Deck 9: The Capital Asset Pricing Model Capm

Full screen (f)

Question

Question

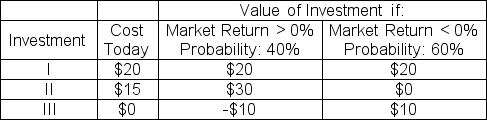

Which of the following investments would a risk-averse investor prefer if the risk-free rate is zero?

A)I only

B)II only

C)III only

D)I and III only

A)I only

B)II only

C)III only

D)I and III only

Question

Question

Question

Question

Question

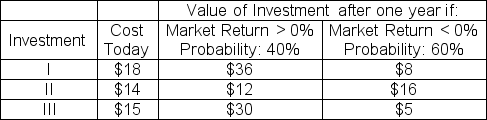

Given the following information, which investment(s)would risk-averse investors prefer if the risk-free rate is 5%?

A)I only

B)II only

C)III only

D)I and II only

A)I only

B)II only

C)III only

D)I and II only

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

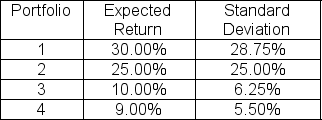

The expected return on the market is 15% with a standard deviation of 12.5% and the risk-free rate is 5%.Which of the following portfolios are correctly priced?

A)1 and 3 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

A)1 and 3 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

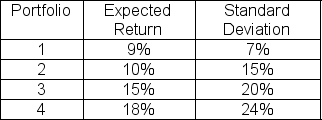

The expected return on the market is 11.5% with a standard deviation of 13% and the risk-free rate is 4%.Which of the following portfolios are undervalued?

A)1 and 2 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

A)1 and 2 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

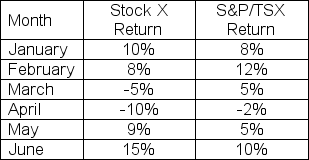

Given the following information, what is the beta of Stock X?

A)0.08

B)0.41

C)0.62

D)1.61

A)0.08

B)0.41

C)0.62

D)1.61

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/115

Play

Full screen (f)

Deck 9: The Capital Asset Pricing Model Capm

1

Which one of the following is NOT true?

A)Insurance premiums change with the level of risk aversion of the investor.

B)Risk premiums change with the level of risk aversion of the investor.

C)All investors are sitting at the same point on the efficient frontier.

D)T-bills represent the lowest level of return that an investor expects to get.

A)Insurance premiums change with the level of risk aversion of the investor.

B)Risk premiums change with the level of risk aversion of the investor.

C)All investors are sitting at the same point on the efficient frontier.

D)T-bills represent the lowest level of return that an investor expects to get.

All investors are sitting at the same point on the efficient frontier.

2

Which of the following investments would a risk-averse investor prefer if the risk-free rate is zero?

A)I only

B)II only

C)III only

D)I and III only

A)I only

B)II only

C)III only

D)I and III only

III only

3

Which of the following is NOT a correct statement?

A)Risk-averse investors will not willingly undertake fair gambles.

B)Risk-averse investors prefer to gamble on a risky situation where there is an equal probability of winning or losing the same amount of money.

C)Risk-averse investors require a risk premium to bear risk; the more risk averse they are, the higher the risk premium they require.

D)Risk-averse investors are willing to pay an insurance premium to get out of a risky situation.

A)Risk-averse investors will not willingly undertake fair gambles.

B)Risk-averse investors prefer to gamble on a risky situation where there is an equal probability of winning or losing the same amount of money.

C)Risk-averse investors require a risk premium to bear risk; the more risk averse they are, the higher the risk premium they require.

D)Risk-averse investors are willing to pay an insurance premium to get out of a risky situation.

Risk-averse investors prefer to gamble on a risky situation where there is an equal probability of winning or losing the same amount of money.

4

Which one of the following is NOT true?

A)The separation theorem states that the borrowing decision and investment decision are separate.

B)Investors should look at investments in terms of their prospective return, not their cost

C)The separation theorem states that you cannot separate your risk-free and stock investments.

D)The market portfolio is the tangent line that goes through the risk-free rate.

A)The separation theorem states that the borrowing decision and investment decision are separate.

B)Investors should look at investments in terms of their prospective return, not their cost

C)The separation theorem states that you cannot separate your risk-free and stock investments.

D)The market portfolio is the tangent line that goes through the risk-free rate.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

5

A portfolio consists of two securities: a 90-day T-bill and the S&P/TSX Composite.The expected return on the T-bill is 4.5%.The expected return on the S&P/TSX Composite is 12% with a standard deviation of 20%.What is the portfolio standard deviation if the expected return for this portfolio is 15%?

A)8.13%

B)12.00%

C)16.80%

D)28.00%

A)8.13%

B)12.00%

C)16.80%

D)28.00%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

6

A portfolio consists of two securities: a risk-free asset and an equity security.The expected return on the risk-free asset is 4.75%.The expected return of the equity security is 17% with a standard deviation of 23%.What is the portfolio expected return if the standard deviation for the portfolio is 18%?

A)7.41%

B)14.34%

C)18.00%

D)20.40%

A)7.41%

B)14.34%

C)18.00%

D)20.40%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

7

Given the following information, which investment(s)would risk-averse investors prefer if the risk-free rate is 5%?

A)I only

B)II only

C)III only

D)I and II only

A)I only

B)II only

C)III only

D)I and II only

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

8

What is the expected value from an investment that is equally likely to move from $100 to $180 or $100 to $70?

A)$ 140

B)$ 115

C)$ 85

D)$ 125

A)$ 140

B)$ 115

C)$ 85

D)$ 125

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

9

A portfolio consists of two securities: a risk-free asset and an equity security.The expected return on the risk-free asset is 4.25%.The expected return of the equity security is 16% with a standard deviation of 22%.What is the portfolio standard deviation if the expected return for the portfolio is 12%?

A)6.99%

B)7.49%

C)10.55%

D)14.51%

A)6.99%

B)7.49%

C)10.55%

D)14.51%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

10

A risk-averse investor has an opportunity to invest in the following securities:

Security A costs $10 today and will have a value of $25 if the market goes up and $0 if the market goes down

Security B costs $8 today and will have a value of $12 if the market goes up and $6 if the market goes down

Security C costs $5 today and will have a value of $20 if the market goes up and -$20 if the market goes down.

If there is a 40% chance that the market will go up and the risk-free rate is zero, which security(ies)will the investor prefer?

A)A only

B)B only

C)C only

D)A and B only

Security A costs $10 today and will have a value of $25 if the market goes up and $0 if the market goes down

Security B costs $8 today and will have a value of $12 if the market goes up and $6 if the market goes down

Security C costs $5 today and will have a value of $20 if the market goes up and -$20 if the market goes down.

If there is a 40% chance that the market will go up and the risk-free rate is zero, which security(ies)will the investor prefer?

A)A only

B)B only

C)C only

D)A and B only

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

11

A portfolio consists of two securities: a 90-day T-bill and the S&P/TSX Composite.The expected return on the T-bill is 4.5%.The expected return of the S&P/TSX Composite is 18% with a standard deviation of 30%.What is the portfolio expected return if the standard deviation for this portfolio is 50%?

A)12.60%

B)27.00%

C)30.00%

D)47.00%

A)12.60%

B)27.00%

C)30.00%

D)47.00%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

12

The market portfolio is most accurately described as:

A)The portfolio that follows market averages like the S&P/TSX or the S&P 500

B)The portfolio similar to the MSCI AC World index

C)The portfolio of all risky assets in the market

D)The portfolio of all assets including risk-free assets

A)The portfolio that follows market averages like the S&P/TSX or the S&P 500

B)The portfolio similar to the MSCI AC World index

C)The portfolio of all risky assets in the market

D)The portfolio of all assets including risk-free assets

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

13

Theoretically, what is meant by the market portfolio?

A)The market index portfolio similar to the S&P 500 or S&P/TSX Composite

B)The world index portfolio similar to the MSCI AC World index

C)All risky assets in the world in their proper proportions

D)All assets including risk-free assets in their proper proportions

A)The market index portfolio similar to the S&P 500 or S&P/TSX Composite

B)The world index portfolio similar to the MSCI AC World index

C)All risky assets in the world in their proper proportions

D)All assets including risk-free assets in their proper proportions

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

14

What is the standard deviation for a portfolio that has $3,500 invested in a risk-free asset with 5% rate of return, and $6,500 invested in a risky asset with a 15% rate of return and a 22% standard deviation?

A)7.70%

B)9.75%

C)5.25%

D)14.30%

A)7.70%

B)9.75%

C)5.25%

D)14.30%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

15

Use the following statements to answer this question:

I.The risk premium is the expected payoff needed to get out of a risky situation.

II.The insurance premium is the payment needed to get into a risky situation.

III.Risk-averse investors willingly take fair gambles.

A)I, II, and III are correct.

B)I, II, and III are incorrect.

C)I, II are correct, and III is incorrect.

D)I, II are incorrect, and III is correct.

I.The risk premium is the expected payoff needed to get out of a risky situation.

II.The insurance premium is the payment needed to get into a risky situation.

III.Risk-averse investors willingly take fair gambles.

A)I, II, and III are correct.

B)I, II, and III are incorrect.

C)I, II are correct, and III is incorrect.

D)I, II are incorrect, and III is correct.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

16

What is the expected payoff from an investment that is equally likely to move from $100 to $180 or $100 to $70?

A)40

B)15

C)-15

D)25

A)40

B)15

C)-15

D)25

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

17

What is the expected return for a portfolio that has $2,500 invested in a risk-free asset with a 5% rate of return, and $7,500 invested in a risky asset with a 17% rate of return and a 28% standard deviation?

A)8.00%

B)10.75%

C)14.00%

D)22.25%

A)8.00%

B)10.75%

C)14.00%

D)22.25%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

18

What are the expected return and standard deviation for a portfolio that has $2,000 invested in a risk-free asset with 5.25% rate of return, and $8,000 invested in a risky asset with a 21% rate of return and a 35% standard deviation?

A)Expected return = 17.85%; standard deviation = 28.00%

B)Expected return = 28.00%; standard deviation = 17.85%

C)Expected return = 7.00%; standard deviation = 8.40%

D)Expected return = 8.40%; standard deviation = 7.00%

A)Expected return = 17.85%; standard deviation = 28.00%

B)Expected return = 28.00%; standard deviation = 17.85%

C)Expected return = 7.00%; standard deviation = 8.40%

D)Expected return = 8.40%; standard deviation = 7.00%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

19

A portfolio has $1,200 invested in a risk-free asset with a 5% rate of return, and $3,800 invested in a risky asset with a 15% rate of return and a 20% standard deviation.What is the standard deviation of the portfolio?

A)4.80%

B)8.75%

C)15.20%

D)16.77%

A)4.80%

B)8.75%

C)15.20%

D)16.77%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is a TRUE statement?

A)The tangent portfolio is the risky portfolio on the efficient frontier whose tangent line cuts the horizontal axis at the risk-free rate.

B)The new (or super)efficient frontier represents the portfolios composed of the risk-free rate and the tangent portfolio that offers the highest expected rate of return for any given level or risk.

C)The separation theorem states that the investment decision, (how to construct the portfolio of risky assets), is not separate from the financing decision, (how much should be invested or borrowed in the risk-free asset).

D)The market portfolio is a portfolio that contains some risky securities in the market.

A)The tangent portfolio is the risky portfolio on the efficient frontier whose tangent line cuts the horizontal axis at the risk-free rate.

B)The new (or super)efficient frontier represents the portfolios composed of the risk-free rate and the tangent portfolio that offers the highest expected rate of return for any given level or risk.

C)The separation theorem states that the investment decision, (how to construct the portfolio of risky assets), is not separate from the financing decision, (how much should be invested or borrowed in the risk-free asset).

D)The market portfolio is a portfolio that contains some risky securities in the market.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

21

The Capital Market Line (CML)relates:

A)expected return to beta.

B)the risk-free rate to the market portfolio's rate of return.

C)risk to beta.

D)expected return to standard deviation.

A)expected return to beta.

B)the risk-free rate to the market portfolio's rate of return.

C)risk to beta.

D)expected return to standard deviation.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

22

The expected return of the market portfolio is 14% with a standard deviation of 25%.The risk-free rate is 6%.What is the weight of the market portfolio in an efficient portfolio with a standard deviation of 30%?

A)1.20

B)0.83

C)0.20

D)0.17

A)1.20

B)0.83

C)0.20

D)0.17

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

23

Greg has $10,000 to invest in a risk-free asset and in the market portfolio.The risk-free rate is 4.8%.The market portfolio has an expected return of 13.6% with a standard deviation of 15%.What are the expected return and standard deviation for a portfolio with 30% of the funds invested in the risk-free asset?

A)Expected return = 10.50%; standard deviation = 10.96%

B)Expected return = 10.96%; standard deviation = 10.50%

C)Expected return = 4.50%; standard deviation = 7.44%

D)Expected return = 7.44%; standard deviation = 4.50%

A)Expected return = 10.50%; standard deviation = 10.96%

B)Expected return = 10.96%; standard deviation = 10.50%

C)Expected return = 4.50%; standard deviation = 7.44%

D)Expected return = 7.44%; standard deviation = 4.50%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

24

The risk-free rate is 5.25%.The expected return on the market is 12% with a standard deviation of 18%.What is the standard deviation of an efficient portfolio with a 16% expected return?

A)7.33%

B)10.12%

C)19.11%

D)28.67%

A)7.33%

B)10.12%

C)19.11%

D)28.67%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

25

The expected return of a portfolio on the Capital Market Line (CML)is 14% with a standard deviation of 25%.The risk-free rate is 6%.What is the expected return on an efficient portfolio with a standard deviation of 30%?

A)9.6%

B)15.6%

C)22.8%

D)16.8%

A)9.6%

B)15.6%

C)22.8%

D)16.8%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

26

By combining the risk-free asset and the efficient frontier, the _____________ will be created.

A)capital market line

B)efficient frontier

C)security market line

D)attainable set

A)capital market line

B)efficient frontier

C)security market line

D)attainable set

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following is a FALSE statement about the Sharpe ratio?

A)It is used to assess the performance of portfolios.

B)It describes how well an asset's return compensates investors for the risk taken.

C)It is the slope of the CML when the portfolio is not the market portfolio.

D)It is a "risk-adjusted" measure of portfolio performance.

A)It is used to assess the performance of portfolios.

B)It describes how well an asset's return compensates investors for the risk taken.

C)It is the slope of the CML when the portfolio is not the market portfolio.

D)It is a "risk-adjusted" measure of portfolio performance.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

28

What is the expected return on an efficient portfolio with a standard deviation of 15%? Assume the risk-free rate is 6% and the expected return on the market portfolio is 14.8% with a standard deviation of 20%.

A)8.20%

B)12.60%

C)16.50%

D)17.73%

A)8.20%

B)12.60%

C)16.50%

D)17.73%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

29

What is the standard deviation of an efficient portfolio with an 8% expected return? Assume the risk-free rate is 3.75% and the expected return on the market portfolio is 10% with a standard deviation of 20%.

A)2.62%

B)6.40%

C)6.80%

D)13.60%

A)2.62%

B)6.40%

C)6.80%

D)13.60%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

30

The Capital Asset Pricing Model (CAPM)relates:

A)expected return to beta.

B)expected return to risk.

C)expected risk to beta.

D)expected return to standard deviation.

A)expected return to beta.

B)expected return to risk.

C)expected risk to beta.

D)expected return to standard deviation.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

31

Use the following three statements to answer this question:

I.The Capital Market Line (CML)must always be upward sloping, and it predicts required returns.

II.The Capital Market Line (CML)is based on expected rates of return, so it is ex post.

III.The Capital Market Line (CML)slope is the Sharpe ratio.

A)I, II, and III are correct.

B)I, II, and III are incorrect.

C)I and III are correct and II is incorrect.

D)I is incorrect, II and III are correct.

I.The Capital Market Line (CML)must always be upward sloping, and it predicts required returns.

II.The Capital Market Line (CML)is based on expected rates of return, so it is ex post.

III.The Capital Market Line (CML)slope is the Sharpe ratio.

A)I, II, and III are correct.

B)I, II, and III are incorrect.

C)I and III are correct and II is incorrect.

D)I is incorrect, II and III are correct.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

32

An efficient portfolio has a 18% expected return.If the expected market return is 11% (with a standard deviation of 18%), and the risk-free rate is 5.5%, what is the standard deviation of the portfolio?

A)9.33%

B)11.12%

C)19.37%

D)40.91%

A)9.33%

B)11.12%

C)19.37%

D)40.91%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following is NOT an implication resulting from the assumption that capital markets are in equilibrium?

A)All assets are assumed to be bought and sold at the equilibrium price established by supply and demand.

B)All assets are not correctly priced to adequately compensate investors for the associated risks.

C)The price for an overpriced asset would eventually fall to an equilibrium level so that the asset is held by all investors.

D)The market portfolio will be the most efficient portfolio, with respect to the weights attached to the individual securities composing it.

A)All assets are assumed to be bought and sold at the equilibrium price established by supply and demand.

B)All assets are not correctly priced to adequately compensate investors for the associated risks.

C)The price for an overpriced asset would eventually fall to an equilibrium level so that the asset is held by all investors.

D)The market portfolio will be the most efficient portfolio, with respect to the weights attached to the individual securities composing it.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

34

You are considering investing in one of three investments - A, B or C.When plotted against the CML, Investment A is below the CML line, Investment B is above the CML line and Investment C is right on the CML line.Which of the following statements is then true?

A)Investment A is the best investment because it will be underpriced in the market because it has a higher level of risk than the other investments

B)Investment B is the best investment because it is underpriced since the expected rate of return is less than the required rate of return

C)Investment C has identical expected and required rates of return so this investment is the most fairly priced

D)The question cannot be answered with the information given

A)Investment A is the best investment because it will be underpriced in the market because it has a higher level of risk than the other investments

B)Investment B is the best investment because it is underpriced since the expected rate of return is less than the required rate of return

C)Investment C has identical expected and required rates of return so this investment is the most fairly priced

D)The question cannot be answered with the information given

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

35

What does the capital market line represent?

A)The highest attainable expected return for any given risk level that includes only efficient portfolios.

B)The frontier of efficient portfolios of risky assets.

C)The best return portfolio.

D)The lowest variance portfolios.

A)The highest attainable expected return for any given risk level that includes only efficient portfolios.

B)The frontier of efficient portfolios of risky assets.

C)The best return portfolio.

D)The lowest variance portfolios.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following is a FALSE statement of the market price of risk?

A)It is the incremental risk divided by the incremental expected return.

B)It is the slope of the capital market line.

C)It is the equilibrium price of risk in the capital market.

D)It indicates the additional expected return that the market demands for an increase in a portfolio's risk.

A)It is the incremental risk divided by the incremental expected return.

B)It is the slope of the capital market line.

C)It is the equilibrium price of risk in the capital market.

D)It indicates the additional expected return that the market demands for an increase in a portfolio's risk.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

37

The CAPM Model makes the following assumptions below EXCEPT:

A)Assumes there are no transactional costs.

B)Assumes there are no personal income taxes.

C)Assumes that all investors have different expectations about expected returns, and standard deviations for all traded securities.

D)Assumes that all investors can borrow/lend at the risk-free rate.

A)Assumes there are no transactional costs.

B)Assumes there are no personal income taxes.

C)Assumes that all investors have different expectations about expected returns, and standard deviations for all traded securities.

D)Assumes that all investors can borrow/lend at the risk-free rate.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

38

The expected return of the market portfolio is 14% with a standard deviation of 25%.The risk-free rate is 6%.What would be the weight of the market portfolio in an efficient portfolio with a standard deviation of 30%, if borrowing is not allowed?

A)16.78%

B)83.33%

C)20%

D)Cannot be constructed

A)16.78%

B)83.33%

C)20%

D)Cannot be constructed

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

39

When applying the Sharpe ratio to assess portfolio management, which of the following statements is NOT true?

A)The higher the Sharpe ratio value then the risk-adjusted return is more favourable

B)The higher the Sharpe ratio value then the risk-adjusted return is less favourable

C)The lower the Sharpe ratio value then the risk-adjusted return is more favourable

D)The Sharpe ratio cannot be used to determine the performance of a portfolio

A)The higher the Sharpe ratio value then the risk-adjusted return is more favourable

B)The higher the Sharpe ratio value then the risk-adjusted return is less favourable

C)The lower the Sharpe ratio value then the risk-adjusted return is more favourable

D)The Sharpe ratio cannot be used to determine the performance of a portfolio

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

40

The expected return on the market is 12.5% with a standard deviation of 25%.The risk-free rate is 5.5%.What is the expected return on an efficient portfolio with a standard deviation of 30%?

A)4.10%

B)11.33%

C)13.90%

D)28.90%

A)4.10%

B)11.33%

C)13.90%

D)28.90%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

41

Under the CAPM, an investor should be compensated for bearing:

A)total risk

B)diversifiable risk

C)systematic risk

D)unsystematic risk

A)total risk

B)diversifiable risk

C)systematic risk

D)unsystematic risk

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

42

Assume that the CAPM holds.If a security has a beta of 1, its expected return is:

A)the risk-free rate

B)1.0 %

C)the return on the market portfolio

D)cannot be determined with the above information

A)the risk-free rate

B)1.0 %

C)the return on the market portfolio

D)cannot be determined with the above information

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

43

The expected return on the market is 15% with a standard deviation of 12.5% and the risk-free rate is 5%.Which of the following portfolios are correctly priced?

A)1 and 3 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

A)1 and 3 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

44

Suppose you have $5,000 to invest in a risk-free asset and the market portfolio.The expected return on the market portfolio is 13.5% with a standard deviation of 18%.The risk-free rate is 4.25%.How much of your funds should be in the risk-free asset if the portfolio has an expected return of 10%?

A)$1,892

B)$2,091

C)$2,909

D)$3,108

A)$1,892

B)$2,091

C)$2,909

D)$3,108

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

45

Suppose you have $2,000 to invest.The market portfolio has an expected return of 10.5% and a standard deviation of 16%.The risk-free rate is 3.75%.How much should you invest in the risk-free asset if you wish to have a 15% return on the portfolio?

A)$667

B)-$667

C)$1,333

D)-$1,333

A)$667

B)-$667

C)$1,333

D)-$1,333

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

46

The expected return on the market is 12% with a standard deviation of 20%.The risk-free rate is 4.5%.What is the Sharpe ratio of a portfolio with an expected return of 10.5% and a standard deviation of 12%?

A)0.38

B)0.50

C)0.70

D)0.88

A)0.38

B)0.50

C)0.70

D)0.88

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following is NOT a correct statement regarding beta?

A)It is a measure of market risk.

B)It measures the risk of an individual stock or portfolio relative to the market portfolio.

C)It is the slope of the capital market line.

D)It changes through time as the risk of the underlying security or portfolio changes.

A)It is a measure of market risk.

B)It measures the risk of an individual stock or portfolio relative to the market portfolio.

C)It is the slope of the capital market line.

D)It changes through time as the risk of the underlying security or portfolio changes.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

48

Use the following three statements to answer this question:

I.A security with a beta of zero implies that all of the variability in this security's return is diversifiable by any investor holding a well-diversified portfolio.

II.A security with a beta of 1 implies that if the market increased (or decreased)by 1%, the return on the security would increase (decrease)by more than 1% on average.

III.A security that has a beta value cannot be priced.

A)I, II and III are correct.

B)I, II and III are incorrect.

C)I is correct, II and III are incorrect.

D)I, II are incorrect, III is correct.

I.A security with a beta of zero implies that all of the variability in this security's return is diversifiable by any investor holding a well-diversified portfolio.

II.A security with a beta of 1 implies that if the market increased (or decreased)by 1%, the return on the security would increase (decrease)by more than 1% on average.

III.A security that has a beta value cannot be priced.

A)I, II and III are correct.

B)I, II and III are incorrect.

C)I is correct, II and III are incorrect.

D)I, II are incorrect, III is correct.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

49

The ____________ measures the sensitivity of the portfolio to changes in the overall market.

A)risk-free rate

B)beta

C)risk

D)market premium

A)risk-free rate

B)beta

C)risk

D)market premium

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

50

Use the following three statements to answer this question:

I.The CAPM points out that rational investors should be compensated for unique risk.

II.The CAPM implies that non-systematic risk is the appropriate measure of risk to determine the risk premium required by investors for holding a risky security.

III.The expected portfolio return from non-systematic risk is zero.

A)I, II and III are correct.

B)I and II are incorrect, III is correct.

C)I, II are correct, III is incorrect.

D)I, III are incorrect, II is correct.

I.The CAPM points out that rational investors should be compensated for unique risk.

II.The CAPM implies that non-systematic risk is the appropriate measure of risk to determine the risk premium required by investors for holding a risky security.

III.The expected portfolio return from non-systematic risk is zero.

A)I, II and III are correct.

B)I and II are incorrect, III is correct.

C)I, II are correct, III is incorrect.

D)I, III are incorrect, II is correct.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

51

The expected return on the market is 12% with a standard deviation of 15% and the risk-free rate is 5%.What is the required return on an efficient portfolio that has a standard deviation of 18%?

A)10.83%

B)12.67%

C)13.40%

D)14.40%

A)10.83%

B)12.67%

C)13.40%

D)14.40%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

52

The expected return of Security A is 12% with a standard deviation of 15%.The expected return of Security B is 9% with a standard deviation of 10%.Securities A and B have a correlation of 0.4.The market return is 11% with a standard deviation of 13% and the risk-free rate is 4%.What is the Sharpe ratio of a portfolio if 35% of the portfolio is in Security A and the remainder in Security B?

A)0.54

B)0.61

C)0.86

D)1.02

A)0.54

B)0.61

C)0.86

D)1.02

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

53

The expected return of Security A is 12% with a standard deviation of 15%.The expected return of Security B is 9% with a standard deviation of 10%.Securities A and B have a correlation of 0.4.The market return is 11% with a standard deviation of 13% and the risk-free rate is 4%.Which one of the following is not an efficient portfolio, as determined by the lowest Sharpe ratio?

A)100% invested in A is efficient

B)100% invested in B is efficient

C)41% in A and 59% B is efficient

D)59% in A and 41% B is efficient

A)100% invested in A is efficient

B)100% invested in B is efficient

C)41% in A and 59% B is efficient

D)59% in A and 41% B is efficient

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

54

The expected returns for Securities ABC and XYZ are 8% and 13%, respectively.The standard deviation is 12% for ABC and 18% for XYZ.There is no relationship between the returns on the two securities.The market return is 12.5% with a standard deviation of 16%.The risk-free rate is 5%.What is the Sharpe ratio of a portfolio with 40% of the funds in ABC and 60% in XYZ?

A)0.47

B)0.51

C)0.75

D)0.93

A)0.47

B)0.51

C)0.75

D)0.93

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

55

Beta is a measure of:

A)Total risk.

B)Diversifiable risk.

C)Systematic risk.

D)Unsystematic risk.

A)Total risk.

B)Diversifiable risk.

C)Systematic risk.

D)Unsystematic risk.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following describes how a portfolio changes relative to changes in the overall market?

A)market risk premium

B)beta

C)risk-free rate

D)systematic risk

A)market risk premium

B)beta

C)risk-free rate

D)systematic risk

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

57

What is the standard deviation of an efficient portfolio with a 7.5% expected rate of return, given that RF is 0.50%, ERm is 6.0% and m is 21%?

A)28.10%

B)3.56%

C)1.50%

D)26.69%

A)28.10%

B)3.56%

C)1.50%

D)26.69%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

58

Use the following three statements to answer this question:

I.The capital market line (CML)depicts the highest attainable expected return for any given risk level that includes only efficient portfolios.

II.The security market line (SML)depicts the required rate of return for any given risk level that includes only individual securities.

III.The Security Market Line (SML)measures the price of systematic risk.

A)I, II and III are correct.

B)I, II and III are incorrect.

C)I and III are correct, II is incorrect.

D)I is incorrect, II and III are correct.

I.The capital market line (CML)depicts the highest attainable expected return for any given risk level that includes only efficient portfolios.

II.The security market line (SML)depicts the required rate of return for any given risk level that includes only individual securities.

III.The Security Market Line (SML)measures the price of systematic risk.

A)I, II and III are correct.

B)I, II and III are incorrect.

C)I and III are correct, II is incorrect.

D)I is incorrect, II and III are correct.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

59

Min has $5,000 to invest.The expected return on the market portfolio is 11% with a standard deviation of 15%.What are the expected return and standard deviation for the portfolio if she borrowed $2,000 at the risk-free rate of 4% to invest in the market portfolio?

A)Expected return = 19.40%; standard deviation = 15.40%

B)Expected return = 15.40%; standard deviation = 19.40%

C)Expected return = 13.80%; standard deviation = 21.00%

D)Expected return = 21.00%; standard deviation = 13.80%

A)Expected return = 19.40%; standard deviation = 15.40%

B)Expected return = 15.40%; standard deviation = 19.40%

C)Expected return = 13.80%; standard deviation = 21.00%

D)Expected return = 21.00%; standard deviation = 13.80%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

60

The expected return on the market is 11.5% with a standard deviation of 13% and the risk-free rate is 4%.Which of the following portfolios are undervalued?

A)1 and 2 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

A)1 and 2 only

B)1 and 4 only

C)2 and 3 only

D)3 and 4 only

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

61

What is the beta of a portfolio if 40% of the funds are invested in a risk-free asset and the balance of the funds is invested in the market portfolio?

A)0.4

B)0.6

C)0.8

D)1.0

A)0.4

B)0.6

C)0.8

D)1.0

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

62

Which one of the following stocks would NOT likely have a beta close to 1?

A)A stock that is part of the most dominant industry.

B)A stock that has a very high capitalization.

C)A newly listed stock.

D)The stock of a well-established firm.

A)A stock that is part of the most dominant industry.

B)A stock that has a very high capitalization.

C)A newly listed stock.

D)The stock of a well-established firm.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

63

Stock X has a standard deviation of 25% and a correlation coefficient of 0.7 with market returns.The expected return of the market is 12% with a standard deviation of 15%.The risk-free rate is 5%.What is the required return of Stock X?

A)7.94%

B)9.56%

C)13.17%

D)15.28%

A)7.94%

B)9.56%

C)13.17%

D)15.28%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

64

The current price of Stock Y is $12.It is expected that the stock will pay an annual dividend of $0.60 and sell for $13.50 in one year.The risk-free rate is 6%.The expected return on the market portfolio is 14% with a standard deviation of 17%.Assume the market is in equilibrium.What is current rate of return on Stock Y?

A)6.50%

B)8.00%

C)12.50%

D)17.50%

A)6.50%

B)8.00%

C)12.50%

D)17.50%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

65

Use the following two statements to answer this question:

I.In equilibrium, the expected return on all properly priced securities will lie on the SML.

II.Securities that are undervalued will lie below the SML.

A)I and II are correct.

B)I and II are incorrect.

C)I is correct, II is incorrect.

D)I is incorrect, II is correct.

I.In equilibrium, the expected return on all properly priced securities will lie on the SML.

II.Securities that are undervalued will lie below the SML.

A)I and II are correct.

B)I and II are incorrect.

C)I is correct, II is incorrect.

D)I is incorrect, II is correct.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

66

Which of the following is a FALSE statement about the security market line (SML)?

A)It is upward sloping, which indicates that investors require a higher expected return on riskier securities.

B)It represents the trade off between total risk and the required rate of return for any risky security.

C)It indicates that the size of the risk premium varies directly with a security's market risk, as measured by beta.

D)It implies that securities with betas less than the market beta of 1.0 are less risky than the "average" stock and will therefore have lower required rates of return.

A)It is upward sloping, which indicates that investors require a higher expected return on riskier securities.

B)It represents the trade off between total risk and the required rate of return for any risky security.

C)It indicates that the size of the risk premium varies directly with a security's market risk, as measured by beta.

D)It implies that securities with betas less than the market beta of 1.0 are less risky than the "average" stock and will therefore have lower required rates of return.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

67

Use the following three statements to answer this question:

I.Beta is constant over time.

II.Empirically beta is never negative.

III.Negative beta implies a negative standard deviation.

A)I, II and III are correct.

B)I, II and III are incorrect.

C)I is correct, II and III are incorrect.

D)I, II are incorrect, III is correct.

I.Beta is constant over time.

II.Empirically beta is never negative.

III.Negative beta implies a negative standard deviation.

A)I, II and III are correct.

B)I, II and III are incorrect.

C)I is correct, II and III are incorrect.

D)I, II are incorrect, III is correct.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

68

Assuming the CAPM is valid, _____________ securities lie _____________the security market line.

A)undervalued, below

B)overvalued, on

C)undervalued, on

D)overvalued, below

A)undervalued, below

B)overvalued, on

C)undervalued, on

D)overvalued, below

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

69

Stock Z has a standard deviation of 18% and a covariance with the market of 0.0625.The expected return of the market is 13 with a standard deviation of 20%.The risk-free rate is 5%.What is the required return of Stock Z?

A)7.50%

B)7.78%

C)17.50%

D)20.43%

A)7.50%

B)7.78%

C)17.50%

D)20.43%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

70

Stock A has a standard deviation of 20% and a correlation coefficient of 0.64 with market returns.The expected return of the market is 12% with a standard deviation of 15%.The risk-free rate is 5%.What is the beta of Stock A?

A)0.48

B)0.75

C)0.85

D)1.33

A)0.48

B)0.75

C)0.85

D)1.33

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

71

The beta of a portfolio can be calculated as:

A)A sum of the betas of the stocks in the portfolio.

B)The weighted sum of the betas in the portfolio.

C)The average of the betas in the portfolios.

D)The weighted sum of the betas plus the correlation between betas.

A)A sum of the betas of the stocks in the portfolio.

B)The weighted sum of the betas in the portfolio.

C)The average of the betas in the portfolios.

D)The weighted sum of the betas plus the correlation between betas.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

72

According to the Capital Asset Pricing Model (CAPM), which one of the following statements is NOT true?

A)The expected rate of return of a security decreases proportionally with a decrease in the risk-free rate.

B)The expected rate of return of a security increases as its beta increases.

C)A fairly priced security has an alpha of zero.

D)In equilibrium, all securities lie on the security market line.

A)The expected rate of return of a security decreases proportionally with a decrease in the risk-free rate.

B)The expected rate of return of a security increases as its beta increases.

C)A fairly priced security has an alpha of zero.

D)In equilibrium, all securities lie on the security market line.

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

73

Stock A has a standard deviation of 20% and a correlation coefficient of 0.64 with market returns.The market risk premium is 12% with a standard deviation of 15%.The risk-free rate is 5%.What is the required rate of return of Stock A?

A)8.58%

B)10.95%

C)12.47%

D)15.20%

A)8.58%

B)10.95%

C)12.47%

D)15.20%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

74

Stock A has a standard deviation of 20% and a correlation coefficient of 0.64 with market returns.The expected return of the market is 12% with a standard deviation of 15%.The risk-free rate is 5%.What is the required rate of return of Stock A?

A)8.58%

B)10.95%

C)12.47%

D)15.20%

A)8.58%

B)10.95%

C)12.47%

D)15.20%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

75

Stock Y has a standard deviation of 22% and a covariance with the market of 0.081.The expected return of the market is 14% with a standard deviation of 18%.The risk-free rate is 5.25%.What is the beta of Stock Y?

A)0.37

B)0.45

C)1.67

D)2.50

A)0.37

B)0.45

C)1.67

D)2.50

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

76

What is the difference between the security market line (SML)and the capital market line (CML)?

A)SML prices total risk where CML prices non-systematic risk

B)SML prices systematic risk where CML prices total risk

C)SML prices total risk where CML prices systematic risk

D)SML prices systematic risk where CML prices non-systematic risk

A)SML prices total risk where CML prices non-systematic risk

B)SML prices systematic risk where CML prices total risk

C)SML prices total risk where CML prices systematic risk

D)SML prices systematic risk where CML prices non-systematic risk

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

77

_____________ is a measure of the risk of a security that cannot be avoided through diversification.

A)Variance

B)Standard deviation

C)Total risk

D)Beta

A)Variance

B)Standard deviation

C)Total risk

D)Beta

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

78

Given the following information, what is the beta of Stock X?

A)0.08

B)0.41

C)0.62

D)1.61

A)0.08

B)0.41

C)0.62

D)1.61

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

79

Stock Y has a standard deviation of 22% and a covariance with the market of 0.081.The expected return of the market is 14% with a standard deviation of 18%.The risk-free rate is 5.25%.What is the required rate of return of Stock Y?

A)6.14%

B)6.65%

C)17.25%

D)27.75%

A)6.14%

B)6.65%

C)17.25%

D)27.75%

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

80

Use the following two statements to answer this question:

I.The characteristic line is a statistical approximation of the SML.

II.The SML ignores non-systematic risk of a security.

A)I and II are correct

B)I is correct, II is incorrect

C)I and II are incorrect

D)I is incorrect and II is correct

I.The characteristic line is a statistical approximation of the SML.

II.The SML ignores non-systematic risk of a security.

A)I and II are correct

B)I is correct, II is incorrect

C)I and II are incorrect

D)I is incorrect and II is correct

Unlock Deck

Unlock for access to all 115 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 115 flashcards in this deck.