Deck 6: Proprietary Funds

Full screen (f)

Question

Question

Question

Question

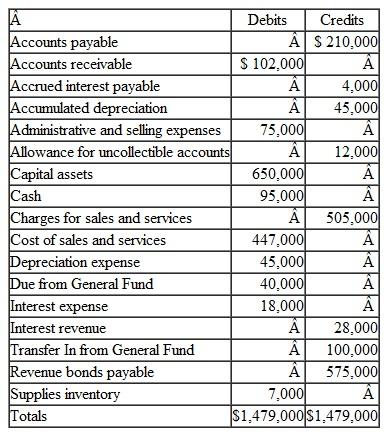

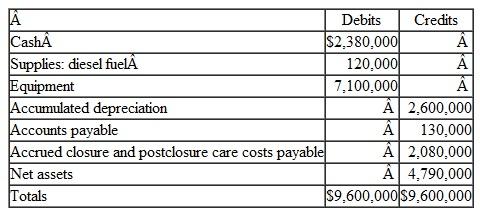

The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2012, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund.

a. Prepare the closing entries for December 31.

a. Prepare the closing entries for December 31.

b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31.

c. Prepare the Net Asset Section of the December 31 balance sheet. (Assume that the revenue bonds were issued to acquire capital assets and there are no restricted assets.)

a. Prepare the closing entries for December 31.b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31.

c. Prepare the Net Asset Section of the December 31 balance sheet. (Assume that the revenue bonds were issued to acquire capital assets and there are no restricted assets.)

Question

Question

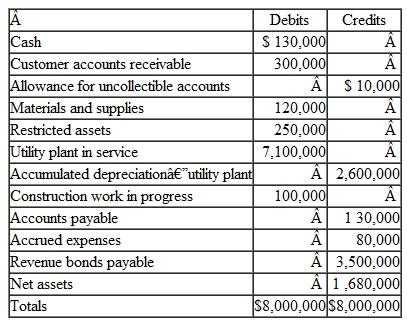

The Town of Wilson has a Water Utility Fund with the following trial balance as of July 1, 2011, the first day of the fiscal year:

During the year ended June 30, 2012, the following transactions and events occurred in the Town of Wilson Water Utility Fund:

During the year ended June 30, 2012, the following transactions and events occurred in the Town of Wilson Water Utility Fund:

1. Accrued expenses at July 1, 2011, were paid in cash.

2. Billings to nongovernmental customers for water usage for the year amounted to $1,400,000; billings to the General Fund amounted to $57,000.

3. Liabilities for the following were recorded during the year:

4. Materials and supplies were used in the amount of $265,700, all for costs of sales and services.

4. Materials and supplies were used in the amount of $265,700, all for costs of sales and services.

5. $8,000 of old accounts receivable were written off.

6. Accounts receivable collections totaled $1,450,000 from nongovernmental customers and $48,400 from the General Fund.

7. $1,035,000 of accounts payable were paid in cash.

8. One year's interest in the amount of $175,000 was paid.

9. Construction was completed on plant assets costing $135,000; that amount was transferred to Utility Plant in Service.

10. Depreciation was recorded in the amount of $235,000.

11. Interest in the amount of $25,000 was charged to Construction Work in Progress. (This was previously paid in item 8.)

12. The Allowance for Uncollectible Accounts was increased by $13,100.

13. As required by the loan agreement, cash in the amount of $100,000 was transferred to Restricted Assets for eventual redemption of the bonds.

14. Accrued expenses, all related to costs of sales and services, amounted to $47,000.

15. Nominal accounts for the year were closed to Net Assets.

Required:

a. Record the transactions for the year in general journal form.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets.

c. Prepare a Statement of Net Assets as of June 30, 2012.

d. Prepare a Statement of Cash Flows for the Year Ended June 30, 2012. Assume all debt and interest are related to capital outlay. Assume the entire $212,200 construction work in progress liability (see item 3) was paid in entry 7. Include restricted assets as cash and cash equivalents.

During the year ended June 30, 2012, the following transactions and events occurred in the Town of Wilson Water Utility Fund:1. Accrued expenses at July 1, 2011, were paid in cash.

2. Billings to nongovernmental customers for water usage for the year amounted to $1,400,000; billings to the General Fund amounted to $57,000.

3. Liabilities for the following were recorded during the year:

4. Materials and supplies were used in the amount of $265,700, all for costs of sales and services.5. $8,000 of old accounts receivable were written off.

6. Accounts receivable collections totaled $1,450,000 from nongovernmental customers and $48,400 from the General Fund.

7. $1,035,000 of accounts payable were paid in cash.

8. One year's interest in the amount of $175,000 was paid.

9. Construction was completed on plant assets costing $135,000; that amount was transferred to Utility Plant in Service.

10. Depreciation was recorded in the amount of $235,000.

11. Interest in the amount of $25,000 was charged to Construction Work in Progress. (This was previously paid in item 8.)

12. The Allowance for Uncollectible Accounts was increased by $13,100.

13. As required by the loan agreement, cash in the amount of $100,000 was transferred to Restricted Assets for eventual redemption of the bonds.

14. Accrued expenses, all related to costs of sales and services, amounted to $47,000.

15. Nominal accounts for the year were closed to Net Assets.

Required:

a. Record the transactions for the year in general journal form.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets.

c. Prepare a Statement of Net Assets as of June 30, 2012.

d. Prepare a Statement of Cash Flows for the Year Ended June 30, 2012. Assume all debt and interest are related to capital outlay. Assume the entire $212,200 construction work in progress liability (see item 3) was paid in entry 7. Include restricted assets as cash and cash equivalents.

Question

Question

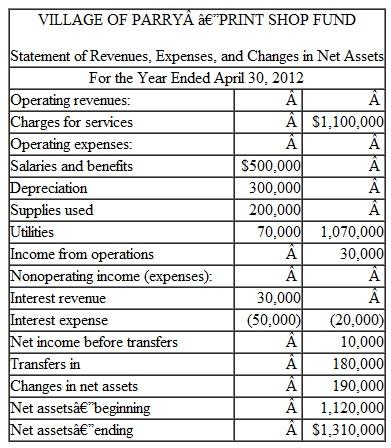

The Village of Parry reported the following for its Print Shop Fund for the year ended April 30, 2012.

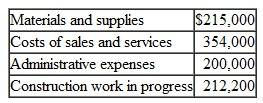

The Print Shop Fund records also revealed the following:

The Print Shop Fund records also revealed the following:

The following balances were observed in current asset and current liability accounts. ( ) denote credit balances:

The following balances were observed in current asset and current liability accounts. ( ) denote credit balances:

Prepare a Statement of Cash Flows for the Village of Parry Print Shop Fund for the Year Ended April 30, 2012. Include the reconciliation of operating income to net cash provided by operating activities.

Prepare a Statement of Cash Flows for the Village of Parry Print Shop Fund for the Year Ended April 30, 2012. Include the reconciliation of operating income to net cash provided by operating activities.

The Print Shop Fund records also revealed the following: The following balances were observed in current asset and current liability accounts. ( ) denote credit balances: Prepare a Statement of Cash Flows for the Village of Parry Print Shop Fund for the Year Ended April 30, 2012. Include the reconciliation of operating income to net cash provided by operating activities. Question

The following is a statement of cash flows for the risk management internal service fund of the City of Wrightville. An inexperienced accountant prepared the statement using the FASB format rather than the format required by GASB. All long-term debt was issued to purchase capital assets. The transfer from the General Fund was to establish the internal service fund and provide the initial working capital necessary for operations.

Prepare a statement of cash flows using the appropriate format as required by GASB. You do not need to prepare the reconciliation of operating income to cash flow from operations.

Prepare a statement of cash flows using the appropriate format as required by GASB. You do not need to prepare the reconciliation of operating income to cash flow from operations.

Prepare a statement of cash flows using the appropriate format as required by GASB. You do not need to prepare the reconciliation of operating income to cash flow from operations. Question

The Town of Frostbite self-insures for some of its liability claims and purchases insurance for others. In an effort to consolidate its risk management activities, the Town recently decided to establish an internal service fund, the Risk Management Fund. The Risk Management Fund's purpose is to obtain liability coverage for the Town, to pay claims not covered by the insurance, and to charge individual departments in amounts sufficient to cover current-year costs and to establish a reserve for losses.

The Town reports proprietary fund expenses by object classification using the following accounts: Personnel services (salaries), Contractual services (for the expired portion of prepaid service contracts), Depreciation, and Insurance Claims. The following transactions relate to the year ended

December 31, 2012, the first year of the Risk Management Fund's operations.

1. The Risk Management Fund is established through a transfer of $500,000 from the General Fund and a long-term advance from the water utility enterprise fund of $250,000.

2. The Risk Management Fund purchased (prepaid) insurance coverage through several commercial insurance companies for $200,000. The policies purchased require the Town to self-insure for $25,000 per incident.

3. Office Equipment is purchased for $10,000.

4. $450,000 is invested in marketable securities.

5. Actuarial estimates were made in the previous fiscal year to determine the amount necessary to attain the goal of accumulating sufficient funds to cover current-year claims and to establish a reserve for losses. It was determined that the General Fund and water utility be assessed a fee of 6 percent of total wages and salaries (Interfund premium). Wages and salaries by department are as follows:

6. Cash received in payment of interfund premiums from the General Fund totaled $275,000 and cash received from the Water Utility totaled $100,000.

6. Cash received in payment of interfund premiums from the General Fund totaled $275,000 and cash received from the Water Utility totaled $100,000.

7. Interest and dividends received totaled $27,000.

8. Salaries for the Risk Management Fund amounted to $200,000 (all paid during the year).

9. Claims paid under self-insurance totaled $150,000 during the year.

10. The office equipment is depreciated on the straight-line basis over 5 years.

11. At year-end, $190,000 of the insurance policies purchased in January had expired.

12. The market value of investments at December 31 totaled $456,000 ( Hint: credit Net Increase in Fair Market Value of Investments ).

13. In addition to the claims paid in entry 9 above, estimates for the liability for the Town's portion of known claims since the inception of the Town's self-insurance program totaled $90,000.

Required:

a. Prepare the journal entries (including closing entries) to record the transactions.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012, for the Risk Management Fund

c. Prepare a Statement of Net Assets as of December 31, 2012, for the Risk Management Fund

d. Prepare a Statement of Cash Flows for the year ended December 31, 2012, for the Risk Management Fund. Assume $10,000 of the transfer from the General Fund was for the purchase of the equipment. Further, assume the remainder of the transfer from the General Fund and all of the advance from the enterprise fund are to establish working capital (noncapital related financing).

e. Comment on whether the interfund premium of 6 percent of wages and salaries is adequate.

The Town reports proprietary fund expenses by object classification using the following accounts: Personnel services (salaries), Contractual services (for the expired portion of prepaid service contracts), Depreciation, and Insurance Claims. The following transactions relate to the year ended

December 31, 2012, the first year of the Risk Management Fund's operations.

1. The Risk Management Fund is established through a transfer of $500,000 from the General Fund and a long-term advance from the water utility enterprise fund of $250,000.

2. The Risk Management Fund purchased (prepaid) insurance coverage through several commercial insurance companies for $200,000. The policies purchased require the Town to self-insure for $25,000 per incident.

3. Office Equipment is purchased for $10,000.

4. $450,000 is invested in marketable securities.

5. Actuarial estimates were made in the previous fiscal year to determine the amount necessary to attain the goal of accumulating sufficient funds to cover current-year claims and to establish a reserve for losses. It was determined that the General Fund and water utility be assessed a fee of 6 percent of total wages and salaries (Interfund premium). Wages and salaries by department are as follows:

6. Cash received in payment of interfund premiums from the General Fund totaled $275,000 and cash received from the Water Utility totaled $100,000.7. Interest and dividends received totaled $27,000.

8. Salaries for the Risk Management Fund amounted to $200,000 (all paid during the year).

9. Claims paid under self-insurance totaled $150,000 during the year.

10. The office equipment is depreciated on the straight-line basis over 5 years.

11. At year-end, $190,000 of the insurance policies purchased in January had expired.

12. The market value of investments at December 31 totaled $456,000 ( Hint: credit Net Increase in Fair Market Value of Investments ).

13. In addition to the claims paid in entry 9 above, estimates for the liability for the Town's portion of known claims since the inception of the Town's self-insurance program totaled $90,000.

Required:

a. Prepare the journal entries (including closing entries) to record the transactions.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012, for the Risk Management Fund

c. Prepare a Statement of Net Assets as of December 31, 2012, for the Risk Management Fund

d. Prepare a Statement of Cash Flows for the year ended December 31, 2012, for the Risk Management Fund. Assume $10,000 of the transfer from the General Fund was for the purchase of the equipment. Further, assume the remainder of the transfer from the General Fund and all of the advance from the enterprise fund are to establish working capital (noncapital related financing).

e. Comment on whether the interfund premium of 6 percent of wages and salaries is adequate.

Question

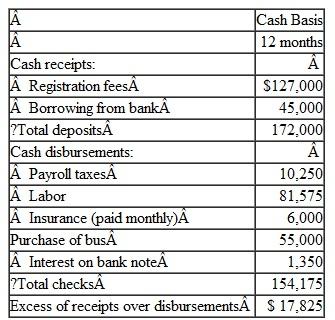

The City of Evansville operated a summer camp program for at-risk youth. Businesses and nonprofit organizations sponsor one or more youth by paying the registration fee for program participants. The following Statement of Cash Receipts and Disbursements summarizes the activity in the program's bank account for the year.

1. At the beginning of 2012, the program had unrestricted cash of

$12,000.

2. The loan from the bank is dated April 1 and is for a five-year period. Interest (6 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012.

2. The loan from the bank is dated April 1 and is for a five-year period. Interest (6 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012.

3. The bus was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 5 years (straight line basis-use monthly depreciation).

4. All invoices and salaries related to 2012 had been paid by close of business on December 31, except for the employer's portion of December payroll taxes, totaling $900.

a. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets assuming the City intends to treat the summer camp program as an enterprise fund.

b. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenditures, and Changes in Fund Balance assuming the City intends to treat the summer camp program as a special revenue fund.

1. At the beginning of 2012, the program had unrestricted cash of

$12,000.

2. The loan from the bank is dated April 1 and is for a five-year period. Interest (6 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012.3. The bus was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 5 years (straight line basis-use monthly depreciation).

4. All invoices and salaries related to 2012 had been paid by close of business on December 31, except for the employer's portion of December payroll taxes, totaling $900.

a. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets assuming the City intends to treat the summer camp program as an enterprise fund.

b. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenditures, and Changes in Fund Balance assuming the City intends to treat the summer camp program as a special revenue fund.

Question

The Town of Thomaston has a Solid Waste Landfill Enterprise Fund with the following trial balance as of January 1, 2012, the first day of the fiscal year.

During the year, the following transactions and events occurred:

During the year, the following transactions and events occurred:

1. Citizens and trash companies dumped 500,000 tons of waste in the landfill, which charges $5.50 a ton payable in cash.

2. Diesel fuel purchases totaled $343,000 (on account).

3. Accounts payable totaling $430,000 were paid.

4. Diesel fuel used in operations amounted to $405,000.

5. Depreciation was recorded in the amount of $735,000.

6. Salaries totaling $75,000 were paid.

7. Future costs to close the landfill and postclosure care costs are expected to total $76,250,000. The total capacity of the landfill is expected to be 25,000,000 tons of waste.

Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012.

During the year, the following transactions and events occurred:1. Citizens and trash companies dumped 500,000 tons of waste in the landfill, which charges $5.50 a ton payable in cash.

2. Diesel fuel purchases totaled $343,000 (on account).

3. Accounts payable totaling $430,000 were paid.

4. Diesel fuel used in operations amounted to $405,000.

5. Depreciation was recorded in the amount of $735,000.

6. Salaries totaling $75,000 were paid.

7. Future costs to close the landfill and postclosure care costs are expected to total $76,250,000. The total capacity of the landfill is expected to be 25,000,000 tons of waste.

Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012.

Question

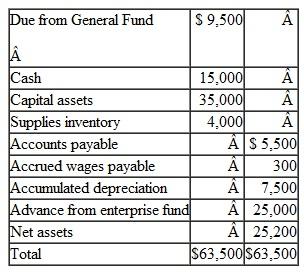

Jefferson County operates a centralized motor pool to service county

vehicles. At the end of 2011, the Motor Pool Internal Service Fund had the following account balances:

The following events took place during 2012:

The following events took place during 2012:

1. Additional supplies were purchased on account in the amount of $35,000.

2. Services provided to other departments on account totaled $95,000. A total of $65,000 was for departments in the General Fund and $30,000 for enterprise fund departments.

3. Supplies used amounted to $36,700.

4. Payments made on accounts payable amounted to $38,200.

5. Cash collected from the General Fund totaled $57,000 and cash colected from the enterprise fund totaled $30,000.

6. Salaries were paid in the amount of $47,000. Included in this amount is the accrued wages payable at the end of 2011. All of these are determined to be part of the cost of services provided.

7. In a previous year, the enterprise fund loaned the Motor Pool money under an advance for the purpose of purchasing garage equipment. In the current year, the Motor Pool repaid the enterprise fund $7,000 of this amount.

8. On July 1, 2012, the Motor Pool Fund borrowed $10,000 from the bank, signing a 12 percent note that is due on June 30, 2013. The borrowings are not related to capital asset purchases but were made to provide working capital.

Additional information includes:

9. Depreciation for the year amounted to $7,500.

10. The payment of interest on the note is payable on June 30, 2013.

11. Unpaid wages relating to the final week of the year totaled $420.

Using the Excel template provided; a separate tab is provided for each of the requirements:

a. Prepare journal entries.

b. Post entries to the T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Fund Net Assets.

e. Prepare a Statement of Net Assets.

f. Prepare a Statement of Cash Flows for the year ending December-31-2012.

vehicles. At the end of 2011, the Motor Pool Internal Service Fund had the following account balances:

The following events took place during 2012:1. Additional supplies were purchased on account in the amount of $35,000.

2. Services provided to other departments on account totaled $95,000. A total of $65,000 was for departments in the General Fund and $30,000 for enterprise fund departments.

3. Supplies used amounted to $36,700.

4. Payments made on accounts payable amounted to $38,200.

5. Cash collected from the General Fund totaled $57,000 and cash colected from the enterprise fund totaled $30,000.

6. Salaries were paid in the amount of $47,000. Included in this amount is the accrued wages payable at the end of 2011. All of these are determined to be part of the cost of services provided.

7. In a previous year, the enterprise fund loaned the Motor Pool money under an advance for the purpose of purchasing garage equipment. In the current year, the Motor Pool repaid the enterprise fund $7,000 of this amount.

8. On July 1, 2012, the Motor Pool Fund borrowed $10,000 from the bank, signing a 12 percent note that is due on June 30, 2013. The borrowings are not related to capital asset purchases but were made to provide working capital.

Additional information includes:

9. Depreciation for the year amounted to $7,500.

10. The payment of interest on the note is payable on June 30, 2013.

11. Unpaid wages relating to the final week of the year totaled $420.

Using the Excel template provided; a separate tab is provided for each of the requirements:

a. Prepare journal entries.

b. Post entries to the T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Fund Net Assets.

e. Prepare a Statement of Net Assets.

f. Prepare a Statement of Cash Flows for the year ending December-31-2012.

Question

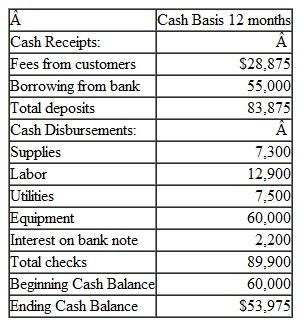

Rural County is an agricultural community located hundreds of miles from any metropolitan center. The County established a television reception improvement fund to serve the public interest by constructing and operating television translator stations. TV translator stations serve communities that cannot receive the signals of free over-the-air TV stations because they are too far away from a broadcasting TV station. Because of the largest distances between customers, commercial cable TV providers are also not inclined to serve rural communities. The fund charges TV owners a monthly fee of $15. The fund was established on December 20, 2011, with a transfer of cash from the General Fund of $100,000. On December 31, 2011, the fund acquired land for its translator stations in the amount of $40,000. The remaining cash and the land are the only resources held by the fund at the beginning of 2012.

1. Other than beginning account balances, no entries have been made in the general ledger.

2. The county prepared a budget for 2012 with estimated customer fees of $30,000, operating costs of $30,000, capital costs of $65,000, and estimated loan proceeds of $55,000.

3. The following information was taken from the checkbook for the year ended December-31-2012.

4. The loan from the bank is dated April 1 and is for a five-year period. Interest (8 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012. The County has elected not to establish a debt service fund but will pay the interest on this note from the Television Reception Improvement Fund.

4. The loan from the bank is dated April 1 and is for a five-year period. Interest (8 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012. The County has elected not to establish a debt service fund but will pay the interest on this note from the Television Reception Improvement Fund.

5. The machinery was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 10 years (straight-line basis).

6. In January 2013, customers remitted fees totaling $2,500 for December 2012 service.

7. Supplies of $500 were received on December 29 and paid in January 2013.

8. Unused supplies on hand amounted to $760 at December 31, 2012.

9. Utilities are paid in the following month. The utility bill for December 2012 was received on January 4, 2013 in the amount of $620. (Utility bills are recorded through accounts payable.)

10. On December 21, the company placed an order for a new computerized control switch in the amount of $1,500 to be delivered and paid in January 2013.

Required:

You have been asked to provide financial statements for the upcoming County Board meeting for the Television Reception Improvement Fund.

Part 1: Assume the County chooses to report the Television Reception Improvement Fund as a Special Revenue Fund following modified accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance.

e. Prepare a Balance Sheet, assuming there are no restricted or committed fund net resources.

Part 2: Assume the County chooses to report the Television Reception Improvement Fund as an Enterprise Fund following accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Net Assets.

e. Prepare a Statement of Net Assets, assuming the bank note is related to capital asset acquisitions.

The Excel template contains separate tabs for (1) special revenue fund journal entries and T-accounts, (2) special revenue fund closing entries, (3) special revenue fund financial statements, (4) enterprise fund journal entries and T-accounts, (5) enterprise fund closing entries, and (6) enterprise fund financial statements. Both the T-accounts and financial statements contain accounts you will not need under either the modified accrual or accrual bases. Similarly, you may not need to record some of the events, depending on the basis of accounting.

1. Other than beginning account balances, no entries have been made in the general ledger.

2. The county prepared a budget for 2012 with estimated customer fees of $30,000, operating costs of $30,000, capital costs of $65,000, and estimated loan proceeds of $55,000.

3. The following information was taken from the checkbook for the year ended December-31-2012.

4. The loan from the bank is dated April 1 and is for a five-year period. Interest (8 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012. The County has elected not to establish a debt service fund but will pay the interest on this note from the Television Reception Improvement Fund.5. The machinery was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 10 years (straight-line basis).

6. In January 2013, customers remitted fees totaling $2,500 for December 2012 service.

7. Supplies of $500 were received on December 29 and paid in January 2013.

8. Unused supplies on hand amounted to $760 at December 31, 2012.

9. Utilities are paid in the following month. The utility bill for December 2012 was received on January 4, 2013 in the amount of $620. (Utility bills are recorded through accounts payable.)

10. On December 21, the company placed an order for a new computerized control switch in the amount of $1,500 to be delivered and paid in January 2013.

Required:

You have been asked to provide financial statements for the upcoming County Board meeting for the Television Reception Improvement Fund.

Part 1: Assume the County chooses to report the Television Reception Improvement Fund as a Special Revenue Fund following modified accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance.

e. Prepare a Balance Sheet, assuming there are no restricted or committed fund net resources.

Part 2: Assume the County chooses to report the Television Reception Improvement Fund as an Enterprise Fund following accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Net Assets.

e. Prepare a Statement of Net Assets, assuming the bank note is related to capital asset acquisitions.

The Excel template contains separate tabs for (1) special revenue fund journal entries and T-accounts, (2) special revenue fund closing entries, (3) special revenue fund financial statements, (4) enterprise fund journal entries and T-accounts, (5) enterprise fund closing entries, and (6) enterprise fund financial statements. Both the T-accounts and financial statements contain accounts you will not need under either the modified accrual or accrual bases. Similarly, you may not need to record some of the events, depending on the basis of accounting.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/14

Play

Full screen (f)

Deck 6: Proprietary Funds

1

Using the annual financial report obtained for Exercise 1-1, answer the following questions:

a. Find the Statement of Net Assets for the proprietary funds. Is the Net Asset or the Balance Sheet format used List the major enterprise funds from that statement. Is the statement classified between current and non- current assets and liabilities Are net assets broken down into the three classifications shown in your text Is a separate column shown for internal service funds

b. Find the Statement of Revenues, Expenses, and Changes in Net Assets for the proprietary funds. Is the "all-inclusive" format used Are revenues reported by source Are expenses (not expenditures) reported by function or by object classification Is depreciation reported separately Is operating income, or a similar title, displayed Are nonoperating revenues and expenses shown separately after operating income Are capital contributions, extraordinary and special items, and transfers shown separately List any extraordinary and special items.

c. Find the Statement of Cash Flows for the proprietary funds. List the four categories of cash flows. Are they the same as shown in the text Are interest receipts reported as cash flows from investing activities Are interest payments shown as financing activities Is the direct method used Is a reconciliation shown from operating income to net cash provided by operations Are capital assets acquired from financing activities shown as decreases in cash flows from financing activities Does the ending cash balance agree with the cash balance shown in the Statement of Net Assets (note that restricted assets may be included)

d. If your government has a CAFR, look to any combining statements and list the nonmajor enterprise funds. List the internal service funds.

e. Look at the financial statements from the point of view of a financial analyst. Write down the unrestricted net asset balances for each of the major enterprise funds, and (if you have a CAFR) the nonmajor enterprise funds and internal service funds. Look at the long-term debt of major enterprise funds. Can you tell from the statements or the notes whether the debt is general obligation or revenue in nature Write down the income before contributions, extraordinary items, special items, and transfers for each of the funds. Compare these numbers with prior years, if the information is provided in your financial statements. Look at the transfers. Can you tell if the general government is subsidizing or is subsidized by enterprise funds

a. Find the Statement of Net Assets for the proprietary funds. Is the Net Asset or the Balance Sheet format used List the major enterprise funds from that statement. Is the statement classified between current and non- current assets and liabilities Are net assets broken down into the three classifications shown in your text Is a separate column shown for internal service funds

b. Find the Statement of Revenues, Expenses, and Changes in Net Assets for the proprietary funds. Is the "all-inclusive" format used Are revenues reported by source Are expenses (not expenditures) reported by function or by object classification Is depreciation reported separately Is operating income, or a similar title, displayed Are nonoperating revenues and expenses shown separately after operating income Are capital contributions, extraordinary and special items, and transfers shown separately List any extraordinary and special items.

c. Find the Statement of Cash Flows for the proprietary funds. List the four categories of cash flows. Are they the same as shown in the text Are interest receipts reported as cash flows from investing activities Are interest payments shown as financing activities Is the direct method used Is a reconciliation shown from operating income to net cash provided by operations Are capital assets acquired from financing activities shown as decreases in cash flows from financing activities Does the ending cash balance agree with the cash balance shown in the Statement of Net Assets (note that restricted assets may be included)

d. If your government has a CAFR, look to any combining statements and list the nonmajor enterprise funds. List the internal service funds.

e. Look at the financial statements from the point of view of a financial analyst. Write down the unrestricted net asset balances for each of the major enterprise funds, and (if you have a CAFR) the nonmajor enterprise funds and internal service funds. Look at the long-term debt of major enterprise funds. Can you tell from the statements or the notes whether the debt is general obligation or revenue in nature Write down the income before contributions, extraordinary items, special items, and transfers for each of the funds. Compare these numbers with prior years, if the information is provided in your financial statements. Look at the transfers. Can you tell if the general government is subsidizing or is subsidized by enterprise funds

THE SOLUTION TO THIS AND THE FIRST EXERCISE OF CHAPTERS 1 THROUGH 9 WILL DIFFER FROM STUDENT TO STUDENT ASSUMING EACH HAS A DIFFERENT CAFR.

2

What accounting problem arises if an internal service fund is operated at a significant profit What accounting problem arises if an internal service fund is operated at a significant loss

Internal service fund is a proprietary fund. And they are reported in the proprietary fund financial statements in a separate column.

The purpose of internal service fund is to account for all the services and goods provided to other departments of the primary government on a cost reimbursement basis.

Thus, it can be concluded that an internal service fund that accounts all its services and goods provided to other department of primary government at no gain or no loss basis or at break even basis.

In the given choice of situation where the problem that one may face if an internal service fund is operated at a significant profit or significant loss is as illustrated below.

Internal service fund is meant to account for services and goods provided to other department of primary government at cost and hence no operating income or loss can be reported.

However, in case an internal service fund is operated at a significant profit, then that implies to show that the expenditure reported in the general fund is incorrect since it exceeds the factual cost of operating government or otherwise overstated true cost of operating government.

Similarly, if an internal service fund is operated at a significant loss, then it demonstrates to say that the expenditure reported in the general fund is understated true cost of the operating government and thus incurring an operative loss.

These are the accounting problem that persists when internal service fund is operated either at significant profit income or significant loss.

The purpose of internal service fund is to account for all the services and goods provided to other departments of the primary government on a cost reimbursement basis.

Thus, it can be concluded that an internal service fund that accounts all its services and goods provided to other department of primary government at no gain or no loss basis or at break even basis.

In the given choice of situation where the problem that one may face if an internal service fund is operated at a significant profit or significant loss is as illustrated below.

Internal service fund is meant to account for services and goods provided to other department of primary government at cost and hence no operating income or loss can be reported.

However, in case an internal service fund is operated at a significant profit, then that implies to show that the expenditure reported in the general fund is incorrect since it exceeds the factual cost of operating government or otherwise overstated true cost of operating government.

Similarly, if an internal service fund is operated at a significant loss, then it demonstrates to say that the expenditure reported in the general fund is understated true cost of the operating government and thus incurring an operative loss.

These are the accounting problem that persists when internal service fund is operated either at significant profit income or significant loss.

3

Why might it be desirable to operate enterprise funds at a profit

Enterprise fund is a proprietary fund. In fact Proprietary fund consist of internal service fund and Enterprise fund.

Enterprise fund is most opted kind of fund in the governmental organization to carry on their enterprising activity. As the name itself describe enterprise fund is used to record commercial activities carried out by primary government and its component units.

For example, water utility or supply of electricity, public transports are few to mention. They all are known to provide goods and services to the general public and known to be exchange transaction.

Enterprise fund is reported based on economic resource measurement focus and accrual basis of accounting.

However, why operating enterprises fund at a profit is desirable is illustrated here under.

As mentioned above, Enterprise fund is used by the government to account for the commercial value of the goods and services supplied to the general public. Therefore, it may be concluded that, unlike Internal service fund, Enterprise fund is similar to commercial business operating on profits which is necessary to sufficiently fund working capital.

Funding working capital from profits generated is only to ensure that expansion of facilities to the general public is properly and effectively rendered. However, the profit so generated can also be used to pay off debts, if any and also to support government expenditure which otherwise enforce government to impose more taxes.

Therefore, in view of the explanation and the facts put forth above, it is conclusively found that operating Enterprises Fund at a Profit is desirable.

Enterprise fund is most opted kind of fund in the governmental organization to carry on their enterprising activity. As the name itself describe enterprise fund is used to record commercial activities carried out by primary government and its component units.

For example, water utility or supply of electricity, public transports are few to mention. They all are known to provide goods and services to the general public and known to be exchange transaction.

Enterprise fund is reported based on economic resource measurement focus and accrual basis of accounting.

However, why operating enterprises fund at a profit is desirable is illustrated here under.

As mentioned above, Enterprise fund is used by the government to account for the commercial value of the goods and services supplied to the general public. Therefore, it may be concluded that, unlike Internal service fund, Enterprise fund is similar to commercial business operating on profits which is necessary to sufficiently fund working capital.

Funding working capital from profits generated is only to ensure that expansion of facilities to the general public is properly and effectively rendered. However, the profit so generated can also be used to pay off debts, if any and also to support government expenditure which otherwise enforce government to impose more taxes.

Therefore, in view of the explanation and the facts put forth above, it is conclusively found that operating Enterprises Fund at a Profit is desirable.

4

The Village of Seaside Pines prepared the following enterprise fund Trial Balance as of December 31, 2012, the last day of its fiscal year. The enterprise fund was established this year through a transfer from the General Fund.

a. Prepare the closing entries for December 31.

b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31.

c. Prepare the Net Asset Section of the December 31 balance sheet. (Assume that the revenue bonds were issued to acquire capital assets and there are no restricted assets.)

a. Prepare the closing entries for December 31.b. Prepare the Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31.

c. Prepare the Net Asset Section of the December 31 balance sheet. (Assume that the revenue bonds were issued to acquire capital assets and there are no restricted assets.)

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

5

Using the information provided in exercise 6-4, prepare the reconciliation of operating income to net cash provided by operating activities that would appear at the bottom of the December 31 Statement of Cash Flows. Recall that the beginning balance of all asset and liabilities is zero.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

6

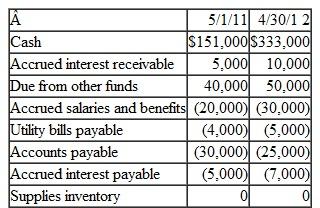

The Town of Wilson has a Water Utility Fund with the following trial balance as of July 1, 2011, the first day of the fiscal year:

During the year ended June 30, 2012, the following transactions and events occurred in the Town of Wilson Water Utility Fund:

1. Accrued expenses at July 1, 2011, were paid in cash.

2. Billings to nongovernmental customers for water usage for the year amounted to $1,400,000; billings to the General Fund amounted to $57,000.

3. Liabilities for the following were recorded during the year:

4. Materials and supplies were used in the amount of $265,700, all for costs of sales and services.

5. $8,000 of old accounts receivable were written off.

6. Accounts receivable collections totaled $1,450,000 from nongovernmental customers and $48,400 from the General Fund.

7. $1,035,000 of accounts payable were paid in cash.

8. One year's interest in the amount of $175,000 was paid.

9. Construction was completed on plant assets costing $135,000; that amount was transferred to Utility Plant in Service.

10. Depreciation was recorded in the amount of $235,000.

11. Interest in the amount of $25,000 was charged to Construction Work in Progress. (This was previously paid in item 8.)

12. The Allowance for Uncollectible Accounts was increased by $13,100.

13. As required by the loan agreement, cash in the amount of $100,000 was transferred to Restricted Assets for eventual redemption of the bonds.

14. Accrued expenses, all related to costs of sales and services, amounted to $47,000.

15. Nominal accounts for the year were closed to Net Assets.

Required:

a. Record the transactions for the year in general journal form.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets.

c. Prepare a Statement of Net Assets as of June 30, 2012.

d. Prepare a Statement of Cash Flows for the Year Ended June 30, 2012. Assume all debt and interest are related to capital outlay. Assume the entire $212,200 construction work in progress liability (see item 3) was paid in entry 7. Include restricted assets as cash and cash equivalents.

During the year ended June 30, 2012, the following transactions and events occurred in the Town of Wilson Water Utility Fund:1. Accrued expenses at July 1, 2011, were paid in cash.

2. Billings to nongovernmental customers for water usage for the year amounted to $1,400,000; billings to the General Fund amounted to $57,000.

3. Liabilities for the following were recorded during the year:

4. Materials and supplies were used in the amount of $265,700, all for costs of sales and services.5. $8,000 of old accounts receivable were written off.

6. Accounts receivable collections totaled $1,450,000 from nongovernmental customers and $48,400 from the General Fund.

7. $1,035,000 of accounts payable were paid in cash.

8. One year's interest in the amount of $175,000 was paid.

9. Construction was completed on plant assets costing $135,000; that amount was transferred to Utility Plant in Service.

10. Depreciation was recorded in the amount of $235,000.

11. Interest in the amount of $25,000 was charged to Construction Work in Progress. (This was previously paid in item 8.)

12. The Allowance for Uncollectible Accounts was increased by $13,100.

13. As required by the loan agreement, cash in the amount of $100,000 was transferred to Restricted Assets for eventual redemption of the bonds.

14. Accrued expenses, all related to costs of sales and services, amounted to $47,000.

15. Nominal accounts for the year were closed to Net Assets.

Required:

a. Record the transactions for the year in general journal form.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets.

c. Prepare a Statement of Net Assets as of June 30, 2012.

d. Prepare a Statement of Cash Flows for the Year Ended June 30, 2012. Assume all debt and interest are related to capital outlay. Assume the entire $212,200 construction work in progress liability (see item 3) was paid in entry 7. Include restricted assets as cash and cash equivalents.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

7

The City of Sandwich purchased a swimming pool from a private operator as of April 1, 2012, for $500,000. Of the $500,000, $250,000 was provided by a one-time contribution from the General Fund, and $250,000 was provided by a loan from the First National Bank, secured by a note. The loan has an annual interest rate 6 percent, payable semiannually on October 1 and April 1; principal payments of $100,000 are to be made annually, beginning on April 1, 2013. The city has a calendar year as its fiscal year. During the year ended December 31, 2012, the following transactions occurred, related to the City of Sandwich Swimming Pool:

1. The amounts were received from the City General Fund and the First National Bank.

2. A short-term loan was provided in the amount of $100,000 from the Water Utility Fund.

3. The purchase of the pool was recorded. Based on an appraisal, it was decided to allocate $100,000 to the land, $300,000 to improvements other than buildings (the pool), and $100,000 to the building. There is a 10-year life for both the pool and the building, and depreciation is to be recorded annually, based on monthly allocations (do not record depreciation until entry 10).

4. Charges to patrons during the season amounted to $340,000, all received in cash.

5. Salaries paid to employees amounted to $200,000, all paid in cash, of which $170,000 was cost of services, and $30,000 was administration.

6. Supplies purchased amounted to $40,000; all but $5,000 was used. Cash was paid for the supplies, all of which was for cost of sales and services.

7. Administrative expenses amounted to $12,000, paid in cash.

8. The first interest payment was made to the First National Bank.

9. The short-term loan was repaid to the Water Utility Fund.

10. Depreciation was accrued for the year. Record 9/12 of the annual amounts.

11. Interest was accrued for the year.

12. Closing entries were prepared.

Required:

a. Prepare entries to record the transactions.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the Year Ended December 31, 2012, for the City of Sandwich Swimming Pool Fund.

c. Prepare a Statement of Net Assets as of December 31, 2012, for the City of Sandwich Swimming Pool Fund.

d. Prepare a Statement of Cash Flows for the Year Ended December 31, 2012, for the City of Sandwich Swimming Pool Fund.

1. The amounts were received from the City General Fund and the First National Bank.

2. A short-term loan was provided in the amount of $100,000 from the Water Utility Fund.

3. The purchase of the pool was recorded. Based on an appraisal, it was decided to allocate $100,000 to the land, $300,000 to improvements other than buildings (the pool), and $100,000 to the building. There is a 10-year life for both the pool and the building, and depreciation is to be recorded annually, based on monthly allocations (do not record depreciation until entry 10).

4. Charges to patrons during the season amounted to $340,000, all received in cash.

5. Salaries paid to employees amounted to $200,000, all paid in cash, of which $170,000 was cost of services, and $30,000 was administration.

6. Supplies purchased amounted to $40,000; all but $5,000 was used. Cash was paid for the supplies, all of which was for cost of sales and services.

7. Administrative expenses amounted to $12,000, paid in cash.

8. The first interest payment was made to the First National Bank.

9. The short-term loan was repaid to the Water Utility Fund.

10. Depreciation was accrued for the year. Record 9/12 of the annual amounts.

11. Interest was accrued for the year.

12. Closing entries were prepared.

Required:

a. Prepare entries to record the transactions.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the Year Ended December 31, 2012, for the City of Sandwich Swimming Pool Fund.

c. Prepare a Statement of Net Assets as of December 31, 2012, for the City of Sandwich Swimming Pool Fund.

d. Prepare a Statement of Cash Flows for the Year Ended December 31, 2012, for the City of Sandwich Swimming Pool Fund.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

8

The Village of Parry reported the following for its Print Shop Fund for the year ended April 30, 2012.

The Print Shop Fund records also revealed the following:

The following balances were observed in current asset and current liability accounts. ( ) denote credit balances:

Prepare a Statement of Cash Flows for the Village of Parry Print Shop Fund for the Year Ended April 30, 2012. Include the reconciliation of operating income to net cash provided by operating activities.

The Print Shop Fund records also revealed the following: The following balances were observed in current asset and current liability accounts. ( ) denote credit balances: Prepare a Statement of Cash Flows for the Village of Parry Print Shop Fund for the Year Ended April 30, 2012. Include the reconciliation of operating income to net cash provided by operating activities. Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

9

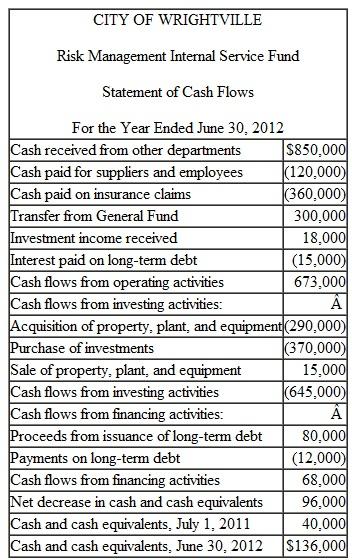

The following is a statement of cash flows for the risk management internal service fund of the City of Wrightville. An inexperienced accountant prepared the statement using the FASB format rather than the format required by GASB. All long-term debt was issued to purchase capital assets. The transfer from the General Fund was to establish the internal service fund and provide the initial working capital necessary for operations.

Prepare a statement of cash flows using the appropriate format as required by GASB. You do not need to prepare the reconciliation of operating income to cash flow from operations.

Prepare a statement of cash flows using the appropriate format as required by GASB. You do not need to prepare the reconciliation of operating income to cash flow from operations. Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

10

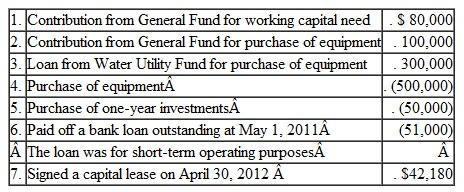

The Town of Frostbite self-insures for some of its liability claims and purchases insurance for others. In an effort to consolidate its risk management activities, the Town recently decided to establish an internal service fund, the Risk Management Fund. The Risk Management Fund's purpose is to obtain liability coverage for the Town, to pay claims not covered by the insurance, and to charge individual departments in amounts sufficient to cover current-year costs and to establish a reserve for losses.

The Town reports proprietary fund expenses by object classification using the following accounts: Personnel services (salaries), Contractual services (for the expired portion of prepaid service contracts), Depreciation, and Insurance Claims. The following transactions relate to the year ended

December 31, 2012, the first year of the Risk Management Fund's operations.

1. The Risk Management Fund is established through a transfer of $500,000 from the General Fund and a long-term advance from the water utility enterprise fund of $250,000.

2. The Risk Management Fund purchased (prepaid) insurance coverage through several commercial insurance companies for $200,000. The policies purchased require the Town to self-insure for $25,000 per incident.

3. Office Equipment is purchased for $10,000.

4. $450,000 is invested in marketable securities.

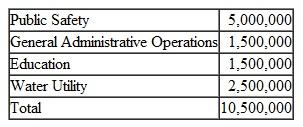

5. Actuarial estimates were made in the previous fiscal year to determine the amount necessary to attain the goal of accumulating sufficient funds to cover current-year claims and to establish a reserve for losses. It was determined that the General Fund and water utility be assessed a fee of 6 percent of total wages and salaries (Interfund premium). Wages and salaries by department are as follows:

6. Cash received in payment of interfund premiums from the General Fund totaled $275,000 and cash received from the Water Utility totaled $100,000.

7. Interest and dividends received totaled $27,000.

8. Salaries for the Risk Management Fund amounted to $200,000 (all paid during the year).

9. Claims paid under self-insurance totaled $150,000 during the year.

10. The office equipment is depreciated on the straight-line basis over 5 years.

11. At year-end, $190,000 of the insurance policies purchased in January had expired.

12. The market value of investments at December 31 totaled $456,000 ( Hint: credit Net Increase in Fair Market Value of Investments ).

13. In addition to the claims paid in entry 9 above, estimates for the liability for the Town's portion of known claims since the inception of the Town's self-insurance program totaled $90,000.

Required:

a. Prepare the journal entries (including closing entries) to record the transactions.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012, for the Risk Management Fund

c. Prepare a Statement of Net Assets as of December 31, 2012, for the Risk Management Fund

d. Prepare a Statement of Cash Flows for the year ended December 31, 2012, for the Risk Management Fund. Assume $10,000 of the transfer from the General Fund was for the purchase of the equipment. Further, assume the remainder of the transfer from the General Fund and all of the advance from the enterprise fund are to establish working capital (noncapital related financing).

e. Comment on whether the interfund premium of 6 percent of wages and salaries is adequate.

The Town reports proprietary fund expenses by object classification using the following accounts: Personnel services (salaries), Contractual services (for the expired portion of prepaid service contracts), Depreciation, and Insurance Claims. The following transactions relate to the year ended

December 31, 2012, the first year of the Risk Management Fund's operations.

1. The Risk Management Fund is established through a transfer of $500,000 from the General Fund and a long-term advance from the water utility enterprise fund of $250,000.

2. The Risk Management Fund purchased (prepaid) insurance coverage through several commercial insurance companies for $200,000. The policies purchased require the Town to self-insure for $25,000 per incident.

3. Office Equipment is purchased for $10,000.

4. $450,000 is invested in marketable securities.

5. Actuarial estimates were made in the previous fiscal year to determine the amount necessary to attain the goal of accumulating sufficient funds to cover current-year claims and to establish a reserve for losses. It was determined that the General Fund and water utility be assessed a fee of 6 percent of total wages and salaries (Interfund premium). Wages and salaries by department are as follows:

6. Cash received in payment of interfund premiums from the General Fund totaled $275,000 and cash received from the Water Utility totaled $100,000.7. Interest and dividends received totaled $27,000.

8. Salaries for the Risk Management Fund amounted to $200,000 (all paid during the year).

9. Claims paid under self-insurance totaled $150,000 during the year.

10. The office equipment is depreciated on the straight-line basis over 5 years.

11. At year-end, $190,000 of the insurance policies purchased in January had expired.

12. The market value of investments at December 31 totaled $456,000 ( Hint: credit Net Increase in Fair Market Value of Investments ).

13. In addition to the claims paid in entry 9 above, estimates for the liability for the Town's portion of known claims since the inception of the Town's self-insurance program totaled $90,000.

Required:

a. Prepare the journal entries (including closing entries) to record the transactions.

b. Prepare a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012, for the Risk Management Fund

c. Prepare a Statement of Net Assets as of December 31, 2012, for the Risk Management Fund

d. Prepare a Statement of Cash Flows for the year ended December 31, 2012, for the Risk Management Fund. Assume $10,000 of the transfer from the General Fund was for the purchase of the equipment. Further, assume the remainder of the transfer from the General Fund and all of the advance from the enterprise fund are to establish working capital (noncapital related financing).

e. Comment on whether the interfund premium of 6 percent of wages and salaries is adequate.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

11

The City of Evansville operated a summer camp program for at-risk youth. Businesses and nonprofit organizations sponsor one or more youth by paying the registration fee for program participants. The following Statement of Cash Receipts and Disbursements summarizes the activity in the program's bank account for the year.

1. At the beginning of 2012, the program had unrestricted cash of

$12,000.

2. The loan from the bank is dated April 1 and is for a five-year period. Interest (6 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012.

3. The bus was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 5 years (straight line basis-use monthly depreciation).

4. All invoices and salaries related to 2012 had been paid by close of business on December 31, except for the employer's portion of December payroll taxes, totaling $900.

a. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets assuming the City intends to treat the summer camp program as an enterprise fund.

b. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenditures, and Changes in Fund Balance assuming the City intends to treat the summer camp program as a special revenue fund.

1. At the beginning of 2012, the program had unrestricted cash of

$12,000.

2. The loan from the bank is dated April 1 and is for a five-year period. Interest (6 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012.3. The bus was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 5 years (straight line basis-use monthly depreciation).

4. All invoices and salaries related to 2012 had been paid by close of business on December 31, except for the employer's portion of December payroll taxes, totaling $900.

a. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets assuming the City intends to treat the summer camp program as an enterprise fund.

b. Prepare the journal entries, closing entries, and a Statement of Revenues, Expenditures, and Changes in Fund Balance assuming the City intends to treat the summer camp program as a special revenue fund.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

12

The Town of Thomaston has a Solid Waste Landfill Enterprise Fund with the following trial balance as of January 1, 2012, the first day of the fiscal year.

During the year, the following transactions and events occurred:

1. Citizens and trash companies dumped 500,000 tons of waste in the landfill, which charges $5.50 a ton payable in cash.

2. Diesel fuel purchases totaled $343,000 (on account).

3. Accounts payable totaling $430,000 were paid.

4. Diesel fuel used in operations amounted to $405,000.

5. Depreciation was recorded in the amount of $735,000.

6. Salaries totaling $75,000 were paid.

7. Future costs to close the landfill and postclosure care costs are expected to total $76,250,000. The total capacity of the landfill is expected to be 25,000,000 tons of waste.

Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012.

During the year, the following transactions and events occurred:1. Citizens and trash companies dumped 500,000 tons of waste in the landfill, which charges $5.50 a ton payable in cash.

2. Diesel fuel purchases totaled $343,000 (on account).

3. Accounts payable totaling $430,000 were paid.

4. Diesel fuel used in operations amounted to $405,000.

5. Depreciation was recorded in the amount of $735,000.

6. Salaries totaling $75,000 were paid.

7. Future costs to close the landfill and postclosure care costs are expected to total $76,250,000. The total capacity of the landfill is expected to be 25,000,000 tons of waste.

Prepare the journal entries, closing entries, and a Statement of Revenues, Expenses, and Changes in Fund Net Assets for the year ended December 31, 2012.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

13

Jefferson County operates a centralized motor pool to service county

vehicles. At the end of 2011, the Motor Pool Internal Service Fund had the following account balances:

The following events took place during 2012:

1. Additional supplies were purchased on account in the amount of $35,000.

2. Services provided to other departments on account totaled $95,000. A total of $65,000 was for departments in the General Fund and $30,000 for enterprise fund departments.

3. Supplies used amounted to $36,700.

4. Payments made on accounts payable amounted to $38,200.

5. Cash collected from the General Fund totaled $57,000 and cash colected from the enterprise fund totaled $30,000.

6. Salaries were paid in the amount of $47,000. Included in this amount is the accrued wages payable at the end of 2011. All of these are determined to be part of the cost of services provided.

7. In a previous year, the enterprise fund loaned the Motor Pool money under an advance for the purpose of purchasing garage equipment. In the current year, the Motor Pool repaid the enterprise fund $7,000 of this amount.

8. On July 1, 2012, the Motor Pool Fund borrowed $10,000 from the bank, signing a 12 percent note that is due on June 30, 2013. The borrowings are not related to capital asset purchases but were made to provide working capital.

Additional information includes:

9. Depreciation for the year amounted to $7,500.

10. The payment of interest on the note is payable on June 30, 2013.

11. Unpaid wages relating to the final week of the year totaled $420.

Using the Excel template provided; a separate tab is provided for each of the requirements:

a. Prepare journal entries.

b. Post entries to the T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Fund Net Assets.

e. Prepare a Statement of Net Assets.

f. Prepare a Statement of Cash Flows for the year ending December-31-2012.

vehicles. At the end of 2011, the Motor Pool Internal Service Fund had the following account balances:

The following events took place during 2012:1. Additional supplies were purchased on account in the amount of $35,000.

2. Services provided to other departments on account totaled $95,000. A total of $65,000 was for departments in the General Fund and $30,000 for enterprise fund departments.

3. Supplies used amounted to $36,700.

4. Payments made on accounts payable amounted to $38,200.

5. Cash collected from the General Fund totaled $57,000 and cash colected from the enterprise fund totaled $30,000.

6. Salaries were paid in the amount of $47,000. Included in this amount is the accrued wages payable at the end of 2011. All of these are determined to be part of the cost of services provided.

7. In a previous year, the enterprise fund loaned the Motor Pool money under an advance for the purpose of purchasing garage equipment. In the current year, the Motor Pool repaid the enterprise fund $7,000 of this amount.

8. On July 1, 2012, the Motor Pool Fund borrowed $10,000 from the bank, signing a 12 percent note that is due on June 30, 2013. The borrowings are not related to capital asset purchases but were made to provide working capital.

Additional information includes:

9. Depreciation for the year amounted to $7,500.

10. The payment of interest on the note is payable on June 30, 2013.

11. Unpaid wages relating to the final week of the year totaled $420.

Using the Excel template provided; a separate tab is provided for each of the requirements:

a. Prepare journal entries.

b. Post entries to the T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Fund Net Assets.

e. Prepare a Statement of Net Assets.

f. Prepare a Statement of Cash Flows for the year ending December-31-2012.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

14

Rural County is an agricultural community located hundreds of miles from any metropolitan center. The County established a television reception improvement fund to serve the public interest by constructing and operating television translator stations. TV translator stations serve communities that cannot receive the signals of free over-the-air TV stations because they are too far away from a broadcasting TV station. Because of the largest distances between customers, commercial cable TV providers are also not inclined to serve rural communities. The fund charges TV owners a monthly fee of $15. The fund was established on December 20, 2011, with a transfer of cash from the General Fund of $100,000. On December 31, 2011, the fund acquired land for its translator stations in the amount of $40,000. The remaining cash and the land are the only resources held by the fund at the beginning of 2012.

1. Other than beginning account balances, no entries have been made in the general ledger.

2. The county prepared a budget for 2012 with estimated customer fees of $30,000, operating costs of $30,000, capital costs of $65,000, and estimated loan proceeds of $55,000.

3. The following information was taken from the checkbook for the year ended December-31-2012.

4. The loan from the bank is dated April 1 and is for a five-year period. Interest (8 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012. The County has elected not to establish a debt service fund but will pay the interest on this note from the Television Reception Improvement Fund.

5. The machinery was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 10 years (straight-line basis).

6. In January 2013, customers remitted fees totaling $2,500 for December 2012 service.

7. Supplies of $500 were received on December 29 and paid in January 2013.

8. Unused supplies on hand amounted to $760 at December 31, 2012.

9. Utilities are paid in the following month. The utility bill for December 2012 was received on January 4, 2013 in the amount of $620. (Utility bills are recorded through accounts payable.)

10. On December 21, the company placed an order for a new computerized control switch in the amount of $1,500 to be delivered and paid in January 2013.

Required:

You have been asked to provide financial statements for the upcoming County Board meeting for the Television Reception Improvement Fund.

Part 1: Assume the County chooses to report the Television Reception Improvement Fund as a Special Revenue Fund following modified accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance.

e. Prepare a Balance Sheet, assuming there are no restricted or committed fund net resources.

Part 2: Assume the County chooses to report the Television Reception Improvement Fund as an Enterprise Fund following accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Net Assets.

e. Prepare a Statement of Net Assets, assuming the bank note is related to capital asset acquisitions.

The Excel template contains separate tabs for (1) special revenue fund journal entries and T-accounts, (2) special revenue fund closing entries, (3) special revenue fund financial statements, (4) enterprise fund journal entries and T-accounts, (5) enterprise fund closing entries, and (6) enterprise fund financial statements. Both the T-accounts and financial statements contain accounts you will not need under either the modified accrual or accrual bases. Similarly, you may not need to record some of the events, depending on the basis of accounting.

1. Other than beginning account balances, no entries have been made in the general ledger.

2. The county prepared a budget for 2012 with estimated customer fees of $30,000, operating costs of $30,000, capital costs of $65,000, and estimated loan proceeds of $55,000.

3. The following information was taken from the checkbook for the year ended December-31-2012.

4. The loan from the bank is dated April 1 and is for a five-year period. Interest (8 percent annual rate) is paid on October 1 and April 1 of each year, beginning October 1, 2012. The County has elected not to establish a debt service fund but will pay the interest on this note from the Television Reception Improvement Fund.5. The machinery was purchased on April 1 with the proceeds provided by the bank loan and has an estimated useful life of 10 years (straight-line basis).

6. In January 2013, customers remitted fees totaling $2,500 for December 2012 service.

7. Supplies of $500 were received on December 29 and paid in January 2013.

8. Unused supplies on hand amounted to $760 at December 31, 2012.

9. Utilities are paid in the following month. The utility bill for December 2012 was received on January 4, 2013 in the amount of $620. (Utility bills are recorded through accounts payable.)

10. On December 21, the company placed an order for a new computerized control switch in the amount of $1,500 to be delivered and paid in January 2013.

Required:

You have been asked to provide financial statements for the upcoming County Board meeting for the Television Reception Improvement Fund.

Part 1: Assume the County chooses to report the Television Reception Improvement Fund as a Special Revenue Fund following modified accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenditures, and Changes in Fund Balance.

e. Prepare a Balance Sheet, assuming there are no restricted or committed fund net resources.

Part 2: Assume the County chooses to report the Television Reception Improvement Fund as an Enterprise Fund following accrual basis statements. Using the Excel template provided,

a. Prepare journal entries recording the events above for the year ending December 31, 2012.

b. Post the journal entries to T-accounts.

c. Prepare closing entries.

d. Prepare a Statement of Revenues, Expenses and Changes in Net Assets.

e. Prepare a Statement of Net Assets, assuming the bank note is related to capital asset acquisitions.

The Excel template contains separate tabs for (1) special revenue fund journal entries and T-accounts, (2) special revenue fund closing entries, (3) special revenue fund financial statements, (4) enterprise fund journal entries and T-accounts, (5) enterprise fund closing entries, and (6) enterprise fund financial statements. Both the T-accounts and financial statements contain accounts you will not need under either the modified accrual or accrual bases. Similarly, you may not need to record some of the events, depending on the basis of accounting.

Unlock Deck

Unlock for access to all 14 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 14 flashcards in this deck.