Deck 11: Communicating Research Results

Full screen (f)

Question

Question

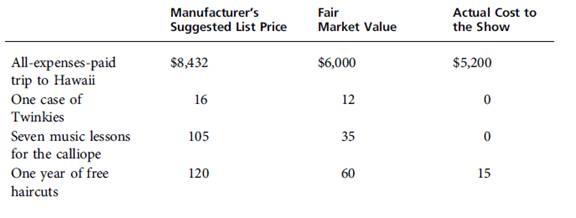

On December 6, Ed Grimely appeared on the game show, "The Wheel of Fate." As a result of his appearance, Grimely won the following prizes.

a. Assuming that Grimely received all these prizes by the end of the year, compute his gross income for the year as a result of his winnings.

b. Will this amount change if Grimely refuses to accept the calliope lessons immediately after the program's taping session is completed

a. Assuming that Grimely received all these prizes by the end of the year, compute his gross income for the year as a result of his winnings.

b. Will this amount change if Grimely refuses to accept the calliope lessons immediately after the program's taping session is completed

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Edna is a well-paid executive with ADley, a firm that uses stock options and deferred compensation as well as high salaries to compensate its most successful employees. When Edna and Ron were divorced, Ron received the rights to a bundle of these deferred-compensation rights. Complete the following table, indicating the required tax results:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/45

Play

Full screen (f)

Deck 11: Communicating Research Results

1

Katie is a one-third owner of an S corporation. After a falling out with the other shareholders, Katie signed an agreement early in January 2014. Under the terms of the agreement, Katie took $200,000 of her capital from the corporation and had eight months to negotiate a purchase of the stock of the other shareholders. She did not complete this task by the end of August 2014. On March 1, 2015, Katie sells all her shares to the remaining shareholders for a $2.5 million gain. For how many of these months does Katie report flow-through income from the S corporation

The case relates to person K that has the one third stakes in the S corporation and it signed the deed in the January after failing out with the stakeholders. As per the deed K took around 200,000 dollars of its capital from the corporation and also negotiated the purchasing of the shares of the other stakeholders.

The job related to the purchase was not completed at the stipulated date by the end of the august. In March 2015, the person K sells all of it's to the remaining shareholder for the gain of the around 2.5 million dollar. The question relates to the computation of the total number of the months that K reported the flow with the income in the same year.

K will have the income for the whole fourteen months as she had the interest benefitted in the corporation for the whole time period. This is because the person K was with the project of purchase with the other shareholders in the present case.

The job related to the purchase was not completed at the stipulated date by the end of the august. In March 2015, the person K sells all of it's to the remaining shareholder for the gain of the around 2.5 million dollar. The question relates to the computation of the total number of the months that K reported the flow with the income in the same year.

K will have the income for the whole fourteen months as she had the interest benefitted in the corporation for the whole time period. This is because the person K was with the project of purchase with the other shareholders in the present case.

2

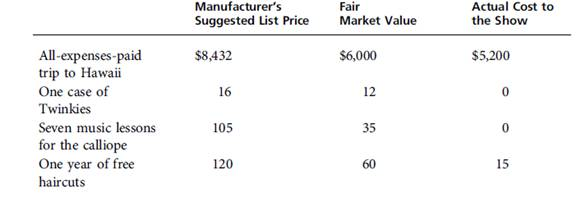

On December 6, Ed Grimely appeared on the game show, "The Wheel of Fate." As a result of his appearance, Grimely won the following prizes.

a. Assuming that Grimely received all these prizes by the end of the year, compute his gross income for the year as a result of his winnings.

b. Will this amount change if Grimely refuses to accept the calliope lessons immediately after the program's taping session is completed

a. Assuming that Grimely received all these prizes by the end of the year, compute his gross income for the year as a result of his winnings.

b. Will this amount change if Grimely refuses to accept the calliope lessons immediately after the program's taping session is completed

Prizes and Awards

As a general rule the prizes and awards that are won in a game show are included in the gross income of the taxpayer and the same is taxed in the year in which the prize is won. There are certain exceptions to this rule as well in which exclusion are allowed from the gross income in case of prize or awards.

In the present case person E has participated in a game show and has won prizes that include free trip, free music classes and one year haircut. In the present case the value of the prizes that is required for the taxation purpose is to be determined.

a.

As per the code section 1.74-1, in case the prize that is won is not in cash but in the form of services or goods, then in such a situation the fair value of the prizes won will be considered for the taxation purpose.

In the present case, the fair value of the free trip is $6,000, music classes is $35, one case of Twinkies is $12 and the fair market value of the free haircuts is $60. Thus, the gross total income of person e will increase by $6,107 as a result of winning in the game show.

b.

The statue did not allow any exclusion of the prize amount in case of refusal of the prize by the tax payer but this situation is confirmed by the Rev. Rul. 57-374 that established that in case where the winner refuses the prize, the same will not be included in the gross income.

In the present case if the person E did not accept the free music classes, the fair market value of the same will not be included in his gross income and the amount calculated above will change.

As a general rule the prizes and awards that are won in a game show are included in the gross income of the taxpayer and the same is taxed in the year in which the prize is won. There are certain exceptions to this rule as well in which exclusion are allowed from the gross income in case of prize or awards.

In the present case person E has participated in a game show and has won prizes that include free trip, free music classes and one year haircut. In the present case the value of the prizes that is required for the taxation purpose is to be determined.

a.

As per the code section 1.74-1, in case the prize that is won is not in cash but in the form of services or goods, then in such a situation the fair value of the prizes won will be considered for the taxation purpose.

In the present case, the fair value of the free trip is $6,000, music classes is $35, one case of Twinkies is $12 and the fair market value of the free haircuts is $60. Thus, the gross total income of person e will increase by $6,107 as a result of winning in the game show.

b.

The statue did not allow any exclusion of the prize amount in case of refusal of the prize by the tax payer but this situation is confirmed by the Rev. Rul. 57-374 that established that in case where the winner refuses the prize, the same will not be included in the gross income.

In the present case if the person E did not accept the free music classes, the fair market value of the same will not be included in his gross income and the amount calculated above will change.

3

The Downtown Wellness Clinic, a tax-exempt organization, sells memberships to corporations so that their employees can work out before and after office hours. Three blocks away, the Power Up Fitness Center has similar facilities and also wants to sell memberships to corporate neighbors. Is the clinic subject to federal income tax on its membership sales

Tax Exempt Organization

As per the code section 501(c), there are 29 types of non-profit organization that treated as tax exempt by the IRS. By tax exempt it means that these types of organization will not be liable to federal taxes.

In the present case D clinic is a tax exempt organization that is selling membership of their fitness club to the different corporations so that their employees can use the facilities of the fitness centre. The liability of the fitness centre for the federal taxes is need to be examined.

As per the code section 511, 512, 513 the organizations that are tax exempt which are having income from an unrelated business activity will be liable to federal tax. But there are three conditions which are required to be met in order to constitute an unrelated business activity first of which is that it should be continued regularly and should not be related to the main object of the organization.

However, the IRS in its Rev. Rul. Ruled that in case where a charity organization us providing fitness services by selling membership has to be considered as a unrelated business activity and will be liable to federal tax.

Thus, in the present case as not much information is available in regards to the D clinic, it can be concluded that the activity of selling the membership to the corporations is an unrelated business activity and will be liable to federal income taxes.

As per the code section 501(c), there are 29 types of non-profit organization that treated as tax exempt by the IRS. By tax exempt it means that these types of organization will not be liable to federal taxes.

In the present case D clinic is a tax exempt organization that is selling membership of their fitness club to the different corporations so that their employees can use the facilities of the fitness centre. The liability of the fitness centre for the federal taxes is need to be examined.

As per the code section 511, 512, 513 the organizations that are tax exempt which are having income from an unrelated business activity will be liable to federal tax. But there are three conditions which are required to be met in order to constitute an unrelated business activity first of which is that it should be continued regularly and should not be related to the main object of the organization.

However, the IRS in its Rev. Rul. Ruled that in case where a charity organization us providing fitness services by selling membership has to be considered as a unrelated business activity and will be liable to federal tax.

Thus, in the present case as not much information is available in regards to the D clinic, it can be concluded that the activity of selling the membership to the corporations is an unrelated business activity and will be liable to federal income taxes.

4

Can an individual make a contribution to an IRA based on the receipt of unemployment compensation

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

5

Sing-Yi receives a $100 debit card every month from her employer, the Porter Group. The debit card is limited so that it can be used only to purchase fare cards and passes on the Metro Transit line that operates trains and subways in town. Sing-Yi throws away the card when it expires at the end of the month, and she is not required to provide any records to Porter about how the card was used. The card logo says "American Airlines Visa," and Sing-Yi picks her own password for the card. Does the card represent $100 monthly gross income to Sing-Yi Explain.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

6

SlimeCo spent $250,000 to build underground storage tanks for its waste byproducts. This is a recurring expenditure for SlimeCo because once the tanks are filled, new ones must be built. When can SlimeCo deduct the $250,000

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

7

HardCo spent $4 million this year on a new graphic design for its product, a yo-yo. Under the prior design, HardCo's name and logo only appeared on the box and wrapping paper, which were discarded by most customers once they started using the product. The new design displayed HardCo's name and newer, flashier logo on both sides of the yo-yo, with a paint that also made it glow in the dark. When can HardCo deduct the $4 million

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

8

Prudence was named a shareholder in her law firm, which operates as an S corporation. Her payments into the firm's capital were to start in approximately nine months, when an audit would determine the full value of the firm and a new corporate year would commence. Paperwork with the pertinent state offices was completed, naming Prudence as a shareholder and director and adding her name to that of The firm. However, Prudence left the firm eight months after the announcement, i.e., before she paid any money for shares. Is Prudence liable for tax on her share of the entity's earnings for the eight months

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

9

Fred was the owner of a three-bedroom cabin in California. During 2013, he contracted with a propertymanagement company to rent the cabin to third parties. In exchange for its services, Fred paid the company a 35 percent commission on all rental income received. The property-management company was responsible for maintaining the property, cleaning the cabin, paying all utilities, providing linens, and so on. The cabin was rented three times during the year for a total of 12 days and nine nights, with the average rental period being three days. Fred visited the cabin eight times during the year and stayed 19 nights and 27 days. Fred claimed $15,000 of Schedule E expenses relating to the rental of the cabin on his return under the active-rental-real-estate exception. Was Fred entitled to the deduction

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

10

Sarah came home one day to find significant water damage in her home. Apparently one of the hoses to her washing machine had worn out and split, spilling water all over the place. Over the next month, mildew appeared as well. Is there any casualty-loss deduction for Sarah Ignore any computational floors and assume that she did not have any homeowner's insurance.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

11

Cal's son has been labeled a "can't miss" NBA prospect since middle school. This year, while the son is a college freshman and classified as an amateur under NCAA rules, Cal spent $14,000 for special clothing, equipment, camps, and personal trainers to keep improving his son's skills. Can Cal deduct these items

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

12

Gina was falsely imprisoned as the result of an auto dealer's criminal complaint against her. Although the charges were later dropped, she was arrested and detained for approximately eight hours. She was not hurt or abused during the arrest and detention but she did see a psychologist for several sessions. She sued the auto dealership for malicious prosecution and received a $25,000 settlement payment from the company. Can Gina exclude the settlement payment from income

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

13

Richie is a wealthy rancher in Texas. He operates his ranch through a grantor trust set up by his grandparents. Richie does not like to get his hands dirty, so he hires a professional management company to run the ranch. The property generated a $500,000 loss this year. Can Richie deduct this loss on his Schedule E given the material participation rules of I.R.C. § 469

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

14

CPA Myrna forgot to tell her client, Freddie, to accelerate the payment of state income and property taxes in a year when Freddie was in an unusually high tax bracket. Upon discovering the error, the parties negotiated a $15,000 payment from Myrna (and her insurance company) to Freddie to compensate Freddie for Myrna's inadequate professional advice. Is this payment gross income to Freddie

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

15

Four individuals formed Triangle Properties as a C corporation in 2008. The corporation is domiciled in North Carolina. The corporation invested in commercial rental properties that generated passive-activity losses. The shareholders made a Subchapter S election for Triangle Properties effective on January 1, 2014. On the date of conversion, Triangle Properties had $118,000 of suspended passive-activity losses from its commercial rental properties. In 2014, the properties generated $44,000 of net rental income. Can Triangle Properties carry forward and deduct the suspended passive losses incurred when it was a C corporation against the passive rental income earned while it was an S corporation

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

16

Maggie could not conceive a child using natural means, so she sought out a woman who would donate an egg to be surgically implanted in Maggie. Which of the following items are deductible by Maggie in her process to find an egg donor

a. Payment to a search firm to find donor candidates.

b. Payment to Maggie's attorney.

c. Payment of a fee to the egg donor.

d. Payment to medical staff to run physiological and psychological tests on the prospective donor.

a. Payment to a search firm to find donor candidates.

b. Payment to Maggie's attorney.

c. Payment of a fee to the egg donor.

d. Payment to medical staff to run physiological and psychological tests on the prospective donor.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

17

How much of the $100,000 interest that is paid on a loan from Everett National Bank can Ben deduct if he invests the loan proceeds in the following Consider each item independently.

a. South Chicago School District bonds

b. AT T bonds, paying $125,000 interest income this year

c. Computer Futures Inc. shares, a growth stock that pays no dividend this year

a. South Chicago School District bonds

b. AT T bonds, paying $125,000 interest income this year

c. Computer Futures Inc. shares, a growth stock that pays no dividend this year

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

18

Sal was born male but diagnosed with gender identity disorder. As a result, he suffered persistent psychological discomfort with his gender and decided to have a sex-change operation. As part of the treatment regimen, Sal had to undergo various hormonal treatments for several years, followed by a period in which he changed his name to Sally and lived for two years as a female before finally having gender-reassignment surgery in 2014. Is Sally entitled to a medical deduction for the costs of the hormone treatment, surgeries, and related expenses

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

19

Larry and Mary obtained a divorce, and the decree as negotiated allowed alimony payments to Mary of $3,000 on the 15th of each month. The divorce was final on July 5, but Mary was short of cash, so Larry made the payments to her starting in March. What is Larry's alimony deduction for the year

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

20

Lilly leases a car that she uses solely for business purposes. The car would be worth $40,050 on the market, and Lilly paid $7,400 in lease payments this year. How are these items treated on her tax return

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

21

Jim Jones owns 50 percent of the stock of an S corporation. In 2014, Jim obtains a health insurance plan providing coverage for himself, his wife, and their two children. Jim makes all premium payments to the plan during 2014 and furnishes proof of the payments to the S corporation, which then reimburses him for the payments and reports the premium payments as wages on Jim's W-2 for the year. Copyright 2015 Cengage Learning. All Rights Reserved. May not be copied, scanned, or duplicated, in whole or in part. Due to electronic rights, some third party content may be suppressed from the eBook and/or eChapter(s). Editorial review has deemed that any suppressed content does not materially affect the overall learning experience. Cengage Learning reserves the right to remove additional content at any time if subsequent rights restrictions require it. Jim reports the amounts as gross income on his 2014 personal tax return. Jim's income from the S corporation exceeds the amount of premiums for the health coverage and he does not participate in any subsidized health plans maintained by another employer or an employer of his spouse. Is Jim allowed to take a deduction on his personal tax return for the health insurance premiums paid during the year

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

22

Sally incurred a 90-mile round-trip commute every day, mainly because she could not get along with her supervisor at the sales office located four miles fromher home. Sally works under a one-year contract, and her assignment to the nearer office is affirmed in the current year's contract, but management has allowed her to travel to the more distant location. How many deductible commuting miles does Sally accumulate on a work day

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

23

Pete is an engineering professor at State University. Under his contract, Pete's inventions while employed at the university are the property of the Board of Regents, but Pete receives an addition to his salary equal to one-third of the royalties received by the university on his patents. This year, Pete received $75,000 on top of his salary, as royalties allocated to him. Does Pete recognize this amount as ordinary income or capital gain

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

24

Chico is a corporation operating in several states on the accrual basis. Chico received a state income tax refund this year (Year 4) based on the following sequence of events. In which tax year does Chico recognize the refund as gross income

Year 1: Generated the operating loss.

Year 2: Filed the loss carryback form with the state.

Year 3: Received notice that the refund was approved.

Year 4: Received the refund check.

Year 1: Generated the operating loss.

Year 2: Filed the loss carryback form with the state.

Year 3: Received notice that the refund was approved.

Year 4: Received the refund check.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

25

Professor White operates a popular CPA exam review course as a sole proprietor. He charges $2,000 tuition to each student, and he guarantees a full refund of the tuition if the student passes an in-course exam but does not pass the actual CPA exam on the first try. White is bold enough to do this because the first-time-pass rate for his students is more than 80 percent. He collected $150,000 tuition for his fall 2013 review section, but he reported the gross receipts on his 2014 Form 1040 because the grades for those taking the fall review are not released until February 2014. Thus, White asserted that he had no constructive receipt of the tuition until February 2014. Is this treatment correct

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

26

Dean and Robin owned a family business, each holding the shares as community property. When they were divorced in 2011, the court did not force them to split the shares, citing damage to the business that could occur if the public learned that ownership of the enterprise was changing. Now it is 2014, and Robin wants to remarry. She and her new husband want to have the business retitle one-half of the shares in Robin's name only. The original divorce court agrees in 2014. Is this transfer subject to income tax Is it subject to gift tax

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

27

After her employer transferred her to another town, Rosemary put her house up for sale. After two years of Internet listings, open houses, repairs, and price cuts, a buyer finally came along. By this time, the house had sat empty for 25 months before the closing occurred, and Rosemary rented it out just to help with the mortgage payments. Rosemary claimed a $40,000 business loss with respect to the house. Do you agree with this filing position

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

28

Lisa, usually a stay-at-home mother, went to the hospital one day for some outpatient surgery. She hired a babysitter for $35 to watch her four-year-old son while she was gone. What tax benefits are available to Lisa for this cash payment

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

29

Dave made a $100,000 cash withdrawal from his IRA. He bought $100,000 of Microcraft stock, and within the rollover period he transferred the stock to another IRA. Does Dave report any gross income

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

30

Edna is a well-paid executive with ADley, a firm that uses stock options and deferred compensation as well as high salaries to compensate its most successful employees. When Edna and Ron were divorced, Ron received the rights to a bundle of these deferred-compensation rights. Complete the following table, indicating the required tax results:

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

31

Same as 7, except that Lisa paid the sitter while she worked as a scout leader for the Girl Scouts.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

32

Gold Partners wanted to complete a like-kind exchange just before it liquidated. Accordingly, it sold the real estate it meant to transfer to the other party, and a qualified intermediary held the resulting cash. When the intermediary found acceptable replacement realty, the intermediary transferred cash and the like-kind property directly to the partners, thereby liquidating Gold. Does I.R.C. § 1031 apply

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

33

Wes and Donna were the only members of an LLC, and they fended off unwanted takeover suitors with a clause in the charter that shares could change hands only with unanimous approval from all the other owners. Wes is now 70 years old, so he wants to start phasing out of the business. He makes a gift of 10 percent of the LLC shares to his son Jeffrey, as agreed to by Donna. The shares are worth $20,000. What is Wes's taxable gift to Jeffrey in the year of the transfer

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

34

Tex's credit union has provided him with financing to acquire his $200,000 home. The loan is set up as a three-year note with a balloon payment, but the credit union always renews the loan for another three years at the current interest rate. This year, the credit union renewed Tex's loan for the third time, charging $3,000 in points. In what year(s) can Tex deduct this $3,000

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

35

HelpCo pays Hank two $100,000 salaries per year, one through its WestCo subsidiary and one through its EastCo subsidiary. How do Hank and HelpCo treat his Social Security tax obligations

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

36

Peg worked with a local IRS-approved charity whose mission was to capture and neuter feral cats and take care of them until they could be released back into the wild. Peg incurred more than $6,000 of expenses for food and medical care for more than 50 cats under her care. Is Peg able to claim any of the $6,000 as a charitable deduction on her tax return

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

37

Amelia and Dave are married and have one child. Detail the tax effects to the couple of making the I.R.C. § 1(g)(7)(A)(iv) election to include their seven-year-old daughter's $10,000 unearned income on their currentyear joint return.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

38

Zhang lived in Atlanta from 2008 through 2010 to carry out her duties as an employee of YourTV.com, receiving an annual salary of $150,000. She was transferred to the San Jose office for 2011 through 2013, and then in 2014 she took an executive position with the Web2.2 LLC in Austin. Zhang owned a home in Atlanta, but she rented an apartment in San Jose. When she withdraws money from her IRA to submit a down payment on her Austin condominium, is a 10 percent penalty due

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

39

As a result of financial difficulties, Acme Company, located in Raleigh, North Carolina, closed all its retail stores and terminated all its employees. The company adopted a plan to compensate terminated employees based on job grade and management level, and each terminated employee received a severance payment as a lump-sum payment. The payments were treated as taxable income to the employees for federal income tax purposes, and Acme reported the payments as wages on W-2 forms. Do the company and the laid-off workers owe Social Security and Medicare taxes on the payments

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

40

Eighty percent of the Willigs' AGI comes from their submarine sandwich shop operated as a sole proprietorship. In 2014, the Willigs lost an IRS audit and owed $12,000 in 2012 federal income taxes, all attributable to inventory computations in their business. Interest on this amount totaled $3,200. All amounts due were paid by the end of 2014. How much of the interest can the Willigs deduct on their 2014 Schedule C

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

41

Give three examples of situations in which the IRS would waive the two-year rule for applying the I.R.C. § 121 exclusion of gain from the sale of a principal residence as a result of "unforeseen circumstances."

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

42

A local law firm recently remodeled its offices. In addition to new office furniture and computers, the company purchased six large paintings from a local art gallery. These paintings are more than 100 years old and cost more than $100,000. The paintings are on display in the offices alongside more recent paintings by lesser-known artists. Are the paintings depreciable for tax purposes

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

43

Al and Amy are divorced. In which of the following circumstances can legal fees be deducted

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

44

LaFollette lives in a condominium with Tourneau. The two are not married, but they each hold a one-half interest in the deed for their unit. In the current year, the condominium association installed a solar water heater. The association paid for the water heating system, but it assessed LaFollette and Tourneau $7,500 for this expenditure, as it did for other unit owners. Tourneau was short of funds, so LaFollette paid the entire assessment before the end of the year. Compute LaFollette's I.R.C. § 25D credit against her Form 1040 liability for the year.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

45

Chris Mac, a local CPA, is a self-employed tax return preparer. Chris works from home in a room that is exclusively used on a regular basis as the principal place of business. Last year, Chris built a new bathroom across the hall for his clients' use. Although the vast majority of use of the bathroom is from clients, occasionally

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 45 flashcards in this deck.