Deck 15: Statement of Cash Flows

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

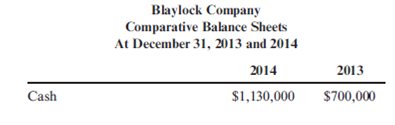

Change in Cash

Blaylock Company provided the following information:

Blaylock Company provided the following information:

Question

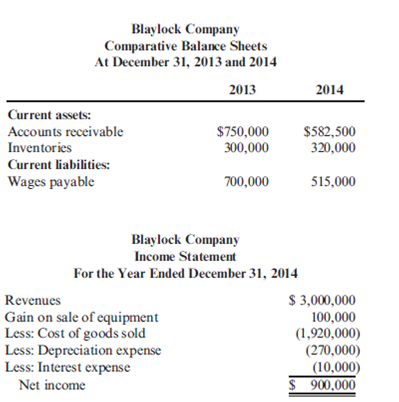

Operating Cash Flows: Indirect Method

Blaylock Company provided the following partial comparative balance sheets and the income statement for 2014.

Blaylock Company provided the following partial comparative balance sheets and the income statement for 2014.

Question

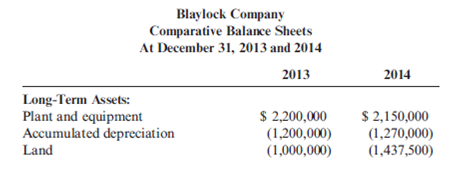

Flows from Investing Activities

During the year, Blaylock Company sold equipment with a book value of $280,000 for $380,000 (original purchase cost of $480,000). New equipment was purchased.

Blaylock provided the following comparative balance sheets:

During the year, Blaylock Company sold equipment with a book value of $280,000 for $380,000 (original purchase cost of $480,000). New equipment was purchased.

Blaylock provided the following comparative balance sheets:

Question

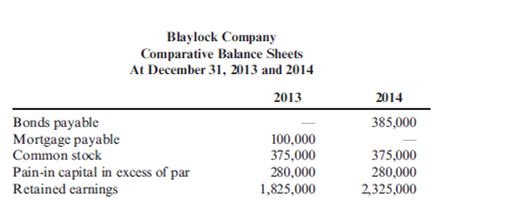

Flows from Financing Activities

Blaylock Company earned net income of $900,000 in 2014. Blaylock provided the following information:

Blaylock Company earned net income of $900,000 in 2014. Blaylock provided the following information:

Question

Question

Operating Cash Flows: Direct Method

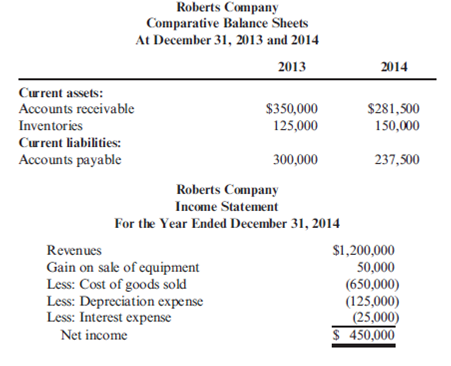

Roberts Company has provided the following partial comparative balance sheets and the income statement for 2014.

Roberts Company has provided the following partial comparative balance sheets and the income statement for 2014.

Question

Worksheet Approach

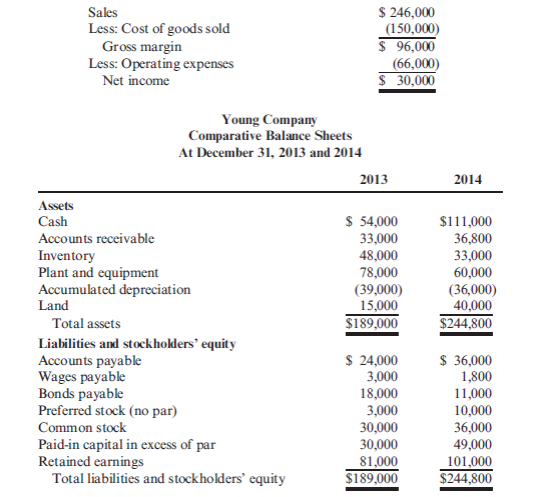

During 2014, Young Company had the following transactions:

a. Cash dividends of $10,000 were paid.

b. Equipment was sold for $4,800. It had an original cost of $18,000 and a book value of $9,000. The loss is included in operating expenses.

c. Land with a fair market value of $25,000 was acquired by issuing common stock with a par value of $6,000.

d. One thousand shares of preferred stock (no par) were sold for $7 per share.

Young provided the following income statement (for 2012) and comparative balance sheets:

During 2014, Young Company had the following transactions:

a. Cash dividends of $10,000 were paid.

b. Equipment was sold for $4,800. It had an original cost of $18,000 and a book value of $9,000. The loss is included in operating expenses.

c. Land with a fair market value of $25,000 was acquired by issuing common stock with a par value of $6,000.

d. One thousand shares of preferred stock (no par) were sold for $7 per share.

Young provided the following income statement (for 2012) and comparative balance sheets:

Question

Question

Question

Question

Operating Cash Flows

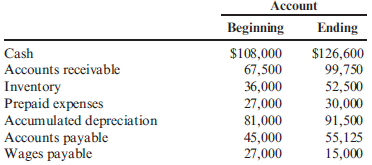

During the year, Hepworth Company earned a net income of $61,725. Beginning and ending balances for the year for selected accounts are as follows:

There were no financing or investing activities for the year. The above balances reflect all of the adjustments needed to adjust net income to operating cash flows.

During the year, Hepworth Company earned a net income of $61,725. Beginning and ending balances for the year for selected accounts are as follows:

There were no financing or investing activities for the year. The above balances reflect all of the adjustments needed to adjust net income to operating cash flows.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Statement of Cash Flows: Indirect Method

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Question

Statement of Cash Flows, Worksheet

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Question

Schedule of Operating Cash Flows: Indirect Method

The income statement for the Mendelin Corporation is as follows:

Additional information is as follows:

a. Interest expense includes $1,800 of discount amortization.

b. The prepaid insurance expense account decreased by $2,000 during the year.

c. Wages payable decreased by $3,000 during the year.

d. Accounts payable increased by $7,500 (this account is for purchase of merchandise only).

e. Accounts receivable increased by $10,000 (net of allowance for doubtful accounts).

f. Inventory decreased by $16,000.

The income statement for the Mendelin Corporation is as follows:

Additional information is as follows:

a. Interest expense includes $1,800 of discount amortization.

b. The prepaid insurance expense account decreased by $2,000 during the year.

c. Wages payable decreased by $3,000 during the year.

d. Accounts payable increased by $7,500 (this account is for purchase of merchandise only).

e. Accounts receivable increased by $10,000 (net of allowance for doubtful accounts).

f. Inventory decreased by $16,000.

Question

Statement of Cash Flows, Indirect Method

The following balance sheets are taken from the records of Golding Company (numbers are expressed in thousands):

Additional information is as follows: (a) Equipment costing $10,000,000 was purchased at yearend. No equipment was sold; and (b) Net income for the year was $25,000,000; $10,000,000 in dividends were paid.

The following balance sheets are taken from the records of Golding Company (numbers are expressed in thousands):

Additional information is as follows: (a) Equipment costing $10,000,000 was purchased at yearend. No equipment was sold; and (b) Net income for the year was $25,000,000; $10,000,000 in dividends were paid.

Question

Question

Question

Direct and Indirect Methods

The comparative balance sheets and income statement of Piura Manufacturing follow.

Additional transactions for 2014 were as follows:

a. Cash dividends of $8,000 were paid.

b. Equipment was acquired by issuing common stock with a par value of $6,000. The fair market value of the equipment is $32,000.

c. Equipment with a book value of $12,000 was sold for $6,000. The original cost of the equipment was $24,000. The loss is included in operating expenses.

d. Two thousand shares of preferred stock were sold for $4 per share.

The comparative balance sheets and income statement of Piura Manufacturing follow.

Additional transactions for 2014 were as follows:

a. Cash dividends of $8,000 were paid.

b. Equipment was acquired by issuing common stock with a par value of $6,000. The fair market value of the equipment is $32,000.

c. Equipment with a book value of $12,000 was sold for $6,000. The original cost of the equipment was $24,000. The loss is included in operating expenses.

d. Two thousand shares of preferred stock were sold for $4 per share.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/63

Play

Full screen (f)

Deck 15: Statement of Cash Flows

1

are cash equivalents? How are cash equivalents treated in preparing a statement of cash flows?

Cash Equivalents:

Cash equivalents are short term, highly liquid investments that are readily convertible into known cash and which are subject to an insignificant risk of change in value. Examples of cash equivalents are Treasury bills, money market funds, and commercial paper.

Treatment of Cash equivalents in preparing a statement of cash flows:

Cash equivalents are treated as cash for the purpose of preparing statement of cash flows. Cash equivalents are to be added to the cash for getting the total cash.

Cash equivalents are short term, highly liquid investments that are readily convertible into known cash and which are subject to an insignificant risk of change in value. Examples of cash equivalents are Treasury bills, money market funds, and commercial paper.

Treatment of Cash equivalents in preparing a statement of cash flows:

Cash equivalents are treated as cash for the purpose of preparing statement of cash flows. Cash equivalents are to be added to the cash for getting the total cash.

2

inflows from operating activities come from

A) payment for raw materials.

B) gains on the sale of operating equipment.

C) collection of sales revenues.

D) issuing capital stock.

E) issuing bonds.

A) payment for raw materials.

B) gains on the sale of operating equipment.

C) collection of sales revenues.

D) issuing capital stock.

E) issuing bonds.

The correct answer is (c) collection of sales revenue.

Because, sales revenue is an operating activity and it is also an inflow.

The other choices are not correct and are not relevant because,

(a) Payment for raw materials is although an operating activity but it involves cash out flow but not inflow.

(b) Gain on sale of operating equipment is not an operating activity but it is an investing activity.

(d) Issuing capital stock is a financing activity though it involves a cash inflow.

(e) Issuing bonds is a financing activity though it involves a cash inflow.

Thus the correct option is (c)

Because, sales revenue is an operating activity and it is also an inflow.

The other choices are not correct and are not relevant because,

(a) Payment for raw materials is although an operating activity but it involves cash out flow but not inflow.

(b) Gain on sale of operating equipment is not an operating activity but it is an investing activity.

(d) Issuing capital stock is a financing activity though it involves a cash inflow.

(e) Issuing bonds is a financing activity though it involves a cash inflow.

Thus the correct option is (c)

3

activity format calls for three categories on the statement of cash flows. Define each category.

The statement of cash flows should report the following three categories of activities during the period.

• Operating Activities

• Investing Activities

• Financing Activities

Operating Activities:

Operating Activities are the principal revenue-producing activities of the enterprise and other activities are not investing and financing activities. Operating activities may increase or decrease the current assets or current liabilities. Examples of cash flows from operating activities are:

a. Cash receipts from the sale of goods and the rendering of services

b. Cash receipts from royalties, fees, commissions, and other revenue

c. Cash payments to suppliers for goods and services

d. Cash payments to and on behalf of employees

Investing Activities:

Investing activities include transactions and events that include the purchase and sale of long term productive assets and not held for resale and other investments. Examples of cash flows arising from investing activities are:

a. Cash payments to acquire fixed assets

b. Cash receipts from disposal of fixed assets

c. Cash payments to acquire shares, warrants etc.

Financing Activities:

Financing Activities are activities that result changes in the size and composition of owners capital and borrowing of the enterprise. Examples of cash flows arising from financing activities are:

a. Cash proceeds from issuing shares or other similar instruments

b. Cash proceeds from issuing debentures, loans, notes etc.

c. Cash repayments of amounts borrowed.

• Operating Activities

• Investing Activities

• Financing Activities

Operating Activities:

Operating Activities are the principal revenue-producing activities of the enterprise and other activities are not investing and financing activities. Operating activities may increase or decrease the current assets or current liabilities. Examples of cash flows from operating activities are:

a. Cash receipts from the sale of goods and the rendering of services

b. Cash receipts from royalties, fees, commissions, and other revenue

c. Cash payments to suppliers for goods and services

d. Cash payments to and on behalf of employees

Investing Activities:

Investing activities include transactions and events that include the purchase and sale of long term productive assets and not held for resale and other investments. Examples of cash flows arising from investing activities are:

a. Cash payments to acquire fixed assets

b. Cash receipts from disposal of fixed assets

c. Cash payments to acquire shares, warrants etc.

Financing Activities:

Financing Activities are activities that result changes in the size and composition of owners capital and borrowing of the enterprise. Examples of cash flows arising from financing activities are:

a. Cash proceeds from issuing shares or other similar instruments

b. Cash proceeds from issuing debentures, loans, notes etc.

c. Cash repayments of amounts borrowed.

4

outflows from operating activities come from

A) collection of sales revenues.

B) payment for operating costs.

C) acquisition of operating equipment.

D) retirement of bonds.

E) none of these.

A) collection of sales revenues.

B) payment for operating costs.

C) acquisition of operating equipment.

D) retirement of bonds.

E) none of these.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

5

the three categories on the statement of cash flows, which do you think provides the most useful information? Explain.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

6

Raising cash by issuing capital stock is an example of

A) a financing activity.

B) an investing activity.

C) an operating activity.

D) a noncash transaction.

E) none of these.

A) a financing activity.

B) an investing activity.

C) an operating activity.

D) a noncash transaction.

E) none of these.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

7

Explain the all-financial-resources approach to reporting financing and investing activities.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

8

Sources of cash include

A) profitable operations.

B) the issuance of long-term debt.

C) the sale of long-term assets.

D) the issuance of capital stock.

E) all of these.

A) profitable operations.

B) the issuance of long-term debt.

C) the sale of long-term assets.

D) the issuance of capital stock.

E) all of these.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

9

is it better to report the noncash investing and financing activities in a supplemental schedule rather than to include these activities on the body of the statement of cash flows?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

10

of cash include

A) cash dividends.

B) the sale of old equipment.

C) the purchase of long-term assets.

D) only a and b.

E) only a and c.

A) cash dividends.

B) the sale of old equipment.

C) the purchase of long-term assets.

D) only a and b.

E) only a and c.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

11

are the five steps for preparing the statement of cash flows? What is the purpose of each step?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

12

difference between the beginning and ending cash balances shown on the balance sheet

A) is added to net income to obtain total cash inflows.

B) serves as a control figure for the statement of cash flows.

C) is deducted from net income to obtain net cash inflows.

D) is the source of all investing and financing activities.

E) is both c and d.

A) is added to net income to obtain total cash inflows.

B) serves as a control figure for the statement of cash flows.

C) is deducted from net income to obtain net cash inflows.

D) is the source of all investing and financing activities.

E) is both c and d.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

13

Explain how a company can report a positive net income and yet still have a negative net operating cash flow.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following adjustments helps to convert accrual income to operating cash flows?

A) Deduct from net income all noncash expenses.

B) Add to net income a decrease in inventories.

C) Add to net income a decrease in accounts payable.

D) Deduct from net income an increase in accounts payable.

E) None of the above.

A) Deduct from net income all noncash expenses.

B) Add to net income a decrease in inventories.

C) Add to net income a decrease in accounts payable.

D) Deduct from net income an increase in accounts payable.

E) None of the above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

15

Explain how a company can report a loss and still have a positive net operating cash flow.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following adjustments to net income is needed to obtain cash flows?

A) Eliminate gains on sale of equipment.

B) Deduct from net income all noncash expenses (e.g., depreciation and amortization).

C) Deduct from net income any increases in current liabilities.

D) Add to net income any increases in inventories.

E) All of the above.

A) Eliminate gains on sale of equipment.

B) Deduct from net income all noncash expenses (e.g., depreciation and amortization).

C) Deduct from net income any increases in current liabilities.

D) Add to net income any increases in inventories.

E) All of the above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

17

computing the period's net operating cash flows, why are increases in current liabilities and decreases in current assets added back to net income?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

18

increase in accounts receivable is deducted from net income to obtain operating cash flows because

A) cash collections increased due to increasing sales.

B) cash collections from customers were less than the revenues reported.

C) cash collections decreased due to declining sales.

D) cash collections from customers were greater than the revenues reported.

E) None of the above.

A) cash collections increased due to increasing sales.

B) cash collections from customers were less than the revenues reported.

C) cash collections decreased due to declining sales.

D) cash collections from customers were greater than the revenues reported.

E) None of the above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

19

computing the period's net operating cash flows, why are decreases in liabilities and increases in current assets deducted from net income?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

20

increase in inventories is deducted from net income to arrive at operating cash flow because

A) cash payments to customers were larger than the purchases made during the period.

B) purchases are larger than the cost of goods sold by the amount that inventories increased.

C) cash payments to customers were less than the purchases made during the period.

D) purchases are less than the cost of goods sold by the amount that inventories increased.

E) All of the above.

A) cash payments to customers were larger than the purchases made during the period.

B) purchases are larger than the cost of goods sold by the amount that inventories increased.

C) cash payments to customers were less than the purchases made during the period.

D) purchases are less than the cost of goods sold by the amount that inventories increased.

E) All of the above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

21

computing the period's net operating cash flows, why are noncash expenses added back to net income?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

22

gain on sale of equipment is deducted from net income to arrive at operating cash flows because

A) the sale of long-term assets is an operating activity.

B) the gain reveals the total cash received.

C) all of the cash received from the sale is reported in the operating section.

D) All of the above.

E) None of the above.

A) the sale of long-term assets is an operating activity.

B) the gain reveals the total cash received.

C) all of the cash received from the sale is reported in the operating section.

D) All of the above.

E) None of the above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

23

Explain the reasoning for including the payment of dividends in the financing section of the statement of cash flows.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is an investing activity?

A) Issuance of a mortgage

B) Increase in accounts receivable

C) Purchase of land

D) Increase in inventories

E) All of these.

A) Issuance of a mortgage

B) Increase in accounts receivable

C) Purchase of land

D) Increase in inventories

E) All of these.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

25

are the advantages in using worksheets when preparing a statement of cash flows?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is a financing activity?

A) Increase in inventories

B) Purchase of land

C) Increase in accounts receivable

D) Issuance of a mortgage

E) All of these.

A) Increase in inventories

B) Purchase of land

C) Increase in accounts receivable

D) Issuance of a mortgage

E) All of these.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

27

Explain how the statement of cash flows can be prepared using the worksheet approach.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

28

Which method calculates operating cash flows by adjusting the income statement on a line-by-line basis?

A) Direct method

B) Indirect method

C) Working paper approach

D) Income method

E) None of these.

A) Direct method

B) Indirect method

C) Working paper approach

D) Income method

E) None of these.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

29

worksheet approach to preparing the statement of cash flows

A) is a useful aid.

B) uses a spreadsheet format.

C) offers an efficient and logical way of organizing the data.

D) allows an easy extraction of the needed data.

E) All of these.

A) is a useful aid.

B) uses a spreadsheet format.

C) offers an efficient and logical way of organizing the data.

D) allows an easy extraction of the needed data.

E) All of these.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

30

a completed worksheet,

A) the debit column contains the cash inflows.

B) the debit column contains the cash outflows.

C) the credit column contains the cash inflows.

D) the credit column contains only operating cash flows.

E) None of the above.

A) the debit column contains the cash inflows.

B) the debit column contains the cash outflows.

C) the credit column contains the cash inflows.

D) the credit column contains only operating cash flows.

E) None of the above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

31

Activity Classification

During the last 2 years of operations, Barnes Company had the following transactions:

a. Purchased a new plant for $5,000,000.

b. Issued bonds with a 6-year maturity date for $2,000,000.

c. Reported profits of $7,000,000 for the most recent year.

d. Sold equipment for $500,000.

e. Paid cash dividends of $2,000,000.

f. Sold a 30% interest in a company.

g. Retired a long-term note payable.

h. Reported a loss for the year ($500,000).

i. Issued common stock for $1,000,000.

During the last 2 years of operations, Barnes Company had the following transactions:

a. Purchased a new plant for $5,000,000.

b. Issued bonds with a 6-year maturity date for $2,000,000.

c. Reported profits of $7,000,000 for the most recent year.

d. Sold equipment for $500,000.

e. Paid cash dividends of $2,000,000.

f. Sold a 30% interest in a company.

g. Retired a long-term note payable.

h. Reported a loss for the year ($500,000).

i. Issued common stock for $1,000,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

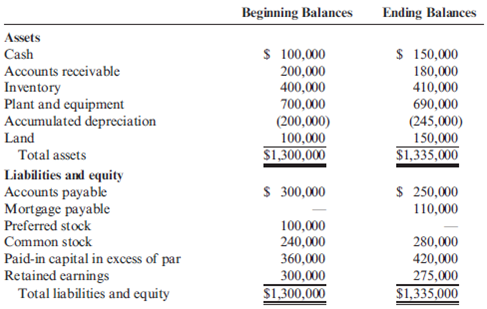

32

Change in Cash

Blaylock Company provided the following information:

Blaylock Company provided the following information:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

33

Operating Cash Flows: Indirect Method

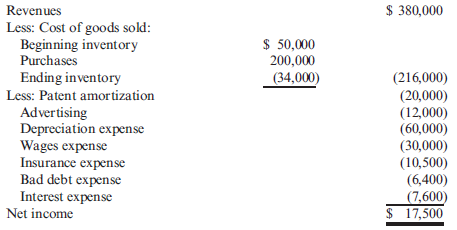

Blaylock Company provided the following partial comparative balance sheets and the income statement for 2014.

Blaylock Company provided the following partial comparative balance sheets and the income statement for 2014.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

34

Flows from Investing Activities

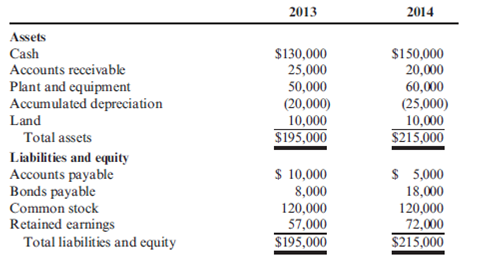

During the year, Blaylock Company sold equipment with a book value of $280,000 for $380,000 (original purchase cost of $480,000). New equipment was purchased.

Blaylock provided the following comparative balance sheets:

During the year, Blaylock Company sold equipment with a book value of $280,000 for $380,000 (original purchase cost of $480,000). New equipment was purchased.

Blaylock provided the following comparative balance sheets:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

35

Flows from Financing Activities

Blaylock Company earned net income of $900,000 in 2014. Blaylock provided the following information:

Blaylock Company earned net income of $900,000 in 2014. Blaylock provided the following information:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

36

Statement of Cash Flows

Refer to the information provided in Cornerstone Exercises 15-19, 15-20, and 15-21.

Required :

1. Prepare a statement of cash flows for Blaylock for 2014.

2. What is the relationship between the statement of cash flows and the change in cash calculated in Cornerstone Exercise 15-18?

Refer to the information provided in Cornerstone Exercises 15-19, 15-20, and 15-21.

Required :

1. Prepare a statement of cash flows for Blaylock for 2014.

2. What is the relationship between the statement of cash flows and the change in cash calculated in Cornerstone Exercise 15-18?

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

37

Operating Cash Flows: Direct Method

Roberts Company has provided the following partial comparative balance sheets and the income statement for 2014.

Roberts Company has provided the following partial comparative balance sheets and the income statement for 2014.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

38

Worksheet Approach

During 2014, Young Company had the following transactions:

a. Cash dividends of $10,000 were paid.

b. Equipment was sold for $4,800. It had an original cost of $18,000 and a book value of $9,000. The loss is included in operating expenses.

c. Land with a fair market value of $25,000 was acquired by issuing common stock with a par value of $6,000.

d. One thousand shares of preferred stock (no par) were sold for $7 per share.

Young provided the following income statement (for 2012) and comparative balance sheets:

During 2014, Young Company had the following transactions:

a. Cash dividends of $10,000 were paid.

b. Equipment was sold for $4,800. It had an original cost of $18,000 and a book value of $9,000. The loss is included in operating expenses.

c. Land with a fair market value of $25,000 was acquired by issuing common stock with a par value of $6,000.

d. One thousand shares of preferred stock (no par) were sold for $7 per share.

Young provided the following income statement (for 2012) and comparative balance sheets:

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

39

Activity Classification

Stillwater Designs is a private company and outsources production of its Kicker speaker lines. Suppose that Stillwater Designs provided you the following transactions.

a. Sold a warehouse for $750,000.

b. Reported a profit of $100,000.

c. Retired long-term bonds.

d. Paid cash dividends of $350,000.

e. Obtained a mortgage for a new building from a local bank.

f. Purchased a new robotic system.

g. Issued a long-term note payable.

h. Purchased a 40% interest in a company.

i. Reported a loss for the year.

j. Negotiated a long-term loan.

Stillwater Designs is a private company and outsources production of its Kicker speaker lines. Suppose that Stillwater Designs provided you the following transactions.

a. Sold a warehouse for $750,000.

b. Reported a profit of $100,000.

c. Retired long-term bonds.

d. Paid cash dividends of $350,000.

e. Obtained a mortgage for a new building from a local bank.

f. Purchased a new robotic system.

g. Issued a long-term note payable.

h. Purchased a 40% interest in a company.

i. Reported a loss for the year.

j. Negotiated a long-term loan.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

40

Adjustments to Net Income

Consider the following independent events:

a. Loss on sale of an asset

b. Decrease in accounts receivable

c. Increase in prepaid insurance

d. Depreciation expense

e. Decrease in accounts payable

f. Uncollectible accounts expense

g. Increase in wages payable

h. Decrease in inventory

i. Amortization of an intangible asset

Consider the following independent events:

a. Loss on sale of an asset

b. Decrease in accounts receivable

c. Increase in prepaid insurance

d. Depreciation expense

e. Decrease in accounts payable

f. Uncollectible accounts expense

g. Increase in wages payable

h. Decrease in inventory

i. Amortization of an intangible asset

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

41

Adjustment for Prepaid Rent

Jarem Company showed $189,000 in prepaid rent on December 31, 2013. On December 31, 2014, the balance in the prepaid rent account was $226,800. Rent expense for 2014 was $472,500.

Jarem Company showed $189,000 in prepaid rent on December 31, 2013. On December 31, 2014, the balance in the prepaid rent account was $226,800. Rent expense for 2014 was $472,500.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

42

Operating Cash Flows

During the year, Hepworth Company earned a net income of $61,725. Beginning and ending balances for the year for selected accounts are as follows:

There were no financing or investing activities for the year. The above balances reflect all of the adjustments needed to adjust net income to operating cash flows.

During the year, Hepworth Company earned a net income of $61,725. Beginning and ending balances for the year for selected accounts are as follows:

There were no financing or investing activities for the year. The above balances reflect all of the adjustments needed to adjust net income to operating cash flows.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

43

Flow from Investing Activities

During 2013, Shorts Company had the following transactions:

a. Purchased $200,000 of 10-year bonds issued by Makenzie Inc.

b. Acquired land valued at $70,000 in exchange for machinery.

c. Sold equipment with original cost of $540,000 for $330,000; accumulated depreciation taken on the equipment to the point of sale was $180,000.

d. Purchased new machinery for $120,000.

e. Purchased common stock in Lemmons Company for $55,000.

During 2013, Shorts Company had the following transactions:

a. Purchased $200,000 of 10-year bonds issued by Makenzie Inc.

b. Acquired land valued at $70,000 in exchange for machinery.

c. Sold equipment with original cost of $540,000 for $330,000; accumulated depreciation taken on the equipment to the point of sale was $180,000.

d. Purchased new machinery for $120,000.

e. Purchased common stock in Lemmons Company for $55,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

44

Flow from Financing Activities

Tidwell Company experienced the following during 2013:

a. Sold preferred stock for $480,000.

b. Declared dividends of $150,000 payable on March 1, 2014.

c. Borrowed $575,000 from bank on a 2-year note.

d. Purchased $80,000 of its own common stock to hold as treasury stock.

e. Repaid 5-year bonds issued in 2008 for $400,000 due in December.

Tidwell Company experienced the following during 2013:

a. Sold preferred stock for $480,000.

b. Declared dividends of $150,000 payable on March 1, 2014.

c. Borrowed $575,000 from bank on a 2-year note.

d. Purchased $80,000 of its own common stock to hold as treasury stock.

e. Repaid 5-year bonds issued in 2008 for $400,000 due in December.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

45

Operating Cash Flows

Refer to the information for Oliver Company on the previous page.

Refer to the information for Oliver Company on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

46

Operating Cash Flows

Refer to the information for Oliver Company on the previous page.

Refer to the information for Oliver Company on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

47

Classification of Transactions

Consider the following independent activities.

a. Payment of a cash dividend

b. Amortization of intangible asset

c. Gain on disposal of equipment

d. Exchange of common stock for land

e. Increase in accrued wages

f. Retirement of preferred stock

g. Purchase of a new plant

h. Depreciation expense

i. Decrease in accounts payable

j. Increase in accounts receivable

k. Proceeds from the sale of land

l. Increase in prepaid expenses

m. Retirement of a bond

n. Purchase of a 60% interest in another company

Consider the following independent activities.

a. Payment of a cash dividend

b. Amortization of intangible asset

c. Gain on disposal of equipment

d. Exchange of common stock for land

e. Increase in accrued wages

f. Retirement of preferred stock

g. Purchase of a new plant

h. Depreciation expense

i. Decrease in accounts payable

j. Increase in accounts receivable

k. Proceeds from the sale of land

l. Increase in prepaid expenses

m. Retirement of a bond

n. Purchase of a 60% interest in another company

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

48

Statement of Cash Flows, Indirect Method

Refer to the information for Solpoder Corporation on the previous page.

Refer to the information for Solpoder Corporation on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

49

Statement of Cash Flows, Direct Method

Refer to the information for Solpoder Corporation on the previous page.

Refer to the information for Solpoder Corporation on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

50

Statement of Cash Flows, Indirect Method

Refer to the information for Roberts Company on the previous page.

Refer to the information for Roberts Company on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

51

Statement of Cash Flows, Direct Method

Refer to the information for Roberts Company on the previous page.

Refer to the information for Roberts Company on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

52

Statement of Cash Flows, Indirect Method

Refer to the information for Booth Manufacturing on the previous page.

Refer to the information for Booth Manufacturing on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

53

Statement of Cash Flows: Direct Method

Refer to the information for Booth Manufacturing on the previous page.

Refer to the information for Booth Manufacturing on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

54

Direct and Indirect Methods

Refer to the information for Rosie-Lee Company above. Additional transactions were as follows:

a. Sold equipment costing $21,600 with accumulated depreciation of $16,200 for $3,600.

b. Issued bonds for $90,000 on December 31.

c. Paid cash dividends of $36,000.

d. Retired mortgage of $108,000 on December 31.

Refer to the information for Rosie-Lee Company above. Additional transactions were as follows:

a. Sold equipment costing $21,600 with accumulated depreciation of $16,200 for $3,600.

b. Issued bonds for $90,000 on December 31.

c. Paid cash dividends of $36,000.

d. Retired mortgage of $108,000 on December 31.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

55

Statement of Cash Flows, Worksheet

Refer to the information for Rosie-Lee Company on the previous page. Additional transactions were as follows:

a. Sold equipment costing $21,600 with accumulated depreciation of $16,200 for $3,600.

b. Issued bonds for $90,000 on December 31.

c. Paid cash dividends of $36,000.

d. Retired a mortgage at a price of $108,000 on December 31.

Refer to the information for Rosie-Lee Company on the previous page. Additional transactions were as follows:

a. Sold equipment costing $21,600 with accumulated depreciation of $16,200 for $3,600.

b. Issued bonds for $90,000 on December 31.

c. Paid cash dividends of $36,000.

d. Retired a mortgage at a price of $108,000 on December 31.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

56

Statement of Cash Flows: Indirect Method

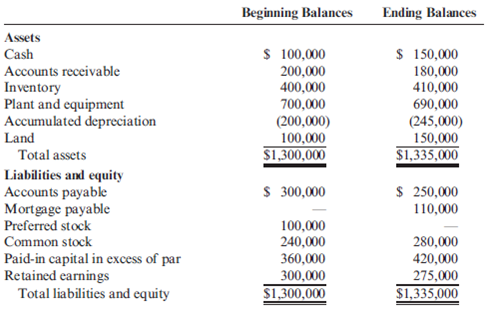

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

57

Statement of Cash Flows, Worksheet

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Balance sheets for Brierwold Corporation follow:

Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000. Additional transactions were as follows:

a. Purchased equipment costing $50,000.

b. Sold equipment costing $60,000 with a book value of $25,000 for $40,000.

c. Retired preferred stock at a cost of $110,000 (the premium is debited to retained earnings).

d. Issued 10,000 shares of common stock (par value, $4) for $10 per share.

e. Reported a loss of $15,000 for the year.

f. Purchased land for $50,000.

Refer to the information for Brierwold Corporation on the previous page.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

58

Schedule of Operating Cash Flows: Indirect Method

The income statement for the Mendelin Corporation is as follows:

Additional information is as follows:

a. Interest expense includes $1,800 of discount amortization.

b. The prepaid insurance expense account decreased by $2,000 during the year.

c. Wages payable decreased by $3,000 during the year.

d. Accounts payable increased by $7,500 (this account is for purchase of merchandise only).

e. Accounts receivable increased by $10,000 (net of allowance for doubtful accounts).

f. Inventory decreased by $16,000.

The income statement for the Mendelin Corporation is as follows:

Additional information is as follows:

a. Interest expense includes $1,800 of discount amortization.

b. The prepaid insurance expense account decreased by $2,000 during the year.

c. Wages payable decreased by $3,000 during the year.

d. Accounts payable increased by $7,500 (this account is for purchase of merchandise only).

e. Accounts receivable increased by $10,000 (net of allowance for doubtful accounts).

f. Inventory decreased by $16,000.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

59

Statement of Cash Flows, Indirect Method

The following balance sheets are taken from the records of Golding Company (numbers are expressed in thousands):

Additional information is as follows: (a) Equipment costing $10,000,000 was purchased at yearend. No equipment was sold; and (b) Net income for the year was $25,000,000; $10,000,000 in dividends were paid.

The following balance sheets are taken from the records of Golding Company (numbers are expressed in thousands):

Additional information is as follows: (a) Equipment costing $10,000,000 was purchased at yearend. No equipment was sold; and (b) Net income for the year was $25,000,000; $10,000,000 in dividends were paid.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

60

Statement of Cash Flows

Refer to the information for Blalock Company above.

Refer to the information for Blalock Company above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

61

Statement of Cash Flows, Worksheet

Refer to the information for Blalock Company above.

Refer to the information for Blalock Company above.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

62

Direct and Indirect Methods

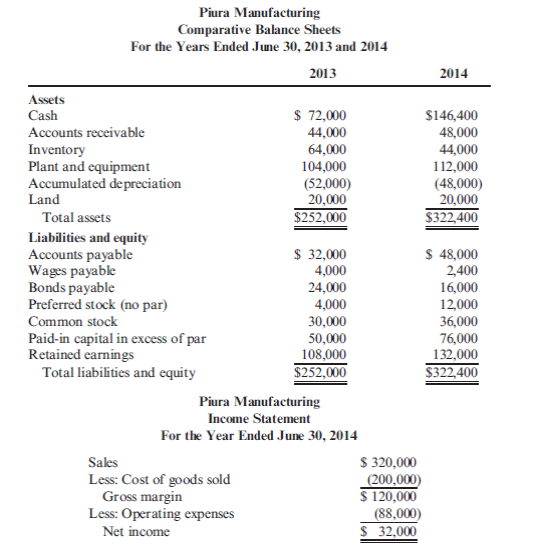

The comparative balance sheets and income statement of Piura Manufacturing follow.

Additional transactions for 2014 were as follows:

a. Cash dividends of $8,000 were paid.

b. Equipment was acquired by issuing common stock with a par value of $6,000. The fair market value of the equipment is $32,000.

c. Equipment with a book value of $12,000 was sold for $6,000. The original cost of the equipment was $24,000. The loss is included in operating expenses.

d. Two thousand shares of preferred stock were sold for $4 per share.

The comparative balance sheets and income statement of Piura Manufacturing follow.

Additional transactions for 2014 were as follows:

a. Cash dividends of $8,000 were paid.

b. Equipment was acquired by issuing common stock with a par value of $6,000. The fair market value of the equipment is $32,000.

c. Equipment with a book value of $12,000 was sold for $6,000. The original cost of the equipment was $24,000. The loss is included in operating expenses.

d. Two thousand shares of preferred stock were sold for $4 per share.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

63

Management of Statement of Cash Flows, Ethical Issues

Fred Jackson, president and owner of Bailey Company, is concerned about the company's ability to obtain a loan from a major bank. The loan is a key factor in the firm's plan to expand its operations. Demand for the firm's product is high-too high for the current production capacity to handle. Fred is convinced that a new plant is needed. Building the new plant, however, will require an infusion of new capital. Fred calls a meeting with Karla Jones, financial vice president.

Fred: Karla, what is the status of our loan application? Do you think that the bank will approve?

Karla: Perhaps, but at this point, there is a real risk. The loan officer has requested a complete set of financials for this year and the past 2 years. He has indicated that he is particularly interested in the statement of cash flows. As you know, our income statement looks great for all 3 years, but the statement of cash flows will show a significant increase in receivables, especially for this year. It will also show a significant increase in inventory, and I'm sure that he'll want to know why inventory is increasing if demand is so great that we need another plant. Both of these effects show decreasing cash flows from operating activities.

Fred: Well, it is certainly true that cash flows have been decreasing. One major problem is the lack of operating cash. This loan will solve that problem. Bill Lawson has agreed to build the plant for the amount of the loan but will actually charge me for only 95% of the stated cost. We get 5% of the loan for operating cash. Bill is willing to pay 5% to get the contract.

Karla: The loan may help with operating cash flows, but we can't get the loan without showing some evidence of cash strength. We need to do something about the increases in inventory and receivables that we expect for this year.

Fred: The increased inventory is easy to explain. We had to work overtime and use subcontractors to take care of one of our biggest customers. That inventory will be gone by the first of next year.

Karla: The problem isn't explaining the inventory. The problem is that the increase in inventory decreases our operating cash flows and this shows up on the statement of cash flows. This effect, coupled with the increase in receivables, depicts us as being cash poor. It'll definitely hurt our chances.

Fred: I see. Well, this can be solved. The inventory is for a customer that I know well. She'll do me a favor. I'll simply get her to take delivery of the inventory early, before the end of our fiscal year. She can pay me next year as originally planned.

Karla: Fred, all that will do is shift the increase from inventory to receivables. It'll still report the same cash position.

Fred: No problem. We'll report the delivery as a cash sale, and I'll have Bill Lawson advance me the cash as a temporary loan. He'll do that to get the contract to build our new plant. In fact, we can do the same with some of our other receivables. We'll report them as collected, and I'll get Bill to cover. If he understands that this is what it takes to get the loan, he'll cooperate. He stands to make a lot of money on the deal.

Karla: Fred, this is getting complicated. The bank will have us audited each year if this loan is approved. If an audit were to reveal some of this manipulation, we could be in big trouble, particularly if the company has any trouble in repaying the loan.

Fred: The company won't have any trouble. Sales are strong, and the problem of collecting receivables can be solved, especially given the extra time that the 5% of the loan proceeds will provide.

Fred Jackson, president and owner of Bailey Company, is concerned about the company's ability to obtain a loan from a major bank. The loan is a key factor in the firm's plan to expand its operations. Demand for the firm's product is high-too high for the current production capacity to handle. Fred is convinced that a new plant is needed. Building the new plant, however, will require an infusion of new capital. Fred calls a meeting with Karla Jones, financial vice president.

Fred: Karla, what is the status of our loan application? Do you think that the bank will approve?

Karla: Perhaps, but at this point, there is a real risk. The loan officer has requested a complete set of financials for this year and the past 2 years. He has indicated that he is particularly interested in the statement of cash flows. As you know, our income statement looks great for all 3 years, but the statement of cash flows will show a significant increase in receivables, especially for this year. It will also show a significant increase in inventory, and I'm sure that he'll want to know why inventory is increasing if demand is so great that we need another plant. Both of these effects show decreasing cash flows from operating activities.

Fred: Well, it is certainly true that cash flows have been decreasing. One major problem is the lack of operating cash. This loan will solve that problem. Bill Lawson has agreed to build the plant for the amount of the loan but will actually charge me for only 95% of the stated cost. We get 5% of the loan for operating cash. Bill is willing to pay 5% to get the contract.

Karla: The loan may help with operating cash flows, but we can't get the loan without showing some evidence of cash strength. We need to do something about the increases in inventory and receivables that we expect for this year.

Fred: The increased inventory is easy to explain. We had to work overtime and use subcontractors to take care of one of our biggest customers. That inventory will be gone by the first of next year.

Karla: The problem isn't explaining the inventory. The problem is that the increase in inventory decreases our operating cash flows and this shows up on the statement of cash flows. This effect, coupled with the increase in receivables, depicts us as being cash poor. It'll definitely hurt our chances.

Fred: I see. Well, this can be solved. The inventory is for a customer that I know well. She'll do me a favor. I'll simply get her to take delivery of the inventory early, before the end of our fiscal year. She can pay me next year as originally planned.

Karla: Fred, all that will do is shift the increase from inventory to receivables. It'll still report the same cash position.

Fred: No problem. We'll report the delivery as a cash sale, and I'll have Bill Lawson advance me the cash as a temporary loan. He'll do that to get the contract to build our new plant. In fact, we can do the same with some of our other receivables. We'll report them as collected, and I'll get Bill to cover. If he understands that this is what it takes to get the loan, he'll cooperate. He stands to make a lot of money on the deal.

Karla: Fred, this is getting complicated. The bank will have us audited each year if this loan is approved. If an audit were to reveal some of this manipulation, we could be in big trouble, particularly if the company has any trouble in repaying the loan.

Fred: The company won't have any trouble. Sales are strong, and the problem of collecting receivables can be solved, especially given the extra time that the 5% of the loan proceeds will provide.

Unlock Deck

Unlock for access to all 63 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 63 flashcards in this deck.