Deck 15: Transfer Pricing

Full screen (f)

Question

Question

Evaluate Transfer Price System

Western States Supply, Inc. (WSS), consists of three divisions-California, Northwest, and Southwest-that operate as if they were independent companies. Each division has its own sales force and production facilities. Each division manager is responsible for sales, cost of operations, acquisition and financing of divisional assets, and working capital management. WSS corporate management evaluates the performance of each division and its managers on the basis of ROI.

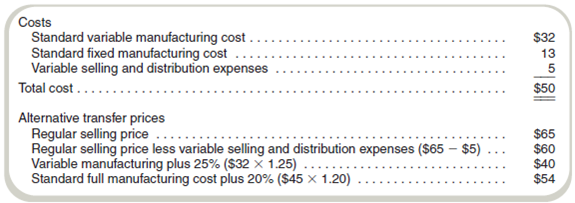

Southwest has just been awarded a contract for a product that uses a component manufactured by outside suppliers as well as by Northwest, which is operating well below capacity. Southwest used a cost figure of $37 for the component in preparing its bid for the new product. Northwest supplied this cost figure in response to Southwest's request for the average variable cost of the component; it represents the standard variable manufacturing cost and variable marketing costs.

Northwest's regular selling price for the component that Southwest needs is $65. Northwest's management indicated that it could supply Southwest the required quantities of the component at the regular selling price less variable selling and distribution expenses. Southwest management responded by offering to pay standard variable manufacturing cost plus 25 percent.

The two divisions have been unable to agree on a transfer price. Corporate management has never established a transfer price policy. The corporate controller suggested a price equal to the standard full manufacturing cost (that is, no selling and distribution expenses) plus a 20 percent markup. The two division managers rejected this price because each considered it grossly unfair. The unit cost structure for the Northwest component and the suggested prices follow.

Required

a. Discuss the effect that each of the proposed prices could have on the attitude of Northwest's management toward intracompany business.

b. Is the negotiation of a price between Northwest and Southwest a satisfactory method to solve the transfer price problem Explain your answer.

c. Should WSS's corporate management become involved in this transfer price controversy Explain your answer.

Western States Supply, Inc. (WSS), consists of three divisions-California, Northwest, and Southwest-that operate as if they were independent companies. Each division has its own sales force and production facilities. Each division manager is responsible for sales, cost of operations, acquisition and financing of divisional assets, and working capital management. WSS corporate management evaluates the performance of each division and its managers on the basis of ROI.

Southwest has just been awarded a contract for a product that uses a component manufactured by outside suppliers as well as by Northwest, which is operating well below capacity. Southwest used a cost figure of $37 for the component in preparing its bid for the new product. Northwest supplied this cost figure in response to Southwest's request for the average variable cost of the component; it represents the standard variable manufacturing cost and variable marketing costs.

Northwest's regular selling price for the component that Southwest needs is $65. Northwest's management indicated that it could supply Southwest the required quantities of the component at the regular selling price less variable selling and distribution expenses. Southwest management responded by offering to pay standard variable manufacturing cost plus 25 percent.

The two divisions have been unable to agree on a transfer price. Corporate management has never established a transfer price policy. The corporate controller suggested a price equal to the standard full manufacturing cost (that is, no selling and distribution expenses) plus a 20 percent markup. The two division managers rejected this price because each considered it grossly unfair. The unit cost structure for the Northwest component and the suggested prices follow.

Required

a. Discuss the effect that each of the proposed prices could have on the attitude of Northwest's management toward intracompany business.

b. Is the negotiation of a price between Northwest and Southwest a satisfactory method to solve the transfer price problem Explain your answer.

c. Should WSS's corporate management become involved in this transfer price controversy Explain your answer.

Question

Question

Question

Question

Segment Reporting

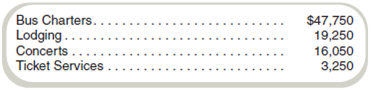

Midwest Entertainment has four operating divisions: Bus Charters, Lodging, Concerts, and Ticket Services. Each division is a separate segment for financial reporting purposes. Revenues and costs related to outside transactions were as follows for the past year (dollars in thousands):

Bus Charters Division participates in a frequent guest program with Lodging Division. During the past year, Bus Charters reported that it traded lodging award coupons for travel that had a retail value of $1.3 million, assuming that the travel was redeemed at full fares. Concerts Division offered 20 percent discounts to Midwest's bus passengers and lodging guests. These discounts to bus passengers were estimated to have a retail value of $350,000. Midwest's lodging guests redeemed $150,000 in concert discount coupons. Midwest's hotels also provided rooms for Bus Charters's employees (drivers and guides). The value of the rooms for the year was $650,000.

The Ticket Services Division sold chartered tours for Bus Charters valued at $200,000 for the year. This service for intracompany lodging was valued at $100,000. It also sold concert tickets for Concerts; tickets for intracompany concert admission were valued at $50,000.

While preparing all of these data for financial statement presentation, Lodging Division's controller stated that the value of the bus coupons should be based on their differential and opportunity costs, not on the full fare. This argument was supported because travel coupons are usually allocated to seats that would otherwise be empty or that are restricted similar to those on discount tickets. If the differential and opportunity costs were used for this transfer price, the value would be $250,000 million instead of $1.3 million. Bus Charters's controller made a similar argument concerning the concert discount coupons. If the differential cost basis were used for the concert coupons, the transfer price would be $50,000 instead of the $350,000 million.

Midwest reports assets in each division as follows (dollars in thousands):

Required

a. Using the retail values for transfer pricing for segment reporting purposes, what are the operating profits for each Midwest division

b. What are the operating profits for each Midwest division using the differential cost basis for pricing transfers

c. Rank each division by ROI using the transfer pricing methods in ( a ) and ( b ). What difference does the transfer pricing system have on the rankings

Midwest Entertainment has four operating divisions: Bus Charters, Lodging, Concerts, and Ticket Services. Each division is a separate segment for financial reporting purposes. Revenues and costs related to outside transactions were as follows for the past year (dollars in thousands):

Bus Charters Division participates in a frequent guest program with Lodging Division. During the past year, Bus Charters reported that it traded lodging award coupons for travel that had a retail value of $1.3 million, assuming that the travel was redeemed at full fares. Concerts Division offered 20 percent discounts to Midwest's bus passengers and lodging guests. These discounts to bus passengers were estimated to have a retail value of $350,000. Midwest's lodging guests redeemed $150,000 in concert discount coupons. Midwest's hotels also provided rooms for Bus Charters's employees (drivers and guides). The value of the rooms for the year was $650,000.

The Ticket Services Division sold chartered tours for Bus Charters valued at $200,000 for the year. This service for intracompany lodging was valued at $100,000. It also sold concert tickets for Concerts; tickets for intracompany concert admission were valued at $50,000.

While preparing all of these data for financial statement presentation, Lodging Division's controller stated that the value of the bus coupons should be based on their differential and opportunity costs, not on the full fare. This argument was supported because travel coupons are usually allocated to seats that would otherwise be empty or that are restricted similar to those on discount tickets. If the differential and opportunity costs were used for this transfer price, the value would be $250,000 million instead of $1.3 million. Bus Charters's controller made a similar argument concerning the concert discount coupons. If the differential cost basis were used for the concert coupons, the transfer price would be $50,000 instead of the $350,000 million.

Midwest reports assets in each division as follows (dollars in thousands):

Required

a. Using the retail values for transfer pricing for segment reporting purposes, what are the operating profits for each Midwest division

b. What are the operating profits for each Midwest division using the differential cost basis for pricing transfers

c. Rank each division by ROI using the transfer pricing methods in ( a ) and ( b ). What difference does the transfer pricing system have on the rankings

Question

Evaluate Transfer Pricing System

Mississippi Company has two decentralized divisions, Illinois and Iowa. Illinois always has purchased certain units from Iowa at $30 per unit. Because Iowa plans to raise the price to $40 per unit, Illinois is considering buying these units from outside suppliers for $30 per unit. Iowa's costs follow:

Required

If Illinois buys from an outside supplier, the facilities that Iowa uses to manufacture these units will remain idle. What will be the result if Mississippi enforces a transfer price of $40 per unit between Illinois and Iowa

Mississippi Company has two decentralized divisions, Illinois and Iowa. Illinois always has purchased certain units from Iowa at $30 per unit. Because Iowa plans to raise the price to $40 per unit, Illinois is considering buying these units from outside suppliers for $30 per unit. Iowa's costs follow:

Required

If Illinois buys from an outside supplier, the facilities that Iowa uses to manufacture these units will remain idle. What will be the result if Mississippi enforces a transfer price of $40 per unit between Illinois and Iowa

Question

Two-Part Transfer Prices

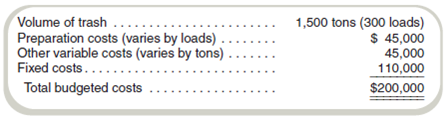

Mathes Corporation manufactures paper products. The company operates a landfill, which it uses to dispose of nonhazardous trash. The trash is hauled from the two nearby manufacturing facilities in trucks that can carry up to 5 tons of trash in a load. The landfill operation requires certain preparation activities regardless of the amount of trash in a truck (i.e., for each load). The budget for the landfill for next year follows:

Mathes is considering making the landfill a profit center and charging the manufacturing plants for disposing of the trash. The landfill has sufficient capacity to operate for at least the next 20 years. Other landfills are available in the area (both private and municipal), and each plant would be free to decide which landfill to use.

Required

a. What transfer pricing rule should Mathes implement at the landfill so that its plant managers would independently make decisions regarding landfill use that would be in the company's best interest

b. Illustrate your rule by computing the transfer price that would be applied to a 4-ton load of trash from one of the plants.

Mathes Corporation manufactures paper products. The company operates a landfill, which it uses to dispose of nonhazardous trash. The trash is hauled from the two nearby manufacturing facilities in trucks that can carry up to 5 tons of trash in a load. The landfill operation requires certain preparation activities regardless of the amount of trash in a truck (i.e., for each load). The budget for the landfill for next year follows:

Mathes is considering making the landfill a profit center and charging the manufacturing plants for disposing of the trash. The landfill has sufficient capacity to operate for at least the next 20 years. Other landfills are available in the area (both private and municipal), and each plant would be free to decide which landfill to use.

Required

a. What transfer pricing rule should Mathes implement at the landfill so that its plant managers would independently make decisions regarding landfill use that would be in the company's best interest

b. Illustrate your rule by computing the transfer price that would be applied to a 4-ton load of trash from one of the plants.

Question

Question

Question

Budget versus Actual Costs

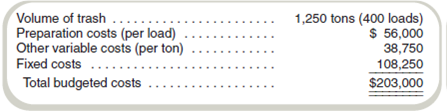

Refer to the data in Problem 15-32. At the end of the year, the following data are available on actual operations at the landfill.

Required

Based on the actual activities and costs, would you change the recommendation you made in Problem 15-32 Why or why not

Refer to the data in Problem 15-32. At the end of the year, the following data are available on actual operations at the landfill.

Required

Based on the actual activities and costs, would you change the recommendation you made in Problem 15-32 Why or why not

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Segment Reporting

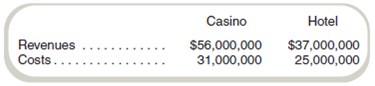

Perth Corporation has two operating divisions, a casino and a hotel. The two divisions meet the requirements for segment disclosures. Before transactions between the two divisions are considered, revenues and costs are as follows:

The casino and the hotel have a joint marketing arrangement by which the hotel gives coupons redeemable at casino slot machines and the casino gives discount coupons good for stays at the hotel. The value of the coupons for the slot machines redeemed during the past year totaled $8,000,000. The discount coupons redeemed at the hotel totaled $3,000,000. As of the end of the year, all coupons for the current year expired.

Required

What are the operating profits for each division considering the effects of the costs arising from the joint marketing agreement

Perth Corporation has two operating divisions, a casino and a hotel. The two divisions meet the requirements for segment disclosures. Before transactions between the two divisions are considered, revenues and costs are as follows:

The casino and the hotel have a joint marketing arrangement by which the hotel gives coupons redeemable at casino slot machines and the casino gives discount coupons good for stays at the hotel. The value of the coupons for the slot machines redeemed during the past year totaled $8,000,000. The discount coupons redeemed at the hotel totaled $3,000,000. As of the end of the year, all coupons for the current year expired.

Required

What are the operating profits for each division considering the effects of the costs arising from the joint marketing agreement

Question

Question

Question

Question

Evaluate Profit Impact of Alternative Transfer Decisions

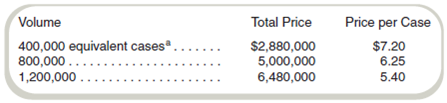

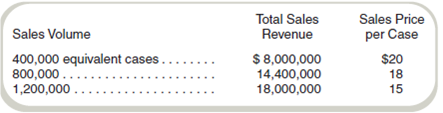

Amazon Beverages produces and bottles a line of soft drinks using exotic fruits from Latin America and Asia. The manufacturing process entails mixing and adding juices and coloring ingredients at the bottling plant, which is a part of Mixing Division. The finished product is packaged in a company-produced glass bottle and packed in cases of 24 bottles each.

Because the appearance of the bottle heavily influences sales volume, Amazon developed a unique bottle production process at the company's container plant, which is a part of Container Division. The Mixing Division uses all of the container plant's production. Each division (Mixing and Container) is considered a separate profit center and evaluated as such. As the new corporate controller, you are responsible for determining the proper transfer price to use for the bottles produced for Mixing Division.

At your request, Container Division's general manager asked other bottle manufacturers to quote a price for the number and sizes demanded by Mixing Division. These competitive prices follow:

a An equivalent case represents 24 bottles.

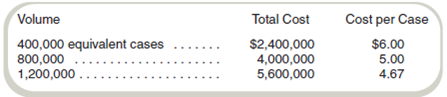

Container Division's cost analysis indicates that it can produce bottles at these costs:

These costs include fixed costs of $800,000 and variable costs of $4 per equivalent case. These data have caused considerable corporate discussion as to the proper price to use in the transfer of bottles from Container Division to Mixing Division. This interest is heightened because a significant portion of a division manager's income is an incentive bonus based on profit center results.

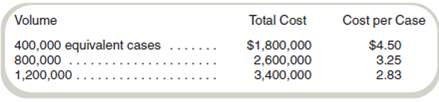

Mixing Division has the following costs in addition to the bottle costs:

The corporate marketing group has furnished the following price-demand relationship for the finished product:

Required

a. Amazon Beverages has used market price transfer prices in the past. Using the current market prices and costs and assuming a volume of 1.2 million cases, calculate operating profits for:

(1) Container Division.

(2) Mixing Division.

(3) Amazon Beverages.

b. Is this production and sales level the most profitable volume for:

(1) Container Division

(2) Mixing Division

(3) Amazon Beverages

Explain.

Amazon Beverages produces and bottles a line of soft drinks using exotic fruits from Latin America and Asia. The manufacturing process entails mixing and adding juices and coloring ingredients at the bottling plant, which is a part of Mixing Division. The finished product is packaged in a company-produced glass bottle and packed in cases of 24 bottles each.

Because the appearance of the bottle heavily influences sales volume, Amazon developed a unique bottle production process at the company's container plant, which is a part of Container Division. The Mixing Division uses all of the container plant's production. Each division (Mixing and Container) is considered a separate profit center and evaluated as such. As the new corporate controller, you are responsible for determining the proper transfer price to use for the bottles produced for Mixing Division.

At your request, Container Division's general manager asked other bottle manufacturers to quote a price for the number and sizes demanded by Mixing Division. These competitive prices follow:

a An equivalent case represents 24 bottles.

Container Division's cost analysis indicates that it can produce bottles at these costs:

These costs include fixed costs of $800,000 and variable costs of $4 per equivalent case. These data have caused considerable corporate discussion as to the proper price to use in the transfer of bottles from Container Division to Mixing Division. This interest is heightened because a significant portion of a division manager's income is an incentive bonus based on profit center results.

Mixing Division has the following costs in addition to the bottle costs:

The corporate marketing group has furnished the following price-demand relationship for the finished product:

Required

a. Amazon Beverages has used market price transfer prices in the past. Using the current market prices and costs and assuming a volume of 1.2 million cases, calculate operating profits for:

(1) Container Division.

(2) Mixing Division.

(3) Amazon Beverages.

b. Is this production and sales level the most profitable volume for:

(1) Container Division

(2) Mixing Division

(3) Amazon Beverages

Explain.

Question

Question

Question

Question

Question

Question

Transfer Pricing: Performance Evaluation Issues

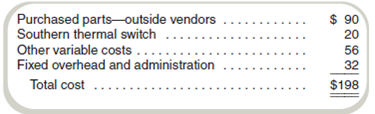

Cochise Corporation's Southern Division is operating at capacity. It has been asked by Northern Division to supply it a thermal switch, which Southern sells to its regular customers for $30 each. Northern, which is operating at 70 percent capacity, is willing to pay $20 each for the switch. Northern will put the switch into a kitchen appliance that it is manufacturing on a cost-plus basis for the Army. Southern has a $17 variable cost of producing the switch.

The cost of the kitchen appliance as built by Northern follows:

Northern believes that the price concession is necessary to get the job.

The company uses ROI and dollar profits in evaluating the division and divisional manager's performance.

Required

a. If you were Southern's division controller, would you recommend supplying the switch to Northern (Ignore any income tax issues.) Why or why not

b. Would it be to the short-run economic advantage of Cochise Corporation for Southern to supply Northern with the switch at $20 each (Ignore any income tax issues.) Explain your answer.

c. Discuss the organizational and managerial behavior difficulties, if any, inherent in this situation. As Cochise's controller, what would you advise the corporation's president to do in this situation

Cochise Corporation's Southern Division is operating at capacity. It has been asked by Northern Division to supply it a thermal switch, which Southern sells to its regular customers for $30 each. Northern, which is operating at 70 percent capacity, is willing to pay $20 each for the switch. Northern will put the switch into a kitchen appliance that it is manufacturing on a cost-plus basis for the Army. Southern has a $17 variable cost of producing the switch.

The cost of the kitchen appliance as built by Northern follows:

Northern believes that the price concession is necessary to get the job.

The company uses ROI and dollar profits in evaluating the division and divisional manager's performance.

Required

a. If you were Southern's division controller, would you recommend supplying the switch to Northern (Ignore any income tax issues.) Why or why not

b. Would it be to the short-run economic advantage of Cochise Corporation for Southern to supply Northern with the switch at $20 each (Ignore any income tax issues.) Explain your answer.

c. Discuss the organizational and managerial behavior difficulties, if any, inherent in this situation. As Cochise's controller, what would you advise the corporation's president to do in this situation

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/35

Play

Full screen (f)

Deck 15: Transfer Pricing

1

How does the choice of a transfer price affect the operating profits of both segments involved in an intracompany transfer Why is the choice of a transfer price important if the total profits of the firm are unaffected by this choice

Transfer Pricing: impact on the individual divisions

Intercompany transfer or inter-division transfer of goods and services affects the balance sheet of individual divisions in significant ways. Let us assume that there are two divisions A B within a company. Output of A can be sold into the market as well as it could be supplied as input to division B for further processing. In the interconnected transactions like this, the profit of both the divisions depends to a large extent on the prices they pay for the input raw materials.

Assume that if A is forced to sell its output to division B at a price which is lower than market price, then the profit shown by A would be lower than what it should have been had it been allowed to sell into the open market whereas the profits of B would be inflated. Contrary to above if B is forced to acquire the output of A at a price higher than market price, A's balancesheet would be showing extra profits it made it on supplies to B, whereas B's profit will be comparatively lower from the position had it been allowed to acquire from the open market.

And since the remuneration of managers are based on the profit that their divisions make. No manager, in such a scenario would like to compromises with his/her remuneration. And will prefer to sell or buy goods at optimal prices which ensures good returns for their division.

Now, these are competing interests because selling division would prefer to have maximum price that it can fetch, and buying division would love to buy the standard required quality goods at the lowest prices possible. The equilibrium amongst the competing divisions reach when they transact at the market price. Why so Say if the selling division prices its output more than the prevalent market prices, then the buying division will have the option to buy its input requirement from the market and not from the selling division. So for the selling division, the market price is the maximum price that it can fetch.

On the other hand, if the buying division put a price which is lower than the market price, then the selling division would prefer its product to be sold into the open market rather than to its own buying division. The nature of competing interest amongst the divisions sometime may lead to hampering of organizational interest as a whole. Therefore modern day organizations prefer to have market price as a transaction price between the competing divisions. Because this is the point where equilibrium is reached and organization doesn't loss anything on account of competing interests of divisions.

Therefore it is essential for keeping the morale of on-line managers high that a just and appropriate transfer price must be developed which address the issues and concerns of on-line managers.

Intercompany transfer or inter-division transfer of goods and services affects the balance sheet of individual divisions in significant ways. Let us assume that there are two divisions A B within a company. Output of A can be sold into the market as well as it could be supplied as input to division B for further processing. In the interconnected transactions like this, the profit of both the divisions depends to a large extent on the prices they pay for the input raw materials.

Assume that if A is forced to sell its output to division B at a price which is lower than market price, then the profit shown by A would be lower than what it should have been had it been allowed to sell into the open market whereas the profits of B would be inflated. Contrary to above if B is forced to acquire the output of A at a price higher than market price, A's balancesheet would be showing extra profits it made it on supplies to B, whereas B's profit will be comparatively lower from the position had it been allowed to acquire from the open market.

And since the remuneration of managers are based on the profit that their divisions make. No manager, in such a scenario would like to compromises with his/her remuneration. And will prefer to sell or buy goods at optimal prices which ensures good returns for their division.

Now, these are competing interests because selling division would prefer to have maximum price that it can fetch, and buying division would love to buy the standard required quality goods at the lowest prices possible. The equilibrium amongst the competing divisions reach when they transact at the market price. Why so Say if the selling division prices its output more than the prevalent market prices, then the buying division will have the option to buy its input requirement from the market and not from the selling division. So for the selling division, the market price is the maximum price that it can fetch.

On the other hand, if the buying division put a price which is lower than the market price, then the selling division would prefer its product to be sold into the open market rather than to its own buying division. The nature of competing interest amongst the divisions sometime may lead to hampering of organizational interest as a whole. Therefore modern day organizations prefer to have market price as a transaction price between the competing divisions. Because this is the point where equilibrium is reached and organization doesn't loss anything on account of competing interests of divisions.

Therefore it is essential for keeping the morale of on-line managers high that a just and appropriate transfer price must be developed which address the issues and concerns of on-line managers.

2

Evaluate Transfer Price System

Western States Supply, Inc. (WSS), consists of three divisions-California, Northwest, and Southwest-that operate as if they were independent companies. Each division has its own sales force and production facilities. Each division manager is responsible for sales, cost of operations, acquisition and financing of divisional assets, and working capital management. WSS corporate management evaluates the performance of each division and its managers on the basis of ROI.

Southwest has just been awarded a contract for a product that uses a component manufactured by outside suppliers as well as by Northwest, which is operating well below capacity. Southwest used a cost figure of $37 for the component in preparing its bid for the new product. Northwest supplied this cost figure in response to Southwest's request for the average variable cost of the component; it represents the standard variable manufacturing cost and variable marketing costs.

Northwest's regular selling price for the component that Southwest needs is $65. Northwest's management indicated that it could supply Southwest the required quantities of the component at the regular selling price less variable selling and distribution expenses. Southwest management responded by offering to pay standard variable manufacturing cost plus 25 percent.

The two divisions have been unable to agree on a transfer price. Corporate management has never established a transfer price policy. The corporate controller suggested a price equal to the standard full manufacturing cost (that is, no selling and distribution expenses) plus a 20 percent markup. The two division managers rejected this price because each considered it grossly unfair. The unit cost structure for the Northwest component and the suggested prices follow.

Required

a. Discuss the effect that each of the proposed prices could have on the attitude of Northwest's management toward intracompany business.

b. Is the negotiation of a price between Northwest and Southwest a satisfactory method to solve the transfer price problem Explain your answer.

c. Should WSS's corporate management become involved in this transfer price controversy Explain your answer.

Western States Supply, Inc. (WSS), consists of three divisions-California, Northwest, and Southwest-that operate as if they were independent companies. Each division has its own sales force and production facilities. Each division manager is responsible for sales, cost of operations, acquisition and financing of divisional assets, and working capital management. WSS corporate management evaluates the performance of each division and its managers on the basis of ROI.

Southwest has just been awarded a contract for a product that uses a component manufactured by outside suppliers as well as by Northwest, which is operating well below capacity. Southwest used a cost figure of $37 for the component in preparing its bid for the new product. Northwest supplied this cost figure in response to Southwest's request for the average variable cost of the component; it represents the standard variable manufacturing cost and variable marketing costs.

Northwest's regular selling price for the component that Southwest needs is $65. Northwest's management indicated that it could supply Southwest the required quantities of the component at the regular selling price less variable selling and distribution expenses. Southwest management responded by offering to pay standard variable manufacturing cost plus 25 percent.

The two divisions have been unable to agree on a transfer price. Corporate management has never established a transfer price policy. The corporate controller suggested a price equal to the standard full manufacturing cost (that is, no selling and distribution expenses) plus a 20 percent markup. The two division managers rejected this price because each considered it grossly unfair. The unit cost structure for the Northwest component and the suggested prices follow.

Required

a. Discuss the effect that each of the proposed prices could have on the attitude of Northwest's management toward intracompany business.

b. Is the negotiation of a price between Northwest and Southwest a satisfactory method to solve the transfer price problem Explain your answer.

c. Should WSS's corporate management become involved in this transfer price controversy Explain your answer.

Transfer pricing

Transfer pricing is the amount charged by one business unit of a company to another business unit for the products supplied. Each business unit is considered as separate responsibility centers and sale from one business unit to another business unit is consider as sale to an outsider. The sales based on transfer pricing are recorded in the accounting books of a firm and transfer prices are used for decision making, merchandise costing and performance assessment.

a.

NW division management will accept the transfer price of $65 which is their regular selling price. They sell their product to outsiders at this price only.

NW division management will accept the transfer price of $60 which is offered by them to S division. For this price amount they are ready to forgo their variable selling and distribution expense i.e. $5 per unit.

NW division management rejected $40 which is variable manufacturing cost plus 25% mark-up proposed by S division management. N Division believe that they should be at least $60.

NW division management rejected $54 which is total manufacturing cost plus 20% mark-up proposed by corporate management. N Division believe that they should be at least $60.

b.

South division has offered the transfer price of $40 which is variable manufacturing cost plus 25% mark-up which is not accepted by N division management.

N Division management has offered the transfer price of $60 which is excluding their variable selling and distribution expense i.e. $5 per unit, but the same is rejected by S division.

It means that negotiated price shall not work out between two division. It would have been the best option if they both agree on some mutually accepted transfer price i.e. negotiated price.

c.

WSS management needs to involve themselves in the transfer price dispute so that business do not suffer.

WSS management should introduce a performance evaluation measures for both the division that motivates them to work hard and agree on some common price. Their performance may be measured more on the basis of productivity and efficiency and less on profitability.

Transfer pricing is the amount charged by one business unit of a company to another business unit for the products supplied. Each business unit is considered as separate responsibility centers and sale from one business unit to another business unit is consider as sale to an outsider. The sales based on transfer pricing are recorded in the accounting books of a firm and transfer prices are used for decision making, merchandise costing and performance assessment.

a.

NW division management will accept the transfer price of $65 which is their regular selling price. They sell their product to outsiders at this price only.

NW division management will accept the transfer price of $60 which is offered by them to S division. For this price amount they are ready to forgo their variable selling and distribution expense i.e. $5 per unit.

NW division management rejected $40 which is variable manufacturing cost plus 25% mark-up proposed by S division management. N Division believe that they should be at least $60.

NW division management rejected $54 which is total manufacturing cost plus 20% mark-up proposed by corporate management. N Division believe that they should be at least $60.

b.

South division has offered the transfer price of $40 which is variable manufacturing cost plus 25% mark-up which is not accepted by N division management.

N Division management has offered the transfer price of $60 which is excluding their variable selling and distribution expense i.e. $5 per unit, but the same is rejected by S division.

It means that negotiated price shall not work out between two division. It would have been the best option if they both agree on some mutually accepted transfer price i.e. negotiated price.

c.

WSS management needs to involve themselves in the transfer price dispute so that business do not suffer.

WSS management should introduce a performance evaluation measures for both the division that motivates them to work hard and agree on some common price. Their performance may be measured more on the basis of productivity and efficiency and less on profitability.

3

When setting a transfer price for goods that are sold across international boundaries, what factors should management consider

Transfer pricing

Transfer pricing is the amount charged by one business unit of a company to another business unit for the products supplied. Each business unit is considered as separate responsibility centers and sale from one business unit to another business unit is consider as sale to an outsider. The sales based on transfer pricing are recorded in the accounting books of a firm and transfer prices are used for decision making, merchandise costing and performance assessment.

Factors affecting transfer pricing of the goods sold across international boundaries

Multinational companies have divisions across the international boundaries and they need to consider following factors while deciding on the transfer prices: -

•The tax rates of two countries i.e. exporting country and importing country, on the profits earned. If the tax rates are high in the importing country, then transfer prices are inflated by the exporting business unit so that amount of tax liability on the profits earned is reduced for importing divisions.

•Perfect market for the goods exported so that correct market price can be established and used as transfer price. It is rare to find the perfect substitute for the products exported or imported.

Taxing authorities carefully check the transfer pricing used while assessing returns submitted by the companies doing international interdivisional sale transactions.

Transfer pricing is the amount charged by one business unit of a company to another business unit for the products supplied. Each business unit is considered as separate responsibility centers and sale from one business unit to another business unit is consider as sale to an outsider. The sales based on transfer pricing are recorded in the accounting books of a firm and transfer prices are used for decision making, merchandise costing and performance assessment.

Factors affecting transfer pricing of the goods sold across international boundaries

Multinational companies have divisions across the international boundaries and they need to consider following factors while deciding on the transfer prices: -

•The tax rates of two countries i.e. exporting country and importing country, on the profits earned. If the tax rates are high in the importing country, then transfer prices are inflated by the exporting business unit so that amount of tax liability on the profits earned is reduced for importing divisions.

•Perfect market for the goods exported so that correct market price can be established and used as transfer price. It is rare to find the perfect substitute for the products exported or imported.

Taxing authorities carefully check the transfer pricing used while assessing returns submitted by the companies doing international interdivisional sale transactions.

4

Transfer Prices and Tax Regulations: Ethical Issues

Gage Corporation has two operating divisions in a semiautonomous organizational structure. Adams Division, located in the United States, produces a specialized electrical component that is an input to Bute Division, located in the south of England. Adams uses idle capacity to produce the component, which has a domestic market price of $12. Its variable costs are $5 per unit. Gage's U.S. tax rate is 40 percent of income.

In addition to the transfer price for each component received from Adams, Bute pays a $3 per unit shipping fee. The component becomes a part of its assembled product, which costs an additional $2 to produce and sells for an equivalent of $23. Bute could purchase the component from a Manchester (England) supplier for $10 per unit. Gage's English tax rate is 70 percent of income. Assume that English tax laws permit transferring at either variable cost or market price.

Required

a. What transfer price is economically optimal for Gage Corporation Show computations.

b. Is it ethical to choose a transfer price for tax purposes that is different from the transfer price used to evaluate a business unit's performance

c. Suppose Gage had a third operating division, Case, in Singapore, where the tax rate is below that of the United States. Would it be ethical for Gage to use different transfer prices for transactions between Adams and Bute and between Adams and Case

Gage Corporation has two operating divisions in a semiautonomous organizational structure. Adams Division, located in the United States, produces a specialized electrical component that is an input to Bute Division, located in the south of England. Adams uses idle capacity to produce the component, which has a domestic market price of $12. Its variable costs are $5 per unit. Gage's U.S. tax rate is 40 percent of income.

In addition to the transfer price for each component received from Adams, Bute pays a $3 per unit shipping fee. The component becomes a part of its assembled product, which costs an additional $2 to produce and sells for an equivalent of $23. Bute could purchase the component from a Manchester (England) supplier for $10 per unit. Gage's English tax rate is 70 percent of income. Assume that English tax laws permit transferring at either variable cost or market price.

Required

a. What transfer price is economically optimal for Gage Corporation Show computations.

b. Is it ethical to choose a transfer price for tax purposes that is different from the transfer price used to evaluate a business unit's performance

c. Suppose Gage had a third operating division, Case, in Singapore, where the tax rate is below that of the United States. Would it be ethical for Gage to use different transfer prices for transactions between Adams and Bute and between Adams and Case

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

5

Apply Transfer Pricing Rules

Best Practices, Inc., is a management consulting firm. Its Corporate Division advises private firms on the adoption and use of cost management systems. Government Division consults with state and local governments. Government Division has a client that is interested in implementing an activity- based costing system in its public works department. The division's head approached the head of Corporate Division about using one of its associates. Corporate Division charges clients $300 per hour for associate services, the same rate other consulting companies charge. The Government Division head complained that it could hire its own associate at an estimated variable cost of $100 per hour, which is what Corporate pays its associates.

Required

a. What is the minimum transfer price that Corporate Division should obtain for its services, assuming that it is operating at capacity

b. What is the maximum price that Government Division should pay

c. Would your answers in ( a ) or ( b ) change if Corporate Division had idle capacity If so, which answer would change, and what would the new amount be

Best Practices, Inc., is a management consulting firm. Its Corporate Division advises private firms on the adoption and use of cost management systems. Government Division consults with state and local governments. Government Division has a client that is interested in implementing an activity- based costing system in its public works department. The division's head approached the head of Corporate Division about using one of its associates. Corporate Division charges clients $300 per hour for associate services, the same rate other consulting companies charge. The Government Division head complained that it could hire its own associate at an estimated variable cost of $100 per hour, which is what Corporate pays its associates.

Required

a. What is the minimum transfer price that Corporate Division should obtain for its services, assuming that it is operating at capacity

b. What is the maximum price that Government Division should pay

c. Would your answers in ( a ) or ( b ) change if Corporate Division had idle capacity If so, which answer would change, and what would the new amount be

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

6

Segment Reporting

Midwest Entertainment has four operating divisions: Bus Charters, Lodging, Concerts, and Ticket Services. Each division is a separate segment for financial reporting purposes. Revenues and costs related to outside transactions were as follows for the past year (dollars in thousands):

Bus Charters Division participates in a frequent guest program with Lodging Division. During the past year, Bus Charters reported that it traded lodging award coupons for travel that had a retail value of $1.3 million, assuming that the travel was redeemed at full fares. Concerts Division offered 20 percent discounts to Midwest's bus passengers and lodging guests. These discounts to bus passengers were estimated to have a retail value of $350,000. Midwest's lodging guests redeemed $150,000 in concert discount coupons. Midwest's hotels also provided rooms for Bus Charters's employees (drivers and guides). The value of the rooms for the year was $650,000.

The Ticket Services Division sold chartered tours for Bus Charters valued at $200,000 for the year. This service for intracompany lodging was valued at $100,000. It also sold concert tickets for Concerts; tickets for intracompany concert admission were valued at $50,000.

While preparing all of these data for financial statement presentation, Lodging Division's controller stated that the value of the bus coupons should be based on their differential and opportunity costs, not on the full fare. This argument was supported because travel coupons are usually allocated to seats that would otherwise be empty or that are restricted similar to those on discount tickets. If the differential and opportunity costs were used for this transfer price, the value would be $250,000 million instead of $1.3 million. Bus Charters's controller made a similar argument concerning the concert discount coupons. If the differential cost basis were used for the concert coupons, the transfer price would be $50,000 instead of the $350,000 million.

Midwest reports assets in each division as follows (dollars in thousands):

Required

a. Using the retail values for transfer pricing for segment reporting purposes, what are the operating profits for each Midwest division

b. What are the operating profits for each Midwest division using the differential cost basis for pricing transfers

c. Rank each division by ROI using the transfer pricing methods in ( a ) and ( b ). What difference does the transfer pricing system have on the rankings

Midwest Entertainment has four operating divisions: Bus Charters, Lodging, Concerts, and Ticket Services. Each division is a separate segment for financial reporting purposes. Revenues and costs related to outside transactions were as follows for the past year (dollars in thousands):

Bus Charters Division participates in a frequent guest program with Lodging Division. During the past year, Bus Charters reported that it traded lodging award coupons for travel that had a retail value of $1.3 million, assuming that the travel was redeemed at full fares. Concerts Division offered 20 percent discounts to Midwest's bus passengers and lodging guests. These discounts to bus passengers were estimated to have a retail value of $350,000. Midwest's lodging guests redeemed $150,000 in concert discount coupons. Midwest's hotels also provided rooms for Bus Charters's employees (drivers and guides). The value of the rooms for the year was $650,000.

The Ticket Services Division sold chartered tours for Bus Charters valued at $200,000 for the year. This service for intracompany lodging was valued at $100,000. It also sold concert tickets for Concerts; tickets for intracompany concert admission were valued at $50,000.

While preparing all of these data for financial statement presentation, Lodging Division's controller stated that the value of the bus coupons should be based on their differential and opportunity costs, not on the full fare. This argument was supported because travel coupons are usually allocated to seats that would otherwise be empty or that are restricted similar to those on discount tickets. If the differential and opportunity costs were used for this transfer price, the value would be $250,000 million instead of $1.3 million. Bus Charters's controller made a similar argument concerning the concert discount coupons. If the differential cost basis were used for the concert coupons, the transfer price would be $50,000 instead of the $350,000 million.

Midwest reports assets in each division as follows (dollars in thousands):

Required

a. Using the retail values for transfer pricing for segment reporting purposes, what are the operating profits for each Midwest division

b. What are the operating profits for each Midwest division using the differential cost basis for pricing transfers

c. Rank each division by ROI using the transfer pricing methods in ( a ) and ( b ). What difference does the transfer pricing system have on the rankings

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

7

Evaluate Transfer Pricing System

Mississippi Company has two decentralized divisions, Illinois and Iowa. Illinois always has purchased certain units from Iowa at $30 per unit. Because Iowa plans to raise the price to $40 per unit, Illinois is considering buying these units from outside suppliers for $30 per unit. Iowa's costs follow:

Required

If Illinois buys from an outside supplier, the facilities that Iowa uses to manufacture these units will remain idle. What will be the result if Mississippi enforces a transfer price of $40 per unit between Illinois and Iowa

Mississippi Company has two decentralized divisions, Illinois and Iowa. Illinois always has purchased certain units from Iowa at $30 per unit. Because Iowa plans to raise the price to $40 per unit, Illinois is considering buying these units from outside suppliers for $30 per unit. Iowa's costs follow:

Required

If Illinois buys from an outside supplier, the facilities that Iowa uses to manufacture these units will remain idle. What will be the result if Mississippi enforces a transfer price of $40 per unit between Illinois and Iowa

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

8

Two-Part Transfer Prices

Mathes Corporation manufactures paper products. The company operates a landfill, which it uses to dispose of nonhazardous trash. The trash is hauled from the two nearby manufacturing facilities in trucks that can carry up to 5 tons of trash in a load. The landfill operation requires certain preparation activities regardless of the amount of trash in a truck (i.e., for each load). The budget for the landfill for next year follows:

Mathes is considering making the landfill a profit center and charging the manufacturing plants for disposing of the trash. The landfill has sufficient capacity to operate for at least the next 20 years. Other landfills are available in the area (both private and municipal), and each plant would be free to decide which landfill to use.

Required

a. What transfer pricing rule should Mathes implement at the landfill so that its plant managers would independently make decisions regarding landfill use that would be in the company's best interest

b. Illustrate your rule by computing the transfer price that would be applied to a 4-ton load of trash from one of the plants.

Mathes Corporation manufactures paper products. The company operates a landfill, which it uses to dispose of nonhazardous trash. The trash is hauled from the two nearby manufacturing facilities in trucks that can carry up to 5 tons of trash in a load. The landfill operation requires certain preparation activities regardless of the amount of trash in a truck (i.e., for each load). The budget for the landfill for next year follows:

Mathes is considering making the landfill a profit center and charging the manufacturing plants for disposing of the trash. The landfill has sufficient capacity to operate for at least the next 20 years. Other landfills are available in the area (both private and municipal), and each plant would be free to decide which landfill to use.

Required

a. What transfer pricing rule should Mathes implement at the landfill so that its plant managers would independently make decisions regarding landfill use that would be in the company's best interest

b. Illustrate your rule by computing the transfer price that would be applied to a 4-ton load of trash from one of the plants.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

9

What is the purpose of a transfer price

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

10

Evaluate Transfer Pricing System

A company permits its decentralized units to "lease" space to one another. Uptown Division has leased some of its idle warehouse space to Downtown Division for $12 per square foot per month. Recently, Uptown obtained a new five-year contract, which will increase its production sufficiently so that the warehouse space is more valuable to it. Uptown has notified Downtown that the rental price will increase to $42 per square foot per month. Downtown can lease space at $24 per square foot in another warehouse from an outside company but prefers to stay in the shared facilities. Downtown's manager states that she would prefer not to move. If Downtown Division continues to use the space, Uptown will have to rent other space for $36 per square foot per month. (The difference in rental prices occurs because Uptown Division requires a more substantial warehouse building than Downtown Division does.)Required

Recommend a transfer price and explain your reasons for choosing that price.

A company permits its decentralized units to "lease" space to one another. Uptown Division has leased some of its idle warehouse space to Downtown Division for $12 per square foot per month. Recently, Uptown obtained a new five-year contract, which will increase its production sufficiently so that the warehouse space is more valuable to it. Uptown has notified Downtown that the rental price will increase to $42 per square foot per month. Downtown can lease space at $24 per square foot in another warehouse from an outside company but prefers to stay in the shared facilities. Downtown's manager states that she would prefer not to move. If Downtown Division continues to use the space, Uptown will have to rent other space for $36 per square foot per month. (The difference in rental prices occurs because Uptown Division requires a more substantial warehouse building than Downtown Division does.)Required

Recommend a transfer price and explain your reasons for choosing that price.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

11

Budget versus Actual Costs

Refer to the data in Problem 15-32. At the end of the year, the following data are available on actual operations at the landfill.

Required

Based on the actual activities and costs, would you change the recommendation you made in Problem 15-32 Why or why not

Refer to the data in Problem 15-32. At the end of the year, the following data are available on actual operations at the landfill.

Required

Based on the actual activities and costs, would you change the recommendation you made in Problem 15-32 Why or why not

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

12

Do transfer prices exist in centralized firms Why

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

13

Evaluate Transfer Pricing System

Division A offers its product to outside markets for $60. It incurs variable costs of $22 per unit and fixed costs of $75,000 per month based on monthly production of 4,000 units. Division B can acquire the product from an alternate supplier for $63 per unit or from Division A for $60 plus $4 per unit in transportation costs in addition to the transfer price charged by Division A.

Required

a. What are the costs and benefits of the alternatives available to Division A and Division B with respect to the transfer of Division A's product Assume that Division A can market all that it can produce.

b. How would your answer change if Division A had idle capacity sufficient to cover all of Division B's needs

Division A offers its product to outside markets for $60. It incurs variable costs of $22 per unit and fixed costs of $75,000 per month based on monthly production of 4,000 units. Division B can acquire the product from an alternate supplier for $63 per unit or from Division A for $60 plus $4 per unit in transportation costs in addition to the transfer price charged by Division A.

Required

a. What are the costs and benefits of the alternatives available to Division A and Division B with respect to the transfer of Division A's product Assume that Division A can market all that it can produce.

b. How would your answer change if Division A had idle capacity sufficient to cover all of Division B's needs

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

14

Custom Freight Systems (A): Transfer Pricing

"We can't drop our prices below $210 per hundred pounds," exclaimed Greg Berman, manager of Forwarders, a division of Custom Freight Systems. "Our margins are already razor thin. Our costs just won't allow us to go any lower. Corporate rewards our division based on our profitability and I won't lower my prices below $210."

Custom Freight Systems is organized into three divisions: Air Cargo provides air cargo services, Logistics Services operates distribution centers and provides truck cargo services, and Forwarders provides international freight forwarding services (see Exhibit 15.6). Freight forwarders typically buy space on planes from international air cargo companies. This is analogous to a charter company that books seats on passenger planes and resells them to passengers. In many cases, freight forwarders hire trucking companies to transport the cargo from the plane to the domestic destination.

Management believes that the three divisions integrate well and are able to provide customers with one-stop transportation services. For example, a Forwarders branch in Singapore would receive cargo from a shipper, prepare the necessary documentation, and then ship the cargo on Air Cargo to a domestic Forwarders station. The domestic Forwarders station would ensure that the cargo passes through customs and would ship it to the final destination with Logistics Services as in Exhibit 15.6.

Management evaluates each division separately and rewards divisional managers based on profit and return on investment (ROI). Responsibility and decision-making authority are decentralized. Similarly, each division has a sales and marketing organization. Divisional salespeople report to the vice president of Operations for Custom Freight Systems. See Exhibit 15.7. Custom Freight Systems believes that it successfully motivates divisional managers by paying bonuses for high divisional profits.

Recently, the Logistics division needed to prepare a bid for a customer. The customer had freight to import from an overseas supplier and wanted Logistics to submit a bid for a distribution package that included supplying air freight, receiving the freight and providing customs clearance services at the airport, warehousing, and then distributing packages to customers.

Because this was a contract for international shipping, Logistics needed to contact different freight forwarders for shipping quotes. Logistics requested quotes from Forwarders and United Systems, a competing freight forwarder. Divisions of Custom Freight Systems are free to use the most appropriate and cost-effective suppliers.

Logistics received bids of $210 per hundred pounds from Forwarders and $185 per hundred pounds from United Systems. Forwarders specified in its bid that it will use Air Cargo, a division of Custom Freight Systems. Forwarders's variable costs were $175 per hundred pounds, which included the cost of subcontracting air transportation. Air Cargo, which was experiencing a period of excess capacity, quoted Forwarders the market rate of $155. Typically, Air Cargo's variable costs are 60 percent of the market rate.

The price difference between the two different bids alarmed Susan Burns, a contract manager at Logistics. She knows this is a competitive business and is concerned because the difference between the high and low bids was at least $1 million (current projections for the contract estimated 4,160,000 pounds during the first year). Susan contacted Greg Berman, the manager of Forwarders, and discussed the quote. "Don't you think full markup is unwarranted due to the fact that you and the airlines have so much excess capacity " she asked.

Susan soon realized that Greg was not going to drop the price quote. "You know how small the margins in this business are. Why should I cut my margins even smaller just to make you look good " he asked.

Susan went to Bennie Espinosa, vice president of Operations for Custom Freight Systems and chairperson for the corporate strategy committee. "That does sound strange," he said. "I need to examine the overall cost structure and talk to Greg. I'll get back to you by noon Monday."

Required

a. Which bid should the Logistics division accept: the internal bid from the Forwarders division or the external bid from United Systems

b. What should be the transfer price on this transaction

c. What should Bennie Espinosa do

d. Do the reward systems for divisional managers support the best interests of both the Forwarders division and Custom Freight Systems Give examples that support your conclusion.

Prepared by Thomas B. Rumzie under the direction of Michael W. Maher. © Copyright Michael W. Maher, 2006.

"We can't drop our prices below $210 per hundred pounds," exclaimed Greg Berman, manager of Forwarders, a division of Custom Freight Systems. "Our margins are already razor thin. Our costs just won't allow us to go any lower. Corporate rewards our division based on our profitability and I won't lower my prices below $210."

Custom Freight Systems is organized into three divisions: Air Cargo provides air cargo services, Logistics Services operates distribution centers and provides truck cargo services, and Forwarders provides international freight forwarding services (see Exhibit 15.6). Freight forwarders typically buy space on planes from international air cargo companies. This is analogous to a charter company that books seats on passenger planes and resells them to passengers. In many cases, freight forwarders hire trucking companies to transport the cargo from the plane to the domestic destination.

Management believes that the three divisions integrate well and are able to provide customers with one-stop transportation services. For example, a Forwarders branch in Singapore would receive cargo from a shipper, prepare the necessary documentation, and then ship the cargo on Air Cargo to a domestic Forwarders station. The domestic Forwarders station would ensure that the cargo passes through customs and would ship it to the final destination with Logistics Services as in Exhibit 15.6.

Management evaluates each division separately and rewards divisional managers based on profit and return on investment (ROI). Responsibility and decision-making authority are decentralized. Similarly, each division has a sales and marketing organization. Divisional salespeople report to the vice president of Operations for Custom Freight Systems. See Exhibit 15.7. Custom Freight Systems believes that it successfully motivates divisional managers by paying bonuses for high divisional profits.

Recently, the Logistics division needed to prepare a bid for a customer. The customer had freight to import from an overseas supplier and wanted Logistics to submit a bid for a distribution package that included supplying air freight, receiving the freight and providing customs clearance services at the airport, warehousing, and then distributing packages to customers.

Because this was a contract for international shipping, Logistics needed to contact different freight forwarders for shipping quotes. Logistics requested quotes from Forwarders and United Systems, a competing freight forwarder. Divisions of Custom Freight Systems are free to use the most appropriate and cost-effective suppliers.

Logistics received bids of $210 per hundred pounds from Forwarders and $185 per hundred pounds from United Systems. Forwarders specified in its bid that it will use Air Cargo, a division of Custom Freight Systems. Forwarders's variable costs were $175 per hundred pounds, which included the cost of subcontracting air transportation. Air Cargo, which was experiencing a period of excess capacity, quoted Forwarders the market rate of $155. Typically, Air Cargo's variable costs are 60 percent of the market rate.

The price difference between the two different bids alarmed Susan Burns, a contract manager at Logistics. She knows this is a competitive business and is concerned because the difference between the high and low bids was at least $1 million (current projections for the contract estimated 4,160,000 pounds during the first year). Susan contacted Greg Berman, the manager of Forwarders, and discussed the quote. "Don't you think full markup is unwarranted due to the fact that you and the airlines have so much excess capacity " she asked.

Susan soon realized that Greg was not going to drop the price quote. "You know how small the margins in this business are. Why should I cut my margins even smaller just to make you look good " he asked.

Susan went to Bennie Espinosa, vice president of Operations for Custom Freight Systems and chairperson for the corporate strategy committee. "That does sound strange," he said. "I need to examine the overall cost structure and talk to Greg. I'll get back to you by noon Monday."

Required

a. Which bid should the Logistics division accept: the internal bid from the Forwarders division or the external bid from United Systems

b. What should be the transfer price on this transaction

c. What should Bennie Espinosa do

d. Do the reward systems for divisional managers support the best interests of both the Forwarders division and Custom Freight Systems Give examples that support your conclusion.

Prepared by Thomas B. Rumzie under the direction of Michael W. Maher. © Copyright Michael W. Maher, 2006.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

15

Many firms prefer to use market prices for transfer prices. Why would they have this preference

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

16

Evaluate Transfer Pricing System

Seattle Transit Ltd. operates a local mass transit system. The transit authority is a state governmental agency. It has an agreement with the state government to provide rides to senior citizens for 25 cents per trip. The government will reimburse Seattle Transit for the "cost" of each trip taken by a senior citizen.

The regular fare is $2 per trip. After analyzing its costs, Seattle Transit figured that with its operating deficit, the full cost of each ride on the transit system is $5. Routes, capacity, and operating costs are unaffected by the number of senior citizens on any route.

Required

a. What alternative prices could be used to determine the governmental reimbursement to Seattle Transit

b. Which price would Seattle Transit prefer Why

c. Which price would the state government prefer Why

d. If Seattle Transit provides an average of 200,000 trips for senior citizens in a given month, what is the monthly value of the difference between the prices in (b) and (c)

Seattle Transit Ltd. operates a local mass transit system. The transit authority is a state governmental agency. It has an agreement with the state government to provide rides to senior citizens for 25 cents per trip. The government will reimburse Seattle Transit for the "cost" of each trip taken by a senior citizen.

The regular fare is $2 per trip. After analyzing its costs, Seattle Transit figured that with its operating deficit, the full cost of each ride on the transit system is $5. Routes, capacity, and operating costs are unaffected by the number of senior citizens on any route.

Required

a. What alternative prices could be used to determine the governmental reimbursement to Seattle Transit

b. Which price would Seattle Transit prefer Why

c. Which price would the state government prefer Why

d. If Seattle Transit provides an average of 200,000 trips for senior citizens in a given month, what is the monthly value of the difference between the prices in (b) and (c)

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

17

Custom Freight Systems (B): Transfer Pricing

Assume that all of the information is the same as in Integrative Case 15-34, but instead of receiving only one outside bid, Logistics receives two. The new bid is from World Services for $195 per hundred pounds. World has offered to use Air Cargo for transporting packages. Air Cargo will charge World $155 per hundred pounds. The bids from Forwarders and United Systems remain the same as in Integrative Case 15-34, $210 and $185, respectively.

Required

Which bid should Logistics Division take Why

Prepared by Thomas B. Rumzie under the direction of Michael W. Maher. © Copyright Michael W. Maher, 2006.

Assume that all of the information is the same as in Integrative Case 15-34, but instead of receiving only one outside bid, Logistics receives two. The new bid is from World Services for $195 per hundred pounds. World has offered to use Air Cargo for transporting packages. Air Cargo will charge World $155 per hundred pounds. The bids from Forwarders and United Systems remain the same as in Integrative Case 15-34, $210 and $185, respectively.

Required

Which bid should Logistics Division take Why

Prepared by Thomas B. Rumzie under the direction of Michael W. Maher. © Copyright Michael W. Maher, 2006.

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

18

What are the limitations of market-based transfer prices What are the limitations of cost- based transfer prices

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

19

Evaluate Transfer Pricing System

Carmen Seville and Don Turco jointly own Bright Green Temp Services (BGTS). Carmen owns 60 percent and Don owns 40 percent. The company provides temporary clerical services at a rate of $40 per hour. During the past year, its clients used 14,000 hours of temporary services.

Big City Developers purchased 2,800 hours of temporary services from BGTS last year. Carmen has a 20 percent interest in Big City Developers, and Don has a 60 percent interest in it. At the end of the year, Don suggested that BGTS give Big City Developers a 10 percent reduction in the hourly rate charged next year in recognition of its large purchases and desirability as a client.

Required

Assuming that Big City Developers purchases the same number of hours and that all other costs and activities remain the same in the coming year, what effect would the price reduction have on BGTS's operating profits that accrue to Carmen and to Don for the coming year

Carmen Seville and Don Turco jointly own Bright Green Temp Services (BGTS). Carmen owns 60 percent and Don owns 40 percent. The company provides temporary clerical services at a rate of $40 per hour. During the past year, its clients used 14,000 hours of temporary services.

Big City Developers purchased 2,800 hours of temporary services from BGTS last year. Carmen has a 20 percent interest in Big City Developers, and Don has a 60 percent interest in it. At the end of the year, Don suggested that BGTS give Big City Developers a 10 percent reduction in the hourly rate charged next year in recognition of its large purchases and desirability as a client.

Required

Assuming that Big City Developers purchases the same number of hours and that all other costs and activities remain the same in the coming year, what effect would the price reduction have on BGTS's operating profits that accrue to Carmen and to Don for the coming year

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

20

When would you advise a firm to use direct intervention to set transfer prices What are the disadvantages of such a practice

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

21

International Transfer Prices: Ethical Issues

Trans Atlantic Metals has two operating divisions. Its forging operation in Finland forges raw metal, cuts it, and then ships it to the United States where the company's Gear Division uses the metal to produce finished gears. Operating expenses amount to $5 million in Finland and $15 million in the United States exclusive of the costs of any goods transferred from Finland. Revenues in the United States are $37.5 million.

If the metal were purchased from one of the company's U.S. forging divisions, the costs would be $7.5 million. However, if it had been purchased from an independent Finnish supplier, the cost would be $10 million. The marginal income tax rate is 60 percent in Finland and 40 percent in the United States.

Required

a. What is the company's total tax liability to both jurisdictions for each of the two alternative transfer pricing scenarios ($7.5 million and $10 million)

b. Is it ethical to choose the transfer price based on the impact on taxes

Trans Atlantic Metals has two operating divisions. Its forging operation in Finland forges raw metal, cuts it, and then ships it to the United States where the company's Gear Division uses the metal to produce finished gears. Operating expenses amount to $5 million in Finland and $15 million in the United States exclusive of the costs of any goods transferred from Finland. Revenues in the United States are $37.5 million.

If the metal were purchased from one of the company's U.S. forging divisions, the costs would be $7.5 million. However, if it had been purchased from an independent Finnish supplier, the cost would be $10 million. The marginal income tax rate is 60 percent in Finland and 40 percent in the United States.

Required

a. What is the company's total tax liability to both jurisdictions for each of the two alternative transfer pricing scenarios ($7.5 million and $10 million)

b. Is it ethical to choose the transfer price based on the impact on taxes

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

22

When would you advise a firm to use prices other than market prices for interdivisional transfers

Unlock Deck

Unlock for access to all 35 flashcards in this deck.

Unlock Deck

k this deck

23

Segment Reporting

Leapin' Larry's Pre-Owned Cars has two divisions, Operations and Financing. Operations is responsible for selling Larry's inventory as quickly as possible and purchasing cars for future sale.

Financing Division takes loan applications and packages loans into pools and sells them in the financial markets. It also services the loans. Both divisions meet the requirements for segment disclosures under accounting rules.

Operations Division had $34 million in sales last year. Costs, other than those charged by Financing Division, totaled $26 million. Financing Division earned revenues of $8 million from servicing mortgages and incurred outside costs of $7 million. In addition, Financing charged Operations $4 million for loan-related fees. Operations's manager complained to Larry that Financing was charging twice the commercial rate for loan-related fees and that Operations would be better off sending its buyers to an outside lender.

Financing's manager replied that although commercial rates could be lower, servicing Larry's loans is more difficult, thereby justifying the higher fees.

Required