Deck 11: College and University Accounting

Full screen (f)

Question

Obtain a copy of the annual report of a private college or university. Answer the following questions from the report. For examples, try:

a. Is the annual report audited Name the auditing firm.

b. Does the organization present (1) a single Statement of Activities, or does it present (2) a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets

c. What additional financial statements are presented

d. Does the organization have temporarily restricted net assets What is the amount of the net assets released from restrictions in the current period

e. Does the organization have permanently restricted net assets

f. Is there a note describing split interest agreements

a. Is the annual report audited Name the auditing firm.

b. Does the organization present (1) a single Statement of Activities, or does it present (2) a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets

c. What additional financial statements are presented

d. Does the organization have temporarily restricted net assets What is the amount of the net assets released from restrictions in the current period

e. Does the organization have permanently restricted net assets

f. Is there a note describing split interest agreements

Question

Question

Question

Question

Question

Question

Question

Presented below are the closing entries for Lee College, a private not-forprofit, for the year ended December 31, 2014.

Assume the January 1, 2015, net asset balances are as follows: $1,000,000 unrestricted net assets; $300,000 temporarily restricted net assets; and $1,760,000 permanently restricted net assets.

a. Prepare a Statement of Activities using the format presented in Illustration 10-2.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets.

Assume the January 1, 2015, net asset balances are as follows: $1,000,000 unrestricted net assets; $300,000 temporarily restricted net assets; and $1,760,000 permanently restricted net assets.

a. Prepare a Statement of Activities using the format presented in Illustration 10-2.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets.

Question

Korner College began the year with the following account balances:

During the year ended June 30, 2015, the following transactions occurred:

1. Cash collections included: accounts receivable, $1,227,000; accrued interest receivable, $49,000; contributions receivable, $4,985,000; and for loans to students and faculty, $155,000. Of the contributions, $1,900,000 was for plant acquisition (use for cash flow statement).

2. Cash payments included accounts payable, $130,000; and the current portion of long-term debt, $150,000.

3. Unrestricted revenues included tuition and fees, $21,740,000; unrestricted income on endowment investments, $400,000; other investment income, $300,000; and sales and services of auxiliary enterprises, $14,800,000. A total of $33,690,000 in cash was received, and the following receivables were increased: accounts receivable, $3,500,000; accrued interest receivable, $50,000.

4. Scholarships, for which no services were required, were applied to student accounts in the amount of $2,700,000.

5. Contributions were received in the following amounts: unrestricted, $4,900,000; temporarily restricted, $5,400,000; permanently restricted, $2,000,000. Of that amount, $7,020,000 was received in cash; contributions receivable increased $5,280,000. None of these contributions were restricted to plant acquisition.

6. Accounts receivable were written off in the amount of $50,000, and contributions receivable were written off in the amount of $20,000. Provisions for bad debts were increased by $175,000 for accounts receivable (tuition and fees) and by $30,000 for unrestricted contributions receivable.

7. Expenses, exclusive of depreciation, were as follows: instruction, $18,460,000; research, $1,980,000; public service, $1,910,000; academic support, $990,000; student services, $1,310,000; institutional support, $1,050,000; and auxiliary enterprises, $13,500,000. The college had an uninsured flood loss in the amount of $600,000. Cash was paid in the amount of $39,200,000, and accounts payable increased by $600,000.

8. Depreciation was charged in the amount of $2,100,000. One-third of that amount was charged each to instruction, institutional support, and auxiliary enterprises.

9. Interest income was earned as follows: addition to temporarily restricted net assets, $30,000; addition to permanently restricted net assets, $35,000. Of those amounts, $55,000 was received in cash and $10,000 was accrued at year-end.

10. Research expense was incurred in the amount of $1,700,000; and property, plant, and equipment were acquired in the amount of $1,400,000. Both were paid in cash.

11. Reclassifications were made from temporarily restricted to unrestricted net assets as follows: on the basis of time restrictions, $1,600,000; for program restrictions (research), $1,700,000; and for fixed asset acquisition restrictions, $1,400,000. Korner records fixed assets as increases in unrestricted net assets.

12. Long-term investments, with a carrying value of $1,700,000, were sold for $1,770,000. Of the $70,000 gain, $40,000 was temporarily restricted by donor agreement and $30,000 is required to be added to permanently restricted net assets.

13. Additional investments were purchased in the amount of $3,970,000. Loans were made to students and faculty in the amount of $200,000.

14. In addition to 13 above, the board of trustees decided to purchase $2,000,000 in long-term investments, from unrestricted net assets, to create a quasi-endowment.

15. At year-end, the fair value of investments increased by $530,000. Of that amount, $300,000 increased unrestricted net assets, $30,000 increased temporarily restricted net assets, and $200,000 increased permanently restricted net assets.

16. $150,000 of the long-term debt was reclassified as a current liability.

17. Closing entries were prepared for ( a ) unrestricted net assets, ( b ) temporarily restricted net assets, and ( c ) permanently restricted net assets.

Required:

a. Prepare journal entries for each of the above transactions.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets for Korner College for the fiscal year ended June 30, 2015.

c. Prepare a Statement of Changes in Net Assets for Korner College for the fiscal year ended June 30, 2015.

d. Prepare a Statement of Financial Position for Korner College as of June 30, 2015.

e. Prepare a Statement of Cash Flows for Korner College for the year ended June 30, 2015. Use the indirect method.

During the year ended June 30, 2015, the following transactions occurred:

1. Cash collections included: accounts receivable, $1,227,000; accrued interest receivable, $49,000; contributions receivable, $4,985,000; and for loans to students and faculty, $155,000. Of the contributions, $1,900,000 was for plant acquisition (use for cash flow statement).

2. Cash payments included accounts payable, $130,000; and the current portion of long-term debt, $150,000.

3. Unrestricted revenues included tuition and fees, $21,740,000; unrestricted income on endowment investments, $400,000; other investment income, $300,000; and sales and services of auxiliary enterprises, $14,800,000. A total of $33,690,000 in cash was received, and the following receivables were increased: accounts receivable, $3,500,000; accrued interest receivable, $50,000.

4. Scholarships, for which no services were required, were applied to student accounts in the amount of $2,700,000.

5. Contributions were received in the following amounts: unrestricted, $4,900,000; temporarily restricted, $5,400,000; permanently restricted, $2,000,000. Of that amount, $7,020,000 was received in cash; contributions receivable increased $5,280,000. None of these contributions were restricted to plant acquisition.

6. Accounts receivable were written off in the amount of $50,000, and contributions receivable were written off in the amount of $20,000. Provisions for bad debts were increased by $175,000 for accounts receivable (tuition and fees) and by $30,000 for unrestricted contributions receivable.

7. Expenses, exclusive of depreciation, were as follows: instruction, $18,460,000; research, $1,980,000; public service, $1,910,000; academic support, $990,000; student services, $1,310,000; institutional support, $1,050,000; and auxiliary enterprises, $13,500,000. The college had an uninsured flood loss in the amount of $600,000. Cash was paid in the amount of $39,200,000, and accounts payable increased by $600,000.

8. Depreciation was charged in the amount of $2,100,000. One-third of that amount was charged each to instruction, institutional support, and auxiliary enterprises.

9. Interest income was earned as follows: addition to temporarily restricted net assets, $30,000; addition to permanently restricted net assets, $35,000. Of those amounts, $55,000 was received in cash and $10,000 was accrued at year-end.

10. Research expense was incurred in the amount of $1,700,000; and property, plant, and equipment were acquired in the amount of $1,400,000. Both were paid in cash.

11. Reclassifications were made from temporarily restricted to unrestricted net assets as follows: on the basis of time restrictions, $1,600,000; for program restrictions (research), $1,700,000; and for fixed asset acquisition restrictions, $1,400,000. Korner records fixed assets as increases in unrestricted net assets.

12. Long-term investments, with a carrying value of $1,700,000, were sold for $1,770,000. Of the $70,000 gain, $40,000 was temporarily restricted by donor agreement and $30,000 is required to be added to permanently restricted net assets.

13. Additional investments were purchased in the amount of $3,970,000. Loans were made to students and faculty in the amount of $200,000.

14. In addition to 13 above, the board of trustees decided to purchase $2,000,000 in long-term investments, from unrestricted net assets, to create a quasi-endowment.

15. At year-end, the fair value of investments increased by $530,000. Of that amount, $300,000 increased unrestricted net assets, $30,000 increased temporarily restricted net assets, and $200,000 increased permanently restricted net assets.

16. $150,000 of the long-term debt was reclassified as a current liability.

17. Closing entries were prepared for ( a ) unrestricted net assets, ( b ) temporarily restricted net assets, and ( c ) permanently restricted net assets.

Required:

a. Prepare journal entries for each of the above transactions.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets for Korner College for the fiscal year ended June 30, 2015.

c. Prepare a Statement of Changes in Net Assets for Korner College for the fiscal year ended June 30, 2015.

d. Prepare a Statement of Financial Position for Korner College as of June 30, 2015.

e. Prepare a Statement of Cash Flows for Korner College for the year ended June 30, 2015. Use the indirect method.

Question

Presented below are comparative post closing trial balances for a college. In addition, cash transactions for the year ended December 31, 2015, are summarized in the T-account.

Comparative activity statements have been prepared for the year ended December 31, 2015, assuming the college is: ( a ) a private not-for-profit (Statement of Activities) and ( b ) a public college (Statement of Revenues, Expenses, and Changes in Fund Net Assets). These are provided in the first tab of the Excel file template.

Using the information above and the Excel template provided, prepare statements of cash flow assuming the college is: ( a ) a private not-for-profit and ( b ) a public college. Assume that all long-term debt is associated with the purchase of property, plant, and equipment.

Comparative activity statements have been prepared for the year ended December 31, 2015, assuming the college is: ( a ) a private not-for-profit (Statement of Activities) and ( b ) a public college (Statement of Revenues, Expenses, and Changes in Fund Net Assets). These are provided in the first tab of the Excel file template.

Using the information above and the Excel template provided, prepare statements of cash flow assuming the college is: ( a ) a private not-for-profit and ( b ) a public college. Assume that all long-term debt is associated with the purchase of property, plant, and equipment.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/10

Play

Full screen (f)

Deck 11: College and University Accounting

1

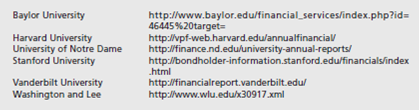

Obtain a copy of the annual report of a private college or university. Answer the following questions from the report. For examples, try:

a. Is the annual report audited Name the auditing firm.

b. Does the organization present (1) a single Statement of Activities, or does it present (2) a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets

c. What additional financial statements are presented

d. Does the organization have temporarily restricted net assets What is the amount of the net assets released from restrictions in the current period

e. Does the organization have permanently restricted net assets

f. Is there a note describing split interest agreements

a. Is the annual report audited Name the auditing firm.

b. Does the organization present (1) a single Statement of Activities, or does it present (2) a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets

c. What additional financial statements are presented

d. Does the organization have temporarily restricted net assets What is the amount of the net assets released from restrictions in the current period

e. Does the organization have permanently restricted net assets

f. Is there a note describing split interest agreements

From the annual report of Harvard University 2013-14 following points are noted-

(a)

Annual report 2013-14 has been audited by Price water house Coopers LLP, 125, High Street, Boston, MA 02110.

(b)

University has prepared a single statement of activities. Three separate columns are used here to indicate unrestricted, temporarily restricted and permanently restricted net asset. Also there are two columns indicating total net assets for the period 2013 and 2014.

(c)

Additional financial statement includes statement of changes in Net Assets of the Endowment. It has been shown analytically by showing funds taken from unrestricted, temporarily restricted and permanently restricted class of net assets.

(d)

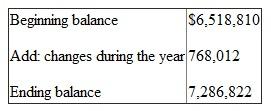

Yes university has temporarily restricted net assets. University has released from temporarily restrictive net asset category to unrestrictive category. The amount is $1,650,254.

(e)

Oxford University has net asset in permanently restrictive category also. The amount is -

(f)

(f)

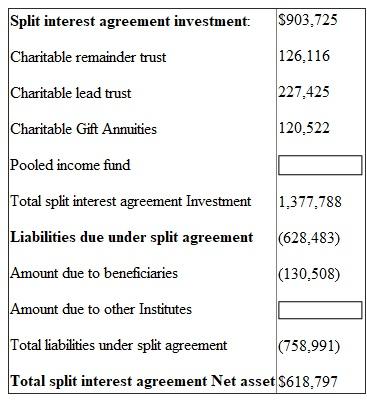

It is an agreement to share donations with different trusts. Annual report also contains details of split agreement. There is a note (11) indicating the detailed break up of split agreement.

As per notes 11 the composition of split agreement is as follows-

(a)

Annual report 2013-14 has been audited by Price water house Coopers LLP, 125, High Street, Boston, MA 02110.

(b)

University has prepared a single statement of activities. Three separate columns are used here to indicate unrestricted, temporarily restricted and permanently restricted net asset. Also there are two columns indicating total net assets for the period 2013 and 2014.

(c)

Additional financial statement includes statement of changes in Net Assets of the Endowment. It has been shown analytically by showing funds taken from unrestricted, temporarily restricted and permanently restricted class of net assets.

(d)

Yes university has temporarily restricted net assets. University has released from temporarily restrictive net asset category to unrestrictive category. The amount is $1,650,254.

(e)

Oxford University has net asset in permanently restrictive category also. The amount is -

(f)It is an agreement to share donations with different trusts. Annual report also contains details of split agreement. There is a note (11) indicating the detailed break up of split agreement.

As per notes 11 the composition of split agreement is as follows-

2

For each of the following, identify (1) which accounting standards-setting body has primary authority, (2) the required financial statements, and (3) the account titles used in the equity section of the balance sheet or equivalent statement.

a. Public (government-owned) colleges and universities.

b. Private not-for-profit colleges and universities.

c. Investor-owned proprietary schools.

a. Public (government-owned) colleges and universities.

b. Private not-for-profit colleges and universities.

c. Investor-owned proprietary schools.

a.

(1)

GSAB (Governmental Accounting Standard Board) has primary authority over setting accounting standards over government colleges and universities.

(2)

Statement of Net assets, Statement of Revenues, Expenses and Changes in Net Assets and Statement of Cash flows are the required Financial statements.

(3)

The following Equity accounts are required:

Net Assets (Position) showing Unrestricted, Restricted and Net investment in capital assets.

b.

(1)

FASB (Financial Accounting Standard Board) has primary authority over setting accounting standards over private, not-for-profit colleges and universities.

(2)

Statement of Financial position, Statement of Activities and Statement of cash flows are the required financial statements.

(3)

The following Equity accounts are required:

Net Assets: Unrestricted, Restricted, and Permanently Restricted.

c.

(1)

FASB (Financial Accounting Standard Board) has the primary authority over setting of accounting standards over investor-owned schools.

(2)

Statement of Financial position (Balance sheet), Income Statement, Statement of Changes in Equity and Statement of Cash flows.

(3)

The following Equity accounts are required:

Owner's equity: Paid-in-capital and Retained earnings.

(1)

GSAB (Governmental Accounting Standard Board) has primary authority over setting accounting standards over government colleges and universities.

(2)

Statement of Net assets, Statement of Revenues, Expenses and Changes in Net Assets and Statement of Cash flows are the required Financial statements.

(3)

The following Equity accounts are required:

Net Assets (Position) showing Unrestricted, Restricted and Net investment in capital assets.

b.

(1)

FASB (Financial Accounting Standard Board) has primary authority over setting accounting standards over private, not-for-profit colleges and universities.

(2)

Statement of Financial position, Statement of Activities and Statement of cash flows are the required financial statements.

(3)

The following Equity accounts are required:

Net Assets: Unrestricted, Restricted, and Permanently Restricted.

c.

(1)

FASB (Financial Accounting Standard Board) has the primary authority over setting of accounting standards over investor-owned schools.

(2)

Statement of Financial position (Balance sheet), Income Statement, Statement of Changes in Equity and Statement of Cash flows.

(3)

The following Equity accounts are required:

Owner's equity: Paid-in-capital and Retained earnings.

3

With regard to private-sector colleges and universities:

a. List the three net asset classes required under FASB Statement 117.

b. List the financial reports required under FASB Statement 117.

c. Distinguish between an endowment, a term endowment, and a quasiendowment. Indicate the accounting required for each.

d. Outline the accounting required by the FASB for

(1) An endowment gift received in cash.

(2) A pledge received in 2014, unrestricted as to purpose but restricted for use in 2015.

(3) A pledge received in 2014, restricted as to purpose other than plant. The purpose was fulfilled in 2015.

a. List the three net asset classes required under FASB Statement 117.

b. List the financial reports required under FASB Statement 117.

c. Distinguish between an endowment, a term endowment, and a quasiendowment. Indicate the accounting required for each.

d. Outline the accounting required by the FASB for

(1) An endowment gift received in cash.

(2) A pledge received in 2014, unrestricted as to purpose but restricted for use in 2015.

(3) A pledge received in 2014, restricted as to purpose other than plant. The purpose was fulfilled in 2015.

Answer (a):

FASB guideline is applicable on non -profit colleges and universities. It is used for preparing financial statement of such institutes. Due to non-profit nature, excess of revenue over expenditure is not shown as profit or surplus. It is indicated as net asset.

Net asset can be of three types. They are -

1. Net assets - unrestricted

2. Net assets - temporarily restricted and

3. Net assets - permanently restricted

Net asset -permanently restricted:

Sometimes a person/institute donating money imposes restriction on use. The money is required to be invested on permanent basis. It is known as donation for endowment. It is classified as net asset permanently restricted.

Instead of investing money on permanent basis, it may be for a specific period. In that case it will not be considered as net asset permanently restricted. Further Institute may create endowment from fund of unrestricted in nature. It is known as quasi-endowment. It should not be considered as permanently restricted net asset. Here donor has not imposed restriction. It has been created by the institute itself.

Income from endowment is not permanently restricted. It will be considered in other two categories. It will either restrict by use or of unrestricted in nature.

Net asset- temporarily restricted:

Donor can also impose some conditions on the donated money. It can be of two types.

a. Use restriction - Donated amount here can be used only for a specified purpose. It may be restricted for use in research work or for purchase of assets.

b. Time restriction - Here donated amount is paid in future or can be used in future. If donation is payable in 206 or can be used only in 2016, then it is restricted by time. First one is pledge. Amount has been promised today but will be paid in 2016. As per FASB guidelines, such pledge amount is recorded in the book at present value in the year of pledge. Thus a pledge of 2014 is recorded in 2014 although amount is receivable in coming years. Further the value of pledge should be escalated on expiry of one year, since its present value will go up due to such passing of time.

Income from endowment is considered as temporarily restrictive in nature, when some use or time restriction has been imposed on them at the time of donation of endowment sum.

Net asset - unrestricted:

All donations not included in above two categories are included here. This fund is free for use. Receiver can use it in any manner. Quasi-endowment is included in net - asset unrestricted although amount has been fixed.

Net asset temporarily restricted is transferred to unrestricted category on fulfillment of time or use restriction.

Answer (b):

Financial reports required under FASB statement 117:

Four types of financial reports are required under FASB guidelines. They are -

1. Statement of unrestricted revenues, Expenses and other changes in unrestricted net asset: It indicates impact of current years transactions on the unrestricted net assets. Consider all -

a. Revenues of unrestricted nature,

b. Expenses and

c. Net assets reclassified to unrestricted class.

If total of (a) and (c) are greater than total of (b), then balance of unrestricted net asset in Balance sheet will go up. This changed amount and ending net asset figure is ascertained from this financial statement.

2. Statement of change in net assets: First statement is showing detailed composition of change in net asset unrestricted in nature. A summarized picture of the first statement is also included here. With this summarized figure detailed calculations of changes in other two categories of net assets are added.

First consider change in net asset- temporarily restrictive in nature. All revenues and expenses affecting this class of net asset are shown in detail. Details are as follows-

a. Consider all revenues increasing this class of net asset

b. Then deduct all expenses made from this class of net assets

c. Also deduct portion of net asset temporarily restrictive that are removed from this class and transferred to unrestricted class.

Finally consider all changes in the net asset -permanently restrictive in nature. Sum of the three classes will constitute total changes in the net assets. Opening net asset figure is added to get closing total net assets.

3. Statement of financial position: It is like balance sheet. It is a statement indicating assets, liabilities, and net assets.

Assets and liabilities are shown sequentially on the basis of liquidity. Most liquid asset is cash. Last item is land, building, plant etc.

Liabilities will also start with the most liquid one. Like accounts payables, it ends with long term loans.

After liabilities, net assets of different types are recorded. Then total of net asset is added with liabilities. This total should agree with the total of assets.

Statement of cash flows: It indicates the causes of change in cash in hand. There are different sources of cash inflows and outflows. They are divided into three groups:

a. Cash inflow from operating activities

b. Cash flow from investing activities and

c. Cash flow from financing activities

In first group cash are inflowing or out flowing from normal activities of institute. In second group money will be related with durable assets. When these assets are bought, cash will out flow. On the other hand cash will inflow from the sale of assets. Finally consider third group. It will include all cash received from issue of new debts. Cash will outflow when interest or loans are repaid.

Answer (c)

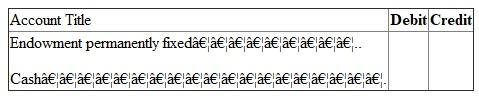

Difference between Endowment, term Endowment and Quasi-endowment:

1. Endowment will mean fixed deposit of permanent nature. In private sector college and Universities main sources of revenues are donations / contribution. Donor can donate the money specifying the purpose of its use. When amount is paid for permanent investment, it becomes Endowment.

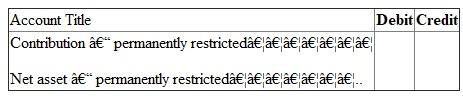

Accounting: since amount received for endowment is not usable in any other manner, the contribution is classified as contribution - permanently restricted. On its receipt accounting entry is -

2. At the time of depositing money as permanent investment, journal is as follows:

2. At the time of depositing money as permanent investment, journal is as follows:

3. At the end of the year, contribution - permanently restricted account is closed by transferring the amount to net asset-permanently restricted. Journal is as follows:

3. At the end of the year, contribution - permanently restricted account is closed by transferring the amount to net asset-permanently restricted. Journal is as follows:

Term Endowment: It is also fixed deposit. But the deposit is not permanent in nature. A person may contribute for 10 years endowment. This amount will remain as fixed deposit for 10 years. After 10 years the deposit can be encased. Money can be used for any other purposes.

Term Endowment: It is also fixed deposit. But the deposit is not permanent in nature. A person may contribute for 10 years endowment. This amount will remain as fixed deposit for 10 years. After 10 years the deposit can be encased. Money can be used for any other purposes.

Accounting: Entries on receipt of money and deposit of cash as term endowment are same as stated in (i) above. It will be debited in term endowment. Also contribution is considered as - temporarily restricted in nature. Thus at the end of the year, contribution received account is closed by transferring the amount to net asset- temporarily restricted by use account.

Like endowment income, the annual earnings (interest) from term endowment is usually unrestricted in nature. The money earned can be used in any manner as desired by the college/ university. If donor has imposed condition specifying its usability, then it will be used only for that purpose.

Quasi-endowment: Sometimes Institute has decided to open endowment from donations of unrestricted nature. The donor has not imposed any endowment. It is known as quasi-endowment.

Accounting entry:

i. On receipt of donation -

ii. On opening of endowment-

ii. On opening of endowment-

iii. At the end of the year, contribution - unrestricted account is closed by transferring it to unrestricted net asset. So journal is as follows:

iii. At the end of the year, contribution - unrestricted account is closed by transferring it to unrestricted net asset. So journal is as follows:

Note that the amount has not been credited in net -asset permanently restrictive class. It is due to self imposed restriction by the concern.

Note that the amount has not been credited in net -asset permanently restrictive class. It is due to self imposed restriction by the concern.

Answer (d1):

Accounting required for endowment of gifts:

This amount of gift is meant for permanent investment. Accounting entries are -

1. On receipt of endowment gift-

2. On deposit of money for fixed endowment-

2. On deposit of money for fixed endowment-

3. At the end of the year-

3. At the end of the year-

Answer (d2): Pledge is a promise to pay some gift in future. It may be unrestricted in nature. Sometimes restriction is imposed on its use also. In this problem, a pledge has been received in the year 2014. It is unrestricted in its usability. But the amount will be used in 2015 although it has been received in 2014.

Answer (d2): Pledge is a promise to pay some gift in future. It may be unrestricted in nature. Sometimes restriction is imposed on its use also. In this problem, a pledge has been received in the year 2014. It is unrestricted in its usability. But the amount will be used in 2015 although it has been received in 2014.

(a) On receipt of money, it will be entered in the book as pledge received for temporarily restricted in nature restriction is on time of its use. Journal is-

(b) At the end of the year, pledge amount is transferred to net asset - temporarily restricted by time. Journal is -

(b) At the end of the year, pledge amount is transferred to net asset - temporarily restricted by time. Journal is -

Answer of (d3):

Answer of (d3):

Now pledge has been received in the year 2014. Purpose of its use is restricted. Journal entries are as follows-

(a) On its receipt in 2014:

(b) At the end of 2015, pledge amount is transferred to net - asset: temporarily restricted by use.

(b) At the end of 2015, pledge amount is transferred to net - asset: temporarily restricted by use.

(c) In the year 2015, on its use for specific purpose, Journal is -

(c) In the year 2015, on its use for specific purpose, Journal is -

(d) After its use, the restriction has been removed. So amount is now transferred from Net asset-temporarily restricted by use account to net asset - unrestricted. Journal is -

(d) After its use, the restriction has been removed. So amount is now transferred from Net asset-temporarily restricted by use account to net asset - unrestricted. Journal is -

FASB guideline is applicable on non -profit colleges and universities. It is used for preparing financial statement of such institutes. Due to non-profit nature, excess of revenue over expenditure is not shown as profit or surplus. It is indicated as net asset.

Net asset can be of three types. They are -

1. Net assets - unrestricted

2. Net assets - temporarily restricted and

3. Net assets - permanently restricted

Net asset -permanently restricted:

Sometimes a person/institute donating money imposes restriction on use. The money is required to be invested on permanent basis. It is known as donation for endowment. It is classified as net asset permanently restricted.

Instead of investing money on permanent basis, it may be for a specific period. In that case it will not be considered as net asset permanently restricted. Further Institute may create endowment from fund of unrestricted in nature. It is known as quasi-endowment. It should not be considered as permanently restricted net asset. Here donor has not imposed restriction. It has been created by the institute itself.

Income from endowment is not permanently restricted. It will be considered in other two categories. It will either restrict by use or of unrestricted in nature.

Net asset- temporarily restricted:

Donor can also impose some conditions on the donated money. It can be of two types.

a. Use restriction - Donated amount here can be used only for a specified purpose. It may be restricted for use in research work or for purchase of assets.

b. Time restriction - Here donated amount is paid in future or can be used in future. If donation is payable in 206 or can be used only in 2016, then it is restricted by time. First one is pledge. Amount has been promised today but will be paid in 2016. As per FASB guidelines, such pledge amount is recorded in the book at present value in the year of pledge. Thus a pledge of 2014 is recorded in 2014 although amount is receivable in coming years. Further the value of pledge should be escalated on expiry of one year, since its present value will go up due to such passing of time.

Income from endowment is considered as temporarily restrictive in nature, when some use or time restriction has been imposed on them at the time of donation of endowment sum.

Net asset - unrestricted:

All donations not included in above two categories are included here. This fund is free for use. Receiver can use it in any manner. Quasi-endowment is included in net - asset unrestricted although amount has been fixed.

Net asset temporarily restricted is transferred to unrestricted category on fulfillment of time or use restriction.

Answer (b):

Financial reports required under FASB statement 117:

Four types of financial reports are required under FASB guidelines. They are -

1. Statement of unrestricted revenues, Expenses and other changes in unrestricted net asset: It indicates impact of current years transactions on the unrestricted net assets. Consider all -

a. Revenues of unrestricted nature,

b. Expenses and

c. Net assets reclassified to unrestricted class.

If total of (a) and (c) are greater than total of (b), then balance of unrestricted net asset in Balance sheet will go up. This changed amount and ending net asset figure is ascertained from this financial statement.

2. Statement of change in net assets: First statement is showing detailed composition of change in net asset unrestricted in nature. A summarized picture of the first statement is also included here. With this summarized figure detailed calculations of changes in other two categories of net assets are added.

First consider change in net asset- temporarily restrictive in nature. All revenues and expenses affecting this class of net asset are shown in detail. Details are as follows-

a. Consider all revenues increasing this class of net asset

b. Then deduct all expenses made from this class of net assets

c. Also deduct portion of net asset temporarily restrictive that are removed from this class and transferred to unrestricted class.

Finally consider all changes in the net asset -permanently restrictive in nature. Sum of the three classes will constitute total changes in the net assets. Opening net asset figure is added to get closing total net assets.

3. Statement of financial position: It is like balance sheet. It is a statement indicating assets, liabilities, and net assets.

Assets and liabilities are shown sequentially on the basis of liquidity. Most liquid asset is cash. Last item is land, building, plant etc.

Liabilities will also start with the most liquid one. Like accounts payables, it ends with long term loans.

After liabilities, net assets of different types are recorded. Then total of net asset is added with liabilities. This total should agree with the total of assets.

Statement of cash flows: It indicates the causes of change in cash in hand. There are different sources of cash inflows and outflows. They are divided into three groups:

a. Cash inflow from operating activities

b. Cash flow from investing activities and

c. Cash flow from financing activities

In first group cash are inflowing or out flowing from normal activities of institute. In second group money will be related with durable assets. When these assets are bought, cash will out flow. On the other hand cash will inflow from the sale of assets. Finally consider third group. It will include all cash received from issue of new debts. Cash will outflow when interest or loans are repaid.

Answer (c)

Difference between Endowment, term Endowment and Quasi-endowment:

1. Endowment will mean fixed deposit of permanent nature. In private sector college and Universities main sources of revenues are donations / contribution. Donor can donate the money specifying the purpose of its use. When amount is paid for permanent investment, it becomes Endowment.

Accounting: since amount received for endowment is not usable in any other manner, the contribution is classified as contribution - permanently restricted. On its receipt accounting entry is -

2. At the time of depositing money as permanent investment, journal is as follows: 3. At the end of the year, contribution - permanently restricted account is closed by transferring the amount to net asset-permanently restricted. Journal is as follows: Term Endowment: It is also fixed deposit. But the deposit is not permanent in nature. A person may contribute for 10 years endowment. This amount will remain as fixed deposit for 10 years. After 10 years the deposit can be encased. Money can be used for any other purposes.Accounting: Entries on receipt of money and deposit of cash as term endowment are same as stated in (i) above. It will be debited in term endowment. Also contribution is considered as - temporarily restricted in nature. Thus at the end of the year, contribution received account is closed by transferring the amount to net asset- temporarily restricted by use account.

Like endowment income, the annual earnings (interest) from term endowment is usually unrestricted in nature. The money earned can be used in any manner as desired by the college/ university. If donor has imposed condition specifying its usability, then it will be used only for that purpose.

Quasi-endowment: Sometimes Institute has decided to open endowment from donations of unrestricted nature. The donor has not imposed any endowment. It is known as quasi-endowment.

Accounting entry:

i. On receipt of donation -

ii. On opening of endowment- iii. At the end of the year, contribution - unrestricted account is closed by transferring it to unrestricted net asset. So journal is as follows: Note that the amount has not been credited in net -asset permanently restrictive class. It is due to self imposed restriction by the concern.Answer (d1):

Accounting required for endowment of gifts:

This amount of gift is meant for permanent investment. Accounting entries are -

1. On receipt of endowment gift-

2. On deposit of money for fixed endowment- 3. At the end of the year- Answer (d2): Pledge is a promise to pay some gift in future. It may be unrestricted in nature. Sometimes restriction is imposed on its use also. In this problem, a pledge has been received in the year 2014. It is unrestricted in its usability. But the amount will be used in 2015 although it has been received in 2014.(a) On receipt of money, it will be entered in the book as pledge received for temporarily restricted in nature restriction is on time of its use. Journal is-

(b) At the end of the year, pledge amount is transferred to net asset - temporarily restricted by time. Journal is - Answer of (d3):Now pledge has been received in the year 2014. Purpose of its use is restricted. Journal entries are as follows-

(a) On its receipt in 2014:

(b) At the end of 2015, pledge amount is transferred to net - asset: temporarily restricted by use. (c) In the year 2015, on its use for specific purpose, Journal is - (d) After its use, the restriction has been removed. So amount is now transferred from Net asset-temporarily restricted by use account to net asset - unrestricted. Journal is - 4

Define and outline the accounting required for each of the following types of agreements:

a. Charitable lead trusts.

b. Charitable remainder trusts.

c. Perpetual trust held by a third party.

a. Charitable lead trusts.

b. Charitable remainder trusts.

c. Perpetual trust held by a third party.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

5

During the year ended June 30, 2015, the following transactions were recorded by St. Ann's College, a private institution:

1. Tuition and fees amounted to $6,800,000, of which $4,450,000 was received in cash. A state appropriation was received in cash in the amount of $550,000. Sales and services of auxiliary enterprises amounted to $3,500,000, all of which was received in cash.

2. Student scholarships were awarded in the amount of $950,000. Recipient students were not required to provide services for this financial aid.

3. The provision for doubtful accounts for the year ended June 30, 2015, amounted to $25,000. During the year, doubtful accounts related to student fees were written off in the amount of $20,000.

4. During the year, contributions received, all in cash, amounted to: unrestricted, $600,000; temporarily restricted for use in the year ended June 30, 2016, $1,100,000 (unrestricted as to purpose); temporarily restricted for certain purposes, $900,000; and restricted for endowments, $1,300,000.

5. During the year, $530,000 was released from restrictions based on time, and $700,000 was released from restrictions for program purposes (research). The applicable research expense of $700,000 was paid in cash.

6. Investment income amounted to: unrestricted income from endowments, $150,000; income from endowments for purposes restricted by program, $200,000; and income from endowments required to be added to the endowment, $15,000.

7. During the year, St. Ann's received a gift of $2,000,000, which was to be used for the future construction of an addition to the library.

8. During the year, $1,300,000 was expended for the construction of a new wing to the student services building. The building was constructed using cash provided by a donor in a previous year for that purpose. St. Ann's records all fixed assets in the unrestricted net asset class.

9. Endowment long-term investments, carried at a basis of $2,000,000, were sold for $2,150,000. The total proceeds were reinvested. Income is to remain as permanently restricted.

10. Expenses for the year (in addition to expenses provided for in other parts of the problem) were instruction, $5,000,000; research, $1,200,000; public service, $300,000; academic support, $200,000; student services, $600,000; institutional support, $700,000; and auxiliary enterprises, $3,400,000. Of this, $10,900,000 was paid in cash and $500,000 was credited to Accounts Payable.

11. Depreciation recorded for the year amounted to $600,000. One-third of that amount was charged to instruction, one-third to institutional support, and one-third to auxiliary enterprises.

12. The institution sustained an uninsured fire loss of $230,000. Repairs were paid in cash and charged to the fire loss account.

13. Closing entries were prepared.

a. Record the transactions on the books of St. Ann's College. Indicate the net asset class for revenues and reclassifications.

b. Prepare, in good form, a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets for St. Ann's College for the year ended June 30, 2015.

c. Prepare, in good form, a Statement of Changes in Net Assets for St. Ann's College for the year ended June 30, 2015. The net assets at the beginning of the year amounted to $2,080,000.

1. Tuition and fees amounted to $6,800,000, of which $4,450,000 was received in cash. A state appropriation was received in cash in the amount of $550,000. Sales and services of auxiliary enterprises amounted to $3,500,000, all of which was received in cash.

2. Student scholarships were awarded in the amount of $950,000. Recipient students were not required to provide services for this financial aid.

3. The provision for doubtful accounts for the year ended June 30, 2015, amounted to $25,000. During the year, doubtful accounts related to student fees were written off in the amount of $20,000.

4. During the year, contributions received, all in cash, amounted to: unrestricted, $600,000; temporarily restricted for use in the year ended June 30, 2016, $1,100,000 (unrestricted as to purpose); temporarily restricted for certain purposes, $900,000; and restricted for endowments, $1,300,000.

5. During the year, $530,000 was released from restrictions based on time, and $700,000 was released from restrictions for program purposes (research). The applicable research expense of $700,000 was paid in cash.

6. Investment income amounted to: unrestricted income from endowments, $150,000; income from endowments for purposes restricted by program, $200,000; and income from endowments required to be added to the endowment, $15,000.

7. During the year, St. Ann's received a gift of $2,000,000, which was to be used for the future construction of an addition to the library.

8. During the year, $1,300,000 was expended for the construction of a new wing to the student services building. The building was constructed using cash provided by a donor in a previous year for that purpose. St. Ann's records all fixed assets in the unrestricted net asset class.

9. Endowment long-term investments, carried at a basis of $2,000,000, were sold for $2,150,000. The total proceeds were reinvested. Income is to remain as permanently restricted.

10. Expenses for the year (in addition to expenses provided for in other parts of the problem) were instruction, $5,000,000; research, $1,200,000; public service, $300,000; academic support, $200,000; student services, $600,000; institutional support, $700,000; and auxiliary enterprises, $3,400,000. Of this, $10,900,000 was paid in cash and $500,000 was credited to Accounts Payable.

11. Depreciation recorded for the year amounted to $600,000. One-third of that amount was charged to instruction, one-third to institutional support, and one-third to auxiliary enterprises.

12. The institution sustained an uninsured fire loss of $230,000. Repairs were paid in cash and charged to the fire loss account.

13. Closing entries were prepared.

a. Record the transactions on the books of St. Ann's College. Indicate the net asset class for revenues and reclassifications.

b. Prepare, in good form, a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets for St. Ann's College for the year ended June 30, 2015.

c. Prepare, in good form, a Statement of Changes in Net Assets for St. Ann's College for the year ended June 30, 2015. The net assets at the beginning of the year amounted to $2,080,000.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

6

Record the following transactions on the books of Calvin College, which follows FASB standards, for Calvin's fiscal year, which ends on June 30, 2015. 2015:

1. During the year, a donor made a cash contribution in the amount of $800,000 with the stipulation that the principal be invested permanently and that the income be used for research in biology. The cash was invested.

2. Also during the year, a donor made an unrestricted cash contribution of $400,000. Calvin's governing board decided to establish this gift as a permanent investment and invested the funds.

3. By the end of the year, the investments mentioned in transaction 1 earned $36,000 and the investments mentioned in transaction 2 earned $18,000; both amounts were received in cash.

4. The fair value of investments in transaction 1 increased by $12,000 at year-end. 2016:

5. During the year ended June 30, 2016, the biology research was completed, using the income mentioned in transaction 3.

1. During the year, a donor made a cash contribution in the amount of $800,000 with the stipulation that the principal be invested permanently and that the income be used for research in biology. The cash was invested.

2. Also during the year, a donor made an unrestricted cash contribution of $400,000. Calvin's governing board decided to establish this gift as a permanent investment and invested the funds.

3. By the end of the year, the investments mentioned in transaction 1 earned $36,000 and the investments mentioned in transaction 2 earned $18,000; both amounts were received in cash.

4. The fair value of investments in transaction 1 increased by $12,000 at year-end. 2016:

5. During the year ended June 30, 2016, the biology research was completed, using the income mentioned in transaction 3.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

7

Record the following transactions on the books of Carnegie College, a private institution that follows FASB standards. The year is 2015.

1. Carnegie received a pledge in the amount of $20,000, unrestricted as to purpose, indicating that the amount was to be paid to and used by the college in 2016.

2. Carnegie received $8,000 in cash from a donor who specified that the funds were to be used for research in voting behavior. The university did not conduct the research in 2015.

3. Carnegie conducted certain research on electrical conductivity during 2015, costing $50,000. A grant had been given in 2014 for just that purpose, but Carnegie hoped to use $30,000 of unrestricted resources for research and keep $30,000 of the original grant for future use in research. ( Hint: Follow the required procedure in this case.)

4. Carnegie reclassified $65,000 of funds that had been given in the previous year to support unspecified activities in 2015.

5. In a previous year, Carnegie received $500,000 to renovate a dormitory. During 2015, $620,000 of the funds were spent. Carnegie records all plant in the unrestricted net asset class.

1. Carnegie received a pledge in the amount of $20,000, unrestricted as to purpose, indicating that the amount was to be paid to and used by the college in 2016.

2. Carnegie received $8,000 in cash from a donor who specified that the funds were to be used for research in voting behavior. The university did not conduct the research in 2015.

3. Carnegie conducted certain research on electrical conductivity during 2015, costing $50,000. A grant had been given in 2014 for just that purpose, but Carnegie hoped to use $30,000 of unrestricted resources for research and keep $30,000 of the original grant for future use in research. ( Hint: Follow the required procedure in this case.)

4. Carnegie reclassified $65,000 of funds that had been given in the previous year to support unspecified activities in 2015.

5. In a previous year, Carnegie received $500,000 to renovate a dormitory. During 2015, $620,000 of the funds were spent. Carnegie records all plant in the unrestricted net asset class.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

8

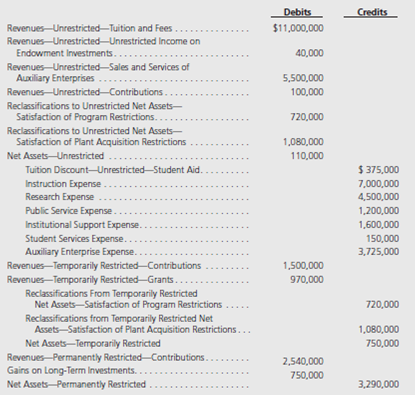

Presented below are the closing entries for Lee College, a private not-forprofit, for the year ended December 31, 2014.

Assume the January 1, 2015, net asset balances are as follows: $1,000,000 unrestricted net assets; $300,000 temporarily restricted net assets; and $1,760,000 permanently restricted net assets.

a. Prepare a Statement of Activities using the format presented in Illustration 10-2.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets.

Assume the January 1, 2015, net asset balances are as follows: $1,000,000 unrestricted net assets; $300,000 temporarily restricted net assets; and $1,760,000 permanently restricted net assets.

a. Prepare a Statement of Activities using the format presented in Illustration 10-2.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets together with a Statement of Changes in Net Assets.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

9

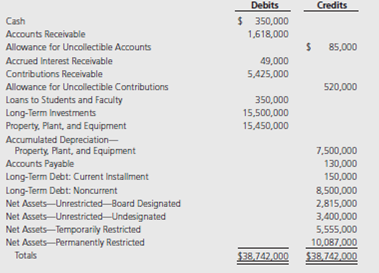

Korner College began the year with the following account balances:

During the year ended June 30, 2015, the following transactions occurred:

1. Cash collections included: accounts receivable, $1,227,000; accrued interest receivable, $49,000; contributions receivable, $4,985,000; and for loans to students and faculty, $155,000. Of the contributions, $1,900,000 was for plant acquisition (use for cash flow statement).

2. Cash payments included accounts payable, $130,000; and the current portion of long-term debt, $150,000.

3. Unrestricted revenues included tuition and fees, $21,740,000; unrestricted income on endowment investments, $400,000; other investment income, $300,000; and sales and services of auxiliary enterprises, $14,800,000. A total of $33,690,000 in cash was received, and the following receivables were increased: accounts receivable, $3,500,000; accrued interest receivable, $50,000.

4. Scholarships, for which no services were required, were applied to student accounts in the amount of $2,700,000.

5. Contributions were received in the following amounts: unrestricted, $4,900,000; temporarily restricted, $5,400,000; permanently restricted, $2,000,000. Of that amount, $7,020,000 was received in cash; contributions receivable increased $5,280,000. None of these contributions were restricted to plant acquisition.

6. Accounts receivable were written off in the amount of $50,000, and contributions receivable were written off in the amount of $20,000. Provisions for bad debts were increased by $175,000 for accounts receivable (tuition and fees) and by $30,000 for unrestricted contributions receivable.

7. Expenses, exclusive of depreciation, were as follows: instruction, $18,460,000; research, $1,980,000; public service, $1,910,000; academic support, $990,000; student services, $1,310,000; institutional support, $1,050,000; and auxiliary enterprises, $13,500,000. The college had an uninsured flood loss in the amount of $600,000. Cash was paid in the amount of $39,200,000, and accounts payable increased by $600,000.

8. Depreciation was charged in the amount of $2,100,000. One-third of that amount was charged each to instruction, institutional support, and auxiliary enterprises.

9. Interest income was earned as follows: addition to temporarily restricted net assets, $30,000; addition to permanently restricted net assets, $35,000. Of those amounts, $55,000 was received in cash and $10,000 was accrued at year-end.

10. Research expense was incurred in the amount of $1,700,000; and property, plant, and equipment were acquired in the amount of $1,400,000. Both were paid in cash.

11. Reclassifications were made from temporarily restricted to unrestricted net assets as follows: on the basis of time restrictions, $1,600,000; for program restrictions (research), $1,700,000; and for fixed asset acquisition restrictions, $1,400,000. Korner records fixed assets as increases in unrestricted net assets.

12. Long-term investments, with a carrying value of $1,700,000, were sold for $1,770,000. Of the $70,000 gain, $40,000 was temporarily restricted by donor agreement and $30,000 is required to be added to permanently restricted net assets.

13. Additional investments were purchased in the amount of $3,970,000. Loans were made to students and faculty in the amount of $200,000.

14. In addition to 13 above, the board of trustees decided to purchase $2,000,000 in long-term investments, from unrestricted net assets, to create a quasi-endowment.

15. At year-end, the fair value of investments increased by $530,000. Of that amount, $300,000 increased unrestricted net assets, $30,000 increased temporarily restricted net assets, and $200,000 increased permanently restricted net assets.

16. $150,000 of the long-term debt was reclassified as a current liability.

17. Closing entries were prepared for ( a ) unrestricted net assets, ( b ) temporarily restricted net assets, and ( c ) permanently restricted net assets.

Required:

a. Prepare journal entries for each of the above transactions.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets for Korner College for the fiscal year ended June 30, 2015.

c. Prepare a Statement of Changes in Net Assets for Korner College for the fiscal year ended June 30, 2015.

d. Prepare a Statement of Financial Position for Korner College as of June 30, 2015.

e. Prepare a Statement of Cash Flows for Korner College for the year ended June 30, 2015. Use the indirect method.

During the year ended June 30, 2015, the following transactions occurred:

1. Cash collections included: accounts receivable, $1,227,000; accrued interest receivable, $49,000; contributions receivable, $4,985,000; and for loans to students and faculty, $155,000. Of the contributions, $1,900,000 was for plant acquisition (use for cash flow statement).

2. Cash payments included accounts payable, $130,000; and the current portion of long-term debt, $150,000.

3. Unrestricted revenues included tuition and fees, $21,740,000; unrestricted income on endowment investments, $400,000; other investment income, $300,000; and sales and services of auxiliary enterprises, $14,800,000. A total of $33,690,000 in cash was received, and the following receivables were increased: accounts receivable, $3,500,000; accrued interest receivable, $50,000.

4. Scholarships, for which no services were required, were applied to student accounts in the amount of $2,700,000.

5. Contributions were received in the following amounts: unrestricted, $4,900,000; temporarily restricted, $5,400,000; permanently restricted, $2,000,000. Of that amount, $7,020,000 was received in cash; contributions receivable increased $5,280,000. None of these contributions were restricted to plant acquisition.

6. Accounts receivable were written off in the amount of $50,000, and contributions receivable were written off in the amount of $20,000. Provisions for bad debts were increased by $175,000 for accounts receivable (tuition and fees) and by $30,000 for unrestricted contributions receivable.

7. Expenses, exclusive of depreciation, were as follows: instruction, $18,460,000; research, $1,980,000; public service, $1,910,000; academic support, $990,000; student services, $1,310,000; institutional support, $1,050,000; and auxiliary enterprises, $13,500,000. The college had an uninsured flood loss in the amount of $600,000. Cash was paid in the amount of $39,200,000, and accounts payable increased by $600,000.

8. Depreciation was charged in the amount of $2,100,000. One-third of that amount was charged each to instruction, institutional support, and auxiliary enterprises.

9. Interest income was earned as follows: addition to temporarily restricted net assets, $30,000; addition to permanently restricted net assets, $35,000. Of those amounts, $55,000 was received in cash and $10,000 was accrued at year-end.

10. Research expense was incurred in the amount of $1,700,000; and property, plant, and equipment were acquired in the amount of $1,400,000. Both were paid in cash.

11. Reclassifications were made from temporarily restricted to unrestricted net assets as follows: on the basis of time restrictions, $1,600,000; for program restrictions (research), $1,700,000; and for fixed asset acquisition restrictions, $1,400,000. Korner records fixed assets as increases in unrestricted net assets.

12. Long-term investments, with a carrying value of $1,700,000, were sold for $1,770,000. Of the $70,000 gain, $40,000 was temporarily restricted by donor agreement and $30,000 is required to be added to permanently restricted net assets.

13. Additional investments were purchased in the amount of $3,970,000. Loans were made to students and faculty in the amount of $200,000.

14. In addition to 13 above, the board of trustees decided to purchase $2,000,000 in long-term investments, from unrestricted net assets, to create a quasi-endowment.

15. At year-end, the fair value of investments increased by $530,000. Of that amount, $300,000 increased unrestricted net assets, $30,000 increased temporarily restricted net assets, and $200,000 increased permanently restricted net assets.

16. $150,000 of the long-term debt was reclassified as a current liability.

17. Closing entries were prepared for ( a ) unrestricted net assets, ( b ) temporarily restricted net assets, and ( c ) permanently restricted net assets.

Required:

a. Prepare journal entries for each of the above transactions.

b. Prepare a Statement of Unrestricted Revenues, Expenses, and Other Changes in Unrestricted Net Assets for Korner College for the fiscal year ended June 30, 2015.

c. Prepare a Statement of Changes in Net Assets for Korner College for the fiscal year ended June 30, 2015.

d. Prepare a Statement of Financial Position for Korner College as of June 30, 2015.

e. Prepare a Statement of Cash Flows for Korner College for the year ended June 30, 2015. Use the indirect method.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

10

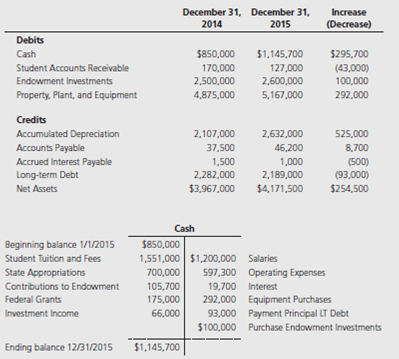

Presented below are comparative post closing trial balances for a college. In addition, cash transactions for the year ended December 31, 2015, are summarized in the T-account.

Comparative activity statements have been prepared for the year ended December 31, 2015, assuming the college is: ( a ) a private not-for-profit (Statement of Activities) and ( b ) a public college (Statement of Revenues, Expenses, and Changes in Fund Net Assets). These are provided in the first tab of the Excel file template.

Using the information above and the Excel template provided, prepare statements of cash flow assuming the college is: ( a ) a private not-for-profit and ( b ) a public college. Assume that all long-term debt is associated with the purchase of property, plant, and equipment.

Comparative activity statements have been prepared for the year ended December 31, 2015, assuming the college is: ( a ) a private not-for-profit (Statement of Activities) and ( b ) a public college (Statement of Revenues, Expenses, and Changes in Fund Net Assets). These are provided in the first tab of the Excel file template.

Using the information above and the Excel template provided, prepare statements of cash flow assuming the college is: ( a ) a private not-for-profit and ( b ) a public college. Assume that all long-term debt is associated with the purchase of property, plant, and equipment.

Unlock Deck

Unlock for access to all 10 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 10 flashcards in this deck.