Deck 8: Government-Wide Statements, Capital Assets, Long-Term Debt

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

The following information is available for the preparation of the government-wide financial statements for the City of Southern Springs as of April 30, 2012:

From the preceding information, prepare (in good form) a Statement of Net Assets for the City of Southern Springs as of April 30, 2012. Assume that outstanding bonds were issued to acquire capital assets and restricted net assets total $554,000 for governmental activities and $215,000 for business-type activities. Include a Total column.

From the preceding information, prepare (in good form) a Statement of Net Assets for the City of Southern Springs as of April 30, 2012. Assume that outstanding bonds were issued to acquire capital assets and restricted net assets total $554,000 for governmental activities and $215,000 for business-type activities. Include a Total column.

From the preceding information, prepare (in good form) a Statement of Net Assets for the City of Southern Springs as of April 30, 2012. Assume that outstanding bonds were issued to acquire capital assets and restricted net assets total $554,000 for governmental activities and $215,000 for business-type activities. Include a Total column. Question

The following information is available for the preparation of the government-wide financial statements for the City of Northern Pines for the year ended June 30, 2012:

From the previous information, prepare, in good form, a Statement of Activities for the City of Northern Pines for the year ended June 30, 2012. Northern Pines has no component units.

From the previous information, prepare, in good form, a Statement of Activities for the City of Northern Pines for the year ended June 30, 2012. Northern Pines has no component units.

From the previous information, prepare, in good form, a Statement of Activities for the City of Northern Pines for the year ended June 30, 2012. Northern Pines has no component units. Question

The City of Grinders Switch maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations.

1. General fixed assets as of the beginning of the year, which had not been recorded, were as follows:

2. During the year, expenditures for capital outlays amounted to $6,113,000. Of that amount, $4,321,000 was for buildings; the remainder was for improvements other than buildings.

2. During the year, expenditures for capital outlays amounted to $6,113,000. Of that amount, $4,321,000 was for buildings; the remainder was for improvements other than buildings.

3. The capital outlay expenditures outlined in (2) were completed at the end of the year (and will begin to be depreciated next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 40 years; improvements other than buildings, 20 years; and equipment, 10 years.

4. In the governmental funds Statement of Revenues, Expenditures, and Changes in Fund Balances, the City reported proceeds from the sale of land in the amount of $600,000. The land originally cost $535,000.

5. At the beginning of the year, general obligation bonds were outstanding in the amount of $4,000,000. Unamortized bond premium amounted to $40,000. Note: This entry is not covered in the text, but is similar to entry 9 in the chapter.

6. During the year, debt service expenditures for the year amounted to: interest, $580,000; principal, $400,000. For purposes of government-wide statements, $4,000 of the bond premium should be amortized. No adjustment is necessary for interest accrual.

7. At year-end, additional general obligation bonds were issued in the amount of $1,200,000, at par.

1. General fixed assets as of the beginning of the year, which had not been recorded, were as follows:

2. During the year, expenditures for capital outlays amounted to $6,113,000. Of that amount, $4,321,000 was for buildings; the remainder was for improvements other than buildings.3. The capital outlay expenditures outlined in (2) were completed at the end of the year (and will begin to be depreciated next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 40 years; improvements other than buildings, 20 years; and equipment, 10 years.

4. In the governmental funds Statement of Revenues, Expenditures, and Changes in Fund Balances, the City reported proceeds from the sale of land in the amount of $600,000. The land originally cost $535,000.

5. At the beginning of the year, general obligation bonds were outstanding in the amount of $4,000,000. Unamortized bond premium amounted to $40,000. Note: This entry is not covered in the text, but is similar to entry 9 in the chapter.

6. During the year, debt service expenditures for the year amounted to: interest, $580,000; principal, $400,000. For purposes of government-wide statements, $4,000 of the bond premium should be amortized. No adjustment is necessary for interest accrual.

7. At year-end, additional general obligation bonds were issued in the amount of $1,200,000, at par.

Question

Question

Question

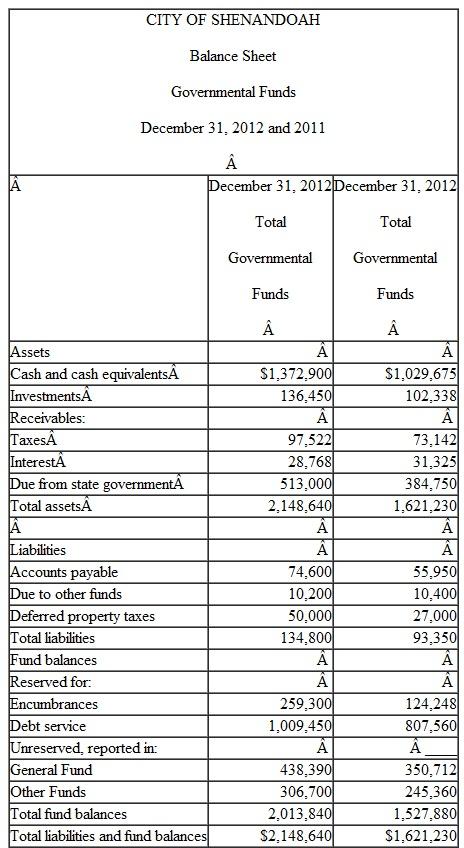

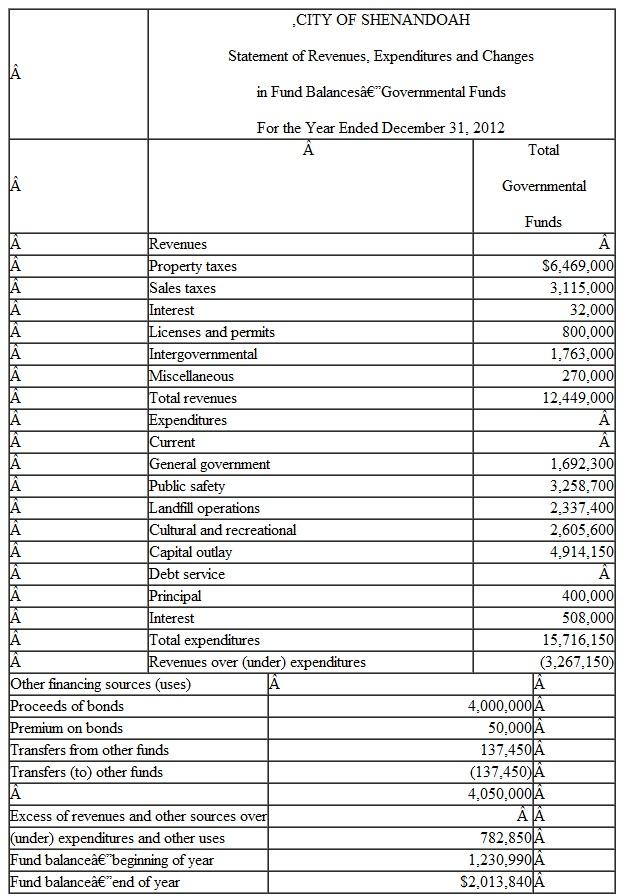

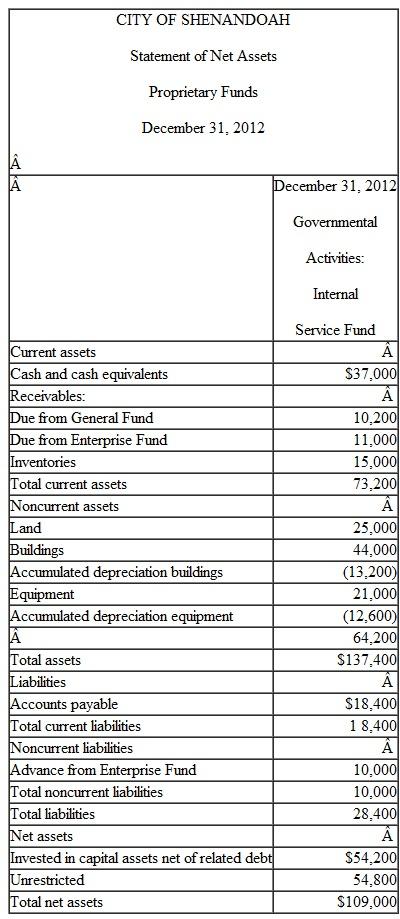

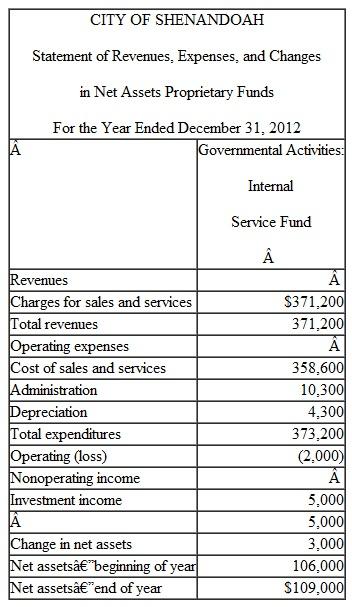

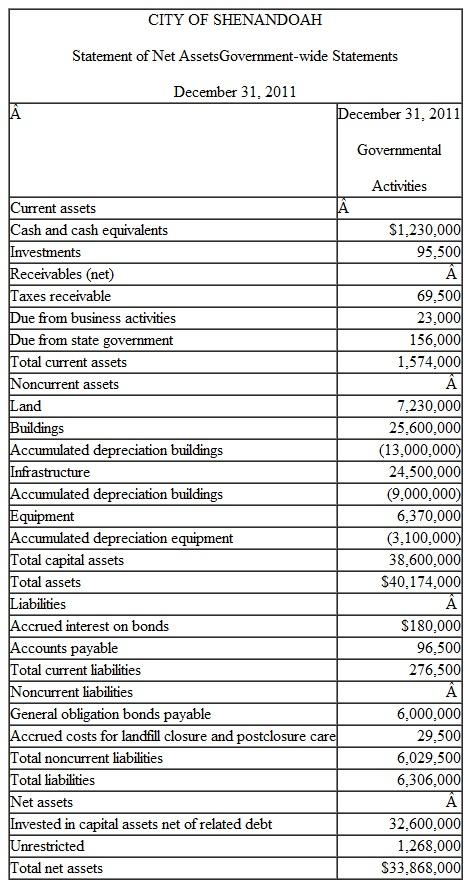

Presented on the following pages are partial financial statements for the City of Shenandoah, including:

Fiscal year 2012:

A. Total Governmental Funds:

Balance Sheet

Statement of Revenues, Expenditures, and Changes in Fund Balance

B. Internal Service Fund:

Statement of Net Assets

Statement of Revenues, Expenses, and Changes in Net Assets

Fiscal year 2011:

A. Total Governmental Funds:

Balance Sheet

B. Government-wide-Governmental Activities:

Statement of Net Assets

Additional Information

Additional Information

1. $445,600 of the capital assets purchased in fiscal year 2012 was equipment. All remaining capital acquisitions were for a new building.

2. Depreciation of general fixed assets: buildings $1,100,000, infrastructure $975,000, and equipment $537,500.

3. The City had $6,000,000 of 6 percent general obligation bonds (issued at par) outstanding at December 31, 2011. In addition, the City issued $4,000,000 of 8 percent bonds on January 2, 2012 (sold at a premium). Interest payments on both bond issues are due on January 1 and July 1. Principal payments are made on January 1. Interest and principal payments for the current year include:

The January interest payments are accrued for purposes of the government- wide statements but not the fund-basis statements. The bond premium is to be amortized in the amount of $2,500 per year.

The January interest payments are accrued for purposes of the government- wide statements but not the fund-basis statements. The bond premium is to be amortized in the amount of $2,500 per year.

4. Property taxes expected to be collected more than 60 days after year-end are deferred in the fund basis statements.

5. At the end of 2012, the accumulated liability for landfill closure and post-closure care costs is estimated to be $37,000. Landfill operations are reported in the General Fund-Public Works.

6. The internal service fund serves several departments of the General Fund, all within the category of "General Government." The internal service fund was created at the end of 2011 and had no capital assets or long-term liabilities at the end of 2011.

Prepare all worksheet journal entries necessary for fiscal year 2012 to convert the governmental fund basis amounts to the economic resources measurement focus and accrual basis required for the governmental activities sections of the government-wide statements.

Fiscal year 2012:

A. Total Governmental Funds:

Balance Sheet

Statement of Revenues, Expenditures, and Changes in Fund Balance

B. Internal Service Fund:

Statement of Net Assets

Statement of Revenues, Expenses, and Changes in Net Assets

Fiscal year 2011:

A. Total Governmental Funds:

Balance Sheet

B. Government-wide-Governmental Activities:

Statement of Net Assets

Additional Information 1. $445,600 of the capital assets purchased in fiscal year 2012 was equipment. All remaining capital acquisitions were for a new building.

2. Depreciation of general fixed assets: buildings $1,100,000, infrastructure $975,000, and equipment $537,500.

3. The City had $6,000,000 of 6 percent general obligation bonds (issued at par) outstanding at December 31, 2011. In addition, the City issued $4,000,000 of 8 percent bonds on January 2, 2012 (sold at a premium). Interest payments on both bond issues are due on January 1 and July 1. Principal payments are made on January 1. Interest and principal payments for the current year include:

The January interest payments are accrued for purposes of the government- wide statements but not the fund-basis statements. The bond premium is to be amortized in the amount of $2,500 per year.4. Property taxes expected to be collected more than 60 days after year-end are deferred in the fund basis statements.

5. At the end of 2012, the accumulated liability for landfill closure and post-closure care costs is estimated to be $37,000. Landfill operations are reported in the General Fund-Public Works.

6. The internal service fund serves several departments of the General Fund, all within the category of "General Government." The internal service fund was created at the end of 2011 and had no capital assets or long-term liabilities at the end of 2011.

Prepare all worksheet journal entries necessary for fiscal year 2012 to convert the governmental fund basis amounts to the economic resources measurement focus and accrual basis required for the governmental activities sections of the government-wide statements.

Question

Question

The fund-basis financial statements of the City of Cottonwood have been completed for the year 2012 and appear in the first tab of the Excel spreadsheet provided with this exercise. In addition, the Statement of Net Assets from the previous fiscal year is provided and should be used to determine beginning balances for accounts not appearing in the fund-basis statements. The following information is also available:

a. Capital Assets:

• Capital assets purchased by governmental funds are charged to capital expenditure and do not appear as assets in the fund-basis balance

sheet. However, the balance is reflected in the statement of net assets in the government-wide financial statements.

• Depreciation on capital assets used in governmental-type activities amounted to $2,450,000 for 2012.

• No capital assets were sold or disposed of in 2012, and all purchases are properly reflected in the fund-basis statements as capital expenditures.

b. Long-term debt

• Proceeds from bonds issued by governmental funds are reflected in other financing sources and do not appear as liabilities in the fund-basis balance sheet. Payments of principal are recognized as expenditures when due. The balance of outstanding bonds balance is reflected in the statement of net assets in the government-wide financial statements.

• Interest is recognized in the fund-basis statements only when payment is due. Interest accrued but not yet payable amounted to $107,500 at December 31, 2012. Interest accrued for purposes of the government-Wide statements in 2011 has been paid and is reflected in interest expenditure in 2012.

• There are no bond discounts or premiums.

c. Deferred Revenues

• Deferred revenues are comprised solely of property taxes expected to be collected more than 60 days after year-end. The balance of deferred taxes at the end of 2011 was $128,200 and was recognized as revenue in the fund-basis statements in 2012.

d. The City accounts for its solid waste landfill in the General Fund (public works department). The estimated liability for closure and post-closure care costs as of December 31, 2012, is $1,580,900 and appears only in the government-wide statements.

e. Transfers

• During the year, the General Fund transferred cash to the courthouse renovation, debt service, and enterprise funds.

f. The City does not operate any Internal Service Funds.

g. When entering amounts in the Statement of Activities, Charges for Services Revenue in the governmental funds is attributable to the following functions:

Required:

Required:

Use the Excel template provided to complete the following requirements; a separate tab is provided in Excel for each of these steps.

1. Prepare the journal entries necessary to convert the governmental fund financial statements to the accrual basis of accounting.

2. Post the journal entries to the conversion worksheet provided.

3. Prepare a government-wide Statement of Activities and Statement of Net Assets for the year 2012.

This is an involved problem, requiring many steps. Here are some

hints.

a. Tab 1 is information to be used in the problem. You do not enter anything here.

b. After you make the journal entries (Tab 2), post these to the worksheet to convert to the accrual basis. This worksheet is set up so that you enter debits as positive numbers and credits as negative. After you post your entries, look at the numbers below the total credit column to see that debits equal credits. If not, you probably entered a credit as a positive number.

c. Make sure that total debits equal total credits in the last column (Balances for government-wide statements).

d. When calculating Restricted Net Assets, recall that permanent fund principal is added to restricted fund balances.

a. Capital Assets:

• Capital assets purchased by governmental funds are charged to capital expenditure and do not appear as assets in the fund-basis balance

sheet. However, the balance is reflected in the statement of net assets in the government-wide financial statements.

• Depreciation on capital assets used in governmental-type activities amounted to $2,450,000 for 2012.

• No capital assets were sold or disposed of in 2012, and all purchases are properly reflected in the fund-basis statements as capital expenditures.

b. Long-term debt

• Proceeds from bonds issued by governmental funds are reflected in other financing sources and do not appear as liabilities in the fund-basis balance sheet. Payments of principal are recognized as expenditures when due. The balance of outstanding bonds balance is reflected in the statement of net assets in the government-wide financial statements.

• Interest is recognized in the fund-basis statements only when payment is due. Interest accrued but not yet payable amounted to $107,500 at December 31, 2012. Interest accrued for purposes of the government-Wide statements in 2011 has been paid and is reflected in interest expenditure in 2012.

• There are no bond discounts or premiums.

c. Deferred Revenues

• Deferred revenues are comprised solely of property taxes expected to be collected more than 60 days after year-end. The balance of deferred taxes at the end of 2011 was $128,200 and was recognized as revenue in the fund-basis statements in 2012.

d. The City accounts for its solid waste landfill in the General Fund (public works department). The estimated liability for closure and post-closure care costs as of December 31, 2012, is $1,580,900 and appears only in the government-wide statements.

e. Transfers

• During the year, the General Fund transferred cash to the courthouse renovation, debt service, and enterprise funds.

f. The City does not operate any Internal Service Funds.

g. When entering amounts in the Statement of Activities, Charges for Services Revenue in the governmental funds is attributable to the following functions:

Required: Use the Excel template provided to complete the following requirements; a separate tab is provided in Excel for each of these steps.

1. Prepare the journal entries necessary to convert the governmental fund financial statements to the accrual basis of accounting.

2. Post the journal entries to the conversion worksheet provided.

3. Prepare a government-wide Statement of Activities and Statement of Net Assets for the year 2012.

This is an involved problem, requiring many steps. Here are some

hints.

a. Tab 1 is information to be used in the problem. You do not enter anything here.

b. After you make the journal entries (Tab 2), post these to the worksheet to convert to the accrual basis. This worksheet is set up so that you enter debits as positive numbers and credits as negative. After you post your entries, look at the numbers below the total credit column to see that debits equal credits. If not, you probably entered a credit as a positive number.

c. Make sure that total debits equal total credits in the last column (Balances for government-wide statements).

d. When calculating Restricted Net Assets, recall that permanent fund principal is added to restricted fund balances.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/14

Play

Full screen (f)

Deck 8: Government-Wide Statements, Capital Assets, Long-Term Debt

1

Using the annual financial report obtained for Exercise 1-1, answer the following questions:

a. Find the reconciliation between the governmental fund balances and the governmental-type activities net assets. This might be on the governmental fund Balance Sheet or in a separate schedule in the basic financial statements. List the major differences. What is the amount shown for capital assets How much is due to the incorporation of internal service funds Was an adjustment made for deferred property taxes or any other revenue What is the adjustment due to the inclusion of long-term liabilities What other adjustments are made

b. Find the reconciliation between the governmental fund changes in fund balances and the governmental-type activities changes in net assets. This might be on the governmental Statement of Revenues, Expenditures, and Changes in Fund Balances or in a separate schedule. List the major differences. How much is due to the difference between depreciation reported on the Statement of Activities and the reported expenditures for capital outlays on the Statement of Revenues, Expenditures, and Changes in Fund Balances How much is due to differences in reporting expenditures versus expenses for debt service How much is due to the incorporation of internal service funds How much is due to differences in reporting proceeds versus gains on sale of capital assets How much is due to additional revenue accruals How much is due to additional expense accruals What other items are listed

c. Look at the Statement of Net Assets, especially the net asset section. Attempt to prove the Net Assets Invested in Capital Assets, Net of Related Debt figure from the information in the statement or the notes. List the individual items of net assets that are restricted; this might require examination of the notes to the financial statements.

d. Look at the Statement of Activities. List the net expenses (revenues) for governmental activities, business-type activities, and component units. List the change in net assets for governmental activities, business-type activities, and component units. Attempt to find from the notes the component units that are discretely presented.

e. Look throughout the annual report for disclosures related to capital assets. This would include the notes to the financial statements, any schedules, and information in the Management's Discussion and Analysis (MD A). Summarize what is included. What depreciation method is used Are lives of major classes of capital assets disclosed

f. Look throughout the annual report for disclosures related to long-term debt. This would include the notes to the financial statements, any schedules in the financial and statistical sections, and the MD A. Summarize what is included. Are the schedules listed in this chapter included What is the debt limit and margin What is the direct debt per capita The direct and overlapping debt per capita

a. Find the reconciliation between the governmental fund balances and the governmental-type activities net assets. This might be on the governmental fund Balance Sheet or in a separate schedule in the basic financial statements. List the major differences. What is the amount shown for capital assets How much is due to the incorporation of internal service funds Was an adjustment made for deferred property taxes or any other revenue What is the adjustment due to the inclusion of long-term liabilities What other adjustments are made

b. Find the reconciliation between the governmental fund changes in fund balances and the governmental-type activities changes in net assets. This might be on the governmental Statement of Revenues, Expenditures, and Changes in Fund Balances or in a separate schedule. List the major differences. How much is due to the difference between depreciation reported on the Statement of Activities and the reported expenditures for capital outlays on the Statement of Revenues, Expenditures, and Changes in Fund Balances How much is due to differences in reporting expenditures versus expenses for debt service How much is due to the incorporation of internal service funds How much is due to differences in reporting proceeds versus gains on sale of capital assets How much is due to additional revenue accruals How much is due to additional expense accruals What other items are listed

c. Look at the Statement of Net Assets, especially the net asset section. Attempt to prove the Net Assets Invested in Capital Assets, Net of Related Debt figure from the information in the statement or the notes. List the individual items of net assets that are restricted; this might require examination of the notes to the financial statements.

d. Look at the Statement of Activities. List the net expenses (revenues) for governmental activities, business-type activities, and component units. List the change in net assets for governmental activities, business-type activities, and component units. Attempt to find from the notes the component units that are discretely presented.

e. Look throughout the annual report for disclosures related to capital assets. This would include the notes to the financial statements, any schedules, and information in the Management's Discussion and Analysis (MD A). Summarize what is included. What depreciation method is used Are lives of major classes of capital assets disclosed

f. Look throughout the annual report for disclosures related to long-term debt. This would include the notes to the financial statements, any schedules in the financial and statistical sections, and the MD A. Summarize what is included. Are the schedules listed in this chapter included What is the debt limit and margin What is the direct debt per capita The direct and overlapping debt per capita

The solution to this and the first exercise of Chapters 1 through 8 will differ from student to student assuming each has a different CAFR.

2

Identify the types of nonexchange revenues that are most likely to result in differences in the timing of recognition between the accrual and modified accrual bases of accounting.

Non-exchange revenue is receiving value in money without directly providing approximately equal value in exchange or non-exchange revenue is receiving value from another entity without directly giving approximately equal value in exchange.

There are mainly 4 types of non-exchange revenues. They are as under.

1. Derived tax revenue where assessments-imposed taxes, penalties are received. For example, income tax, sales tax and any other imposed taxes on earnings or consumption. They are derived based on facts considered valid to be tax assessed to be imposed.

2. Imposed non exchange revenue where assessments-imposed taxes are levied on nongovernmental entities including individuals. For example, property tax, fines and penalties.

3. Government mandated non exchange transactions where a government provides resources to another government, may be a local government or a local governing body for a purpose. For example, federal programs that state or local government are bound to perform.

4. Voluntary non-exchange transaction resulted by legislations or contractual agreement entered willingly by the parties for other than exchanges. For example, Donations, grants.

These are the four kind of non-exchange revenues that affect in the timing of recognition between accrual and modified accrual bases of accounting.

However, GASB's statement 33 provides guidance on timing of recognition for each type non-exchange revenue.

There are mainly 4 types of non-exchange revenues. They are as under.

1. Derived tax revenue where assessments-imposed taxes, penalties are received. For example, income tax, sales tax and any other imposed taxes on earnings or consumption. They are derived based on facts considered valid to be tax assessed to be imposed.

2. Imposed non exchange revenue where assessments-imposed taxes are levied on nongovernmental entities including individuals. For example, property tax, fines and penalties.

3. Government mandated non exchange transactions where a government provides resources to another government, may be a local government or a local governing body for a purpose. For example, federal programs that state or local government are bound to perform.

4. Voluntary non-exchange transaction resulted by legislations or contractual agreement entered willingly by the parties for other than exchanges. For example, Donations, grants.

These are the four kind of non-exchange revenues that affect in the timing of recognition between accrual and modified accrual bases of accounting.

However, GASB's statement 33 provides guidance on timing of recognition for each type non-exchange revenue.

3

The government-wide Statement of Net Assets separately displays governmental activities and business activities. Why are internal service funds most commonly displayed as governmental activities

Internal service fund can be defined as a fund authorized and recognized to fund or finance for good and or services provided by one governmental department to another governmental department and reimbursed or paid on a cost to cost basis.

In other words, internal service fund are those funds that would commonly provide good and or services to governmental department subjected to governmental activities.

It may be noted that the revenues and expenditure of internal service fund are reported and included with the governmental activities on the statement of activities.

This causes difference between the net change in the fund balance reported on the statement of revenues, expenditure and changes in fund balances of the governmental fund and change in the net assets of the governmental activities reported on the statement of activities.

Because of this, the net change in the fund balances of governmental activities will increase.

However, it may be noted that internal service fund revenues and expenses are not reported in the governmental fund financial statement because of which net change in fund balances of the governmental funds does not include internal service fund revenues and expenses.

And because of this reason, internal service fund is more commonly displayed as governmental activities to reconcile the change in the net assets of the governmental activities with the net change in the fund balances of the governmental funds.

In other words, internal service fund are those funds that would commonly provide good and or services to governmental department subjected to governmental activities.

It may be noted that the revenues and expenditure of internal service fund are reported and included with the governmental activities on the statement of activities.

This causes difference between the net change in the fund balance reported on the statement of revenues, expenditure and changes in fund balances of the governmental fund and change in the net assets of the governmental activities reported on the statement of activities.

Because of this, the net change in the fund balances of governmental activities will increase.

However, it may be noted that internal service fund revenues and expenses are not reported in the governmental fund financial statement because of which net change in fund balances of the governmental funds does not include internal service fund revenues and expenses.

And because of this reason, internal service fund is more commonly displayed as governmental activities to reconcile the change in the net assets of the governmental activities with the net change in the fund balances of the governmental funds.

4

Answer the following questions with regard to infrastructure:

a. What is infrastructure

b. What are the two methods that might be used to record infrastructure expense from year to year How is the accounting different under the two methods

c. What conditions must exist in order to use the modified approach to record and report infrastructure

d. What are the disclosure requirements if the modified approach is used

a. What is infrastructure

b. What are the two methods that might be used to record infrastructure expense from year to year How is the accounting different under the two methods

c. What conditions must exist in order to use the modified approach to record and report infrastructure

d. What are the disclosure requirements if the modified approach is used

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

5

Under the reporting model required by GASB Statement 34, fund statements are required for governmental, proprietary, and fiduciary funds. Government-wide statements include the Statement of Net Assets and Statement of Activities. Answer the following questions related to the reporting model:

1. What is the measurement focus and basis of accounting for: governmental fund statements; proprietary fund statements; fiduciary fund statements; and government-wide statements

2. Indicate differences between fund financial statements and government-wide statements with regard to: component units; fiduciary funds; and location of internal service funds.

3. Indicate what should be included in the Statement of Net Assets categories: Invested in Capital Assets, Net of Related Debt; Restricted; and Unrestricted.

1. What is the measurement focus and basis of accounting for: governmental fund statements; proprietary fund statements; fiduciary fund statements; and government-wide statements

2. Indicate differences between fund financial statements and government-wide statements with regard to: component units; fiduciary funds; and location of internal service funds.

3. Indicate what should be included in the Statement of Net Assets categories: Invested in Capital Assets, Net of Related Debt; Restricted; and Unrestricted.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

6

List some of the major adjustments required when converting from fund financial statements to government-wide statements.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

7

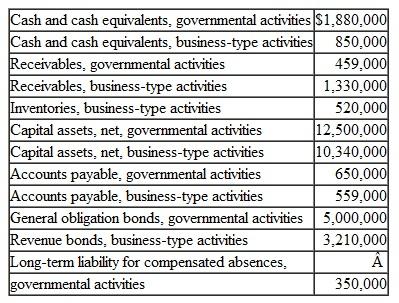

The following information is available for the preparation of the government-wide financial statements for the City of Southern Springs as of April 30, 2012:

From the preceding information, prepare (in good form) a Statement of Net Assets for the City of Southern Springs as of April 30, 2012. Assume that outstanding bonds were issued to acquire capital assets and restricted net assets total $554,000 for governmental activities and $215,000 for business-type activities. Include a Total column.

From the preceding information, prepare (in good form) a Statement of Net Assets for the City of Southern Springs as of April 30, 2012. Assume that outstanding bonds were issued to acquire capital assets and restricted net assets total $554,000 for governmental activities and $215,000 for business-type activities. Include a Total column. Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

8

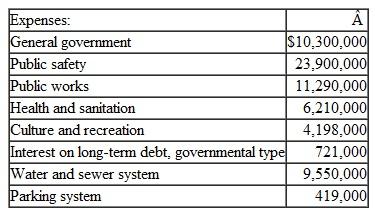

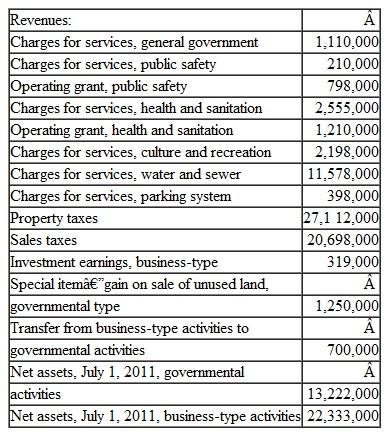

The following information is available for the preparation of the government-wide financial statements for the City of Northern Pines for the year ended June 30, 2012:

From the previous information, prepare, in good form, a Statement of Activities for the City of Northern Pines for the year ended June 30, 2012. Northern Pines has no component units.

From the previous information, prepare, in good form, a Statement of Activities for the City of Northern Pines for the year ended June 30, 2012. Northern Pines has no component units. Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

9

The City of Grinders Switch maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations.

1. General fixed assets as of the beginning of the year, which had not been recorded, were as follows:

2. During the year, expenditures for capital outlays amounted to $6,113,000. Of that amount, $4,321,000 was for buildings; the remainder was for improvements other than buildings.

3. The capital outlay expenditures outlined in (2) were completed at the end of the year (and will begin to be depreciated next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 40 years; improvements other than buildings, 20 years; and equipment, 10 years.

4. In the governmental funds Statement of Revenues, Expenditures, and Changes in Fund Balances, the City reported proceeds from the sale of land in the amount of $600,000. The land originally cost $535,000.

5. At the beginning of the year, general obligation bonds were outstanding in the amount of $4,000,000. Unamortized bond premium amounted to $40,000. Note: This entry is not covered in the text, but is similar to entry 9 in the chapter.

6. During the year, debt service expenditures for the year amounted to: interest, $580,000; principal, $400,000. For purposes of government-wide statements, $4,000 of the bond premium should be amortized. No adjustment is necessary for interest accrual.

7. At year-end, additional general obligation bonds were issued in the amount of $1,200,000, at par.

1. General fixed assets as of the beginning of the year, which had not been recorded, were as follows:

2. During the year, expenditures for capital outlays amounted to $6,113,000. Of that amount, $4,321,000 was for buildings; the remainder was for improvements other than buildings.3. The capital outlay expenditures outlined in (2) were completed at the end of the year (and will begin to be depreciated next year). For purposes of financial statement presentation, all capital assets are depreciated using the straight-line method, with no estimated salvage value. Estimated lives are as follows: buildings, 40 years; improvements other than buildings, 20 years; and equipment, 10 years.

4. In the governmental funds Statement of Revenues, Expenditures, and Changes in Fund Balances, the City reported proceeds from the sale of land in the amount of $600,000. The land originally cost $535,000.

5. At the beginning of the year, general obligation bonds were outstanding in the amount of $4,000,000. Unamortized bond premium amounted to $40,000. Note: This entry is not covered in the text, but is similar to entry 9 in the chapter.

6. During the year, debt service expenditures for the year amounted to: interest, $580,000; principal, $400,000. For purposes of government-wide statements, $4,000 of the bond premium should be amortized. No adjustment is necessary for interest accrual.

7. At year-end, additional general obligation bonds were issued in the amount of $1,200,000, at par.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

10

The City of South Pittsburgh maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. You are to prepare, in journal form, worksheet adjustments for each of the following situations:

1. Deferred property taxes of $89,000 at the end of the previous fiscal year were recognized as property tax revenue in the current year's Statement of Revenues, Expenditures, and Changes in Fund Balance.

2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $300,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $100,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting.

3. In addition to the expenditures recognized under modified accrual accounting, the City computed that $250,000 should be accrued for compensated absences and charged to public safety.

4. The City's actuary estimated that the annual required contribution (ARC) under the City's public safety employees pension plan is $229,000 for the current year. The City, however, only provided $207,000 to the pension plan during the current year.

5. In the Statement of Revenues, Expenditures, and Changes in Fund Balances, General Fund transfers out included $500,000 to a debt service fund, $600,000 to a special revenue fund, and $900,000 to an enterprise fund.

1. Deferred property taxes of $89,000 at the end of the previous fiscal year were recognized as property tax revenue in the current year's Statement of Revenues, Expenditures, and Changes in Fund Balance.

2. The City levied property taxes for the current fiscal year in the amount of $10,000,000. When making the entries, it was estimated that 2 percent of the taxes would not be collected. At year-end, $600,000 of the taxes had not been collected. It was estimated that $300,000 of that amount would be collected during the 60-day period after the end of the fiscal year and that $100,000 would be collected after that time. The City had recognized the maximum of property taxes allowable under modified accrual accounting.

3. In addition to the expenditures recognized under modified accrual accounting, the City computed that $250,000 should be accrued for compensated absences and charged to public safety.

4. The City's actuary estimated that the annual required contribution (ARC) under the City's public safety employees pension plan is $229,000 for the current year. The City, however, only provided $207,000 to the pension plan during the current year.

5. In the Statement of Revenues, Expenditures, and Changes in Fund Balances, General Fund transfers out included $500,000 to a debt service fund, $600,000 to a special revenue fund, and $900,000 to an enterprise fund.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

11

The City of Southern Pines maintains its books so as to prepare fund accounting statements and records worksheet adjustments in order to prepare government-wide statements. As such, the City's internal service fund, a motor pool fund, is included in the proprietary funds statements. Prepare necessary adjustments in order to incorporate the internal service fund in the government-wide statements as a part of governmental activities.

1. Balance sheet asset accounts include: Cash, $150,000; Investments, $125,000; Due from the General Fund, $15,000; Inventories, $325,000; and Capital Assets (net), $1,340,000. Liability accounts include: Accounts Payable, $50,000; Long-Term Advance from Enterprise Fund, $800,000.

2. The only transaction in the internal service fund that is external to the government is interest revenue in the amount of $5,300.

3. Exclusive of the interest revenue, the internal service fund reported net income in the amount of $36,000. An examination of the records indicates that services were provided as follows: one-third to general government, one-third to public safety, and one-third to public works.

1. Balance sheet asset accounts include: Cash, $150,000; Investments, $125,000; Due from the General Fund, $15,000; Inventories, $325,000; and Capital Assets (net), $1,340,000. Liability accounts include: Accounts Payable, $50,000; Long-Term Advance from Enterprise Fund, $800,000.

2. The only transaction in the internal service fund that is external to the government is interest revenue in the amount of $5,300.

3. Exclusive of the interest revenue, the internal service fund reported net income in the amount of $36,000. An examination of the records indicates that services were provided as follows: one-third to general government, one-third to public safety, and one-third to public works.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

12

Presented on the following pages are partial financial statements for the City of Shenandoah, including:

Fiscal year 2012:

A. Total Governmental Funds:

Balance Sheet

Statement of Revenues, Expenditures, and Changes in Fund Balance

B. Internal Service Fund:

Statement of Net Assets

Statement of Revenues, Expenses, and Changes in Net Assets

Fiscal year 2011:

A. Total Governmental Funds:

Balance Sheet

B. Government-wide-Governmental Activities:

Statement of Net Assets

Additional Information

1. $445,600 of the capital assets purchased in fiscal year 2012 was equipment. All remaining capital acquisitions were for a new building.

2. Depreciation of general fixed assets: buildings $1,100,000, infrastructure $975,000, and equipment $537,500.

3. The City had $6,000,000 of 6 percent general obligation bonds (issued at par) outstanding at December 31, 2011. In addition, the City issued $4,000,000 of 8 percent bonds on January 2, 2012 (sold at a premium). Interest payments on both bond issues are due on January 1 and July 1. Principal payments are made on January 1. Interest and principal payments for the current year include:

The January interest payments are accrued for purposes of the government- wide statements but not the fund-basis statements. The bond premium is to be amortized in the amount of $2,500 per year.

4. Property taxes expected to be collected more than 60 days after year-end are deferred in the fund basis statements.

5. At the end of 2012, the accumulated liability for landfill closure and post-closure care costs is estimated to be $37,000. Landfill operations are reported in the General Fund-Public Works.

6. The internal service fund serves several departments of the General Fund, all within the category of "General Government." The internal service fund was created at the end of 2011 and had no capital assets or long-term liabilities at the end of 2011.

Prepare all worksheet journal entries necessary for fiscal year 2012 to convert the governmental fund basis amounts to the economic resources measurement focus and accrual basis required for the governmental activities sections of the government-wide statements.

Fiscal year 2012:

A. Total Governmental Funds:

Balance Sheet

Statement of Revenues, Expenditures, and Changes in Fund Balance

B. Internal Service Fund:

Statement of Net Assets

Statement of Revenues, Expenses, and Changes in Net Assets

Fiscal year 2011:

A. Total Governmental Funds:

Balance Sheet

B. Government-wide-Governmental Activities:

Statement of Net Assets

Additional Information 1. $445,600 of the capital assets purchased in fiscal year 2012 was equipment. All remaining capital acquisitions were for a new building.

2. Depreciation of general fixed assets: buildings $1,100,000, infrastructure $975,000, and equipment $537,500.

3. The City had $6,000,000 of 6 percent general obligation bonds (issued at par) outstanding at December 31, 2011. In addition, the City issued $4,000,000 of 8 percent bonds on January 2, 2012 (sold at a premium). Interest payments on both bond issues are due on January 1 and July 1. Principal payments are made on January 1. Interest and principal payments for the current year include:

The January interest payments are accrued for purposes of the government- wide statements but not the fund-basis statements. The bond premium is to be amortized in the amount of $2,500 per year.4. Property taxes expected to be collected more than 60 days after year-end are deferred in the fund basis statements.

5. At the end of 2012, the accumulated liability for landfill closure and post-closure care costs is estimated to be $37,000. Landfill operations are reported in the General Fund-Public Works.

6. The internal service fund serves several departments of the General Fund, all within the category of "General Government." The internal service fund was created at the end of 2011 and had no capital assets or long-term liabilities at the end of 2011.

Prepare all worksheet journal entries necessary for fiscal year 2012 to convert the governmental fund basis amounts to the economic resources measurement focus and accrual basis required for the governmental activities sections of the government-wide statements.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

13

The fund-basis financial statements of Jefferson County have been completed for the year 2012 and appear in the first tab of the Excel spreadsheet provided with this exercise. The following information is also available:

a. Capital Assets

• Capital assets purchased in previous years through governmental type funds totaled $752,000 (net of accumulated depreciation) as of January 1, 2012.

• Depreciation on capital assets used in governmental-type activities amounted to $79,500 for 2012.

• No capital assets were sold or disposed of in 2012 and all purchases are properly reflected in the fund-basis statements as capital expenditures.

b. Long-term Debt

• There was no outstanding long-term debt associated with governmental-type funds as of January 1, 2012.

• April 1, 2012, 6 percent bonds with a face value of $700,000 were issued in the amount of $720,000. Bond payments are made on October 1 and April 1 of each year. Interest is based on an annual rate of 6 percent and principal payments are $17,500 each. The first payment (interest and principal) was made on October 1.

• Amortization of the bond premium for the current year is $1,000.

c. Deferred Revenues

• Deferred revenues (comprised solely of property taxes) are expected to be collected more than 60 days after year-end. The balance of deferred taxes at the end of 2011 was $18,200.

d. Transfers

• Transfers were between governmental-type funds.

e. Internal Service Fund

• The (motor pool) internal service fund's revenue is predominantly derived from departments classified as governmental-type activities.

• There were no amounts due to the internal service fund from the General Fund. The outstanding balance of "due to other funds" was with the Enterprise Fund and is not capital related.

• The enterprise fund provided a long-term advance to the internal service fund (not capital related).

Required:

Use the Excel template provided to complete the following requirements; a separate tab is provided in Excel for each of these steps.

1. Prepare the journal entries necessary to convert the governmental fund financial statements to the accrual basis of accounting.

2. Post the journal entries to the conversion worksheet provided.

3. Prepare a government-wide Statement of Activities and Statement of Net Assets for the year 2012. All of the governmental fund revenues are "general revenues."

This is an involved problem, requiring many steps. Here are some hints.

a. Tab 1 is information to be used in the problem. You do not enter anything here.

b. After you make the journal entries (Tab 2), post these to the worksheet to convert to the accrual basis. This worksheet is set up so that you enter debits as positive numbers and credits as negative. After you post your entries, look at the numbers below the total credit column to see that debits equal credits. If not, you probably entered a credit as a positive number.

c. Make sure that total debits equal total credits in the last column (balances for government-wide statements).

d. When calculating Restricted Net Assets, recall that permanent fund principal is added to restricted fund balances.

a. Capital Assets

• Capital assets purchased in previous years through governmental type funds totaled $752,000 (net of accumulated depreciation) as of January 1, 2012.

• Depreciation on capital assets used in governmental-type activities amounted to $79,500 for 2012.

• No capital assets were sold or disposed of in 2012 and all purchases are properly reflected in the fund-basis statements as capital expenditures.

b. Long-term Debt

• There was no outstanding long-term debt associated with governmental-type funds as of January 1, 2012.

• April 1, 2012, 6 percent bonds with a face value of $700,000 were issued in the amount of $720,000. Bond payments are made on October 1 and April 1 of each year. Interest is based on an annual rate of 6 percent and principal payments are $17,500 each. The first payment (interest and principal) was made on October 1.

• Amortization of the bond premium for the current year is $1,000.

c. Deferred Revenues

• Deferred revenues (comprised solely of property taxes) are expected to be collected more than 60 days after year-end. The balance of deferred taxes at the end of 2011 was $18,200.

d. Transfers

• Transfers were between governmental-type funds.

e. Internal Service Fund

• The (motor pool) internal service fund's revenue is predominantly derived from departments classified as governmental-type activities.

• There were no amounts due to the internal service fund from the General Fund. The outstanding balance of "due to other funds" was with the Enterprise Fund and is not capital related.

• The enterprise fund provided a long-term advance to the internal service fund (not capital related).

Required:

Use the Excel template provided to complete the following requirements; a separate tab is provided in Excel for each of these steps.

1. Prepare the journal entries necessary to convert the governmental fund financial statements to the accrual basis of accounting.

2. Post the journal entries to the conversion worksheet provided.

3. Prepare a government-wide Statement of Activities and Statement of Net Assets for the year 2012. All of the governmental fund revenues are "general revenues."

This is an involved problem, requiring many steps. Here are some hints.

a. Tab 1 is information to be used in the problem. You do not enter anything here.

b. After you make the journal entries (Tab 2), post these to the worksheet to convert to the accrual basis. This worksheet is set up so that you enter debits as positive numbers and credits as negative. After you post your entries, look at the numbers below the total credit column to see that debits equal credits. If not, you probably entered a credit as a positive number.

c. Make sure that total debits equal total credits in the last column (balances for government-wide statements).

d. When calculating Restricted Net Assets, recall that permanent fund principal is added to restricted fund balances.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

14

The fund-basis financial statements of the City of Cottonwood have been completed for the year 2012 and appear in the first tab of the Excel spreadsheet provided with this exercise. In addition, the Statement of Net Assets from the previous fiscal year is provided and should be used to determine beginning balances for accounts not appearing in the fund-basis statements. The following information is also available:

a. Capital Assets:

• Capital assets purchased by governmental funds are charged to capital expenditure and do not appear as assets in the fund-basis balance

sheet. However, the balance is reflected in the statement of net assets in the government-wide financial statements.

• Depreciation on capital assets used in governmental-type activities amounted to $2,450,000 for 2012.

• No capital assets were sold or disposed of in 2012, and all purchases are properly reflected in the fund-basis statements as capital expenditures.

b. Long-term debt

• Proceeds from bonds issued by governmental funds are reflected in other financing sources and do not appear as liabilities in the fund-basis balance sheet. Payments of principal are recognized as expenditures when due. The balance of outstanding bonds balance is reflected in the statement of net assets in the government-wide financial statements.

• Interest is recognized in the fund-basis statements only when payment is due. Interest accrued but not yet payable amounted to $107,500 at December 31, 2012. Interest accrued for purposes of the government-Wide statements in 2011 has been paid and is reflected in interest expenditure in 2012.

• There are no bond discounts or premiums.

c. Deferred Revenues

• Deferred revenues are comprised solely of property taxes expected to be collected more than 60 days after year-end. The balance of deferred taxes at the end of 2011 was $128,200 and was recognized as revenue in the fund-basis statements in 2012.

d. The City accounts for its solid waste landfill in the General Fund (public works department). The estimated liability for closure and post-closure care costs as of December 31, 2012, is $1,580,900 and appears only in the government-wide statements.

e. Transfers

• During the year, the General Fund transferred cash to the courthouse renovation, debt service, and enterprise funds.

f. The City does not operate any Internal Service Funds.

g. When entering amounts in the Statement of Activities, Charges for Services Revenue in the governmental funds is attributable to the following functions:

Required:

Use the Excel template provided to complete the following requirements; a separate tab is provided in Excel for each of these steps.

1. Prepare the journal entries necessary to convert the governmental fund financial statements to the accrual basis of accounting.

2. Post the journal entries to the conversion worksheet provided.

3. Prepare a government-wide Statement of Activities and Statement of Net Assets for the year 2012.

This is an involved problem, requiring many steps. Here are some

hints.

a. Tab 1 is information to be used in the problem. You do not enter anything here.

b. After you make the journal entries (Tab 2), post these to the worksheet to convert to the accrual basis. This worksheet is set up so that you enter debits as positive numbers and credits as negative. After you post your entries, look at the numbers below the total credit column to see that debits equal credits. If not, you probably entered a credit as a positive number.

c. Make sure that total debits equal total credits in the last column (Balances for government-wide statements).

d. When calculating Restricted Net Assets, recall that permanent fund principal is added to restricted fund balances.

a. Capital Assets:

• Capital assets purchased by governmental funds are charged to capital expenditure and do not appear as assets in the fund-basis balance

sheet. However, the balance is reflected in the statement of net assets in the government-wide financial statements.

• Depreciation on capital assets used in governmental-type activities amounted to $2,450,000 for 2012.

• No capital assets were sold or disposed of in 2012, and all purchases are properly reflected in the fund-basis statements as capital expenditures.

b. Long-term debt

• Proceeds from bonds issued by governmental funds are reflected in other financing sources and do not appear as liabilities in the fund-basis balance sheet. Payments of principal are recognized as expenditures when due. The balance of outstanding bonds balance is reflected in the statement of net assets in the government-wide financial statements.

• Interest is recognized in the fund-basis statements only when payment is due. Interest accrued but not yet payable amounted to $107,500 at December 31, 2012. Interest accrued for purposes of the government-Wide statements in 2011 has been paid and is reflected in interest expenditure in 2012.

• There are no bond discounts or premiums.

c. Deferred Revenues

• Deferred revenues are comprised solely of property taxes expected to be collected more than 60 days after year-end. The balance of deferred taxes at the end of 2011 was $128,200 and was recognized as revenue in the fund-basis statements in 2012.

d. The City accounts for its solid waste landfill in the General Fund (public works department). The estimated liability for closure and post-closure care costs as of December 31, 2012, is $1,580,900 and appears only in the government-wide statements.

e. Transfers

• During the year, the General Fund transferred cash to the courthouse renovation, debt service, and enterprise funds.

f. The City does not operate any Internal Service Funds.

g. When entering amounts in the Statement of Activities, Charges for Services Revenue in the governmental funds is attributable to the following functions:

Required: Use the Excel template provided to complete the following requirements; a separate tab is provided in Excel for each of these steps.

1. Prepare the journal entries necessary to convert the governmental fund financial statements to the accrual basis of accounting.

2. Post the journal entries to the conversion worksheet provided.

3. Prepare a government-wide Statement of Activities and Statement of Net Assets for the year 2012.

This is an involved problem, requiring many steps. Here are some

hints.

a. Tab 1 is information to be used in the problem. You do not enter anything here.

b. After you make the journal entries (Tab 2), post these to the worksheet to convert to the accrual basis. This worksheet is set up so that you enter debits as positive numbers and credits as negative. After you post your entries, look at the numbers below the total credit column to see that debits equal credits. If not, you probably entered a credit as a positive number.

c. Make sure that total debits equal total credits in the last column (Balances for government-wide statements).

d. When calculating Restricted Net Assets, recall that permanent fund principal is added to restricted fund balances.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 14 flashcards in this deck.