Deck 7: Earnings Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Harrison Industries (a GVV case)

Questions

1. What are the real and anticipated arguments that could be made by those at Harrison Industries who may try to convince Donna to go along with the accounting for future severance payments? Include in your discussion the possible motivation for the accounting treatment.

2. What is at stake for the key parties? What are Donna's ethical obligations to them?

3. What is Donna's most powerful and persuasive response to the reasons and rationalizations she needs to address? To whom should the argument be made?

4. What is Donna's most effective approach to giving voice to her values? Explain.

Questions

1. What are the real and anticipated arguments that could be made by those at Harrison Industries who may try to convince Donna to go along with the accounting for future severance payments? Include in your discussion the possible motivation for the accounting treatment.

2. What is at stake for the key parties? What are Donna's ethical obligations to them?

3. What is Donna's most powerful and persuasive response to the reasons and rationalizations she needs to address? To whom should the argument be made?

4. What is Donna's most effective approach to giving voice to her values? Explain.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

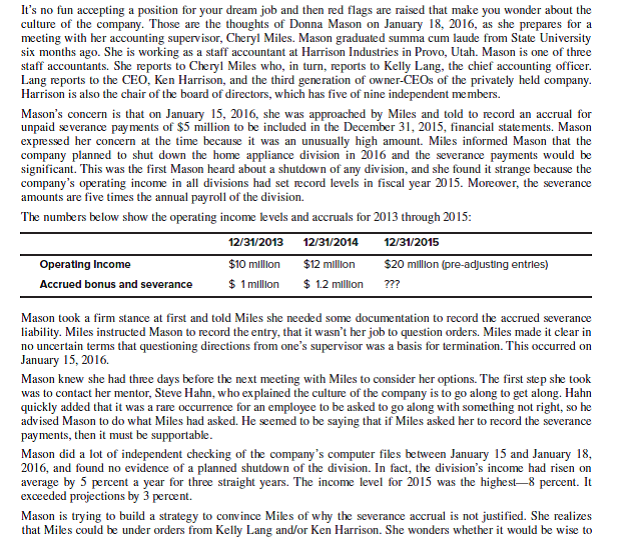

The auditor of Beastie Company is reviewing the following client information for the prior year ended December 31, 2015, and all four quarters of 2016.

Characterize the accruals as discretionary or nondiscretionary. What are the potential issues that the auditors should address given these numbers?

Characterize the accruals as discretionary or nondiscretionary. What are the potential issues that the auditors should address given these numbers?

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/35

Play

Full screen (f)

Deck 7: Earnings Management

1

Nortel Networks

Questions

1. Discuss Nortel's accounting for the following transactions and why they were not in conformity with GAAP:

• Revenue recognition

• Reserve accounting

• Accounting for contingent liabilities

2. The following two statements are made in the case:

• Accounting experts said the case is sure to be closely watched by others in the business community for the message it sends about where the line lies between fraud and the acceptable use of discretion in accounting.

• Darren Henderson opined that "The message... is that it is okay to use accounting judgments to achieve desired outcomes, [such as] a certain earnings target."

Evaluate these statements from the perspectives of representational faithfulness and fair presentation of the financial results reported by Nortel.

3. During the trial, lawyers for the accused said that the men believed that the accounting decisions they made were appropriate at the time, and that the accounting treatment was approved by Nortel's auditors from Deloitte Touche. Judge Marrocco accepted these arguments. Marrocco added he was "not satisfied beyond a reasonable doubt" that the trio [i.e., Dunn, Beatty, and Gollogly] had "deliberately misrepresented" financial results. Given the facts of the case do you believe Judge Marrocco's decision was justified? Explain.

4. Does it appear from the facts of the case that the Deloitte auditors met their ethical and professional responsibilities in the audit of Nortel's financial statements?

Questions

1. Discuss Nortel's accounting for the following transactions and why they were not in conformity with GAAP:

• Revenue recognition

• Reserve accounting

• Accounting for contingent liabilities

2. The following two statements are made in the case:

• Accounting experts said the case is sure to be closely watched by others in the business community for the message it sends about where the line lies between fraud and the acceptable use of discretion in accounting.

• Darren Henderson opined that "The message... is that it is okay to use accounting judgments to achieve desired outcomes, [such as] a certain earnings target."

Evaluate these statements from the perspectives of representational faithfulness and fair presentation of the financial results reported by Nortel.

3. During the trial, lawyers for the accused said that the men believed that the accounting decisions they made were appropriate at the time, and that the accounting treatment was approved by Nortel's auditors from Deloitte Touche. Judge Marrocco accepted these arguments. Marrocco added he was "not satisfied beyond a reasonable doubt" that the trio [i.e., Dunn, Beatty, and Gollogly] had "deliberately misrepresented" financial results. Given the facts of the case do you believe Judge Marrocco's decision was justified? Explain.

4. Does it appear from the facts of the case that the Deloitte auditors met their ethical and professional responsibilities in the audit of Nortel's financial statements?

Facts:

The case is that of accounting and financial fraud committed by Canada's N Telecom, one of the world's premier Telecommunications companies.

The Company during 1990's engaged in a series of accounting fraud such as recording revenue which is not yet received by the company and the company maintained secret cash reserves which are not revealed in the books.

The company's efforts are to improve the stock price of the company in the stock exchanges, investments made by the company backfired and as a result the company filed for bankruptcy in U.S, Canada and Europe.

Investigating agencies launched a full scale investigation into the financial fraud committed by the company.

Revenue Recognition:

GAAP offered specific guidelines based on which revenue recognition can be done, for example, GAAP mentions that revenue resulting from financial transactions can be recorded only when a particular transaction takes place and the revenue is measurable.

Reserve accounting:

It is an accounting practice in which profits are reserved for a particular purpose such as purchase of fixed assets, purchase of machinery etc.

This categorized use of profits for a special use is referred as reserve accounting.

Contingent liability accounting:

Contingent liabilities are recorded as liabilities which are most likely to happen and the expenses are recorded only when the exact amount of expenses to meet the liability are known.

1.

Discussion:

The Company engaged in accounting and financial fraud by resorting to fraudulent revenue recognition, reserve accounting and contingency liability accounting procedures.

They are done in the following manner:

Revenue recognition:

The company had huge surplus of inventory left with them and is unable to sell them in the market because of lack of orders.

In order to convert this into revenue, the company opted for a technique called as "bill and hold", in which customers can order certain equipment, bill for it and wait to take the delivery at a later period of time.

Reserve Accounting:

The company resorted to creation of unrecorded reserves of funds and engaged in activities such as releasing the reserves into income to boost the income whenever needed.

Contingency planning:

The company kept hidden reserves which are off the records so that they can be used at a later period whenever it is necessary.

They are not in confirmation with the GAAP regulations because of improper recording of information and failure to use proper accounts management principles.

2.

The accounting practices followed by N Telecommunications Company in the case and the discretion they have adapted in keeping the information are in total disagreement with the statement offered by accounting experts.

Accounting experts say that a certain amount of discretion is required by the firms when disclosing key financial information.

However, basic factual information cannot be neglected and left out from the records, similarly key information such as profits and reserves cannot be left out of records. Thus, the accounting practices are in total disagreement with the opinion of the experts.

3.

Judge M's statements regarding the justification of the accounting practices advocated by the defendants are not justified.

This is because the actions of the defendants are in practice for a long time, during the later period of 1990's and at a time when the company is facing a slowdown in the market.

Thus judge M's comments are not justified.

4.

The auditors of N Telecommunications failed to display professional responsibility while performing the audit of the N T's case.

This is because they have failed to suggest correction measures to correct the accounting irregularities in the financial statements.

Also, the auditors failed to suggest proper internal controls for controlling and preventing accounting irregularities.

Thus, the auditors failed to perform their professional responsibilities.

The case is that of accounting and financial fraud committed by Canada's N Telecom, one of the world's premier Telecommunications companies.

The Company during 1990's engaged in a series of accounting fraud such as recording revenue which is not yet received by the company and the company maintained secret cash reserves which are not revealed in the books.

The company's efforts are to improve the stock price of the company in the stock exchanges, investments made by the company backfired and as a result the company filed for bankruptcy in U.S, Canada and Europe.

Investigating agencies launched a full scale investigation into the financial fraud committed by the company.

Revenue Recognition:

GAAP offered specific guidelines based on which revenue recognition can be done, for example, GAAP mentions that revenue resulting from financial transactions can be recorded only when a particular transaction takes place and the revenue is measurable.

Reserve accounting:

It is an accounting practice in which profits are reserved for a particular purpose such as purchase of fixed assets, purchase of machinery etc.

This categorized use of profits for a special use is referred as reserve accounting.

Contingent liability accounting:

Contingent liabilities are recorded as liabilities which are most likely to happen and the expenses are recorded only when the exact amount of expenses to meet the liability are known.

1.

Discussion:

The Company engaged in accounting and financial fraud by resorting to fraudulent revenue recognition, reserve accounting and contingency liability accounting procedures.

They are done in the following manner:

Revenue recognition:

The company had huge surplus of inventory left with them and is unable to sell them in the market because of lack of orders.

In order to convert this into revenue, the company opted for a technique called as "bill and hold", in which customers can order certain equipment, bill for it and wait to take the delivery at a later period of time.

Reserve Accounting:

The company resorted to creation of unrecorded reserves of funds and engaged in activities such as releasing the reserves into income to boost the income whenever needed.

Contingency planning:

The company kept hidden reserves which are off the records so that they can be used at a later period whenever it is necessary.

They are not in confirmation with the GAAP regulations because of improper recording of information and failure to use proper accounts management principles.

2.

The accounting practices followed by N Telecommunications Company in the case and the discretion they have adapted in keeping the information are in total disagreement with the statement offered by accounting experts.

Accounting experts say that a certain amount of discretion is required by the firms when disclosing key financial information.

However, basic factual information cannot be neglected and left out from the records, similarly key information such as profits and reserves cannot be left out of records. Thus, the accounting practices are in total disagreement with the opinion of the experts.

3.

Judge M's statements regarding the justification of the accounting practices advocated by the defendants are not justified.

This is because the actions of the defendants are in practice for a long time, during the later period of 1990's and at a time when the company is facing a slowdown in the market.

Thus judge M's comments are not justified.

4.

The auditors of N Telecommunications failed to display professional responsibility while performing the audit of the N T's case.

This is because they have failed to suggest correction measures to correct the accounting irregularities in the financial statements.

Also, the auditors failed to suggest proper internal controls for controlling and preventing accounting irregularities.

Thus, the auditors failed to perform their professional responsibilities.

2

In Arthur Levitt's speech, referred to in the opening quote, he also said, "I fear that we are witnessing an erosion in the quality of earnings, and therefore, the quality of financial reporting. Managing may be giving way to manipulation; integrity may be losing out to illusion." Explain what you think Levitt meant by this statement. What role do financial analysts' earnings expectations play in the quality of earnings?

In the given statement, A thinks that sales are recognized prematurely or sales may have booked prior to prices have been fixed or finalization of contracts or booking of sales revenue even when a customer is in a condition to void or terminate or delay the sale. He describes the practices of improperly booking of revenues. Financial reporting is the base for investor, creditor and other stake holders to judge the performance of the company. They all feel that company that has quality built in financial reporting is much safer to invest and such company will be able to raise fund from market easily.

The financial analyst plays an important role in earning expectation and reporting quality of earning. The auditors meet their ethical obligation properly and hence show true picture of company and protect interest of public and help in detecting fraud. In view of financial analyst, quality of earning is also an important consideration. When earnings are reported properly without any error then financial analyst can clearly derive its conclusion and clearly report it as what it meant to report.

The financial analyst plays an important role in earning expectation and reporting quality of earning. The auditors meet their ethical obligation properly and hence show true picture of company and protect interest of public and help in detecting fraud. In view of financial analyst, quality of earning is also an important consideration. When earnings are reported properly without any error then financial analyst can clearly derive its conclusion and clearly report it as what it meant to report.

3

Solutions Network, Inc. (a GVV case)

Questions

1. What are the main arguments Sarah is trying to counter? That is, what are the reasons and rationalizations she needs to address in deciding how to handle the meeting with Paul?

2. What is at stake for the key parties in this case? What are Sarah's ethical obligations to them?

3. Should Sarah follow Shannon's advice? What if she does and Paul does not back off? What additional levers can she use to influence Paul and make her values understood?

4. What is the most powerful and persuasive response to the reasons and rationalizations Sarah needs to address? To whom should the argument be made? When and in what context?

Questions

1. What are the main arguments Sarah is trying to counter? That is, what are the reasons and rationalizations she needs to address in deciding how to handle the meeting with Paul?

2. What is at stake for the key parties in this case? What are Sarah's ethical obligations to them?

3. Should Sarah follow Shannon's advice? What if she does and Paul does not back off? What additional levers can she use to influence Paul and make her values understood?

4. What is the most powerful and persuasive response to the reasons and rationalizations Sarah needs to address? To whom should the argument be made? When and in what context?

Every business is set up with a motive (sometimes profit is the motive while sometimes service is the motive) and to fulfill the motive many people are involved in the business (employees as well as other stakeholders). All the people involved also can have their own personal as well as professional motives to fulfill and move ahead.

Companies sometimes want to grow bigger and faster and so get involved in some unethical practices. Such things done by some companies makes it difficult for the public to believe and find out which company is working honestly and which is not. So to keep a check and give authentic, certified information to the public and other stakeholders about the company there are many regulatory bodies as per the industry/ sector any particular company is working in. Similarly, accounting norms are also different industries and companies in different industries.

One thing that is common for all industries is the Audit requirements that is, every company registered under a specific act has to maintain some books of accounts (financial records) to show them to various stakeholders (like shareholders, employees, investors, bankers etc.) about the financial position of the company. Now, Auditors have a role to play that is, Auditors certify that the records maintained and shown by the specific company are reflecting true and fair position of the company.

Auditors do face many challenges and pressures from the company's management to show various things or sometimes to compromise on the documentation part or may be sometimes proper documents/ proofs are not available with the company and they start pressurizing the auditors to compromise on it.

Sometimes auditors face pressures from their own companies to finish the audit work faster or within deadlines and so they compromise on checking the documents etc. So many of them face many such challenges and pressures but their job is to handle these pressures and still do not compromise and be answerable to the public (their first stakeholders).

1.

Doing the audit and representing the useful information of the financial statements faithfully is a basic requirement and expectation from all auditors by the all stakeholders whether it is general public or shareholders or Banks etc. the basic reason behind this is everybody wants to have a clear picture of the performance as well as position of the company at the year-end because everybody has some stake or the other involved in the company.

Auditors have this responsibility of providing true and fair position of the company to all the stakeholders so that they can take their decisions based on company's performance last year as well as plan of action suggested for upcoming years.

In this case, Ms. S is trying to counter arguments on:

1. The ideal situation of company disclosing the actual facts and figures even if they were not able to meet the projected sales targets so that corrective measures can be thought of for the next year.

2. as given in the case, if the company discloses the transaction as a sale transaction than it is not the right recording of the transaction because that is only first half part of the agreement executed and next half of the agreement is supposed to be executed after 30 days so, it is not right to record an incomplete transaction.

3. Ms. S will have to answer their client about "if the company is not recording this transaction than the company's sales as well as net income target is not met so how to justify that in front of the stakeholders.

4. Also, justification should be given to other stakeholders like: shareholders, Banks etc. if the company does not the transaction because as per the auditors, transactions should be reported on the economic substance of the transactions rather than on the legal form of the transactions. That is, if this transaction is reported as a sale and later on, the company fulfills (or not) its agreement than what will be the effect of the same on the company's financial status.

The rationalizations that Ms. S needs to address when in meeting with Mr. P are:

1. it's the duty of auditors to show a True and Fair position of the company for all the stakeholders.

2. What can be the after effects of recording an incomplete transaction and what if they are caught later?

3. Ms. S will have to provide a genuine justification for the stakeholders for why the company was not able to meet the sales as well as income targets and what are future plans regarding the same.

4. By recording incomplete/ wrong transactions company's financial status as well as financial position of the company can have serious impact on the company as well as the stakeholders.

2.

The key parties involved in this are: the company (SN Inc.), CFO (Mr. P), Audit committee and other stakeholders.

The company has a stake because its yearly performance is showcased after this audit and so if this transaction (as referred in the question) is not included than the sales are not meeting the targeted sales and so the company can face problems in terms of decrease in

goodwill, decrease in net income and sales and further other financial parameters will be suffering.

CFO has a stake because he is representing the company and will be answerable to the Board of Directors as well as shareholders and other stakeholders for company's performance. Also, he is under pressure to show results so he is expecting Ms. To include the revenue from an incomplete transaction to be included in the yearly revenue of the company.

Audit committee and Ms. S (specifically in the Audit Committee) has a stake because she is conducting the audit (internally) and is responsible for recording of transactions and if any such transaction is caught by the external Auditors (expected on January 15, 2016) she will be the one answering them.

She has some ethical obligations to give a True and Fair position of the company for other stakeholders to take right decisions as per their respective requirements. Also, Ms. S is responsible for the company's performance. If Ms. S gives wrong figures about the company's sales etc. than it can mislead the various stakeholders and their many things can be at stake for this so Ms. S has ethical obligations towards the various stakeholders also

Other stakeholders like: shareholders, Bankers, debtors, creditors etc. have all the rights to know about the exact financial position of the company for them to take appropriate decisions based on the current financial position of the company.

3.

Yes, Ms. S should follow her friend's advice and try to explain the ethical obligations because of which she is not convinced to record the partial sale transaction in the books of accounts.

She is into ethical dilemma because the transaction is not complete as per the agreement and so should not be recorded before the transaction is completed (by both parties) as per agreement. Recording the partial completion as a complete sale transaction can be misleading for the stakeholders because if something goes wrong and the transaction is cancelled than it will have huge impact on the net income and revenues. As given in the question the deal in question is of $ 20 million and the net income increase (because of this revenue) is $ 1 million. This transaction although helps management to justify the sales as per the budget but in case it is not completed than it will affect the net income in turns the stakeholders.

If still Mr. P does not back off than she can give examples of companies like Enron etc. who's frauds were highlighted later and the whole management, finance department was involved in giving misleading figures in the books of accounts. Also, she can talk about the various surveys conducted and finally the cookie-jar effect to be used as a rescue for them at later time if income goes down and create a reserve right now rather than showing higher income by manipulating the transaction records.

4.

Ms. S needs to address rationalizations given by Mr. P about the budgeted sales figures required to be achieved by the year end and the company will be very close to the target sales with this single transaction (because the transaction is a material transaction) if recorded in the books of accounts while as per Ms. S this transaction should not be recorded as of now because it is an incomplete transaction till the year end (as per agreement).

Although it is a material transaction and will be give a positive impact on the Net Income and sales of the company for all the stakeholders to look at the financial position but at the same time it is their duty to keep the stakeholders informed about the true and fair position of the company rather than giving any misleading figures just to upkeep the company's image. All the stakeholders have their own interests and reasons to know about the exact financial position of the company and so it is their (company and CPAs) duty to keep them informed about the true and fair position of the company.

Companies sometimes want to grow bigger and faster and so get involved in some unethical practices. Such things done by some companies makes it difficult for the public to believe and find out which company is working honestly and which is not. So to keep a check and give authentic, certified information to the public and other stakeholders about the company there are many regulatory bodies as per the industry/ sector any particular company is working in. Similarly, accounting norms are also different industries and companies in different industries.

One thing that is common for all industries is the Audit requirements that is, every company registered under a specific act has to maintain some books of accounts (financial records) to show them to various stakeholders (like shareholders, employees, investors, bankers etc.) about the financial position of the company. Now, Auditors have a role to play that is, Auditors certify that the records maintained and shown by the specific company are reflecting true and fair position of the company.

Auditors do face many challenges and pressures from the company's management to show various things or sometimes to compromise on the documentation part or may be sometimes proper documents/ proofs are not available with the company and they start pressurizing the auditors to compromise on it.

Sometimes auditors face pressures from their own companies to finish the audit work faster or within deadlines and so they compromise on checking the documents etc. So many of them face many such challenges and pressures but their job is to handle these pressures and still do not compromise and be answerable to the public (their first stakeholders).

1.

Doing the audit and representing the useful information of the financial statements faithfully is a basic requirement and expectation from all auditors by the all stakeholders whether it is general public or shareholders or Banks etc. the basic reason behind this is everybody wants to have a clear picture of the performance as well as position of the company at the year-end because everybody has some stake or the other involved in the company.

Auditors have this responsibility of providing true and fair position of the company to all the stakeholders so that they can take their decisions based on company's performance last year as well as plan of action suggested for upcoming years.

In this case, Ms. S is trying to counter arguments on:

1. The ideal situation of company disclosing the actual facts and figures even if they were not able to meet the projected sales targets so that corrective measures can be thought of for the next year.

2. as given in the case, if the company discloses the transaction as a sale transaction than it is not the right recording of the transaction because that is only first half part of the agreement executed and next half of the agreement is supposed to be executed after 30 days so, it is not right to record an incomplete transaction.

3. Ms. S will have to answer their client about "if the company is not recording this transaction than the company's sales as well as net income target is not met so how to justify that in front of the stakeholders.

4. Also, justification should be given to other stakeholders like: shareholders, Banks etc. if the company does not the transaction because as per the auditors, transactions should be reported on the economic substance of the transactions rather than on the legal form of the transactions. That is, if this transaction is reported as a sale and later on, the company fulfills (or not) its agreement than what will be the effect of the same on the company's financial status.

The rationalizations that Ms. S needs to address when in meeting with Mr. P are:

1. it's the duty of auditors to show a True and Fair position of the company for all the stakeholders.

2. What can be the after effects of recording an incomplete transaction and what if they are caught later?

3. Ms. S will have to provide a genuine justification for the stakeholders for why the company was not able to meet the sales as well as income targets and what are future plans regarding the same.

4. By recording incomplete/ wrong transactions company's financial status as well as financial position of the company can have serious impact on the company as well as the stakeholders.

2.

The key parties involved in this are: the company (SN Inc.), CFO (Mr. P), Audit committee and other stakeholders.

The company has a stake because its yearly performance is showcased after this audit and so if this transaction (as referred in the question) is not included than the sales are not meeting the targeted sales and so the company can face problems in terms of decrease in

goodwill, decrease in net income and sales and further other financial parameters will be suffering.

CFO has a stake because he is representing the company and will be answerable to the Board of Directors as well as shareholders and other stakeholders for company's performance. Also, he is under pressure to show results so he is expecting Ms. To include the revenue from an incomplete transaction to be included in the yearly revenue of the company.

Audit committee and Ms. S (specifically in the Audit Committee) has a stake because she is conducting the audit (internally) and is responsible for recording of transactions and if any such transaction is caught by the external Auditors (expected on January 15, 2016) she will be the one answering them.

She has some ethical obligations to give a True and Fair position of the company for other stakeholders to take right decisions as per their respective requirements. Also, Ms. S is responsible for the company's performance. If Ms. S gives wrong figures about the company's sales etc. than it can mislead the various stakeholders and their many things can be at stake for this so Ms. S has ethical obligations towards the various stakeholders also

Other stakeholders like: shareholders, Bankers, debtors, creditors etc. have all the rights to know about the exact financial position of the company for them to take appropriate decisions based on the current financial position of the company.

3.

Yes, Ms. S should follow her friend's advice and try to explain the ethical obligations because of which she is not convinced to record the partial sale transaction in the books of accounts.

She is into ethical dilemma because the transaction is not complete as per the agreement and so should not be recorded before the transaction is completed (by both parties) as per agreement. Recording the partial completion as a complete sale transaction can be misleading for the stakeholders because if something goes wrong and the transaction is cancelled than it will have huge impact on the net income and revenues. As given in the question the deal in question is of $ 20 million and the net income increase (because of this revenue) is $ 1 million. This transaction although helps management to justify the sales as per the budget but in case it is not completed than it will affect the net income in turns the stakeholders.

If still Mr. P does not back off than she can give examples of companies like Enron etc. who's frauds were highlighted later and the whole management, finance department was involved in giving misleading figures in the books of accounts. Also, she can talk about the various surveys conducted and finally the cookie-jar effect to be used as a rescue for them at later time if income goes down and create a reserve right now rather than showing higher income by manipulating the transaction records.

4.

Ms. S needs to address rationalizations given by Mr. P about the budgeted sales figures required to be achieved by the year end and the company will be very close to the target sales with this single transaction (because the transaction is a material transaction) if recorded in the books of accounts while as per Ms. S this transaction should not be recorded as of now because it is an incomplete transaction till the year end (as per agreement).

Although it is a material transaction and will be give a positive impact on the Net Income and sales of the company for all the stakeholders to look at the financial position but at the same time it is their duty to keep the stakeholders informed about the true and fair position of the company rather than giving any misleading figures just to upkeep the company's image. All the stakeholders have their own interests and reasons to know about the exact financial position of the company and so it is their (company and CPAs) duty to keep them informed about the true and fair position of the company.

4

Are the use of non-GAAP financial measures ethical?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

5

GE: "Imagination at Work"

Questions

1. Review the SEC's complaint against GE (see Note 1) and explain the specifics of the company's hedging transactions and why they violated GAAP.

2. Did GE violate the rules for revenue recognition (pre-2016-change) on the "sale" of its locomotives? Explain.

3. Did GE engage in earnings management? How would you make that determination given the facts of the case?

Questions

1. Review the SEC's complaint against GE (see Note 1) and explain the specifics of the company's hedging transactions and why they violated GAAP.

2. Did GE violate the rules for revenue recognition (pre-2016-change) on the "sale" of its locomotives? Explain.

3. Did GE engage in earnings management? How would you make that determination given the facts of the case?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

6

Relevance and faithful representation are the qualitative characteristics of useful information under SFAC No. 8. 93 How does ethical reasoning enter into making determinations about the relevance and faithful representation of financial information?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

7

Harrison Industries (a GVV case)

Questions

1. What are the real and anticipated arguments that could be made by those at Harrison Industries who may try to convince Donna to go along with the accounting for future severance payments? Include in your discussion the possible motivation for the accounting treatment.

2. What is at stake for the key parties? What are Donna's ethical obligations to them?

3. What is Donna's most powerful and persuasive response to the reasons and rationalizations she needs to address? To whom should the argument be made?

4. What is Donna's most effective approach to giving voice to her values? Explain.

Questions

1. What are the real and anticipated arguments that could be made by those at Harrison Industries who may try to convince Donna to go along with the accounting for future severance payments? Include in your discussion the possible motivation for the accounting treatment.

2. What is at stake for the key parties? What are Donna's ethical obligations to them?

3. What is Donna's most powerful and persuasive response to the reasons and rationalizations she needs to address? To whom should the argument be made?

4. What is Donna's most effective approach to giving voice to her values? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

8

Evaluate earnings management from a utilitarian perspective. Can earnings management be an ethical practice? Discuss why or why not.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

9

Dell Computer

Background

Questions

1. How would you characterize Dell's accounting techniques described in the case? Was it a case of aggressive accounting? Was it earnings management? Link your discussion to the specific accounting methodology and GAAP rules.

2. Identify the red flags that should have alerted PwC that Dell may have been engaging in fraud. Given that Dell issued clean opinions during the fraud years, do you think it is possible that the firm conducted its audit in accordance with GAAS? What indicators would you look for to make that determination?

3. The court decision relied on the concept of scienter for not holding PwC legally liable for issuing clean opinions when the financial statements did not fairly present financial position. Would you reach the same conclusion from an ethical perspective? Explain.

Background

Questions

1. How would you characterize Dell's accounting techniques described in the case? Was it a case of aggressive accounting? Was it earnings management? Link your discussion to the specific accounting methodology and GAAP rules.

2. Identify the red flags that should have alerted PwC that Dell may have been engaging in fraud. Given that Dell issued clean opinions during the fraud years, do you think it is possible that the firm conducted its audit in accordance with GAAS? What indicators would you look for to make that determination?

3. The court decision relied on the concept of scienter for not holding PwC legally liable for issuing clean opinions when the financial statements did not fairly present financial position. Would you reach the same conclusion from an ethical perspective? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

10

Evaluate the following statements from an ethical perspective:

"Earnings management in a narrow sense is the behavior of management to play with the discretionary accrual component to determine high or low earnings."

"Earnings are potentially managed, because financial accounting standards still provide alternative methods."

"Earnings management in a narrow sense is the behavior of management to play with the discretionary accrual component to determine high or low earnings."

"Earnings are potentially managed, because financial accounting standards still provide alternative methods."

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

11

TierOne Bank

Questions

1. Was TierOne's accounting for the loan loss reserve indicative of "managed earnings?" How would you make that determination?

2. What role does professional judgment have in auditing the adequacy of a loan loss reserve? Do you believe KPMG exercised a degree of care and professional skepticism that is consistent with the level of ethical and professional judgment expected by the accounting profession? What about the public?

3. Given the facts of the case with respect to audit work performed by Aesoph and. Bennett, do you believe the sanctions imposed by the SEC were appropriate? Explain.

Questions

1. Was TierOne's accounting for the loan loss reserve indicative of "managed earnings?" How would you make that determination?

2. What role does professional judgment have in auditing the adequacy of a loan loss reserve? Do you believe KPMG exercised a degree of care and professional skepticism that is consistent with the level of ethical and professional judgment expected by the accounting profession? What about the public?

3. Given the facts of the case with respect to audit work performed by Aesoph and. Bennett, do you believe the sanctions imposed by the SEC were appropriate? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

12

Comment on the statement that materiality is in the eye of the beholder. How does this statement relate to the discussion in this chapter of how to gauge materiality in assessing financial statement restatements? Is materiality inconsistent with the notion of representational faithfulness?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

13

Sunbeam Corporation

Questions

1. How did pressures for financial performance contribute to Sunbeam's culture, where quarterly sales were manipulated to influence investors? To what extent do you believe the Andersen auditors should have considered the resulting culture in planning and executing its audit?

2. Why is it important for auditors to use analytical comparisons such as the ratios in the Sunbeam case to evaluate possible red flags that may indicate additional auditing is required? How does making such calculations enable auditors to meet their ethical obligations?

3. Assume you were the technical advisory partner for Andersen on the Sunbeam engagement and reported directly to Harlow. You have just reviewed all the workpapers on the audit including materiality judgments. You are concerned about what you have just seen. Further assume that you consider yourself to be a pragmatist, one who is concerned with your own material welfare, but also with moral ideals. Develop a plan of action for voicing your values to ensure you are heard by Harlow and others in the firm. Consider the following in developing the plan to do the right thing:

• What do you need to say to Harlow?

• What are the likely objections or pushback?

• What would you say next? To whom, and in what sequence?

Questions

1. How did pressures for financial performance contribute to Sunbeam's culture, where quarterly sales were manipulated to influence investors? To what extent do you believe the Andersen auditors should have considered the resulting culture in planning and executing its audit?

2. Why is it important for auditors to use analytical comparisons such as the ratios in the Sunbeam case to evaluate possible red flags that may indicate additional auditing is required? How does making such calculations enable auditors to meet their ethical obligations?

3. Assume you were the technical advisory partner for Andersen on the Sunbeam engagement and reported directly to Harlow. You have just reviewed all the workpapers on the audit including materiality judgments. You are concerned about what you have just seen. Further assume that you consider yourself to be a pragmatist, one who is concerned with your own material welfare, but also with moral ideals. Develop a plan of action for voicing your values to ensure you are heard by Harlow and others in the firm. Consider the following in developing the plan to do the right thing:

• What do you need to say to Harlow?

• What are the likely objections or pushback?

• What would you say next? To whom, and in what sequence?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

14

Needles talks about the use of a continuum ranging from questionable or highly conservative to fraud to assess the amount to be recorded for an estimated expense. Do you believe that the choice of an overly conservative or overly aggressive amount would reflect earnings management? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

15

Sino-Forest: Accounting for Trees

Questions

1. Should operational and cultural considerations play a role in determining whether Sino-Forest committed a fraud? Explain.

2. Did Sino-Forest manage earnings? Refer to the discussion in this chapter about different perspectives on earnings management in responding.

3. Critically evaluate the audit work of Ernst Young from the perspective of generally accepted auditing standards and professional ethics. Was this a failed audit?

Questions

1. Should operational and cultural considerations play a role in determining whether Sino-Forest committed a fraud? Explain.

2. Did Sino-Forest manage earnings? Refer to the discussion in this chapter about different perspectives on earnings management in responding.

3. Critically evaluate the audit work of Ernst Young from the perspective of generally accepted auditing standards and professional ethics. Was this a failed audit?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

16

In 2010, LinkedIn reported trade payable obligations totaling $10.8 million in other accrued expenses within accrued liabilities instead of accounts payable. In 2011, note 2 in the 10-Kfinancial statements described the use of accrued liabilities instead of accounts payable as a classification. Do you believe LinkedIn's accounting qualifies as a financial shenanigan?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

17

The North Face, Inc.

Questions

1. Use the fraud triangle to analyze the red flags that existed in the case and the role and responsibilities of the auditors at Deloitte Touche in The North Face accounting fraud.

2. Identify the general principles that dictate when revenue should be recorded. How did North Face violate those rules?

3. Evaluate the actions of Deloitte Touche first proposing an audit adjustment on the $1.64 million balance of the December 29, 1997, transaction with the barter company and then passing on the adjustment based on it not having a material effect on the financial statements. In this regard, should auditors conceal materiality levels from audit clients?

Questions

1. Use the fraud triangle to analyze the red flags that existed in the case and the role and responsibilities of the auditors at Deloitte Touche in The North Face accounting fraud.

2. Identify the general principles that dictate when revenue should be recorded. How did North Face violate those rules?

3. Evaluate the actions of Deloitte Touche first proposing an audit adjustment on the $1.64 million balance of the December 29, 1997, transaction with the barter company and then passing on the adjustment based on it not having a material effect on the financial statements. In this regard, should auditors conceal materiality levels from audit clients?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

18

Comment on the statement that what a company's income statement reveals is interesting, but what it conceals is vital.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

19

Beazer Homes

Questions

1. What role did organizational ethics play in the Beazer Homes fraud? Is this something the auditors of Deloitte should have been more conscious of? Explain.

2. Evaluate Beazer's accounting for cost-to-complete reserves from a GAAP perspective. Was the initial accounting for the reserve in conformity with GAAP? What was the company trying to achieve with its accounting?

3. Categorize the accounting devices used by Beazer into one the financial shenanigan groupings. Include a discussion of how earnings were managed in each case.

4. Assume you were hired to analyze the information in this case and write a two- to three-page report on your findings. Discuss each element of the fraud and why Beazer, Rand, and/or Deloitte violated ethical and professional standards.

Questions

1. What role did organizational ethics play in the Beazer Homes fraud? Is this something the auditors of Deloitte should have been more conscious of? Explain.

2. Evaluate Beazer's accounting for cost-to-complete reserves from a GAAP perspective. Was the initial accounting for the reserve in conformity with GAAP? What was the company trying to achieve with its accounting?

3. Categorize the accounting devices used by Beazer into one the financial shenanigan groupings. Include a discussion of how earnings were managed in each case.

4. Assume you were hired to analyze the information in this case and write a two- to three-page report on your findings. Discuss each element of the fraud and why Beazer, Rand, and/or Deloitte violated ethical and professional standards.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

20

Maines and Wahlen 94 state in their research paper on the reliability of accounting information:" Accrual estimates require judgment and discretion, which some firms under certain incentive conditions will exploit to report non-neutral accruals estimates within GAAP. Accounting standard scan enhance the information in accrual estimates by linking them to the underlying economic constructs they portray." Explain what the authors meant by this statement with respect to the possible existence of earnings management.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

21

Krispy Kreme was involved in an accounting fraud where the company reported false quarterly and annual earnings and falsely claimed that, as a result of those earnings, it had achieved what had become a prime benchmark of its historical performance, that is, reporting quarterly earnings per share that exceeded its previously announced EPS guidance by 1¢. One method used to report higher earnings was to ship two or three times more doughnuts to franchisees than ordered in order to meet monthly quotas. Would you characterize what Krispy Kreme did as earnings management? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

22

Safety-Kleen issued a major financial restatement in 2001. The next year, the company restated(reduced) previously reported net income by $534 million for the period 1997-1999. PwC withdrew its financial statement audit reports for those years. Do you believe that financial restatements and withdrawing an audit report are prima facie indicators that a failed audit has occurred? Explain.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

23

Revenue recognition in the Xerox case called for determining the stand-alone selling price for each of the deliverables and using it to separate out the revenue amounts. Why do you think it is important to separate out the selling prices of each element of a bundled transaction? How do these considerations relate to what Xerox did to manage its earnings? Do you think the new revenue recognition standard will change the criteria in accounting for transactions like at Xerox?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

24

Tinseltown Construction just received a $2 billion contract to construct a modern football stadium in the City of Industry, located in southern California, for a new National Football League (NFL)team called the Los Angeles Devils of Industry. The company estimates that it will cost $1.5 billion to construct the stadium. Explain how Tinseltown can make revenue recognition decisions each year that enable it to manage earnings over the three-year duration of the contract.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

25

Explain how a company might use the accounting rules for impairment of long-lived assets to manage earnings.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

26

The SEC's new rules on posting financial information on social media sites such as Twitter means that companies can now tweet their earnings in 140 characters or less. What are the problems that may arise in using a social media platform to report key financial data including the potential effects on shareholders and the company?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

27

Do you agree with each of the following statements? Explain.

• EBITDA makes companies with asset-heavy balance sheets look healthier than they may actually be.

• EBITDA portrays a company's debt service ability- but only some types of debt.

• EBITDA isn't a determinant of cash flow at all.

• EBITDA makes companies with asset-heavy balance sheets look healthier than they may actually be.

• EBITDA portrays a company's debt service ability- but only some types of debt.

• EBITDA isn't a determinant of cash flow at all.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

28

Critics of IFRS argue that the more principles-based standards are not as precise as, and therefore easier to manipulate than, the more rules-based GAAP. The reason for this is that IFRS requires more professional judgment from both auditors and corporate accountants with regard to the practical application of the rules. The application of professional judgment opens the door to increased opportunities for earnings management. Do you agree with these concerns expressed about principles-based IFRS? Relate your discussion to the research results discussed in this chapter.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

29

In the Enron case, the company eventually turned to "back-door" guaranteeing of the debt of Chewco, one of its SPEs, to satisfy equity investors. Assume that a $16 million loan agreement required that Enron stock should not fall below $40 per share. If the share price did decline below that trigger amount, either the loan would be called by the bank or the bank could choose to increase the guaranteed number of Enron shares based on the new price (assume $32). If the bank decides to increase the number of shares guaranteed, what would be (1) the original number of shares in the guarantee and (2) the new number of shares? Why would it be important from an accounting and ethical perspective for Enron to disclose information about the guarantee in its financial statements?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

30

In the study of earnings quality by Dichev et al. 95 , CFOs stated that "current earnings are considered to be high quality if they serve as a good guide to the long-run profits of the firm." Discuss how and why current earnings may not be a good barometer of the long-term profits of the firm.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

31

The auditor of Beastie Company is reviewing the following client information for the prior year ended December 31, 2015, and all four quarters of 2016.

Characterize the accruals as discretionary or nondiscretionary. What are the potential issues that the auditors should address given these numbers?

Characterize the accruals as discretionary or nondiscretionary. What are the potential issues that the auditors should address given these numbers?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

32

Explain the meaning of the following two statements and why each may be true:

a. Where management does not try to manipulate earnings, there is a positive effect on earnings quality.

b. The absence of earnings management does not, however, guarantee high earnings quality.

a. Where management does not try to manipulate earnings, there is a positive effect on earnings quality.

b. The absence of earnings management does not, however, guarantee high earnings quality.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

33

Big Pharma has been criticized for making deals that may bring harm to shareholder interests. Evaluate the following transaction from earnings management and ethical perspectives: A pharmaceutical drug company agreed to make payments to wholesalers if they bought drugs they did not need. The company paid $66 million to wholesalers who then "bought" $720 million of the company's drugs for which no customers existed.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

34

In well-governed companies, a sense of accountability and ethical leadership create a culture that places organizational ethics above all else. What role does organizational culture play in preventing financial shenanigans from being used to manage earnings?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

35

Evaluate the following statement: Do the ends of positive organizational consequences justify the means of earnings management?

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 35 flashcards in this deck.