Deck 21: Management: Employment Discrimination

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Escott v BarChris Constr. Corp.

283 F. Supp. 643 (S.D.N.Y. 1968)

Bowling for Fraud: Right Up Our Alley

FACTS

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid- 1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By 1960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

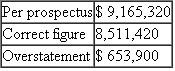

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered on the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

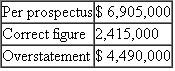

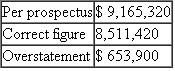

1. 1960 Earnings

(a) Sales

(b) Net Operating Income

(b) Net Operating Income

(c) Earnings per Share

(c) Earnings per Share

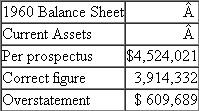

2. 1960 Balance Sheet

2. 1960 Balance Sheet

Current Assets

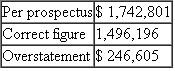

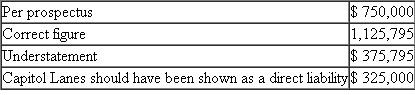

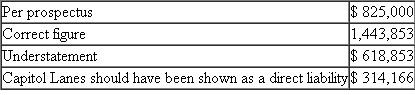

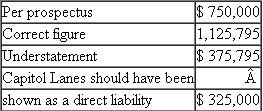

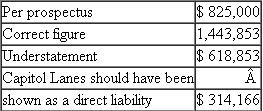

3. Contingent Liabilities as of December 31, 1960, on Alternative Method of Financing

3. Contingent Liabilities as of December 31, 1960, on Alternative Method of Financing

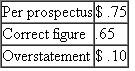

4. Contingent Liabilities as of April 30, 1961

4. Contingent Liabilities as of April 30, 1961

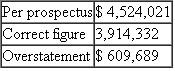

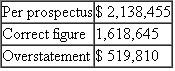

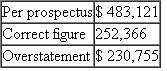

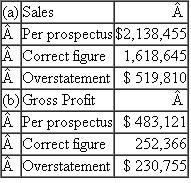

5. Earnings Figures for Quarter Ending

5. Earnings Figures for Quarter Ending

March 31, 1961

(a) Sales

(b) Gross Profit

(b) Gross Profit

6. Backlog as of March 31, 1961

6. Backlog as of March 31, 1961

7. Failure to Disclose Officers' Loans Outstanding and Unpaid on

7. Failure to Disclose Officers' Loans Outstanding and Unpaid on

0

0

8. Failure to Disclose Use of Proceeds in Manner Not Revealed in Prospectus: Approx. $1,160,000

9. Failure to Disclose Customers' Delinquencies in May 1961 and BarChris's Potential Liability with Respect Thereto: Over $1,350,000

10. Failure to Disclose the Fact that BarChris Was Already Engaged and Was About to Be More Heavily Engaged in the Operation of Bowling Alleys

The federal district court reviewed all of the exhibits and statements included in the prospectus and dealt with each defendant individually in issuing its decisions. The defendants consisted of those officers and directors who signed the registration statement, the underwriters of the debenture offering, the auditors (Peat, Marwick, Mitchell Co.5), and BarChris's attorneys and directors.

JUDICIAL OPINION

McLEAN, District Judge

Russo. Russo was, to all intents and purposes, the chief executive officer of BarChris. He was a member of the executive committee. He was familiar with all aspects of the business. He was personally in charge of dealings with the factors. He acted on BarChris's behalf in making the financing agreement with Talcott and he handled the negotiations with Talcott in the spring of 1961. He talked with customers about their delinquencies.

Russo prepared the list of jobs which went into the backlog figure. He knew the status of those jobs.

It was Russo who arranged for the temporary increase in BarChris's cash in banks on December 31, 1960, a transaction which borders on the fraudulent. He was thoroughly aware of BarChris's stringent financial condition in May 1961. He had personally advanced large sums to BarChris of which $175,000 remained unpaid as of May 16.

In short, Russo knew all the relevant facts. He could not have believed that there were no untrue statements or material omissions in the prospectus. Russo has no due diligence defenses.

Vitolo and Pugliese. They were the founders of the business who stuck with it to the end. Vitolo was president and Pugliese was vice president. Despite their titles, their field of responsibility in the administration of BarChris's affairs during the period in question seems to have been less all-embracing than Russo's. Pugliese in particular appears to have limited his activities to supervising the actual construction work. Vitolo and Pugliese are each men of limited education. It is not hard to believe that for them the prospectus was difficult reading, if indeed they read it at all.

But whether it was or not is irrelevant. The liability of a director who signs a registration statement does not depend upon whether or not he read it or, if he did, whether or not he understood what he was reading.

And in any case, Vitolo and Pugliese were not as naive as they claim to be. They were members of BarChris's executive committee. At meetings of that committee BarChris's affairs were discussed at length. They must have known what was going on. Certainly they knew of the inadequacy of cash in 1961. They knew of their own large advances to the company which remained unpaid. They knew that they had agreed not to deposit their checks until the financing proceeds were received. They knew and intended that part of the proceeds were to be used to pay their own loans.

All in all, the position of Vitolo and Pugliese is not significantly different, for present purposes, from Russo's. They could not have believed that the registration statement was wholly true and that no material facts had been omitted. And in any case, there is nothing to show that they made any investigation of anything which they may not have known about or understood. They have not proved their due diligence defenses.

Kircher. Kircher was treasurer of BarChris and its chief financial officer. He is a certified public accountant and an intelligent man. He was thoroughly familiar with BarChris's financial affairs. He knew the terms of BarChris's agreements with Talcott. He knew of the customers' delinquency problems. He participated actively with Russo in May 1961 in the successful effort to hold Talcott off until the financing proceeds came in. He knew how the financing proceeds were to be applied and he saw to it that they were so applied. He arranged the officers' loans and he knew all the facts concerning them.

Moreover, as a member of the executive committee, Kircher was kept informed as to those branches of the business of which he did not have direct charge. He knew about the operation of alleys, present and prospective. In brief, Kircher knew all the relevant facts.

Knowing the facts, Kircher had reason to believe that the expertised portion of the prospectus, i.e., the 1960 figures, was in part incorrect. He could not shut his eyes to the facts and rely on Peat, Marwick for that portion.

As to the rest of the prospectus, knowing the facts, he did not have a reasonable ground to believe it to be true. On the contrary, he must have known that in part it was untrue. Under these circumstances, he was not entitled to sit back and place the blame on the lawyers for not advising him about it. Kircher has not proved his due diligence defenses.

Trilling. Trilling's position is somewhat different from Kircher's. He was BarChris's controller. He signed the registration statement in that capacity, although he was not a director.

Trilling entered BarChris's employ in October 1960. He was Kircher's subordinate. When Kircher asked him for information, he furnished it. On at least one occasion he got it wrong.

Trilling may well have been unaware of several of the inaccuracies in the prospectus. But he must have known of some of them. As a financial officer, he was familiar with BarChris's finances and with its books of account. He knew that part of the cash on deposit on December 31, 1960, had been procured temporarily by Russo for window dressing purposes. He should have known, although perhaps through carelessness he did not know at the time, that BarChris's contingent liability was greater than the prospectus stated. In the light of these facts, I cannot find that Trilling believed the entire prospectus to be true.

But even if he did, he still did not establish his due diligence defenses. He did not prove that as to the parts of the prospectus expertised by Peat, Marwick he had no reasonable ground to believe that it was untrue. He also failed to prove, as to the parts of the prospectus not expertised by Peat, Marwick, that he made a reasonable investigation which afforded him a reasonable ground to believe that it was true. As far as appears, he made no investigation. As a signer, he could not avoid responsibility by leaving it up to others to make it accurate. Trilling did not sustain the burden of proving his due diligence defenses.

Birnbaum. Birnbaum was a young lawyer, admitted to the bar in 1957, who, after brief periods of employment by two different law firms and an equally brief period of practicing in his own firm, was employed by BarChris as house counsel and assistant secretary in October 1960. Unfortunately for him, he became secretary and director of BarChris on April 17, 1961, after the first version of the registration statement had been filed with the Securities and Exchange Commission. He signed the later amendments, thereby becoming responsible for the accuracy of the prospectus in its final form.

It seems probable that Birnbaum did not know of many of the inaccuracies in the prospectus. He must, however, have appreciated some of them. In any case, he made no investigation and relied on the others to get it right. Unlike Trilling, he was entitled to rely upon Peat, Marwick for the 1960 figures, for as far as appears, he had no personal knowledge of the company's books of account or financial transactions. As a lawyer, he should have known his obligations under the statute. He should have known that he was required to make a reasonable investigation of the truth of all the statements in the unexpertised portion of the document which he signed. Having failed to make such an investigation, he did not have reasonable ground to believe that all these statements were true. Birnbaum has not established his due diligence defenses except as to the audited 1960 exhibits.

Auslander. Auslander was an "outside" director, i.e., one who was not an officer of BarChris. He was chairman of the board of Valley Stream National Bank in Valley Stream, Long Island. In February 1961 Vitolo asked him to become a director of BarChris. As an inducement, Vitolo said that when BarChris received the proceeds of a forthcoming issue of securities, it would deposit $1 million in Auslander's bank.

Auslander was elected a director on April 17, 1961. The registration statement in its original form had already been filed, of course without his signature. On May 10, 1961, he signed a signature page for the first amendment to the registration statement which was filed on May 11, 1961. This was a separate sheet without any document attached. Auslander did not know that it was a signature page for a registration statement. He vaguely understood that it was something "for the SEC."

Auslander attended a meeting of BarChris's directors on May 15, 1961. At that meeting he, along with the other directors, signed the signature sheet for the second amendment which constituted the registration statement in its final form. Again, this was only a separate sheet without any document attached. Auslander never saw a copy of the registration statement in its final form. It is true that Auslander became a director on the eve of the financing. He had little opportunity to familiarize himself with the company's affairs.

Section 11 imposes liability in the first instance upon a director, no matter how new he is.

Peat, Marwick. Peat, Marwick's work was in general charge of a member of the firm, Cummings, and more immediately in charge of Peat, Marwick's manager, Logan. Most of the actual work was performed by a senior accountant, Berardi, who had junior assistants, one of whom was Kennedy.

Berardi was then about thirty years old. He was not yet a CPA. He had had no previous experience with the bowling industry. This was his first job as a senior accountant. He could hardly have been given a more difficult assignment.

After obtaining a little background information on BarChris by talking to Logan and reviewing Peat, Marwick's work papers on its 1959 audit, Berardi examined the results of test checks of BarChris's accounting procedures which one of the junior accountants had made, and he prepared an "internal control questionnaire" and an "audit program." Thereafter, for a few days subsequent to December 30, 1960, he inspected BarChris's inventories and examined certain alley construction. Finally, on January 13, 1961, he began his auditing work which he carried on substantially continuously until it was completed on February 24, 1961. Toward the close of the work, Logan reviewed it and made various comments and suggestions to Berardi.

It is unnecessary to recount everything that Berardi did in the course of the audit. We are concerned only with the evidence relating to what Berardi did or did not do with respect to those items found to have been incorrectly reported in the 1960 figures in the prospectus.

Accountants should not be held to a standard higher than that recognized in their profession. I do not do so here. Berardi's review did not come up to that standard. He did not take some of the steps which Peat, Marwick's written program prescribed. He did not spend an adequate amount of time on a task of this magnitude. Most important of all, he was too easily satisfied with glib answers to his inquiries.

This is not to say that he should have made a complete audit. But there were enough danger signals in the materials which he did examine to require some further investigation on his part. Generally accepted accounting standards required such further investigation under these circumstances. It is not always sufficient merely to ask questions.

How much time transpired between the sale of the debentures and BarChris's bankruptcy?

283 F. Supp. 643 (S.D.N.Y. 1968)

Bowling for Fraud: Right Up Our Alley

FACTS

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid- 1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By 1960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered on the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

1. 1960 Earnings

(a) Sales

(b) Net Operating Income (c) Earnings per Share 2. 1960 Balance Sheet Current Assets

3. Contingent Liabilities as of December 31, 1960, on Alternative Method of Financing 4. Contingent Liabilities as of April 30, 1961 5. Earnings Figures for Quarter Ending March 31, 1961

(a) Sales

(b) Gross Profit 6. Backlog as of March 31, 1961 7. Failure to Disclose Officers' Loans Outstanding and Unpaid on 08. Failure to Disclose Use of Proceeds in Manner Not Revealed in Prospectus: Approx. $1,160,000

9. Failure to Disclose Customers' Delinquencies in May 1961 and BarChris's Potential Liability with Respect Thereto: Over $1,350,000

10. Failure to Disclose the Fact that BarChris Was Already Engaged and Was About to Be More Heavily Engaged in the Operation of Bowling Alleys

The federal district court reviewed all of the exhibits and statements included in the prospectus and dealt with each defendant individually in issuing its decisions. The defendants consisted of those officers and directors who signed the registration statement, the underwriters of the debenture offering, the auditors (Peat, Marwick, Mitchell Co.5), and BarChris's attorneys and directors.

JUDICIAL OPINION

McLEAN, District Judge

Russo. Russo was, to all intents and purposes, the chief executive officer of BarChris. He was a member of the executive committee. He was familiar with all aspects of the business. He was personally in charge of dealings with the factors. He acted on BarChris's behalf in making the financing agreement with Talcott and he handled the negotiations with Talcott in the spring of 1961. He talked with customers about their delinquencies.

Russo prepared the list of jobs which went into the backlog figure. He knew the status of those jobs.

It was Russo who arranged for the temporary increase in BarChris's cash in banks on December 31, 1960, a transaction which borders on the fraudulent. He was thoroughly aware of BarChris's stringent financial condition in May 1961. He had personally advanced large sums to BarChris of which $175,000 remained unpaid as of May 16.

In short, Russo knew all the relevant facts. He could not have believed that there were no untrue statements or material omissions in the prospectus. Russo has no due diligence defenses.

Vitolo and Pugliese. They were the founders of the business who stuck with it to the end. Vitolo was president and Pugliese was vice president. Despite their titles, their field of responsibility in the administration of BarChris's affairs during the period in question seems to have been less all-embracing than Russo's. Pugliese in particular appears to have limited his activities to supervising the actual construction work. Vitolo and Pugliese are each men of limited education. It is not hard to believe that for them the prospectus was difficult reading, if indeed they read it at all.

But whether it was or not is irrelevant. The liability of a director who signs a registration statement does not depend upon whether or not he read it or, if he did, whether or not he understood what he was reading.

And in any case, Vitolo and Pugliese were not as naive as they claim to be. They were members of BarChris's executive committee. At meetings of that committee BarChris's affairs were discussed at length. They must have known what was going on. Certainly they knew of the inadequacy of cash in 1961. They knew of their own large advances to the company which remained unpaid. They knew that they had agreed not to deposit their checks until the financing proceeds were received. They knew and intended that part of the proceeds were to be used to pay their own loans.

All in all, the position of Vitolo and Pugliese is not significantly different, for present purposes, from Russo's. They could not have believed that the registration statement was wholly true and that no material facts had been omitted. And in any case, there is nothing to show that they made any investigation of anything which they may not have known about or understood. They have not proved their due diligence defenses.

Kircher. Kircher was treasurer of BarChris and its chief financial officer. He is a certified public accountant and an intelligent man. He was thoroughly familiar with BarChris's financial affairs. He knew the terms of BarChris's agreements with Talcott. He knew of the customers' delinquency problems. He participated actively with Russo in May 1961 in the successful effort to hold Talcott off until the financing proceeds came in. He knew how the financing proceeds were to be applied and he saw to it that they were so applied. He arranged the officers' loans and he knew all the facts concerning them.

Moreover, as a member of the executive committee, Kircher was kept informed as to those branches of the business of which he did not have direct charge. He knew about the operation of alleys, present and prospective. In brief, Kircher knew all the relevant facts.

Knowing the facts, Kircher had reason to believe that the expertised portion of the prospectus, i.e., the 1960 figures, was in part incorrect. He could not shut his eyes to the facts and rely on Peat, Marwick for that portion.

As to the rest of the prospectus, knowing the facts, he did not have a reasonable ground to believe it to be true. On the contrary, he must have known that in part it was untrue. Under these circumstances, he was not entitled to sit back and place the blame on the lawyers for not advising him about it. Kircher has not proved his due diligence defenses.

Trilling. Trilling's position is somewhat different from Kircher's. He was BarChris's controller. He signed the registration statement in that capacity, although he was not a director.

Trilling entered BarChris's employ in October 1960. He was Kircher's subordinate. When Kircher asked him for information, he furnished it. On at least one occasion he got it wrong.

Trilling may well have been unaware of several of the inaccuracies in the prospectus. But he must have known of some of them. As a financial officer, he was familiar with BarChris's finances and with its books of account. He knew that part of the cash on deposit on December 31, 1960, had been procured temporarily by Russo for window dressing purposes. He should have known, although perhaps through carelessness he did not know at the time, that BarChris's contingent liability was greater than the prospectus stated. In the light of these facts, I cannot find that Trilling believed the entire prospectus to be true.

But even if he did, he still did not establish his due diligence defenses. He did not prove that as to the parts of the prospectus expertised by Peat, Marwick he had no reasonable ground to believe that it was untrue. He also failed to prove, as to the parts of the prospectus not expertised by Peat, Marwick, that he made a reasonable investigation which afforded him a reasonable ground to believe that it was true. As far as appears, he made no investigation. As a signer, he could not avoid responsibility by leaving it up to others to make it accurate. Trilling did not sustain the burden of proving his due diligence defenses.

Birnbaum. Birnbaum was a young lawyer, admitted to the bar in 1957, who, after brief periods of employment by two different law firms and an equally brief period of practicing in his own firm, was employed by BarChris as house counsel and assistant secretary in October 1960. Unfortunately for him, he became secretary and director of BarChris on April 17, 1961, after the first version of the registration statement had been filed with the Securities and Exchange Commission. He signed the later amendments, thereby becoming responsible for the accuracy of the prospectus in its final form.

It seems probable that Birnbaum did not know of many of the inaccuracies in the prospectus. He must, however, have appreciated some of them. In any case, he made no investigation and relied on the others to get it right. Unlike Trilling, he was entitled to rely upon Peat, Marwick for the 1960 figures, for as far as appears, he had no personal knowledge of the company's books of account or financial transactions. As a lawyer, he should have known his obligations under the statute. He should have known that he was required to make a reasonable investigation of the truth of all the statements in the unexpertised portion of the document which he signed. Having failed to make such an investigation, he did not have reasonable ground to believe that all these statements were true. Birnbaum has not established his due diligence defenses except as to the audited 1960 exhibits.

Auslander. Auslander was an "outside" director, i.e., one who was not an officer of BarChris. He was chairman of the board of Valley Stream National Bank in Valley Stream, Long Island. In February 1961 Vitolo asked him to become a director of BarChris. As an inducement, Vitolo said that when BarChris received the proceeds of a forthcoming issue of securities, it would deposit $1 million in Auslander's bank.

Auslander was elected a director on April 17, 1961. The registration statement in its original form had already been filed, of course without his signature. On May 10, 1961, he signed a signature page for the first amendment to the registration statement which was filed on May 11, 1961. This was a separate sheet without any document attached. Auslander did not know that it was a signature page for a registration statement. He vaguely understood that it was something "for the SEC."

Auslander attended a meeting of BarChris's directors on May 15, 1961. At that meeting he, along with the other directors, signed the signature sheet for the second amendment which constituted the registration statement in its final form. Again, this was only a separate sheet without any document attached. Auslander never saw a copy of the registration statement in its final form. It is true that Auslander became a director on the eve of the financing. He had little opportunity to familiarize himself with the company's affairs.

Section 11 imposes liability in the first instance upon a director, no matter how new he is.

Peat, Marwick. Peat, Marwick's work was in general charge of a member of the firm, Cummings, and more immediately in charge of Peat, Marwick's manager, Logan. Most of the actual work was performed by a senior accountant, Berardi, who had junior assistants, one of whom was Kennedy.

Berardi was then about thirty years old. He was not yet a CPA. He had had no previous experience with the bowling industry. This was his first job as a senior accountant. He could hardly have been given a more difficult assignment.

After obtaining a little background information on BarChris by talking to Logan and reviewing Peat, Marwick's work papers on its 1959 audit, Berardi examined the results of test checks of BarChris's accounting procedures which one of the junior accountants had made, and he prepared an "internal control questionnaire" and an "audit program." Thereafter, for a few days subsequent to December 30, 1960, he inspected BarChris's inventories and examined certain alley construction. Finally, on January 13, 1961, he began his auditing work which he carried on substantially continuously until it was completed on February 24, 1961. Toward the close of the work, Logan reviewed it and made various comments and suggestions to Berardi.

It is unnecessary to recount everything that Berardi did in the course of the audit. We are concerned only with the evidence relating to what Berardi did or did not do with respect to those items found to have been incorrectly reported in the 1960 figures in the prospectus.

Accountants should not be held to a standard higher than that recognized in their profession. I do not do so here. Berardi's review did not come up to that standard. He did not take some of the steps which Peat, Marwick's written program prescribed. He did not spend an adequate amount of time on a task of this magnitude. Most important of all, he was too easily satisfied with glib answers to his inquiries.

This is not to say that he should have made a complete audit. But there were enough danger signals in the materials which he did examine to require some further investigation on his part. Generally accepted accounting standards required such further investigation under these circumstances. It is not always sufficient merely to ask questions.

How much time transpired between the sale of the debentures and BarChris's bankruptcy?

Question

Escott v BarChris Constr. Corp. 283 F. Supp. 643 (S.D.N.Y. 1968)

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Question

Escott v BarChris Constr. Corp. 283 F. Supp. 643 (S.D.N.Y. 1968)

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Contingent Liabilities as of December 32, I960 , on Alternative Method of Financing

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Contingent Liabilities as of December 32, I960 , on Alternative Method of Financing

Question

Escott v BarChris Constr. Corp. 283 F. Supp. 643 (S.D.N.Y. 1968)

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Contingent Liabilities as of April 30, 1961

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Contingent Liabilities as of April 30, 1961

Question

Escott v BarChris Constr. Corp. 283 F. Supp. 643 (S.D.N.Y. 1968)

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Earnings Figures for Quarter Ending March 31 , 1961

Bowling for Fraud Right Up Our Alley

Facts

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid-1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By I960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered around the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

Earnings Figures for Quarter Ending March 31 , 1961

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/21

Play

Full screen (f)

Deck 21: Management: Employment Discrimination

1

Beginning in March 1981, R. Foster Winans was a Wall Street Journal reporter and one of the writers of the "Heard on the Street" column (the "Heard" column), a widely read and influential column in the Journal. David Carpenter worked as a news clerk at the Journal from December 1981 through May 1983. Kenneth Felis, who was a stockbroker at the brokerage house of Kidder Peabody, had been brought to that firm by another Kidder Peabody stockbroker, Peter Brant, Mr. Felis's longtime friend, who later became the government's key witness in this case.

Since February 2, 1981, it had been the practice of Dow Jones, the parent company of the Wall Street Journal, to distribute to all new employees "The Insider Story," a 40-page manual with 7 pages devoted to the company's conflicts-of-interest policy. Mr. Winans and Mr. Carpenter knew that company policy deemed all news material gleaned by an employee during the course of employment to be company property and that company policy required employees to treat nonpublic information learned on the job as confidential.

Notwithstanding company policy, Mr. Winans participated in a scheme with Mr. Brant, and later Mr. Felis and Mr. Carpenter, in which he agreed to provide the two stockbrokers (Mr. Brant and Mr. Felis) with securitiesrelated information that was scheduled to appear in "Heard" columns; based on this advance information, the two brokers would buy or sell the subject securities. Mr. Carpenter, who was involved in a private, personal, nonbusiness relationship with Mr. Winans, served primarily as a messenger for the conspirators. Trading accounts were established in the names of Kenneth Felis, David Carpenter, R. Foster Winans, Peter Brant, David Clark, Western Hemisphere, and Stephen Spratt. During 1983 and early 1984, these defendants made prepublication trades on the basis of their advance knowledge of approximately 27 Wall Street Journal "Heard" columns, although not all of those columns were written by Mr. Winans. Generally, he would inform Mr. Brant of an article's subject the day before its scheduled publication, usually by calls from a pay phone and often using a fictitious name. The net profits from the scheme approached $690,000. Was this scheme a 10(b) violation? [ United States v Carpenter, 791 F.2d 1024 (2d Cir. 1986); affirmed, Carpenter v United States, 484 U.S. 19 (1987)]

Since February 2, 1981, it had been the practice of Dow Jones, the parent company of the Wall Street Journal, to distribute to all new employees "The Insider Story," a 40-page manual with 7 pages devoted to the company's conflicts-of-interest policy. Mr. Winans and Mr. Carpenter knew that company policy deemed all news material gleaned by an employee during the course of employment to be company property and that company policy required employees to treat nonpublic information learned on the job as confidential.

Notwithstanding company policy, Mr. Winans participated in a scheme with Mr. Brant, and later Mr. Felis and Mr. Carpenter, in which he agreed to provide the two stockbrokers (Mr. Brant and Mr. Felis) with securitiesrelated information that was scheduled to appear in "Heard" columns; based on this advance information, the two brokers would buy or sell the subject securities. Mr. Carpenter, who was involved in a private, personal, nonbusiness relationship with Mr. Winans, served primarily as a messenger for the conspirators. Trading accounts were established in the names of Kenneth Felis, David Carpenter, R. Foster Winans, Peter Brant, David Clark, Western Hemisphere, and Stephen Spratt. During 1983 and early 1984, these defendants made prepublication trades on the basis of their advance knowledge of approximately 27 Wall Street Journal "Heard" columns, although not all of those columns were written by Mr. Winans. Generally, he would inform Mr. Brant of an article's subject the day before its scheduled publication, usually by calls from a pay phone and often using a fictitious name. The net profits from the scheme approached $690,000. Was this scheme a 10(b) violation? [ United States v Carpenter, 791 F.2d 1024 (2d Cir. 1986); affirmed, Carpenter v United States, 484 U.S. 19 (1987)]

This case discusses the legality of a security trade involving private and personal relationship. If a person gets some information or tip from insider then he cannot do trade because it is illegal. It will be illegal if the person passing the confidential information have some interest in it or get benefit from it. The SEC clearly says that there is enough of a personal benefit even in case of private and personal relationship and that is sufficient to make the trade illegal. Here the money earned is illegal.

2

United States v O'Hagan 521 U.S. 657 (1997)

Pillsbury Dough Boy: The Lawyer\Insider Who Cashed In

Facts

James Herman O'Hagan (respondent) was a partner in the law firm of Dorsey Whitney in Minneapolis, Minnesota. In July 1988, Grand Metropolitan PLC (Grand Met), a company based in London, retained Dorsey Whitney as local counsel to represent it regarding a potential tender offer for common stock of Pillsbury Company (based in Minneapolis).

Mr. O'Hagan did no work on the Grand Met matter, so on August 18, 1988, he began purchasing call options for Pillsbury stock. Each option gave him the right to purchase 100 shares of Pillsbury stock. By the end of September, Mr. O'Hagan owned more than 2,500 Pillsbury options. Also in September, Mr. O'Hagan purchased 5,000 shares of Pillsbury stock at $39 per share.

Grand Met announced its tender offer in October, and Pillsbury stock rose to $60 per share. Mr. O'Hagan sold his call options and made a profit of $4.3 million.

The SEC indicted Mr. O'Hagan on 57 counts of illegal trading on inside information, including mail fraud, securities fraud, fraudulent trading, and money laundering. The SEC alleged that Mr. O'Hagan used his profits from the Pillsbury options to conceal his previous embezzlement and conversion of his clients' trust funds. Mr. O'Hagan was convicted by a jury on all 57 counts and sentenced to 41 months in prison. A divided Court of Appeals reversed the conviction, and the SEC appealed.

Judicial Opinion

GINSBURG, Justice

We hold, in accord with several other Courts of Appeals, that criminal liability under § 10(b) may be predicated on the misappropriation theory.

Under the "traditional" or "classical theory" of insider trading liability, § 10(b) and Rule 10b-5 are violated when a corporate insider trades in the securities of his corporation on the basis of material, nonpublic information. Trading on such information qualifies as a "deceptive device" under § 10(b), we have affirmed, because "a relationship of trust and confidence [exists] between the shareholders of a corporation and those insiders who have obtained confidential information by reason of their position with that corporation." Chiarella v United States , 445 U.S. 222, 228 (1980). That relationship, we recognized, "gives rise to a duty to disclose [or to abstain from trading] because of the 'necessity of preventing a corporate insider from. tak[ing] unfair advantage of. uninformed. stockholders\" The classical theory applies not only to officers, directors, and other permanent insiders of a corporation, but also to attorneys, accountants, consultants, and others who temporarily become fiduciaries of a corporation. See Dirks v SEC , 463 U.S. 646, 655, n. 14 (1983).

The "misappropriation theory" holds that a person commits fraud "in connection with" a securities transaction, and thereby violates § 10(b) and Rule 10b-5, when he misappropriates confidential information for securities trading purposes, in breach of a duty owed to the source of the information. Under this theory, a fiduciary's undisclosed, self-serving use of a principal's information to purchase or sell securities, in breach of a duty of loyalty and confidentiality, defrauds the principal of the exclusive use of that information. In lieu of premising liability on a fiduciary relationship between company insider and purchaser or seller of the company's stock, the misappropriation theory premises liability on a fiduciary-turned-trader's deception of those who entrusted him with access to confidential information.

The two theories are complementary, each addressing efforts to capitalize on nonpublic information through the purchase or sale of securities. The classical theory targets a corporate insider's breach of duty to shareholders with whom the insider transacts; the misappropriation theory outlaws trading on the basis of nonpublic information by a corporate "outsider" in breach of a duty owed not to a trading party, but to the source of the information. The misappropriation theory is thus designed to "protec[t] the integrity of the securities markets against abuses by 'outsiders' to a corporation who have access to confidential information that will affect th[e] corporation's security price when revealed, but who owe no fiduciary or other duty to that corporation's shareholders."

We agree with the Government that misappropriation, as just defined, satisfies § 10(b)'s requirement that chargeable conduct involve a "deceptive device or contrivance" used "in connection with" the purchase or sale of securities. We observe, first, that misappropriators, as the Government describes them, deal in deception. A fiduciary who "[pretends] loyalty to the principal while secretly converting the principal's information for personal gain" "dupes" or defrauds the principal.

Deception through nondisclosure is central to the theory of liability for which the Government seeks recognition.

The misappropriation theory comports with § 10(b)'s language. The theory is also well-tuned to an animating purpose of the Exchange Act: to insure honest securities markets and thereby promote investor confidence. Although informational disparity is inevitable in the securities markets, investors likely would hesitate to venture their capital in a market where trading based on misappropriated nonpublic information is unchecked by law. An investor's informational disadvantage vis-a-vis a misappropriator with material, nonpublic information stems from contrivance, not luck; it is a disadvantage that cannot be overcome with research or skill.

In sum, considering the inhibiting impact on market participation of trading on misappropriated information, and the congressional purposes underlying § 10(b), it makes scant sense to hold a lawyer like O'Hagan a § 10(b) violator if he works for a law firm representing the target of a tender offer, but not if he works for a law firm representing the bidder.

In sum, the misappropriation theory, as we have examined and explained it in this opinion, is both consistent with the statute and with our precedent. Vital to our decision that criminal liability may be sustained under the misappropriation theory, we emphasize, are two sturdy safeguards Congress has provided regarding scienter. To establish a criminal violation of Rule 10b-5, the Government must prove that a person "willfully" violated the provision. In addition, the statute's "requirement of the presence of culpable intent as a necessary element of the offense does much to destroy any force in the argument that application of the [statute]" in circumstances such as O'Hagan's is unjust.

The Eighth Circuit erred in holding that the misappropriation theory is inconsistent with § 10(b). The Court of Appeals may address on remand O'Hagan's other challenges to his convictions under § 10(b) and Rule 10b-5.

Reversed.

Will Mr. O'Hagan's conviction stand?

Pillsbury Dough Boy: The Lawyer\Insider Who Cashed In

Facts

James Herman O'Hagan (respondent) was a partner in the law firm of Dorsey Whitney in Minneapolis, Minnesota. In July 1988, Grand Metropolitan PLC (Grand Met), a company based in London, retained Dorsey Whitney as local counsel to represent it regarding a potential tender offer for common stock of Pillsbury Company (based in Minneapolis).

Mr. O'Hagan did no work on the Grand Met matter, so on August 18, 1988, he began purchasing call options for Pillsbury stock. Each option gave him the right to purchase 100 shares of Pillsbury stock. By the end of September, Mr. O'Hagan owned more than 2,500 Pillsbury options. Also in September, Mr. O'Hagan purchased 5,000 shares of Pillsbury stock at $39 per share.

Grand Met announced its tender offer in October, and Pillsbury stock rose to $60 per share. Mr. O'Hagan sold his call options and made a profit of $4.3 million.

The SEC indicted Mr. O'Hagan on 57 counts of illegal trading on inside information, including mail fraud, securities fraud, fraudulent trading, and money laundering. The SEC alleged that Mr. O'Hagan used his profits from the Pillsbury options to conceal his previous embezzlement and conversion of his clients' trust funds. Mr. O'Hagan was convicted by a jury on all 57 counts and sentenced to 41 months in prison. A divided Court of Appeals reversed the conviction, and the SEC appealed.

Judicial Opinion

GINSBURG, Justice

We hold, in accord with several other Courts of Appeals, that criminal liability under § 10(b) may be predicated on the misappropriation theory.

Under the "traditional" or "classical theory" of insider trading liability, § 10(b) and Rule 10b-5 are violated when a corporate insider trades in the securities of his corporation on the basis of material, nonpublic information. Trading on such information qualifies as a "deceptive device" under § 10(b), we have affirmed, because "a relationship of trust and confidence [exists] between the shareholders of a corporation and those insiders who have obtained confidential information by reason of their position with that corporation." Chiarella v United States , 445 U.S. 222, 228 (1980). That relationship, we recognized, "gives rise to a duty to disclose [or to abstain from trading] because of the 'necessity of preventing a corporate insider from. tak[ing] unfair advantage of. uninformed. stockholders\" The classical theory applies not only to officers, directors, and other permanent insiders of a corporation, but also to attorneys, accountants, consultants, and others who temporarily become fiduciaries of a corporation. See Dirks v SEC , 463 U.S. 646, 655, n. 14 (1983).

The "misappropriation theory" holds that a person commits fraud "in connection with" a securities transaction, and thereby violates § 10(b) and Rule 10b-5, when he misappropriates confidential information for securities trading purposes, in breach of a duty owed to the source of the information. Under this theory, a fiduciary's undisclosed, self-serving use of a principal's information to purchase or sell securities, in breach of a duty of loyalty and confidentiality, defrauds the principal of the exclusive use of that information. In lieu of premising liability on a fiduciary relationship between company insider and purchaser or seller of the company's stock, the misappropriation theory premises liability on a fiduciary-turned-trader's deception of those who entrusted him with access to confidential information.

The two theories are complementary, each addressing efforts to capitalize on nonpublic information through the purchase or sale of securities. The classical theory targets a corporate insider's breach of duty to shareholders with whom the insider transacts; the misappropriation theory outlaws trading on the basis of nonpublic information by a corporate "outsider" in breach of a duty owed not to a trading party, but to the source of the information. The misappropriation theory is thus designed to "protec[t] the integrity of the securities markets against abuses by 'outsiders' to a corporation who have access to confidential information that will affect th[e] corporation's security price when revealed, but who owe no fiduciary or other duty to that corporation's shareholders."

We agree with the Government that misappropriation, as just defined, satisfies § 10(b)'s requirement that chargeable conduct involve a "deceptive device or contrivance" used "in connection with" the purchase or sale of securities. We observe, first, that misappropriators, as the Government describes them, deal in deception. A fiduciary who "[pretends] loyalty to the principal while secretly converting the principal's information for personal gain" "dupes" or defrauds the principal.

Deception through nondisclosure is central to the theory of liability for which the Government seeks recognition.

The misappropriation theory comports with § 10(b)'s language. The theory is also well-tuned to an animating purpose of the Exchange Act: to insure honest securities markets and thereby promote investor confidence. Although informational disparity is inevitable in the securities markets, investors likely would hesitate to venture their capital in a market where trading based on misappropriated nonpublic information is unchecked by law. An investor's informational disadvantage vis-a-vis a misappropriator with material, nonpublic information stems from contrivance, not luck; it is a disadvantage that cannot be overcome with research or skill.

In sum, considering the inhibiting impact on market participation of trading on misappropriated information, and the congressional purposes underlying § 10(b), it makes scant sense to hold a lawyer like O'Hagan a § 10(b) violator if he works for a law firm representing the target of a tender offer, but not if he works for a law firm representing the bidder.

In sum, the misappropriation theory, as we have examined and explained it in this opinion, is both consistent with the statute and with our precedent. Vital to our decision that criminal liability may be sustained under the misappropriation theory, we emphasize, are two sturdy safeguards Congress has provided regarding scienter. To establish a criminal violation of Rule 10b-5, the Government must prove that a person "willfully" violated the provision. In addition, the statute's "requirement of the presence of culpable intent as a necessary element of the offense does much to destroy any force in the argument that application of the [statute]" in circumstances such as O'Hagan's is unjust.

The Eighth Circuit erred in holding that the misappropriation theory is inconsistent with § 10(b). The Court of Appeals may address on remand O'Hagan's other challenges to his convictions under § 10(b) and Rule 10b-5.

Reversed.

Will Mr. O'Hagan's conviction stand?

Mr. O' Hagan was charged with doing fraud in connection with security transaction. He was charged for violation of section 10(b) of misappropriation theory. The misappropriation theory says that a person does fraud if he knows the confidential information about a security transaction and exploits the information for his own profit. in such case the person violates the section 10 (b). The insider is said to have committed misappropriation if he takes advantage of certain confidential information over the uninformed shareholders.

It was clear that he did not work with the issue of representing a potential tender but he worked for potential bidder instead. Now it must be decided whether to apply misappropriation theory in this case or not. It would be unjust to apply misappropriation theory in this case as he simply worked as a potential bidder and had no information about the potential tender.

It was clear that he did not work with the issue of representing a potential tender but he worked for potential bidder instead. Now it must be decided whether to apply misappropriation theory in this case or not. It would be unjust to apply misappropriation theory in this case as he simply worked as a potential bidder and had no information about the potential tender.

3

Raymond Dirks was an officer in a Wall Street brokerage house. He was told by Ronald Secrist a former officer of the Equity Funding of America Company, that Equity Funding had significantly overstated its assets by writing phony insurance policies. Mr. Secristurged Mr. Dirks to investigate and expose the fraudulent practices. Mr. Dirks checked with Equity Funding management and received denials from them, but he received affirmations from employees.

Mr. Dirks discussed the issue with clients, and they "dumped" nearly $6 million in Equity Funding stock, but Mr. Dirks and his firm did not trade the stock. The price of the stock fell from $26 to $15 during Mr. Dirks's investigation. He contacted the Wall Street Journal bureau chief about the problem, but the bureau chief declined to get involved.

The SEC charged Mr. Dirks with violations of 10b-5 for his assistance to his clients. Did he violate 10b-5? [ Dirks v SEC, 463 U.S. 646 (1983)]

Mr. Dirks discussed the issue with clients, and they "dumped" nearly $6 million in Equity Funding stock, but Mr. Dirks and his firm did not trade the stock. The price of the stock fell from $26 to $15 during Mr. Dirks's investigation. He contacted the Wall Street Journal bureau chief about the problem, but the bureau chief declined to get involved.

The SEC charged Mr. Dirks with violations of 10b-5 for his assistance to his clients. Did he violate 10b-5? [ Dirks v SEC, 463 U.S. 646 (1983)]

SEC 10b-5 is an important rule regarding security exchange and trade. It prohibits a person to use confidential information for doing security trade. A person could be charged with doing fraud in connection with security transaction. He could be charged for violation of section 10(b) of misappropriation theory. The misappropriation theory says that a person does fraud if he knows the confidential information about a security transaction and exploits the information for his own profit. In such case the person violates the section 10 (b). The insider is said to have committed misappropriation if he takes advantage of certain confidential information over the uninformed shareholders.

4

Vincent Chiarella was employed as a printer in a financial printing firm that handled the printing for takeover bids. Although the firm names were left out of the financial materials and inserted at the last moment, Mr. Chiarella was able to deduce who was being taken over and by whom from other information in the reports being printed. Using this information, Mr. Chiarella was able to dabble in the stock market over a 14-month period for a net gain of $30,000. After an SEC investigation, he signed a consent decree that required him to return all of his profits to the sellers he purchased from during that 14-month period. He was then indicted for violation of 10(b) of the 1934 act and the SEC's Rule 10b-5. Did Mr. Chiarella violate 10b-5? [ Chiarella v United States , 445 U.S. 222 (1980)]

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

5

The president's letter in Rockwood Computer Corporation's annual report stated that most of its inventory consisted of its old computer series. The letter suggested that its new series would cost more money for all users. However, the letter did not disclose, although evidence had indicated, that the new system might be less expensive for those who needed greater performance and capacity. Walter Beissinger (who sold his shares based on the information) brought suit under 10(b). Rockwood claims the statements were based on opinions of sales and were not statements of fact. Who should win? [ Beissinger v Rockwood Computer Corp., 529 F. Supp. 770 (E.D. Pa. 1981)]

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

6

William H. Sullivan, Jr., gained control of the New England Patriots Football Club (Patriots) by forming a separate corporation (New Patriots) and merging it with the old one. Plaintiffs are a class of stockholders who voted to accept New Patriots' offer of $15 a share for their common stock in the Patriots' corporation. They now claim that they were induced to accept this offer by a misleading proxy statement drafted under the direction of Mr. Sullivan, who owned a controlling share in the voting stock of the Patriots at the time of the merger. The proxy statement, plaintiffs claim, contained various misrepresentations designed to paint a gloomy picture of the financial position and prospects of the Patriots, so that the shareholders undervalued their stock. They seek to rescind the merger or to receive a higher price per share for the stock they sold. Does the court have the authority to rescind under Section 14? [ Pavlidis v New England Patriots Football Club , 737 F.2d 1227 (1st Cir. 1984)]

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

7

The National Bank of Yugoslavia placed $71 million with Drexel Burnham Lambert, Inc., for short-term investment just months before Drexel's bankruptcy. In effect, the bank made a time deposit. Would the bank be able to proceed under a theory of securities laws violations? Would these time deposits be considered securities? [ National Bank of Yugoslavia v Drexel Burnham Lambert, Inc., 768 F.Supp. 1010 (S.D.N.Y 1991)]

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

8

More Than a Book Offering

Simon Simon, Inc. (SSI), is a Fortune 500 company primarily-involved in publishing magazines and fiction and non-fiction popular press. Like other publishing firms, SSI has been interested in expansion through the acquisition of publishing firms or companies with a multimedia focus. Its shares are listed on the New York Stock Exchange.

SSI has been approached by University Press (UP), a small but successful publishing house with a focus on academic and research-oriented books that would like to sell its assets (physical as well as titles [copyrights]) to SSI. UP is a national company that markets largely through direct mailings and whose stock is sold on the over-the-counter market. SSI has its own bookstores in malls, downtown city centers, and a few strip malls. It releases approximately 30 major fiction titles (excluding its romance novel line) and 20 major nonfiction titles each year. Other releases include children's books, cookbooks, "how to" books, coffee table (art) books, and several college and test-preparation guides. These types of releases total 100 per year. UP releases 25 new books each year, but it is in the unique position of having some of its titles continue selling long after the usual six-month hard-cover life of popular press books.

UP's board authorized its CEO to approach SSI. SSI's board heard the proposal for the first time yesterday. SSI's CEO told them, "We should act quickly The price is right." Another board member asked, "Aren't there some legal issues here? Can we act this quickly?"

Prepare a memorandum for the SSI board and also for the UP board outlining all the legal issues, including corporate, antitrust, and securities issues.

Simon Simon, Inc. (SSI), is a Fortune 500 company primarily-involved in publishing magazines and fiction and non-fiction popular press. Like other publishing firms, SSI has been interested in expansion through the acquisition of publishing firms or companies with a multimedia focus. Its shares are listed on the New York Stock Exchange.

SSI has been approached by University Press (UP), a small but successful publishing house with a focus on academic and research-oriented books that would like to sell its assets (physical as well as titles [copyrights]) to SSI. UP is a national company that markets largely through direct mailings and whose stock is sold on the over-the-counter market. SSI has its own bookstores in malls, downtown city centers, and a few strip malls. It releases approximately 30 major fiction titles (excluding its romance novel line) and 20 major nonfiction titles each year. Other releases include children's books, cookbooks, "how to" books, coffee table (art) books, and several college and test-preparation guides. These types of releases total 100 per year. UP releases 25 new books each year, but it is in the unique position of having some of its titles continue selling long after the usual six-month hard-cover life of popular press books.

UP's board authorized its CEO to approach SSI. SSI's board heard the proposal for the first time yesterday. SSI's CEO told them, "We should act quickly The price is right." Another board member asked, "Aren't there some legal issues here? Can we act this quickly?"

Prepare a memorandum for the SSI board and also for the UP board outlining all the legal issues, including corporate, antitrust, and securities issues.

Unlock Deck

Unlock for access to all 21 flashcards in this deck.

Unlock Deck

k this deck

9

Escott v BarChris Constr. Corp.

283 F. Supp. 643 (S.D.N.Y. 1968)

Bowling for Fraud: Right Up Our Alley

FACTS

BarChris was a bowling alley company established in 1946. The bowling industry grew rapidly when automatic pin resetters went on the market in the mid- 1950s. BarChris began a program of rapid expansion and in 1960 was responsible for the construction of over 3 percent of all bowling alleys in the United States. BarChris used two methods of financing the construction of these alleys, both of which substantially drained the company's cash flow.

In 1959 BarChris sold approximately one-half million shares of common stock. By 1960, its cash flow picture was still troublesome, and it sold debentures. The debenture issue was registered with the SEC, approved, and sold. In spite of the cash boost from the sale, BarChris was still experiencing financial difficulties and declared bankruptcy in October 1962. The debenture holders were not paid their interest; BarChris defaulted.

The purchasers of the BarChris debentures brought suit under Section 11 of the 1933 act. They claimed that the registration statement filed by BarChris contained false information and failed to disclose certain material information. Their suit, which centered on the audited financial statements prepared by a CPA firm, claimed that the statements were inaccurate and full of omissions. The following chart summarizes the problems with the financial statements submitted with the registration statements.

1. 1960 Earnings

(a) Sales

(b) Net Operating Income

(c) Earnings per Share

2. 1960 Balance Sheet

Current Assets

3. Contingent Liabilities as of December 31, 1960, on Alternative Method of Financing

4. Contingent Liabilities as of April 30, 1961

5. Earnings Figures for Quarter Ending

March 31, 1961

(a) Sales

(b) Gross Profit

6. Backlog as of March 31, 1961

7. Failure to Disclose Officers' Loans Outstanding and Unpaid on

0

8. Failure to Disclose Use of Proceeds in Manner Not Revealed in Prospectus: Approx. $1,160,000

9. Failure to Disclose Customers' Delinquencies in May 1961 and BarChris's Potential Liability with Respect Thereto: Over $1,350,000

10. Failure to Disclose the Fact that BarChris Was Already Engaged and Was About to Be More Heavily Engaged in the Operation of Bowling Alleys

The federal district court reviewed all of the exhibits and statements included in the prospectus and dealt with each defendant individually in issuing its decisions. The defendants consisted of those officers and directors who signed the registration statement, the underwriters of the debenture offering, the auditors (Peat, Marwick, Mitchell Co.5), and BarChris's attorneys and directors.

JUDICIAL OPINION

McLEAN, District Judge

Russo. Russo was, to all intents and purposes, the chief executive officer of BarChris. He was a member of the executive committee. He was familiar with all aspects of the business. He was personally in charge of dealings with the factors. He acted on BarChris's behalf in making the financing agreement with Talcott and he handled the negotiations with Talcott in the spring of 1961. He talked with customers about their delinquencies.

Russo prepared the list of jobs which went into the backlog figure. He knew the status of those jobs.

It was Russo who arranged for the temporary increase in BarChris's cash in banks on December 31, 1960, a transaction which borders on the fraudulent. He was thoroughly aware of BarChris's stringent financial condition in May 1961. He had personally advanced large sums to BarChris of which $175,000 remained unpaid as of May 16.

In short, Russo knew all the relevant facts. He could not have believed that there were no untrue statements or material omissions in the prospectus. Russo has no due diligence defenses.

Vitolo and Pugliese. They were the founders of the business who stuck with it to the end. Vitolo was president and Pugliese was vice president. Despite their titles, their field of responsibility in the administration of BarChris's affairs during the period in question seems to have been less all-embracing than Russo's. Pugliese in particular appears to have limited his activities to supervising the actual construction work. Vitolo and Pugliese are each men of limited education. It is not hard to believe that for them the prospectus was difficult reading, if indeed they read it at all.

But whether it was or not is irrelevant. The liability of a director who signs a registration statement does not depend upon whether or not he read it or, if he did, whether or not he understood what he was reading.

And in any case, Vitolo and Pugliese were not as naive as they claim to be. They were members of BarChris's executive committee. At meetings of that committee BarChris's affairs were discussed at length. They must have known what was going on. Certainly they knew of the inadequacy of cash in 1961. They knew of their own large advances to the company which remained unpaid. They knew that they had agreed not to deposit their checks until the financing proceeds were received. They knew and intended that part of the proceeds were to be used to pay their own loans.

All in all, the position of Vitolo and Pugliese is not significantly different, for present purposes, from Russo's. They could not have believed that the registration statement was wholly true and that no material facts had been omitted. And in any case, there is nothing to show that they made any investigation of anything which they may not have known about or understood. They have not proved their due diligence defenses.

Kircher. Kircher was treasurer of BarChris and its chief financial officer. He is a certified public accountant and an intelligent man. He was thoroughly familiar with BarChris's financial affairs. He knew the terms of BarChris's agreements with Talcott. He knew of the customers' delinquency problems. He participated actively with Russo in May 1961 in the successful effort to hold Talcott off until the financing proceeds came in. He knew how the financing proceeds were to be applied and he saw to it that they were so applied. He arranged the officers' loans and he knew all the facts concerning them.

Moreover, as a member of the executive committee, Kircher was kept informed as to those branches of the business of which he did not have direct charge. He knew about the operation of alleys, present and prospective. In brief, Kircher knew all the relevant facts.

Knowing the facts, Kircher had reason to believe that the expertised portion of the prospectus, i.e., the 1960 figures, was in part incorrect. He could not shut his eyes to the facts and rely on Peat, Marwick for that portion.

As to the rest of the prospectus, knowing the facts, he did not have a reasonable ground to believe it to be true. On the contrary, he must have known that in part it was untrue. Under these circumstances, he was not entitled to sit back and place the blame on the lawyers for not advising him about it. Kircher has not proved his due diligence defenses.

Trilling. Trilling's position is somewhat different from Kircher's. He was BarChris's controller. He signed the registration statement in that capacity, although he was not a director.

Trilling entered BarChris's employ in October 1960. He was Kircher's subordinate. When Kircher asked him for information, he furnished it. On at least one occasion he got it wrong.

Trilling may well have been unaware of several of the inaccuracies in the prospectus. But he must have known of some of them. As a financial officer, he was familiar with BarChris's finances and with its books of account. He knew that part of the cash on deposit on December 31, 1960, had been procured temporarily by Russo for window dressing purposes. He should have known, although perhaps through carelessness he did not know at the time, that BarChris's contingent liability was greater than the prospectus stated. In the light of these facts, I cannot find that Trilling believed the entire prospectus to be true.