Deck 3: Professional Ethics, Regulation and Liability

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

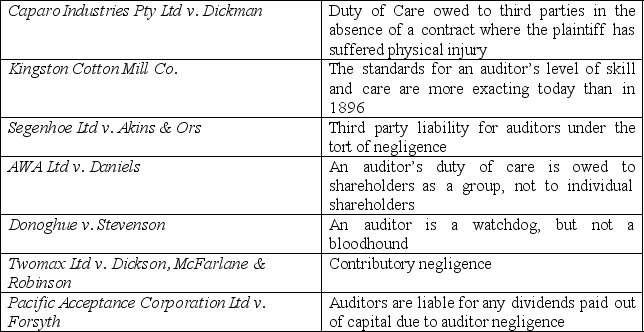

Match the case with the ruling:

Cases: Rulings:

Cases: Rulings:

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/67

Play

Full screen (f)

Deck 3: Professional Ethics, Regulation and Liability

1

Threats to auditor independence can come from various sources.Which of these is referred to in the Code of Ethics as a self-review threat?

A)The possibility of potential employment with the audit client.

B)Preparation of original data used to generate a financial statement that is the subject matter of the audit engagement.

C)Concern on the part of the auditor about the possibility of losing the engagement.

D)Pressure to reduce inappropriately the extent of work performed in order to reduce fees.

A)The possibility of potential employment with the audit client.

B)Preparation of original data used to generate a financial statement that is the subject matter of the audit engagement.

C)Concern on the part of the auditor about the possibility of losing the engagement.

D)Pressure to reduce inappropriately the extent of work performed in order to reduce fees.

B

2

Which of these jeopardises audit independence?

A)Extensive educational requirements for entry into the profession.

B)Monitoring and disciplinary procedures.

C)Familiarity with a client and their systems.

D)None of the above would jeopardise audit independence.

A)Extensive educational requirements for entry into the profession.

B)Monitoring and disciplinary procedures.

C)Familiarity with a client and their systems.

D)None of the above would jeopardise audit independence.

C

3

What is not a category of safeguards that can be used by professional accountants?

A)Safeguards created by the profession, by legislation or by regulation.

B)Safeguards developed by CALDB.

C)Safeguards which are engagement specific.

D)Safeguards within the client's systems.

A)Safeguards created by the profession, by legislation or by regulation.

B)Safeguards developed by CALDB.

C)Safeguards which are engagement specific.

D)Safeguards within the client's systems.

B

4

The fundamental ethical characteristics required of professional accountants are:

A)competence, objectivity and integrity.

B)professionalism, experience and expertise.

C)self-interest, self-review and familiarity.

D)authority, community sanction and knowledge.

A)competence, objectivity and integrity.

B)professionalism, experience and expertise.

C)self-interest, self-review and familiarity.

D)authority, community sanction and knowledge.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

5

The purpose of ethical decision making models is to:

A)direct the auditor on which action to take.

B)help the auditor arrive at a well-informed and ethical decision.

C)supplement the code of ethics.

D)identify the appropriate standard to use.

A)direct the auditor on which action to take.

B)help the auditor arrive at a well-informed and ethical decision.

C)supplement the code of ethics.

D)identify the appropriate standard to use.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

6

John resigned from an assurance engagement because his independence was impaired.He was concerned that if he did not resign then ASIC would have a case against the firm and its reputation would suffer as a result.This is an example of:

A)consequentialism.

B)non-consequentialism.

C)virtue ethics.

D)ethical relativism.

A)consequentialism.

B)non-consequentialism.

C)virtue ethics.

D)ethical relativism.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

7

The word 'ethics' is derived from the Greek word ethos, meaning character.Which of these is not a doctrine or theory of ethics?

A)Consequentialism.

B)Theology.

C)Utilitarianism.

D)Deontology.

A)Consequentialism.

B)Theology.

C)Utilitarianism.

D)Deontology.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

8

The conceptual approach to independence requires that there is:

A)independence in mind and actions.

B)independence in fact and appearance.

C)independence in mind and appearance.

D)independence in actions and appearance.

A)independence in mind and actions.

B)independence in fact and appearance.

C)independence in mind and appearance.

D)independence in actions and appearance.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

9

In relation to specific threats to auditor independence, taxation services supplied to audit clients:

A)create a threat.

B)generally not seen to create a threat.

C)create a threat only in public practice.

D)create a threat if they are performed by a subsidiary.

A)create a threat.

B)generally not seen to create a threat.

C)create a threat only in public practice.

D)create a threat if they are performed by a subsidiary.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

10

Which of these bodies in Australia established a code of professional conduct?

A)AARF and AASB.

B)ASIC and CALDB.

C)CAANZ and CPA Australia.

D)APESB

A)AARF and AASB.

B)ASIC and CALDB.

C)CAANZ and CPA Australia.

D)APESB

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

11

The main area of practice covered in the IFAC Code of Ethics for Professional Accountants is:

A)fundamental principles applicable to all professional accountants.

B)fundamental principles applicable to professional accountants in public practice.

C)fundamental principles applicable to professional accountants in business.

D)all the above.

A)fundamental principles applicable to all professional accountants.

B)fundamental principles applicable to professional accountants in public practice.

C)fundamental principles applicable to professional accountants in business.

D)all the above.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following would characterise a duty of a professional person?

A)Holding membership of a professional body.

B)The objective and confidential provision of their services.

C)Accepting the enforceability of the professional body's code of conduct.

D)All of the above would characterise a duty of a professional person.

A)Holding membership of a professional body.

B)The objective and confidential provision of their services.

C)Accepting the enforceability of the professional body's code of conduct.

D)All of the above would characterise a duty of a professional person.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

13

The statement about auditor independence that is true is:

A)statutory law does not recognise the need for audit independence.

B)statutory law recognises the need for audit independence.

C)all auditor appointments must be made by the shareholders in the AGM.

D)the auditor has no right to be heard at the AGM.

A)statutory law does not recognise the need for audit independence.

B)statutory law recognises the need for audit independence.

C)all auditor appointments must be made by the shareholders in the AGM.

D)the auditor has no right to be heard at the AGM.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

14

Which of these is not identified as a type of threat to compliance with the fundamental principles in the IFAC Code applicable to professional accountants in public practice?

A)Advertising.

B)Self-review.

C)Self-interest.

D)All are identified as a threat to compliance.

A)Advertising.

B)Self-review.

C)Self-interest.

D)All are identified as a threat to compliance.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

15

Threats to auditor independence can come from various sources.Which of these is referred to in the Code of Ethics as a self-interest threat?

A)A loan or guarantee from an officer of an assurance client to the auditor.

B)Undue dependence of the audit firm on total fees from an assurance client.

C)Long association of a senior member of an assurance team with the assurance client.

D)a and b.

A)A loan or guarantee from an officer of an assurance client to the auditor.

B)Undue dependence of the audit firm on total fees from an assurance client.

C)Long association of a senior member of an assurance team with the assurance client.

D)a and b.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

16

According to Greenwood which of these is not necessarily an attribute of a profession?

A)Self-regulation.

A)A culture.

B)Community sanction.

D)Authority.

A)Self-regulation.

A)A culture.

B)Community sanction.

D)Authority.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

17

Using the same senior personnel on an assurance engagement over a long period may create what type of threat to audit independence?

A)Advocacy.

B)Intimidation.

C)Familiarity.

D)Self-interest.

A)Advocacy.

B)Intimidation.

C)Familiarity.

D)Self-interest.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

18

The view that ethics is not just a matter of what people do but what people are, is known as:

A)teleology.

B)consequentialism.

C)virtue ethics.

D)ethical relativism.

A)teleology.

B)consequentialism.

C)virtue ethics.

D)ethical relativism.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

19

The significance of economic, financial or other relationships in determining independence in appearance is evaluated by:

A)what a reasonable and informed third party would conclude as unacceptable.

B)what the auditor general decides is significant.

C)what the auditor believes is unacceptable.

D)what the company deems to be unacceptable.

A)what a reasonable and informed third party would conclude as unacceptable.

B)what the auditor general decides is significant.

C)what the auditor believes is unacceptable.

D)what the company deems to be unacceptable.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

20

Which of these views consider moral values to be relative in regard to a particular environment?

A)Teleology.

B)Deontology.

C)Virtue ethics.

D)Ethical relativism.

A)Teleology.

B)Deontology.

C)Virtue ethics.

D)Ethical relativism.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

21

In respect of the provision of auditing services, the auditor will be liable to compensate the plaintiff if:

A)a duty of care is owed to the plaintiff.

B)the audit is negligently performed or the opinion negligently given.

C)the plaintiff has suffered a quantifiable loss as a result of the auditor's negligence.

D)all of the above.

A)a duty of care is owed to the plaintiff.

B)the audit is negligently performed or the opinion negligently given.

C)the plaintiff has suffered a quantifiable loss as a result of the auditor's negligence.

D)all of the above.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

22

As a result of the rulings in Kingston Cotton Mill and the London and General Bank cases:

A)overall audit quality improved.

B)too literal an interpretation has retarded the development of improved auditing practices.

C)auditors stopped designing procedures that would detect fraud.

D)auditors became more vigilant in the detection of fraud.

A)overall audit quality improved.

B)too literal an interpretation has retarded the development of improved auditing practices.

C)auditors stopped designing procedures that would detect fraud.

D)auditors became more vigilant in the detection of fraud.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

23

What is the term used when a failure on the part of a plaintiff to meet certain required standards of care is a factor leading to a loss by the plaintiff?

A)Damages.

B)Negligence.

C)Contributory negligence.

D)Reasonable foreseeability.

A)Damages.

B)Negligence.

C)Contributory negligence.

D)Reasonable foreseeability.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

24

The two cases that formed the basis for most subsequent decisions as to the determination of auditor negligence were:

A)JEB Fasteners and Twomax.

B)Caparo Industries and Esanda.

C)Hedley Byrne and AWA.

D)Kingston Cotton Mill and London and General Bank.

A)JEB Fasteners and Twomax.

B)Caparo Industries and Esanda.

C)Hedley Byrne and AWA.

D)Kingston Cotton Mill and London and General Bank.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

25

Which of these would not be a basis for disciplinary action by the National Council of the CPA Australia?

A)An auditor failed to observe a proper standard of professional care and skill.

B)An auditor has become insolvent under administration.

C)An auditor has breached the By-Laws of the CPA Australia.

D)An auditor has resigned due to a dispute with a client over accounting policies.

A)An auditor failed to observe a proper standard of professional care and skill.

B)An auditor has become insolvent under administration.

C)An auditor has breached the By-Laws of the CPA Australia.

D)An auditor has resigned due to a dispute with a client over accounting policies.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

26

In an audit engagement, which of the following would be considered to be one stage removed from the privity of contract?

A)The auditor.

B)Future creditors.

C)Shareholders.

D)The company.

A)The auditor.

B)Future creditors.

C)Shareholders.

D)The company.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

27

The landmark case for the principle of contributory negligence is:

A)Segenhoe Ltd.

B)Pacific Acceptance.

C)AWA Ltd.

D)Kingston Cotton Mill.

A)Segenhoe Ltd.

B)Pacific Acceptance.

C)AWA Ltd.

D)Kingston Cotton Mill.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

28

The party that is unable to sue the auditors under contract law is:

A)the directors (on behalf of the company).

B)the liquidator.

C)individual shareholders.

D)the receiver.

A)the directors (on behalf of the company).

B)the liquidator.

C)individual shareholders.

D)the receiver.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

29

The more exacting auditor responsibility showing the evolving expectations in respect to higher standards of reasonable care was set forth in the:

A)London and General Bank case.

B)Pacific Acceptance case.

C)Kingston Cotton Mills case.

D)Donoghue v Stevenson case.

A)London and General Bank case.

B)Pacific Acceptance case.

C)Kingston Cotton Mills case.

D)Donoghue v Stevenson case.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

30

Which of these is not a primary element of a fiduciary relationship?

A)The fiduciary has undertaken to act in the interests of another.

B)The fiduciary is properly certified.

C)The person to whom the fiduciary duty is owed is vulnerable to the fiduciary's abuse of his or her position.

D)All of the above are primary elements of a fiduciary relationship.

A)The fiduciary has undertaken to act in the interests of another.

B)The fiduciary is properly certified.

C)The person to whom the fiduciary duty is owed is vulnerable to the fiduciary's abuse of his or her position.

D)All of the above are primary elements of a fiduciary relationship.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

31

The term 'privity of contract' refers to:

A)the contractual relationship that exists between two or more contracting parties.

B)the fact that an audit is to be performed in accordance with professional standards.

C)the fact that an auditor appointed to conduct a statutory audit cannot reduce their liability by contract .

D)the mandatory requirement that there must be an engagement letter setting out the terms of the audit contract.

A)the contractual relationship that exists between two or more contracting parties.

B)the fact that an audit is to be performed in accordance with professional standards.

C)the fact that an auditor appointed to conduct a statutory audit cannot reduce their liability by contract .

D)the mandatory requirement that there must be an engagement letter setting out the terms of the audit contract.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

32

Which case prompted the development of more specific and comprehensive Auditing Standards in Australia?

A)McKesson and Robbins.

B)Pacific Acceptance.

C)Cambridge Credit.

D)AWA.

A)McKesson and Robbins.

B)Pacific Acceptance.

C)Cambridge Credit.

D)AWA.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

33

In Segenhoe Ltd, the company claimed that the auditors' negligence caused them to pay a dividend out of capital.What was the outcome of this case?

A)The auditors were found to be liable for the dividends.

B)The shareholders were ordered to return the dividends.

C)The company lost as there was no causal relationship.

D)The company was found to have contributed to the negligence.

A)The auditors were found to be liable for the dividends.

B)The shareholders were ordered to return the dividends.

C)The company lost as there was no causal relationship.

D)The company was found to have contributed to the negligence.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following is true regarding damages?

A)Damages are only available under tort.

B)Damages are available under tort and contract.

C)Damages are limited to the audit fees paid.

D)Damages are unquantifiable.

A)Damages are only available under tort.

B)Damages are available under tort and contract.

C)Damages are limited to the audit fees paid.

D)Damages are unquantifiable.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

35

A possible form of discipline not found in CPA Australia's Articles of Association for members failing to meet required standards is:

A)fines.

B)imprisonment.

C)forfeiture of membership.

D)suspension from membership.

A)fines.

B)imprisonment.

C)forfeiture of membership.

D)suspension from membership.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

36

The so-called 'deep-pockets' theory in relation to alleged audit failures, refers to:

A)the auditor being the only party left with sufficient funds to indemnify the plaintiff's losses.

B)the requirement to hold a public practice certificate.

C)several widely-reported business failures that resulted in significant loss to investors.

D)the gap between the potential liability and the available insurance cover.

A)the auditor being the only party left with sufficient funds to indemnify the plaintiff's losses.

B)the requirement to hold a public practice certificate.

C)several widely-reported business failures that resulted in significant loss to investors.

D)the gap between the potential liability and the available insurance cover.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

37

The judgement in the Pacific Acceptance case was wide-ranging and covered procedures that should exist in a normally competent audit.Which of the following is not accurate concerning procedures listed in the judgement?

A)Promptly report fraud or warn of suspicion of fraud whether material or not.

B)Closely supervise and review the work of inexperienced staff.

C)Be very wary about reporting bad news to shareholders always keeping in mind it can affect the value of their investment.

D)Audit the whole of the year, not just the year-end balances.

A)Promptly report fraud or warn of suspicion of fraud whether material or not.

B)Closely supervise and review the work of inexperienced staff.

C)Be very wary about reporting bad news to shareholders always keeping in mind it can affect the value of their investment.

D)Audit the whole of the year, not just the year-end balances.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

38

Which case laid down the fundamental auditing principles of the 'watchdog' role and the notion of taking reasonable skill and care?

A)Kingston Cotton Mill.

B)Pacific Acceptance.

C)AWA.

D)London and General Bank.

A)Kingston Cotton Mill.

B)Pacific Acceptance.

C)AWA.

D)London and General Bank.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

39

In an audit engagement, which of the following would be considered to be two stages removed from the privity of contract?

A)The company.

B)The auditor.

C)Shareholders.

D)Future creditors.

A)The company.

B)The auditor.

C)Shareholders.

D)Future creditors.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

40

Auditors are accountable in law for their professional conduct.This accountability arises under:

A)Tort law.

B)Common law.

C)Statute law.

D)all of the above.

A)Tort law.

B)Common law.

C)Statute law.

D)all of the above.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

41

A.Explain the impact that the Pacific Acceptance case had on existing auditing practice.

B.List four of the procedures or practices that were identified in the ruling as being part of a competent audit.

B.List four of the procedures or practices that were identified in the ruling as being part of a competent audit.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

42

Classify each of the following threats as either; self-interest, self-review, advocacy, familiarity or intimidation.

1 The CEO threatens to change auditors unless an unqualified opinion is issued

2 Each member of the audit team received a holiday cruise as a gift from the client

3 The audit partner owns a significant amount of shares in the client company

4 The audit partner is the brother-in-law of the client company's director

5 The audit firm is promoting a new issue of shares from the client company

6 The audit firm is acting as an advocate on behalf of the client in a dispute with a third party

7 Management is pressuring the firm to reduce its audit hours in order to reduce the fees

8 The audit partner has been approached about becoming a board member with the client company next year

9 A member of the audit team was recently a director of the client company

10 The audit must cover an inventory valuation system which was implemented by the audit firm after last year's audit.

1 The CEO threatens to change auditors unless an unqualified opinion is issued

2 Each member of the audit team received a holiday cruise as a gift from the client

3 The audit partner owns a significant amount of shares in the client company

4 The audit partner is the brother-in-law of the client company's director

5 The audit firm is promoting a new issue of shares from the client company

6 The audit firm is acting as an advocate on behalf of the client in a dispute with a third party

7 Management is pressuring the firm to reduce its audit hours in order to reduce the fees

8 The audit partner has been approached about becoming a board member with the client company next year

9 A member of the audit team was recently a director of the client company

10 The audit must cover an inventory valuation system which was implemented by the audit firm after last year's audit.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

43

The decision in the Caparo case (1990) reduced the duty of care of auditors to:

A)all users known to the auditor.

B)all users that ought reasonably to have been known to the auditor.

C)the shareholders as a group.

D)all users of the financial statements, except for investors.

A)all users known to the auditor.

B)all users that ought reasonably to have been known to the auditor.

C)the shareholders as a group.

D)all users of the financial statements, except for investors.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

44

Katie is part of an audit team who have been sent to Eastern Europe to conduct an audit of one of their client's subsidiary companies.During the audit, Katie uncovers a series of bribes that the company has paid to local authorities.Bribes are considered a normal part of business in this particular city so the subsidiary company feels as though they have done nothing wrong.It is likely that the bribes will not be uncovered but there is a chance that they will be, and that the parent company, the audit firm, and Katie personally will all suffer negative consequences if they are.If Katie does report the bribes, then the subsidiary company will suffer and there will be a scandal for the parent company.However, the impact of reporting the bribes is likely to be less than if they are discovered at a later date by other authorities.Katie thinks of herself as an honest person and is trying to decide what the ethically 'right' thing to do is.

Try to determine what decision Katie will make regarding whether or not she will report the bribes by applying the ethical theories of teleology, deontology, virtue ethics, and ethical relativism.

Try to determine what decision Katie will make regarding whether or not she will report the bribes by applying the ethical theories of teleology, deontology, virtue ethics, and ethical relativism.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

45

Which case does not appear to support the recent narrowing of the exposure of auditors to third parties?

A)Lowe Lippmann.

B)Esanda Finance.

C)Royal Bank of Scotland.

D)Columbia Coffee.

A)Lowe Lippmann.

B)Esanda Finance.

C)Royal Bank of Scotland.

D)Columbia Coffee.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

46

The outcome in the Hedley Byrne case was:

A)the bank was not found liable as no duty of care was owed.

B)the advertising agency was found to have contributed to the loss.

C)the bank was found liable for the loss.

D)the bank was not found liable due to the disclaimer.

A)the bank was not found liable as no duty of care was owed.

B)the advertising agency was found to have contributed to the loss.

C)the bank was found liable for the loss.

D)the bank was not found liable due to the disclaimer.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

47

Independence is made up of independence in mind and independence in appearance.Describe these two aspects of independence.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

48

Describe three different ethical theories.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

49

Identify the six threats to compliance with the IFAC code by professional accountants in public practice and give an example of each.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

50

Which of these precautions taken by auditors would avoid or minimise the consequences of litigation?

A)Using an engagement letter for all professional services offered by the firm.

B)Thoroughly investigating all potential clients before accepting an engagement.

C)Ensuring professional pronouncements are fully complied with by the firm.

D)All the above.

A)Using an engagement letter for all professional services offered by the firm.

B)Thoroughly investigating all potential clients before accepting an engagement.

C)Ensuring professional pronouncements are fully complied with by the firm.

D)All the above.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

51

To determine risks and potential exposure to litigation, professional accountants commonly use an inspection program.An inspection program should be flexible and could contain:

A)routine inspection of all risks.

B)routine inspection of a particular area of risk.

C)inspections as a result of incidents or accidents.

D)all of the above.

A)routine inspection of all risks.

B)routine inspection of a particular area of risk.

C)inspections as a result of incidents or accidents.

D)all of the above.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

52

Under the Hedley Byrne principle, auditors' liability to third parties to whom they owe a duty of care:

A)is no different from their liability to their clients.

B)is more onerous than their liability to their clients.

C)does not exist.

D)none of the above.

A)is no different from their liability to their clients.

B)is more onerous than their liability to their clients.

C)does not exist.

D)none of the above.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

53

For each of the following safeguards, identify whether they are:

safeguards created by the profession, by legislation or by regulation

safeguards developed by the firm

safeguards which are engagement specific

safeguards within the client's systems.

1 disclosure of fees

2 competence of employees

3 using different partners and teams with separate reporting lines for the provision of non-assurance services to an assurance client

4 professional standards and pronouncements

5 timely communication of policies and procedures to all partners and professional staff

6 internal procedures to ensure objective decisions on engagements

7 professional review by other professional accountants

8 involving another firm to perform or re-perform part of the engagement

9 corporate or other governance regulations

10 firm leadership which emphasises compliance and ethics.

safeguards created by the profession, by legislation or by regulation

safeguards developed by the firm

safeguards which are engagement specific

safeguards within the client's systems.

1 disclosure of fees

2 competence of employees

3 using different partners and teams with separate reporting lines for the provision of non-assurance services to an assurance client

4 professional standards and pronouncements

5 timely communication of policies and procedures to all partners and professional staff

6 internal procedures to ensure objective decisions on engagements

7 professional review by other professional accountants

8 involving another firm to perform or re-perform part of the engagement

9 corporate or other governance regulations

10 firm leadership which emphasises compliance and ethics.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

54

Why has the reaction to the verdict in Caparo Industries generally been unfavourable?

A)It is strongly thought that the loss was not quantifiable.

B)The verdict appears to treat auditors more favourably than it treats other experts on whom third parties rely.

C)The principle of proximity was not sufficiently established.

D)It is felt that the auditors were not responsible.

A)It is strongly thought that the loss was not quantifiable.

B)The verdict appears to treat auditors more favourably than it treats other experts on whom third parties rely.

C)The principle of proximity was not sufficiently established.

D)It is felt that the auditors were not responsible.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

55

Name the elements necessary to be successful in a case of negligence and show how these were applied in the case of Twomax Ltd v.Dickson, McFarlane & Robinson.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

56

Read the following scenario and identify any threats to compliance with the IFAC Code.

ABC firm is the auditor of Company Ltd and has been for 10 years.During this time, the audit partner responsible has always been John.The other partner in the firm, Robert, has been the review auditor for this assurance engagement.Robert has not been the lead audit partner as his wife's father is the CEO of Company Ltd.

Every year Company Ltd celebrates the end of the audit by throwing an all expenses paid weekend away for their staff that worked on the audit and for the audit firm.This has led to a good relationship between the auditors and the company that makes the audit less formal.The staff all know each other well and the company believes it is money well spent.

Recently John was approached by the board of Company Ltd with an offer of employment as a director starting in two years time.The only condition was that the audit fees have to be reduced for the current and next year's audit.

ABC firm is the auditor of Company Ltd and has been for 10 years.During this time, the audit partner responsible has always been John.The other partner in the firm, Robert, has been the review auditor for this assurance engagement.Robert has not been the lead audit partner as his wife's father is the CEO of Company Ltd.

Every year Company Ltd celebrates the end of the audit by throwing an all expenses paid weekend away for their staff that worked on the audit and for the audit firm.This has led to a good relationship between the auditors and the company that makes the audit less formal.The staff all know each other well and the company believes it is money well spent.

Recently John was approached by the board of Company Ltd with an offer of employment as a director starting in two years time.The only condition was that the audit fees have to be reduced for the current and next year's audit.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

57

i.Why would audit firms provide non-assurance services to assurance clients?

ii.List four types of non-assurance services.

iii.Identify safeguards which would eliminate or reduce the threat to independence for non-assurance services.

ii.List four types of non-assurance services.

iii.Identify safeguards which would eliminate or reduce the threat to independence for non-assurance services.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

58

Which of these is not a precaution auditors take to avoid litigation?

A)Comply fully with professional pronouncements.

B)Never issue a privity letter.

C)Maintain adequate professional indemnity cover.

D)All of the above are precautions auditors take to avoid litigation.

A)Comply fully with professional pronouncements.

B)Never issue a privity letter.

C)Maintain adequate professional indemnity cover.

D)All of the above are precautions auditors take to avoid litigation.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following cases did not extend the liability of auditors in regard to the concept of proximity?

A)Shaddock and Associates.

B)Jeb Fasteners.

C)Caparo Industries.

D)Twomax.

A)Shaddock and Associates.

B)Jeb Fasteners.

C)Caparo Industries.

D)Twomax.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

60

Describe the deep-pockets theory.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

61

Why would the courts want to limit the ability of third parties to sue auditors who have been negligent? Are there any arguments that this liability should not be limited?

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

62

A.Identify who the parties are in the contractual relationship regarding an audit and what this relationship is termed.

B.Identify who may sue the auditors under contract.

B.Identify who may sue the auditors under contract.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

63

Explain how engagement letters can be used to avoid litigation.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

64

What were the causes and results of the 'hard insurance market' in Australia?

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

65

Match the case with the ruling:

Cases: Rulings:

Cases: Rulings:

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

66

The Australian case of Esanda Corporation v.Peat Marwick Hungerfords established the elements that would be necessary for a third party to succeed in an action of negligence against the auditor due to reliance on the audited accounts.Identify what these elements are.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

67

List five precautions auditors may take to avoid litigation.

Unlock Deck

Unlock for access to all 67 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 67 flashcards in this deck.