Deck 6: Budgets and Budgeting

Full screen (f)

Question

Question

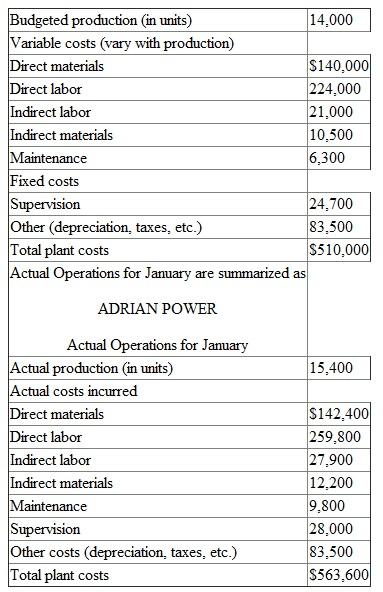

Adrian Power manufactures small power supplies for car stereos. The company uses flexible budgeting techniques to deal with the seasonal and cyclical nature of the business. The accounting department provided the accompanying data on budgeted manufacturing costs for the month of January:

ADRIAN POWER

Planned Level of Production for January

Required:

Required:

a. Prepare a report comparing the actual operating results with the flexible budget at actual production.

b. Write a short memo analyzing the report prepared in (a). What likely managerial implications do you draw from this report What are the numbers telling you

ADRIAN POWER

Planned Level of Production for January

Required: a. Prepare a report comparing the actual operating results with the flexible budget at actual production.

b. Write a short memo analyzing the report prepared in (a). What likely managerial implications do you draw from this report What are the numbers telling you

Question

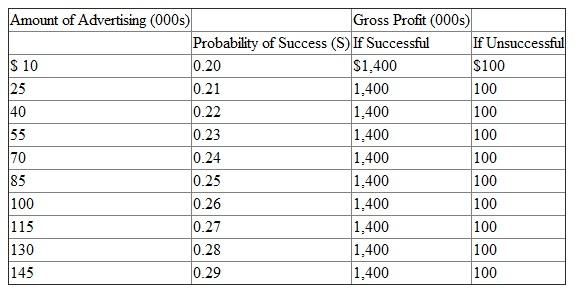

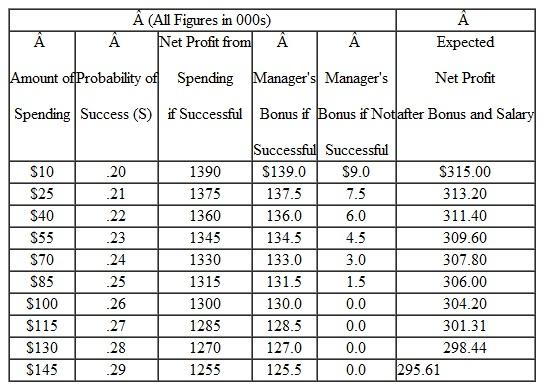

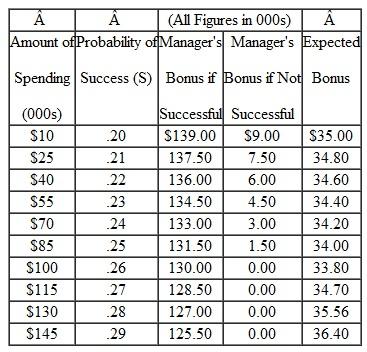

James, Inc., a large mail-order catalog firm, is thinking of expanding into Canada. The Buffalo district office would manage the expansion and must decide how much to spend on the advertising campaign. The expansion project will be either successful (S) or unsuccessful (U). The probability of success depends on the amount spent on the advertising campaign. If the project is successful, the gross profit (before advertising) is $1.4 million. If the project is unsuccessful, the gross profit (before advertising) is $100,000. The accompanying table lists how the probability of success varies with the amount of spending on the Canadian venture.

James, Inc., is a publicly traded firm and its senior managers and shareholders wish to maximize expected net cash flows from this venture. The Buffalo manager receives a bonus of 10 percent of the net profit (gross profit less advertising).

James, Inc., is a publicly traded firm and its senior managers and shareholders wish to maximize expected net cash flows from this venture. The Buffalo manager receives a bonus of 10 percent of the net profit (gross profit less advertising).

The bonus is paid only if the firm has gross profit net of advertising. If gross profit less advertising is negative, no bonus is paid. The manager wants to maximize her bonus and has private knowledge of how the probability of success varies with advertising.

Required:

a. What advertising level would senior managers choose if they had access to the Buffalo manager's specialized knowledge

b. What advertising level will the Buffalo manager select, knowing that senior managers do not have the specialized knowledge of the payoffs

c. If the advertising levels in (a) and (b) differ, explain why.

James, Inc., is a publicly traded firm and its senior managers and shareholders wish to maximize expected net cash flows from this venture. The Buffalo manager receives a bonus of 10 percent of the net profit (gross profit less advertising).The bonus is paid only if the firm has gross profit net of advertising. If gross profit less advertising is negative, no bonus is paid. The manager wants to maximize her bonus and has private knowledge of how the probability of success varies with advertising.

Required:

a. What advertising level would senior managers choose if they had access to the Buffalo manager's specialized knowledge

b. What advertising level will the Buffalo manager select, knowing that senior managers do not have the specialized knowledge of the payoffs

c. If the advertising levels in (a) and (b) differ, explain why.

Question

LaserFlo

Marti Meyers, vice president of marketing for LaserFlo, was concerned as she reviewed the costs for the AP2000 laser printer she was planning to launch next month. The AP2000 is a new commercial printer that LaserFlo designed for medium-sized direct mail businesses. The basic system price was set at $74,500; the unit manufacturing cost of the AP2000 is $46,295, and selling and administrative cost is budgeted at 33 percent of the selling price. The maintenance price she planned to announce was $85 per hour of LaserFlo technician time. While the $74,500 base price is competitive, $85 per hour is a bit higher than the industry average of $82 per hour. However, Meyers believed she could live with the $85 price. She is concerned because she has just received a memo from the Field Service organization stating that it was increasing its projected hourly charge for service from $35.05 to $38.25.

The $85 price Meyers was prepared to charge for service was based on last year's $35.05 service cost. She thought that using last year's cost was conservative since Field Service had been downsizing and she expected the cost to go down, not up. The $35.05 cost still did not yield the 60 percent margin on service that was the standard for other LaserFlo printers, but Meyers had difficulty justifying a higher maintenance price given the competition. With a service cost of $38.25, Meyers knows she cannot raise the price to the customer enough to cover the higher costs without significantly reducing sales. Given the higher cost of the LaserFlo field technicians and the prices charged for maintenance by the competition, she will not be able to make the profit target in her plan.

Background

LaserFlo manufactures, sells, and services its printers throughout the United States using direct sales and service forces. It has been in business for 22 years and is the largest of three manufacturers of high-speed laser printers for direct mailers in the United States. LaserFlo maintains its market leadership by innovating new technology. Direct mail marketing firms produce customized letters of solicitation for bank credit cards, real estate offers, life insurance, colleges and universities, and magazine giveaway contests. Personalized letters are printed on high-speed printers attached to computers that have the mailing information. The printers print either the entire letter or the address and salutation ("Dear Mrs. Jeremy McConnell") on preprinted forms. Direct mail firms have computer systems to manage their address lists and mailings, and LaserFlo printers are attached to the client's computer system.

Direct mail laser printers process very high volumes; a single printer commonly addresses 75,000 letters a day. Hence, LaserFlo printers for direct mail marketers differ from general-purpose high-speed printers. In particular, they have specialized paper transfer mechanisms to handle the often custom, heavy paper; varying paper sizes; and high-speed paper flows. With such high paper flow rates, these printers require regular adjustments to prevent paper jams and misalignments. LaserFlo's nationwide field service organization of about 500 employees maintains these printers.

The standard LaserFlo sales contract contains two parts: the purchase price of the equipment and a maintenance contract for the equipment. All LaserFlo printers are maintained by LaserFlo field service personnel, and the maintenance contract specifies the price per hour charged for routine and unscheduled maintenance. Most of LaserFlo's profits come from printer maintenance. Printers have about a 5 to 10 percent markup over manufacturing and selling cost, but the markup on maintenance has historically averaged about 60 percent.

LaserFlo printers have a substantial amount of built-in intelligence to control the printing and for self-diagnostics. Each printer has its own microcomputer with memory to hold the data to be printed. These internal microcomputers also keep track of printing statistics and can alert the operator to impending problems (low toner, paper alignment problems, form breaks). When customers change their operating system or computer, this often necessitates a LaserFlo service call to ensure that the new system is compatible with the printer. The standard service contract calls for normal maintenance after a fixed number of impressions (pages); for example, the AP2000 requires service after every 500,000 pages are printed. Its microcomputer is programmed to call LaserFlo's central computer to schedule maintenance whenever the machine has produced 375,000 pages since the last servicing.

LaserFlo organization

LaserFlo is organized into engineering, manufacturing, marketing, field service, and administration divisions. Engineering designs the new printers and provides consulting services to marketing and field service regarding system installation and maintenance. Engineering is evaluated as a cost center. Manufacturing produces the printers, which are assembled from purchased parts and subassemblies. LaserFlo's comparative advantage is quality control and design. Manufacturing also provides parts for field service maintenance. Manufacturing is treated as a cost center and evaluated based on meeting cost targets and delivery schedules. Manufacturing's unit cost is charged to marketing for each printer sold.

Marketing, a profit center, is responsible for designing the marketing campaigns, pricing the printers, and managing the field sales staff. LaserFlo sells six different printers; each has a separate marketing program manager. The six marketing program managers report to Marti Meyers, vice president of marketing, who also manages field sales.

Field sales is organized around four regional managers responsible for the sales offices in their region. Each of the 27 sales offices has a direct sales force that contacts potential customers and sells the six programs. Salespeople receive a salary and a commission depending on the printer and options sold. The salesperson continues to receive commissions from ongoing revenues paid by the account for service. Since ongoing maintenance forms a significant amount of a printer's total profit, the salesperson has an incentive to keep the customer with LaserFlo.

Field service contains the technical people who install and maintain the printers. Headed by Phil Hansen, vice president of field service, field service usually shares office space with field sales in the cities where they operate. Field service is a cost center, and its direct and indirect costs are charged to programs when the printers are serviced. The price charged is based on the budgeted rate set at the beginning of the year. Any difference between the actual amount charged to the programs and the total cost incurred by the field service group is charged to a corporate overhead account, not to the marketing programs.

Administration manages human resources, finance, accounting, and field office leases. It handles customer billing and collections, payroll, and negotiating office space for the field sales and field service people. Administration is evaluated as a cost center. While local office space is managed by administration, the cost of the office space is allocated to the field sales and service groups and included in their budgets and monthly operating statements.

Service contracts

Each LaserFlo printer sold requires a service contract. The AP2000's service contract calls for normal maintenance every 500,000 pages at a price of $0.51 per 1,000 pages. Normal maintenance requires three hours. The typical AP2000 prints 12 million pages per year. Besides normal maintenance (sometimes called preventive maintenance ), unscheduled maintenance occurs due to improper operator setups, paper jams, system upgrades, and harsh usage of the equipment. Past statistical studies have shown that each normal maintenance hour generates 0.50 unscheduled maintenance hours. Unscheduled maintenance is billed to the customer at the service contract rate of $85 per hour.

When maintenance is performed on a particular machine, the service revenues less field service costs are credited to the marketing manager for that program. All the programs' actual service profits are compared with the plan; they form part of Meyers's performance evaluation. The field salesperson receives a commission based on the total service revenue generated by the account. In evaluating each new printer program, LaserFlo uses the following procedure. Profits from service are expected to create an annuity that will last for five years at 18 percent interest. To evaluate a proposed new printer, the one-year maintenance profits are multiplied by 3.127 to reflect the present value of the future service profits each printer is expected to generate over its life (about five years).

Parts

Any parts used during service are charged directly to the customer and do not flow through field service budgets or operating statements. LaserFlo purchases most of the printers' parts from outside suppliers, and the customer pays only a token markup. Marketing does not receive any revenue, nor is it charged any costs when customers use parts in the service process. The reason for not charging customers a larger markup on parts stems from an antitrust case filed against LaserFlo and other printer companies six years ago. A third-party service company, Servwell, sued the printer manufacturers for restraint of trade, claiming they prevented Servwell from maintaining the printers by only selling replacement parts at very high prices. To prevent other such claims, LaserFlo sells parts at a small markup over costs. Yet Servwell and other third-party service firms have never been able to penetrate LaserFlo's service markets because laser printing technology changes rapidly, and an outside company cannot keep a work force trained to fix the latest products. Besides, each printer usually has at least two engineering modifications each year to fix problems or upgrade the printer or its microcomputer hardware and/or software. An outside service company cannot learn of these changes and provide the same level of service as LaserFlo.

Recent changes in field service

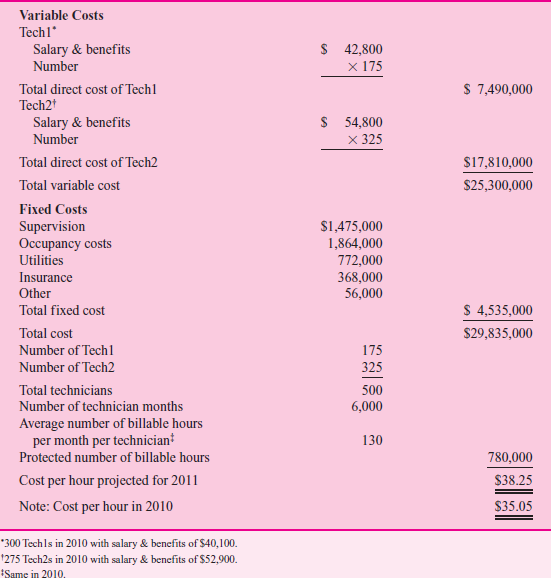

LaserFlo field service had two types of technicians: Tech1 and Tech2. Both were trained to repair electromechanical problems, but Tech2s had more training in electronics and computers to work on the latest, most sophisticated printers.

Field service had been trying to reduce the size of the service force the last few years through voluntary retirements and attrition. As the printers became more sophisticated, they became more reliable. The newer systems had self-diagnosing software that allowed a service technician to call up a customer's printer and run a diagnostic program. Often the problem was solved over the phone line by having a LaserFlo technician make the repair in the software. If a mechanical problem was detected, the technician dispatched a repair person (often a Tech1) with the right part. Also, past customers replaced their older printers with newer ones that required less maintenance. The result was excess capacity in the field staff.

The voluntary retirements over the past few years did not produce the reductions necessary to eliminate the excess capacity. In 2010, field service went through a very large involuntary reduction of its workforce. Through attrition, early retirements, and terminations, LaserFlo reduced the number of technicians by 75, down to 500 budgeted for 2011. The company simultaneously improved the skill level of its remaining field force substantially.

AP2000 sales plan for 2011

Marti Meyers's 2011 sales plan for the AP2000 calls for 120 placements this year and a program profit projection of about $2.5 million based on capitalizing the service income using the 3.127 annuity factor. If she were to raise the service price much above $0.51 per 1,000 pages, LaserFlo would lose sales, which are already ambitious. She called Phil Hansen and raised her concerns with him.

"Phil," she began, "explain to me how you downsized your field personnel, cut some office locations, consolidated inventories, and reduced other fixed costs, yet the price I'm being charged for service increased from $35.05 per hour to $38.25. I thought the whole purpose of the field service reorganization was to streamline and make us more cost competitive. You know that our service costs were out of line with our competitors'. We were planning to charge $85 an hour for the AP2000 service contract. Even at $85 per hour, I would be violating the corporate policy of maintaining a 60 percent markup on service. If I were to follow the 60 percent rule, I would have to charge $87.63 per hour if you had kept your cost to me at $35.05. But with your cost of $38.25 and my price at $85, the margin falls to 55 percent. I already had to get special permission to lower the margin to 59 percent with $35.05."

Hansen replied, "Well, there are a number of issues that you've just raised. Let me respond to a few over the phone now and suggest we meet to discuss this more fully next week when I'm back in the office. In the meantime, I'll send you our projected budget for next year that derived the $38.25 rate. Regarding the key question as to how our hourly rate could go up after downsizing, it's really quite simple. We had a lot of idle time being built into the numbers. People just pretended to be busy. Had we not downsized, the hourly charge would have gone up even more than it did. For example, on the AP2000 that you mentioned, we would have used 3.25 hours per normal servicing had we kept our labor force mix of Tech1s and 2s the same as in 2010. Had we not downsized, our fixed costs in 2011 would have remained the same as they were in 2010, and our variable costs for Tech1s and 2s would have increased to the 2011 amounts because of wage increases and inflation. Let me get you our numbers so you can see for yourself how much progress we've been making."

That afternoon, Meyers received a fax from Hansen's office (see Table 1). In trying to decide how to proceed, Meyers would like you to address the following questions:

a. Calculate the projected five-year profits of an AP2000 using first the $35.05 and then the $38.25 service cost.

T ABLE 1 Field Service Projected Hourly Rate for 2011

b. Why did the field service hourly cost increase? What caused the hourly rate to go from $35.05 to $38.25?

c. Did the reorganization of field service reduce the cost of servicing the AP2000? Calculate what the total annual service cost of the AP2000 would have been had the reorganization not occurred.

d. Identify the various options Meyers has for dealing with the service cost increase and analyze them.

e. Why does LaserFlo make more money on servicing printers than selling them? Does such a policy make sense?

Marti Meyers, vice president of marketing for LaserFlo, was concerned as she reviewed the costs for the AP2000 laser printer she was planning to launch next month. The AP2000 is a new commercial printer that LaserFlo designed for medium-sized direct mail businesses. The basic system price was set at $74,500; the unit manufacturing cost of the AP2000 is $46,295, and selling and administrative cost is budgeted at 33 percent of the selling price. The maintenance price she planned to announce was $85 per hour of LaserFlo technician time. While the $74,500 base price is competitive, $85 per hour is a bit higher than the industry average of $82 per hour. However, Meyers believed she could live with the $85 price. She is concerned because she has just received a memo from the Field Service organization stating that it was increasing its projected hourly charge for service from $35.05 to $38.25.

The $85 price Meyers was prepared to charge for service was based on last year's $35.05 service cost. She thought that using last year's cost was conservative since Field Service had been downsizing and she expected the cost to go down, not up. The $35.05 cost still did not yield the 60 percent margin on service that was the standard for other LaserFlo printers, but Meyers had difficulty justifying a higher maintenance price given the competition. With a service cost of $38.25, Meyers knows she cannot raise the price to the customer enough to cover the higher costs without significantly reducing sales. Given the higher cost of the LaserFlo field technicians and the prices charged for maintenance by the competition, she will not be able to make the profit target in her plan.

Background

LaserFlo manufactures, sells, and services its printers throughout the United States using direct sales and service forces. It has been in business for 22 years and is the largest of three manufacturers of high-speed laser printers for direct mailers in the United States. LaserFlo maintains its market leadership by innovating new technology. Direct mail marketing firms produce customized letters of solicitation for bank credit cards, real estate offers, life insurance, colleges and universities, and magazine giveaway contests. Personalized letters are printed on high-speed printers attached to computers that have the mailing information. The printers print either the entire letter or the address and salutation ("Dear Mrs. Jeremy McConnell") on preprinted forms. Direct mail firms have computer systems to manage their address lists and mailings, and LaserFlo printers are attached to the client's computer system.

Direct mail laser printers process very high volumes; a single printer commonly addresses 75,000 letters a day. Hence, LaserFlo printers for direct mail marketers differ from general-purpose high-speed printers. In particular, they have specialized paper transfer mechanisms to handle the often custom, heavy paper; varying paper sizes; and high-speed paper flows. With such high paper flow rates, these printers require regular adjustments to prevent paper jams and misalignments. LaserFlo's nationwide field service organization of about 500 employees maintains these printers.

The standard LaserFlo sales contract contains two parts: the purchase price of the equipment and a maintenance contract for the equipment. All LaserFlo printers are maintained by LaserFlo field service personnel, and the maintenance contract specifies the price per hour charged for routine and unscheduled maintenance. Most of LaserFlo's profits come from printer maintenance. Printers have about a 5 to 10 percent markup over manufacturing and selling cost, but the markup on maintenance has historically averaged about 60 percent.

LaserFlo printers have a substantial amount of built-in intelligence to control the printing and for self-diagnostics. Each printer has its own microcomputer with memory to hold the data to be printed. These internal microcomputers also keep track of printing statistics and can alert the operator to impending problems (low toner, paper alignment problems, form breaks). When customers change their operating system or computer, this often necessitates a LaserFlo service call to ensure that the new system is compatible with the printer. The standard service contract calls for normal maintenance after a fixed number of impressions (pages); for example, the AP2000 requires service after every 500,000 pages are printed. Its microcomputer is programmed to call LaserFlo's central computer to schedule maintenance whenever the machine has produced 375,000 pages since the last servicing.

LaserFlo organization

LaserFlo is organized into engineering, manufacturing, marketing, field service, and administration divisions. Engineering designs the new printers and provides consulting services to marketing and field service regarding system installation and maintenance. Engineering is evaluated as a cost center. Manufacturing produces the printers, which are assembled from purchased parts and subassemblies. LaserFlo's comparative advantage is quality control and design. Manufacturing also provides parts for field service maintenance. Manufacturing is treated as a cost center and evaluated based on meeting cost targets and delivery schedules. Manufacturing's unit cost is charged to marketing for each printer sold.

Marketing, a profit center, is responsible for designing the marketing campaigns, pricing the printers, and managing the field sales staff. LaserFlo sells six different printers; each has a separate marketing program manager. The six marketing program managers report to Marti Meyers, vice president of marketing, who also manages field sales.

Field sales is organized around four regional managers responsible for the sales offices in their region. Each of the 27 sales offices has a direct sales force that contacts potential customers and sells the six programs. Salespeople receive a salary and a commission depending on the printer and options sold. The salesperson continues to receive commissions from ongoing revenues paid by the account for service. Since ongoing maintenance forms a significant amount of a printer's total profit, the salesperson has an incentive to keep the customer with LaserFlo.

Field service contains the technical people who install and maintain the printers. Headed by Phil Hansen, vice president of field service, field service usually shares office space with field sales in the cities where they operate. Field service is a cost center, and its direct and indirect costs are charged to programs when the printers are serviced. The price charged is based on the budgeted rate set at the beginning of the year. Any difference between the actual amount charged to the programs and the total cost incurred by the field service group is charged to a corporate overhead account, not to the marketing programs.

Administration manages human resources, finance, accounting, and field office leases. It handles customer billing and collections, payroll, and negotiating office space for the field sales and field service people. Administration is evaluated as a cost center. While local office space is managed by administration, the cost of the office space is allocated to the field sales and service groups and included in their budgets and monthly operating statements.

Service contracts

Each LaserFlo printer sold requires a service contract. The AP2000's service contract calls for normal maintenance every 500,000 pages at a price of $0.51 per 1,000 pages. Normal maintenance requires three hours. The typical AP2000 prints 12 million pages per year. Besides normal maintenance (sometimes called preventive maintenance ), unscheduled maintenance occurs due to improper operator setups, paper jams, system upgrades, and harsh usage of the equipment. Past statistical studies have shown that each normal maintenance hour generates 0.50 unscheduled maintenance hours. Unscheduled maintenance is billed to the customer at the service contract rate of $85 per hour.

When maintenance is performed on a particular machine, the service revenues less field service costs are credited to the marketing manager for that program. All the programs' actual service profits are compared with the plan; they form part of Meyers's performance evaluation. The field salesperson receives a commission based on the total service revenue generated by the account. In evaluating each new printer program, LaserFlo uses the following procedure. Profits from service are expected to create an annuity that will last for five years at 18 percent interest. To evaluate a proposed new printer, the one-year maintenance profits are multiplied by 3.127 to reflect the present value of the future service profits each printer is expected to generate over its life (about five years).

Parts

Any parts used during service are charged directly to the customer and do not flow through field service budgets or operating statements. LaserFlo purchases most of the printers' parts from outside suppliers, and the customer pays only a token markup. Marketing does not receive any revenue, nor is it charged any costs when customers use parts in the service process. The reason for not charging customers a larger markup on parts stems from an antitrust case filed against LaserFlo and other printer companies six years ago. A third-party service company, Servwell, sued the printer manufacturers for restraint of trade, claiming they prevented Servwell from maintaining the printers by only selling replacement parts at very high prices. To prevent other such claims, LaserFlo sells parts at a small markup over costs. Yet Servwell and other third-party service firms have never been able to penetrate LaserFlo's service markets because laser printing technology changes rapidly, and an outside company cannot keep a work force trained to fix the latest products. Besides, each printer usually has at least two engineering modifications each year to fix problems or upgrade the printer or its microcomputer hardware and/or software. An outside service company cannot learn of these changes and provide the same level of service as LaserFlo.

Recent changes in field service

LaserFlo field service had two types of technicians: Tech1 and Tech2. Both were trained to repair electromechanical problems, but Tech2s had more training in electronics and computers to work on the latest, most sophisticated printers.

Field service had been trying to reduce the size of the service force the last few years through voluntary retirements and attrition. As the printers became more sophisticated, they became more reliable. The newer systems had self-diagnosing software that allowed a service technician to call up a customer's printer and run a diagnostic program. Often the problem was solved over the phone line by having a LaserFlo technician make the repair in the software. If a mechanical problem was detected, the technician dispatched a repair person (often a Tech1) with the right part. Also, past customers replaced their older printers with newer ones that required less maintenance. The result was excess capacity in the field staff.

The voluntary retirements over the past few years did not produce the reductions necessary to eliminate the excess capacity. In 2010, field service went through a very large involuntary reduction of its workforce. Through attrition, early retirements, and terminations, LaserFlo reduced the number of technicians by 75, down to 500 budgeted for 2011. The company simultaneously improved the skill level of its remaining field force substantially.

AP2000 sales plan for 2011

Marti Meyers's 2011 sales plan for the AP2000 calls for 120 placements this year and a program profit projection of about $2.5 million based on capitalizing the service income using the 3.127 annuity factor. If she were to raise the service price much above $0.51 per 1,000 pages, LaserFlo would lose sales, which are already ambitious. She called Phil Hansen and raised her concerns with him.

"Phil," she began, "explain to me how you downsized your field personnel, cut some office locations, consolidated inventories, and reduced other fixed costs, yet the price I'm being charged for service increased from $35.05 per hour to $38.25. I thought the whole purpose of the field service reorganization was to streamline and make us more cost competitive. You know that our service costs were out of line with our competitors'. We were planning to charge $85 an hour for the AP2000 service contract. Even at $85 per hour, I would be violating the corporate policy of maintaining a 60 percent markup on service. If I were to follow the 60 percent rule, I would have to charge $87.63 per hour if you had kept your cost to me at $35.05. But with your cost of $38.25 and my price at $85, the margin falls to 55 percent. I already had to get special permission to lower the margin to 59 percent with $35.05."

Hansen replied, "Well, there are a number of issues that you've just raised. Let me respond to a few over the phone now and suggest we meet to discuss this more fully next week when I'm back in the office. In the meantime, I'll send you our projected budget for next year that derived the $38.25 rate. Regarding the key question as to how our hourly rate could go up after downsizing, it's really quite simple. We had a lot of idle time being built into the numbers. People just pretended to be busy. Had we not downsized, the hourly charge would have gone up even more than it did. For example, on the AP2000 that you mentioned, we would have used 3.25 hours per normal servicing had we kept our labor force mix of Tech1s and 2s the same as in 2010. Had we not downsized, our fixed costs in 2011 would have remained the same as they were in 2010, and our variable costs for Tech1s and 2s would have increased to the 2011 amounts because of wage increases and inflation. Let me get you our numbers so you can see for yourself how much progress we've been making."

That afternoon, Meyers received a fax from Hansen's office (see Table 1). In trying to decide how to proceed, Meyers would like you to address the following questions:

a. Calculate the projected five-year profits of an AP2000 using first the $35.05 and then the $38.25 service cost.

T ABLE 1 Field Service Projected Hourly Rate for 2011

b. Why did the field service hourly cost increase? What caused the hourly rate to go from $35.05 to $38.25?

c. Did the reorganization of field service reduce the cost of servicing the AP2000? Calculate what the total annual service cost of the AP2000 would have been had the reorganization not occurred.

d. Identify the various options Meyers has for dealing with the service cost increase and analyze them.

e. Why does LaserFlo make more money on servicing printers than selling them? Does such a policy make sense?

Question

Panarude Airfreight is an international air freight hauler with more than 45 jet aircraft operating in the United States and the Pacific Rim. The firm is headquartered in Melbourne, Australia, and is organized into five geographic areas: Australia, Japan, Taiwan, Korea, and the United States. Supporting these areas are several centralized corporate function services (cost centers): human resources, data processing, fleet acquisition and maintenance, and telecommunications. Each responsibility center has a budget, negotiated at the beginning of the year with the vice president of finance. Funds unspent at the end of the year do not carry over to the next fiscal year. The firm is on a January-to-December fiscal year.

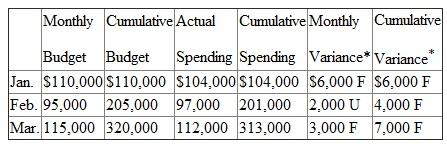

After reviewing the month-to-month variances, Panarude senior management became concerned about the increased spending occurring in the last three months of each fiscal year. In particular, in the first nine months of the year, expenditure accounts typically show favorable variances (actual spending is less than budget), but in the last three months, unfavorable variances are the norm. In an attempt to smooth out these spending patterns, each responsibility center is reviewed at the end of each calendar quarter and any unspent funds can be deleted from the budget for the remainder of the year. The accompanying table shows the budget and actual spending in the telecommunications department for the first quarter of this year.

PANARUDE AIRFREIGHT Telecommunications Department: First Quarter Budget and Actual Spending (Australian Dollars)

At the end of the first quarter, telecommunications' total annual budget for this year can be reduced by $7,000, the total budget underrun in the first quarter. In addition, the remaining nine monthly budgets for telecommunications are reduced by $778 (or $7,000 9). If, at the end of

At the end of the first quarter, telecommunications' total annual budget for this year can be reduced by $7,000, the total budget underrun in the first quarter. In addition, the remaining nine monthly budgets for telecommunications are reduced by $778 (or $7,000 9). If, at the end of

the second quarter, telecommunications' budget shows an unfavorable variance of, say, $8,000 (after the original budget is reduced for the first-quarter underrun), management of telecommunications is held responsible for the entire $8,000 unfavorable variance. The first-quarter underrun is not restored. If the second-quarter budget variance is also favorable, the remaining six monthly budgets are each reduced further by one-sixth of the second-quarter favorable budget variance.

Required:

a. What behavior would this budgeting scheme engender in the responsibility center managers

b. Compare the advantages and disadvantages of the previous budget regime, where any end- of-year budget surpluses do not carry over to the next fiscal year, with the system of quarterly budget adjustments just described.

After reviewing the month-to-month variances, Panarude senior management became concerned about the increased spending occurring in the last three months of each fiscal year. In particular, in the first nine months of the year, expenditure accounts typically show favorable variances (actual spending is less than budget), but in the last three months, unfavorable variances are the norm. In an attempt to smooth out these spending patterns, each responsibility center is reviewed at the end of each calendar quarter and any unspent funds can be deleted from the budget for the remainder of the year. The accompanying table shows the budget and actual spending in the telecommunications department for the first quarter of this year.

PANARUDE AIRFREIGHT Telecommunications Department: First Quarter Budget and Actual Spending (Australian Dollars)

At the end of the first quarter, telecommunications' total annual budget for this year can be reduced by $7,000, the total budget underrun in the first quarter. In addition, the remaining nine monthly budgets for telecommunications are reduced by $778 (or $7,000 9). If, at the end ofthe second quarter, telecommunications' budget shows an unfavorable variance of, say, $8,000 (after the original budget is reduced for the first-quarter underrun), management of telecommunications is held responsible for the entire $8,000 unfavorable variance. The first-quarter underrun is not restored. If the second-quarter budget variance is also favorable, the remaining six monthly budgets are each reduced further by one-sixth of the second-quarter favorable budget variance.

Required:

a. What behavior would this budgeting scheme engender in the responsibility center managers

b. Compare the advantages and disadvantages of the previous budget regime, where any end- of-year budget surpluses do not carry over to the next fiscal year, with the system of quarterly budget adjustments just described.

Question

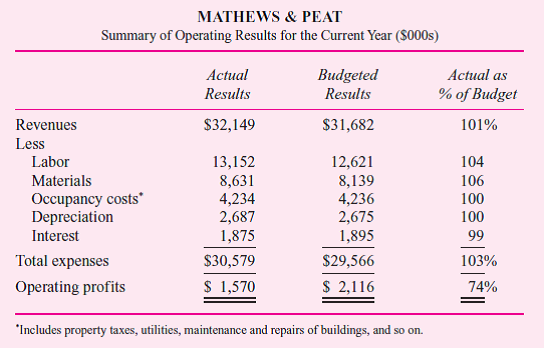

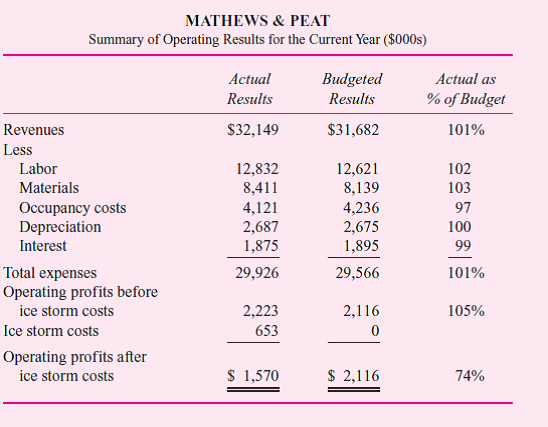

In March, a devastating ice storm struck Monroe County, New York, causing millions of dollars of damage. Mathews Peat (M P), a large horticultural nursery, was hit hard. As a result of the storm, $653,000 of additional labor and maintenance costs were incurred to clean up the nursery, remove and replace damaged plants, repair fencing, and replace glass broken when nearby tree limbs fell on some of the greenhouses.

Mathews Peat is a wholly owned subsidiary of Agro Inc., an international agricultural conglomerate. The manager of Mathews Peat, R. Dye, is reviewing the operating performance of the subsidiary for the year. Here are the results for the year as compared with budget:

After thinking about how to present the performance of M P for the year, Dye decides to break out the costs of the ice storm from the individual items affected by it and report the storm separately. The total cost of the ice storm, $653,000, consists of additional labor costs of $320,000, additional materials of $220,000, and additional occupancy costs of $113,000. These amounts are net of the insurance payments received due to the storm. The alternative performance statement follows:

Required:

a. Put yourself in Dye's position and write a short, concise cover memo for the second operating statement summarizing the essential points you want to communicate to your superiors.

b. Critically evaluate the differences between the two performance reports as presented.

Mathews Peat is a wholly owned subsidiary of Agro Inc., an international agricultural conglomerate. The manager of Mathews Peat, R. Dye, is reviewing the operating performance of the subsidiary for the year. Here are the results for the year as compared with budget:

After thinking about how to present the performance of M P for the year, Dye decides to break out the costs of the ice storm from the individual items affected by it and report the storm separately. The total cost of the ice storm, $653,000, consists of additional labor costs of $320,000, additional materials of $220,000, and additional occupancy costs of $113,000. These amounts are net of the insurance payments received due to the storm. The alternative performance statement follows:

Required:

a. Put yourself in Dye's position and write a short, concise cover memo for the second operating statement summarizing the essential points you want to communicate to your superiors.

b. Critically evaluate the differences between the two performance reports as presented.

Question

Question

Question

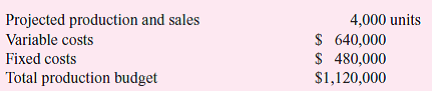

Madigan produces a single high-speed modem. The following table summarizes the current month's budget for Madigan's modem production:

Actual production and sales for the month were 3,900 units. Total production costs were $1,114,800, of which $631,800 were variable costs.

Required:

a. Prepare an end-of-month variance report for the production department using the beginning-of-month static budget.

b. Prepare an end-of-month variance report for the production department using the beginning-of-month flexible budget.

c. Write a short memo evaluating the performance of the production manager based on the variance report in (a).

d. Write a short memo evaluating the performance of the production manager based on the variance report in (b).

e. Which variance report-the one in (a) or (b)-best reflects the performance of the production manager Why

Actual production and sales for the month were 3,900 units. Total production costs were $1,114,800, of which $631,800 were variable costs.

Required:

a. Prepare an end-of-month variance report for the production department using the beginning-of-month static budget.

b. Prepare an end-of-month variance report for the production department using the beginning-of-month flexible budget.

c. Write a short memo evaluating the performance of the production manager based on the variance report in (a).

d. Write a short memo evaluating the performance of the production manager based on the variance report in (b).

e. Which variance report-the one in (a) or (b)-best reflects the performance of the production manager Why

Question

Question

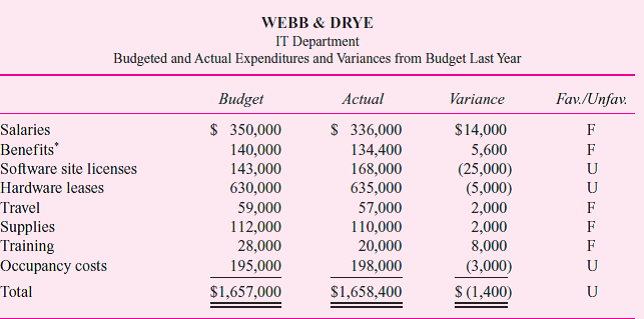

Webb Drye (WD) is a New York City law firm with over 200 attorneys. WD has a sophisticated set of information technologies-including intranets and extranets, e-mail servers, the firm's accounting, payroll, and client billing software, and document management systems-that allows WD attorneys and their expert witnesses access to millions of pages of scanned documents that often accompany large class action lawsuits. Bev Piccaretto was hired at the beginning of last year to manage WD's IT department. She and her staff maintain these various systems, but they also act as an internal consulting group to WD's professional staff. They help the staff connect to and use the various IT systems and troubleshoot problems the staff may encounter.

The IT department is a cost center. Piccaretto receives an annual operating budget and believes she is accountable for not exceeding the budget while simultaneously providing high- quality IT services to WD. Piccaretto reports to Marge Malone, WD's chief operating officer. Malone is responsible for IT, accounting, marketing, human resources, and finance functions for Webb Drye. She reports directly to WD's managing partner, who is the firm's chief executive officer.

The fiscal year has just ended. The following table contains IT's annual budget, actual amounts spent, and variances from the budget.

Malone expresses her concern that the IT department had substantial deviations from the original budgeted amounts for software licenses and salaries, and that Piccaretto should have informed Malone of these actions before they were implemented. Piccaretto argues that since total spending within the IT department was in line with the total budget of $1,657,000 she managed her budget well. Furthermore, Piccaretto points out that she had to buy more sophisticated antivirus software to protect the firm from hacker attacks and that, in paying for these software upgrades, she did not replace a staff person who left in the fourth quarter of the year. Malone counters that this open position adversely affected a large lawsuit because the attorneys working on the case had trouble downloading the scanned documents in the document management system that IT is responsible for maintaining.

Required:

Write a short memo analyzing the disagreement between Malone and Piccaretto. What issues underlie the disagreement Who is right and who is wrong What corrective actions (if any) do you recommend

The IT department is a cost center. Piccaretto receives an annual operating budget and believes she is accountable for not exceeding the budget while simultaneously providing high- quality IT services to WD. Piccaretto reports to Marge Malone, WD's chief operating officer. Malone is responsible for IT, accounting, marketing, human resources, and finance functions for Webb Drye. She reports directly to WD's managing partner, who is the firm's chief executive officer.

The fiscal year has just ended. The following table contains IT's annual budget, actual amounts spent, and variances from the budget.

Malone expresses her concern that the IT department had substantial deviations from the original budgeted amounts for software licenses and salaries, and that Piccaretto should have informed Malone of these actions before they were implemented. Piccaretto argues that since total spending within the IT department was in line with the total budget of $1,657,000 she managed her budget well. Furthermore, Piccaretto points out that she had to buy more sophisticated antivirus software to protect the firm from hacker attacks and that, in paying for these software upgrades, she did not replace a staff person who left in the fourth quarter of the year. Malone counters that this open position adversely affected a large lawsuit because the attorneys working on the case had trouble downloading the scanned documents in the document management system that IT is responsible for maintaining.

Required:

Write a short memo analyzing the disagreement between Malone and Piccaretto. What issues underlie the disagreement Who is right and who is wrong What corrective actions (if any) do you recommend

Question

Question

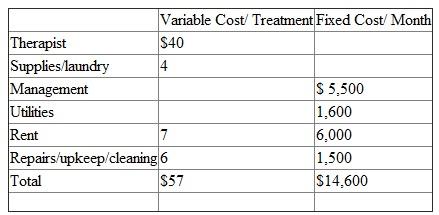

Spa Ariana promotes itself as an upscale spa offering a variety of treatments, including massages, facials, and manicures, performed in a luxurious setting by qualified therapists. The owners of Spa Ariana invested close to $450,000 of their own money three years ago in building and decorating the interior of their new spa (six treatment rooms, relaxation rooms, showers, and waiting area). Located on the main street in a ski resort, the spa has a five-year renewable lease from the building owner. The owners hire a manager to run the spa.

The average one-hour treatment is priced at $100. Ariana has the following cost structure:

Assume that all treatments have the same variable cost structure depicted in the table.

Assume that all treatments have the same variable cost structure depicted in the table.

Required:

a. Calculate the number of treatments Spa Ariana must perform each month in order to break even.

b. In April, the owners of Ariana expect to perform 550 treatments. Prepare a budget for April assuming 550 treatments are given.

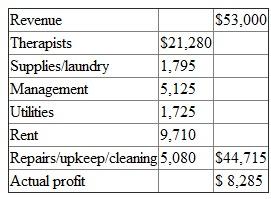

c. In April Spa Ariana performs 530 treatments and incurs the following actual costs. Prepare a performance report for April comparing actual performance to the static budget in part (b) based on 550 treatments.

Actual Operating Results for April

d. Prepare a performance report for April comparing actual performance to a flexible budget based on the actual number of treatments performed in April of 530.

d. Prepare a performance report for April comparing actual performance to a flexible budget based on the actual number of treatments performed in April of 530.

e. Which of the two performance reports you prepared in parts (c) and (d) best reflect the true performance of the Spa Ariana in April Explain your reasoning.

f. Do the break-even calculation you performed in part (a) and the budgeted and actual profits computed in parts (a) - (d) accurately capture the true economics of the Ariana Spa Explain why or why not.

The average one-hour treatment is priced at $100. Ariana has the following cost structure:

Assume that all treatments have the same variable cost structure depicted in the table.Required:

a. Calculate the number of treatments Spa Ariana must perform each month in order to break even.

b. In April, the owners of Ariana expect to perform 550 treatments. Prepare a budget for April assuming 550 treatments are given.

c. In April Spa Ariana performs 530 treatments and incurs the following actual costs. Prepare a performance report for April comparing actual performance to the static budget in part (b) based on 550 treatments.

Actual Operating Results for April

d. Prepare a performance report for April comparing actual performance to a flexible budget based on the actual number of treatments performed in April of 530.e. Which of the two performance reports you prepared in parts (c) and (d) best reflect the true performance of the Spa Ariana in April Explain your reasoning.

f. Do the break-even calculation you performed in part (a) and the budgeted and actual profits computed in parts (a) - (d) accurately capture the true economics of the Ariana Spa Explain why or why not.

Question

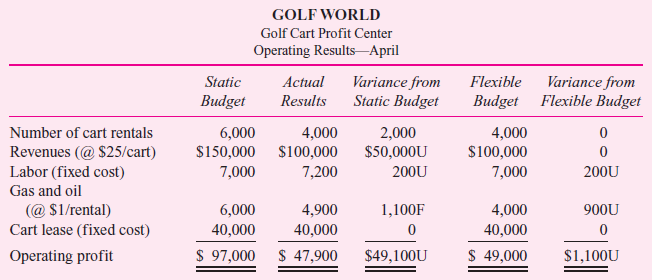

Golf World is a 1,000-room luxury resort with swimming pools, tennis courts, three golf courses, and many other resort amenities.

The head golf course superintendent, Sandy Green, is responsible for all golf course maintenance and conditioning. Green also has the final say as to whether a particular course is open or closed due to weather conditions and whether players can rent motorized riding golf carts for use on a particular course. If the course is very wet, the golf carts will damage the turf, which Green's maintenance crew will have to repair. Since she is out on the courses every morning supervising the maintenance crews, she knows the condition of the courses.

Wiley Grimes is in charge of the golf cart rentals. His crew maintains the golf cart fleet of over 200 cars, cleans them, puts oil and gas in them, and repairs minor damage. He also is responsible for leasing the carts from the manufacturer, including the terms of the lease, the number of carts to lease, and the choice of cart vendor. When guests arrive at the golf course to play, they pay greens fees to play and a cart fee if they wish to use a cart. If they do not wish to rent a cart, they pay only the greens fee and walk the course.

Grimes and Green manage separate profit centers. The golf cart profit center's revenue is composed of the fees collected from the carts. The golf course profit center's revenue is from the greens fees collected. When the results from April were reviewed, golf cart operating profits were only 49 percent of budget. Wiley argued that the poor results were due to the unusually heavy rains in April. He complained that there were several days when, though only a few areas of the course were wet, the entire course was closed to carts because the grounds crew was too busy to rope off these areas.

To better analyze the performance of the golf cart profit center, the controller's office recently implemented a flexible budget based on the number of cart rentals:

Required:

a. Evaluate the performance of the golf cart profit center for the month of April.

b. What are the advantages and disadvantages of the controller's new budgeting system

c. What additional recommendations would you make regarding the operations of Golf World

The head golf course superintendent, Sandy Green, is responsible for all golf course maintenance and conditioning. Green also has the final say as to whether a particular course is open or closed due to weather conditions and whether players can rent motorized riding golf carts for use on a particular course. If the course is very wet, the golf carts will damage the turf, which Green's maintenance crew will have to repair. Since she is out on the courses every morning supervising the maintenance crews, she knows the condition of the courses.

Wiley Grimes is in charge of the golf cart rentals. His crew maintains the golf cart fleet of over 200 cars, cleans them, puts oil and gas in them, and repairs minor damage. He also is responsible for leasing the carts from the manufacturer, including the terms of the lease, the number of carts to lease, and the choice of cart vendor. When guests arrive at the golf course to play, they pay greens fees to play and a cart fee if they wish to use a cart. If they do not wish to rent a cart, they pay only the greens fee and walk the course.

Grimes and Green manage separate profit centers. The golf cart profit center's revenue is composed of the fees collected from the carts. The golf course profit center's revenue is from the greens fees collected. When the results from April were reviewed, golf cart operating profits were only 49 percent of budget. Wiley argued that the poor results were due to the unusually heavy rains in April. He complained that there were several days when, though only a few areas of the course were wet, the entire course was closed to carts because the grounds crew was too busy to rope off these areas.

To better analyze the performance of the golf cart profit center, the controller's office recently implemented a flexible budget based on the number of cart rentals:

Required:

a. Evaluate the performance of the golf cart profit center for the month of April.

b. What are the advantages and disadvantages of the controller's new budgeting system

c. What additional recommendations would you make regarding the operations of Golf World

Question

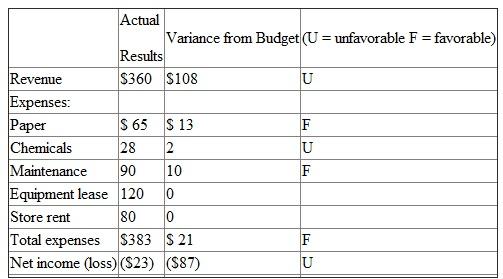

Picture Maker is a freestanding photo kiosk consumers use to download their digital photos and make prints. Shashi Sharma has a small business that leases several Picture Makers from the manufacturer for $120 per month per kiosk, and she places them in high-traffic retail locations. Customers pay $0.18 per print. (The kiosk only makes six- by eight-inch prints.) Sharma has one kiosk located in the Sanchez Drug Store, for which Sharma pays Sanchez $80 per month rent. Sharma checks each of her kiosks every few days, refilling the photographic paper and chemicals, and collects the money. Sharma hires a service company that cleans the machine, replaces any worn or defective parts, and resets the kiosk's settings to ensure the kiosk continues to provide high-quality prints. This maintenance is performed monthly and is independent of the number of prints made during the month. The average cost of the service runs about $90 per month, but it can vary depending on the extent of repairs and parts required to maintain the equipment.

Paper and chemicals are variable costs, and maintenance, equipment lease, and store rent are fixed costs. If the kiosk is malfunctioning and the print quality deteriorates, Sanchez refunds the customer's money and then gets his money back from Sharma when she comes by to check the paper and chemical supplies. These occasional refunds cause her variable costs perprint for paper and chemicals to vary over time.

The following table reports the results from operating the kiosk at the Sanchez Drug Store last month. Budget variances are computed as the difference between actual and budgeted amounts. An unfavorable variance (U) exists when actual revenues fall short of budget or when actual expenses exceed the budget. Last month, the kiosk had a net loss of $23, which was $87 more than budgeted.

Sanchez Drug Store Kiosk Last Month

Required:

Required:

a. Prepare a schedule that shows the budget Sharma used in calculating the variances in the preceding report.

b. How many good prints were made last month at the Sanchez Drug Store kiosk

c. Prepare a flexible budget for the Sanchez Drug Store kiosk based on a volume of 2,000 prints.

Paper and chemicals are variable costs, and maintenance, equipment lease, and store rent are fixed costs. If the kiosk is malfunctioning and the print quality deteriorates, Sanchez refunds the customer's money and then gets his money back from Sharma when she comes by to check the paper and chemical supplies. These occasional refunds cause her variable costs perprint for paper and chemicals to vary over time.

The following table reports the results from operating the kiosk at the Sanchez Drug Store last month. Budget variances are computed as the difference between actual and budgeted amounts. An unfavorable variance (U) exists when actual revenues fall short of budget or when actual expenses exceed the budget. Last month, the kiosk had a net loss of $23, which was $87 more than budgeted.

Sanchez Drug Store Kiosk Last Month

Required: a. Prepare a schedule that shows the budget Sharma used in calculating the variances in the preceding report.

b. How many good prints were made last month at the Sanchez Drug Store kiosk

c. Prepare a flexible budget for the Sanchez Drug Store kiosk based on a volume of 2,000 prints.

Question

Question

Question

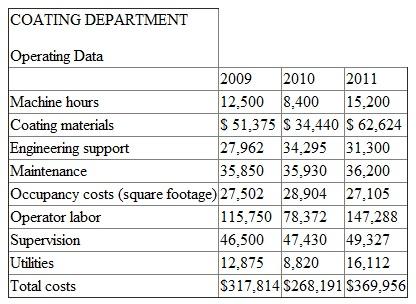

The coating department of a parts manufacturing department coats various parts with an antirust, zinc- based material. The parts to be processed are loaded into baskets; the baskets are passed through a coating machine that dips the parts into the zinc solution. The machine then heats the parts to ensure that the coating bonds properly. All parts being coated are assigned a cost for the coating department based on the number of hours the parts spend in the coating machine. Prior to the beginning of the year, cost categories are accumulated by department (including the coating department). These cost categories are classified as either fixed or variable and then a flexible budget for the department is constructed. Given an estimate of machine hours for the next year, the coating department's projected cost per machine hour is computed.

Here are data for the last three operating years. Expected coating machine hours for 2012 arre 16,000 hours.

Required:

Required:

a. Estimate the coating department's flexible budget for 2012. Explicitly state and justify the assumptions used in deriving your estimates.

b. Calculate the coating department's cost per machine hour for 2012.

Here are data for the last three operating years. Expected coating machine hours for 2012 arre 16,000 hours.

Required:a. Estimate the coating department's flexible budget for 2012. Explicitly state and justify the assumptions used in deriving your estimates.

b. Calculate the coating department's cost per machine hour for 2012.

Question

Question

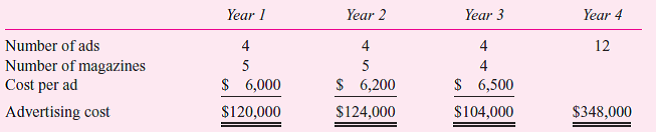

Robin Jensen, manager of market planning for Viral Products of the IDP Pharmaceutical Co., is responsible for advertising a class of products. She has designed a three-year marketing plan to increase the market share of her product class. Her plan involves a major increase in magazine advertising. She has met with an advertising agency that has designed a three-year ad campaign involving 12 separate ads that build on a common theme. Each ad will run in three consecutive monthly medi285cal magazines and then be followed by the next ad in the sequence. Up to five medical journals will carry the ad campaign. Direct mail campaigns and direct sales promotional material will be designed to follow the theme of the ad currently appearing. The accompanying table summarizes the cost of the campaign:

The firm's normal policy is to budget each year as a separate entity without carrying forward unspent monies. Jensen is requesting that, instead of just approving the budget for next year (Year 1 above), the firm approve and budget the entire three-year project. This would allow her to move forward with her campaign and give her the freedom to apply any unspent funds in one year to the next year or to use them in another part of the campaign. She argues that the ad campaign is an integrated project stretching over three years and should be either approved or rejected in its entirety.

Required:

Critically evaluate Jensen's request and make a recommendation as to whether a three-year budget should be approved per her proposal. (Assume that the advertising campaign is expected to be a profitable project.)

The firm's normal policy is to budget each year as a separate entity without carrying forward unspent monies. Jensen is requesting that, instead of just approving the budget for next year (Year 1 above), the firm approve and budget the entire three-year project. This would allow her to move forward with her campaign and give her the freedom to apply any unspent funds in one year to the next year or to use them in another part of the campaign. She argues that the ad campaign is an integrated project stretching over three years and should be either approved or rejected in its entirety.

Required:

Critically evaluate Jensen's request and make a recommendation as to whether a three-year budget should be approved per her proposal. (Assume that the advertising campaign is expected to be a profitable project.)

Question

Question

Potter-Bowen (PB) manufactures and sells postage meters throughout the world. Postage meters print the necessary postage on envelopes, eliminating the need to affix stamps. The meter keeps track of the postage, the user takes the meter's counter to a post office and pays money, and the post office initializes the meter to print postage totaling that amount. The firm offers about 30 different postage systems, ranging from small manual systems (costing a few hundred dollars) to large automated ones (costing up to $75,000).

PB is organized into Research and Development, Manufacturing, and Marketing. Marketing is further subdivided into four sectors: North America, South America, Europe, and Asia. The North American marketing sector has a sales force organized into 32 regions with approximately 75 to 200 salespeople per region.

The budgeting process begins with the chief financial officer (CFO) and the vice president of marketing jointly projecting the total sales for the next year. Their staffs look at trends of the various PB models and project total unit sales by model within each marketing sector. Price increases are forecast and dollar sales per model are calculated. The North American sector is then given a target number of units and a target revenue by model for the year. The manager of the North American sector, Helen Neumann, and her staff then allocate the division's target units and target revenue by region.

The target unit sales for each model per region are derived by taking the region's historical percentage sales for that machine times North America's target for that model. For example, model 6103 has North American target unit sales of 18,500 for next year. The Utah region last year sold 4.1 percent of all model 6103s sold in North America. Therefore, Utah's target of 6103s for next year is 758 units (4.1% X 18,500). The average sales price of the 6103 is set at $11,000. Thus, Utah's revenue budget for 6103s is $8,338,000. Given the total forecasted unit sales, average selling prices, and historical sales of each model in all regions, each region is assigned a unit target and revenue budget by model. The region's total revenue budget is the sum of the individual models' revenue targets.

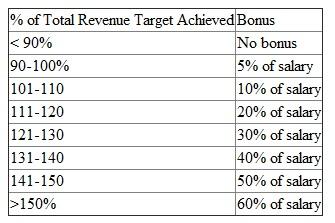

Each salesperson in the region is given a unit and revenue target by model using a similar procedure. If Gary Lindenmeyer (a salesperson in Utah) sold 6 percent of Utah's 6103s last year, his unit sales target of 6103s next year is 45 units (6% X 758). His total revenue target for 6103s is $495,000 (or 45 X $11,000). Totaling all the models gives each salesperson's total revenue budget. Salespeople are paid a fixed salary plus a bonus. The bonus is calculated based on the following table:

Required:

Required:

Critically evaluate PB's sales budgeting system and sales force compensation system. Describe any potential dysfunctional behaviors that PB's systems are likely to generate.

PB is organized into Research and Development, Manufacturing, and Marketing. Marketing is further subdivided into four sectors: North America, South America, Europe, and Asia. The North American marketing sector has a sales force organized into 32 regions with approximately 75 to 200 salespeople per region.

The budgeting process begins with the chief financial officer (CFO) and the vice president of marketing jointly projecting the total sales for the next year. Their staffs look at trends of the various PB models and project total unit sales by model within each marketing sector. Price increases are forecast and dollar sales per model are calculated. The North American sector is then given a target number of units and a target revenue by model for the year. The manager of the North American sector, Helen Neumann, and her staff then allocate the division's target units and target revenue by region.

The target unit sales for each model per region are derived by taking the region's historical percentage sales for that machine times North America's target for that model. For example, model 6103 has North American target unit sales of 18,500 for next year. The Utah region last year sold 4.1 percent of all model 6103s sold in North America. Therefore, Utah's target of 6103s for next year is 758 units (4.1% X 18,500). The average sales price of the 6103 is set at $11,000. Thus, Utah's revenue budget for 6103s is $8,338,000. Given the total forecasted unit sales, average selling prices, and historical sales of each model in all regions, each region is assigned a unit target and revenue budget by model. The region's total revenue budget is the sum of the individual models' revenue targets.

Each salesperson in the region is given a unit and revenue target by model using a similar procedure. If Gary Lindenmeyer (a salesperson in Utah) sold 6 percent of Utah's 6103s last year, his unit sales target of 6103s next year is 45 units (6% X 758). His total revenue target for 6103s is $495,000 (or 45 X $11,000). Totaling all the models gives each salesperson's total revenue budget. Salespeople are paid a fixed salary plus a bonus. The bonus is calculated based on the following table:

Required:Critically evaluate PB's sales budgeting system and sales force compensation system. Describe any potential dysfunctional behaviors that PB's systems are likely to generate.

Question

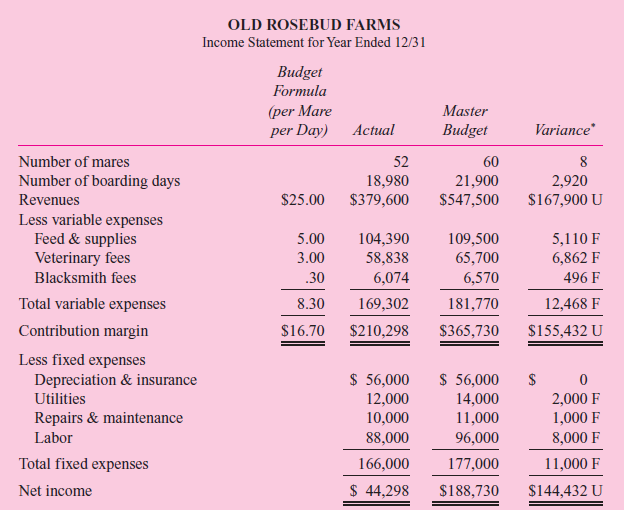

Old Rosebud is a Kentucky horse farm that specializes in boarding thoroughbred breeding mares and their foals. Customers bring their breeding mares to Old Rosebud for delivery of their foals and after-birth care of the mare and foal. Recent changes in the tax laws brought about a substantial

decline in thoroughbred breeding. As a result, profits declined in the thoroughbred boarding industry.

Old Rosebud prepared a master budget for the current year by splitting costs into variable costs and fixed costs. The budget was prepared before the extent of the downturn was fully recognized. Table 1 above compares actual with budget for the current year.

Required:

Prepare an analysis of the operating performance of Old Rosebud Farms. Supporting tables or calculations should be clearly labeled.

decline in thoroughbred breeding. As a result, profits declined in the thoroughbred boarding industry.

Old Rosebud prepared a master budget for the current year by splitting costs into variable costs and fixed costs. The budget was prepared before the extent of the downturn was fully recognized. Table 1 above compares actual with budget for the current year.

Required:

Prepare an analysis of the operating performance of Old Rosebud Farms. Supporting tables or calculations should be clearly labeled.

Question

Question

Question

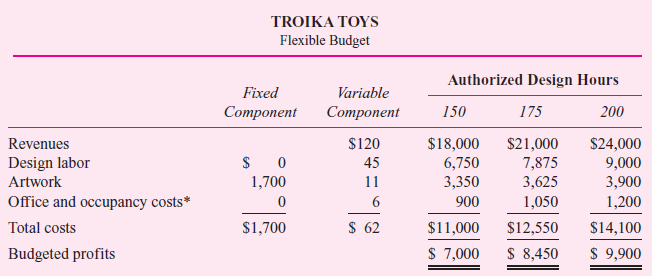

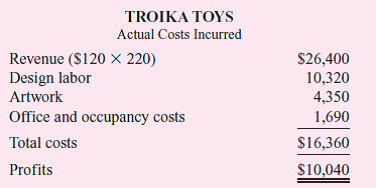

Adrian and Pells (AP) is an advertising agency that uses flexible budgeting for both planning and control. One of its clients, Troika Toys, asked AP to prepare an ad campaign for a new toy. AP's contract with Troika calls for paying AP $120 per design hour for between 150 and 200 hours.

AP has a staff of ad campaign designers who prepare the ad campaigns. Customers are billed only for the time designers work on their project. Partner time is not billed directly to the customer. As part of the planning process, Sue Bent, partner-in-charge of the Troika account, prepared the following flexible budget. "Authorized Design Hours" is the estimated range of time AP expects the job to require and what the client agrees to authorize.

AP's executive committee reviewed Bent's budget and approved it and the Troika contract. After some preliminary work, Troika liked the ideas so much it expanded the authorized time range to be between 175 and 250 hours.

Bent and her design team finished the Troika project. Two hundred and twenty design hours were logged and billed to Troika at the contract price ($120 per hour). Upon completion of the Troika campaign, the following revenues and costs had been accumulated:

AP's accounting manager keeps track of actual costs incurred by AP on each account. AP employs a staff of designers. Their average salary is $45 per hour. New designers earn less than the average; those with more experience earn more. The actual design labor costs charged to each project are the actual hours times the designer's actual hourly cost. Artwork consists of both in-house and out-of-house artists who draw up the art for the ads designed by the designers. Office and occupancy costs consist of a charge per designer hour to cover rent, photocopying, and phones, plus actual long-distance calls, faxes, and overnight delivery services.

Required:

Prepare a table that reports on Sue Bent's performance on the Troika Toys account and write a short memo to the executive committee that summarizes her performance on this project.

AP has a staff of ad campaign designers who prepare the ad campaigns. Customers are billed only for the time designers work on their project. Partner time is not billed directly to the customer. As part of the planning process, Sue Bent, partner-in-charge of the Troika account, prepared the following flexible budget. "Authorized Design Hours" is the estimated range of time AP expects the job to require and what the client agrees to authorize.

AP's executive committee reviewed Bent's budget and approved it and the Troika contract. After some preliminary work, Troika liked the ideas so much it expanded the authorized time range to be between 175 and 250 hours.

Bent and her design team finished the Troika project. Two hundred and twenty design hours were logged and billed to Troika at the contract price ($120 per hour). Upon completion of the Troika campaign, the following revenues and costs had been accumulated:

AP's accounting manager keeps track of actual costs incurred by AP on each account. AP employs a staff of designers. Their average salary is $45 per hour. New designers earn less than the average; those with more experience earn more. The actual design labor costs charged to each project are the actual hours times the designer's actual hourly cost. Artwork consists of both in-house and out-of-house artists who draw up the art for the ads designed by the designers. Office and occupancy costs consist of a charge per designer hour to cover rent, photocopying, and phones, plus actual long-distance calls, faxes, and overnight delivery services.

Required:

Prepare a table that reports on Sue Bent's performance on the Troika Toys account and write a short memo to the executive committee that summarizes her performance on this project.

Question

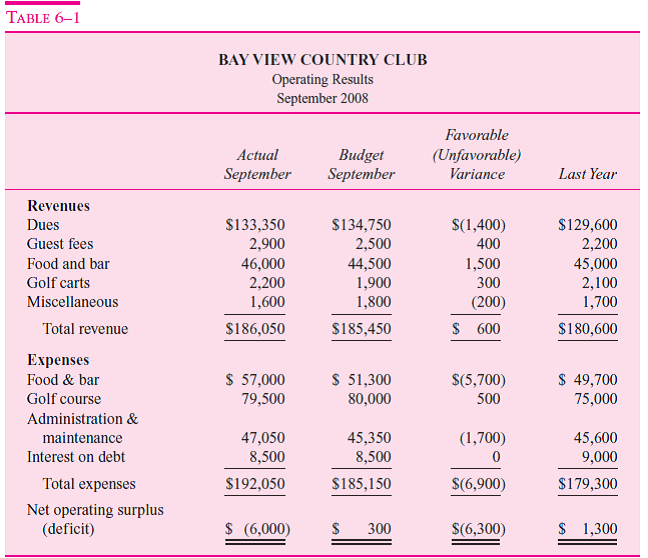

Using the data in Table 6-1 (on page 241), how much did it cost the members of Bay View Country Club to operate the club for September 2008

Question

Access.Com produces and sells software to libraries and schools to block access to Web sites deemed inappropriate by the customer. In addition, the software also tracks and reports on Web sites visited and advises the customer of other Web sites the customer might choose to block. Access.Com's software sells for between $15,000 and $20,000.

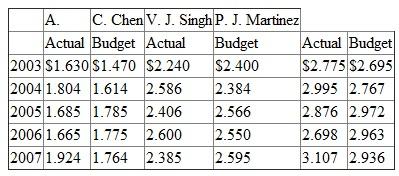

Three account managers (V J. Singh, A. C. Chen, and P. J. Martinez) sell the software and are paid a fixed salary plus a percentage of all sales in excess of targeted (budgeted) sales. Vice President of Marketing S. B. Ro sets the budgeted sales amount for each account manager. The following table reports actual and budgeted sales for the three account managers for the past five years.

Required:

Required:

a. Based on the data in the table, describe the process used by Ro to set sales quotas for each account manager.

b. Discuss the pros and cons of Access.Com's budgeting process for setting account managers' sales targets.

Three account managers (V J. Singh, A. C. Chen, and P. J. Martinez) sell the software and are paid a fixed salary plus a percentage of all sales in excess of targeted (budgeted) sales. Vice President of Marketing S. B. Ro sets the budgeted sales amount for each account manager. The following table reports actual and budgeted sales for the three account managers for the past five years.

Required: a. Based on the data in the table, describe the process used by Ro to set sales quotas for each account manager.

b. Discuss the pros and cons of Access.Com's budgeting process for setting account managers' sales targets.

Question

Question

Question

Videx is the premier firm in the security systems industry. Martha Rameriz is an account manager at Videx responsible for selling residential systems. She is compensated based on beating a predetermined sales budget. The last seven years' sales budgets and actual sales data follow. Videx sets its sales budgets centrally in a top-down fashion.

Required:

Required:

a. Martha Rameriz sells $908,000 in year 7. What budget will she be assigned for year 8

b. Suppose Rameriz sells $900,000 of systems in year 7. What budget will she be assigned in year 8

Required: a. Martha Rameriz sells $908,000 in year 7. What budget will she be assigned for year 8

b. Suppose Rameriz sells $900,000 of systems in year 7. What budget will she be assigned in year 8

Question

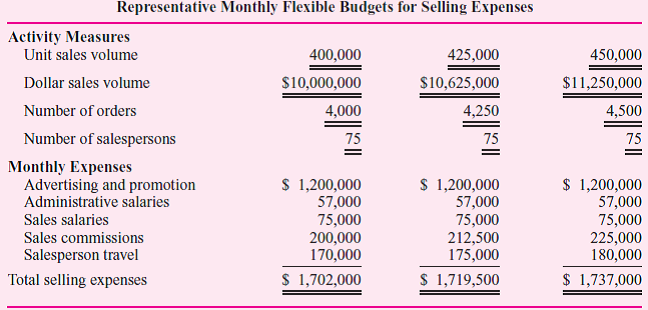

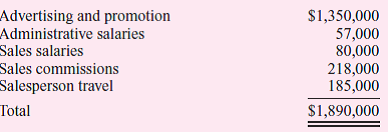

Wielson Company employs flexible budgeting techniques to evaluate the performance of several of its activities. The selling expense flexible budgets for three representative monthly activity levels are shown here.

The following assumptions were used to develop the selling expense flexible budgets:

• The average size of Wielson's sales force during the year was planned to be 75 people.

• Salespeople are paid a monthly salary plus commissions on gross dollar sales.

• Travel costs are best characterized as step-variable costs. The fixed portion is related to the number of salespeople, while the variable portion fluctuates with gross dollar sales.

A sales force of 80 people generated a total of 4,300 orders resulting in a sales volume of 420,000 units during November. Gross dollar sales amounted to $10.9 million. Selling expenses incurred for November were as follows:

Required:

Prepare a selling expense report for November that Wielson Company can use to evaluate its control

over selling expenses. The report should have a line for each selling expense item showing the appropriate budgeted amount, the actual selling expense, and the monthly dollar variation.

The following assumptions were used to develop the selling expense flexible budgets:

• The average size of Wielson's sales force during the year was planned to be 75 people.

• Salespeople are paid a monthly salary plus commissions on gross dollar sales.

• Travel costs are best characterized as step-variable costs. The fixed portion is related to the number of salespeople, while the variable portion fluctuates with gross dollar sales.

A sales force of 80 people generated a total of 4,300 orders resulting in a sales volume of 420,000 units during November. Gross dollar sales amounted to $10.9 million. Selling expenses incurred for November were as follows:

Required:

Prepare a selling expense report for November that Wielson Company can use to evaluate its control

over selling expenses. The report should have a line for each selling expense item showing the appropriate budgeted amount, the actual selling expense, and the monthly dollar variation.

Question

Question

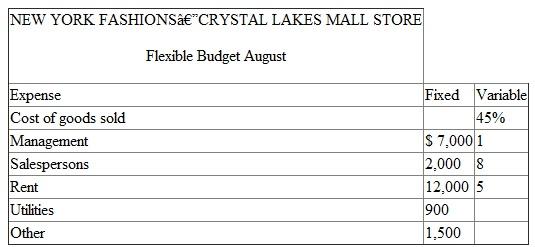

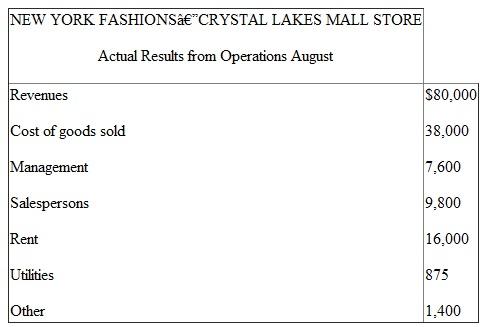

New York Fashions owns 87 women's clothing stores in shopping malls. Corporate headquarters of New York Fashions uses flexible budgets to control the operations of each of the stores. The following table presents the August flexible budget for the New York Fashions store located in the Crystal Lakes Mall:

Variable costs are based on a percentage of revenues.

Variable costs are based on a percentage of revenues.

Required:

a. Revenues for August were $80,000. Calculate budgeted profits for August.

b. Actual results for August are summarized in the following table:

Prepare a report for the New York Fashions-Crystal Lakes Mall store for the month of August comparing actual results to the budget.

Prepare a report for the New York Fashions-Crystal Lakes Mall store for the month of August comparing actual results to the budget.

c. Analyze the performance of the Crystal Lakes Mall store in August.

d. How does a flexible budget change the incentives of managers held responsible for meeting the flexible budget as compared to the incentives created by meeting a static (fixed) budget

Variable costs are based on a percentage of revenues.Required:

a. Revenues for August were $80,000. Calculate budgeted profits for August.

b. Actual results for August are summarized in the following table:

Prepare a report for the New York Fashions-Crystal Lakes Mall store for the month of August comparing actual results to the budget.c. Analyze the performance of the Crystal Lakes Mall store in August.