Deck 12: Business and Consumer Loans

Full screen (f)

Question

Round money amounts to the nearest cent and rates to the nearest tenth of a percent.

Find the amount and interest earned of each of the following ordinary annuities.

Find the amount and interest earned of each of the following ordinary annuities.

Question

Question

Question

Question

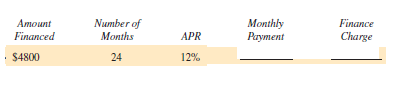

Find the finance charge (FC) and the total installment cost (TIC) for the following. (See Example.)

Finding the Total Installment Cost

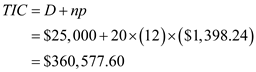

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Finding the Total Installment Cost

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Question

Explain the difference between open-end credit and installment loans. (See Section and OBJECTIVE of this section.)

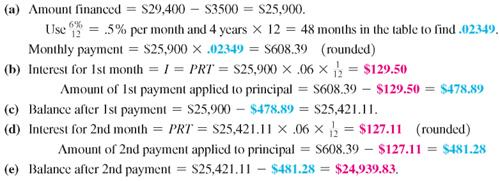

Define installment loan. A loan is amortized if both principal and interest are paid off by a sequence of equal periodic payments. This type of loan is called an installment loan. People use installment loans for cars, boats, home improvements, and even for consolidating several loans into one affordable loan. Firms use installment loans to purchase equipment, computers, vehicles, mining equipment, etc. The graphic shows the total interest that must be paid when financing a new Ford Escape over 3, 4, and 5 years. Notice that financing the SUV over 5 years results in interest costs of $2600, thereby increasing the total cost of the $25,000 loan to $27,600 or by 10.4%.

Quick TIP

The interest rates on installments loans can be very high.

Notice that the total interest paid is much higher the longer the term of the loan. It may be difficult to make the higher payments of a short-term loan, but it results in less total interest!

The federal Truth in Lending Act (Regulation Z) of 1969 requires lenders to disclose their finance charge (the charge for credit) and annual percentage rate (APR) on installment loans. The federal government does not regulate rates. Each individual state sets the maximum allowable rates and charges.

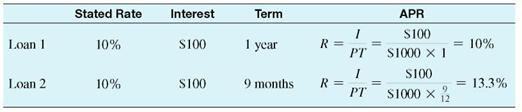

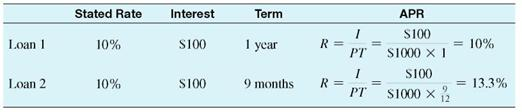

The interest rate that is stated (in the newspaper, a marketing brochure, or a problem in a textbook) is also called the nominal rate. The nominal or stated rate can differ from the annual percentage rate or APR, which is based on the actual amount received by the borrower. The APR is the true effective annual interest rate for a loan. Information on two loans of $1000 each is shown below. An advertisement indicates a rate of 10, for each loan, and the actual interest is $100 for each. However, the terms differ as do the APRs.

The interest rates on these two loans are very different. In fact, interest rate charges vary a surprising amount from one lender to another, so it pays to shop around for the lowest APR. Furthermore, institutions usually charge a much higher interest rate for individuals with poor credit history. Thus, it is worth it to maintain a good credit history by paying all bills on time.

Define installment loan. A loan is amortized if both principal and interest are paid off by a sequence of equal periodic payments. This type of loan is called an installment loan. People use installment loans for cars, boats, home improvements, and even for consolidating several loans into one affordable loan. Firms use installment loans to purchase equipment, computers, vehicles, mining equipment, etc. The graphic shows the total interest that must be paid when financing a new Ford Escape over 3, 4, and 5 years. Notice that financing the SUV over 5 years results in interest costs of $2600, thereby increasing the total cost of the $25,000 loan to $27,600 or by 10.4%.

Quick TIP

The interest rates on installments loans can be very high.

Notice that the total interest paid is much higher the longer the term of the loan. It may be difficult to make the higher payments of a short-term loan, but it results in less total interest!

The federal Truth in Lending Act (Regulation Z) of 1969 requires lenders to disclose their finance charge (the charge for credit) and annual percentage rate (APR) on installment loans. The federal government does not regulate rates. Each individual state sets the maximum allowable rates and charges.

The interest rate that is stated (in the newspaper, a marketing brochure, or a problem in a textbook) is also called the nominal rate. The nominal or stated rate can differ from the annual percentage rate or APR, which is based on the actual amount received by the borrower. The APR is the true effective annual interest rate for a loan. Information on two loans of $1000 each is shown below. An advertisement indicates a rate of 10, for each loan, and the actual interest is $100 for each. However, the terms differ as do the APRs.

The interest rates on these two loans are very different. In fact, interest rate charges vary a surprising amount from one lender to another, so it pays to shop around for the lowest APR. Furthermore, institutions usually charge a much higher interest rate for individuals with poor credit history. Thus, it is worth it to maintain a good credit history by paying all bills on time.

Question

Find the balance due on the maturity date of the following notes. Find the total amount of interest paid on each note. Use the United States Rule. (See Examples 1 and 2.)

Question

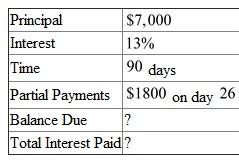

Solve the following application problem using the United States Rule.

PARTIAL PAYMENT Johnson Solar Technologies borrowed $92,000 on May 7, signing a note due in 90 days at 11.25% interest. On June 24, the company made a partial payment of $24,350. Find (a) the amount due on the maturity date of the note __________ and (b) the interest paid on the note. __________

PARTIAL PAYMENT Johnson Solar Technologies borrowed $92,000 on May 7, signing a note due in 90 days at 11.25% interest. On June 24, the company made a partial payment of $24,350. Find (a) the amount due on the maturity date of the note __________ and (b) the interest paid on the note. __________

Question

Find the payment necessary to amortize the following loans using the amortization table. Round to the nearest cent if needed. (See Example.)

Amortizing a Loan

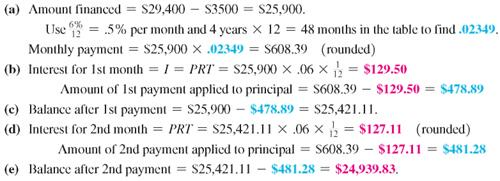

Sven Yarborough earned a degree at a community college and is now a mechanic at a Ford dealership. He was so impressed with the quality of Fords that he purchased an SUV at a cost of $29,400, including tax, title, and license, after the rebate. He made a down payment of $3500 and was able to finance the balance at a rate of 6% per year for 4 years. Find (a) the monthly payment, (b) the portion of the first payment that is interest, (c) the balance due after one payment, (d) the interest owed for the second month, and (e) the balance after the second payment.

SOLUTION

Amortizing a Loan

Sven Yarborough earned a degree at a community college and is now a mechanic at a Ford dealership. He was so impressed with the quality of Fords that he purchased an SUV at a cost of $29,400, including tax, title, and license, after the rebate. He made a down payment of $3500 and was able to finance the balance at a rate of 6% per year for 4 years. Find (a) the monthly payment, (b) the portion of the first payment that is interest, (c) the balance due after one payment, (d) the interest owed for the second month, and (e) the balance after the second payment.

SOLUTION

Question

Solve the following application problems. Use the loan payoff table. (See Objective.)

Set up an amortization schedule.

SMART PHONE Ben Watson needs $50,000 to set up his own booth at a local mall. He has $15,000 and financed the balance at a high rate of 14% for 36 months since he did not have much credit history. Prepare an amortization schedule showing the first 5 payments.

Set up an amortization schedule.

SMART PHONE Ben Watson needs $50,000 to set up his own booth at a local mall. He has $15,000 and financed the balance at a high rate of 14% for 36 months since he did not have much credit history. Prepare an amortization schedule showing the first 5 payments.

Question

Solve the following application problems.

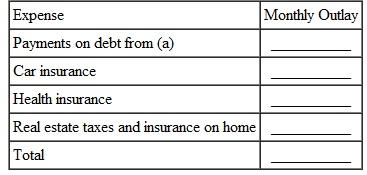

HOME PURCHASE The Potters want to buy a cottage costing $127,000 with annual insurance and taxes of $720 and $2300, respectively. They have saved $10,000 for a down payment, and they can get a

, 30-year mortgage from Citibank. They are qualified for a home loan as long as the total monthly payment does not exceed $1200. Are they qualified?

, 30-year mortgage from Citibank. They are qualified for a home loan as long as the total monthly payment does not exceed $1200. Are they qualified?

HOME PURCHASE The Potters want to buy a cottage costing $127,000 with annual insurance and taxes of $720 and $2300, respectively. They have saved $10,000 for a down payment, and they can get a

, 30-year mortgage from Citibank. They are qualified for a home loan as long as the total monthly payment does not exceed $1200. Are they qualified? Question

These monthly expenses do not include car insurance ($215 per month), health insurance ($290 per month), or real estate taxes and insurance on their home ($3350 per year), among other expenses. Find their total monthly outlay for all of these expenses.

Question

Round money amounts to the nearest cent and rates to the nearest tenth of a percent.

Find the required payment into a sinking fund.

Find the required payment into a sinking fund.

Question

Question

Find the finance charge for the following revolving charge accounts. Assume that interest is calculated on the average daily balance of the account. (See Example 2.)

Question

Find the finance charge (FC) and the total installment cost (TIC) for the following. (See Example.)

Finding the Total Installment Cost

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Finding the Total Installment Cost

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Question

Make a list of all of the items that you have bought on an installment loan. Make another list of things you plan to buy in the next 2 years on an installment loan. (See Objective.)

Define installment loan. A loan is amortized if both principal and interest are paid off by a sequence of equal periodic payments. This type of loan is called an installment loan. People use installment loans for cars, boats, home improvements, and even for consolidating several loans into one affordable loan. Firms use installment loans to purchase equipment, computers, vehicles, mining equipment, etc. The graphic shows the total interest that must be paid when financing a new Ford Escape over 3, 4, and 5 years. Notice that financing the SUV over 5 years results in interest costs of $2600, thereby increasing the total cost of the $25,000 loan to $27,600 or by 10.4%.

Quick TIP

The interest rates on installments loans can be very high.

Notice that the total interest paid is much higher the longer the term of the loan. It may be difficult to make the higher payments of a short-term loan, but it results in less total interest!

The federal Truth in Lending Act (Regulation Z) of 1969 requires lenders to disclose their finance charge (the charge for credit) and annual percentage rate (APR) on installment loans. The federal government does not regulate rates. Each individual state sets the maximum allowable rates and charges.

The interest rate that is stated (in the newspaper, a marketing brochure, or a problem in a textbook) is also called the nominal rate. The nominal or stated rate can differ from the annual percentage rate or APR, which is based on the actual amount received by the borrower. The APR is the true effective annual interest rate for a loan. Information on two loans of $1000 each is shown below. An advertisement indicates a rate of 10, for each loan, and the actual interest is $100 for each. However, the terms differ as do the APRs.

The interest rates on these two loans are very different. In fact, interest rate charges vary a surprising amount from one lender to another, so it pays to shop around for the lowest APR. Furthermore, institutions usually charge a much higher interest rate for individuals with poor credit history. Thus, it is worth it to maintain a good credit history by paying all bills on time.

Define installment loan. A loan is amortized if both principal and interest are paid off by a sequence of equal periodic payments. This type of loan is called an installment loan. People use installment loans for cars, boats, home improvements, and even for consolidating several loans into one affordable loan. Firms use installment loans to purchase equipment, computers, vehicles, mining equipment, etc. The graphic shows the total interest that must be paid when financing a new Ford Escape over 3, 4, and 5 years. Notice that financing the SUV over 5 years results in interest costs of $2600, thereby increasing the total cost of the $25,000 loan to $27,600 or by 10.4%.

Quick TIP

The interest rates on installments loans can be very high.

Notice that the total interest paid is much higher the longer the term of the loan. It may be difficult to make the higher payments of a short-term loan, but it results in less total interest!

The federal Truth in Lending Act (Regulation Z) of 1969 requires lenders to disclose their finance charge (the charge for credit) and annual percentage rate (APR) on installment loans. The federal government does not regulate rates. Each individual state sets the maximum allowable rates and charges.

The interest rate that is stated (in the newspaper, a marketing brochure, or a problem in a textbook) is also called the nominal rate. The nominal or stated rate can differ from the annual percentage rate or APR, which is based on the actual amount received by the borrower. The APR is the true effective annual interest rate for a loan. Information on two loans of $1000 each is shown below. An advertisement indicates a rate of 10, for each loan, and the actual interest is $100 for each. However, the terms differ as do the APRs.

The interest rates on these two loans are very different. In fact, interest rate charges vary a surprising amount from one lender to another, so it pays to shop around for the lowest APR. Furthermore, institutions usually charge a much higher interest rate for individuals with poor credit history. Thus, it is worth it to maintain a good credit history by paying all bills on time.

Question

Find the balance due on the maturity date of the following notes. Find the total amount of interest paid on each note. Use the United States Rule. (See Examples 1 and 2.)

Question

Solve the following application problem using the United States Rule.

REMODELING The Second Avenue Butcher Shop financed a remodeling program by giving the builder a note for $32,500. The note was made on September 14 and is due in 120 days. Interest on the note is 9.75%. On December 9, the firm makes a partial payment of $9000. Find (a) the amount due on the maturity date of the note __________ and (b) the interest paid on the note. __________

REMODELING The Second Avenue Butcher Shop financed a remodeling program by giving the builder a note for $32,500. The note was made on September 14 and is due in 120 days. Interest on the note is 9.75%. On December 9, the firm makes a partial payment of $9000. Find (a) the amount due on the maturity date of the note __________ and (b) the interest paid on the note. __________

Question

Find the payment necessary to amortize the following loans using the amortization table. Round to the nearest cent if needed. (See Example.)

Amortizing a Loan

Sven Yarborough earned a degree at a community college and is now a mechanic at a Ford dealership. He was so impressed with the quality of Fords that he purchased an SUV at a cost of $29,400, including tax, title, and license, after the rebate. He made a down payment of $3500 and was able to finance the balance at a rate of 6% per year for 4 years. Find (a) the monthly payment, (b) the portion of the first payment that is interest, (c) the balance due after one payment, (d) the interest owed for the second month, and (e) the balance after the second payment.

SOLUTION

Amortizing a Loan

Sven Yarborough earned a degree at a community college and is now a mechanic at a Ford dealership. He was so impressed with the quality of Fords that he purchased an SUV at a cost of $29,400, including tax, title, and license, after the rebate. He made a down payment of $3500 and was able to finance the balance at a rate of 6% per year for 4 years. Find (a) the monthly payment, (b) the portion of the first payment that is interest, (c) the balance due after one payment, (d) the interest owed for the second month, and (e) the balance after the second payment.

SOLUTION

Question

Solve the following application problems. Use the loan payoff table. (See Objective.)

Set up an amortization schedule.

SCUBA EQUIPMENT Jessica Chien needed $280,000 for inventory for a scuba diving shop that she was opening. She had $40,000, and the bank loaned her the balance at 11% for 30 months. Prepare an amortization schedule showing the first 5 payments.

Set up an amortization schedule.

SCUBA EQUIPMENT Jessica Chien needed $280,000 for inventory for a scuba diving shop that she was opening. She had $40,000, and the bank loaned her the balance at 11% for 30 months. Prepare an amortization schedule showing the first 5 payments.

Question

Question

Question

Question

Solve the following application problems using 360-day years where applicable.

The Hodges purchase an older 4-bedroom home for $195,000 with 5 down. They finance the balance at

per year for 30 years. If insurance is $720 per year and taxes are $4140 per year, find the monthly payment.

per year for 30 years. If insurance is $720 per year and taxes are $4140 per year, find the monthly payment.

The Hodges purchase an older 4-bedroom home for $195,000 with 5 down. They finance the balance at

per year for 30 years. If insurance is $720 per year and taxes are $4140 per year, find the monthly payment. Question

Find the finance charge for the following revolving charge accounts. Assume that interest is calculated on the average daily balance of the account. (See Example 2.)

Question

Find the finance charge (FC) and the total installment cost (TIC) for the following. (See Example.)

Finding the Total Installment Cost

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Finding the Total Installment Cost

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Question

Question

Find the balance due on the maturity date of the following notes. Find the total amount of interest paid on the note. Use the United States Rule. (See Examples.)

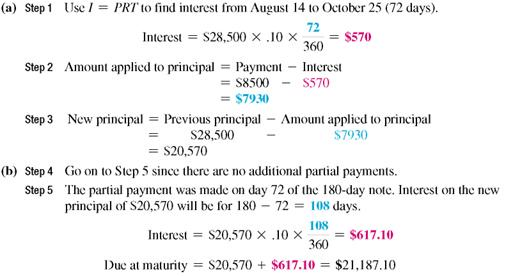

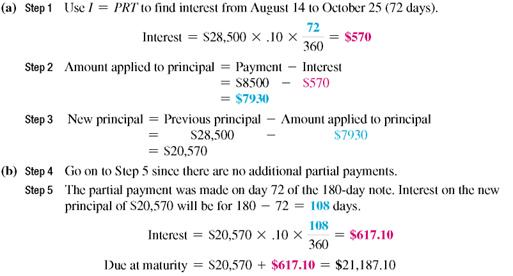

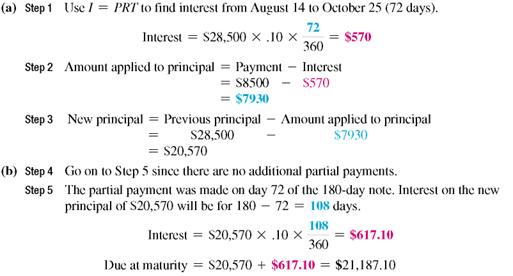

Finding the Amount Due

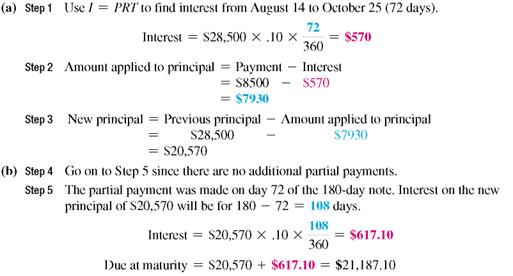

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

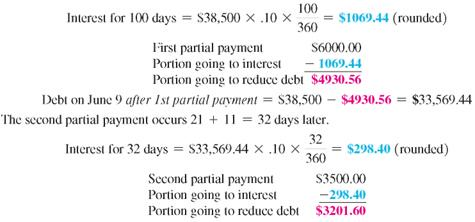

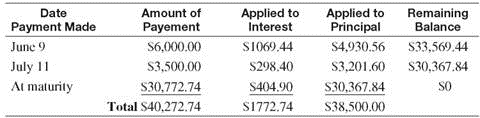

Finding the Interest Paid and Amount Due

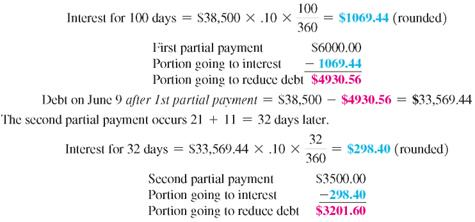

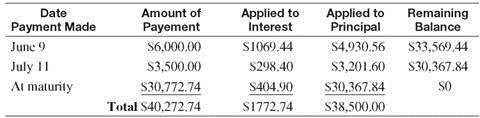

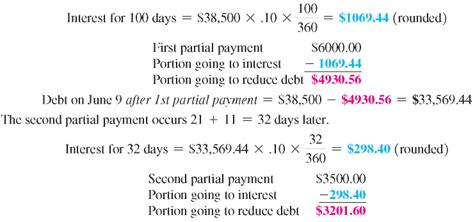

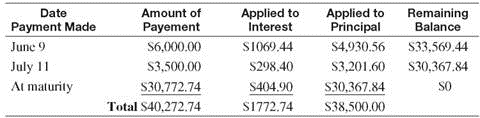

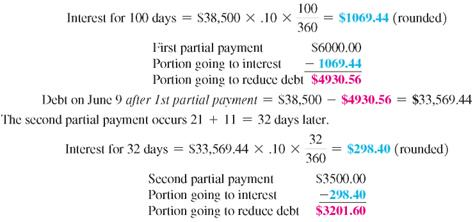

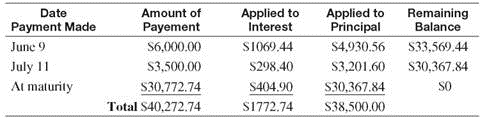

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Finding the Amount Due

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

Finding the Interest Paid and Amount Due

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Question

Question

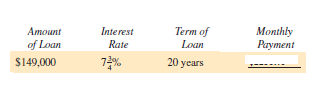

Use the loan payoff table to find the monthly payment (MP) and finance charge (FC) for each of the following loans. (See Example 3.)

Question

Use the real estate amortization table to find the monthly payment for the following loans. (See Example 1.)

Question

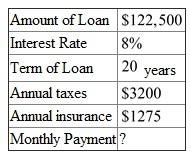

Solve the following application problems.

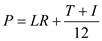

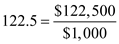

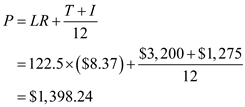

HOME LOAN June and Bill Able borrow $122,500 on their home at

for 15 years. Prepare a repayment schedule for the first two payments. (See Example.)

for 15 years. Prepare a repayment schedule for the first two payments. (See Example.)

Preparing a Repayment Schedule

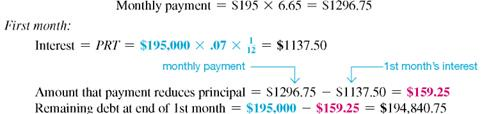

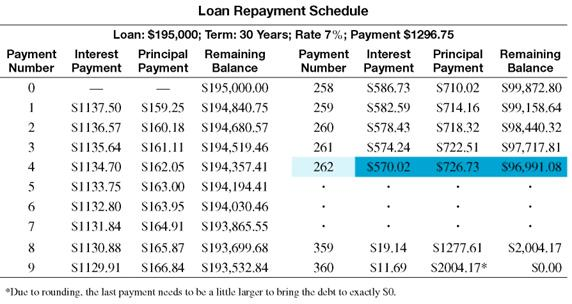

The Zinks purchase a house by borrowing $195,000 at 7% for 30 years. Prepare a loan repayment schedule for this loan.

SOLUTION

First find the monthly payment, then use simple interest calculations for the first two months. Be sure to round to the nearest cent at each step.

Every time a payment is made, interest is first subtracted from the payment. As a result, only a small portion of the first payment is applied to reduce the principal.

These and other results are shown in the table. Notice that at first the amount applied to interest is large and the amount applied to reduce principal is small. But every month, the debt goes down, resulting in lower interest the following month, and more of each payment is applied to reduce the principal. It requires 262 months (nearly 22 years) to pay off half of the debt and only 98 months (just over 8 years) to pay off the other half of the loan.

HOME LOAN June and Bill Able borrow $122,500 on their home at

for 15 years. Prepare a repayment schedule for the first two payments. (See Example.)Preparing a Repayment Schedule

The Zinks purchase a house by borrowing $195,000 at 7% for 30 years. Prepare a loan repayment schedule for this loan.

SOLUTION

First find the monthly payment, then use simple interest calculations for the first two months. Be sure to round to the nearest cent at each step.

Every time a payment is made, interest is first subtracted from the payment. As a result, only a small portion of the first payment is applied to reduce the principal.

These and other results are shown in the table. Notice that at first the amount applied to interest is large and the amount applied to reduce principal is small. But every month, the debt goes down, resulting in lower interest the following month, and more of each payment is applied to reduce the principal. It requires 262 months (nearly 22 years) to pay off half of the debt and only 98 months (just over 8 years) to pay off the other half of the loan.

Question

Question

Round money amounts to the nearest cent and rates to the nearest tenth of a percent.

Find the required payment into a sinking fund.

Find the required payment into a sinking fund.

Question

Question

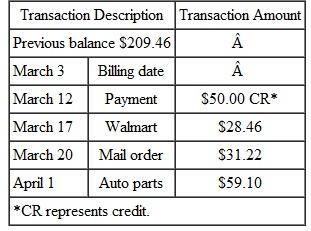

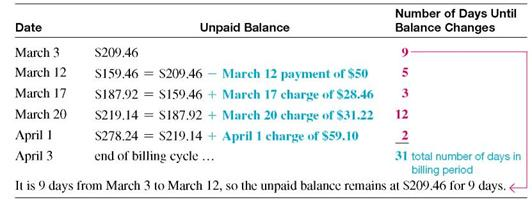

Find the finance charge for the following revolving charge accounts. Assume that interest is calculated on the average daily balance of the account. (See Example.)

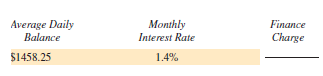

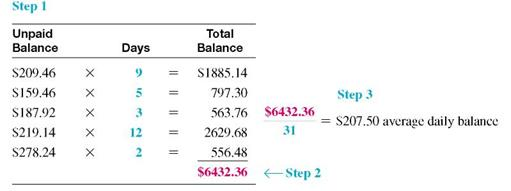

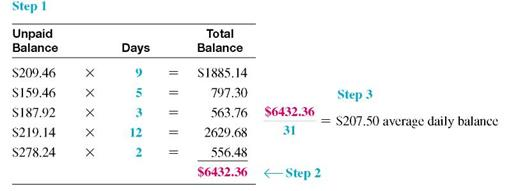

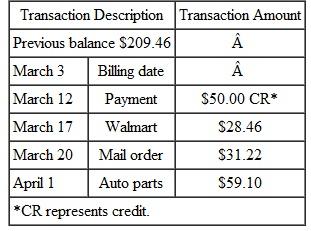

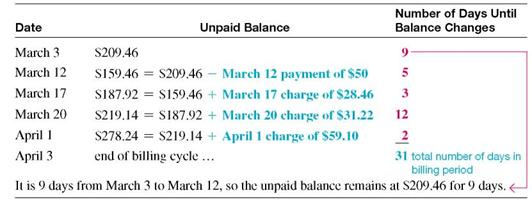

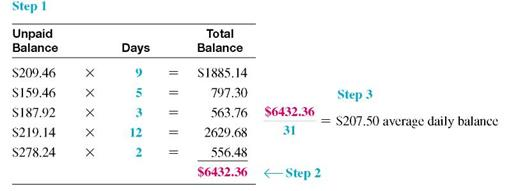

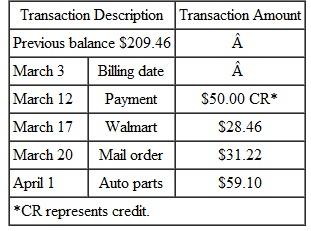

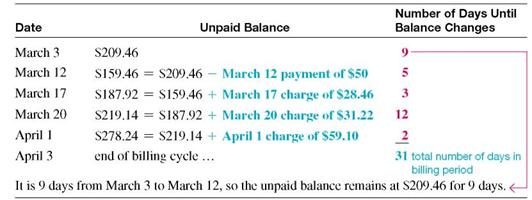

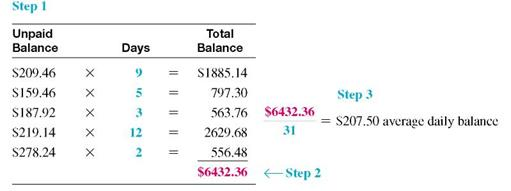

Finding the Average Daily Balance

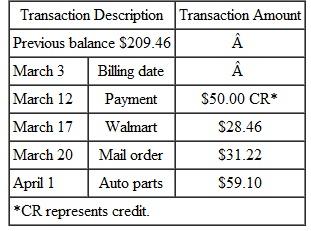

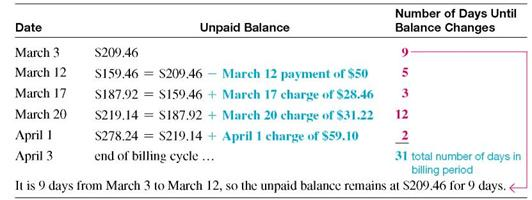

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION

SOLUTION

(a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Finding the Average Daily Balance

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION (a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Question

Find the finance charge (FC) and the total installment cost (TIC) for the following. (See Example.)

Finding the Total Installment Cost

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Finding the Total Installment Cost

Frank Kimlicko recently received his master's degree and began work at a large community college as a music professor specializing in classical guitar. He purchased an exquisite-sounding classical guitar costing $3800 with $500 down and 36 monthly payments of $109.61 each. Find (a) the total installment cost, (b) the finance charge, and (c) the amount financed.

Quick TIP

To find the total installment cost, add the down payment to the sum of all monthly payments.

SOLUTION

(a) The total installment cost is the down payment plus the total of all monthly payments.

Total installment cost = $500 + 1$109.61 × 362 = $4445.96

(b) The finance charge is the total installment cost less the cash price.

Finance charge = $4445.96 ? $ 3800 = $645.96

(c) The amount financed is $3800 ? $500 = $3300.

Question

Question

Find the balance due on the maturity date of the following notes. Find the total amount of interest paid on the note. Use the United States Rule. (See Examples.)

Finding the Amount Due

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

Finding the Interest Paid and Amount Due

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Finding the Amount Due

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

Finding the Interest Paid and Amount Due

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Question

Question

Use the loan payoff table to find the monthly payment (MP) and finance charge (FC) for each of the following loans. (See Example 3.)

Question

Use the real estate amortization table to find the monthly payment for the following loans. (See Example 1.)

Question

Solve the following application problems.

ELDERLY HOUSING Tom Ajax purchases a tiny home for his elderly mother. After a large down payment, he finances $88,600 at

for 10 years. Prepare a repayment schedule for the first two payments. (See Example 2.)

for 10 years. Prepare a repayment schedule for the first two payments. (See Example 2.)

ELDERLY HOUSING Tom Ajax purchases a tiny home for his elderly mother. After a large down payment, he finances $88,600 at

for 10 years. Prepare a repayment schedule for the first two payments. (See Example 2.) Question

Round money amounts to the nearest cent and rates to the nearest tenth of a percent.

Find the amount of each annuity due and the interest earned.

Find the amount of each annuity due and the interest earned.

Question

Question

Question

Find the finance charge for the following revolving charge accounts. Assume that interest is calculated on the average daily balance of the account. (See Example.)

Finding the Average Daily Balance

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION

SOLUTION

(a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Finding the Average Daily Balance

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION (a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Question

Find the approximate annual percentage rate using the approximate annual percentage rate formula. Round to the nearest tenth of a percent. (See Example 2.)

Question

Solve the following application problem. Use formula to estimate the APR, and round rates to the nearest tenth of a percent.

ELECTRIC GUITAR Yanni Benjamin purchased a good-quality electric guitar with amplifier and financed $3600 over 12 months. The finance charge was $260. (a) Estimate the APR,___________ then (b) find the exact APR using the table.___________

ELECTRIC GUITAR Yanni Benjamin purchased a good-quality electric guitar with amplifier and financed $3600 over 12 months. The finance charge was $260. (a) Estimate the APR,___________ then (b) find the exact APR using the table.___________

Question

Find the balance due on the maturity date of the following notes. Find the total amount of interest paid on the note. Use the United States Rule. (See Examples.)

Finding the Amount Due

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

Finding the Interest Paid and Amount Due

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Finding the Amount Due

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

Finding the Interest Paid and Amount Due

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Question

Question

Use the loan payoff table to find the monthly payment (MP) and finance charge (FC) for each of the following loans. (See Example.)

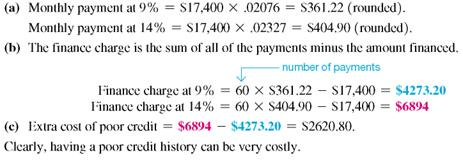

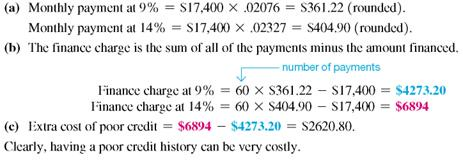

Finding Amortization Payments

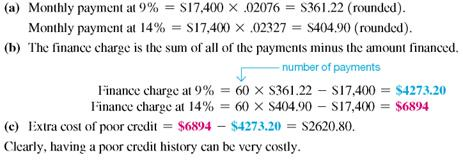

After a trade-in, Vickie Ewing owes $17,400 on a new Harley-Davidson motorcycle and wishes to pay the loan off in 60 months. She has found that she can finance the loan at 9% per year if she has a good credit history, but at 14, per year if she has a poor credit history.

(a) Find the monthly payment at both interest rates.

(b) Find the total finance charge at both interest rates.

(c) Find the extra cost of having poor credit.

SOLUTION

Finding Amortization Payments

After a trade-in, Vickie Ewing owes $17,400 on a new Harley-Davidson motorcycle and wishes to pay the loan off in 60 months. She has found that she can finance the loan at 9% per year if she has a good credit history, but at 14, per year if she has a poor credit history.

(a) Find the monthly payment at both interest rates.

(b) Find the total finance charge at both interest rates.

(c) Find the extra cost of having poor credit.

SOLUTION

Question

Use the real estate amortization table to find the monthly payment for the following loans. (See Example 1.)

Question

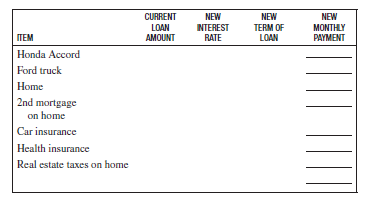

Roberto and Julie Hernandez are struggling to make their monthly payments. They accumulated too much debt, which was easy to do with two young kids at home. Julie works 30 hours a week and takes care of the two kids. Their credit history had been poor, but Roberto took on a second job during the evenings and they have been making payments regularly for 8 months.

After discussing things with Jackie Waterton at Citibank, the Hernandez's have learned that they can (1) refinance the remaining $14,900 amount on the Honda Accord at 12 over 4 years, (2) refinance the remaining $8600 loan amount on the Ford truck at 12 over 3 years, (3) refinance the remaining $94,800 loan amount on their home at 8 over 30 years, and (4) reduce their car insurance payments by $28 per month. Complete the following table.

After discussing things with Jackie Waterton at Citibank, the Hernandez's have learned that they can (1) refinance the remaining $14,900 amount on the Honda Accord at 12 over 4 years, (2) refinance the remaining $8600 loan amount on the Ford truck at 12 over 3 years, (3) refinance the remaining $94,800 loan amount on their home at 8 over 30 years, and (4) reduce their car insurance payments by $28 per month. Complete the following table.

Question

Question

Question

Find the finance charge for the following revolving charge accounts. Assume that interest is calculated on the average daily balance of the account. (See Example.)

Finding the Average Daily Balance

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION

SOLUTION

(a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Finding the Average Daily Balance

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION (a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Question

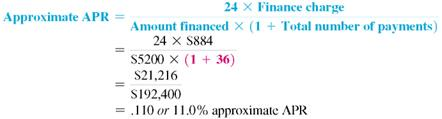

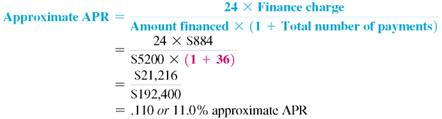

Find the approximate annual percentage rate using the approximate annual percentage rate formula. Round to the nearest tenth of a percent. (See Example.)

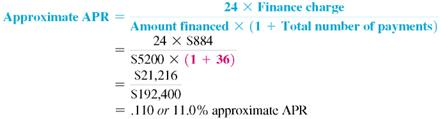

Finding the Annual Percentage Rate

Ed Chamski decides to buy a used car for $6400. He makes a down payment of $1200 and monthly payments of $169 for 36 months. Find the approximate annual percentage rate rounded to the nearest tenth of a percent.

SOLUTION

Use the steps outlined above.

Quick TIP

The precise APR can be found using a financial calculator as shown in examples in Appendix C.

Use the formula for approximate APR. Replace the finance charge with $884, the amount financed with $5200, and the number of payments with 36.

The approximate annual percentage rate on this loan is 11%. Example shows how to find the actual APR for this loan.

Finding the Annual Percentage Rate

In Example, a used car costing $6400 was financed at $169 per month for 36 months after a down payment of $1200. The total finance charge was $884, and the amount financed was $5200. Find the annual percentage rate.

SOLUTION

Step 1 Multiply the finance charge by $100, and divide by the amount financed.

Quick TIP

When using the annual percentage rate table, select the column with the table number that is closest to the finance charge per $100 of amount financed.

This gives the finance charge per $100 financed.

Step 2 Read down the left column of the annual percentage rate table to the line for 36 months (the actual number of monthly payments). Follow across to the right to find the number closest to $17.00. Here, find 17.01. Read the number at the top of this column of figures to find the annual percentage rate, 10.50%.

In this example, 10.50% is the annual percentage rate that must be disclosed to the buyer of the car. In Example, the formula for the approximate annual percentage rate gave an answer of 11%, which is not accurate enough to meet the requirements of the law.

Finding the Annual Percentage Rate

Ed Chamski decides to buy a used car for $6400. He makes a down payment of $1200 and monthly payments of $169 for 36 months. Find the approximate annual percentage rate rounded to the nearest tenth of a percent.

SOLUTION

Use the steps outlined above.

Quick TIP

The precise APR can be found using a financial calculator as shown in examples in Appendix C.

Use the formula for approximate APR. Replace the finance charge with $884, the amount financed with $5200, and the number of payments with 36.

The approximate annual percentage rate on this loan is 11%. Example shows how to find the actual APR for this loan.

Finding the Annual Percentage Rate

In Example, a used car costing $6400 was financed at $169 per month for 36 months after a down payment of $1200. The total finance charge was $884, and the amount financed was $5200. Find the annual percentage rate.

SOLUTION

Step 1 Multiply the finance charge by $100, and divide by the amount financed.

Quick TIP

When using the annual percentage rate table, select the column with the table number that is closest to the finance charge per $100 of amount financed.

This gives the finance charge per $100 financed.

Step 2 Read down the left column of the annual percentage rate table to the line for 36 months (the actual number of monthly payments). Follow across to the right to find the number closest to $17.00. Here, find 17.01. Read the number at the top of this column of figures to find the annual percentage rate, 10.50%.

In this example, 10.50% is the annual percentage rate that must be disclosed to the buyer of the car. In Example, the formula for the approximate annual percentage rate gave an answer of 11%, which is not accurate enough to meet the requirements of the law.

Question

Question

Find the balance due on the maturity date of the following notes. Find the total amount of interest paid on the note. Use the United States Rule. (See Examples.)

Finding the Amount Due

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

Finding the Interest Paid and Amount Due

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Finding the Amount Due

On August 14, Dr. Jane Ficker signed a 180-day note for $28,500 for a used x-ray machine for her dental office. The note has an interest rate of 10% compounded annually. On October 25, a payment of $8500 is made. (a) Find the balance owed on the principal after the payment. (b) If no additional payments are made, find the amount due at maturity of the loan.

SOLUTION

Finding the Interest Paid and Amount Due

On March 1, Boston Dairy signs a promissory note for $38,500 to replace some milking equipment for their Holsteins. The note is for 180 days at a rate of 10%. The dairy makes the following partial payments: $6000 on June 9 and $3500 on July 11. Find the interest paid on the note and the amount due on the due date of the note.

SOLUTION

The first partial payment is on June 9 or, using the number of days in each month, after

(30 + 30 + 31 + 9) = 100 days.

Debt on July 11 after 2nd partial payment = $33,569.44 ? $3201.60 = $ 30,367.84

The first partial payment is made after 100 days, and the second partial payment is made after an additional 32 days. Thus, the due date of the note is 180 ? 100 ? 32 = 48 days after the second partial payment.

Question

Solve the following application problems using the Rule of 78. (See Example.)

Finding Unearned Interest and Balance Due

Aaron Ortego borrowed $6000, which he is paying back in 24 monthly payments of $295 each. With 9 payments remaining, he decides to repay the loan in full. Find (a) the amount of unearned interest and (b) the amount necessary to repay the loan in full. Use the Rule of 78.

SOLUTION

Find the amount of unearned interest as follows. The finance charge is $1080, the scheduled number of payments is 24, and the loan is paid off with 9 payments left. Solve as follows.

(b) When Ortego decides to pay off the loan, he has 9 payments of $295 left.

Ortego saves the unearned interest of $162 by paying off the loan early. Therefore, the amount needed to pay the loan in full is the sum of the remaining payments minus the unearned interest.

GARBAGE TRUCK Haul-it-Away, Inc., purchased a dump truck for $62,000. The owners made a down payment of $22,000 and financed the remainder with 36 payments of $1328.57 each. They paid off the note with 12 payments remaining. Find (a) the amount of unearned interest __________ and (b) the amount necessary to pay the loan in full. __________

Finding Unearned Interest and Balance Due

Aaron Ortego borrowed $6000, which he is paying back in 24 monthly payments of $295 each. With 9 payments remaining, he decides to repay the loan in full. Find (a) the amount of unearned interest and (b) the amount necessary to repay the loan in full. Use the Rule of 78.

SOLUTION

Find the amount of unearned interest as follows. The finance charge is $1080, the scheduled number of payments is 24, and the loan is paid off with 9 payments left. Solve as follows.

(b) When Ortego decides to pay off the loan, he has 9 payments of $295 left.

Ortego saves the unearned interest of $162 by paying off the loan early. Therefore, the amount needed to pay the loan in full is the sum of the remaining payments minus the unearned interest.

GARBAGE TRUCK Haul-it-Away, Inc., purchased a dump truck for $62,000. The owners made a down payment of $22,000 and financed the remainder with 36 payments of $1328.57 each. They paid off the note with 12 payments remaining. Find (a) the amount of unearned interest __________ and (b) the amount necessary to pay the loan in full. __________

Question

Use the loan payoff table to find the monthly payment (MP) and finance charge (FC) for each of the following loans. (See Example.)

Finding Amortization Payments

After a trade-in, Vickie Ewing owes $17,400 on a new Harley-Davidson motorcycle and wishes to pay the loan off in 60 months. She has found that she can finance the loan at 9% per year if she has a good credit history, but at 14, per year if she has a poor credit history.

(a) Find the monthly payment at both interest rates.

(b) Find the total finance charge at both interest rates.

(c) Find the extra cost of having poor credit.

SOLUTION

Finding Amortization Payments

After a trade-in, Vickie Ewing owes $17,400 on a new Harley-Davidson motorcycle and wishes to pay the loan off in 60 months. She has found that she can finance the loan at 9% per year if she has a good credit history, but at 14, per year if she has a poor credit history.

(a) Find the monthly payment at both interest rates.

(b) Find the total finance charge at both interest rates.

(c) Find the extra cost of having poor credit.

SOLUTION

Question

Use the real estate amortization table to find the monthly payment for the following loans. (See Example.)

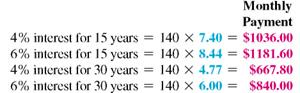

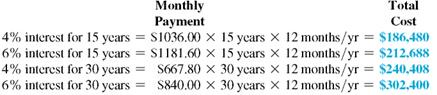

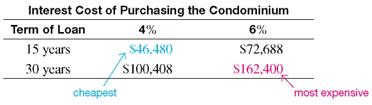

Understanding the Effects of Rate and Term

After making a down payment, the Stringers need to borrow $140,000 to purchase a condominium. They want to know the effect of the interest rate and term of the loan on cost. (a) Find the monthly payment for both 15 and 30 years at 4% and 6%. Then find (b) the total cost of the home with each loan and (c) the finance charge for each loan.

Quick TIP

Be sure to divide the loan amount by $1000 before calculating the monthly payment.

SOLUTION

(a) The amount to be financed in thousands = $140,000 ÷ $1000 = 140. Multiply this value by the appropriate factor from the real estate amortization table.

Monthly payments range from $667.80 to $1181.60, depending on the interest rate and length of the loan. The lowest payment of $667.80 may look good at first, but read part (b) below.

(b) The total cost of the home is the sum of all payments over the respective months and years.

(c) The finance charge, or interest cost, of each of the loans is the total cost found in part (b) minus the amount financed of $140,000.

Quick TIP

You can reduce your long-term cost of a mortgage by paying more than the required payment every month. Even an extra $60 per month can make a big difference over the long run.

First, notice that interest adds quite a bit to the cost of the $140,000 loan. The longer term of 30 years results in a significantly lower house payment, but it also results in a much higher eventual cost. So, the longer term loan of 30 years is not necessarily the best choice. Clearly, higher interest rates and longer terms ADD HUGE amounts to the interest that must be paid to purchase a property.

Understanding the Effects of Rate and Term

After making a down payment, the Stringers need to borrow $140,000 to purchase a condominium. They want to know the effect of the interest rate and term of the loan on cost. (a) Find the monthly payment for both 15 and 30 years at 4% and 6%. Then find (b) the total cost of the home with each loan and (c) the finance charge for each loan.

Quick TIP

Be sure to divide the loan amount by $1000 before calculating the monthly payment.

SOLUTION

(a) The amount to be financed in thousands = $140,000 ÷ $1000 = 140. Multiply this value by the appropriate factor from the real estate amortization table.

Monthly payments range from $667.80 to $1181.60, depending on the interest rate and length of the loan. The lowest payment of $667.80 may look good at first, but read part (b) below.

(b) The total cost of the home is the sum of all payments over the respective months and years.

(c) The finance charge, or interest cost, of each of the loans is the total cost found in part (b) minus the amount financed of $140,000.

Quick TIP

You can reduce your long-term cost of a mortgage by paying more than the required payment every month. Even an extra $60 per month can make a big difference over the long run.

First, notice that interest adds quite a bit to the cost of the $140,000 loan. The longer term of 30 years results in a significantly lower house payment, but it also results in a much higher eventual cost. So, the longer term loan of 30 years is not necessarily the best choice. Clearly, higher interest rates and longer terms ADD HUGE amounts to the interest that must be paid to purchase a property.

Question

Question

Question

Question

Find the finance charge for the following revolving charge accounts. Assume that interest is calculated on the average daily balance of the account. (See Example.)

Finding the Average Daily Balance

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION

SOLUTION

(a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Finding the Average Daily Balance

Beth Hogan's balance on a Visa card was $209.46 on March 3. Her activity for the next 30 days is shown in the table. (a) Find the average daily balance on April 3. Given finance charges based on 1 1 2 % on the average daily balance, find (b) the finance charge for the month and (c) the balance owed on April 3.

SOLUTION (a)

Quick TIP

The billing period in Example is 31 days. Some billing periods are 30 days (or 28 or 29 days in February). Be sure to use the correct number of days for the month of the billing period.

There are 31 days in the billing period (March has 31 days). Find the average daily balance as follows:

Step 1 Multiply each unpaid balance by the number of days for that balance.

Step 2 Total these amounts.

Step 3 Divide by the number of days in that particular billing cycle (month).

Hogan will pay a finance charge based on the average daily balance of $207.50.

(b) The finance charge is.015 × $207.50 = $3.11 (rounded).(c) The amount owed on April 3 is the beginning unpaid balance less any returns or payments, plus new charges and the finance charge.

Question

Find the approximate annual percentage rate using the approximate annual percentage rate formula. Round to the nearest tenth of a percent. (See Example.)

Finding the Annual Percentage Rate

Ed Chamski decides to buy a used car for $6400. He makes a down payment of $1200 and monthly payments of $169 for 36 months. Find the approximate annual percentage rate rounded to the nearest tenth of a percent.

SOLUTION

Use the steps outlined above.

Quick TIP

The precise APR can be found using a financial calculator as shown in examples in Appendix C.

Use the formula for approximate APR. Replace the finance charge with $884, the amount financed with $5200, and the number of payments with 36.

The approximate annual percentage rate on this loan is 11%. Example shows how to find the actual APR for this loan.

Finding the Annual Percentage Rate

In Example, a used car costing $6400 was financed at $169 per month for 36 months after a down payment of $1200. The total finance charge was $884, and the amount financed was $5200. Find the annual percentage rate.

SOLUTION

Step 1 Multiply the finance charge by $100, and divide by the amount financed.

Quick TIP

When using the annual percentage rate table, select the column with the table number that is closest to the finance charge per $100 of amount financed.

This gives the finance charge per $100 financed.

Step 2 Read down the left column of the annual percentage rate table to the line for 36 months (the actual number of monthly payments). Follow across to the right to find the number closest to $17.00. Here, find 17.01. Read the number at the top of this column of figures to find the annual percentage rate, 10.50%.

In this example, 10.50% is the annual percentage rate that must be disclosed to the buyer of the car. In Example, the formula for the approximate annual percentage rate gave an answer of 11%, which is not accurate enough to meet the requirements of the law.

Finding the Annual Percentage Rate

Ed Chamski decides to buy a used car for $6400. He makes a down payment of $1200 and monthly payments of $169 for 36 months. Find the approximate annual percentage rate rounded to the nearest tenth of a percent.

SOLUTION

Use the steps outlined above.

Quick TIP

The precise APR can be found using a financial calculator as shown in examples in Appendix C.

Use the formula for approximate APR. Replace the finance charge with $884, the amount financed with $5200, and the number of payments with 36.

The approximate annual percentage rate on this loan is 11%. Example shows how to find the actual APR for this loan.

Finding the Annual Percentage Rate

In Example, a used car costing $6400 was financed at $169 per month for 36 months after a down payment of $1200. The total finance charge was $884, and the amount financed was $5200. Find the annual percentage rate.

SOLUTION

Step 1 Multiply the finance charge by $100, and divide by the amount financed.

Quick TIP

When using the annual percentage rate table, select the column with the table number that is closest to the finance charge per $100 of amount financed.

This gives the finance charge per $100 financed.

Step 2 Read down the left column of the annual percentage rate table to the line for 36 months (the actual number of monthly payments). Follow across to the right to find the number closest to $17.00. Here, find 17.01. Read the number at the top of this column of figures to find the annual percentage rate, 10.50%.

In this example, 10.50% is the annual percentage rate that must be disclosed to the buyer of the car. In Example, the formula for the approximate annual percentage rate gave an answer of 11%, which is not accurate enough to meet the requirements of the law.

Question

Question

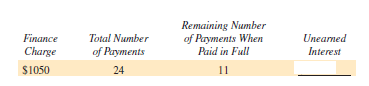

Each of the following loans is paid in full before the date of maturity. Find the amount of unearned interest. Use the Rule of 78. (See Example 3.)

Question

Solve the following application problems using the Rule of 78. (See Example.)

Finding Unearned Interest and Balance Due

Aaron Ortego borrowed $6000, which he is paying back in 24 monthly payments of $295 each. With 9 payments remaining, he decides to repay the loan in full. Find (a) the amount of unearned interest and (b) the amount necessary to repay the loan in full. Use the Rule of 78.

SOLUTION

Find the amount of unearned interest as follows. The finance charge is $1080, the scheduled number of payments is 24, and the loan is paid off with 9 payments left. Solve as follows.

(b) When Ortego decides to pay off the loan, he has 9 payments of $295 left.

Ortego saves the unearned interest of $162 by paying off the loan early. Therefore, the amount needed to pay the loan in full is the sum of the remaining payments minus the unearned interest.

PRINTING BlackTop Printing made a $5000 down payment on a special copy machine costing $23,800. The loan agreement with Citibank called for 20 monthly payments of $1025 each. Find (a) the finance charge, __________ (b) the unearned interest, __________ and (c) the amount necessary to pay the loan in full after the 14th payment. __________

Finding Unearned Interest and Balance Due

Aaron Ortego borrowed $6000, which he is paying back in 24 monthly payments of $295 each. With 9 payments remaining, he decides to repay the loan in full. Find (a) the amount of unearned interest and (b) the amount necessary to repay the loan in full. Use the Rule of 78.

SOLUTION

Find the amount of unearned interest as follows. The finance charge is $1080, the scheduled number of payments is 24, and the loan is paid off with 9 payments left. Solve as follows.

(b) When Ortego decides to pay off the loan, he has 9 payments of $295 left.

Ortego saves the unearned interest of $162 by paying off the loan early. Therefore, the amount needed to pay the loan in full is the sum of the remaining payments minus the unearned interest.

PRINTING BlackTop Printing made a $5000 down payment on a special copy machine costing $23,800. The loan agreement with Citibank called for 20 monthly payments of $1025 each. Find (a) the finance charge, __________ (b) the unearned interest, __________ and (c) the amount necessary to pay the loan in full after the 14th payment. __________

Question

Use the loan payoff table to find the monthly payment (MP) and finance charge (FC) for each of the following loans. (See Example.)

Finding Amortization Payments

After a trade-in, Vickie Ewing owes $17,400 on a new Harley-Davidson motorcycle and wishes to pay the loan off in 60 months. She has found that she can finance the loan at 9% per year if she has a good credit history, but at 14, per year if she has a poor credit history.

(a) Find the monthly payment at both interest rates.

(b) Find the total finance charge at both interest rates.

(c) Find the extra cost of having poor credit.

SOLUTION

Finding Amortization Payments

After a trade-in, Vickie Ewing owes $17,400 on a new Harley-Davidson motorcycle and wishes to pay the loan off in 60 months. She has found that she can finance the loan at 9% per year if she has a good credit history, but at 14, per year if she has a poor credit history.

(a) Find the monthly payment at both interest rates.

(b) Find the total finance charge at both interest rates.

(c) Find the extra cost of having poor credit.

SOLUTION

Question

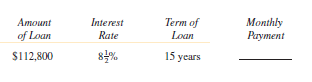

Use the real estate amortization table to find the monthly payment for the following loans. (See Example 1.)

Question

Find the annual percentage rate, using the annual percentage rate table.

Question

Question

Question

Solve the following application problems.

HOT TUB PURCHASE Betty Thomas borrowed $6500 on her Visa card to install a hot tub with landscaping around it. The interest charges are 1.6% per month on the unpaid balance. (a) Find the interest charges. __________ (b) Find the interest charges if she moves the debt to a credit card charging 1% per month on the unpaid balance. __________ (c) Find the monthly savings.__________

HOT TUB PURCHASE Betty Thomas borrowed $6500 on her Visa card to install a hot tub with landscaping around it. The interest charges are 1.6% per month on the unpaid balance. (a) Find the interest charges. __________ (b) Find the interest charges if she moves the debt to a credit card charging 1% per month on the unpaid balance. __________ (c) Find the monthly savings.__________

Question

Find the approximate annual percentage rate using the approximate annual percentage rate formula. Round to the nearest tenth of a percent. (See Example.)

Finding the Annual Percentage Rate

Ed Chamski decides to buy a used car for $6400. He makes a down payment of $1200 and monthly payments of $169 for 36 months. Find the approximate annual percentage rate rounded to the nearest tenth of a percent.

SOLUTION

Use the steps outlined above.

Quick TIP

The precise APR can be found using a financial calculator as shown in examples in Appendix C.

Use the formula for approximate APR. Replace the finance charge with $884, the amount financed with $5200, and the number of payments with 36.

The approximate annual percentage rate on this loan is 11%. Example shows how to find the actual APR for this loan.

Finding the Annual Percentage Rate

In Example, a used car costing $6400 was financed at $169 per month for 36 months after a down payment of $1200. The total finance charge was $884, and the amount financed was $5200. Find the annual percentage rate.

SOLUTION

Step 1 Multiply the finance charge by $100, and divide by the amount financed.

Quick TIP

When using the annual percentage rate table, select the column with the table number that is closest to the finance charge per $100 of amount financed.

This gives the finance charge per $100 financed.

Step 2 Read down the left column of the annual percentage rate table to the line for 36 months (the actual number of monthly payments). Follow across to the right to find the number closest to $17.00. Here, find 17.01. Read the number at the top of this column of figures to find the annual percentage rate, 10.50%.

In this example, 10.50% is the annual percentage rate that must be disclosed to the buyer of the car. In Example, the formula for the approximate annual percentage rate gave an answer of 11%, which is not accurate enough to meet the requirements of the law.

Finding the Annual Percentage Rate

Ed Chamski decides to buy a used car for $6400. He makes a down payment of $1200 and monthly payments of $169 for 36 months. Find the approximate annual percentage rate rounded to the nearest tenth of a percent.

SOLUTION

Use the steps outlined above.

Quick TIP

The precise APR can be found using a financial calculator as shown in examples in Appendix C.

Use the formula for approximate APR. Replace the finance charge with $884, the amount financed with $5200, and the number of payments with 36.

The approximate annual percentage rate on this loan is 11%. Example shows how to find the actual APR for this loan.

Finding the Annual Percentage Rate

In Example, a used car costing $6400 was financed at $169 per month for 36 months after a down payment of $1200. The total finance charge was $884, and the amount financed was $5200. Find the annual percentage rate.

SOLUTION

Step 1 Multiply the finance charge by $100, and divide by the amount financed.

Quick TIP

When using the annual percentage rate table, select the column with the table number that is closest to the finance charge per $100 of amount financed.

This gives the finance charge per $100 financed.

Step 2 Read down the left column of the annual percentage rate table to the line for 36 months (the actual number of monthly payments). Follow across to the right to find the number closest to $17.00. Here, find 17.01. Read the number at the top of this column of figures to find the annual percentage rate, 10.50%.

In this example, 10.50% is the annual percentage rate that must be disclosed to the buyer of the car. In Example, the formula for the approximate annual percentage rate gave an answer of 11%, which is not accurate enough to meet the requirements of the law.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/168

Play

Full screen (f)

Deck 12: Business and Consumer Loans

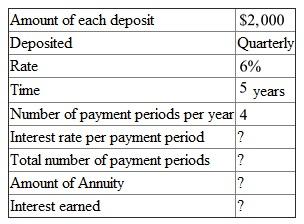

1

Round money amounts to the nearest cent and rates to the nearest tenth of a percent.

Find the amount and interest earned of each of the following ordinary annuities.

Find the amount and interest earned of each of the following ordinary annuities.

This is a problem of finding the amount of an annuity.

The following table is given, There are

There are  payment periods.

payment periods.

The interest rate per payment period is .

.

Look across the top of the Amount of an Annuity Table for and down the side for

and down the side for  periods to find

periods to find  .

.

Recall the formula, Finding Amount of an Annuity,

" , or

, or  "

"

Use , and

, and  in the formula above,

in the formula above,  Therefore, the amount of annuity is

Therefore, the amount of annuity is  .

.

Recall the formula, Finding Interest of an Annuity,

" , or

, or  "

"

Use ,

,  , and

, and  in the formula above,

in the formula above,  Therefore, the interest earned is

Therefore, the interest earned is  .

.

The following table is given,

There are payment periods. The interest rate per payment period is

. Look across the top of the Amount of an Annuity Table for

and down the side for periods to find . Recall the formula, Finding Amount of an Annuity,

"

, or "Use

, and in the formula above, Therefore, the amount of annuity is .Recall the formula, Finding Interest of an Annuity,

"

, or "Use

, , and in the formula above, Therefore, the interest earned is . 2

Solve the following application problems.