Deck 14: Other Issues in Corporate Taxation

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

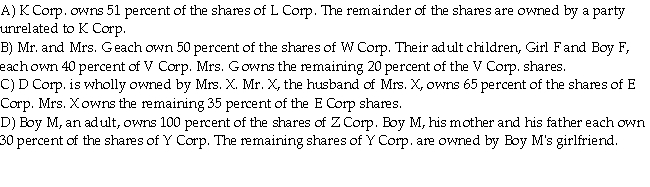

Which of the following situations does NOT describe two associated corporations?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Ambee Ltd. commenced operations in 2019, and has two separate lines of business. They are a mail order operation selling organic food products, and an operation that provides accounting services to small business. The income (loss)of the two operations for the years 2019 and 2020 are as follows:  The Company has no deductions from Net Income For Tax Purposes other than possible loss carry forwards from 2019.

The Company has no deductions from Net Income For Tax Purposes other than possible loss carry forwards from 2019.

Determine the minimum Taxable Income for each of the two years, and any loss carry forward available at the end of the year assuming that there was no acquisition of control in either year. How would your answer be different if there was an acquisition of control on January 1, 2020?

The Company has no deductions from Net Income For Tax Purposes other than possible loss carry forwards from 2019.Determine the minimum Taxable Income for each of the two years, and any loss carry forward available at the end of the year assuming that there was no acquisition of control in either year. How would your answer be different if there was an acquisition of control on January 1, 2020?

Question

Question

Question

Question

Question

During its taxation year ending December 31, 2020, all of the shares of Vick Ltd. are acquired by a new owner. The acquisition occurs on May 1, 2020 and, at that time, Vick has available a net capital loss of $175,000 [(1/2)($350,000)]. Also at that time the company has the following assets: ![During its taxation year ending December 31, 2020, all of the shares of Vick Ltd. are acquired by a new owner. The acquisition occurs on May 1, 2020 and, at that time, Vick has available a net capital loss of $175,000 [(1/2)($350,000)]. Also at that time the company has the following assets: For the period January 1, 2020 through April 30, 2020, the company has an operating loss of $143,000. Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.<div style=padding-top: 35px>](https://storage.examlex.com/TB8606/11eb9a05_65c8_464e_9571_e596ecea5dd8_TB8606_00.jpg) For the period January 1, 2020 through April 30, 2020, the company has an operating loss of $143,000.

For the period January 1, 2020 through April 30, 2020, the company has an operating loss of $143,000.

Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.

For the period January 1, 2020 through April 30, 2020, the company has an operating loss of $143,000.Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.

Question

Question

Question

Question

Question

Static Controls Inc. has a December 31 year end. On May 1, 2020, all of the Company's shares are acquired by a new owner. For the period January 1, 2020 through April 30, 2020, the Company has an operating loss of $91,000.

On April 30, 2020, the Company has available a net capital loss carry forward of $125,000 [(1/2)($250,000)]. In addition, the Company has the following assets:![Static Controls Inc. has a December 31 year end. On May 1, 2020, all of the Company's shares are acquired by a new owner. For the period January 1, 2020 through April 30, 2020, the Company has an operating loss of $91,000. On April 30, 2020, the Company has available a net capital loss carry forward of $125,000 [(1/2)($250,000)]. In addition, the Company has the following assets: Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.<div style=padding-top: 35px>](https://storage.examlex.com/TB8606/11eb9a05_65c7_f82d_9571_cfc1f252b67a_TB8606_00.jpg) Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.

Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.

On April 30, 2020, the Company has available a net capital loss carry forward of $125,000 [(1/2)($250,000)]. In addition, the Company has the following assets:

Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results. Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/96

Play

Full screen (f)

Deck 14: Other Issues in Corporate Taxation

1

When there is a winding up of a Canadian corporation, the shareholders will receive some amount of proceeds from the disposition of their shares. What are the tax consequences of receiving these proceeds?

To the extent of the PUC of the shares, the distribution will be received tax free. However, the excess of the distribution over the PUC of the shares will be treated as a deemed dividend. This deemed dividend is further subdivided as follows:

• To the extent that the corporation has a balance in its capital dividend account, part of the distribution will be considered a separate capital dividend, which will be received on a tax free basis under ITA 83(2). This treatment will only apply if an appropriate election is made.

• To the extent that the company has a pre-1972 capital surplus on hand account, the balance will be deemed not to be a dividend.

• Any remaining amount of the deemed dividend will be treated as a taxable dividend under ITA 84(2), subject to either the eligible or non-eligible dividend gross up and tax credit procedures.

• To the extent that the corporation has a balance in its capital dividend account, part of the distribution will be considered a separate capital dividend, which will be received on a tax free basis under ITA 83(2). This treatment will only apply if an appropriate election is made.

• To the extent that the company has a pre-1972 capital surplus on hand account, the balance will be deemed not to be a dividend.

• Any remaining amount of the deemed dividend will be treated as a taxable dividend under ITA 84(2), subject to either the eligible or non-eligible dividend gross up and tax credit procedures.

2

How is "group" defined by the associated corporations legislation?

ITA 256(1.2)(a)defines a group as simply two or more persons, each of whom owns shares in the corporation in question. This would include corporations, individuals, and trusts. There is no requirement that they be related.

3

For purposes of applying the associated company rules, how is control defined?

For purposes of applying the associated company rules, control is defined as follows:

Control - A corporation is deemed to be controlled by another corporation, a person, or a group of persons, if the corporation, person, or group of persons owns either:

• shares (common and/or preferred)of capital stock with a fair market value of more than 50 percent of all issued and outstanding shares of capital stock; or

• common shares with a fair market value of more than 50 percent of all issued and outstanding common shares.

Control - A corporation is deemed to be controlled by another corporation, a person, or a group of persons, if the corporation, person, or group of persons owns either:

• shares (common and/or preferred)of capital stock with a fair market value of more than 50 percent of all issued and outstanding shares of capital stock; or

• common shares with a fair market value of more than 50 percent of all issued and outstanding common shares.

4

For purposes of applying the associated company rules, there is a deeming rule with respect to the holding of rights. Briefly describe this rule.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

5

In general, investment tax credits require a taxpayer to exchange a given amount of tax deductions for the same amount of tax credits. Explain why this is favourable to the taxpayer.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

6

How is an acquisition of control defined? Describe a common event that would result in an acquisition of control.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

7

A redemption of shares may result in an ITA 84(3)deemed dividend. As the redemption is also a disposition, there may also be a capital gain. Explain how tax legislation avoids some part of the proceeds received for the shares from being double counted as both a deemed dividend and a capital gain.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

8

Indicate the types of taxpayers that are eligible for refundable investment tax credits.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

9

ITA 249(4)requires that, when there is an acquisition of control, the acquired corporation will have deemed year end on the day preceding the acquisition of control. What is the objective of this requirement?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

10

When control of a corporation is acquired, ITA 111(4)(e)permits the acquired corporation to elect to have a deemed disposition of any of its capital properties on which there is either unrealized recapture of CCA or unrealized capital gains. Under what circumstances would you advise a client to make this election? Briefly explain your conclusion.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

11

The per share value for Paid Up Capital (PUC)will often be different than the per share value for Adjusted Cost Base (ACB). Briefly explain how such differences arise.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

12

What is the basic purpose of the capital dividend account?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

13

Why does the government believe that it is necessary to have rules related to the acquisition of control of a corporation that has accumulated losses.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

14

Corporations sometimes issue new shares in order to retire existing debt. In some cases, the value of the shares issued will exceed the value of the debt retired. Describe the tax consequences that result from such a transaction.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

15

What characteristics define "shares of a specified class" under the provisions governing associated companies? What is a common designation for such shares?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

16

Why is it necessary to have the associated company rules?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

17

If the government wanted to provide additional tax benefits, how would they choose between using a general rate reduction and, alternatively, one or more investment tax credits?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

18

When a business receives an investment tax credit as the result of the acquisition of a depreciable asset, how does this affect the amount of CCA taken in the current and subsequent years?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

19

Briefly describe the basic tax consequences that result from an acquisition of control.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

20

What is a stock dividend? What are the tax consequences for an individual receiving such dividends, as well as for the corporation issuing the dividend?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

21

Any net capital losses that remain unused after an acquisition of control cannot be used in years subsequent to the acquisition of control.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

22

For purposes of determining associated companies, a group is any two or more related persons who hold shares in a corporation.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

23

Because no assets are distributed, stock dividends do not increase shareholders' Net Income For Tax Purposes.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

24

When there is an acquisition of control, any non-depreciable asset with an adjusted cost base in excess of its fair market value must be written down to its fair market value.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

25

When a corporation redeems all or part of its outstanding shares, the difference between the proceeds of redemption and the PUC of the shares will be treated as a capital gain for tax purposes.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

26

Non-refundable investment tax credits that are not used during the current year can be carried back 3 years and forward for 20 years.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following is NOT an implication of a deemed year end which creates a short fiscal period?

A)The corporate tax rate must be prorated for the shortened year.

B)CCA calculations must be based on a fraction of a year.

C)The annual business limit must be prorated.

D)The period during which time-limited losses can be used is shortened.

A)The corporate tax rate must be prorated for the shortened year.

B)CCA calculations must be based on a fraction of a year.

C)The annual business limit must be prorated.

D)The period during which time-limited losses can be used is shortened.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

28

When a deemed year end is required as the result of an acquisition of control, this event will always be followed by a short fiscal period.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

29

An individual investor's PUC per share will generally be changed if the corporation issues additional shares, despite the fact that his adjusted base per share will not be changed.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

30

VanDeKamp Holdings operates two separate lines of business - a catering business and a cookbook publishing business. During the year ended December 31, 2020, the company lost $300,000 from the catering business and earned a profit of $100,000 from the cookbook publishing business. The $200,000 non-capital loss could not be carried back, and as a result it was carried forward. On January 1, 2021, VanDeKamp Holdings is acquired by another company. During the 2021 year, the catering business lost another $150,000 while the cookbook publishing business earned $350,000. What portion of the loss carry forward can be deducted in the 2021 fiscal year?

A)None.

B)$100,000.

C)$150,000.

D)$200,000.

A)None.

B)$100,000.

C)$150,000.

D)$200,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

31

While dividends in kind are treated as a taxable dividend to the recipient shareholders, they have no tax consequences for the corporation declaring the dividend.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

32

When a business receives an investment tax credit as a result of making a capital expenditure, the amount of the credit must be deducted from the UCC of the capital expenditures class in the taxation year in which the credit is received.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

33

Capital dividends that have been declared using the ITA 83(2)election are not subject to the usual gross up and tax credit procedures.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

34

If a corporation elects to have a deemed disposition of a non-depreciable property whose fair market value is greater than its adjusted cost base prior to an acquisition of control, the elected value can be any value between the adjusted cost base and the fair market value of the property.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements with respect to acquisition of control procedures is NOT correct?

A)Prior to the deemed year end, non-depreciable assets will have to be written down to their fair market value.

B)Net capital losses cannot be carried back to a year prior to the acquisition of control.

C)Subsequent to the deemed year end, non-capital losses can be deducted against any type of income.

D)Prior to the deemed year end, the acquired company can elect to have a deemed disposition of any of their capital assets.

A)Prior to the deemed year end, non-depreciable assets will have to be written down to their fair market value.

B)Net capital losses cannot be carried back to a year prior to the acquisition of control.

C)Subsequent to the deemed year end, non-capital losses can be deducted against any type of income.

D)Prior to the deemed year end, the acquired company can elect to have a deemed disposition of any of their capital assets.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

36

Which of the following is NOT a consequence of an acquisition of control?

A)A deemed year end.

B)The inability to deduct existing non-capital losses subsequent to the acquisition of control.

C)The inability to deduct existing net capital losses subsequent to the acquisition of control.

D)A requirement to write down non-depreciable assets to their fair market value.

A)A deemed year end.

B)The inability to deduct existing non-capital losses subsequent to the acquisition of control.

C)The inability to deduct existing net capital losses subsequent to the acquisition of control.

D)A requirement to write down non-depreciable assets to their fair market value.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following items would NOT be lost when there is an acquisition of control?

A)Unused charitable donations.

B)Farm losses.

C)Allowable business investment losses.

D)Net capital losses.

A)Unused charitable donations.

B)Farm losses.

C)Allowable business investment losses.

D)Net capital losses.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

38

Which of the following is NOT a restriction that applies to the use of non-capital losses after an acquisition of control?

A)The corporation must continue to carry on the business in which the loss occurred.

B)There must be a reasonable expectation of profit in that business.

C)The losses cannot be applied in any shortened year ends that occur as a result of the acquisition of control.

D)The losses can only be applied against future income generated by the same or a similar business.

A)The corporation must continue to carry on the business in which the loss occurred.

B)There must be a reasonable expectation of profit in that business.

C)The losses cannot be applied in any shortened year ends that occur as a result of the acquisition of control.

D)The losses can only be applied against future income generated by the same or a similar business.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

39

For purposes of determining associated companies, a parent is deemed to own any of a corporation's shares that are held by any of his children who are under the age of 18.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

40

A private corporation sells a depreciable asset for $250,000. The asset had a capital cost of $200,000. The balance in its CCA Class was $1,200,000 and there were other assets in the Class. There will an addition to the capital dividend account of $50,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

41

Mira Glow Ltd. is a CCPC throughout the 2020 taxation year. For 2019, the company had Taxable Capital Employed in Canada of $14,000,000. The corresponding figure for 2020, was $15,000,000. What is the annual SR&ED expenditure limit for Mira Glow Ltd. for 2020?

A)$ 3,000,000

B)$ 2,700,000

C)$ 1,950,000

D)$ 300,000

A)$ 3,000,000

B)$ 2,700,000

C)$ 1,950,000

D)$ 300,000

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

42

Vadel Inc., a Canadian public company, has 1,000,000 shares outstanding with a total PUC of $1,750,000. Mr. Vincent Dorval owns 5,000 of these shares with an adjusted cost base of $11,250. Vadel Inc. declares a 5 percent non-eligible stock dividend at a time when its shares are trading at $2.50 per share. Which of the following statements is correct?

A)Mr. Dorval's Taxable Income will increase by $719 as a result of the dividend.

B)After the dividend, the adjusted cost base of Mr. Dorval's shares will be $11,875.

C)After the dividend, the PUC of Vadel's shares will be $1,875,000.

D)All of the above.

E)None of the above.

A)Mr. Dorval's Taxable Income will increase by $719 as a result of the dividend.

B)After the dividend, the adjusted cost base of Mr. Dorval's shares will be $11,875.

C)After the dividend, the PUC of Vadel's shares will be $1,875,000.

D)All of the above.

E)None of the above.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

43

Simon Williams owns 100 percent of Wonder Technologies Inc. Peter Maximoff owns 100 percent of Speedy Delivery Service Ltd. Simon and Peter each own 50 percent of Scarlet Decorating Ltd. Simon is married to Peter's sister, Wanda. Assuming each of the three corporations is a CCPC and has at least $500,000 of active business income earned in Canada, what is the maximum combined corporate income on which the three corporations can claim the small business deduction?

A)Nil.

B)$ 500,000.

C)$1,000,000.

D)$1,500,000.

A)Nil.

B)$ 500,000.

C)$1,000,000.

D)$1,500,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

44

Tardex Inc. has only one class of shares. At the end of 2020, the company had 30,000 shares outstanding. The shares had been sold in 3 blocks of 10,000 each. The first block was sold at $8 per share, the second at $9 per share, and the third at $11 per share. Mark Forest acquired 200 shares of the first offering and an additional 300 shares of the second offering. The total PUC of Mark's shares is equal to:

A)$4,300.

B)$4,665.

C)$4,250.

D)$5,500.

A)$4,300.

B)$4,665.

C)$4,250.

D)$5,500.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

45

Mr. Hanes owns 100 percent of the common shares of Jimbo Corp. and 40 percent of the common shares of Hughes Corp. Hughes Corp. owns 80 percent of the common shares of ARC Ltd. Mr. Hanes' daughter-in-law also owns 5 percent of the common shares of Hughes Corp., and 15 percent of the common shares of ARC Ltd. The remaining shares are held by parties who deal at arm's length with Mr. Hanes and his daughter-in-law. The following Companies are associated under ITA 256 of the Income Tax Act:

A)Only Jimbo and Hughes are associated.

B)Only Jimbo and ARC are associated

C)Hughes and ARC are associated, and Jimbo and ARC are associated.

D)Only Hughes and ARC are associated.

E)None of Jimbo Corp., Hughes Corp., and ARC Ltd. are associated.

A)Only Jimbo and Hughes are associated.

B)Only Jimbo and ARC are associated

C)Hughes and ARC are associated, and Jimbo and ARC are associated.

D)Only Hughes and ARC are associated.

E)None of Jimbo Corp., Hughes Corp., and ARC Ltd. are associated.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

46

Which of the following items would NOT be added to the capital dividend account of a private company?

A)Life insurance proceeds received.

B)Dividends received from other taxable Canadian corporations.

C)Capital dividends received from other corporations.

D)The non-taxable portion of capital gains.

A)Life insurance proceeds received.

B)Dividends received from other taxable Canadian corporations.

C)Capital dividends received from other corporations.

D)The non-taxable portion of capital gains.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

47

With respect to dividends in kind, which of the following statements is correct?

A)A dividend in kind is not subject to the usual gross up and tax credit procedures.

B)A dividend in kind will not affect the income of the declaring corporation.

C)A dividend in kind can result in a capital gain for the declaring corporation.

D)A dividend in kind can never be designated as an eligible dividend.

A)A dividend in kind is not subject to the usual gross up and tax credit procedures.

B)A dividend in kind will not affect the income of the declaring corporation.

C)A dividend in kind can result in a capital gain for the declaring corporation.

D)A dividend in kind can never be designated as an eligible dividend.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

48

When there is an acquisition of control of a corporation, which of the following is correct?

A)A capital loss arising prior to the acquisition of control may be applied against capital gains realized by the business that incurred the capital loss on assets that were held prior to the acquisition of control.

B)Any capital losses that arise subsequent to the acquisition of control will be lost.

C)Non-capital losses arising prior to the acquisition of control may be applied against income earned by the business that incurred the loss as long as the loss has not expired.

D)Non-capital losses and capital losses arising prior to the acquisition of control will beloit.

A)A capital loss arising prior to the acquisition of control may be applied against capital gains realized by the business that incurred the capital loss on assets that were held prior to the acquisition of control.

B)Any capital losses that arise subsequent to the acquisition of control will be lost.

C)Non-capital losses arising prior to the acquisition of control may be applied against income earned by the business that incurred the loss as long as the loss has not expired.

D)Non-capital losses and capital losses arising prior to the acquisition of control will beloit.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

49

Solis Enterprises Inc. operates two separate lines of business - a fashion design business and an investment firm. During the year ended December 31, 2020, the company lost $3 million from the fashion design business and earned a profit of $1 million from the investment firm. The $2 million non-capital loss could not be carried back, and as a result it was carried forward. On January 1, 2021, Solis Enterprises Inc. is acquired by another company. During the 2021 year, the fashion design business lost $1.5 million while the investment firm earned $4 million. What is the minimum taxable income for 2021?

A)Nil.

B)$500,000.

C)$2,500,000.

D)$4,000,000.

A)Nil.

B)$500,000.

C)$2,500,000.

D)$4,000,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following statements about tax based shareholders' equity is NOT correct?

A)Paid up capital is the tax equivalent of contributed capital under GAAP.

B)The capital dividend account has no equivalent balance under GAAP.

C)The per share value of PUC is the same for all shareholders of a specified class.

D)While the components may be different, retained earnings will have the same value in both tax based shareholders' equity and in GAAP based financial statements.

A)Paid up capital is the tax equivalent of contributed capital under GAAP.

B)The capital dividend account has no equivalent balance under GAAP.

C)The per share value of PUC is the same for all shareholders of a specified class.

D)While the components may be different, retained earnings will have the same value in both tax based shareholders' equity and in GAAP based financial statements.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

51

Which of the following statements with respect to stock dividends is correct?

A)Stock dividends are not subject to the usual gross up and tax credit procedures.

B)A stock dividend can never be designated as an eligible dividend.

C)A dividend will be taxable to the extent that the corporation has increased its PUC in the process of declaring the dividend.

D)When an investor receives a stock dividend, it does not affect the adjusted cost base of his shareholding.

A)Stock dividends are not subject to the usual gross up and tax credit procedures.

B)A stock dividend can never be designated as an eligible dividend.

C)A dividend will be taxable to the extent that the corporation has increased its PUC in the process of declaring the dividend.

D)When an investor receives a stock dividend, it does not affect the adjusted cost base of his shareholding.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

52

Hagrid Inc. is subject to an acquisition of control on January 1, 2021. The company has an operating loss of $65,000 in the year prior to the acquisition of control, which cannot be carried back. On December 31, 2020, the company had two assets, a piece of land with an ACB of $150,000 and fair market value of $65,000; and a depreciable asset with a capital cost of $100,000, a UCC of $75,000 and a fair market value of $200,000. Assuming Hagrid will continue in business and will return to profitability in 2021, what write downs and elections are available to Hagrid Inc. in order to optimize the amount of losses carried forward to the 2021 year?

A)Hagrid Inc. should elect to recognize the allowable capital loss of $42,500 on the land at the end of 2020. A gain on the depreciable asset must be recorded, and this would be comprised of recapture of $25,000 and a taxable capital gain of $50,000.

B)Hagrid Inc. will be required to write the land down to its fair market value and recognize the allowable capital loss of $42,500 at the end of 2020. A deemed disposition of the depreciable asset should be elected at a value of $185,000, resulting in recapture of $25,000 and a taxable capital gain of $42,500.

C)Hagrid Inc. will be required to write the land down to its fair market value and recognize the allowable capital loss of $42,500 at the end of 2020. No elections are available to the company.

D)Hagrid Inc. should elect to recognize the allowable capital loss of $42,500 on the land at the end of 2020. A deemed disposition of the depreciable asset should be elected at a value of $100,000, resulting in recapture of $25,000.

A)Hagrid Inc. should elect to recognize the allowable capital loss of $42,500 on the land at the end of 2020. A gain on the depreciable asset must be recorded, and this would be comprised of recapture of $25,000 and a taxable capital gain of $50,000.

B)Hagrid Inc. will be required to write the land down to its fair market value and recognize the allowable capital loss of $42,500 at the end of 2020. A deemed disposition of the depreciable asset should be elected at a value of $185,000, resulting in recapture of $25,000 and a taxable capital gain of $42,500.

C)Hagrid Inc. will be required to write the land down to its fair market value and recognize the allowable capital loss of $42,500 at the end of 2020. No elections are available to the company.

D)Hagrid Inc. should elect to recognize the allowable capital loss of $42,500 on the land at the end of 2020. A deemed disposition of the depreciable asset should be elected at a value of $100,000, resulting in recapture of $25,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

53

Torin Inc. has 500,000 shares issued and outstanding. These shares were issued for total consideration of $1,125,000. At a later point in time, Jane Dow acquired 1,000 of these shares at a total cost of $3,500. With respect to Ms. Dow's holding of Torin shares, which of the following statements is NOT correct?

A)The PUC of Ms. Dow's shares is $2,250.

B)The adjusted cost base of Ms. Dow's shares is $3,500.

C)If she were to sell the Torin shares for $4,000, she would have a taxable capital gain of $250.

D)If she were to sell the Torin shares for $4,000, she would have a deemed dividend of $500.

A)The PUC of Ms. Dow's shares is $2,250.

B)The adjusted cost base of Ms. Dow's shares is $3,500.

C)If she were to sell the Torin shares for $4,000, she would have a taxable capital gain of $250.

D)If she were to sell the Torin shares for $4,000, she would have a deemed dividend of $500.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

54

In which of the following situations are A Ltd. and B Ltd. associated?

A)Mrs. Jax owns 60 percent of A Ltd. and Mrs. Jax's niece owns 80 percent of B Ltd. Mrs. Jax's husband owns the other 40 percent of A Ltd. and 20 percent of B Ltd.

B)Mr. B. owns 60 percent of A Ltd. and 20 percent of B Ltd. Mrs. B,Mr. B's spouse, owns the remaining 40 percent of A Ltd. The remaining 80 percent of B Ltd. is owned equally by Mr. and Mrs. D, who are not related to Mr. and Mrs. B.

C)Amos Dans owns 35 percent of each of A Ltd. and B Ltd. Amos Dan's brother owns an additional 20 percent of A Ltd. and 30 percent of B Ltd. The remaining 45 percent of A Ltd. and 35 percent of B Ltd. are owned by XYZ Ltd. and JBC Ltd., respectively. XYZ Ltd. and JBC Ltd. are not associated companies.

D)Young Ltd. owns 55 percent of B Ltd. and 40 percent of A Ltd. Boyle Holdings Ltd. owns the remaining 45 percent of B Ltd., and Kula Holdings Ltd. owns the remaining 60 percent of A Ltd. Kula Holdings Ltd. and Boyle Holdings Ltd. are owned by L. Kula and A. Boyle, respectively, who are not related.

A)Mrs. Jax owns 60 percent of A Ltd. and Mrs. Jax's niece owns 80 percent of B Ltd. Mrs. Jax's husband owns the other 40 percent of A Ltd. and 20 percent of B Ltd.

B)Mr. B. owns 60 percent of A Ltd. and 20 percent of B Ltd. Mrs. B,Mr. B's spouse, owns the remaining 40 percent of A Ltd. The remaining 80 percent of B Ltd. is owned equally by Mr. and Mrs. D, who are not related to Mr. and Mrs. B.

C)Amos Dans owns 35 percent of each of A Ltd. and B Ltd. Amos Dan's brother owns an additional 20 percent of A Ltd. and 30 percent of B Ltd. The remaining 45 percent of A Ltd. and 35 percent of B Ltd. are owned by XYZ Ltd. and JBC Ltd., respectively. XYZ Ltd. and JBC Ltd. are not associated companies.

D)Young Ltd. owns 55 percent of B Ltd. and 40 percent of A Ltd. Boyle Holdings Ltd. owns the remaining 45 percent of B Ltd., and Kula Holdings Ltd. owns the remaining 60 percent of A Ltd. Kula Holdings Ltd. and Boyle Holdings Ltd. are owned by L. Kula and A. Boyle, respectively, who are not related.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

55

Which of the following is NOT a component of retained earnings for a CCPC from a tax perspective?

A)Post-1971 Undistributed Surplus

B)Pre-1972 Capital Surplus On Hand

C)Capital Dividend Account

D)LRIP

A)Post-1971 Undistributed Surplus

B)Pre-1972 Capital Surplus On Hand

C)Capital Dividend Account

D)LRIP

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following situations does NOT describe two associated corporations?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

57

Miracle Works Inc. is located in Newfoundland. The company hires 3 eligible apprentices, paying each of them $30,000 in the current year. It also acquires $2,000,000 in qualified depreciable property. What are the tax consequences of these transactions for the current year?

A)The company will receive investment tax credits of $206,000. CCA for the current year will be based on the addition of $2,000,000 to the CCA class of the qualified property.

B)The company will receive investment tax credits of $6,000. CCA for the current year will be based on the addition of $2,000,000 to the CCA class of the qualified property.

C)The company will receive investment tax credits of $206,000. CCA for the current year will be based on the addition of $1,800,000 to the CCA class of the qualified property.

D)The company will receive investment tax credits of $209,000. CCA for the current year will be based on the addition of $2,000,000 to the CCA class of the qualified property.

A)The company will receive investment tax credits of $206,000. CCA for the current year will be based on the addition of $2,000,000 to the CCA class of the qualified property.

B)The company will receive investment tax credits of $6,000. CCA for the current year will be based on the addition of $2,000,000 to the CCA class of the qualified property.

C)The company will receive investment tax credits of $206,000. CCA for the current year will be based on the addition of $1,800,000 to the CCA class of the qualified property.

D)The company will receive investment tax credits of $209,000. CCA for the current year will be based on the addition of $2,000,000 to the CCA class of the qualified property.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

58

Low Tech Inc. is a CCPC with 2020 SR&ED expenditures of $685,000. In 2019, the Company's Taxable Capital Employed In Canada was $7 million. Determine their total investment tax credit for 2020 and indicate the amount that would be refundable.

A)The total credit would be $239,750. The refundable amount would be $239,750.

B)The total credit would be $239,750. The refundable amount would be $102,750.

C)The total credit would be $102,750. The refundable amount would be $102,750.

D)The total credit would be $102,750. The refundable amount would be $41,100.

A)The total credit would be $239,750. The refundable amount would be $239,750.

B)The total credit would be $239,750. The refundable amount would be $102,750.

C)The total credit would be $102,750. The refundable amount would be $102,750.

D)The total credit would be $102,750. The refundable amount would be $41,100.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

59

Gains Inc. had a balance in its capital dividend account of $150,000 at January 1, 2020. During the 2020 year, the company had a taxable capital gain of $50,000, allowable capital losses of $30,000, received a capital dividend of $35,000 from a subsidiary, and paid eligible dividends of $45,000. On November 15, 2020, a capital dividend of $32,000 was paid, and the appropriate election was filed. What is the balance in the capital dividend account at December 31, 2020?

A)$128,000

B)$138,000

C)$173,000

D)$203,000

A)$128,000

B)$138,000

C)$173,000

D)$203,000

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

60

John Dough owns 100 percent of the shares of Doughboy Ltd. His wife, Kneada Dough, owns 100 percent of the shares of Yeast Ltd. and 100 percent of the shares of Flour Inc. Which of the following statements is correct?

A)Doughboy and Yeast are associated.

B)Flour and Yeast are associated.

C)Doughboy and Flour are associated.

D)Doughboy is associated with both Yeast and Flour.

A)Doughboy and Yeast are associated.

B)Flour and Yeast are associated.

C)Doughboy and Flour are associated.

D)Doughboy is associated with both Yeast and Flour.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

61

Which of the following transactions will NOT result in a deemed dividend?

A)Paying off $500,000 in debt by issuing shares with a fair market value of $525,000.

B)Redeeming shares for $350,000. The PUC of the shares was $350,000 and the adjusted cost base was $250,000.

C)A liquidating dividend is paid to shareholders in the amount of $400,000. At this time, PUC is reduced by $300,000.

D)A total of $1,000,000 was paid to shareholders as part of a winding-up. The PUC of the shares was $200,000 and there was no capital dividend account balance.

A)Paying off $500,000 in debt by issuing shares with a fair market value of $525,000.

B)Redeeming shares for $350,000. The PUC of the shares was $350,000 and the adjusted cost base was $250,000.

C)A liquidating dividend is paid to shareholders in the amount of $400,000. At this time, PUC is reduced by $300,000.

D)A total of $1,000,000 was paid to shareholders as part of a winding-up. The PUC of the shares was $200,000 and there was no capital dividend account balance.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

62

Anderson Inc., BDO Ltd., and Copper Inc., are three Canadian controlled private corporations.

The common share ownership is as follows:

Anderson Inc. - John Anderson owns 100 percent of the common shares of this Company.

BDO Ltd. - John Anderson owns 30 percent of the common shares and his spouse, Wilma Anderson, owns 10 percent of the common shares. Basil Copper owns 35 percent of the common shares and his spouse, Holly Copper, owns 25 percent of the common shares. Holly Copper is John Anderson's sister.

Copper Inc. - Basil Copper and Holly Copper each own 50 percent of the common shares of this Company.

Indicate which of the Companies described are associated. Explain your conclusions.

The common share ownership is as follows:

Anderson Inc. - John Anderson owns 100 percent of the common shares of this Company.

BDO Ltd. - John Anderson owns 30 percent of the common shares and his spouse, Wilma Anderson, owns 10 percent of the common shares. Basil Copper owns 35 percent of the common shares and his spouse, Holly Copper, owns 25 percent of the common shares. Holly Copper is John Anderson's sister.

Copper Inc. - Basil Copper and Holly Copper each own 50 percent of the common shares of this Company.

Indicate which of the Companies described are associated. Explain your conclusions.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

63

During the taxation year ending December 31, 2020, Forward Ltd. makes the following expenditures that qualify for investment tax credits:

• $1,450,000 in current expenditures for Scientific Research And Experimental Development.

• $220,000 in expenditures for Qualified Property in the Atlantic Provinces.

The Company is a CCPC with Taxable Income in 2019 of $417,000. Also for 2019, its Taxable Capital Employed in Canada was $6,200,000. The Company has no Tax Payable for 2020 or in any of the three preceding taxation years.

Determine the amount of the refund that Forward Ltd. will receive as a result of earning these investment tax credits and any available carry forwards. Include in your answer any other tax consequences of these investment tax credits.

• $1,450,000 in current expenditures for Scientific Research And Experimental Development.

• $220,000 in expenditures for Qualified Property in the Atlantic Provinces.

The Company is a CCPC with Taxable Income in 2019 of $417,000. Also for 2019, its Taxable Capital Employed in Canada was $6,200,000. The Company has no Tax Payable for 2020 or in any of the three preceding taxation years.

Determine the amount of the refund that Forward Ltd. will receive as a result of earning these investment tax credits and any available carry forwards. Include in your answer any other tax consequences of these investment tax credits.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

64

Mark is the only shareholder of Sico Ltd., a Canadian controlled private corporation. The CCPC has no balance in its GRIP account. In 2020, Sico paid a dividend in kind by distributing securities with fair market value of $72,000 and an adjusted cost base of $56,000. Which of the following statements properly reflects the tax consequences of this transaction?

A)Sico has Taxable Income of $8,000 and Mark has Taxable Income of $72,000.

B)Sico has Taxable Income of $8,000 and Mark has Taxable Income of $82,800.

C)Sico has Taxable Income of nil and Mark has Taxable Income of $72,000.

D)Sico has Taxable Income of $16,000 and Mark has Taxable Income of $82,800.

A)Sico has Taxable Income of $8,000 and Mark has Taxable Income of $72,000.

B)Sico has Taxable Income of $8,000 and Mark has Taxable Income of $82,800.

C)Sico has Taxable Income of nil and Mark has Taxable Income of $72,000.

D)Sico has Taxable Income of $16,000 and Mark has Taxable Income of $82,800.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

65

Sarah Kern owns 80 percent of the shares of Kern Ltd. and 5 percent of the shares of Lorne Inc. Kern Ltd. owns 30 percent of the shares of Lorne Inc. Sarah's 12 year old daughter owns 25 percent of the shares of Lorne Inc. There are no other shareholders who hold shares in both Companies. Are Kern Ltd. and Lorne Inc. associated? Explain your conclusion.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

66

Ambee Ltd. commenced operations in 2019, and has two separate lines of business. They are a mail order operation selling organic food products, and an operation that provides accounting services to small business. The income (loss)of the two operations for the years 2019 and 2020 are as follows: The Company has no deductions from Net Income For Tax Purposes other than possible loss carry forwards from 2019.

Determine the minimum Taxable Income for each of the two years, and any loss carry forward available at the end of the year assuming that there was no acquisition of control in either year. How would your answer be different if there was an acquisition of control on January 1, 2020?

The Company has no deductions from Net Income For Tax Purposes other than possible loss carry forwards from 2019.Determine the minimum Taxable Income for each of the two years, and any loss carry forward available at the end of the year assuming that there was no acquisition of control in either year. How would your answer be different if there was an acquisition of control on January 1, 2020?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following transactions that involve an increase in PUC will result in an ITA 84(1)deemed dividend?

A)A stock dividend is declared that increases PUC in excess of the increase in net assets.

B)The PUC of one class of shares is increased, and the PUC of another class is decreased an equivalent amount.

C)A corporation issues shares to a creditor in order to settle debt with a carrying value less than the PUC of the newly issued shares.

D)When consideration received for shares issued is in excess of the amount added to PUC.

A)A stock dividend is declared that increases PUC in excess of the increase in net assets.

B)The PUC of one class of shares is increased, and the PUC of another class is decreased an equivalent amount.

C)A corporation issues shares to a creditor in order to settle debt with a carrying value less than the PUC of the newly issued shares.

D)When consideration received for shares issued is in excess of the amount added to PUC.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

68

What are the tax consequences associated with a corporation issuing shares to a creditor in order to retire a debt that has a carrying value lower than the PUC of the shares issued?

A)There will be a reduction in PUC and ACB for all the shares that were outstanding prior to the debt retirement transaction.

B)There will be a deemed dividend which will be allocated to all shareholders including the new shareholder who acquired shares by giving up debt securities. The adjusted cost base of the shares will increase by the amount of the deemed dividend.

C)There will be a deemed dividend allocated to the new shareholder who acquired shares by giving up debt securities. The adjusted cost base of the shares will increase by the amount of the deemed dividend.

D)There will be a deemed dividend allocated to all shareholders including the new shareholder who acquired shares by giving up debt securities. The adjusted cost base of the shares will not be affected.

A)There will be a reduction in PUC and ACB for all the shares that were outstanding prior to the debt retirement transaction.

B)There will be a deemed dividend which will be allocated to all shareholders including the new shareholder who acquired shares by giving up debt securities. The adjusted cost base of the shares will increase by the amount of the deemed dividend.

C)There will be a deemed dividend allocated to the new shareholder who acquired shares by giving up debt securities. The adjusted cost base of the shares will increase by the amount of the deemed dividend.

D)There will be a deemed dividend allocated to all shareholders including the new shareholder who acquired shares by giving up debt securities. The adjusted cost base of the shares will not be affected.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

69

At the beginning of the current year, Brou Inc. sells all of its assets and pays its liabilities. Afterwards, the company has $350,000 in cash which is distributed to the sole shareholder, Mr. Daniel. Mr. Daniel purchased the shares from the former shareholder for $50,000. The PUC of the shares is $10,000. The balance in the capital dividend account is $65,000, and the company makes all appropriate elections with respect to this balance. What is the amount of the deemed dividend to Mr. Daniel?

A)$ 65,000.

B)$ 275,000.

C)$ 300,000.

D)$ 340,000.

A)$ 65,000.

B)$ 275,000.

C)$ 300,000.

D)$ 340,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

70

During the taxation year ending December 31, 2020, Dwanto Ltd. makes current expenditures of $460,000 on which a 10 percent investment tax credit is available. In addition, it acquires $675,000 of Class 10 assets on which a 10 percent investment tax credit is available.

Describe the 2020 and 2021 tax consequences associated with making these expenditures and claiming the related investment tax credits. Include in your solution the CCA for 2020 and 2021.

Describe the 2020 and 2021 tax consequences associated with making these expenditures and claiming the related investment tax credits. Include in your solution the CCA for 2020 and 2021.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

71

During its taxation year ending December 31, 2020, all of the shares of Vick Ltd. are acquired by a new owner. The acquisition occurs on May 1, 2020 and, at that time, Vick has available a net capital loss of $175,000 [(1/2)($350,000)]. Also at that time the company has the following assets: For the period January 1, 2020 through April 30, 2020, the company has an operating loss of $143,000.

Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.

For the period January 1, 2020 through April 30, 2020, the company has an operating loss of $143,000.Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

72

At the beginning of the current year, Shahbaz Inc., a CCPC, has shares with a PUC of $4,000,000, and a balance of $300,000 in its capital dividend account. The company was started by Mr. Sheikh, who made a $4,000,000 investment in the common shares. During the current year, the company has disposed of a major division, and it will distribute $1,000,000 to its sole shareholder, Mr. Sheikh. The company will reduce the PUC by $600,000 in order to minimize the tax consequences to Mr. Sheikh. What is the ACB of Mr. Sheikh's shares after this transaction is completed?

A)$3,000,000.

B)$3,400,000.

C)$3,600,000.

D)$4,000,000.

A)$3,000,000.

B)$3,400,000.

C)$3,600,000.

D)$4,000,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

73

Lead Services Ltd. operates two separate lines of business, one of which sells drafting pencils, the other provides professional engineering services. In its first year of operations ending December 31, 2019, the engineering services business had a loss of $104,000, and the pencil business had income of $24,600, resulting in a Net Income For Tax Purposes of nil.

For the taxation year ending December 31, 2020, the engineering services business had income of $21,250 and the pencil business had income of $133,400, resulting in a Net Income For Tax Purposes of $154,650. The Company has no deductions from Net Income For Tax Purposes other than possible loss carry forwards from 2019. Determine the minimum Taxable Income for each of the two years, and any loss carry forward available at the end of the year assuming that there was no acquisition of control in either year. How would your answer be different if there was an acquisition of control on January 1, 2020?

For the taxation year ending December 31, 2020, the engineering services business had income of $21,250 and the pencil business had income of $133,400, resulting in a Net Income For Tax Purposes of $154,650. The Company has no deductions from Net Income For Tax Purposes other than possible loss carry forwards from 2019. Determine the minimum Taxable Income for each of the two years, and any loss carry forward available at the end of the year assuming that there was no acquisition of control in either year. How would your answer be different if there was an acquisition of control on January 1, 2020?

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

74

During the taxation year ending December 31, 2020, Future Ventures has made a number of expenditures that qualify for investment tax credits. They are as follows:

• $132,000 in Qualified Property in the Gaspe Peninsula.

• $1,060,000 in current expenditures for Scientific Research And Experimental Development.

The Company is a Canadian controlled private corporation. For 2019, Future Ventures has Taxable Income of $161,000 and Taxable Capital Employed In Canada of $8,500,000. The Company has no Tax Payable for 2020 or in any of the three preceding years.

Determine the amount of the refund that Future Ventures will receive as a result of earning these investment tax credits and any available carry forwards. Include in your answer any other tax consequences of these investment tax credits.

• $132,000 in Qualified Property in the Gaspe Peninsula.

• $1,060,000 in current expenditures for Scientific Research And Experimental Development.

The Company is a Canadian controlled private corporation. For 2019, Future Ventures has Taxable Income of $161,000 and Taxable Capital Employed In Canada of $8,500,000. The Company has no Tax Payable for 2020 or in any of the three preceding years.

Determine the amount of the refund that Future Ventures will receive as a result of earning these investment tax credits and any available carry forwards. Include in your answer any other tax consequences of these investment tax credits.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

75

When it was first established, Lichter Inc. issued 123,000 shares at a price of $5.60 per share. Four years later, an additional 32,000 shares were issued for $8.62 per share. During the current year, a further 81,000 shares were issued for $10.15 per share. One of the investors in the Company acquired 1,350 shares of the first group of shares issued, and an additional 4,230 shares from the most recent issue. Determine the adjusted cost base per share, as well as the total PUC of this investor's shares.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

76

Static Controls Inc. has a December 31 year end. On May 1, 2020, all of the Company's shares are acquired by a new owner. For the period January 1, 2020 through April 30, 2020, the Company has an operating loss of $91,000.

On April 30, 2020, the Company has available a net capital loss carry forward of $125,000 [(1/2)($250,000)]. In addition, the Company has the following assets: Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results.

On April 30, 2020, the Company has available a net capital loss carry forward of $125,000 [(1/2)($250,000)]. In addition, the Company has the following assets:

Advise the Company with respect to the most appropriate elections to be made prior to the acquisition of control and explain your results. Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

77

During the taxation year ending December 31, 2020, Enco Ltd. makes current expenditures of $722,000 on which a 10 percent investment tax credit is available. They also acquire $942,000 in Class 8 assets on which a 10 percent investment tax credit is available. Describe the 2020 and 2021 tax consequences associated with making these expenditures and claiming the related investment tax credits. Include in your solution the CCA for 2020 and 2021.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

78

Aris Ltd. has 2,000,000 shares outstanding with a total PUC of $30,000,000. The Company is a CCPC and has no balance in its GRIP account. John Aris owns 10 percent of these shares. They were acquired at a total cost of $2,250,000. During the current year, John's shares were redeemed by the corporation for proceeds of $3,500,000. Which of the following amounts must be included in John's income as a result of this redemption?

A)$1,250,000

B)$ 950,000

C)$1,325,000

D)$ 875,000

A)$1,250,000

B)$ 950,000

C)$1,325,000

D)$ 875,000

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

79

SSS Corp agrees to accept common shares with a PUC of $100,000 from TTT Ltd. in exchange for the retirement of debt with a carrying value of $90,000. What are the tax consequences of this exchange?

A)The shareholders of TTT Ltd. will be deemed to have received a dividend of $10,000.

B)The shareholders of SSS Corp will be deemed to have received a dividend of $10,000.

C)SSS Corp will have realized a capital gain of $10,000.

D)There will be no immediate tax consequences.

A)The shareholders of TTT Ltd. will be deemed to have received a dividend of $10,000.

B)The shareholders of SSS Corp will be deemed to have received a dividend of $10,000.

C)SSS Corp will have realized a capital gain of $10,000.

D)There will be no immediate tax consequences.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

80

Scranton Inc. is a CCPC with a nil GRIP balance. It has 100,000 shares outstanding, all of which were issued at a price of $8.00 per share. Nellie Ward owns 10,000 of these shares which she acquired at a cost of $7.00 per share. During 2020, the company redeems Nellie's shares at a price of $10.00 per share. Which of the following amounts will be included in Nellie's Net Income For Tax Purposes as a result of the redemption?

A)$25,000.

B)$33,000.

C)$30,000.

D)$28,000.

A)$25,000.

B)$33,000.

C)$30,000.

D)$28,000.

Unlock Deck

Unlock for access to all 96 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 96 flashcards in this deck.