Deck 1: The Nature of Fraud

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

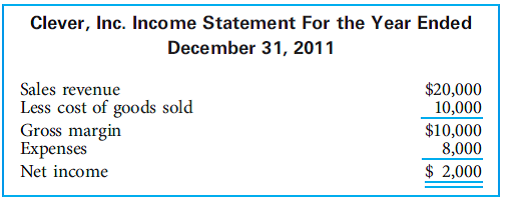

Clever, Inc., is a car manufacturer. Its 2011 income statement is as follows:

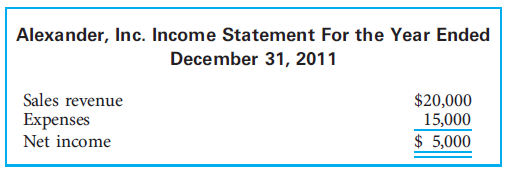

Alexander, Inc., is a car rental agency based in Florida. Its 2011 income statement is as follows:

During 2011, both Clever, Inc., and Alexander, Inc., incurred a $1,000 fraud loss.

1. How much additional revenue must each company generate to recover the losses from the fraud

2. Why are these amounts different

3. Which company will probably have to generate less revenue to recover the losses

Alexander, Inc., is a car rental agency based in Florida. Its 2011 income statement is as follows:

During 2011, both Clever, Inc., and Alexander, Inc., incurred a $1,000 fraud loss.

1. How much additional revenue must each company generate to recover the losses from the fraud

2. Why are these amounts different

3. Which company will probably have to generate less revenue to recover the losses

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/88

Play

Full screen (f)

Deck 1: The Nature of Fraud

1

Fraud is considered to be:

A) A serious problem that continues to grow.

B) A problem that affects very few individuals.

C) A mild problem that most businesses need not worry about.

D) A problem under control.

A) A serious problem that continues to grow.

B) A problem that affects very few individuals.

C) A mild problem that most businesses need not worry about.

D) A problem under control.

Selecting the correct option among four:

Explanation:

Option (a) is correct because fraud is a serious problem and the number of frauds committed. The total dollar amounts lost to fraud is increasing hugely.

Nowadays, through computer and internet it is easy for the perpetrators to cheat his/her employers only by misdirecting the purchase invoices.

They can induce the suppliers. Operating a computer program in a wrong way is another type of attempts taken by the perpetrators.

That is why option

is correct.

is correct.

• Fraud is a serious problem and affects a large number of individuals or company/organization. That is why option (b) is incorrect.

• Fraud is not a mild problem and the businesses should take this seriously. Employees can cheat the employers of any organization by taking their property, money, or assets. That is why option (c) is incorrect.

• Fraud is not under control. Sometimes especially when this is committed through internet or computers, this is not easy to detect the perpetrator. That is why option (d) is incorrect.

Explanation:

Option (a) is correct because fraud is a serious problem and the number of frauds committed. The total dollar amounts lost to fraud is increasing hugely.

Nowadays, through computer and internet it is easy for the perpetrators to cheat his/her employers only by misdirecting the purchase invoices.

They can induce the suppliers. Operating a computer program in a wrong way is another type of attempts taken by the perpetrators.

That is why option

is correct.• Fraud is a serious problem and affects a large number of individuals or company/organization. That is why option (b) is incorrect.

• Fraud is not a mild problem and the businesses should take this seriously. Employees can cheat the employers of any organization by taking their property, money, or assets. That is why option (c) is incorrect.

• Fraud is not under control. Sometimes especially when this is committed through internet or computers, this is not easy to detect the perpetrator. That is why option (d) is incorrect.

2

Investment scams most often include:

A) An action by top management against employees.

B) Worthless investments or assets sold to unsuspecting investors.

C) An overcharge for purchased goods.

D) Nonpayment of invoices for goods purchased by customers.

A) An action by top management against employees.

B) Worthless investments or assets sold to unsuspecting investors.

C) An overcharge for purchased goods.

D) Nonpayment of invoices for goods purchased by customers.

Finding the correct option among four:

Explanation:

In investment fraud, the fraud is committed on the internet where useless funds are sold to innocent investors.

In telemarketing, the confidence of the individual is gained to get them to invest money in useless scheme.

That is why option

is correct.

is correct.

• In management fraud, which is often known as financial statement fraud, the top management is involved in the process. That is why option (a) is incorrect.

• Overcharged for purchased goods occurred in vendor fraud. Here the perpetrator is the organization's vendors and the victim is the organization itself where the vendor sells goods. The purchased goods are charged quite high and the vendors deliver inferior goods. Even sometimes, they do not deliver goods for which the payments are already done. That is why option (c) is incorrect.

• In customer fraud, the customers do not pay for the purchased goods. That is why option (d) is incorrect.

Explanation:

In investment fraud, the fraud is committed on the internet where useless funds are sold to innocent investors.

In telemarketing, the confidence of the individual is gained to get them to invest money in useless scheme.

That is why option

is correct.• In management fraud, which is often known as financial statement fraud, the top management is involved in the process. That is why option (a) is incorrect.

• Overcharged for purchased goods occurred in vendor fraud. Here the perpetrator is the organization's vendors and the victim is the organization itself where the vendor sells goods. The purchased goods are charged quite high and the vendors deliver inferior goods. Even sometimes, they do not deliver goods for which the payments are already done. That is why option (c) is incorrect.

• In customer fraud, the customers do not pay for the purchased goods. That is why option (d) is incorrect.

3

Which of the following is the least reliable resource for fraud statistics

A) FBI agencies.

B) Health agencies.

C) Insurance organizations.

D) Fraud perpetrators.

A) FBI agencies.

B) Health agencies.

C) Insurance organizations.

D) Fraud perpetrators.

Finding the correct option among four:

Explanation:

The persons who commit the fraud are called the perpetrator. Therefore, this is not possible for the perpetrators to be a reliable source for fraud statistics because they will not confess their job by themselves.

That is why option

is correct.

is correct.

• FBI agencies and health agencies issue the statistic of fraud timely. All the information they provide are straightly associated to their jurisdiction. The scenario of fraud is incomplete because the information is insufficient. That is why options (a) and (b) are incorrect.

• The insurance companies provide the information about loyalty bonding or coverage against employee and other fraud. This information is gathered after investigating the fraud and fraud statistics are established. This is why option (d) is incorrect.

Option (d) is correct because the study of fraud examination is very interesting. This study is important in every part of any career. Financial consultants will be better prepared to help their clients by avoiding high-risk and false investments. Document examination and evidence-gathering skills are important for an auditor. For every possible profession, interviewing skill is very important for any fresher. That is why option

is correct.

is correct.

Explanation:

The persons who commit the fraud are called the perpetrator. Therefore, this is not possible for the perpetrators to be a reliable source for fraud statistics because they will not confess their job by themselves.

That is why option

is correct.• FBI agencies and health agencies issue the statistic of fraud timely. All the information they provide are straightly associated to their jurisdiction. The scenario of fraud is incomplete because the information is insufficient. That is why options (a) and (b) are incorrect.

• The insurance companies provide the information about loyalty bonding or coverage against employee and other fraud. This information is gathered after investigating the fraud and fraud statistics are established. This is why option (d) is incorrect.

Option (d) is correct because the study of fraud examination is very interesting. This study is important in every part of any career. Financial consultants will be better prepared to help their clients by avoiding high-risk and false investments. Document examination and evidence-gathering skills are important for an auditor. For every possible profession, interviewing skill is very important for any fresher. That is why option

is correct. 4

What is the most important element in successful fraud schemes

A) Promised benefits.

B) Confidence in the perpetrator.

C) Profitable activities.

D) Complexity.

A) Promised benefits.

B) Confidence in the perpetrator.

C) Profitable activities.

D) Complexity.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

5

"Deceptive manipulation of financial statements" describes which kind of fraud

A) Management fraud.

B) Criminal fraud.

C) Stock market fraud.

D) Bookkeeping fraud.

A) Management fraud.

B) Criminal fraud.

C) Stock market fraud.

D) Bookkeeping fraud.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

6

One of the most common responses to fraud is disbelief by those around the fraud.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

7

When perpetrators are criminally convicted of fraud, they often serve jail sentences and/or pay fines.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

8

In civil cases, fraud experts are rarely used as expert witnesses.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

9

Fraud losses generally reduce a firm's income on a dollar-for-dollar basis.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

10

A negative outcome in a civil lawsuit usually results in jail time for the perpetrator.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

11

Fellow students in your fraud examination class are having a hard time understanding why statistics on fraud are so difficult to obtain. What would you say to enlighten them

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

12

After receiving an anonymous note indicating fraudulent activities in the company, XYZ Company officials discover that an employee has embezzled a total of $50,000 over the past year. Unfortunately, this employee used an assumed identity and has suddenly disappeared. The CFO at XYZ wants to know how badly this fraud has hurt the company. If XYZ has a profit margin of 7 percent, approximately how much additional revenue will XYZ have to generate to cover the loss

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

13

Bob, who works as a credit manager for a large bank, has a reputation for being a very hard worker. His convenient downtown apartment is located near the bank, which allows him to work undisturbed late into the night. Everyone knows that Bob loves his job because he has been with the bank for many years and hardly ever takes a vacation. He is a very strict credit manager and has the reputation for asking very difficult questions to loan applicants before approving any credit.

Nancy, Bob's director, noticed that Bob had not taken a mandatory week-long vacation for a number of years. Given Bob's history of being tough on approving credit for the bank, should Nancy be concerned

Nancy, Bob's director, noticed that Bob had not taken a mandatory week-long vacation for a number of years. Given Bob's history of being tough on approving credit for the bank, should Nancy be concerned

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following characters is least likely to be involved in a fraud

A) A middle-aged person with a middle management position.

B) A long-haired teenager wearing leather pants.

C) A recent college graduate.

D) A senior executive who has significant stock options.

A) A middle-aged person with a middle management position.

B) A long-haired teenager wearing leather pants.

C) A recent college graduate.

D) A senior executive who has significant stock options.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following is required to become a CFE

A) An individual must commit to abide by a strict code of professional conduct and ethics.

B) Be an associate member, in good standing, of the ACFE.

C) Be of high moral character.

D) All of the above are required to become a CFE.

A) An individual must commit to abide by a strict code of professional conduct and ethics.

B) Be an associate member, in good standing, of the ACFE.

C) Be of high moral character.

D) All of the above are required to become a CFE.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

16

Clever, Inc., is a car manufacturer. Its 2011 income statement is as follows:

Alexander, Inc., is a car rental agency based in Florida. Its 2011 income statement is as follows:

During 2011, both Clever, Inc., and Alexander, Inc., incurred a $1,000 fraud loss.

1. How much additional revenue must each company generate to recover the losses from the fraud

2. Why are these amounts different

3. Which company will probably have to generate less revenue to recover the losses

Alexander, Inc., is a car rental agency based in Florida. Its 2011 income statement is as follows:

During 2011, both Clever, Inc., and Alexander, Inc., incurred a $1,000 fraud loss.

1. How much additional revenue must each company generate to recover the losses from the fraud

2. Why are these amounts different

3. Which company will probably have to generate less revenue to recover the losses

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

17

What is the difference between civil and criminal laws

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

18

How do employee fraud and management fraud differ

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

19

Why does it usually require trust for someone to be able to commit a fraud

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

20

The single most critical element for a fraud to be successful is opportunity.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

21

When fraud is committed, criminal prosecution usually proceeds first.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

22

Gus Jackson was hired away from a "Big Four" public accounting firm to start a new internal audit function for ABC Company, a newly acquired subsidiary of a large organization. His first task involved getting to know ABC's management and supporting the public accountants in their year-end audit work. Once the year-end work was finished, Gus started an audit of the accounts payable function. Jane Ramon, who had worked on the parent company's internal audit staff for about four years, supported him in this activity.

The accounts payable audit went smoothly, although many employees made no effort to conceal their hostility and resentment toward anyone associated with the new parent company. One exception was Hank Duckworth, the accounts payable manager. Hank was extremely helpful and complimentary of the professional approach used by the auditors. Gus had actually met Hank four years earlier, when Hank had been an accounting supervisor for an audit client where Gus was the junior accountant.

As the audit neared completion, Gus reviewed an audit comment Jane had written-a statement concerning some accounts payable checks that lacked complete endorsement by the payees. Both Gus and Jane recognized that in some situations and in some organizations less-than-perfect endorsements were not a critical concern; but these checks were payable to dual payees, and the endorsement of each payee was required. Gus asked Jane to make some photocopies of the examples so the evidence would be available for the audit closeout meeting with management.

Jane returned 20 minutes later with a puzzled expression. "I pulled the examples," she said, "but look at these!" Jane placed five checks on the desk in front of Gus. "What do you make of these " she asked.

"Make of what " asked Gus.

"Don't you see it The handwriting on all the endorsements looks the same, even though the names are different! And these are manual checks, which in this system usually means they were pushed through the system as rush payments."

"They do look similar," Gus replied, "but a lot of people have similar handwriting."

It hit Jane and Gus at the same time. All five checks had been cashed at the same convenience store less than five miles from the home office, even though the mailing address of the payee on one of the checks was over 200 miles away!

Jane decided to pull the supporting documentation for the payments but found there was none! She then identified other payments to the same payees and retrieved the paid checks. The endorsements did not look at all like the endorsements on the suspicious checks. To determine which of the endorsements were authentic, Jane located other examples of the payees' signatures in the lease, correspondence, and personnel files. The checks with supporting documentation matched other signatures on file for the payees.

Gus and Jane decided to assess the extent of the problem while investigating quietly. They wanted to avoid prematurely alerting perpetrators or management that an investigation was underway. With the help of other internal auditors from the parent company, they worked after normal business hours and reviewed endorsements on 60,000 paid checks in three nights. Ninety-five checks that had been cashed at the convenience store were identified.

Still, all Gus and Jane had were suspicions-no proof. They decided to alert executive management at the subsidiary and get their help for their next step.

The Follow-Through

Since the subsidiary had little experience with dishonest and fraudulent activity, it had no formalized approach or written fraud policy. Gus and Jane, therefore, maintained control of the investigation all the way to conclusion. With the help of operating management, the auditors contacted carefully selected payees. As is often the case involving fictitious payments to real payees, the real payees had no knowledge of the payments and had no money due to them. The auditors obtained affidavits of forgery.

In order to identify the perpetrator, the auditors documented the processing inmore detail than had been done in the original preliminary survey for the routine audit. There were seven people who had access, opportunity, and knowledge to commit the fraud. The auditors then prepared a personnel spreadsheet detailing information about every employee in the department. The spreadsheet revealed that one employee had evidence of severe financial problems in his personnel file. It also showed that Hank Duckworth's former residence was three blocks from the convenience store.

Armed with the affidavits of forgery, the auditors advised management that the case was no longer merely based on suspicions. Along with members of operating management, the auditors confronted the convenience store owners to learn why they had cashed the checks, and who had cashed them.

The convenience store manager had a ready answer. "We cash those for Hank Duckworth. He brings in several checks a month to be cashed. He used to live down the street. Never had one of those checks come back!"

The rest is history. Hank was confronted and confessed. The fully documented case was turned over to law enforcement. Hank pled guilty and received a probated sentence in return for full restitution, which he paid.

Questions

1. What clues caused Jane to suspect that fraud was involved

2. Why is it important for fraud examiners to follow up on even the smallest inconsistencies

3. In an attempt to identify possible suspects, the auditors researched the personal files of every employee in the department. What things might they have been looking for to help them identify possible suspects

The accounts payable audit went smoothly, although many employees made no effort to conceal their hostility and resentment toward anyone associated with the new parent company. One exception was Hank Duckworth, the accounts payable manager. Hank was extremely helpful and complimentary of the professional approach used by the auditors. Gus had actually met Hank four years earlier, when Hank had been an accounting supervisor for an audit client where Gus was the junior accountant.

As the audit neared completion, Gus reviewed an audit comment Jane had written-a statement concerning some accounts payable checks that lacked complete endorsement by the payees. Both Gus and Jane recognized that in some situations and in some organizations less-than-perfect endorsements were not a critical concern; but these checks were payable to dual payees, and the endorsement of each payee was required. Gus asked Jane to make some photocopies of the examples so the evidence would be available for the audit closeout meeting with management.

Jane returned 20 minutes later with a puzzled expression. "I pulled the examples," she said, "but look at these!" Jane placed five checks on the desk in front of Gus. "What do you make of these " she asked.

"Make of what " asked Gus.

"Don't you see it The handwriting on all the endorsements looks the same, even though the names are different! And these are manual checks, which in this system usually means they were pushed through the system as rush payments."

"They do look similar," Gus replied, "but a lot of people have similar handwriting."

It hit Jane and Gus at the same time. All five checks had been cashed at the same convenience store less than five miles from the home office, even though the mailing address of the payee on one of the checks was over 200 miles away!

Jane decided to pull the supporting documentation for the payments but found there was none! She then identified other payments to the same payees and retrieved the paid checks. The endorsements did not look at all like the endorsements on the suspicious checks. To determine which of the endorsements were authentic, Jane located other examples of the payees' signatures in the lease, correspondence, and personnel files. The checks with supporting documentation matched other signatures on file for the payees.

Gus and Jane decided to assess the extent of the problem while investigating quietly. They wanted to avoid prematurely alerting perpetrators or management that an investigation was underway. With the help of other internal auditors from the parent company, they worked after normal business hours and reviewed endorsements on 60,000 paid checks in three nights. Ninety-five checks that had been cashed at the convenience store were identified.

Still, all Gus and Jane had were suspicions-no proof. They decided to alert executive management at the subsidiary and get their help for their next step.

The Follow-Through

Since the subsidiary had little experience with dishonest and fraudulent activity, it had no formalized approach or written fraud policy. Gus and Jane, therefore, maintained control of the investigation all the way to conclusion. With the help of operating management, the auditors contacted carefully selected payees. As is often the case involving fictitious payments to real payees, the real payees had no knowledge of the payments and had no money due to them. The auditors obtained affidavits of forgery.

In order to identify the perpetrator, the auditors documented the processing inmore detail than had been done in the original preliminary survey for the routine audit. There were seven people who had access, opportunity, and knowledge to commit the fraud. The auditors then prepared a personnel spreadsheet detailing information about every employee in the department. The spreadsheet revealed that one employee had evidence of severe financial problems in his personnel file. It also showed that Hank Duckworth's former residence was three blocks from the convenience store.

Armed with the affidavits of forgery, the auditors advised management that the case was no longer merely based on suspicions. Along with members of operating management, the auditors confronted the convenience store owners to learn why they had cashed the checks, and who had cashed them.

The convenience store manager had a ready answer. "We cash those for Hank Duckworth. He brings in several checks a month to be cashed. He used to live down the street. Never had one of those checks come back!"

The rest is history. Hank was confronted and confessed. The fully documented case was turned over to law enforcement. Hank pled guilty and received a probated sentence in return for full restitution, which he paid.

Questions

1. What clues caused Jane to suspect that fraud was involved

2. Why is it important for fraud examiners to follow up on even the smallest inconsistencies

3. In an attempt to identify possible suspects, the auditors researched the personal files of every employee in the department. What things might they have been looking for to help them identify possible suspects

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

23

People who commit fraud are usually:

A) New employees.

B) Not well groomed and have long hair and tattoos.

C) People with strong personalities.

D) Trusted individuals.

A) New employees.

B) Not well groomed and have long hair and tattoos.

C) People with strong personalities.

D) Trusted individuals.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is not true of civil fraud

A) It usually begins when one party files a complaint.

B) The purpose is to compensate for harm done to another.

C) It must be heard by 12 jurors.

D) Only "the preponderance of the evidence" is needed for the plaintiff to be successful.

A) It usually begins when one party files a complaint.

B) The purpose is to compensate for harm done to another.

C) It must be heard by 12 jurors.

D) Only "the preponderance of the evidence" is needed for the plaintiff to be successful.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

25

Which of the following statements is true

A) Bank robberies are more costly than frauds.

B) Fraud is often labeled the fastest growing crime.

C) FBI agencies are currently spending approximately 35 percent of their time on fraudulent activities.

D) None of the above statements are true.

A) Bank robberies are more costly than frauds.

B) Fraud is often labeled the fastest growing crime.

C) FBI agencies are currently spending approximately 35 percent of their time on fraudulent activities.

D) None of the above statements are true.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following is not a fraud type

A) Direct employee embezzlement.

B) Indirect employee embezzlement.

C) Supervisor fraud.

D) Investment scams.

A) Direct employee embezzlement.

B) Indirect employee embezzlement.

C) Supervisor fraud.

D) Investment scams.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following is not true regarding the ACFE.

A) It is the largest anti-fraud organization in the world.

B) It has roughly 12,000 members throughout the world.

C) The entire organization is dedicated to antifraud- fighting efforts.

D) It is the premier provider of anti-fraud training.

A) It is the largest anti-fraud organization in the world.

B) It has roughly 12,000 members throughout the world.

C) The entire organization is dedicated to antifraud- fighting efforts.

D) It is the premier provider of anti-fraud training.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

28

What is fraud

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

29

Manufacturing companies with a profit margin of 10 percent must usually generate about 10 times as much revenue as the dollar amount of the fraud in order to restore net income to its pre-fraud level.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

30

Management fraud is deception perpetrated by an organization's top management.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

31

Many companies try to hide their losses from fraud rather than make them public.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

32

Fraud perpetrators are often those who are least suspected and most trusted.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

33

A fraudmay be perpetrated through an unintentional mistake.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

34

Why does fraud seem to be increasing at such an alarming rate

A) Computers, the Internet, and technology make fraud easier to commit.

B) Most frauds today are detected, whereas in the past many were not.

C) A new law requires that fraud be reported within 24 hours.

D) People understand the consequences of fraud to organizations.

A) Computers, the Internet, and technology make fraud easier to commit.

B) Most frauds today are detected, whereas in the past many were not.

C) A new law requires that fraud be reported within 24 hours.

D) People understand the consequences of fraud to organizations.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

35

You're telling your boyfriend about your classes for the new semester. He is very interested and intrigued by the idea of becoming a fraud detective, but wants to know whether fraud detectives will have job security and the type of work that is available. How would you respond to his questions

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

36

Your friend John works for an insurance company. John holds a business degree and has been involved in the insurance business for many years. In a recent conversation, John shares some company information with you. He has heard that the internal auditors estimate that the company has lost about $2.5 million over the last year as a result of fraud. Because you are a certified fraud examiner, John asks you how this will affect the company's profitability. John doesn't have access to the company's financial information.

1. Compute the additional revenues needed to make up for the lost money, assuming that the company has profit margins of 5, 10, and 15 percent.

2. Give examples of three types of fraud that could affect the insurance company.

3. In the case, who are the victims and who are the perpetrators

1. Compute the additional revenues needed to make up for the lost money, assuming that the company has profit margins of 5, 10, and 15 percent.

2. Give examples of three types of fraud that could affect the insurance company.

3. In the case, who are the victims and who are the perpetrators

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

37

Upon hearing that you are enrolled in a fraud class, a manager of a local business asks, "I don't understand what is happening with all these major scandals such as the Bernie Madoff scandal, the Goldman Sachs accusations, and the Enron fraud. There are billions of dollars being stolen and manipulated. How can any good auditor not notice when billions of dollars are missing " How would you respond

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is not a form of vendor fraud

A) Overcharging for purchased goods.

B) Shipment of inferior goods.

C) Nonshipment of goods even though payment has been made.

D) Not paying for goods purchased.

A) Overcharging for purchased goods.

B) Shipment of inferior goods.

C) Nonshipment of goods even though payment has been made.

D) Not paying for goods purchased.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

39

It is most often people who are not trusted that commit fraud.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

40

All frauds that are detected by organizations are made public.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

41

For each of the following, indicate whether it is a characteristic of a civil or a criminal case:

a. Jury may consist of fewer than 12 jurors.

b. Verdict must be unanimous.

c. Multiple claims may be joined in one action.

d. "Beyond a reasonable doubt."

e. Purpose is to right a public wrong.

f. Purpose is to obtain remedy.

g. Consequences of jail and/or fines.

h. Juries may have a less-than-unanimous verdict.

a. Jury may consist of fewer than 12 jurors.

b. Verdict must be unanimous.

c. Multiple claims may be joined in one action.

d. "Beyond a reasonable doubt."

e. Purpose is to right a public wrong.

f. Purpose is to obtain remedy.

g. Consequences of jail and/or fines.

h. Juries may have a less-than-unanimous verdict.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

42

Do you think the demand for careers in fraud prevention and detection is increasing or decreasing Why

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

43

In what ways is the Ponzi scam similar to other frauds

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

44

Unintentional errors in financial statements are a form of fraud.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

45

Management fraud is when managers intentionally deceive their employees about the potential of raises, vacations, and other perks.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

46

You are having lunch with another graduate student. During the course of your conversation, you tell your friend about your new fraud examination class. After you explain the devastating impact of fraud on businesses today, she asks you the following questions:

1. What is the difference between fraud and error

2. With all the advances in technology, why is fraud a growing problem

1. What is the difference between fraud and error

2. With all the advances in technology, why is fraud a growing problem

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

47

"The use of one's occupation for personal enrichment through the deliberate misuse or misapplication of the employing organization's resources or assets" is the definition of which of the following types of fraud

A) Employee embezzlement or occupational fraud.

B) Investment scams.

C) Management fraud.

D) Vendor fraud.

A) Employee embezzlement or occupational fraud.

B) Investment scams.

C) Management fraud.

D) Vendor fraud.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

48

Future careers in fraud will most likely be:

A) In low demand.

B) In moderate demand.

C) Low paying.

D) In high demand and financially rewarding.

A) In low demand.

B) In moderate demand.

C) Low paying.

D) In high demand and financially rewarding.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

49

Which of the following is not an element of fraud

A) False representation.

B) Accidental behavior.

C) Damage to a victim.

D) Intentional or reckless behavior.

A) False representation.

B) Accidental behavior.

C) Damage to a victim.

D) Intentional or reckless behavior.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

50

Civil law performs which of the following functions

A) Remedy for violation of private rights.

B) Remedy for violations against society as a whole.

C) Punishment for guilt "beyond reasonable doubt."

D) Monetary fines for federal damages.

A) Remedy for violation of private rights.

B) Remedy for violations against society as a whole.

C) Punishment for guilt "beyond reasonable doubt."

D) Monetary fines for federal damages.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

51

Despite intense measures meant to impede it, fraud appears to be one of the fastest growing crimes in the United States.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

52

Sweepstakes-legitimate or deceptive

Sweepstakes Company Agrees to Pay Up

A recent newspaper contained the following story:

Publishers Clearing House agreed to pay $34 million in a deal with 26 states to settle allegations the sweepstakes company employed deceptive marketing practices. The $34 million will cover customer refunds, legal expenses, and administrative cost to the states. Each state's share has yet to be determined. In the lawsuits, state attorney generals accused Publishers Clearing House of deceptive marketing for its sweepstakes promotions. The suit alleged that the company was misleading consumers by making them believe they had won prizes or would win if they bought magazines from Publishers Clearing House.

As part of the settlement, the company will no longer use phrases like "guaranteed winner." "This will in fact revolutionize the sweepstakes industry," Michigan Attorney General Jennifer Granholm stated. "We listened to the states' concerns and have agreed to responsive and significant changes that will make our promotions the clearest, most reliable and trustworthy in the industry," said Robin Smith, chairman and CEO of the Port Washington, N.Y.-based company.

Publishers Clearing House reached an $18 million settlement last August with 24 states and the District of Columbia. The states involved in the latest settlement are: Arizona, Arkansas, Colorado, Connecticut, Delaware, Florida, Indiana, Iowa, Kansas, Kentucky, Maine, Maryland, Massachusetts, Michigan, Minnesota, Missouri, New Jersey, North Carolina, Oregon, Pennsylvania, Rhode Island, Tennessee, Texas, Vermont,West Virginia, andWisconsin.

Questions

1. Based on this information, do you believe Publishers Clearing House has committed fraud

2. Why or why not

Sweepstakes Company Agrees to Pay Up

A recent newspaper contained the following story:

Publishers Clearing House agreed to pay $34 million in a deal with 26 states to settle allegations the sweepstakes company employed deceptive marketing practices. The $34 million will cover customer refunds, legal expenses, and administrative cost to the states. Each state's share has yet to be determined. In the lawsuits, state attorney generals accused Publishers Clearing House of deceptive marketing for its sweepstakes promotions. The suit alleged that the company was misleading consumers by making them believe they had won prizes or would win if they bought magazines from Publishers Clearing House.

As part of the settlement, the company will no longer use phrases like "guaranteed winner." "This will in fact revolutionize the sweepstakes industry," Michigan Attorney General Jennifer Granholm stated. "We listened to the states' concerns and have agreed to responsive and significant changes that will make our promotions the clearest, most reliable and trustworthy in the industry," said Robin Smith, chairman and CEO of the Port Washington, N.Y.-based company.

Publishers Clearing House reached an $18 million settlement last August with 24 states and the District of Columbia. The states involved in the latest settlement are: Arizona, Arkansas, Colorado, Connecticut, Delaware, Florida, Indiana, Iowa, Kansas, Kentucky, Maine, Maryland, Massachusetts, Michigan, Minnesota, Missouri, New Jersey, North Carolina, Oregon, Pennsylvania, Rhode Island, Tennessee, Texas, Vermont,West Virginia, andWisconsin.

Questions

1. Based on this information, do you believe Publishers Clearing House has committed fraud

2. Why or why not

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

53

Fraud involves using physical force to take something from someone.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

54

A Ponzi scheme is considered to be a type of investment scam.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

55

The only group/business that must report employee embezzlement is the federal government.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

56

Occupational fraud is fraud committed on behalf of an organization.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

57

The ACFE is a nonprofit organization dedicated to the prevention and dedication of fraud throughout the world.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

58

How does fraud affect individuals, consumers, and organizations

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

59

A bookkeeper in a $3 million retail company had earned the trust of her supervisor, so various functions normally reserved for management were assigned to her, including the authority to authorize and issue customer refunds. She proceeded to issue refunds to nonexistent customers and created documents with false names and addresses. She adjusted the accounting records and stole about $15,000 cash. She was caught when an auditor sent routine confirmations to customers on a mailing list and received an excessive number of "return-to-sender" replies. The investigation disclosed a telling pattern. The bookkeeper initially denied accusations but admitted the crime upon presentation of the evidence.

You are a lawyer for this retail company. Now that her fraud has been detected, would you prosecute her criminally, civilly, or both What processes would you use to try to recover the $15,000

You are a lawyer for this retail company. Now that her fraud has been detected, would you prosecute her criminally, civilly, or both What processes would you use to try to recover the $15,000

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

60

You are an accounting student at the local university pursuing your master's degree. One of your friends has been intrigued by the numerous frauds that have recently been reported in the news. This friend knows you are going to pursue a job as an auditor with a large public accounting firm, but your friend does not understand the difference between what you will be doing and what fraud examiners do. Write a paragraph that explains the difference between auditing and fraud examination.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

61

While discussing your class schedule with a friend who is an accounting major, your friend describes why she decided not to take the fraud class you are enrolled in: "With advances in audit technology and the increased digitalization of business records, fraud detection is a dying part of a financial statement audit." How would you respond

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

62

Fraud fighting can include which of the following type(s) of careers

A) Professors.

B) Lawyers.

C) CPA firms.

D) All of the above.

A) Professors.

B) Lawyers.

C) CPA firms.

D) All of the above.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

63

There is no difference between a Certified Fraud Examiner (CFE) and a Certified Public Accountant (CPA).

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

64

Which of the following is not an important element of fraud

A) Confidence.

B) Deception.

C) Trickery.

D) Intelligence.

A) Confidence.

B) Deception.

C) Trickery.

D) Intelligence.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

65

Why was Charles Ponzi so successful with his fraud scheme

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

66

Why are accurate fraud statistics hard to find

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

67

In your own words describe a CFE.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

68

Companies that commit financial statement fraud are often experiencing net losses or have profits that are significantly lower than expectations.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

69

Perpetrators use trickery, confidence, and deception to commit fraud.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

70

Corporate employee fraud-fighters:

A) Work as postal inspectors and law enforcement officials.

B) Prevent, detect, and investigate fraud within a company.

C) Are lawyers who defend and/or prosecute fraud cases.

D) None of the above.

A) Work as postal inspectors and law enforcement officials.

B) Prevent, detect, and investigate fraud within a company.

C) Are lawyers who defend and/or prosecute fraud cases.

D) None of the above.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

71

Studying fraud will help you:

A) Learn evidence-gathering skills.

B) Avoid high-risk and fraudulent activities.

C) Learn valuable interviewing skills.

D) All of the above.

A) Learn evidence-gathering skills.

B) Avoid high-risk and fraudulent activities.

C) Learn valuable interviewing skills.

D) All of the above.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

72

What is the best way to minimize fraud within an organization

A) Detection of fraud.

B) Investigation of fraudulent behavior.

C) Prevention activities.

D) Research company activities.

A) Detection of fraud.

B) Investigation of fraudulent behavior.

C) Prevention activities.

D) Research company activities.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

73

Which of the following is not an example of employee embezzlement

A) Land conservation employees stealing equipment.

B) Cashiers stealing money from the cash register.

C) Angry employees vandalizing the building with spray paint.

D) Salespeople overcharging for products and pocketing the excess cash.

A) Land conservation employees stealing equipment.

B) Cashiers stealing money from the cash register.

C) Angry employees vandalizing the building with spray paint.

D) Salespeople overcharging for products and pocketing the excess cash.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

74

For each of the following examples, identify whether the fraud is employee embezzlement, management fraud, investment scam, vendor fraud, customer fraud, or miscellaneous fraud.

1. Marcus bought a $70 basketball for only $30, simply by exchanging the price tags before purchasing the ball.

2. Craig lost $500 by investing in a multilevel marketing scam.

3. The Bank of San Felipe lost over $20,000 in 2011. One of its employees took money from a wealthy customer's account and put it into his own account. By the time the fraud was detected, the employee had spent the money and the bank was held responsible.

4. The CEO of Los Andes Real Estate was fined and sentenced to six months in prison for deceiving investors into believing that the company made a profit in 2011, when it actually lost over $150 million.

5. The government lost over $50 million in 2011 because many of its contractors and subcontractors charged for fictitious hours and equipment on a project in the Middle East.

6. A student broke into the school's computer system and changed her grade in order to be accepted into graduate school.

1. Marcus bought a $70 basketball for only $30, simply by exchanging the price tags before purchasing the ball.

2. Craig lost $500 by investing in a multilevel marketing scam.

3. The Bank of San Felipe lost over $20,000 in 2011. One of its employees took money from a wealthy customer's account and put it into his own account. By the time the fraud was detected, the employee had spent the money and the bank was held responsible.

4. The CEO of Los Andes Real Estate was fined and sentenced to six months in prison for deceiving investors into believing that the company made a profit in 2011, when it actually lost over $150 million.

5. The government lost over $50 million in 2011 because many of its contractors and subcontractors charged for fictitious hours and equipment on a project in the Middle East.

6. A student broke into the school's computer system and changed her grade in order to be accepted into graduate school.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

75

Telemarketing fraud is an example of employee embezzlement.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

76

Most people agree that fraud-related careers will be in demand in the future.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

77

Advances in technology have had no effect either on the size or frequency of fraud or on the detection or investigation of fraud.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

78

Indirect fraud occurs when a company's assets go directly into the perpetrator's pockets without the involvement of third parties.

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

79

Trading after Hours

Several years ago, Prudential Securities was charged with fraud for late trading. This was the first major brokerage house to be charged with the illegal practice of buying mutual funds after hours.

The regulators who accused Prudential Securities charged them with carrying out a large-scale, late

trading scheme that involved more than 1,212 trades that were valued at a remarkable $162.4 million. These trades were placed after hours in order to benefit favored hedge funds. The complaint did not contain information regarding any profits that were protected by the scandal.

The regulators who accused Prudential stated that Prudential should have noticed the considerable number of trades that were being placed after 4 p.m. and should have begun an internal inquiry. However, the complaint stated that Prudential possessed "no internal supervisory procedures" to detect trades placed after hours.

Market timing, often done in conjunction with late trading, involves rapid in and out trading of a mutual fund designed to take advantage of delays in marking up prices of securities in the funds. By buying before the markups and selling quickly after them, Prudential traders realized quick profits for the firm's clients at the expense of others. A group of managers and topproducing brokers were charged by the SEC and/or state in separate civil actions related to market timing. The firm denied all wrongdoing.

Normally, orders to buy funds after 4 p.m. should be filled at the price set the next day. In late trading, which is illegal, orders instead get the same day's 4 p.m. price, enabling investors to react to news a day ahead of other investors.

In order to accomplish late trading, the complaint stated that Prudential clients would engage in the following activities: Prudential clients would submit a list of potential trades to brokers before the 4 p.m. deadline by fax, e-mail, or telephone. After 4 p.m., clients notified Prudential which of the long list of trades it wished to execute. Prudential brokers would take the original order, cross out the trades the client didn't want to execute, and then forward the order to the firm's New York trading desk. The time stamp on the fax would often deceptively reflect the time it was received originally, not the time that the client confirmed the order. For example, in just one afternoon, at 4:58 p.m., Prudential's New York office executed more than 65 mutual fund trades, for a total of $12.98 million.

According to the complaint, Prudential did nothing to substantiate the orders that were received before 4 p.m. In early 2003, the brokerage firm issued a policy change requiring branch managers to initial a cover sheet for trades before faxing them to New York. Lists of trades could be received at Prudential's New York trading desk as late as 4:45 p.m. Accusations against the firm state that, "The orders were never rejected and were always executed at same-day prices."

The complaint further stated that Prudential also allowed the brokers involved in the market-timing and late-trading scheme to have dedicated wire-room personnel to execute trades. It has been suggested that the brokers compensated the wire-room employees for their efforts, by sharing year-end bonuses. The state alleges that Prudential also authorized one broker to obtain special software that gave the employee "electronic capacity to enter bulk mutual fund exchanges after 4 p.m."

Questions

1. Determine whether this case would be prosecuted as a criminal or civil offense, and state reasons to support your conclusion.

2. Who are the victims of this late-trading scheme, and what losses do they incur

Several years ago, Prudential Securities was charged with fraud for late trading. This was the first major brokerage house to be charged with the illegal practice of buying mutual funds after hours.

The regulators who accused Prudential Securities charged them with carrying out a large-scale, late

trading scheme that involved more than 1,212 trades that were valued at a remarkable $162.4 million. These trades were placed after hours in order to benefit favored hedge funds. The complaint did not contain information regarding any profits that were protected by the scandal.

The regulators who accused Prudential stated that Prudential should have noticed the considerable number of trades that were being placed after 4 p.m. and should have begun an internal inquiry. However, the complaint stated that Prudential possessed "no internal supervisory procedures" to detect trades placed after hours.

Market timing, often done in conjunction with late trading, involves rapid in and out trading of a mutual fund designed to take advantage of delays in marking up prices of securities in the funds. By buying before the markups and selling quickly after them, Prudential traders realized quick profits for the firm's clients at the expense of others. A group of managers and topproducing brokers were charged by the SEC and/or state in separate civil actions related to market timing. The firm denied all wrongdoing.

Normally, orders to buy funds after 4 p.m. should be filled at the price set the next day. In late trading, which is illegal, orders instead get the same day's 4 p.m. price, enabling investors to react to news a day ahead of other investors.

In order to accomplish late trading, the complaint stated that Prudential clients would engage in the following activities: Prudential clients would submit a list of potential trades to brokers before the 4 p.m. deadline by fax, e-mail, or telephone. After 4 p.m., clients notified Prudential which of the long list of trades it wished to execute. Prudential brokers would take the original order, cross out the trades the client didn't want to execute, and then forward the order to the firm's New York trading desk. The time stamp on the fax would often deceptively reflect the time it was received originally, not the time that the client confirmed the order. For example, in just one afternoon, at 4:58 p.m., Prudential's New York office executed more than 65 mutual fund trades, for a total of $12.98 million.

According to the complaint, Prudential did nothing to substantiate the orders that were received before 4 p.m. In early 2003, the brokerage firm issued a policy change requiring branch managers to initial a cover sheet for trades before faxing them to New York. Lists of trades could be received at Prudential's New York trading desk as late as 4:45 p.m. Accusations against the firm state that, "The orders were never rejected and were always executed at same-day prices."

The complaint further stated that Prudential also allowed the brokers involved in the market-timing and late-trading scheme to have dedicated wire-room personnel to execute trades. It has been suggested that the brokers compensated the wire-room employees for their efforts, by sharing year-end bonuses. The state alleges that Prudential also authorized one broker to obtain special software that gave the employee "electronic capacity to enter bulk mutual fund exchanges after 4 p.m."

Questions

1. Determine whether this case would be prosecuted as a criminal or civil offense, and state reasons to support your conclusion.

2. Who are the victims of this late-trading scheme, and what losses do they incur

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

80

You are a new summer intern working for a major professional services firm. During your lunch break each day, you and a fellow intern, Bob, eat at a local sandwich shop. One day, Bob's girlfriend joins you for lunch. When the bill arrives, Bob pays with a company credit card and writes the meal off as a business expense. Bob and his girlfriend continue to be "treated" to lunch for a number of days. You know Bob is well aware of a recent memo that came down from management stating casual lunches are not valid business expenses. When you ask Bob about the charges, he replies, "Hey, we're interns. Those memos don't apply to us. We can expense anything we want."

1. Is fraud being committed against the firm

2. What responsibility, if any, do you have to report the activity

1. Is fraud being committed against the firm

2. What responsibility, if any, do you have to report the activity

Unlock Deck

Unlock for access to all 88 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 88 flashcards in this deck.