Deck 2: Governance and the Auditor

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

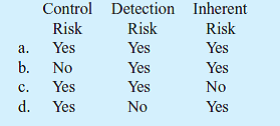

Which of the following audit risk components may be assessed in nonquantitative terms

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/28

Play

Full screen (f)

Deck 2: Governance and the Auditor

1

How do audit strategy and audit plan differ How are both related to the assessed risk of material misstatement

Financial statement:

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Audit risk:

Audit risk is the risk that the auditor fails to detect the error or fraud in the financial statement of the company. This means that the financial statement contains some errors that the auditor fails to find out in the auditing process.

Audit strategy:

• The audit strategy is the planning of audit engagement, objectives, timing and nature of the audit.

• It is the method of conducting the audit.

Audit plan:

• It is the written documents that contain details of the audits.

• It includes audit strategy and objectives.

• It is the detailed documents of steps in the audit.

Both the audit strategy and audit plan are related to the assessment of audit risk because in the planning phase of the audit process the company prepares the audit plan and audit risk according to the audit risk. The collection of proper evidence reduces the audit risk and increases the ability of the company to prepare an accurate audit plan and audit strategy.

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Audit risk:

Audit risk is the risk that the auditor fails to detect the error or fraud in the financial statement of the company. This means that the financial statement contains some errors that the auditor fails to find out in the auditing process.

Audit strategy:

• The audit strategy is the planning of audit engagement, objectives, timing and nature of the audit.

• It is the method of conducting the audit.

Audit plan:

• It is the written documents that contain details of the audits.

• It includes audit strategy and objectives.

• It is the detailed documents of steps in the audit.

Both the audit strategy and audit plan are related to the assessment of audit risk because in the planning phase of the audit process the company prepares the audit plan and audit risk according to the audit risk. The collection of proper evidence reduces the audit risk and increases the ability of the company to prepare an accurate audit plan and audit strategy.

2

Xerox

The Securities and Exchange Commission sued KPMG, LLP, and four KPMG partners in 2004 in connection with the Xerox Corporation audits from 1997-2000. According to the SEC, KPMG allowed Xerox to manipulate its earnings by making "top-side" adjustments to its financial statements at year-end to meet earnings targets. KPMG auditors in Europe, Brazil, Canada, and Japan warned KPMG auditors in Rochester, New York, the main Xerox office, that its executives were preparing entries to improve revenue and that the entries distorted true income. The partners charged in the lawsuit worked in KPMG's New York headquarters or in its Stamford, Connecticut, office near the Xerox headquarters. The partners ignored the warnings from those working on the audit in KPMG offices around the world and failed to investigate the practices Xerox used to manipulate income. According to the SEC, the auditors failed in their professional duty as auditors because they did not want to risk a "lucrative financial relationship with a premier client."

To manipulate earnings, Xerox accelerated the recognition of revenue from its sales type leases. According to the financial reporting framework (U.S. GAAP), revenue related to a product's value should be recognized immediately, but revenue related to financing, servicing, and supply services should be recognized over the life of the lease. Beginning in 1997, Xerox recognized financing and service revenue as part of the value of the equipment, allowing it to recognize revenue immediately. Either executives in Stamford or local managers gave instructions for the calculations to use to accelerate revenue recognition. Xerox told KPMG that it needed to make these changes because the method previously used to calculate revenue was outdated.

When the accelerated revenue policies became known to KPMG auditors in Europe, Brazil, Canada, and Japan, they expressed reservations about the change. Some of their comments included these: the new method was "not supportable" and it presented an "unnecessary control risk with regard to accounting methods." KPMG auditors in the United Kingdom (U.K.) repeatedly objected to the new revenue calculations, stating that they carried a "high risk of significant misstatement" and were "potentially arbitrary." In 2000, the U.K. auditor told Michael Conway, the partner in charge of the audit in the United States at that time, that the method for accelerating revenue did not produce earnings results that reflected economic reality.

Ronald Safran, KPMG engagement partner for Xerox in 1998 and 1999, expressed misgivings to Conway, the managing partner of KPMG's Department of Professional Practice, in 1999. Safran expressed concern about the risk of fraudulent financial reporting at Xerox. He worried about its tendency to adjust its methods to accelerate revenue recognition late in the year so the auditors would not have enough time to review the proposed change. Safran believed that company executives made adjusting entries at the end of the quarter as needed to meet earnings targets. He also believed that KPMG had an obligation to report these concerns to the Xerox Audit Committee but did not do so and ultimately signed off on the 1999 financial statements.

After the investigation, Xerox restated its earnings for $6.1 billion for 1997-2000. The company also paid a $10 million civil penalty for the earnings fraud.

a. Describe how the audit risk model might have helped the auditor perform the Xerox audit.

b. Did the auditors assess control risk too low Explain your answer.

c. Did the auditors assess inherent risk too low Explain your answer.

d. How should an auditor use materiality to plan the audit work related to revenue

e. Why did the auditors fail to give Xerox a qualified opinion or to ask the company to stop its accelerated revenue recognition program

The Securities and Exchange Commission sued KPMG, LLP, and four KPMG partners in 2004 in connection with the Xerox Corporation audits from 1997-2000. According to the SEC, KPMG allowed Xerox to manipulate its earnings by making "top-side" adjustments to its financial statements at year-end to meet earnings targets. KPMG auditors in Europe, Brazil, Canada, and Japan warned KPMG auditors in Rochester, New York, the main Xerox office, that its executives were preparing entries to improve revenue and that the entries distorted true income. The partners charged in the lawsuit worked in KPMG's New York headquarters or in its Stamford, Connecticut, office near the Xerox headquarters. The partners ignored the warnings from those working on the audit in KPMG offices around the world and failed to investigate the practices Xerox used to manipulate income. According to the SEC, the auditors failed in their professional duty as auditors because they did not want to risk a "lucrative financial relationship with a premier client."

To manipulate earnings, Xerox accelerated the recognition of revenue from its sales type leases. According to the financial reporting framework (U.S. GAAP), revenue related to a product's value should be recognized immediately, but revenue related to financing, servicing, and supply services should be recognized over the life of the lease. Beginning in 1997, Xerox recognized financing and service revenue as part of the value of the equipment, allowing it to recognize revenue immediately. Either executives in Stamford or local managers gave instructions for the calculations to use to accelerate revenue recognition. Xerox told KPMG that it needed to make these changes because the method previously used to calculate revenue was outdated.

When the accelerated revenue policies became known to KPMG auditors in Europe, Brazil, Canada, and Japan, they expressed reservations about the change. Some of their comments included these: the new method was "not supportable" and it presented an "unnecessary control risk with regard to accounting methods." KPMG auditors in the United Kingdom (U.K.) repeatedly objected to the new revenue calculations, stating that they carried a "high risk of significant misstatement" and were "potentially arbitrary." In 2000, the U.K. auditor told Michael Conway, the partner in charge of the audit in the United States at that time, that the method for accelerating revenue did not produce earnings results that reflected economic reality.

Ronald Safran, KPMG engagement partner for Xerox in 1998 and 1999, expressed misgivings to Conway, the managing partner of KPMG's Department of Professional Practice, in 1999. Safran expressed concern about the risk of fraudulent financial reporting at Xerox. He worried about its tendency to adjust its methods to accelerate revenue recognition late in the year so the auditors would not have enough time to review the proposed change. Safran believed that company executives made adjusting entries at the end of the quarter as needed to meet earnings targets. He also believed that KPMG had an obligation to report these concerns to the Xerox Audit Committee but did not do so and ultimately signed off on the 1999 financial statements.

After the investigation, Xerox restated its earnings for $6.1 billion for 1997-2000. The company also paid a $10 million civil penalty for the earnings fraud.

a. Describe how the audit risk model might have helped the auditor perform the Xerox audit.

b. Did the auditors assess control risk too low Explain your answer.

c. Did the auditors assess inherent risk too low Explain your answer.

d. How should an auditor use materiality to plan the audit work related to revenue

e. Why did the auditors fail to give Xerox a qualified opinion or to ask the company to stop its accelerated revenue recognition program

Financial statement:

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Audit risk:

Audit risk is the risk that the auditor fails to detect the error or fraud in the financial statement of the company. This means that the financial statement contains some errors that the auditor fails to find out in the auditing process.

There are three types of audit risk:

1.

Inherent risk: Inherent risk is the risk or chances of fraud even after auditing. This risk is the most difficult risk to avoid because it can't avoid by increasing the training of the auditor. In the auditing, the auditor selects some samples from the financial statements of the company.

2.

Control risk: Control risk means a risk that occurs due to a lack of control. It is an internal risk that is not deducted under the internal control that results in a misstatement in the financial statement. This is the result of a lack of proper application of accounting practices and proper accounting system.

3.

Detection risk: This is the risk that the auditor fails to detect the fraud or error in the financial statements of the company. This is because of a lack of knowledge and experience.

a.

The audit risk model is a method to assess audit risk. In this, the auditor assesses the audit risk and tries to reduce it to an acceptably low level. It increases the accuracy of the audit report. But in this case, the auditor assesses the audit risk on the condition that "it doesn't want to lose a big client".

b.

No, the auditor does not assess the control risk very low. The company recognized the revenue against the accounting framework. This means that the control risk very high. As a result, the auditor of the company expressed that this method of recording revenue is "not supportable".

c.

Yes, because the company accelerates the revenue of the company on the last day of the year. Because of a lack of time the auditor not able to review it accurately.

d.

In planning the audit, the concept of materiality is very important. It is an acceptable level of misstatement. Every auditor needs to set the level of materiality in the planning phase of the audit. It is very important in planning to make estimates.

e.

The company fails to perform accurately because it doesn't want to lose a big client. This is against the rules of auditing.

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Audit risk:

Audit risk is the risk that the auditor fails to detect the error or fraud in the financial statement of the company. This means that the financial statement contains some errors that the auditor fails to find out in the auditing process.

There are three types of audit risk:

1.

Inherent risk: Inherent risk is the risk or chances of fraud even after auditing. This risk is the most difficult risk to avoid because it can't avoid by increasing the training of the auditor. In the auditing, the auditor selects some samples from the financial statements of the company.

2.

Control risk: Control risk means a risk that occurs due to a lack of control. It is an internal risk that is not deducted under the internal control that results in a misstatement in the financial statement. This is the result of a lack of proper application of accounting practices and proper accounting system.

3.

Detection risk: This is the risk that the auditor fails to detect the fraud or error in the financial statements of the company. This is because of a lack of knowledge and experience.

a.

The audit risk model is a method to assess audit risk. In this, the auditor assesses the audit risk and tries to reduce it to an acceptably low level. It increases the accuracy of the audit report. But in this case, the auditor assesses the audit risk on the condition that "it doesn't want to lose a big client".

b.

No, the auditor does not assess the control risk very low. The company recognized the revenue against the accounting framework. This means that the control risk very high. As a result, the auditor of the company expressed that this method of recording revenue is "not supportable".

c.

Yes, because the company accelerates the revenue of the company on the last day of the year. Because of a lack of time the auditor not able to review it accurately.

d.

In planning the audit, the concept of materiality is very important. It is an acceptable level of misstatement. Every auditor needs to set the level of materiality in the planning phase of the audit. It is very important in planning to make estimates.

e.

The company fails to perform accurately because it doesn't want to lose a big client. This is against the rules of auditing.

3

What is audit risk Explain how the auditor reduces it to an "acceptably low level."

Financial statement:

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Audit risk:

Audit risk is the risk that the auditor fails to detect the error or fraud in the financial statement of the company. This means that the financial statement contains some errors that the auditor fails to find out in the auditing process.

Audit risk is the result of many factors like the complex process of the company, lack of accounting management, Lack of knowledge of the auditor, short period of auditing time.

There are three types of audit risk:

1.

Inherent risk: Inherent risk is the risk or chances of fraud even after auditing. This risk is the most difficult risk to avoid because it can't avoid by increasing the training of the auditor. In the auditing, the auditor selects some samples from the financial statements of the company.

2.

Control risk: Control risk means a risk that occurs due to a lack of control. It is an internal risk that is not deducted under the internal control that results in a misstatement in the financial statement. This is the result of a lack of proper application of accounting practices and proper accounting system.

3.

Detection risk: This is the risk that the auditor fails to detect the fraud or error in the financial statements of the company. This is because of a lack of knowledge and experience.

The auditor is able to reduce the detection risk only because the inherent risk and control risk is not a part of the audit process. He has no control over other risks involved in the auditing process. The auditor can reduce the detection risk to minimize the overall level of risk in the audit.

The financial statement of a company is the record of past year activities. There are many financial statements like cash flow statement, balance sheet, income statement, profit and loss account, etc.

Audit:

The audit is the process of checking the financial statements of a company `to ensure that it is 100% authentic and free from any kind of bias or fraud.

Audit risk:

Audit risk is the risk that the auditor fails to detect the error or fraud in the financial statement of the company. This means that the financial statement contains some errors that the auditor fails to find out in the auditing process.

Audit risk is the result of many factors like the complex process of the company, lack of accounting management, Lack of knowledge of the auditor, short period of auditing time.

There are three types of audit risk:

1.

Inherent risk: Inherent risk is the risk or chances of fraud even after auditing. This risk is the most difficult risk to avoid because it can't avoid by increasing the training of the auditor. In the auditing, the auditor selects some samples from the financial statements of the company.

2.

Control risk: Control risk means a risk that occurs due to a lack of control. It is an internal risk that is not deducted under the internal control that results in a misstatement in the financial statement. This is the result of a lack of proper application of accounting practices and proper accounting system.

3.

Detection risk: This is the risk that the auditor fails to detect the fraud or error in the financial statements of the company. This is because of a lack of knowledge and experience.

The auditor is able to reduce the detection risk only because the inherent risk and control risk is not a part of the audit process. He has no control over other risks involved in the auditing process. The auditor can reduce the detection risk to minimize the overall level of risk in the audit.

4

Parmalat

Parmalat, one of Italy's largest companies, is best known for its shelf stable milk products. The company filed for bankruptcy protection in December 2003 after a ten-year fraud that removed at least $17.4 billion from the company. The fraud was referred to as a Ponzi scheme in which company executives borrowed billions of dollars from investors around the world to cover up the company's losses. As a result of the fraud, U.S. investors suffered one of their largest losses in foreign securities when the debt securities became worthless.

Deloitte Touche SpA, the Italian arm of the international accounting firm Deloitte Touche, was hired as the Parmalat audit firm in 1999. At the end of the audit engagement in 2001, Parmalat's audit committee requested Deloitte to reexamine its audit fee. The Deloitte office in Italy referred to the Parmalat audit as a "crown jewel for our organization worldwide." To keep the prized audit client happy, Deloitte agreed to lower its audit fees. Auditors in Deloitte's office in New Jersey, where the U.S. Parmalat office was located, found their audit fee reduced from $165 per hour rate to about $90 per hour.

Many Deloitte offices were involved in the audit because Parmalat had business operations in at least thirty countries. The Deloitte working papers indicate that auditors outside of Italy frequently gave in to the wishes of the Italian auditor because they feared being fired by such an important client. Deloitte auditors of Bonlat Financing Corporation, located in the Cayman Islands, a unit of Parmalat, expressed concern about the financial transactions recorded in Bonlat. Despite the warnings given by several Deloitte offices involved in the audit, the office in Italy continued to issue clean audit reports. Its Italian office warned auditors in the other Deloitte offices to avoid asking questions regarding the business operations at Bonlat to prevent Parmalat from being annoyed and ending its multimilliondollar audit engagement with Deloitte.

Parmalat officials later acknowledged that they had created Bonlat to hide fraudulent business transactions, referring to it as a "virtual garbage can." Auditors at Deloitte in Italy missed an opportunity to expose one of Europe's largest accounting frauds and to prevent shareholder loss when stock price declined.

a. Describe how the audit risk model might have helped the auditor perform the Parmalat audit.

b. Did the auditor control audit risk to an acceptably low level Explain your answer.

c. What role would the risk of material misstatement have played in the audit decisions Deloitte made

d. Did the auditor fail to ask Parmalat to correct the financial statements because the audit adjustments were quantitatively immaterial Explain your answer.

e. What do you think of the request to keep audit fees low to please a multinational client

f. What do you think of a request to avoid asking the client difficult questions because it might fire the auditor

Parmalat, one of Italy's largest companies, is best known for its shelf stable milk products. The company filed for bankruptcy protection in December 2003 after a ten-year fraud that removed at least $17.4 billion from the company. The fraud was referred to as a Ponzi scheme in which company executives borrowed billions of dollars from investors around the world to cover up the company's losses. As a result of the fraud, U.S. investors suffered one of their largest losses in foreign securities when the debt securities became worthless.

Deloitte Touche SpA, the Italian arm of the international accounting firm Deloitte Touche, was hired as the Parmalat audit firm in 1999. At the end of the audit engagement in 2001, Parmalat's audit committee requested Deloitte to reexamine its audit fee. The Deloitte office in Italy referred to the Parmalat audit as a "crown jewel for our organization worldwide." To keep the prized audit client happy, Deloitte agreed to lower its audit fees. Auditors in Deloitte's office in New Jersey, where the U.S. Parmalat office was located, found their audit fee reduced from $165 per hour rate to about $90 per hour.

Many Deloitte offices were involved in the audit because Parmalat had business operations in at least thirty countries. The Deloitte working papers indicate that auditors outside of Italy frequently gave in to the wishes of the Italian auditor because they feared being fired by such an important client. Deloitte auditors of Bonlat Financing Corporation, located in the Cayman Islands, a unit of Parmalat, expressed concern about the financial transactions recorded in Bonlat. Despite the warnings given by several Deloitte offices involved in the audit, the office in Italy continued to issue clean audit reports. Its Italian office warned auditors in the other Deloitte offices to avoid asking questions regarding the business operations at Bonlat to prevent Parmalat from being annoyed and ending its multimilliondollar audit engagement with Deloitte.

Parmalat officials later acknowledged that they had created Bonlat to hide fraudulent business transactions, referring to it as a "virtual garbage can." Auditors at Deloitte in Italy missed an opportunity to expose one of Europe's largest accounting frauds and to prevent shareholder loss when stock price declined.

a. Describe how the audit risk model might have helped the auditor perform the Parmalat audit.

b. Did the auditor control audit risk to an acceptably low level Explain your answer.

c. What role would the risk of material misstatement have played in the audit decisions Deloitte made

d. Did the auditor fail to ask Parmalat to correct the financial statements because the audit adjustments were quantitatively immaterial Explain your answer.

e. What do you think of the request to keep audit fees low to please a multinational client

f. What do you think of a request to avoid asking the client difficult questions because it might fire the auditor

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

5

During the initial planning phase of an audit, a CPA most likely would a. Identify specific internal control activities that are likely to prevent fraud.

B) Evaluate the reasonableness of the client's accounting estimates.

C) Discuss the timing of the audit procedures with the client's management.

D) Inquire of the client's attorney as to whether any unrecorded claims are probably of assertion.

B) Evaluate the reasonableness of the client's accounting estimates.

C) Discuss the timing of the audit procedures with the client's management.

D) Inquire of the client's attorney as to whether any unrecorded claims are probably of assertion.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

6

BJ Services

BJ Services, a U.S. company, sells products and services to petroleum companies worldwide. BJ Services, S.A., a wholly owned subsidiary of BJ that operates in Argentina, made illegal payments of $72,000 in 2001 to Argentine customs officials so they would allow the company to import equipment. If the payments had not been made, the equipment would not have cleared customs and would have been returned to Venezuela (the source of the shipment). From 1998 to 2002, other improper payments of $151,000 were made to custom agents to facilitate custom clearance of equipment in Argentina. Once an internal investigation discovered the payments, the board of directors ordered a full investigation into potential foreign corrupt practices violations.

The Foreign Corrupt Practices Act makes bribing foreign officials illegal. The investigation found no indication that anyone in management had approved the payments. The SEC issued a cease-and-desist order against the company, which agreed to improve its internal controls to prevent future illegal payments.

a. In 2001, BJ Services had revenue of $2,233,520,000 and total assets of $1,985,367,000. Calculate the company's materiality.

b. Are the illegal payments quantitatively material Explain your answer.

c. Are the illegal payments material for other reasons Explain your answer.

d. What impact would the illegal payments have on your risk assessment for the company

e. What audit procedures would you perform to control the risk arising from the illegal payments

BJ Services, a U.S. company, sells products and services to petroleum companies worldwide. BJ Services, S.A., a wholly owned subsidiary of BJ that operates in Argentina, made illegal payments of $72,000 in 2001 to Argentine customs officials so they would allow the company to import equipment. If the payments had not been made, the equipment would not have cleared customs and would have been returned to Venezuela (the source of the shipment). From 1998 to 2002, other improper payments of $151,000 were made to custom agents to facilitate custom clearance of equipment in Argentina. Once an internal investigation discovered the payments, the board of directors ordered a full investigation into potential foreign corrupt practices violations.

The Foreign Corrupt Practices Act makes bribing foreign officials illegal. The investigation found no indication that anyone in management had approved the payments. The SEC issued a cease-and-desist order against the company, which agreed to improve its internal controls to prevent future illegal payments.

a. In 2001, BJ Services had revenue of $2,233,520,000 and total assets of $1,985,367,000. Calculate the company's materiality.

b. Are the illegal payments quantitatively material Explain your answer.

c. Are the illegal payments material for other reasons Explain your answer.

d. What impact would the illegal payments have on your risk assessment for the company

e. What audit procedures would you perform to control the risk arising from the illegal payments

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

7

When planning an audit, an auditor should a. Consider whether substantive tests may be reduced based on the results of the internal control documentation.

B) Make preliminary judgments about materiality levels for audit purposes.

C) Conclude whether changes in compliance with prescribed controls require a change in the assessed level of control risk.

D) Prepare a preliminary draft of the management representation letter.

B) Make preliminary judgments about materiality levels for audit purposes.

C) Conclude whether changes in compliance with prescribed controls require a change in the assessed level of control risk.

D) Prepare a preliminary draft of the management representation letter.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

8

Select a company that you believe is in a risky business. Review its annual report to determine how it handles risk. Is it mentioned in the opinion or in the footnotes Discuss the auditor's disclosure of risk in the financial statement.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

9

An auditor obtains knowledge about a new client's business and its industry to a. Make constructive suggestions concerning improvements to the client's internal control.

B) Develop an attitude of professional skepticism concerning management's financial statement assertions.

C) Evaluate whether the aggregation of known misstatements causes the financial statements taken as a whole to be materially misstated.

D) Understand the events and transactions that may have an effect on the client's financial statements.

B) Develop an attitude of professional skepticism concerning management's financial statement assertions.

C) Evaluate whether the aggregation of known misstatements causes the financial statements taken as a whole to be materially misstated.

D) Understand the events and transactions that may have an effect on the client's financial statements.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

10

Using a database that contains audit opinions, search for qualified opinions (adverse, disclaimer, except for) and review some of the opinions to determine the factor that risk played in the qualification. Describe several opinions related to risk.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

11

The existence of audit risk is recognized by the statement in the auditor's standard report that the a. Auditor is responsible for expressing an opinion on the financial statements, which are the responsibility of management.

B) Financial statements are presented fairly, in all material respects, in accordance with the financial reporting framework.

C) Audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements.

D) Auditor obtains reasonable assurance about whether the financial statements are free of material misstatement.

B) Financial statements are presented fairly, in all material respects, in accordance with the financial reporting framework.

C) Audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements.

D) Auditor obtains reasonable assurance about whether the financial statements are free of material misstatement.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

12

The risk that an auditor's procedures will lead to the conclusion that a material misstatement does not exist in an account balance or class of transactions when, in fact, such misstatement does exist is a. Audit risk.

B) Inherent risk.

C) Control risk.

D) Detection risk.

B) Inherent risk.

C) Control risk.

D) Detection risk.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

13

Inherent risk and control risk differ from detection risk in that they a. Arise from the misapplication of auditing procedures.

B) May be assessed in either quantitative or nonquantitative terms.

C) Exist independently of the financial statement audit.

D) Can be changed at the auditor's discretion.

B) May be assessed in either quantitative or nonquantitative terms.

C) Exist independently of the financial statement audit.

D) Can be changed at the auditor's discretion.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

14

As the acceptable level of detection risk decreases, an auditor may a. Reduce substantive testing by relying on the assessments of inherent risk and control risk.

B) Postpone the planned timing of substantive tests from interim dates to the year-end.

C) Eliminate the assessed level of inherent risk from consideration as a planning factor.

D) Lower the assessed level of control risk from the maximum level to below the maximum.

B) Postpone the planned timing of substantive tests from interim dates to the year-end.

C) Eliminate the assessed level of inherent risk from consideration as a planning factor.

D) Lower the assessed level of control risk from the maximum level to below the maximum.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

15

What is the purpose of an audit

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

16

As the acceptable level of detection risk decreases, an auditor may change the a. Timing of substantive tests by performing them at an interim date rather than at year-end.

B) Nature of substantive tests from a less effective to a more effective procedure.

C) Timing of tests of controls by performing them at several dates rather than at one time.

D) Assessed level of inherent risk to a higher amount.

B) Nature of substantive tests from a less effective to a more effective procedure.

C) Timing of tests of controls by performing them at several dates rather than at one time.

D) Assessed level of inherent risk to a higher amount.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

17

Describe the phases in the audit process including the steps in each phase.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following audit risk components may be assessed in nonquantitative terms

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

19

What is the purpose of the engagement letter How does it benefit both the auditor and the client's management

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

20

Using the audit risk model to plan the audit. You are in charge of planning the audit for BCS, Inc., and will use the audit risk model to plan the internal control testing and the substantive testing for the client.

a. If inherent risk is assessed at 0.5 for the purchase cycle and internal control risk is assessed at 0.3, what is detection risk Assume that audit risk = 0.05.

b. What evidence would you gather to support the assessment of inherent risk and control risk

c. Assume that you determine that control risk is 0.5 instead of 0.3 after your internal control testing.

(1) Calculate the new detection risk.

(2) In this situation, will you perform more or less substantive test work than when the control risk was assessed at 0.3 Explain your answer using the audit risk model.

(3) In general, will you perform more or less internal control test work when control risk is 0.3 than when control risk is 0.50

d. If you decrease control risk from 0.7 to 0.5, will you do more or less internal control testing More or less substantive testing Explain your answer using the audit risk model.

e. Does the auditor control inherent risk, control risk, detection risk, or audit risk Explain your answer.

f. What is audit risk Does it differ from one client to another client Explain your answer.

g. How does the auditor control audit risk Explain why it is important to keep audit risk to an acceptably low level What is an acceptably low level

a. If inherent risk is assessed at 0.5 for the purchase cycle and internal control risk is assessed at 0.3, what is detection risk Assume that audit risk = 0.05.

b. What evidence would you gather to support the assessment of inherent risk and control risk

c. Assume that you determine that control risk is 0.5 instead of 0.3 after your internal control testing.

(1) Calculate the new detection risk.

(2) In this situation, will you perform more or less substantive test work than when the control risk was assessed at 0.3 Explain your answer using the audit risk model.

(3) In general, will you perform more or less internal control test work when control risk is 0.3 than when control risk is 0.50

d. If you decrease control risk from 0.7 to 0.5, will you do more or less internal control testing More or less substantive testing Explain your answer using the audit risk model.

e. Does the auditor control inherent risk, control risk, detection risk, or audit risk Explain your answer.

f. What is audit risk Does it differ from one client to another client Explain your answer.

g. How does the auditor control audit risk Explain why it is important to keep audit risk to an acceptably low level What is an acceptably low level

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

21

Describe the quality control measures the audit firm uses to ensure that the audit process corresponds to professional standards.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

22

Materiality and audit opinions. Describe how materiality is used in (1) planning and performing the audit and (2) evaluating evidence gathered during the audit process.

a. Provide an example describing how materiality might be used in planning and performing the audit.

b. Provide an example describing how materiality might be used in evaluating the results of test work in the audit of the revenue business process.

c. Should an auditor issue an unqualified opinion if the evidence gathered during the audit indicates that the dollar amount of misstatement in the financial statements is material Explain your answer. What should the auditor do in this situation

d. Can an auditor issue an unqualified opinion gathering only internal control evidence for some business processes Explain your answer.

e. Can an auditor issue an unqualified opinion after gathering only substantive evidence for some business processes Explain your answer.

f. Can an auditor issue an unqualified opinion based on a combination of internal control and substantive testing How does the auditor combine the results from internal control testing and substantive testing to keep audit risk to an acceptably low level

a. Provide an example describing how materiality might be used in planning and performing the audit.

b. Provide an example describing how materiality might be used in evaluating the results of test work in the audit of the revenue business process.

c. Should an auditor issue an unqualified opinion if the evidence gathered during the audit indicates that the dollar amount of misstatement in the financial statements is material Explain your answer. What should the auditor do in this situation

d. Can an auditor issue an unqualified opinion gathering only internal control evidence for some business processes Explain your answer.

e. Can an auditor issue an unqualified opinion after gathering only substantive evidence for some business processes Explain your answer.

f. Can an auditor issue an unqualified opinion based on a combination of internal control and substantive testing How does the auditor combine the results from internal control testing and substantive testing to keep audit risk to an acceptably low level

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

23

How does the auditor gain an understanding of the audit client and its environment

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

24

Calculating materiality. Dell Computers reported total revenue of $49,205,000,000 and total assets of $23,215,000,000 in 2005.

a. Calculate materiality for the company using the worksheet in this chapter.

b. How will the auditor use this materiality level in planning the audit

c. Describe how the materiality level might be used in evaluating audit evidence.

d. How does the materiality level impact the audit opinion

a. Calculate materiality for the company using the worksheet in this chapter.

b. How will the auditor use this materiality level in planning the audit

c. Describe how the materiality level might be used in evaluating audit evidence.

d. How does the materiality level impact the audit opinion

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

25

The auditing standards require the auditor to determine materiality. How does the auditor do this

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

26

Using the audit process to plan and perform the audit. You are in charge of planning the audit for a large bookstore selling CDs, DVDs, and books. Follow the steps discussed in the chapter. Assume that you have agreed to perform the audit and an engagement letter has been signed. The client has a December 31 year-end.

You are planning the audit in September. The company expects revenue to be $1,675,000,000 and total assets to be $1,235,000,000 at year-end. Use these numbers to calculate materiality.

a. Describe an audit strategy appropriate for planning the audit.

b. Calculate the bookstore's materiality. Describe how you will use it in the audit.

c. Identify significant accounts and relevant assertions for them. How will you assess inherent risk and control risk for the significant accounts Assume that the bookstore leases its retail site and has no long-term debt.

d. Describe at least two analytical procedures you would perform during the planning process. What will you do with the results

e. Assume that control risk for inventory has been assessed at 0.50. How will you support this assessment What will happen if the results of the tests do not support an assessment of control risk at 0.50

f. What impact does the control testing have on substantive testing

g. Assume that during substantive testing, you found misstatements in net income equal to $2,837,000. What decision would you make regarding the financial statements What action would you take

h. Describe how you would determine the appropriate audit opinion for the client.

You are planning the audit in September. The company expects revenue to be $1,675,000,000 and total assets to be $1,235,000,000 at year-end. Use these numbers to calculate materiality.

a. Describe an audit strategy appropriate for planning the audit.

b. Calculate the bookstore's materiality. Describe how you will use it in the audit.

c. Identify significant accounts and relevant assertions for them. How will you assess inherent risk and control risk for the significant accounts Assume that the bookstore leases its retail site and has no long-term debt.

d. Describe at least two analytical procedures you would perform during the planning process. What will you do with the results

e. Assume that control risk for inventory has been assessed at 0.50. How will you support this assessment What will happen if the results of the tests do not support an assessment of control risk at 0.50

f. What impact does the control testing have on substantive testing

g. Assume that during substantive testing, you found misstatements in net income equal to $2,837,000. What decision would you make regarding the financial statements What action would you take

h. Describe how you would determine the appropriate audit opinion for the client.

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

27

What is the risk of material misstatement in the financial statements How should the auditor respond to this risk

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

28

Identifying significant accounts and calculating materiality. Anaheim Enterprises, which operates in California, sells patio furniture imported from China; the merchandise is marketable twelve months of the year in California. Shipments from China come by sea and take two months to arrive unless a strike idles the shipping ports. The firm does not have a retail store but rents warehouse space with a small office. Anaheim sells on the Internet and through phone orders from customers and retail shops. The firm stocks fifty different sets of tables and chairs and a variety of benches, lounge chairs, and table umbrellas. It places all orders four months before delivery, and its payment is expected when it places the order.

Anaheim accepts credit cards and extends thirty days of credit to retail stores. Its balance sheet shows cash, accounts receivable, inventory, and office equipment. On the liability side of the balance sheet are a few accounts payable and a shortterm bank loan to cover the payment for goods before they arrive. The income statement shows revenue from both Internet and phone sales, cost of goods sold (averaging about 60% of revenue), and a few operating expenses (mainly rent and utilities). At any one time, the firm has on hand a three-month supply of inventory, which turns over about four times a year. The inventory does not tend to become obsolete. Anaheim is not a public company, but its books are audited to allow it to obtain bank financing. The company's two owners have no employees. The firm's total revenue is $2,800,000 for the current year; it had total assets of $700,000 at year-end. You are working on the year-end audit.

a. Calculate the company's materiality, and describe how you used it in the audit.

b. Identify significant accounts and disclosures for the company as well as any relevant assertions associated with the significant accounts. Explain how you determined the significant accounts and disclosures.

c. Did you test internal controls at this company Explain your answer.

d. How did you gather evidence regarding the significant accounts and disclosures

e. Assume that during substantive testing, you found misstatements in net income equal to $32,206. What decision would you make regarding the financial statements What action would you take

Anaheim accepts credit cards and extends thirty days of credit to retail stores. Its balance sheet shows cash, accounts receivable, inventory, and office equipment. On the liability side of the balance sheet are a few accounts payable and a shortterm bank loan to cover the payment for goods before they arrive. The income statement shows revenue from both Internet and phone sales, cost of goods sold (averaging about 60% of revenue), and a few operating expenses (mainly rent and utilities). At any one time, the firm has on hand a three-month supply of inventory, which turns over about four times a year. The inventory does not tend to become obsolete. Anaheim is not a public company, but its books are audited to allow it to obtain bank financing. The company's two owners have no employees. The firm's total revenue is $2,800,000 for the current year; it had total assets of $700,000 at year-end. You are working on the year-end audit.

a. Calculate the company's materiality, and describe how you used it in the audit.

b. Identify significant accounts and disclosures for the company as well as any relevant assertions associated with the significant accounts. Explain how you determined the significant accounts and disclosures.

c. Did you test internal controls at this company Explain your answer.

d. How did you gather evidence regarding the significant accounts and disclosures

e. Assume that during substantive testing, you found misstatements in net income equal to $32,206. What decision would you make regarding the financial statements What action would you take

Unlock Deck

Unlock for access to all 28 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 28 flashcards in this deck.