Deck 17: Completing the Audit Engagement

Full screen (f)

Question

Question

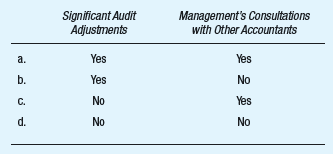

Which of the following matters should an auditor communicate to those charged with governance?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/33

Play

Full screen (f)

Deck 17: Completing the Audit Engagement

1

What are the types of subsequent events relevant to financial statement audits? Give one example of each type of subsequent event that might materially affect the financial statements.

The examples for each type of subsequent events that might have materially affected the financial statements are as follows:

• Example for Type 1 - A bad debt from the outstanding sundry debtors of a company, as the customer who owed money to the company became insolvent

• Example for Type 2 - Litigation was settled after the date of the balance sheet in order to pay the claims raised by the injured parties.

• Example for Type 1 - A bad debt from the outstanding sundry debtors of a company, as the customer who owed money to the company became insolvent

• Example for Type 2 - Litigation was settled after the date of the balance sheet in order to pay the claims raised by the injured parties.

2

Which of the following matters should an auditor communicate to those charged with governance?

(A) Significant audit adjustments - 'Yes' and Management's consultations with other accountants - 'Yes'

Justification

As per the auditing standards, the auditor should communicate the matters of "significant audit adjustments" and the "management's consultants with other accountants" to the board of directors and the audit committee. It enhances an effective two-way communication between them about the financial reporting issues. The communication to those charged with governance on these matters, by the auditor, provides sufficient information about the audit related issues.

Justification

As per the auditing standards, the auditor should communicate the matters of "significant audit adjustments" and the "management's consultants with other accountants" to the board of directors and the audit committee. It enhances an effective two-way communication between them about the financial reporting issues. The communication to those charged with governance on these matters, by the auditor, provides sufficient information about the audit related issues.

3

Under what circumstances would the auditor dual date an audit report?

Dual dating

Dual dating is the stating of two dates in the audit report.

The auditor dual dates the auditor report when any events are disclosed in the financial statements after the date of collecting sufficient and reliable evidences, but before the issue of the financial statements.

Dual dating is the stating of two dates in the audit report.

The auditor dual dates the auditor report when any events are disclosed in the financial statements after the date of collecting sufficient and reliable evidences, but before the issue of the financial statements.

4

Which of the following events occurring after the issuance of a set of financial statements and the accompanying auditor's report would be most likely to cause the auditor to make further inquiries about the financial statements?

A) A technological development in the industry that could affect the entity's future ability to continue as a going concern.

B) The entity's sale of a subsidiary that accounts for 30 percent of the entity's consolidated sales.

C) The discovery of information regarding a contingency that existed before the financial statements were issued.

D) The final resolution of a lawsuit explained in a separate paragraph of the auditor's report.

A) A technological development in the industry that could affect the entity's future ability to continue as a going concern.

B) The entity's sale of a subsidiary that accounts for 30 percent of the entity's consolidated sales.

C) The discovery of information regarding a contingency that existed before the financial statements were issued.

D) The final resolution of a lawsuit explained in a separate paragraph of the auditor's report.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

5

Are analytical procedures required as part of the final overall review of the financial statements? What is the purpose of such analytical procedures?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

6

During an audit engagement, Harper, CPA, has satisfactorily completed an examination of accounts payable and other liabilities and now plans to determine whether there are any loss contingencies arising from litigation, claims, or assessments.

Required:

What audit procedures should Harper follow with respect to the existence of loss contingencies arising from litigation, claims, and assessments? Do not discuss reporting requirements.

(AICPA, adapted)

Required:

What audit procedures should Harper follow with respect to the existence of loss contingencies arising from litigation, claims, and assessments? Do not discuss reporting requirements.

(AICPA, adapted)

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

7

Why does the auditor obtain a representation letter from management?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

8

Cole Cole, CPAs, are auditing the financial statements of Consolidated Industries Company for the year ended December 31, 2013. On April 2, 2014, an inquiry letter to J. J. Young, Consolidated's outside attorney, was drafted to corroborate the information furnished to Cole by management concerning pending and threatened litigation, claims, and assessments, as well as unasserted claims and assessments. On May 6, 2014, C. R. Cao, Consolidated's chief financial officer, gave Cole a draft of the inquiry letter below for Cole's review before mailing it to Young.

May 6, 2014

J. J. Young, Attorney at Law

123 Main Street

Any town, USA

Dear J. J. Young:

In connection with an audit of our financial statements at December 31, 2013, and for the year then ended, management of the company has prepared, and furnished to our auditors, Cole Cole, CPAs, 456 Broadway, Anytown, USA, a description and evaluation of certain contingencies, including those set forth below involving matters with respect to which you have been engaged and to which you have devoted substantive attention on behalf of the company in the form of legal consultation or representation. Your response should include matters that existed at December 31, 2013. Because of the confidentiality of all these matters, your response may be limited.

In November 2013, an action was brought against the company by an outside salesman alleging breach of contract for sales commissions and pleading a second cause of action for an accounting with respect to claims for fees and commissions. The salesman's action claims damages of $300,000, but the company believes it has meritorious defenses to the claims. The possible exposure of the company to a successful judgment on behalf of the plaintiff is slight.

In July 2013, an action was brought against the company by Industrial Manufacturing Company ("Industrial") alleging patent infringement and seeking damages of $20 million. The action in U.S. District Court resulted in a decision on October 16, 2013, holding that the company had infringed seven Industrial patents and awarding damages of $14 million. The company vigorously denies these allegations and has filed an appeal with the U.S. Court of Appeals for the Federal Circuit. The appeal process is expected to take approximately two years, but there is some chance that Industrial may ultimately prevail.

Please furnish to our auditors such explanation, if any, that you consider necessary to supplement the foregoing information, including an explanation of those matters as to which your views may differ from those stated and an identification of the omission of any pending or threatened litigation, claims, and assessments or a statement that the list of such matters is complete. Your response may be quoted or referred to in the financial statements without further correspondence with you.

You also consulted on various other matters considered pending or threatened litigation. However, you may not comment on these matters because publicizing them may alert potential plaintiffs to the strengths of their cases. In addition, various other matters probable of assertion that have some chance of an unfavorable outcome, as of December 31, 2013, are unasserted claims and assessments.

C. R. Cao

Chief Financial Officer

Required:

Describe the omissions, ambiguities, and inappropriate statements and terminology in Cao's letter.

(AICPA, adapted)

May 6, 2014

J. J. Young, Attorney at Law

123 Main Street

Any town, USA

Dear J. J. Young:

In connection with an audit of our financial statements at December 31, 2013, and for the year then ended, management of the company has prepared, and furnished to our auditors, Cole Cole, CPAs, 456 Broadway, Anytown, USA, a description and evaluation of certain contingencies, including those set forth below involving matters with respect to which you have been engaged and to which you have devoted substantive attention on behalf of the company in the form of legal consultation or representation. Your response should include matters that existed at December 31, 2013. Because of the confidentiality of all these matters, your response may be limited.

In November 2013, an action was brought against the company by an outside salesman alleging breach of contract for sales commissions and pleading a second cause of action for an accounting with respect to claims for fees and commissions. The salesman's action claims damages of $300,000, but the company believes it has meritorious defenses to the claims. The possible exposure of the company to a successful judgment on behalf of the plaintiff is slight.

In July 2013, an action was brought against the company by Industrial Manufacturing Company ("Industrial") alleging patent infringement and seeking damages of $20 million. The action in U.S. District Court resulted in a decision on October 16, 2013, holding that the company had infringed seven Industrial patents and awarding damages of $14 million. The company vigorously denies these allegations and has filed an appeal with the U.S. Court of Appeals for the Federal Circuit. The appeal process is expected to take approximately two years, but there is some chance that Industrial may ultimately prevail.

Please furnish to our auditors such explanation, if any, that you consider necessary to supplement the foregoing information, including an explanation of those matters as to which your views may differ from those stated and an identification of the omission of any pending or threatened litigation, claims, and assessments or a statement that the list of such matters is complete. Your response may be quoted or referred to in the financial statements without further correspondence with you.

You also consulted on various other matters considered pending or threatened litigation. However, you may not comment on these matters because publicizing them may alert potential plaintiffs to the strengths of their cases. In addition, various other matters probable of assertion that have some chance of an unfavorable outcome, as of December 31, 2013, are unasserted claims and assessments.

C. R. Cao

Chief Financial Officer

Required:

Describe the omissions, ambiguities, and inappropriate statements and terminology in Cao's letter.

(AICPA, adapted)

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

9

Describe the purposes of an independent engagement quality review by a quality review partner.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

10

Namiki, CPA, is auditing the financial statements of Taylor Corporation for the year ended December 31, 2013. Namiki plans to complete the fieldwork and sign the auditor's report about March 10, 2014. Namiki is concerned about events and transactions occurring after December 31, 2013, that may affect the 2013 financial statements.

Required:

a. What general types of subsequent events require Namiki's consideration and evaluation?

b. What auditing procedures should Namiki consider performing to gather evidence concerning subsequent events?

(AICPA, adapted)

Required:

a. What general types of subsequent events require Namiki's consideration and evaluation?

b. What auditing procedures should Namiki consider performing to gather evidence concerning subsequent events?

(AICPA, adapted)

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

11

List the three overall steps in the going concern evaluation process.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

12

For each of the following items, assume that Josh Feldstein, CPA, is expressing an opinion on Scornick Company's financial statements for the year ended December 31, 2013; that he completed fieldwork on January 21, 2014; and that he now is preparing his opinion to accompany the financial statements. In each item a subsequent event is described. This event was disclosed to the CPA either in connection with his review of subsequent events or after the date on which the auditor has obtained sufficient appropriate audit evidence. Describe the financial statement effects, if any, of each of the following subsequent events. Each of the five items is independent of the other four and is to be considered separately.

1. A large account receivable from Agronowitz Company (material to financial statement presentation) was considered fully collectible at December 31, 2013. Agronowitz suffered a plant explosion on January 25, 2014. Because Agronowitz was uninsured, it is unlikely that the account will be paid.

2. The tax court ruled in favor of the company on January 25, 2014. Litigation involved deductions claimed on the 2010 and 2011 tax returns. In accrued taxes payable, Scornick had provided for the full amount of the potential disallowances. The Internal Revenue Service will not appeal the tax court's ruling.

3. Scornick's Manufacturing Division, whose assets constituted 45 percent of Scornick's total assets at December 31, 2013, was sold on February 1, 2014. The new owner assumed the bonded indebtedness associated with this property.

4. On January 15, 2014, R. E. Fogler, a major investment adviser, issued a negative report on Scornick's long-term prospects. The market price of Scornick's common stock subsequently declined by 40 percent.

5. At its January 5, 2014, meeting, Scornick's board of directors voted to increase substantially the advertising budget for the coming year and authorized a change in advertising agencies.

1. A large account receivable from Agronowitz Company (material to financial statement presentation) was considered fully collectible at December 31, 2013. Agronowitz suffered a plant explosion on January 25, 2014. Because Agronowitz was uninsured, it is unlikely that the account will be paid.

2. The tax court ruled in favor of the company on January 25, 2014. Litigation involved deductions claimed on the 2010 and 2011 tax returns. In accrued taxes payable, Scornick had provided for the full amount of the potential disallowances. The Internal Revenue Service will not appeal the tax court's ruling.

3. Scornick's Manufacturing Division, whose assets constituted 45 percent of Scornick's total assets at December 31, 2013, was sold on February 1, 2014. The new owner assumed the bonded indebtedness associated with this property.

4. On January 15, 2014, R. E. Fogler, a major investment adviser, issued a negative report on Scornick's long-term prospects. The market price of Scornick's common stock subsequently declined by 40 percent.

5. At its January 5, 2014, meeting, Scornick's board of directors voted to increase substantially the advertising budget for the coming year and authorized a change in advertising agencies.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

13

What four major categories of events or conditions may indicate going concern problems? Give two examples for each category.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

14

Arenas, an assistant accountant with the firm of Gonzales Ramirez, CPAs, is auditing the financial statements of Tech Consolidated Industries, Inc. The firm's audit program calls for the preparation of a written management representation letter.

Required:

a. In an audit of financial statements, in what circumstances is the auditor required to obtain a management representation letter? What are the purposes of obtaining the letter?

b. To whom should the representation letter be addressed, and when should it be dated? Who should sign the letter, and what would be the effect of his or her refusal to sign the letter?

c. In what respects may an auditor's other responsibilities be relieved by obtaining a management representation letter?

(AICPA, adapted)

Required:

a. In an audit of financial statements, in what circumstances is the auditor required to obtain a management representation letter? What are the purposes of obtaining the letter?

b. To whom should the representation letter be addressed, and when should it be dated? Who should sign the letter, and what would be the effect of his or her refusal to sign the letter?

c. In what respects may an auditor's other responsibilities be relieved by obtaining a management representation letter?

(AICPA, adapted)

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

15

What items should be included in the auditor's communication with those charged with governance (i.e., the audit committee or similar group)?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

16

During the examination of the annual financial statements of Amis Manufacturing, Inc., a nonpublic company, the company's president, R. Heinrich, and Luddy, the auditor, reviewed the matters that were to be included in a written representation letter. Upon receipt of the following entity representation letter, Luddy contacted Heinrich to state that it was incomplete.

To: E. K. Luddy, CPA

In connection with your examination of the balance sheet of Amis Manufacturing, Inc., as of December 31, 2013, and the related statements of income, retained earnings, and cash flows for the year then ended, for the purpose of expressing an opinion as to whether the financial statements present fairly the financial position, results of operations, and cash flows of Amis Manufacturing, Inc., in conformity with generally accepted accounting principles, we confirm, to the best of our knowledge and belief, the following representations made to you during your examination. There were no

• Plans or intentions that may materially affect the carrying value or classification of assets and liabilities.

• Communications from regulatory agencies concerning noncompliance with, or deficiencies in, financial reporting practices.

• Agreements to repurchase assets previously sold.

• Violations or possible violations of laws or regulations whose effects should be considered for disclosure in the financial statements or as a basis for recording a loss contingency.

• Unasserted claims or assessments that our lawyer has advised are probable of assertion and must be disclosed in accordance with FASB ASC Topic 450, "Contingencies."

• Capital stock repurchase options or agreements or capital stock reserved for options, warrants, conversions, or other requirements.

• Compensating balance or other arrangements involving restrictions on cash balances.

R. Heinrich, President

Amis Manufacturing, Inc.

March 14, 2014

Required:

Identify the other matters that Heinrich's representation letter should specifically confirm.

(AICPA, adapted)

To: E. K. Luddy, CPA

In connection with your examination of the balance sheet of Amis Manufacturing, Inc., as of December 31, 2013, and the related statements of income, retained earnings, and cash flows for the year then ended, for the purpose of expressing an opinion as to whether the financial statements present fairly the financial position, results of operations, and cash flows of Amis Manufacturing, Inc., in conformity with generally accepted accounting principles, we confirm, to the best of our knowledge and belief, the following representations made to you during your examination. There were no

• Plans or intentions that may materially affect the carrying value or classification of assets and liabilities.

• Communications from regulatory agencies concerning noncompliance with, or deficiencies in, financial reporting practices.

• Agreements to repurchase assets previously sold.

• Violations or possible violations of laws or regulations whose effects should be considered for disclosure in the financial statements or as a basis for recording a loss contingency.

• Unasserted claims or assessments that our lawyer has advised are probable of assertion and must be disclosed in accordance with FASB ASC Topic 450, "Contingencies."

• Capital stock repurchase options or agreements or capital stock reserved for options, warrants, conversions, or other requirements.

• Compensating balance or other arrangements involving restrictions on cash balances.

R. Heinrich, President

Amis Manufacturing, Inc.

March 14, 2014

Required:

Identify the other matters that Heinrich's representation letter should specifically confirm.

(AICPA, adapted)

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

17

What types of events would generally require restatement of the issued financial statements? What procedures should the auditor follow when the entity refuses to cooperate and make the necessary disclosures?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

18

Items 1 through 16 represent a series of unrelated statements, questions, excerpts, and comments taken from various parts of an auditor's working paper file. Below is a list of the likely sources of the statements, questions, excerpts, and comments. Select, as the best answer for each item, the most likely source. Select only one source for each item. A source may be selected once, more than once, or not at all.

1. During our audit we discovered evidence of the company's failure to safeguard inventory from loss, damage, and misappropriation.

2. The company considers the decline in value of equity securities classified as available-for-sale to be temporary.

3. There have been no communications from regulatory agencies concerning noncompliance with or deficiencies in financial reporting practices.

4. It is our opinion that the possible liability to the company in this proceeding is nominal in amount.

5. As discussed in Note 4 to the financial statements, the company experienced a net loss for the year ended July 31, 2013, and is currently in default under substantially all of its debt agreements. In addition, on September 25, 2013, the company filed a prenegotiated voluntary petition for relief under Chapter 11 of the U.S. Bankruptcy Code. These matters raise substantial doubt about the company's ability to continue as a going concern.

6. During the year under audit, we were advised that management consulted with Gonzales Ramirez, CPAs. The purpose of this consultation was to obtain another CPA firm's opinion concerning the company's recognition of certain revenue that we believe should be deferred to future periods. Gonzales Ramirez's opinion was consistent with our opinion, so management did not recognize the revenue in the current year.

7. The company believes that all material expenditures that have been deferred to future periods will be recoverable.

8. Our use of professional judgment and the assessment of audit risk and materiality for the purpose of our audit mean that matters may have existed that would have been assessed differently by you. We make no representation as to the sufficiency or appropriateness of the information in our working papers for your purposes.

9. Indicate in the space provided below whether this information agrees with your records. If there are exceptions, please provide any information that will assist the auditor in reconciling the difference.

10. Blank checks are maintained in an unlocked cabinet along with the check-signing machine. Blank checks and the check-signing machine should be locked in separate locations to prevent the embezzlement of funds.

11. The company has insufficient expertise and controls over the selection and application of accounting policies that are in conformity with GAAP.

12. The timetable set by management to complete our audit was unreasonable considering the failure of the company's personnel to complete schedules on a timely basis and delays in providing necessary information.

13. Several employees have disabled the antivirus detection software on their PCs because the software slows the processing of data and occasionally rings false alarms. The company should obtain antivirus software that runs continuously at all system entry points and that cannot be disabled by unauthorized personnel.

14. In connection with an audit of our financial statements, please furnish to our auditors a description and evaluation of any pending or probable litigation against our company of which you are aware.

15. The company has no plans or intentions that may materially affect the carrying value or classification of assets and liabilities.

16. In planning the sampling application, was appropriate consideration given to the relationship of the sample to the assertion and to planning materiality?

List of Sources:

A. Practitioner's report on management's assertion about an entity's compliance with specified requirements.

B. Auditor's communications on significant deficiencies and material weakness.

C. Audit inquiry letter to legal counsel.

D. Lawyer's response to audit inquiry letter.

E. Audit committee's communication to the auditor.

F. Auditor's communication to those charged with governance (other than with respect to significant deficiencies and material weakness).

G. Report on the application of accounting principles.

H Auditor's engagement letter.

I. Letter for underwriters.

J. Accounts receivable confirmation request.

K. Request for bank cutoff statement.

L. Explanatory paragraph of an auditor's report on financial statements.

M. Partner's engagement review notes.

N. Management representation letter.

O. Successor auditor's communication with predecessor auditor.

P. Predecessor auditor's communication with successor auditor.

1. During our audit we discovered evidence of the company's failure to safeguard inventory from loss, damage, and misappropriation.

2. The company considers the decline in value of equity securities classified as available-for-sale to be temporary.

3. There have been no communications from regulatory agencies concerning noncompliance with or deficiencies in financial reporting practices.

4. It is our opinion that the possible liability to the company in this proceeding is nominal in amount.

5. As discussed in Note 4 to the financial statements, the company experienced a net loss for the year ended July 31, 2013, and is currently in default under substantially all of its debt agreements. In addition, on September 25, 2013, the company filed a prenegotiated voluntary petition for relief under Chapter 11 of the U.S. Bankruptcy Code. These matters raise substantial doubt about the company's ability to continue as a going concern.

6. During the year under audit, we were advised that management consulted with Gonzales Ramirez, CPAs. The purpose of this consultation was to obtain another CPA firm's opinion concerning the company's recognition of certain revenue that we believe should be deferred to future periods. Gonzales Ramirez's opinion was consistent with our opinion, so management did not recognize the revenue in the current year.

7. The company believes that all material expenditures that have been deferred to future periods will be recoverable.

8. Our use of professional judgment and the assessment of audit risk and materiality for the purpose of our audit mean that matters may have existed that would have been assessed differently by you. We make no representation as to the sufficiency or appropriateness of the information in our working papers for your purposes.

9. Indicate in the space provided below whether this information agrees with your records. If there are exceptions, please provide any information that will assist the auditor in reconciling the difference.

10. Blank checks are maintained in an unlocked cabinet along with the check-signing machine. Blank checks and the check-signing machine should be locked in separate locations to prevent the embezzlement of funds.

11. The company has insufficient expertise and controls over the selection and application of accounting policies that are in conformity with GAAP.

12. The timetable set by management to complete our audit was unreasonable considering the failure of the company's personnel to complete schedules on a timely basis and delays in providing necessary information.

13. Several employees have disabled the antivirus detection software on their PCs because the software slows the processing of data and occasionally rings false alarms. The company should obtain antivirus software that runs continuously at all system entry points and that cannot be disabled by unauthorized personnel.

14. In connection with an audit of our financial statements, please furnish to our auditors a description and evaluation of any pending or probable litigation against our company of which you are aware.

15. The company has no plans or intentions that may materially affect the carrying value or classification of assets and liabilities.

16. In planning the sampling application, was appropriate consideration given to the relationship of the sample to the assertion and to planning materiality?

List of Sources:

A. Practitioner's report on management's assertion about an entity's compliance with specified requirements.

B. Auditor's communications on significant deficiencies and material weakness.

C. Audit inquiry letter to legal counsel.

D. Lawyer's response to audit inquiry letter.

E. Audit committee's communication to the auditor.

F. Auditor's communication to those charged with governance (other than with respect to significant deficiencies and material weakness).

G. Report on the application of accounting principles.

H Auditor's engagement letter.

I. Letter for underwriters.

J. Accounts receivable confirmation request.

K. Request for bank cutoff statement.

L. Explanatory paragraph of an auditor's report on financial statements.

M. Partner's engagement review notes.

N. Management representation letter.

O. Successor auditor's communication with predecessor auditor.

P. Predecessor auditor's communication with successor auditor.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

19

An auditor would be most likely to identify a contingent liability by obtaining a(n)

A) Accounts payable confirmation.

B) Bank confirmation of the entity's cash balance.

C) Letter from the entity's general legal counsel.

D) List of subsequent cash receipts.

A) Accounts payable confirmation.

B) Bank confirmation of the entity's cash balance.

C) Letter from the entity's general legal counsel.

D) List of subsequent cash receipts.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

20

In February 2014, Ceramic Crucibles of America was notified by the state of Colorado that the state was investigating the company's Durango facility to determine if there were any violations of federal or state environmental laws. In formulating your opinion on the 2013 financial statements, you determined that, based primarily on management's representations, he investigation did not pose a serious threat to the company's financial well-being.

The company subsequently retained a local law firm to represent it in dealing with the state commission. At the end of 2013, you concluded that he action did not represent a severe threat. However, you have just received the attorney's letter, which is a little unsettling. It states:

On January 31, 2014, the U.S. Environmental Protection Agency (EPA) listed the Durango site in Durango, Colorado, on the National Priorities List under the Comprehensive Environmental Response, Compensation, and Liability Act (Superfund). The site includes property adjoining the western boundary of Ceramic Crucibles' plant in Durango and includes parts of Ceramic Crucibles' property. The EPA has listed Ceramic Crucibles as one of the three "potentially responsible parties" ("PRPs") that may be liable for the costs of investigating and cleaning up the site. The EPA has authorized $400,000 for a "Remedial Investigation and Feasibility Study" of the site, but that study will not begin until sometime later in 2014. Thus, we do not deem it possible or appropriate at this time to evaluate this matter with regard to potential liability or cost to the company.

You immediately set up a meeting with Dave Buff, Ceramic Crucibles' vice president; Ron Bonner, the company's attorney; and Margaret Osmond, an attorney who specializes in EPA-related issues. At the meeting you ascertain that

• Ceramic Crucibles bought the Durango facility from TW Industries in 2003.

• TW Industries had operated the facility as a manufacturer of ceramic tiles, and it had used lead extensively in incorporating color into the tile.

• The site has been placed on the National Priorities List ("the List") apparently because each state must have at least one site on the List. All sites on the List are rated on a composite score that reflects the relative extent of pollution. The Durango site has a rating of 8.3 compared to a rating of no less than 25 for the other sites on the List.

• The most severe lead pollution (based on toxicity) is in an area located on the other side of a levee behind Ceramic Crucibles' facilities. Although the area close to the building contains traces of lead pollution, the toxicity in this area is about 50 parts per million (ppm), compared to 19,000 ppm beyond the levee.

• Although Ceramic Crucibles used lead in coloring its crucibles until about 2005, the lead was locked into a ceramic glaze that met FDA requirements for appliances used in the preparation of food. Apparently, the acids used in determining the leaching properties of lead for EPA tests are stronger than that used by the FDA. Since 2005, Ceramic Crucibles has used leadfree mud in its crucibles.

• Affidavits taken from present and former employees of Ceramic Crucibles indicate that no wastewater has been discharged though the levee since Ceramic Crucibles acquired the property in 2003.

• The other PRPs and TW Industries are viable companies that should be in a position to meet their responsibilities resulting from any possible EPA action.

Materiality for purposes of evaluating a potential loss is $10 million to $13 million. This is based on the assumption that the loss would be deductible for income tax purposes. In that case, the loss would represent a reduction in stockholders' equity of 4.5 percent to 7.0 percent. Your best guess is that the company's exposure does not exceed that amount. Further, based on the financial strength of the company and its available lines of credit, you believe such an assessment would not result in financial distress to the company.

The creation of the Environmental Protection Agency (EPA) and that of the Comprehensive Environmental Response, Compensation, and Liability Act is a result of the increasing concern of Americans about pollution. An amendment to the act permits the EPA to perform the cleanup. The EPA has a national priorities list of several thousand sites thought to be severely damaged. The average cost of conducting remedial investigation and feasibility studies ranges from $750,000 to over $1 million, and such studies may take as long as three years. Cleanup costs can often exceed $10 million to $12 million. It is said that the current estimates of $100 billion to clean up nonfederal hazardous waste sites may be conservative.

The law requires the EPA to identify toxic waste sites and request records from PRPs. The PRPs are responsible for the cost of cleanup, but if they lack the funds, the EPA uses its funds for the cleanup. The EPA has spent $3.3 billion from its trust fund and collected only $65 million from polluters since the passage of the legislation.

Required:

a. How would this type of contingency be classified in the accounting literature, and how should it be accounted for?

b. Would the amount be material to the financial statements?

c. What additional evidence would you gather, and what kinds of representations should you require from the entity?

d. Should the investigation affect your opinion on those financial statements?

The company subsequently retained a local law firm to represent it in dealing with the state commission. At the end of 2013, you concluded that he action did not represent a severe threat. However, you have just received the attorney's letter, which is a little unsettling. It states:

On January 31, 2014, the U.S. Environmental Protection Agency (EPA) listed the Durango site in Durango, Colorado, on the National Priorities List under the Comprehensive Environmental Response, Compensation, and Liability Act (Superfund). The site includes property adjoining the western boundary of Ceramic Crucibles' plant in Durango and includes parts of Ceramic Crucibles' property. The EPA has listed Ceramic Crucibles as one of the three "potentially responsible parties" ("PRPs") that may be liable for the costs of investigating and cleaning up the site. The EPA has authorized $400,000 for a "Remedial Investigation and Feasibility Study" of the site, but that study will not begin until sometime later in 2014. Thus, we do not deem it possible or appropriate at this time to evaluate this matter with regard to potential liability or cost to the company.

You immediately set up a meeting with Dave Buff, Ceramic Crucibles' vice president; Ron Bonner, the company's attorney; and Margaret Osmond, an attorney who specializes in EPA-related issues. At the meeting you ascertain that

• Ceramic Crucibles bought the Durango facility from TW Industries in 2003.

• TW Industries had operated the facility as a manufacturer of ceramic tiles, and it had used lead extensively in incorporating color into the tile.

• The site has been placed on the National Priorities List ("the List") apparently because each state must have at least one site on the List. All sites on the List are rated on a composite score that reflects the relative extent of pollution. The Durango site has a rating of 8.3 compared to a rating of no less than 25 for the other sites on the List.

• The most severe lead pollution (based on toxicity) is in an area located on the other side of a levee behind Ceramic Crucibles' facilities. Although the area close to the building contains traces of lead pollution, the toxicity in this area is about 50 parts per million (ppm), compared to 19,000 ppm beyond the levee.

• Although Ceramic Crucibles used lead in coloring its crucibles until about 2005, the lead was locked into a ceramic glaze that met FDA requirements for appliances used in the preparation of food. Apparently, the acids used in determining the leaching properties of lead for EPA tests are stronger than that used by the FDA. Since 2005, Ceramic Crucibles has used leadfree mud in its crucibles.

• Affidavits taken from present and former employees of Ceramic Crucibles indicate that no wastewater has been discharged though the levee since Ceramic Crucibles acquired the property in 2003.

• The other PRPs and TW Industries are viable companies that should be in a position to meet their responsibilities resulting from any possible EPA action.

Materiality for purposes of evaluating a potential loss is $10 million to $13 million. This is based on the assumption that the loss would be deductible for income tax purposes. In that case, the loss would represent a reduction in stockholders' equity of 4.5 percent to 7.0 percent. Your best guess is that the company's exposure does not exceed that amount. Further, based on the financial strength of the company and its available lines of credit, you believe such an assessment would not result in financial distress to the company.

The creation of the Environmental Protection Agency (EPA) and that of the Comprehensive Environmental Response, Compensation, and Liability Act is a result of the increasing concern of Americans about pollution. An amendment to the act permits the EPA to perform the cleanup. The EPA has a national priorities list of several thousand sites thought to be severely damaged. The average cost of conducting remedial investigation and feasibility studies ranges from $750,000 to over $1 million, and such studies may take as long as three years. Cleanup costs can often exceed $10 million to $12 million. It is said that the current estimates of $100 billion to clean up nonfederal hazardous waste sites may be conservative.

The law requires the EPA to identify toxic waste sites and request records from PRPs. The PRPs are responsible for the cost of cleanup, but if they lack the funds, the EPA uses its funds for the cleanup. The EPA has spent $3.3 billion from its trust fund and collected only $65 million from polluters since the passage of the legislation.

Required:

a. How would this type of contingency be classified in the accounting literature, and how should it be accounted for?

b. Would the amount be material to the financial statements?

c. What additional evidence would you gather, and what kinds of representations should you require from the entity?

d. Should the investigation affect your opinion on those financial statements?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

21

An auditor should request that an audited entity send a letter of inquiry to those attorneys who have been consulted concerning litigation, claims, or assessments. The primary reason for this request is to provide

A) The opinion of a specialist as to whether loss contingencies are possible, probable, or remote.

B) A description of litigation, claims, and assessments that have a reasonable possibility of unfavorable outcome.

C) An objective appraisal of management's policies and procedures adopted for identifying and evaluating legal matters.

D) Corroboration of the information furnished by management concerning litigation, claims, and assessments.

A) The opinion of a specialist as to whether loss contingencies are possible, probable, or remote.

B) A description of litigation, claims, and assessments that have a reasonable possibility of unfavorable outcome.

C) An objective appraisal of management's policies and procedures adopted for identifying and evaluating legal matters.

D) Corroboration of the information furnished by management concerning litigation, claims, and assessments.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

22

Medical Products, Inc. (MPI) was created in 2011 and entered the optical equipment industry. Its made-to-order optical equipment requires large investments in research and development. To fund these needs, MPI made a public stock offering, which was completed in 2012. Although the offering was moderately successful, MPI's ambitious management is convinced that it must report a good profit this year (2013) to maintain the current market price of the stock. MPI's president recently stressed this point when he told his controller, Pam Adams, "If we don't make $1.25 million pretax this year, our stock will tank."

Adams was pleased that even after adjustments for accrued vacation pay, 2013 pretax profit was $1.35 million. However, MPI's auditors, Hammer Bammer (HB), proposed an additional adjustment for inventory valuation that would reduce this profit to $900,000. HB's proposed adjustment had been discussed during the 2012 audit.

An additional issue discussed in 2012 was MPI's failure to accrue executive vacation pay. At that time HB did not insist on the adjustment because the amount ($20,000) was not material to the 2012 results and because MPI agreed to begin accruing vacation pay in future years. The cumulative accrued executive vacation pay amounts to $300,000 and has been accrued at the end of 2013.

The inventory issue arose in 2011 when MPI purchased $450,000 of specialized computer components to be used with its optical scanners for a special order. The order was subsequently canceled, and HB proposed to write down this inventory in 2012. MPI explained, however, that the components could easily be sold without a loss during 2013, and no adjustment was made. However, the equipment was not sold by the end of 2013, and prospects for future sales were considered nonexistent. HB proposed a write-off of the entire $450,000 in 2013.

The audit partner, Johanna Schmidt, insisted that Adams make the inventory adjustment. Adams tried to convince her that there were other alternatives, but Schmidt was adamant. Adams knew the inventory was worthless, but she reminded Schmidt of the importance of this year's reported income. Adams continued her argument, "You can't take both the write-down and the vacation accrual in one year; it doesn't fairly present our performance this year. If you insist on taking that write-down, I'm taking back the accrual. Actually, that's a good idea because the executives are such workaholics, they don't take their vacations anyway."

As Adams calmed down, she said, "Johanna, let's be reasonable; we like you-and we want to continue our good working relationship with your firm into the future. But we won't have a future unless we put off this accrual for another year."

Required:

a. Should the inventory adjustment be made in the 2013 financial statements?

b. Irrespective of your decision regarding the inventory adjustment, what is your reaction to Adams' suggestion to release the vacation accrual? Should the auditor insist on keeping the accrual of the executives' vacation pay?

c. Consider the conflict between Adams and Schmidt. Assuming that Schmidt believes the inventory adjustment and vacation pay accrual must be made and that she does not want to lose the audit fee from the MPI audit, what should she do?

Adams was pleased that even after adjustments for accrued vacation pay, 2013 pretax profit was $1.35 million. However, MPI's auditors, Hammer Bammer (HB), proposed an additional adjustment for inventory valuation that would reduce this profit to $900,000. HB's proposed adjustment had been discussed during the 2012 audit.

An additional issue discussed in 2012 was MPI's failure to accrue executive vacation pay. At that time HB did not insist on the adjustment because the amount ($20,000) was not material to the 2012 results and because MPI agreed to begin accruing vacation pay in future years. The cumulative accrued executive vacation pay amounts to $300,000 and has been accrued at the end of 2013.

The inventory issue arose in 2011 when MPI purchased $450,000 of specialized computer components to be used with its optical scanners for a special order. The order was subsequently canceled, and HB proposed to write down this inventory in 2012. MPI explained, however, that the components could easily be sold without a loss during 2013, and no adjustment was made. However, the equipment was not sold by the end of 2013, and prospects for future sales were considered nonexistent. HB proposed a write-off of the entire $450,000 in 2013.

The audit partner, Johanna Schmidt, insisted that Adams make the inventory adjustment. Adams tried to convince her that there were other alternatives, but Schmidt was adamant. Adams knew the inventory was worthless, but she reminded Schmidt of the importance of this year's reported income. Adams continued her argument, "You can't take both the write-down and the vacation accrual in one year; it doesn't fairly present our performance this year. If you insist on taking that write-down, I'm taking back the accrual. Actually, that's a good idea because the executives are such workaholics, they don't take their vacations anyway."

As Adams calmed down, she said, "Johanna, let's be reasonable; we like you-and we want to continue our good working relationship with your firm into the future. But we won't have a future unless we put off this accrual for another year."

Required:

a. Should the inventory adjustment be made in the 2013 financial statements?

b. Irrespective of your decision regarding the inventory adjustment, what is your reaction to Adams' suggestion to release the vacation accrual? Should the auditor insist on keeping the accrual of the executives' vacation pay?

c. Consider the conflict between Adams and Schmidt. Assuming that Schmidt believes the inventory adjustment and vacation pay accrual must be made and that she does not want to lose the audit fee from the MPI audit, what should she do?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

23

An auditor issued an audit report that was dual dated for a subsequent event occurring after the date on which the auditor has obtained sufficient appropriate audit evidence but before issuance of the financial statements. The auditor's responsibility for events occurring subsequent to the date on which the auditor has obtained sufficient appropriate audit evidence was

A) Limited to the specific event referenced.

B) Extended to include all events occurring since the date on which the auditor has obtained sufficient appropriate audit evidence.

C) Extended to subsequent events occurring through the date of issuance of the report.

D) Limited to events occurring up to the date of the last subsequent event referenced.

A) Limited to the specific event referenced.

B) Extended to include all events occurring since the date on which the auditor has obtained sufficient appropriate audit evidence.

C) Extended to subsequent events occurring through the date of issuance of the report.

D) Limited to events occurring up to the date of the last subsequent event referenced.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

24

Wyly Waste Management. Wyly Waste Management ("WWM") is an SEC registrant and your firm is its auditor. Overall materiality for the audit is $100,000. Shortly after the end of the year, WWM's CFO is meeting with your audit partner to review the preliminary results of the audit. The engagement partner presents a copy of the draft unadjusted error summary to the CFO, which contains one error. During the year, WWM did not capitalize individual expenditures of less than $10,000, which is in accordance with its company policy. In the past, WWM's capital expenditures have been relatively constant each period and the expensing of the items has not caused any material errors. In the prior two years, the expensed items totaled $7,500 and $5,000, respectively. However, in the current year, WWM undertook significant development of a new waste disposal plant. As a result, WWM incurred eight capital expenditures of less than $10,000 each that were not capitalized. These purchases totaled $75,000.

Required:

a. Should your partner require WWM to record an adjustment for the expensed items in the current year?

b. Suppose the facts were changed and the expensed items for the prior two years totaled $22,500 and $15,000, respectively. Should your partner require WWM to record an adjustment for the expensed items in the current year?

c. Given the facts as presented in (b), above, how much of an adjustment should the auditor require before being willing to issue an unqualified audit opinion?

Required:

a. Should your partner require WWM to record an adjustment for the expensed items in the current year?

b. Suppose the facts were changed and the expensed items for the prior two years totaled $22,500 and $15,000, respectively. Should your partner require WWM to record an adjustment for the expensed items in the current year?

c. Given the facts as presented in (b), above, how much of an adjustment should the auditor require before being willing to issue an unqualified audit opinion?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following procedures would an auditor most likely perform to obtain evidence about the occurrence of any changes in internal control that might affect financial reporting between the end of the reporting period and the date of the auditor's report?

A) Review a fire insurance settlement during the subsequent period.

B) Examine relevant internal audit reports issued during the subsequent period.

C) Inquire of the entity's legal counsel concerning litigation, claims, and assessments arising after year-end.

D) Confirm bank accounts established after year-end.

A) Review a fire insurance settlement during the subsequent period.

B) Examine relevant internal audit reports issued during the subsequent period.

C) Inquire of the entity's legal counsel concerning litigation, claims, and assessments arising after year-end.

D) Confirm bank accounts established after year-end.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

26

A number of companies have pending lawsuits or other contingent liabilities reported in their financial statements.

Required:

a. Search the EDGAR database found at http://www.sec.gov/edgar/searchedgar/companysearch.html to find a company's 10-K that reports a contingent liability. Write a paragraph summarizing one of the liabilities found in the financial statements. Did the company disclose the liability in the footnotes only, or did it recognize the liability in the financial statements?

b. What procedures might the auditors use to search for the contingent liabilities listed in part (a)?

Required:

a. Search the EDGAR database found at http://www.sec.gov/edgar/searchedgar/companysearch.html to find a company's 10-K that reports a contingent liability. Write a paragraph summarizing one of the liabilities found in the financial statements. Did the company disclose the liability in the footnotes only, or did it recognize the liability in the financial statements?

b. What procedures might the auditors use to search for the contingent liabilities listed in part (a)?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

27

Define what is meant by contingent liability. What three categories are used to classify a contingent liability? Give four examples of a contingent liability.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

28

Final analytical procedures are generally intended to

A) Provide the auditor with a final, overall evaluation of the relationships among financial statement balances.

B) Test transactions to corroborate management's financial statement assertions.

C) Gather evidence concerning account balances that have not yet been investigated.

D) Retest control activities that appeared to be ineffective during the assessment of control risk.

A) Provide the auditor with a final, overall evaluation of the relationships among financial statement balances.

B) Test transactions to corroborate management's financial statement assertions.

C) Gather evidence concerning account balances that have not yet been investigated.

D) Retest control activities that appeared to be ineffective during the assessment of control risk.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

29

Over the past 10 years it has become quite common for an accounting firm to withdraw its opinion on a set of previously issued financial statements. Search the Internet to find a recent example of a company that has had to restate its financials and whose public accounting firm has withdrawn its opinion. Write a brief description of the reason for which the entity's financial statements were restated, and write down the wording that the accounting firm used to indicate that its audit opinion was withdrawn.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

30

What information does the auditor ask the attorney to provide on pending or threatened litigation?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following audit procedures is most likely to assist an auditor in identifying conditions and events that may indicate substantial doubt about an entity's ability to continue as a going concern?

A) Review compliance with the terms of debt agreements.

B) Review management's plans to dispose of assets.

C) Evaluate management's plans to borrow money or restructure debt.

D) Consider management's plans to reduce or delay expenditures.

A) Review compliance with the terms of debt agreements.

B) Review management's plans to dispose of assets.

C) Evaluate management's plans to borrow money or restructure debt.

D) Consider management's plans to reduce or delay expenditures.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

32

Provide two examples of commitments. Under what conditions do such commitments result in a decrease in Other Comprehensive Income?

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

33

Auditing standards primarily encourage which of the following conversations about financial reporting?

A) A conversation with those charged with governance to discuss matters pertaining to financial reporting.

B) A conversation with only management to discuss matters pertaining to financial reporting.

C) A conversation with the head of the entity's internal audit department and those charged with governance to discuss matters pertaining to financial reporting.

D) A conversation in which those charged with governance report on management's views on matters pertaining to financial reporting.

A) A conversation with those charged with governance to discuss matters pertaining to financial reporting.

B) A conversation with only management to discuss matters pertaining to financial reporting.

C) A conversation with the head of the entity's internal audit department and those charged with governance to discuss matters pertaining to financial reporting.

D) A conversation in which those charged with governance report on management's views on matters pertaining to financial reporting.

Unlock Deck

Unlock for access to all 33 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 33 flashcards in this deck.