Deck 14: Planning for Retirement

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/11

Play

Full screen (f)

Deck 14: Planning for Retirement

1

Comparing retirement plans. Chelsea Lombardo has just graduated from college and is considering job offers from two companies. Although the salary and insurance benefits are similar, the retirement programs are not. One firm offers a 401(k) plan that matches employee contributions with 25 cents for every dollar contributed by the employee, up to a $10,000 limit. The other has a contributory plan that allows employees to contribute up to 10 percent of their annual salary through payroll deduction and matches it dollar for dollar; this plan vests fully after five years. Because Chelsea is unfamiliar with these plans, she turns to you for help. Explain the features of each plan so that Chelsea can make an informed decision.

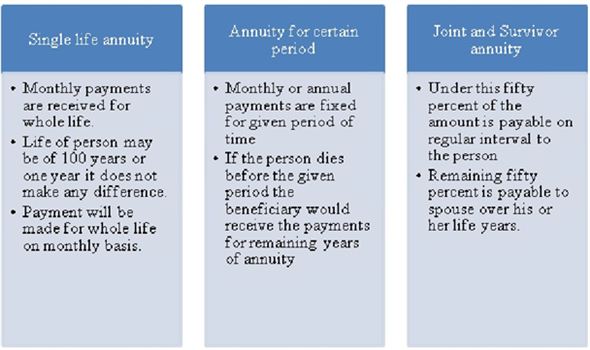

The amount might be lump sum payment or annuity payment. The annuity plan is of different types. Some of the important retirement plans are the following:

CL has just graduated and considering two job offers. The retirement plans of two companies are different. One company offers 401(k) plan under which the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. This plan has the following advantages:

CL has just graduated and considering two job offers. The retirement plans of two companies are different. One company offers 401(k) plan under which the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. This plan has the following advantages:

• Under this plan the employer also contributes. The employer contribution is four times the contribution of the employee.

• The accumulated fund earns interest.

• However, this plan creates a burden of regular deduction from the salary.

The other company offers the plan which allows employee to contribute up to 10 percent of their annual salary. The employer contributes equally. This amount is accumulated for five years and vests fully after five years. This plan carries the following advantages and disadvantages to the employee:

• The employee does not have to contribute monthly.

• There is annual deduction of 10 percent from the salary of employee.

• The amount can be withdrawn after five years.

• However, the amount of employer contribution is equal to employee contribution.

Conclusion:

401(k) plan seems to be better for her due to the following reasons:

• The amount of deduction from the salary is lesser in the case of 401(k) plan.

• The employer contribution is higher than other plan.

• The fund accumulates for the longer period.

• Hence, it is advisable for her to select the plan of 401(k) if she does not require the fund in shorter period of time (in five years).

CL has just graduated and considering two job offers. The retirement plans of two companies are different. One company offers 401(k) plan under which the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. This plan has the following advantages:• Under this plan the employer also contributes. The employer contribution is four times the contribution of the employee.

• The accumulated fund earns interest.

• However, this plan creates a burden of regular deduction from the salary.

The other company offers the plan which allows employee to contribute up to 10 percent of their annual salary. The employer contributes equally. This amount is accumulated for five years and vests fully after five years. This plan carries the following advantages and disadvantages to the employee:

• The employee does not have to contribute monthly.

• There is annual deduction of 10 percent from the salary of employee.

• The amount can be withdrawn after five years.

• However, the amount of employer contribution is equal to employee contribution.

Conclusion:

401(k) plan seems to be better for her due to the following reasons:

• The amount of deduction from the salary is lesser in the case of 401(k) plan.

• The employer contribution is higher than other plan.

• The fund accumulates for the longer period.

• Hence, it is advisable for her to select the plan of 401(k) if she does not require the fund in shorter period of time (in five years).

2

After-tax cost of 401(k) contribution. Alfonso Venegas is an operations manager for a large manufacturer. He earned $68,500 in 2015 and plans to contribute the maximum allowed to the firm's 401(k) plan. Assuming that alfonso is in the 25 percent tax bracket, calculate his taxable income and the amount of his tax savings. How much did it actually cost alfonso on an after-tax basis to make this retirement plan contribution?

Retirement planning is the planning for the retirement by the person. Retirement planning is done with the investment in annuities and purchase of several plans available in the market. The retirement plan can be selected according to the requirement of money after retirement to the individual and his or her saving capacity. The different types of retirement plans carry different benefits. The individual can select the best plan according to capacity and requirement.

AV is an operation manager for a large manufacturer. He earned $68,500 during the year 2015. He is planning to take 401(k) plan under which the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. This plan has the following advantages:

• Under this plan the employer also contributes. The employer contribution is four times the contribution of the employee.

• The accumulated fund earns interest.

• However, this plan creates a burden of regular deduction from the salary.

He is under the tax bracket of 25 percent. His total earning is $68,500. The annual limit for the year 2015-16 for deduction under 401 (k) plans is $18,000 (except for person above 50 years of age). The annual deduction of $18,000 will be reduced from his total income to get the taxable income. His income after tax will be:

Now, compute the income after tax as follows:

Now, compute the income after tax as follows:

Hence, the income after tax will be

Hence, the income after tax will be

The tax saving is the amount of tax saved on annual deduction of $18,000.

The tax saving is the amount of tax saved on annual deduction of $18,000.

Hence, the tax saving will be

Hence, the tax saving will be

Under 401(k) plan the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. Hence, the cost to AV will be only 25 percent.

Under 401(k) plan the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. Hence, the cost to AV will be only 25 percent.

AV is an operation manager for a large manufacturer. He earned $68,500 during the year 2015. He is planning to take 401(k) plan under which the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. This plan has the following advantages:

• Under this plan the employer also contributes. The employer contribution is four times the contribution of the employee.

• The accumulated fund earns interest.

• However, this plan creates a burden of regular deduction from the salary.

He is under the tax bracket of 25 percent. His total earning is $68,500. The annual limit for the year 2015-16 for deduction under 401 (k) plans is $18,000 (except for person above 50 years of age). The annual deduction of $18,000 will be reduced from his total income to get the taxable income. His income after tax will be:

Now, compute the income after tax as follows: Hence, the income after tax will be The tax saving is the amount of tax saved on annual deduction of $18,000. Hence, the tax saving will be Under 401(k) plan the employee contributes 25 cents for every dollar contributed by the employer up to $10,000. Hence, the cost to AV will be only 25 percent. 3

Deciding between traditional and Roth IRAs. Malcolm Richards is in his early 30s and is thinking about opening an IRA. He can't decide whether to open a traditional/deductible IRA or a Roth IRA, so he turns to you for help.

a. To support your explanation, you decide to run some comparative numbers on the two types of accounts; for starters, use a 25-year period to show Malcolm what contributions of $5,000 per year will amount to (after 25 years) if he can earn, say, 10 percent on his money. Will the type of account he opens have any impact on this amount? Explain.

b. Assuming that Malcolm is in the 15 percent tax bracket (and will remain there for the next 25 years), determine the annual and total (over 25 years) tax savings he'll enjoy from the $5,500-a-year contributions to his IRA. Contrast the (annual and total) tax savings he'd generate from a traditional IRA with those from a Roth IRa.c. Now, fast-forward 25 years. Given the size of Malcolm's account in 25 years (as computed in part a), assume that he takes it all out in one lump sum. If he's now in the 40 percent tax bracket, how much will he have, after taxes, with a traditional IRA as compared with a Roth IRA? How do the taxes computed here compare with those computed in part b? Comment on your findings.

d. Based on the numbers you have computed as well as any other factors, what kind of IRA would you recommend to Malcolm? Explain. Would knowing that maximum contributions are scheduled to increase to $7,000 per year make any difference in your analysis? Explain.

a. To support your explanation, you decide to run some comparative numbers on the two types of accounts; for starters, use a 25-year period to show Malcolm what contributions of $5,000 per year will amount to (after 25 years) if he can earn, say, 10 percent on his money. Will the type of account he opens have any impact on this amount? Explain.

b. Assuming that Malcolm is in the 15 percent tax bracket (and will remain there for the next 25 years), determine the annual and total (over 25 years) tax savings he'll enjoy from the $5,500-a-year contributions to his IRA. Contrast the (annual and total) tax savings he'd generate from a traditional IRA with those from a Roth IRa.c. Now, fast-forward 25 years. Given the size of Malcolm's account in 25 years (as computed in part a), assume that he takes it all out in one lump sum. If he's now in the 40 percent tax bracket, how much will he have, after taxes, with a traditional IRA as compared with a Roth IRA? How do the taxes computed here compare with those computed in part b? Comment on your findings.

d. Based on the numbers you have computed as well as any other factors, what kind of IRA would you recommend to Malcolm? Explain. Would knowing that maximum contributions are scheduled to increase to $7,000 per year make any difference in your analysis? Explain.

not answer

4

Explain the circumstances in which it make sense to convert a traditional IRA to a Roth IRa.

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

5

Explain how buying a variable annuity is much like investing in a mutual fund. Do you, as a buyer, have any control over the amount of investment risk to which you're exposed in a variable annuity contract? Explain.

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

6

Fixed vs. variable annuities. What are the main differences between fixed and variable annuities? Which type is more appropriate for someone who is 60 years old and close to retirement?

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

7

Retirement planning pitfalls. Explain the three most common pitfalls in retirement planning.

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

8

Calculating amount available at retirement. Kaitlyn tabor, a 25-year-old personal loan officer at First national Bank, understands the importance of starting early when it comes to saving for retirement. She has committed $3,000 per year for her retirement fund and assumes that she'll retire at age 65.

a. How much will she have accumulated when she turns 65 if she invests in equities and earns 8 percent on average?

b. Kaitlyn is urging her friend, Stuart Pyle, to start his plan right away, too, because he's 35. What would his nest egg amount to if he invested in the same manner as Kaitlyn and he, too, retires at age 65? Comment on your findings.

a. How much will she have accumulated when she turns 65 if she invests in equities and earns 8 percent on average?

b. Kaitlyn is urging her friend, Stuart Pyle, to start his plan right away, too, because he's 35. What would his nest egg amount to if he invested in the same manner as Kaitlyn and he, too, retires at age 65? Comment on your findings.

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

9

Calculating annual investment to meet retirement goal. Use Worksheet 14.1 to help greg and theresa Stoddard who'd like to retire while they're still relatively young-in about 20 years. Both have promising careers, and both make good money. As a result, they're willing to put aside whatever is necessary to achieve a comfortable lifestyle in retirement. Their current level of household expenditures (excluding savings) is around $75,000 a year, and they expect to spend even more in retirement; they think they'll need about 125 percent of that amount. ( Note: 125 percent equals a multiplier factor of 1.25.) They estimate that their Social Security benefits will amount to $20,000 a year in today's dollars and that they'll receive another $35,000 annually from their company pension plans. Greg and theresa feel that future inflation will amount to about 3 percent a year, and they think they'll be able to earn about 6 percent on their investments before retirement and about 4 percent afterward. Use Worksheet 14.1 to find out how big the Stoddards' investment nest egg will have to be and how much they'll have to save annually to accumulate the needed amount within the next 20 years.

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

10

Average Social Security benefits and taxes. Use Exhibit 14.2 to estimate the average Social Security benefits for a retired couple. Assume that one spouse has a part-time job that pays $24,000 a year, and that this person also receives another $47,000 a year from a company pension. Based on current policies, would this couple be liable for any tax on their Social Security income?

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

11

Retirement planning. At what age would you like to retire? Describe the type of lifestyle you envision-where you want to live, whether you want to work parttime, and so on. Discuss the steps you think you should take to realize this goal.

Unlock Deck

Unlock for access to all 11 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 11 flashcards in this deck.