Deck 9: Materiality and Audit Evidence

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

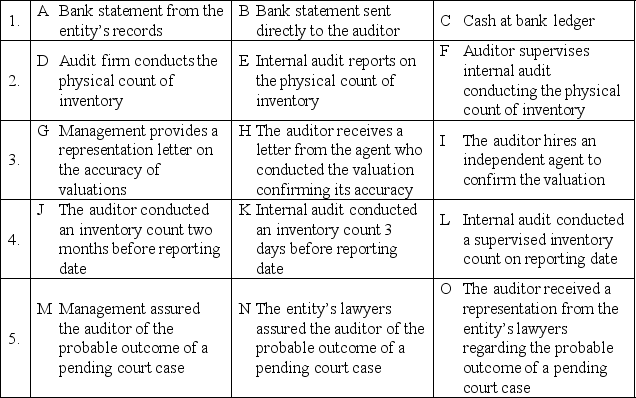

For each of the following combinations of audit evidence, rank the items in terms of their reliability:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/34

Play

Full screen (f)

Deck 9: Materiality and Audit Evidence

1

The recorded balance in an account generally represents:

A)the upper limit on the amount by which it may be overstated.

B)the lower limit on the amount by which it may be overstated.

C)the upper limit on the amount by which it may be understated.

D)the lower limit on the amount by which it may be understated.

A)the upper limit on the amount by which it may be overstated.

B)the lower limit on the amount by which it may be overstated.

C)the upper limit on the amount by which it may be understated.

D)the lower limit on the amount by which it may be understated.

A

2

Which of the following would not be considered underlying accounting data?

A)Related accounting manuals.

B)Books of original entry.

C)The general ledger.

D)Sales invoices.

A)Related accounting manuals.

B)Books of original entry.

C)The general ledger.

D)Sales invoices.

D

3

An auditor has obtained an understanding of the internal control structure and has decided that the appropriate controls are ineffective.The most appropriate audit strategy is:

A)the lower assessed level of control risk approach.

B)the predominantly substantive approach.

C)a combination of the lower assessed level of control risk approach and the predominantly substantive approach.

D)the analytical procedures approach.

A)the lower assessed level of control risk approach.

B)the predominantly substantive approach.

C)a combination of the lower assessed level of control risk approach and the predominantly substantive approach.

D)the analytical procedures approach.

B

4

All else being equal, as the level of materiality decreases, the amount of evidence required will:

A)decrease.

B)increase.

C)change in an unpredictable fashion.

D)remain the same.

A)decrease.

B)increase.

C)change in an unpredictable fashion.

D)remain the same.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

5

In general, as an account balance decreases, the amount of evidence required will:

A)increase.

B)decrease.

C)remain the same.

D)change in an unpredictable fashion.

A)increase.

B)decrease.

C)remain the same.

D)change in an unpredictable fashion.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

6

In planning the audit, the auditor should assess materiality at two levels:

A)the preliminary level and the final level.

B)the company level and the divisional level.

C)the financial report level and the account balance level.

D)the account balance level and the transaction level.

A)the preliminary level and the final level.

B)the company level and the divisional level.

C)the financial report level and the account balance level.

D)the account balance level and the transaction level.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

7

The completeness assertion would be violated if:

A)the allowance for doubtful accounts was understated.

B)unbilled shipments had occurred during the period.

C)the balance of accounts payable was overstated.

D)all of the above would violate the completeness assertion.

A)the allowance for doubtful accounts was understated.

B)unbilled shipments had occurred during the period.

C)the balance of accounts payable was overstated.

D)all of the above would violate the completeness assertion.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

8

During the audit of XYZ Ltd the auditor found a misstatement that equated to 7% of the base amount.Based on historical practice, this amount is deemed to be:

A)a matter of professional judgement whether it is considered material.

B)material.

C)not material.

D)none of the above.

A)a matter of professional judgement whether it is considered material.

B)material.

C)not material.

D)none of the above.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

9

The auditor has determined that, as the assessment of control risk is high, the audit strategy adopted will be the predominantly substantive approach.What is the cost of this audit likely to be?

A)Low.

B)Moderate.

C)High.

D)Cannot be determined.

A)Low.

B)Moderate.

C)High.

D)Cannot be determined.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is not a course of action an auditor may take if they discover material misstatements in the accounts?

A)Consider issuing an unqualified audit opinion.

B)Consider issuing a qualified audit opinion.

C)Perform additional audit procedures.

D)Ask management to correct the errors.

A)Consider issuing an unqualified audit opinion.

B)Consider issuing a qualified audit opinion.

C)Perform additional audit procedures.

D)Ask management to correct the errors.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

11

"Tolerable error" (or tolerable misstatement) is the term used to indicate materiality at the:

A)balance sheet level.

B)income statement level.

C)account balance level.

D)transactions level.

A)balance sheet level.

B)income statement level.

C)account balance level.

D)transactions level.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

12

Which of these would not be considered corroborating information?

A)The accountant's work sheet.

B)Cancelled cheques held by the client.

C)Confirmation from vendors.

D)Oral evidence obtained from client personnel.

A)The accountant's work sheet.

B)Cancelled cheques held by the client.

C)Confirmation from vendors.

D)Oral evidence obtained from client personnel.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

13

On each engagement, the specific audit objectives will normally be:

A)the same for all clients in the same industry.

B)equal to the number of categories of management's financial report assertions.

C)similar for all clients in the same industry.

D)tailored to fit the individual client.

A)the same for all clients in the same industry.

B)equal to the number of categories of management's financial report assertions.

C)similar for all clients in the same industry.

D)tailored to fit the individual client.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

14

Qualitative factors are applicable to materiality levels for particular classes of transactions, account balances or disclosures.The auditor considers the nature and other related matters of the items that might give risk to the risk of material misstatement such as:

A)the circumstances of the entity.

B)the applicable financial reporting framework.

C)qualitative disclosures that are important to users of the financial report because of the nature of the entity.

D)all of the above.

A)the circumstances of the entity.

B)the applicable financial reporting framework.

C)qualitative disclosures that are important to users of the financial report because of the nature of the entity.

D)all of the above.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

15

Assertions about account balances and related disclosures include all of the following except:

A)occurrence.

B)completeness.

C)rights and obligations.

D)classification.

A)occurrence.

B)completeness.

C)rights and obligations.

D)classification.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

16

In determining the sufficiency of evidential matter, which of the following would not normally be a factor?

A)Materiality of the account.

B)Audit risk.

C)The sampling technique used.

D)The size of the population.

A)Materiality of the account.

B)Audit risk.

C)The sampling technique used.

D)The size of the population.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

17

Which of these would generally be considered the least appropriate form of evidence?

A)The auditor's computation of earnings per share.

B)Pre-numbered sales invoices prepared by the accounts receivable clerk.

C)The auditor's inspection of new machinery acquisitions for the current year where the client is a computer manufacturer.

D)Correspondence from the client's solicitor concerning litigation.

A)The auditor's computation of earnings per share.

B)Pre-numbered sales invoices prepared by the accounts receivable clerk.

C)The auditor's inspection of new machinery acquisitions for the current year where the client is a computer manufacturer.

D)Correspondence from the client's solicitor concerning litigation.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

18

The auditor has assessed control risk as high.Which of the following is not true?

A)A predominantly substantive approach will be used.

B)The extent of substantive procedures will result in a costly audit.

C)The auditor will conduct extensive tests of controls.

D)The auditor is not placing reliance on the internal controls.

A)A predominantly substantive approach will be used.

B)The extent of substantive procedures will result in a costly audit.

C)The auditor will conduct extensive tests of controls.

D)The auditor is not placing reliance on the internal controls.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

19

If the bank reconciliation is incorrect the assertion violated would be:

A)accuracy, valuation and allocation.

B)existence.

C)rights and obligations.

D)completeness.

A)accuracy, valuation and allocation.

B)existence.

C)rights and obligations.

D)completeness.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

20

In making judgements about materiality at the account balance level, the auditor must consider the relationship between it and overall materiality.This should lead the auditor to plan the audit to detect misstatements that:

A)are individually material to the statements taken as a whole.

B)are individually immaterial to the statements taken as a whole.

C)bring the cumulative total of known misstatements to the level of materiality established by management.

D)may be immaterial individually, but may aggregate with misstatements in other accounts to a material level.

A)are individually material to the statements taken as a whole.

B)are individually immaterial to the statements taken as a whole.

C)bring the cumulative total of known misstatements to the level of materiality established by management.

D)may be immaterial individually, but may aggregate with misstatements in other accounts to a material level.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

21

The subject of the auditing procedure 'observation' is least likely to be:

A)procedures.

B)inventory taking.

C)physical assets.

D)processes.

A)procedures.

B)inventory taking.

C)physical assets.

D)processes.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

22

Use of the auditing procedure 'confirmation' would normally involve all of the following except:

A)auditor control of the mailing.

B)written request and an oral response.

C)a high degree of reliability.

D)direct evidence being obtained from outsiders.

A)auditor control of the mailing.

B)written request and an oral response.

C)a high degree of reliability.

D)direct evidence being obtained from outsiders.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

23

For each of the following combinations of audit evidence, rank the items in terms of their reliability:

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

24

An auditor contacts an accounts receivable of the client directly in order to confirm the balance owing.This is an example of:

A)test of control.

B)test of details of balances.

C)tests of details of transactions.

D)analytical procedure.

A)test of control.

B)test of details of balances.

C)tests of details of transactions.

D)analytical procedure.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

25

The auditor has determined that there is a preponderance of persuasive evidence for each financial statement assertion that is material, and therefore a reasonable basis for their opinion.Which of the following would not be a possible opinion that the auditor could issue?

A)An unqualified opinion.

B)An 'except for' opinion.

C)An adverse opinion.

D)An inability to form an opinion.

A)An unqualified opinion.

B)An 'except for' opinion.

C)An adverse opinion.

D)An inability to form an opinion.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

26

The statement that is most accurate about the procedures that can be performed by computer-assisted audit techniques is:

A)they can physically check the quantity of inventory on hand.

B)they can check for the existence of non-current assets.

C)they can observe the operation of control procedures throughout the period under audit.

D)they can re-perform a variety of calculations and perform calculations and comparisons used for analytical procedures.

A)they can physically check the quantity of inventory on hand.

B)they can check for the existence of non-current assets.

C)they can observe the operation of control procedures throughout the period under audit.

D)they can re-perform a variety of calculations and perform calculations and comparisons used for analytical procedures.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

27

List and define four types of corroborating evidence.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

28

What is the purpose of tests of control?

A)To obtain an understanding of the control over assets.

B)To provide evidence as to the fairness of management's financial statement assertions.

C)To provide evidence about the effectiveness of the internal control structure, policies and procedures.

D)None of the above.

A)To obtain an understanding of the control over assets.

B)To provide evidence as to the fairness of management's financial statement assertions.

C)To provide evidence about the effectiveness of the internal control structure, policies and procedures.

D)None of the above.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

29

Which of these is not a substantive procedure?

A)Tests of controls.

B)Analytical procedures.

C)Tests of details of transactions.

D)All are substantive procedures.

A)Tests of controls.

B)Analytical procedures.

C)Tests of details of transactions.

D)All are substantive procedures.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

30

OPQ Audit Firm was planning the audit for its existing client, Alpha & Beta Corp.The audit partner was trying to determine the best audit strategy to use.Alpha & Beta Corp is a small retailing company that does not have any warehousing facilities as all stock is kept on the premises.Being small, they only have a small team of staff, which makes the separation of duties principle difficult to achieve.The preliminary tests of controls found that the internal control procedures are well designed, but not always observed due to the small amount of staff.Previous experience with this client also showed that controls were not always observed.Despite this, OPQ has never discovered a material misstatement in the accounts.

Required: determine what audit strategy should be used and justify your answer.

Required: determine what audit strategy should be used and justify your answer.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

31

Identify and explain each of the four broad categories of management's assertions about account balances.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

32

The appropriateness of audit evidence does not refer to:

A)the quality of audit evidence.

B)the quantity of audit evidence.

C)the sufficiency of the evidence with respect to the auditor's objectives.

D)the relevance and reliability of the audit evidence.

A)the quality of audit evidence.

B)the quantity of audit evidence.

C)the sufficiency of the evidence with respect to the auditor's objectives.

D)the relevance and reliability of the audit evidence.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following procedures does not involve tracing?

a.Selecting entries in the accounting records and inspecting the documentation that served as the basis for the entries.

b.Inspecting documents created when transactions were executed and determining whether that information was properly recorded in the accounting records.

c.Checking the original flow of the data through the accounting system.

d.Ensuring that data from source documents are included in the accounts.

a.Selecting entries in the accounting records and inspecting the documentation that served as the basis for the entries.

b.Inspecting documents created when transactions were executed and determining whether that information was properly recorded in the accounting records.

c.Checking the original flow of the data through the accounting system.

d.Ensuring that data from source documents are included in the accounts.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

34

'The auditor shall obtain sufficient appropriate audit evidence to be able to draw reasonable conclusions on which to base the auditor's opinion' - ASA 500 (ISA 500).

Identify the factors that may affect the sufficiency and appropriateness of audit evidence and briefly explain how they impact on these criteria.

Identify the factors that may affect the sufficiency and appropriateness of audit evidence and briefly explain how they impact on these criteria.

Unlock Deck

Unlock for access to all 34 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 34 flashcards in this deck.