Deck 14: Business Unit Performance Measurement

Full screen (f)

Question

Question

Compute Divisional Income

Refer to Exercise 14-18. The results for year 2 have just been posted:

Required

Compute divisional operating income for the two divisions. How well have these divisions performed

Refer to Exercise 14-18. The results for year 2 have just been posted:

Required

Compute divisional operating income for the two divisions. How well have these divisions performed

Question

Question

Question

Question

Question

Question

Question

Question

Question

Compare Alternative Measures of Division Performance

The following data are available for two divisions of Solomons Company:

The cost of capital for the company is 15 percent. Ignore taxes.

Required

a. If Solomons measures performance using ROI, which division had the better performance

b. If Solomons measures performance using economic value added, which division had the better performance (The divisions have no current liabilities.)c. Would your evaluation change if the company's cost of capital were 30 percent

The following data are available for two divisions of Solomons Company:

The cost of capital for the company is 15 percent. Ignore taxes.

Required

a. If Solomons measures performance using ROI, which division had the better performance

b. If Solomons measures performance using economic value added, which division had the better performance (The divisions have no current liabilities.)c. Would your evaluation change if the company's cost of capital were 30 percent

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

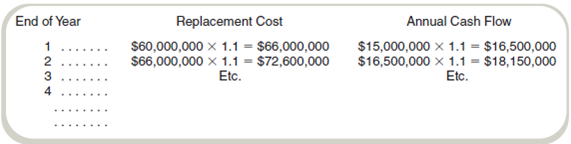

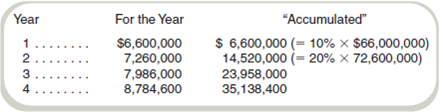

Compare Current Cost to Historical Cost

Refer to the information in Exercise 14-26. In computing ROI, this division uses end-of-year asset values. Assume that all cash flows increase 10 percent at the end of each year. This has the following effect on the assets' replacement cost and annual cash flows:

Depreciation is as follows:

Note that "accumulated" depreciation is 10 percent of the gross book value of depreciable assets after one year, 20 percent after two years, and so forth.

Required

a. Compute ROI using historical cost, net book value.

b. Compute ROI using historical cost, gross book value.

c. Compute ROI using current cost, net book value.

d. Compute ROI using current cost, gross book value.

Refer to the information in Exercise 14-26. In computing ROI, this division uses end-of-year asset values. Assume that all cash flows increase 10 percent at the end of each year. This has the following effect on the assets' replacement cost and annual cash flows:

Depreciation is as follows:

Note that "accumulated" depreciation is 10 percent of the gross book value of depreciable assets after one year, 20 percent after two years, and so forth.

Required

a. Compute ROI using historical cost, net book value.

b. Compute ROI using historical cost, gross book value.

c. Compute ROI using current cost, net book value.

d. Compute ROI using current cost, gross book value.

Question

Question

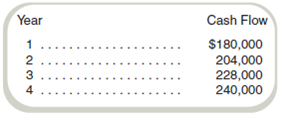

Effects of Current Cost on Performance Measurements

Upper Division of Lower Company acquired an asset with a cost of $600,000 and a four-year life. The cash flows from the asset, considering the effects of inflation, were scheduled as follows:

The cost of the asset is expected to increase at a rate of 10 percent per year, compounded each year. Performance measures are based on beginning-of-year gross book values for the investment base. Ignore taxes.

Required

a. What is the ROI for each year of the asset's life, using a historical cost approach

b. What is the ROI for each year of the asset's life if both the investment base and depreciation are determined by the current cost of the asset at the start of each year

Upper Division of Lower Company acquired an asset with a cost of $600,000 and a four-year life. The cash flows from the asset, considering the effects of inflation, were scheduled as follows:

The cost of the asset is expected to increase at a rate of 10 percent per year, compounded each year. Performance measures are based on beginning-of-year gross book values for the investment base. Ignore taxes.

Required

a. What is the ROI for each year of the asset's life, using a historical cost approach

b. What is the ROI for each year of the asset's life if both the investment base and depreciation are determined by the current cost of the asset at the start of each year

Question

Question

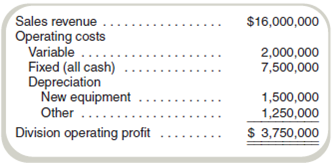

Equipment Replacement and Performance Measures

Oscar Clemente is the manager of Forbes Division of Pitt, Inc., a manufacturer of biotech products. Forbes Division, which has $4 million in assets, manufactures a special testing device. At the beginning of the current year, Forbes invested $5 million in automated equipment for test machine assembly. The division's expected income statement at the beginning of the year was as follows:

A sales representative from LSI Machine Company approached Oscar in October. LSI has for $6.5 million a new assembly machine that offers significant improvements over the equipment Oscar bought at the beginning of the year. The new equipment would expand division output by 10 percent while reducing cash fixed costs by 5 percent. It would be depreciated for accounting purposes over a three-year life. Depreciation would be net of the $500,000 salvage value of the new machine. The new equipment meets Pitt's 20 percent cost of capital criterion. If Oscar purchases the new machine, it must be installed prior to the end of the year. For practical purposes, though, Oscar can ignore depreciation on the new machine because it will not go into operation until the start of the next year.

The old machine, which has no salvage value, must be disposed of to make room for the new machine.

Pitt has a performance evaluation and bonus plan based on ROI. The return includes any losses on disposal of equipment. Investment is computed based on the end-of-year balance of assets, net book value. Ignore taxes.

Required

a. What is Forbes Division's ROI if Oscar does not acquire the new machine

b. What is Forbes Division's ROI this year if Oscar acquires the new machine

c. If Oscar acquires the new machine and it operates according to specifications, what ROI is expected for next year

Oscar Clemente is the manager of Forbes Division of Pitt, Inc., a manufacturer of biotech products. Forbes Division, which has $4 million in assets, manufactures a special testing device. At the beginning of the current year, Forbes invested $5 million in automated equipment for test machine assembly. The division's expected income statement at the beginning of the year was as follows:

A sales representative from LSI Machine Company approached Oscar in October. LSI has for $6.5 million a new assembly machine that offers significant improvements over the equipment Oscar bought at the beginning of the year. The new equipment would expand division output by 10 percent while reducing cash fixed costs by 5 percent. It would be depreciated for accounting purposes over a three-year life. Depreciation would be net of the $500,000 salvage value of the new machine. The new equipment meets Pitt's 20 percent cost of capital criterion. If Oscar purchases the new machine, it must be installed prior to the end of the year. For practical purposes, though, Oscar can ignore depreciation on the new machine because it will not go into operation until the start of the next year.

The old machine, which has no salvage value, must be disposed of to make room for the new machine.

Pitt has a performance evaluation and bonus plan based on ROI. The return includes any losses on disposal of equipment. Investment is computed based on the end-of-year balance of assets, net book value. Ignore taxes.

Required

a. What is Forbes Division's ROI if Oscar does not acquire the new machine

b. What is Forbes Division's ROI this year if Oscar acquires the new machine

c. If Oscar acquires the new machine and it operates according to specifications, what ROI is expected for next year

Question

Question

Question

Question

Question

Question

Question

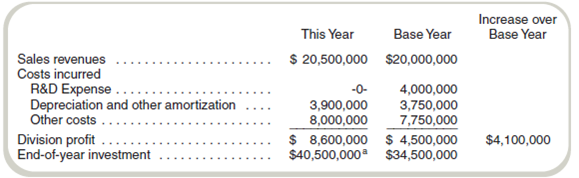

Impact of Decisions to Capitalize or Expense on Performance Measurement: Ethical Issues

Pharmaceutical firms, oil and gas companies, and other ventures inevitably incur costs on unsuccessful investments in new projects (e.g., new drugs or new wells). For oil and gas firms, a debate continues over whether those costs should be written off as period expense or capitalized as part of the full cost of finding profitable oil and gas ventures. For pharmaceutical firms, GAAP in the United States is clear that R D costs are to be expensed when incurred.

Pharm-It has been writing R D costs off to expense as incurred for both financial reporting and internal performance measurement. However, this year a new management team was hired to improve the profit of Pharm-It's Cardiology Division. The new management team was hired with the provision that it would receive a bonus equal to 10 percent of any profits in excess of base-year profits of the division. However, no bonus would be paid if profits were less than 20 percent of end-of-year investment. The following information was included in the performance report for the division:

a Includes other investments not at issue here.

During the year, the new team spent $5 million on R D activities, of which $4,500,000 was for unsuccessful ventures. The new management team has included the $4,500,000 in the current end-of-year investment base because "You can't invent successful drugs without missing on a few unsuccessful ones."

Required

a. What is the ROI for the base year and the current year Ignore taxes.

b. What is the amount of the bonus that the new management team is likely to claim Is this ethical

c. If you were on Pharm-It's board of directors, how would you respond to the new management's claim for the bonus

Pharmaceutical firms, oil and gas companies, and other ventures inevitably incur costs on unsuccessful investments in new projects (e.g., new drugs or new wells). For oil and gas firms, a debate continues over whether those costs should be written off as period expense or capitalized as part of the full cost of finding profitable oil and gas ventures. For pharmaceutical firms, GAAP in the United States is clear that R D costs are to be expensed when incurred.

Pharm-It has been writing R D costs off to expense as incurred for both financial reporting and internal performance measurement. However, this year a new management team was hired to improve the profit of Pharm-It's Cardiology Division. The new management team was hired with the provision that it would receive a bonus equal to 10 percent of any profits in excess of base-year profits of the division. However, no bonus would be paid if profits were less than 20 percent of end-of-year investment. The following information was included in the performance report for the division:

a Includes other investments not at issue here.

During the year, the new team spent $5 million on R D activities, of which $4,500,000 was for unsuccessful ventures. The new management team has included the $4,500,000 in the current end-of-year investment base because "You can't invent successful drugs without missing on a few unsuccessful ones."

Required

a. What is the ROI for the base year and the current year Ignore taxes.

b. What is the amount of the bonus that the new management team is likely to claim Is this ethical

c. If you were on Pharm-It's board of directors, how would you respond to the new management's claim for the bonus

Question

Question

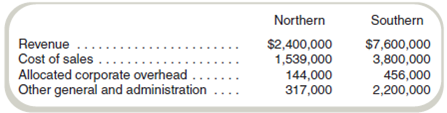

Compute Divisional Income

Eastern Merchants shows the following information for its two divisions for year 1:

Required

Compute divisional operating income for the two divisions. Ignore taxes. How well have these divisions performed

Eastern Merchants shows the following information for its two divisions for year 1:

Required

Compute divisional operating income for the two divisions. Ignore taxes. How well have these divisions performed

Question

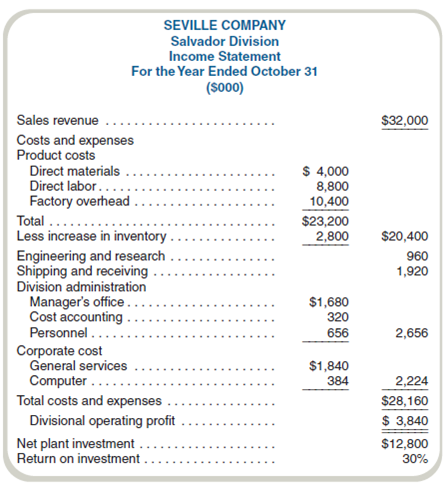

Evaluate Performance Evaluation System: Behavioral Issues

Several years ago, Seville Company acquired Salvador Components. Prior to the acquisition, Salvador manufactured and sold automotive components products to third-party customers. Since becoming a division of Seville, Salvador has manufactured components only for products made by Seville's Luxo Division.

Seville's corporate management gives the Salvador Division management considerable latitude in running the division's operations. However, corporate management retains authority for decisions regarding capital investments, product pricing, and production quantities.

Seville has a formal performance evaluation program for all division managements. The evaluation program relies substantially on each division's ROI. Salvador Division's income statement provides the basis for the evaluation of Salvador's management. (See the following income statement.)The corporate accounting staff prepares the divisional financial statements. Corporate general services costs are allocated on the basis of sales dollars, and the computer department's actual costs are apportioned among the divisions on the basis of use. The net divisional investment includes divisional fixed assets at net book value (cost less depreciation), divisional inventory, and corporate working capital apportioned to the divisions on the basis of sales dollars.

Required

a. Discuss Seville Company's financial reporting and performance evaluation program as it relates to the responsibilities of Salvador Division.

b. Based on your response to requirement ( a ), recommend appropriate revisions of the financial information and reports used to evaluate the performance of Salvador's divisional management. If revisions are not necessary, explain why.

(CMA adapted)

Several years ago, Seville Company acquired Salvador Components. Prior to the acquisition, Salvador manufactured and sold automotive components products to third-party customers. Since becoming a division of Seville, Salvador has manufactured components only for products made by Seville's Luxo Division.

Seville's corporate management gives the Salvador Division management considerable latitude in running the division's operations. However, corporate management retains authority for decisions regarding capital investments, product pricing, and production quantities.

Seville has a formal performance evaluation program for all division managements. The evaluation program relies substantially on each division's ROI. Salvador Division's income statement provides the basis for the evaluation of Salvador's management. (See the following income statement.)The corporate accounting staff prepares the divisional financial statements. Corporate general services costs are allocated on the basis of sales dollars, and the computer department's actual costs are apportioned among the divisions on the basis of use. The net divisional investment includes divisional fixed assets at net book value (cost less depreciation), divisional inventory, and corporate working capital apportioned to the divisions on the basis of sales dollars.

Required

a. Discuss Seville Company's financial reporting and performance evaluation program as it relates to the responsibilities of Salvador Division.

b. Based on your response to requirement ( a ), recommend appropriate revisions of the financial information and reports used to evaluate the performance of Salvador's divisional management. If revisions are not necessary, explain why.

(CMA adapted)

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/38

Play

Full screen (f)

Deck 14: Business Unit Performance Measurement

1

What are the advantages of using an ROI-type measure rather than the absolute value of division profits as a performance evaluation technique for business units

Using absolute value of division profits as a performance evaluation technique for measuring business unit performance is simple and easy to compare. But, this performance measure suffers from two limitations/disadvantages that are the divisions should be same in size and its investment (assets) should be same.

If, the divisions are at different sizes and/or its investment (assets) are differ then using "absolute value of division profits" as performance measure is ineffective. To come out of the two limitations/disadvantages that the management should use return on investment (ROI) technique for measuring the business unit performance.

Therefore, the advantages of return on investment (ROI) technique are as follows:

i) Return on investment (ROI) adjusts divisional income for different size business units.

ii) Return on investment (ROI) takes assets acquisition, usage and disposal in to consideration while measuring the divisional performance.

If, the divisions are at different sizes and/or its investment (assets) are differ then using "absolute value of division profits" as performance measure is ineffective. To come out of the two limitations/disadvantages that the management should use return on investment (ROI) technique for measuring the business unit performance.

Therefore, the advantages of return on investment (ROI) technique are as follows:

i) Return on investment (ROI) adjusts divisional income for different size business units.

ii) Return on investment (ROI) takes assets acquisition, usage and disposal in to consideration while measuring the divisional performance.

2

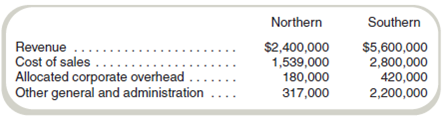

Compute Divisional Income

Refer to Exercise 14-18. The results for year 2 have just been posted:

Required

Compute divisional operating income for the two divisions. How well have these divisions performed

Refer to Exercise 14-18. The results for year 2 have just been posted:

Required

Compute divisional operating income for the two divisions. How well have these divisions performed

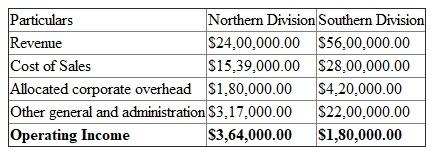

Divisional Income

The divisional income is internal performance measure. It is calculated by considering revenue and cost activities of the division in general accounting to assess the divisional performance.

Computation of divisional income

The divisional income is calculated by deducting cost of sales, other general and administration and allocated corporate overhead from revenues. The overhead of entire corporate is to be allocated to the divisions for computation of divisional income.

The divisional income for the two divisions is computed as follows:

The northern division is generating USD 3, 64,000.00 operating income and southern division is generating USD 1, 80,000.00. The northern division is leading showing success and ability of decision of the division. The reason behind the higher operating income may be the ability of divisional manager.

The northern division is generating USD 3, 64,000.00 operating income and southern division is generating USD 1, 80,000.00. The northern division is leading showing success and ability of decision of the division. The reason behind the higher operating income may be the ability of divisional manager.

The divisional income is internal performance measure. It is calculated by considering revenue and cost activities of the division in general accounting to assess the divisional performance.

Computation of divisional income

The divisional income is calculated by deducting cost of sales, other general and administration and allocated corporate overhead from revenues. The overhead of entire corporate is to be allocated to the divisions for computation of divisional income.

The divisional income for the two divisions is computed as follows:

The northern division is generating USD 3, 64,000.00 operating income and southern division is generating USD 1, 80,000.00. The northern division is leading showing success and ability of decision of the division. The reason behind the higher operating income may be the ability of divisional manager. 3

ROI, EVA, and Different Asset Bases

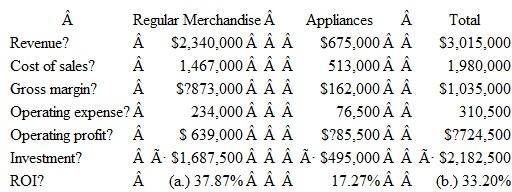

House Station, Inc., is a nationwide hardware and furnishings chain. The manager of the House Station Store in Portland is evaluated using ROI. House Station headquarters requires an ROI of 10 percent of assets. For the coming year, the manager estimates revenues will be $2,340,000, cost of goods will be $1,467,000, and operating expenses for this level of sales will be $234,000. Investment in the store assets throughout the year is $1,687,500 before considering the following proposal.

A representative of Sharp's Appliances approached the manager about carrying Sharp's line of appliances. This line is expected to generate $675,000 in sales in the coming year at the Portland House Station store with a merchandise cost of $513,000. Annual operating expenses for this additional merchandise line total $76,500. To carry the line of goods, an inventory investment of $495,000 throughout the year is required. Sharp's is willing to floor plan the merchandise so that the House Station store will not have to invest in any inventory. The cost of floor planning would be $60,750 per year. House Station's marginal cost of capital is 10 percent. Ignore taxes.

Required

a. What is the Portland House Station store's expected ROI for the coming year if it does not carry Sharp's appliances

b. What is the store's expected ROI if the manager invests in Sharp's inventory and carries the appliance line

c. What would the store's expected ROI be if the manager elected to take the floor plan option

d. Would the manager prefer ( a ), ( b ), or ( c ) Why

e. Would your answers to any of the above change if EVA was used to evaluate performance For purposes of this problem, assume no current liabilities.

House Station, Inc., is a nationwide hardware and furnishings chain. The manager of the House Station Store in Portland is evaluated using ROI. House Station headquarters requires an ROI of 10 percent of assets. For the coming year, the manager estimates revenues will be $2,340,000, cost of goods will be $1,467,000, and operating expenses for this level of sales will be $234,000. Investment in the store assets throughout the year is $1,687,500 before considering the following proposal.

A representative of Sharp's Appliances approached the manager about carrying Sharp's line of appliances. This line is expected to generate $675,000 in sales in the coming year at the Portland House Station store with a merchandise cost of $513,000. Annual operating expenses for this additional merchandise line total $76,500. To carry the line of goods, an inventory investment of $495,000 throughout the year is required. Sharp's is willing to floor plan the merchandise so that the House Station store will not have to invest in any inventory. The cost of floor planning would be $60,750 per year. House Station's marginal cost of capital is 10 percent. Ignore taxes.

Required

a. What is the Portland House Station store's expected ROI for the coming year if it does not carry Sharp's appliances

b. What is the store's expected ROI if the manager invests in Sharp's inventory and carries the appliance line

c. What would the store's expected ROI be if the manager elected to take the floor plan option

d. Would the manager prefer ( a ), ( b ), or ( c ) Why

e. Would your answers to any of the above change if EVA was used to evaluate performance For purposes of this problem, assume no current liabilities.

a. and b.

Income statements to summarize the alternatives are as follows:

Although the appliances provide a return greater than the cost of capital, it lowers the status quo ROI.

Although the appliances provide a return greater than the cost of capital, it lowers the status quo ROI.

c. If the floor plan is used, the investment base will be $1,687,500. Total operating profits will equal $724,500 minus the floor plan charge of $60,750 for a net profit of $663,750. The ROI will be 39.33% which is $663,750 ¸ $1,687,500.

d. The manager would prefer the floor plan because it would raise the store's ROI above the current ROI of 37.87%.

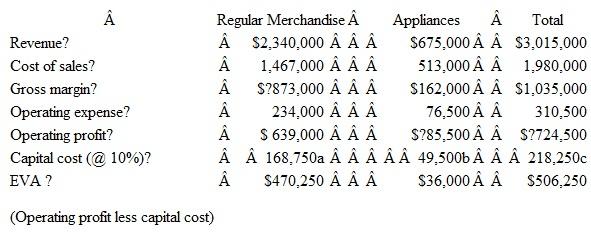

e.

Income statements to summarize the alternatives are as follows: ($ in thousands) a $168,750 = 10% × $1,687,500.

a $168,750 = 10% × $1,687,500.

b $49,500 = 10% × $495,000.

c $218,250 = 10% × $2,182,500.

Appliances provide a return greater than the cost of capital, so EVA is positive. It increases the status quo EVA.

If the floor plan is used, the investment base will be $1,687,500. Total operating profits will equal $724,500 minus the floor plan charge of $60,750 for a net profit of $663,750. The EVA will be $495,000 (= $663,750 - 10% × $1,687,500).

The manager would not prefer the floor plan because it would lower the store's EVA. The floor plan charge is $60,750. The cost of the investment in the appliances is $49,500 (= 10% × $495,000).

Income statements to summarize the alternatives are as follows:

Although the appliances provide a return greater than the cost of capital, it lowers the status quo ROI.c. If the floor plan is used, the investment base will be $1,687,500. Total operating profits will equal $724,500 minus the floor plan charge of $60,750 for a net profit of $663,750. The ROI will be 39.33% which is $663,750 ¸ $1,687,500.

d. The manager would prefer the floor plan because it would raise the store's ROI above the current ROI of 37.87%.

e.

Income statements to summarize the alternatives are as follows: ($ in thousands)

a $168,750 = 10% × $1,687,500.b $49,500 = 10% × $495,000.

c $218,250 = 10% × $2,182,500.

Appliances provide a return greater than the cost of capital, so EVA is positive. It increases the status quo EVA.

If the floor plan is used, the investment base will be $1,687,500. Total operating profits will equal $724,500 minus the floor plan charge of $60,750 for a net profit of $663,750. The EVA will be $495,000 (= $663,750 - 10% × $1,687,500).

The manager would not prefer the floor plan because it would lower the store's EVA. The floor plan charge is $60,750. The cost of the investment in the appliances is $49,500 (= 10% × $495,000).

4

Give an example in which the use of ROI measures might lead the manager to make a decision that is not in the firm's interests.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

5

Compute RI and ROI

Bonds Division of Giant Bank has assets of $3.6 billion. During the past year, the division had profits of $900 million. Giant Bank has a cost of capital of 12 percent. Ignore taxes.

Required

a. Compute the divisional ROI.

b. Compute the divisional RI.

Bonds Division of Giant Bank has assets of $3.6 billion. During the past year, the division had profits of $900 million. Giant Bank has a cost of capital of 12 percent. Ignore taxes.

Required

a. Compute the divisional ROI.

b. Compute the divisional RI.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

6

Economic Value Added

Biddle Company uses EVA to evaluate the performance of division managers. Wallace Division had the following results for Year 3. After-tax divisional income was $200,000.

The company adjusts the after-tax income for advertising expenses. First, it adds the annual advertising expenses back to after-tax divisional income. Second, the company managers believe that advertising has a three-year positive effect on the sale of the company's products, so it amortizes advertising over three years. Advertising expenses in Year 1 will be expensed 50 percent, 40 percent in Year 2, and 10 percent in Year 3. Advertising expenses in Year 2 will be expensed 50 percent, 40 percent in Year 3, and 10 percent in Year 4. Advertising expenses in Year 3 will be amortized 50 percent, 40 percent in Year 4, and 10 percent in Year 5. Third, unamortized advertising expenses become part of the divisional investment in the EVA calculations. Wallace Division had incurred advertising expenses of $50,000 in Year 1 and $100,000 in Year 2. It incurred $120,000 of advertising in Year 3.

Before considering the unamortized advertising, the Wallace Division had total assets of $2,100,000 and current liabilities of $300,000 at the beginning of Year 3. Biddle Company calculates EVA using the divisional investment at the beginning of the year. The company uses a 10 percent cost of capital to compute EVA.

Required

Compute the EVA for the Wallace Division for Year 3. Is the division adding value to shareholders

Biddle Company uses EVA to evaluate the performance of division managers. Wallace Division had the following results for Year 3. After-tax divisional income was $200,000.

The company adjusts the after-tax income for advertising expenses. First, it adds the annual advertising expenses back to after-tax divisional income. Second, the company managers believe that advertising has a three-year positive effect on the sale of the company's products, so it amortizes advertising over three years. Advertising expenses in Year 1 will be expensed 50 percent, 40 percent in Year 2, and 10 percent in Year 3. Advertising expenses in Year 2 will be expensed 50 percent, 40 percent in Year 3, and 10 percent in Year 4. Advertising expenses in Year 3 will be amortized 50 percent, 40 percent in Year 4, and 10 percent in Year 5. Third, unamortized advertising expenses become part of the divisional investment in the EVA calculations. Wallace Division had incurred advertising expenses of $50,000 in Year 1 and $100,000 in Year 2. It incurred $120,000 of advertising in Year 3.

Before considering the unamortized advertising, the Wallace Division had total assets of $2,100,000 and current liabilities of $300,000 at the beginning of Year 3. Biddle Company calculates EVA using the divisional investment at the beginning of the year. The company uses a 10 percent cost of capital to compute EVA.

Required

Compute the EVA for the Wallace Division for Year 3. Is the division adding value to shareholders

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

7

How does residual income differ from ROI

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

8

ROI versus RI

Adivision is considering the acquisition of a new asset that will cost $720,000 and have a cash flow of $280,000 per year for each of the five years of its life. Depreciation is computed on a straight-line basis with no salvage value. Ignore taxes.

Required

a. What is the ROI for each year of the asset's life if the division uses beginning-of-year asset balances and net book value for the computation

b. What is the residual income each year if the cost of capital is 25 percent

Adivision is considering the acquisition of a new asset that will cost $720,000 and have a cash flow of $280,000 per year for each of the five years of its life. Depreciation is computed on a straight-line basis with no salvage value. Ignore taxes.

Required

a. What is the ROI for each year of the asset's life if the division uses beginning-of-year asset balances and net book value for the computation

b. What is the residual income each year if the cost of capital is 25 percent

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

9

Barrows Consumer Products (A)I thought evaluating performance would be easier than this. I have three vice presidents, operating the same business in three different countries. I need to be able to compare them in order to prepare compensation recommendations to the board. The problem is that there are so many variables that each of the managers can make some claim to having the best performance. I hope our consultant can help me sort this out.

Alice Karlson, Executive Vice President

Southeast Asia Emerging Markets Sector

Barrows Consumer Products

Organization

Barrows Consumer Products is a large, multinational consumer products firm based in the United States. In the mid-1990s, Barrows made a strategic decision to enter the transitional and emerging markets. Each of the new markets was led by an executive vice president and organized along country lines. Barrows believed this form of organization made it easier to evaluate each country and also made it easier to exit from a country it identified as unprofitable.

One of the new markets developed by Barrows was Southeast Asia. Although there was significant competition in the region from other Asian and European competitors, the management of Barrows believed its advantage was in its portfolio of products with widely recognized brand names. Barrows chose three countries to enter initially: Indonesia, the Philippines, and Vietnam. At the time of the decision, all three appeared to represent significant growth opportunities.

Barrows's policy in these new markets was to install a Barrows manager originally from the country who was willing to return and manage the business. Barrows believed that this policy resulted in additional goodwill and also allowed the managers to use their knowledge of local business customs. (It also hoped to take advantage of any personal ties the managers might have in business and government, but this was not included in its policy statement.) A simplified organization chart for the Southeast Asia Emerging Markets Sector is provided in Exhibit 14.12.

Although all three countries could be classified as emerging or transitional economies, there are considerable differences among them. Indonesia has a very large population, while the Philippines and Vietnam are smaller. The Philippines, however, has a higher level of per capita income; Vietnam is the poorest of the three countries. Selected demographic data for the three countries are shown in Exhibit 14.13.

Performance Evaluation

Barrows has a well-developed set of performance measures that is used for managerial evaluation. The two primary measures that are used for groups in the United States, Canada, Western Europe, and Japan are division (or country) profit and return on investment (ROI). Return on investment is computed by dividing division (or country) operating income (essentially, income before taxes) by division (or country) total assets. While profit and ROI are commonly used in much of the company, the executive vice presidents in emerging market sectors are given considerable leeway in evaluating their individual country vice presidents. This performance evaluation is important to these managers. Compensation in the Southeast Asia Sector consists of salary and bonus.

The bonus pool for the three managers is dictated by corporate headquarters of Barrows in the United States. The bonus pool formula is not explicitly defined although there is a clear correlation between the size of the pool and the profitability of the sector, however measured.

The allocation of the pool to the individual country managers is at the discretion of Ms. Karlson, the sector executive vice president. In March of year 9, the financial results from the three countries for year 8 have been tabulated and she is now evaluating them. Because this is her first year in this position, she has not had to perform this task in the past. She has hired a local compensation consultant to advise her on the relative performance of the three managers.

The financial staff at sector headquarters receives the financial statements from the controller's staff in each of the three countries and ensures that the statements are consistently prepared in a common currency. The income statements for year 8 are shown in Exhibit 14.14. The balance sheets as of the beginning of year 8 are shown in Exhibit 14.15. Ms. Karlson discusses the source of her concern.

When I look at the financial statements, I can see immediately that Ade [Darmadi, V.P.-Indonesia] has outperformed Isadore [Real, V.P.-Philippines]. But Indonesia is a much larger market than the Philippines. So I calculate ROI to try and adjust for size and now Isadore is outperforming Ade. When I mention this to Ade, she counters that although Indonesia is larger, it is also poorer and geographically dispersed, leading to higher distribution costs. The only thing I can say for sure is that Binh has not developed much of a market.

I also wonder whether headquarters is looking at the right performance measure. I recently attended a seminar on new performance evaluation measures and the seminar speaker spent quite a bit of time on something called economic value added (EVA). The way I understand it, EVA adjusts profit and subtracts a capital charge from it. The capital charge is the cost of capital multiplied by the net assets (total assets less current liabilities) employed. I guess I would use the cost of capital of 20 percent after-tax that corporate policy requires I use for investment decisions. The problem I have is I am not sure how to adjust income, which is an accounting measure, into something more meaningful. We don't do any R D here, so the only item on the statements that was mentioned at the seminar is advertising. (Note: Advertising expenses for the previous three years are shown in Exhibit 14.16.) When I was working in the United States, I came across a study stating that advertising expenditures in our industry have an expected life of about three years. If that's true, then clearly the way we account for advertising is wrong and I should adjust these results accordingly.

There are other issues that I think are more ambiguous. For one thing, Binh developed a new approach for delivering products that cut distribution costs in Vietnam. At our annual retreat, he shared his ideas with Ade and Isadore about how they could adapt this to their markets. In addition, many customers want their stores in Vietnam and Indonesia to be entirely served from Indonesia, so Binh receives no credit for that business.

Required

a. What are some of the factors causing the problems in measuring performance in the Southeast Asia Sector

b. Rank the three countries using each of the following measures of performance:

1. Country profit.

2. Return on investment.

3. Economic value added (EVA).

c. Are there other performance measures you would suggest How would you measure these

d. Write a one-page memo to Ms. Karlson explaining which country performed best. Be sure to explain your reasoning.

Alice Karlson, Executive Vice President

Southeast Asia Emerging Markets Sector

Barrows Consumer Products

Organization

Barrows Consumer Products is a large, multinational consumer products firm based in the United States. In the mid-1990s, Barrows made a strategic decision to enter the transitional and emerging markets. Each of the new markets was led by an executive vice president and organized along country lines. Barrows believed this form of organization made it easier to evaluate each country and also made it easier to exit from a country it identified as unprofitable.

One of the new markets developed by Barrows was Southeast Asia. Although there was significant competition in the region from other Asian and European competitors, the management of Barrows believed its advantage was in its portfolio of products with widely recognized brand names. Barrows chose three countries to enter initially: Indonesia, the Philippines, and Vietnam. At the time of the decision, all three appeared to represent significant growth opportunities.

Barrows's policy in these new markets was to install a Barrows manager originally from the country who was willing to return and manage the business. Barrows believed that this policy resulted in additional goodwill and also allowed the managers to use their knowledge of local business customs. (It also hoped to take advantage of any personal ties the managers might have in business and government, but this was not included in its policy statement.) A simplified organization chart for the Southeast Asia Emerging Markets Sector is provided in Exhibit 14.12.

Although all three countries could be classified as emerging or transitional economies, there are considerable differences among them. Indonesia has a very large population, while the Philippines and Vietnam are smaller. The Philippines, however, has a higher level of per capita income; Vietnam is the poorest of the three countries. Selected demographic data for the three countries are shown in Exhibit 14.13.

Performance Evaluation

Barrows has a well-developed set of performance measures that is used for managerial evaluation. The two primary measures that are used for groups in the United States, Canada, Western Europe, and Japan are division (or country) profit and return on investment (ROI). Return on investment is computed by dividing division (or country) operating income (essentially, income before taxes) by division (or country) total assets. While profit and ROI are commonly used in much of the company, the executive vice presidents in emerging market sectors are given considerable leeway in evaluating their individual country vice presidents. This performance evaluation is important to these managers. Compensation in the Southeast Asia Sector consists of salary and bonus.

The bonus pool for the three managers is dictated by corporate headquarters of Barrows in the United States. The bonus pool formula is not explicitly defined although there is a clear correlation between the size of the pool and the profitability of the sector, however measured.

The allocation of the pool to the individual country managers is at the discretion of Ms. Karlson, the sector executive vice president. In March of year 9, the financial results from the three countries for year 8 have been tabulated and she is now evaluating them. Because this is her first year in this position, she has not had to perform this task in the past. She has hired a local compensation consultant to advise her on the relative performance of the three managers.

The financial staff at sector headquarters receives the financial statements from the controller's staff in each of the three countries and ensures that the statements are consistently prepared in a common currency. The income statements for year 8 are shown in Exhibit 14.14. The balance sheets as of the beginning of year 8 are shown in Exhibit 14.15. Ms. Karlson discusses the source of her concern.

When I look at the financial statements, I can see immediately that Ade [Darmadi, V.P.-Indonesia] has outperformed Isadore [Real, V.P.-Philippines]. But Indonesia is a much larger market than the Philippines. So I calculate ROI to try and adjust for size and now Isadore is outperforming Ade. When I mention this to Ade, she counters that although Indonesia is larger, it is also poorer and geographically dispersed, leading to higher distribution costs. The only thing I can say for sure is that Binh has not developed much of a market.

I also wonder whether headquarters is looking at the right performance measure. I recently attended a seminar on new performance evaluation measures and the seminar speaker spent quite a bit of time on something called economic value added (EVA). The way I understand it, EVA adjusts profit and subtracts a capital charge from it. The capital charge is the cost of capital multiplied by the net assets (total assets less current liabilities) employed. I guess I would use the cost of capital of 20 percent after-tax that corporate policy requires I use for investment decisions. The problem I have is I am not sure how to adjust income, which is an accounting measure, into something more meaningful. We don't do any R D here, so the only item on the statements that was mentioned at the seminar is advertising. (Note: Advertising expenses for the previous three years are shown in Exhibit 14.16.) When I was working in the United States, I came across a study stating that advertising expenditures in our industry have an expected life of about three years. If that's true, then clearly the way we account for advertising is wrong and I should adjust these results accordingly.

There are other issues that I think are more ambiguous. For one thing, Binh developed a new approach for delivering products that cut distribution costs in Vietnam. At our annual retreat, he shared his ideas with Ade and Isadore about how they could adapt this to their markets. In addition, many customers want their stores in Vietnam and Indonesia to be entirely served from Indonesia, so Binh receives no credit for that business.

Required

a. What are some of the factors causing the problems in measuring performance in the Southeast Asia Sector

b. Rank the three countries using each of the following measures of performance:

1. Country profit.

2. Return on investment.

3. Economic value added (EVA).

c. Are there other performance measures you would suggest How would you measure these

d. Write a one-page memo to Ms. Karlson explaining which country performed best. Be sure to explain your reasoning.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

10

How does EVA differ from residual income

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

11

Compare Alternative Measures of Division Performance

The following data are available for two divisions of Solomons Company:

The cost of capital for the company is 15 percent. Ignore taxes.

Required

a. If Solomons measures performance using ROI, which division had the better performance

b. If Solomons measures performance using economic value added, which division had the better performance (The divisions have no current liabilities.)c. Would your evaluation change if the company's cost of capital were 30 percent

The following data are available for two divisions of Solomons Company:

The cost of capital for the company is 15 percent. Ignore taxes.

Required

a. If Solomons measures performance using ROI, which division had the better performance

b. If Solomons measures performance using economic value added, which division had the better performance (The divisions have no current liabilities.)c. Would your evaluation change if the company's cost of capital were 30 percent

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

12

Capital Investment Analysis and Decentralized Performance Measurement

The following exchange occurred just after the finance staff at Diversified Electronics rejected a capital investment proposal.

David Parker (Product Development): I just don't understand why you rejected my proposal.

We can expect to make $230,000 on it before tax.

Shannon West (Finance): David, get real. This product proposal does not meet our short-term ROI target of 15 percent after tax.

David: I'm not so sure about the ROI target, but it is profitable-$230,000 worth.

Shannon: We believe that a company like Diversified Electronics should have a return on investment of 15 percent after tax. The Professional Services division consistently comes in with a 15 percent or better ROI, while your division, Residential Products, has managed to get only 10 percent. The performance of the Aerospace Products division has been especially dismal, with an ROI of only 6 percent. We expect divisions in the future to carry their share of the load.

Diversified Electronics, a growing company in the electronics industry, had grown to its present size of more than $140 million in sales. (See Exhibits 14.17 and 14.18 for Diversified's year 1 and year 2 income statements and balance sheets, respectively.) Diversified Electronics has three divisions, Residential Products, Aerospace Products, and Professional Services, each of which accounts for about one-third of Diversified Electronics's sales. Residential Products, the oldest division, produces furnace thermostats and similar products. The Aerospace Products division is a large job shop that builds electronic devices to customer specifications. A typical job or batch

takes several months to complete. About one-half of Aerospace Products's sales are to the U.S. Defense Department. The newest of the three divisions, Professional Services, provides consulting engineering services. This division has grown tremendously since Diversified Electronics acquired it seven years ago.

Each division operates independently of the others, and corporate management treats each as a separate entity. Division managers make many of the operating decisions. Corporate management coordinates the activities of the various divisions, including the review of all investment proposals over $400,000.

Diversified Electronics measures return on investment as the division's net income divided by total assets. Each division's expenses include the allocated portion of corporate administrative expenses. Since each of Diversified Electronics's divisions is located in a separate facility, management can easily attribute most assets, including receivables, to specific divisions. Management allocates the corporate office assets, including the centrally controlled cash account, to the divisions on the basis of divisional revenues.

Exhibit 14.19 shows the details of David Parker's rejected product proposal.

Required

a. Was the decision to reject the new product proposal the right one If top management used the discounted cash flow (DCF) method instead, what would the results be The company uses a 15 percent after-tax cost of capital (i.e., discount rate) in evaluating projects such as these.

b. Evaluate the manner in which Diversified Electronics has implemented the investment center concept. What pitfalls did it apparently not anticipate What, if anything, should be done with regard to the investment center approach and the use of ROI as a measure of performance

c. What conflicting incentives for managers can occur when yearly ROI is used as a performance measure and DCF is used for capital budgeting

The following exchange occurred just after the finance staff at Diversified Electronics rejected a capital investment proposal.

David Parker (Product Development): I just don't understand why you rejected my proposal.

We can expect to make $230,000 on it before tax.

Shannon West (Finance): David, get real. This product proposal does not meet our short-term ROI target of 15 percent after tax.

David: I'm not so sure about the ROI target, but it is profitable-$230,000 worth.

Shannon: We believe that a company like Diversified Electronics should have a return on investment of 15 percent after tax. The Professional Services division consistently comes in with a 15 percent or better ROI, while your division, Residential Products, has managed to get only 10 percent. The performance of the Aerospace Products division has been especially dismal, with an ROI of only 6 percent. We expect divisions in the future to carry their share of the load.

Diversified Electronics, a growing company in the electronics industry, had grown to its present size of more than $140 million in sales. (See Exhibits 14.17 and 14.18 for Diversified's year 1 and year 2 income statements and balance sheets, respectively.) Diversified Electronics has three divisions, Residential Products, Aerospace Products, and Professional Services, each of which accounts for about one-third of Diversified Electronics's sales. Residential Products, the oldest division, produces furnace thermostats and similar products. The Aerospace Products division is a large job shop that builds electronic devices to customer specifications. A typical job or batch

takes several months to complete. About one-half of Aerospace Products's sales are to the U.S. Defense Department. The newest of the three divisions, Professional Services, provides consulting engineering services. This division has grown tremendously since Diversified Electronics acquired it seven years ago.

Each division operates independently of the others, and corporate management treats each as a separate entity. Division managers make many of the operating decisions. Corporate management coordinates the activities of the various divisions, including the review of all investment proposals over $400,000.

Diversified Electronics measures return on investment as the division's net income divided by total assets. Each division's expenses include the allocated portion of corporate administrative expenses. Since each of Diversified Electronics's divisions is located in a separate facility, management can easily attribute most assets, including receivables, to specific divisions. Management allocates the corporate office assets, including the centrally controlled cash account, to the divisions on the basis of divisional revenues.

Exhibit 14.19 shows the details of David Parker's rejected product proposal.

Required

a. Was the decision to reject the new product proposal the right one If top management used the discounted cash flow (DCF) method instead, what would the results be The company uses a 15 percent after-tax cost of capital (i.e., discount rate) in evaluating projects such as these.

b. Evaluate the manner in which Diversified Electronics has implemented the investment center concept. What pitfalls did it apparently not anticipate What, if anything, should be done with regard to the investment center approach and the use of ROI as a measure of performance

c. What conflicting incentives for managers can occur when yearly ROI is used as a performance measure and DCF is used for capital budgeting

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

13

What impact does the use of gross book value or net book value in the investment base have on the computation of ROI

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

14

Impact of New Project on Performance Measures

Ocean Division currently earns $780,000 and has divisional assets of $2.6 million. The division manager is considering the acquisition of a new asset that will add to profit. The investment has a cost of $450,000 and will have a yearly cash flow of $168,000. The asset will be depreciated using the straight-line method over a six-year life and is expected to have no salvage value. Divisional performance is measured using ROI with beginning-of-year net book values in the denominator. The company's cost of capital is 20 percent. Ignore taxes.

Required

a. What is the divisional ROI before acquisition of the new asset

b. What is the divisional ROI in the first year after acquisition of the new asset

Ocean Division currently earns $780,000 and has divisional assets of $2.6 million. The division manager is considering the acquisition of a new asset that will add to profit. The investment has a cost of $450,000 and will have a yearly cash flow of $168,000. The asset will be depreciated using the straight-line method over a six-year life and is expected to have no salvage value. Divisional performance is measured using ROI with beginning-of-year net book values in the denominator. The company's cost of capital is 20 percent. Ignore taxes.

Required

a. What is the divisional ROI before acquisition of the new asset

b. What is the divisional ROI in the first year after acquisition of the new asset

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

15

What are the dangers of using only business unit measures to evaluate the performance of business unit managers

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

16

Impact of Leasing on Performance Measures

Refer to the data in Exercise 14-23. The division manager learns that he has the option to lease the asset on a year-to-year lease for $148,000 per year. All depreciation and other tax benefits would accrue to the lessor. What is the divisional ROI if the asset is leased

Refer to the data in Exercise 14-23. The division manager learns that he has the option to lease the asset on a year-to-year lease for $148,000 per year. All depreciation and other tax benefits would accrue to the lessor. What is the divisional ROI if the asset is leased

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

17

A company prepares the master budget by taking each division manager's estimate of revenues and costs for the coming period and entering the data into the budget without adjustment. At the end of the year, division managers are given a bonus if their actual division profit exceeds the budgeted profit. Do you see any problems with this system

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

18

Residual Income Measures and New Project Consideration

Refer to the information in Exercises 14-23 and 14-24.

a. What is the division's residual income before considering the project

b. What is the division's residual income if the asset is purchased

c. What is the division's residual income if the asset is leased

Refer to the information in Exercises 14-23 and 14-24.

a. What is the division's residual income before considering the project

b. What is the division's residual income if the asset is purchased

c. What is the division's residual income if the asset is leased

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

19

"If every division manager maximizes divisional income, we will maximize firm income. Therefore, divisional income is the best performance measure." Comment.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

20

Compare Historical Cost, Net Book Value to Gross Book Value

The Caribbean Division of Mega-Entertainment Corporation just started operations. It purchased depreciable assets costing $30 million and having a four-year expected life, after which the assets can be salvaged for $6 million. In addition, the division has $30 million in assets that are not depreciable. After four years, the division will have $30 million available from these nondepreciable assets. This means that the division has invested $60 million in assets with a salvage value of $36 million. Annual depreciation is $6 million. Annual operating cash flows are $15 million. In computing ROI, this division uses end-of-year asset values in the denominator. Depreciation is computed on a straight-line basis, recognizing the salvage values noted. Ignore taxes.

Required

a. Compute ROI, using net book value for each year.

b. Compute ROI, using gross book value for each year.

The Caribbean Division of Mega-Entertainment Corporation just started operations. It purchased depreciable assets costing $30 million and having a four-year expected life, after which the assets can be salvaged for $6 million. In addition, the division has $30 million in assets that are not depreciable. After four years, the division will have $30 million available from these nondepreciable assets. This means that the division has invested $60 million in assets with a salvage value of $36 million. Annual depreciation is $6 million. Annual operating cash flows are $15 million. In computing ROI, this division uses end-of-year asset values in the denominator. Depreciation is computed on a straight-line basis, recognizing the salvage values noted. Ignore taxes.

Required

a. Compute ROI, using net book value for each year.

b. Compute ROI, using gross book value for each year.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

21

What problems might there be if the same methods used to compute firm income are used to compute divisional income Does your answer depend on the type of business a firm is in

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

22

Compare ROI Using Net Book and Gross Book Values

Refer to the data in Exercise 14-26. Assume that the division uses beginning-of-year asset values in the denominator for computing ROI.

Required

a. Compute ROI, using net book value.

b. Compute ROI, using gross book value.

c. If you worked Exercise 14-26, compare those results with those in this exercise. How different is the ROI computed using end-of-year asset values, as in Exercise 14-26, from the ROI using beginning-of-year values in this exercise

Refer to the data in Exercise 14-26. Assume that the division uses beginning-of-year asset values in the denominator for computing ROI.

Required

a. Compute ROI, using net book value.

b. Compute ROI, using gross book value.

c. If you worked Exercise 14-26, compare those results with those in this exercise. How different is the ROI computed using end-of-year asset values, as in Exercise 14-26, from the ROI using beginning-of-year values in this exercise

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

23

The chapter identified some problems with ROI-type measures and suggested that residual income reduces some of them. Why do you think that ROI is a more common performance measure in practice than residual income

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

24

Compare Current Cost to Historical Cost

Refer to the information in Exercise 14-26. In computing ROI, this division uses end-of-year asset values. Assume that all cash flows increase 10 percent at the end of each year. This has the following effect on the assets' replacement cost and annual cash flows:

Depreciation is as follows:

Note that "accumulated" depreciation is 10 percent of the gross book value of depreciable assets after one year, 20 percent after two years, and so forth.

Required

a. Compute ROI using historical cost, net book value.

b. Compute ROI using historical cost, gross book value.

c. Compute ROI using current cost, net book value.

d. Compute ROI using current cost, gross book value.

Refer to the information in Exercise 14-26. In computing ROI, this division uses end-of-year asset values. Assume that all cash flows increase 10 percent at the end of each year. This has the following effect on the assets' replacement cost and annual cash flows:

Depreciation is as follows:

Note that "accumulated" depreciation is 10 percent of the gross book value of depreciable assets after one year, 20 percent after two years, and so forth.

Required

a. Compute ROI using historical cost, net book value.

b. Compute ROI using historical cost, gross book value.

c. Compute ROI using current cost, net book value.

d. Compute ROI using current cost, gross book value.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

25

"Failure to invest in projects is not a problem when you use ROI. If there is a good project, corporate headquarters will just tell the division manager to invest." What are the difficulties with this view

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

26

Effects of Current Cost on Performance Measurements

Upper Division of Lower Company acquired an asset with a cost of $600,000 and a four-year life. The cash flows from the asset, considering the effects of inflation, were scheduled as follows:

The cost of the asset is expected to increase at a rate of 10 percent per year, compounded each year. Performance measures are based on beginning-of-year gross book values for the investment base. Ignore taxes.

Required

a. What is the ROI for each year of the asset's life, using a historical cost approach

b. What is the ROI for each year of the asset's life if both the investment base and depreciation are determined by the current cost of the asset at the start of each year

Upper Division of Lower Company acquired an asset with a cost of $600,000 and a four-year life. The cash flows from the asset, considering the effects of inflation, were scheduled as follows:

The cost of the asset is expected to increase at a rate of 10 percent per year, compounded each year. Performance measures are based on beginning-of-year gross book values for the investment base. Ignore taxes.

Required

a. What is the ROI for each year of the asset's life, using a historical cost approach

b. What is the ROI for each year of the asset's life if both the investment base and depreciation are determined by the current cost of the asset at the start of each year

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

27

How would you respond to the following comment "Residual income and economic value added are identical."

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

28

Equipment Replacement and Performance Measures

Oscar Clemente is the manager of Forbes Division of Pitt, Inc., a manufacturer of biotech products. Forbes Division, which has $4 million in assets, manufactures a special testing device. At the beginning of the current year, Forbes invested $5 million in automated equipment for test machine assembly. The division's expected income statement at the beginning of the year was as follows:

A sales representative from LSI Machine Company approached Oscar in October. LSI has for $6.5 million a new assembly machine that offers significant improvements over the equipment Oscar bought at the beginning of the year. The new equipment would expand division output by 10 percent while reducing cash fixed costs by 5 percent. It would be depreciated for accounting purposes over a three-year life. Depreciation would be net of the $500,000 salvage value of the new machine. The new equipment meets Pitt's 20 percent cost of capital criterion. If Oscar purchases the new machine, it must be installed prior to the end of the year. For practical purposes, though, Oscar can ignore depreciation on the new machine because it will not go into operation until the start of the next year.

The old machine, which has no salvage value, must be disposed of to make room for the new machine.

Pitt has a performance evaluation and bonus plan based on ROI. The return includes any losses on disposal of equipment. Investment is computed based on the end-of-year balance of assets, net book value. Ignore taxes.

Required

a. What is Forbes Division's ROI if Oscar does not acquire the new machine

b. What is Forbes Division's ROI this year if Oscar acquires the new machine

c. If Oscar acquires the new machine and it operates according to specifications, what ROI is expected for next year

Oscar Clemente is the manager of Forbes Division of Pitt, Inc., a manufacturer of biotech products. Forbes Division, which has $4 million in assets, manufactures a special testing device. At the beginning of the current year, Forbes invested $5 million in automated equipment for test machine assembly. The division's expected income statement at the beginning of the year was as follows:

A sales representative from LSI Machine Company approached Oscar in October. LSI has for $6.5 million a new assembly machine that offers significant improvements over the equipment Oscar bought at the beginning of the year. The new equipment would expand division output by 10 percent while reducing cash fixed costs by 5 percent. It would be depreciated for accounting purposes over a three-year life. Depreciation would be net of the $500,000 salvage value of the new machine. The new equipment meets Pitt's 20 percent cost of capital criterion. If Oscar purchases the new machine, it must be installed prior to the end of the year. For practical purposes, though, Oscar can ignore depreciation on the new machine because it will not go into operation until the start of the next year.

The old machine, which has no salvage value, must be disposed of to make room for the new machine.

Pitt has a performance evaluation and bonus plan based on ROI. The return includes any losses on disposal of equipment. Investment is computed based on the end-of-year balance of assets, net book value. Ignore taxes.

Required

a. What is Forbes Division's ROI if Oscar does not acquire the new machine

b. What is Forbes Division's ROI this year if Oscar acquires the new machine

c. If Oscar acquires the new machine and it operates according to specifications, what ROI is expected for next year

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

29

Management of Division A is evaluated based on residual income measures. The division can either rent or buy a certain asset. Might the performance evaluation technique have an impact on the rent-or-buy decision Why or why not Will your answer change if EVA is used

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

30

Evaluate Trade-Offs in Return Measurement

Oscar Clemente (Problem 14-30) is still assessing the problem of whether to acquire LSI's assembly machine. He learns that the new machine could be acquired next year, but if he waits until then, it will cost 15 percent more. The salvage value would still be $500,000. Other costs or revenue estimates would be apportioned on a month-by-month basis for the time each machine (either the current machine or the machine Oscar is considering) is in use. Fractions of months may be ignored. Ignore taxes.

Required

a. When would Oscar want to purchase the new machine if he waits until next year

b. What are the costs that must be considered in making this decision

Oscar Clemente (Problem 14-30) is still assessing the problem of whether to acquire LSI's assembly machine. He learns that the new machine could be acquired next year, but if he waits until then, it will cost 15 percent more. The salvage value would still be $500,000. Other costs or revenue estimates would be apportioned on a month-by-month basis for the time each machine (either the current machine or the machine Oscar is considering) is in use. Fractions of months may be ignored. Ignore taxes.

Required

a. When would Oscar want to purchase the new machine if he waits until next year

b. What are the costs that must be considered in making this decision

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

31

"Every one of our company's divisions has a return on investment in excess of our cost of capital. Our company must be a blockbuster." Comment on this statement.

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

32

ROI and Management Behavior: Ethical Issues

Division managers at Stryker Company are granted a wide range of decision authority. With the exception of managing cash, which is done at corporate headquarters, divisions are responsible for sales, pricing, production, costs of operations, and management of accounts receivable, inventories, accounts payable, and use of existing facilities.

If divisions require funds for investment, division executives present investment proposals to corporate management, which analyzes and documents them. The final decision to commit funds for investment purposes rests with corporate management.

The corporation evaluates divisional executive performance by using the ROI measure. The asset base is composed of fixed assets employed plus working capital, exclusive of cash. The ROI performance of a division executive is the most important appraisal factor for salary changes. In addition, each executive's annual performance bonus is based on ROI results, with increases in ROI having a significant impact on the amount of the bonus.

Stryker adopted the ROI performance measure and related compensation procedures about 10 years ago and seems to have benefited from it. The ROI for the corporation as a whole increased during the first years of the program. Although the ROI continued to increase in each division, corporate ROI has declined in recent years. The corporation has accumulated a sizable amount of short-term marketable securities in the past three years.

Corporate management is concerned about the increase in the short-term marketable securities. A recent article in a financial publication suggested that some companies have overemphasized the use of ROI, with results similar to those experienced by Stryker.

Required

a. Describe the specific actions that division managers might have taken to cause the ROI to increase in each division but decrease for the corporation. Illustrate your explanation with appropriate examples.

b. Using the concepts of goal congruence and motivation of division executives, explain how the overemphasis on the use of the ROI measure at Stryker Company might have resulted in the recent decline in the company's ROI and the increase in cash and short-term marketable securities.

c. What changes could be made in Stryker Company's compensation policy to avoid this problem Explain your answer.

d. Is it ethical for a manager to take actions that increase her ROI but decrease the firm's ROI

(CMA adapted)

Division managers at Stryker Company are granted a wide range of decision authority. With the exception of managing cash, which is done at corporate headquarters, divisions are responsible for sales, pricing, production, costs of operations, and management of accounts receivable, inventories, accounts payable, and use of existing facilities.

If divisions require funds for investment, division executives present investment proposals to corporate management, which analyzes and documents them. The final decision to commit funds for investment purposes rests with corporate management.

The corporation evaluates divisional executive performance by using the ROI measure. The asset base is composed of fixed assets employed plus working capital, exclusive of cash. The ROI performance of a division executive is the most important appraisal factor for salary changes. In addition, each executive's annual performance bonus is based on ROI results, with increases in ROI having a significant impact on the amount of the bonus.

Stryker adopted the ROI performance measure and related compensation procedures about 10 years ago and seems to have benefited from it. The ROI for the corporation as a whole increased during the first years of the program. Although the ROI continued to increase in each division, corporate ROI has declined in recent years. The corporation has accumulated a sizable amount of short-term marketable securities in the past three years.

Corporate management is concerned about the increase in the short-term marketable securities. A recent article in a financial publication suggested that some companies have overemphasized the use of ROI, with results similar to those experienced by Stryker.

Required

a. Describe the specific actions that division managers might have taken to cause the ROI to increase in each division but decrease for the corporation. Illustrate your explanation with appropriate examples.

b. Using the concepts of goal congruence and motivation of division executives, explain how the overemphasis on the use of the ROI measure at Stryker Company might have resulted in the recent decline in the company's ROI and the increase in cash and short-term marketable securities.

c. What changes could be made in Stryker Company's compensation policy to avoid this problem Explain your answer.

d. Is it ethical for a manager to take actions that increase her ROI but decrease the firm's ROI

(CMA adapted)

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

33

What are the advantages of divisional income as a business unit performance measure What are the disadvantages

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

34

"Residual income solves some of the problems with ROI, but because it is an absolute number, it is difficult to compare divisions. We should use residual income divided by assets and then we would have the best of both measures." Do you agree with this statement

Unlock Deck

Unlock for access to all 38 flashcards in this deck.

Unlock Deck

k this deck

35

Impact of Decisions to Capitalize or Expense on Performance Measurement: Ethical Issues

Pharmaceutical firms, oil and gas companies, and other ventures inevitably incur costs on unsuccessful investments in new projects (e.g., new drugs or new wells). For oil and gas firms, a debate continues over whether those costs should be written off as period expense or capitalized as part of the full cost of finding profitable oil and gas ventures. For pharmaceutical firms, GAAP in the United States is clear that R D costs are to be expensed when incurred.