyze inventory turnover rates to obtain evidence concerning management's balance assertions about

A)existence.

B)rights and obligations.

C)completeness.

D)accuracy and valuation.

A)existence.

B)rights and obligations.

C)completeness.

D)accuracy and valuation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following would be considered an analytical procedure?

A)Testing purchasing, shipping, and receiving cutoff activities.

B)Comparing inventory balances to recent sales activities.

C)Projecting the deviation rate of a statistical sample to the population.

D)Reconciling physical counts to perpetual records and general ledger balances.

A)Testing purchasing, shipping, and receiving cutoff activities.

B)Comparing inventory balances to recent sales activities.

C)Projecting the deviation rate of a statistical sample to the population.

D)Reconciling physical counts to perpetual records and general ledger balances.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

55

Production planning interacts with the preparation of _______.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

56

When evaluating inventory controls, an auditor would be least likely to

A)inspect documents.

B)make inquiries.

C)observe procedures.

D)consider policy and procedure manuals.

A)inspect documents.

B)make inquiries.

C)observe procedures.

D)consider policy and procedure manuals.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

57

The auditor tests the quantity of materials charged to work-in-process by vouching these quantities to

A)cost ledgers.

B)perpetual inventory records.

C)receiving reports.

D)material requisitions.

A)cost ledgers.

B)perpetual inventory records.

C)receiving reports.

D)material requisitions.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

58

At the beginning of the observation of the inventory count, the auditor records the last bill of lading used by the company to

A)test inventory cut-off.

B)search for unrecorded sales.

C)verify inventory ownership.

D)record the inventory valuation of items received.

A)test inventory cut-off.

B)search for unrecorded sales.

C)verify inventory ownership.

D)record the inventory valuation of items received.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following is the assertion with the highest inherent risk in auditing inventory?

A)Completeness.

B)Rights.

C)Existence.

D)Properly classification on the balance sheet.

A)Completeness.

B)Rights.

C)Existence.

D)Properly classification on the balance sheet.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

60

_______ are used by the purchasing department to place orders for materials.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

61

Auditors _______ the inventory taking and make _______ , but they seldom _______ the entire inventory.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

62

A material error or fraud in inventory typically has a _______ on financial statements.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

63

A sample from the perpetual inventory records meets the _______ requirement to determine whether all recorded transactions are supported by reports and documents.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

64

A sample from the source documents meets the _______ requirement to determine whether transactions were actually recorded in the inventory records.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

65

Materials requisitions should be compared in the _______ department with the ________ on the production order.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

66

The physical observation procedures for inventory are principally designed to audit for the balance assertions of _______ , _______ , and _______ .

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

67

Selecting inventory from locations on the warehouse floor, obtaining a test count, and tracing the count to the final inventory compilation produces evidence for the _______ ASB balance assertion.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

68

_______ can be used in connection with knowledge of the shape of management's plans for the year under audit.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

69

Audit planning requires that the auditor consider possible inventory errors or frauds that might occur that could affect the financial statements. For each of the types of inventory errors listed in the following table, indicate what would be the possible effect in the inventory and cost of sales accounts: overstated, understated, or no effect.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

70

An inventory trial balance can be used to scan for _______ and as a population for sample selection for the _______ .

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

71

Prepare an audit plan for inventory pricing and compilation.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

72

Tracing production cost accumulation forward into the production cost reports in the cost accounting department is a test for _______ .

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

73

The auditors of Mikel's Shops obtained the following information when performing cutoff testing procedures during their observation of Mikel's physical inventory count at December 31, 2020:

When comparing the cutoff information to the sales records, the auditors found that all these shipments were recorded as 2020 sales. The goods shipped on bills of lading 1235 and 1236 were not counted in the inventory, but the goods on bill of lading 1237 and 1238 were included.Required:Prepare the appropriate journal entry to correct the cutoff error. (If no entry is required for a transaction/event, select "No journal entry required")

When comparing the cutoff information to the sales records, the auditors found that all these shipments were recorded as 2020 sales. The goods shipped on bills of lading 1235 and 1236 were not counted in the inventory, but the goods on bill of lading 1237 and 1238 were included.Required:Prepare the appropriate journal entry to correct the cutoff error. (If no entry is required for a transaction/event, select "No journal entry required")

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

74

Production reports of finished units should be signed by the _______ and finished goods inventory custodian and forwarded to _______ .

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

75

The function of _______ refers to comparing the physical count of inventory to the perpetual inventory records.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

76

The cost accounting department at Blue Manufacturing Company receives various types of information at the end of each week. The production floor reports time and production work data directly to the cost accounting department. Also, the payroll department sends labor cost data to the cost accounting department. What is the cost accounting department likely to do with this information? Why?

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

78

Prepare an audit plan for the observation of an inventory count.

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

79

With a sample of open and closed production cost reports, vouching labor cost to ________ is a test for ________ .

Unlock Deck

Unlock for access to all 78 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 78 flashcards in this deck.