Deck 27: Epilogue: the Story of Macroeconomics

Full screen (f)

Question

Question

Question

Question

Question

Question

Nontraditional macroeconomic policy: financial policy and quantitative easing

Interpret the interest rate as the federal funds rate, the pol-icy interest rate of the Federal Reserve. Assume that there is an unusually high premium added to the federal funds rate when firms borrow to invest.

a. Suppose that the government takes action to improve the solvency of the financial system. If the government's action is successful, and banks become more willing to lend-both to one another and to nonfinancial firms-what is likely to happen to the premium What will happen to the IS-LM diagram Can we con-sider financial policy a kind of macroeconomic policy

b. Faced with a zero nominal interest rate, suppose the Fed decides to purchase securities directly to facilitate the flow of credit in the financial markets. This policy is called quantitative easing. If quantitative easing is successful, so that it becomes easier for financial and nonfinancial firms to obtain credit, what is likely to hap-pen to the premium What effect will this have on the 1S-LM diagram If quantitative easing has some effect, is it true that the Fed has no policy options to stimulate the economy when the federal funds rate is zero

Interpret the interest rate as the federal funds rate, the pol-icy interest rate of the Federal Reserve. Assume that there is an unusually high premium added to the federal funds rate when firms borrow to invest.

a. Suppose that the government takes action to improve the solvency of the financial system. If the government's action is successful, and banks become more willing to lend-both to one another and to nonfinancial firms-what is likely to happen to the premium What will happen to the IS-LM diagram Can we con-sider financial policy a kind of macroeconomic policy

b. Faced with a zero nominal interest rate, suppose the Fed decides to purchase securities directly to facilitate the flow of credit in the financial markets. This policy is called quantitative easing. If quantitative easing is successful, so that it becomes easier for financial and nonfinancial firms to obtain credit, what is likely to hap-pen to the premium What effect will this have on the 1S-LM diagram If quantitative easing has some effect, is it true that the Fed has no policy options to stimulate the economy when the federal funds rate is zero

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/7

Play

Full screen (f)

Deck 27: Epilogue: the Story of Macroeconomics

1

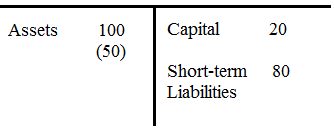

The Troubled Asset Relief Program (TARP) Consider a bank that has assets of 100, capital of 20, and short-tent credit of 80. Among the bank's assets are securitized assets whose value depends on the price of houses. These assets have a value of.50.

a. Set tip the bank's balance sheet. Suppose that ate result of a housing price decline, the value of the bank's securitized assets falls by an uncertain amount, so that these assets are now worth somewhere between 25 and 45. Call the securitized assets "troubled assets." The value of the other assets remains at 50. As a result of the uncertainty about the value of the bank's assets, lenders are reluctant to provide any short-term credit to the bank.

b. Given the uncertainty about the value of the bank's assets, what is the range in the value of the bank's capital Ma response to this problem, the government considers purchasing the troubled assets, with the intention of selling them again when the markets stabilize. (This is the original version of the TARP.)

c. lithe government pays 25 for the troubled assets, what will be the value of the bank's capital How much would the government have to pay for the troubled assets to ensure that the bank's capital does not have a negative value If the government pays 45 for the troubled assets, but the true value turns out to be much lower, who bears the cost of this mistaken valuation Explain.

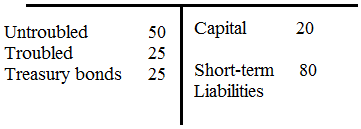

Suppose instead of buying the troubled assets, the government provides capital to the bank by buying ownership shares, with the intention of selling the shares again when the markets stabilize. (This is what the TARP ultimately became.) The government exchanges treasury bonds (which become assets for the bank) for ownership shares.

d. Suppose the government exchanges 25 of Treasury bonds for ownership shares. Assuming the worst case scenario (so that the troubled assets are worth only 25), set up the new balance sheet of the bank. (Remember that the firm now has three assets: 50 of untroubled assets. 25 of troubled assets, and 25 of treasury bonds.) What is the total value of the bank's capital Will the bank be Insolvent

e. Given your answers and the material in the text, why might recapitalization be a better policy than buying the troubled assets

a. Set tip the bank's balance sheet. Suppose that ate result of a housing price decline, the value of the bank's securitized assets falls by an uncertain amount, so that these assets are now worth somewhere between 25 and 45. Call the securitized assets "troubled assets." The value of the other assets remains at 50. As a result of the uncertainty about the value of the bank's assets, lenders are reluctant to provide any short-term credit to the bank.

b. Given the uncertainty about the value of the bank's assets, what is the range in the value of the bank's capital Ma response to this problem, the government considers purchasing the troubled assets, with the intention of selling them again when the markets stabilize. (This is the original version of the TARP.)

c. lithe government pays 25 for the troubled assets, what will be the value of the bank's capital How much would the government have to pay for the troubled assets to ensure that the bank's capital does not have a negative value If the government pays 45 for the troubled assets, but the true value turns out to be much lower, who bears the cost of this mistaken valuation Explain.

Suppose instead of buying the troubled assets, the government provides capital to the bank by buying ownership shares, with the intention of selling the shares again when the markets stabilize. (This is what the TARP ultimately became.) The government exchanges treasury bonds (which become assets for the bank) for ownership shares.

d. Suppose the government exchanges 25 of Treasury bonds for ownership shares. Assuming the worst case scenario (so that the troubled assets are worth only 25), set up the new balance sheet of the bank. (Remember that the firm now has three assets: 50 of untroubled assets. 25 of troubled assets, and 25 of treasury bonds.) What is the total value of the bank's capital Will the bank be Insolvent

e. Given your answers and the material in the text, why might recapitalization be a better policy than buying the troubled assets

(a) For this part of the problem, you need to setup a balance sheet for the bank basing on the given information. Make a note that securitized assets make up 50 of the 100 of the bank's assets. You can note this by putting the securitized asset value in parenthesis.

Assets Liabilities + Equity (b) You must remember the accounting identity that assets equal liabilities plus equity. Now that the securitized asset value is between 25 and 45 while the other asset value is 50, the new value of the bank's capital is between -5 and 15. This is true because short term liabilities cannot shrink. Regardless of the value of the bank's assets, its short-term liabilities are the same. However, according to the accounting identity, if assets shrink liabilities or equity must shrink, then capital, which is equity, must shrink by the same amount that asset value shrinks. Thus, the value of capital is between -5 and 15.

(b) You must remember the accounting identity that assets equal liabilities plus equity. Now that the securitized asset value is between 25 and 45 while the other asset value is 50, the new value of the bank's capital is between -5 and 15. This is true because short term liabilities cannot shrink. Regardless of the value of the bank's assets, its short-term liabilities are the same. However, according to the accounting identity, if assets shrink liabilities or equity must shrink, then capital, which is equity, must shrink by the same amount that asset value shrinks. Thus, the value of capital is between -5 and 15.

(c) If the government paid the bank 25 in capital for the banks troubled assets, it would be purchasing the securitized assets. This occurs because the securitized assets are those whose value is uncertain. By paying 25 in capital for troubled assets, the bank is essentially purchasing the low end of this valuation. This means that the previous valuation of between 25 and 45 is no longer applicable. The government is guaranteeing that these assets will be worth 25 no matter what. However, the risk that the value of these assets is only 25 poses the risk of leaving the bank insolvent. If these assets are only worth 25, the bank would still be 5 short on its liabilities. If this happens, the government would likely have to commit more money for purchasing bad assets to ensure the bank remains solvent.

(d) Below is the new balance sheet of the bank as per the given information:

Assets Liabilities + Equity Since total assets, which are now 100, must equal total equity plus total liabilities, the new value of the bank's capital is 20 now. Although there is a possibility that the bank could become insolvent because short-term liabilities are 5 more than untroubled assets, this would mean that the default rate on troubled assets is 80%, which is highly unlikely.

Since total assets, which are now 100, must equal total equity plus total liabilities, the new value of the bank's capital is 20 now. Although there is a possibility that the bank could become insolvent because short-term liabilities are 5 more than untroubled assets, this would mean that the default rate on troubled assets is 80%, which is highly unlikely.

(e) Given these answers, recapitalization might be a better policy than buying the troubled assets because there is less risk that the government might lose money due to bad valuations. If the government just purchases assets, it could wind up purchasing too little based on bad valuations, which would still leave the bank insolvent. If this happens, the government would need to step in and recapitalize the bank itself. By having the bank recapitalize itself, the government decreases the risk of the bank becoming insolvent.

Assets Liabilities + Equity

(b) You must remember the accounting identity that assets equal liabilities plus equity. Now that the securitized asset value is between 25 and 45 while the other asset value is 50, the new value of the bank's capital is between -5 and 15. This is true because short term liabilities cannot shrink. Regardless of the value of the bank's assets, its short-term liabilities are the same. However, according to the accounting identity, if assets shrink liabilities or equity must shrink, then capital, which is equity, must shrink by the same amount that asset value shrinks. Thus, the value of capital is between -5 and 15.(c) If the government paid the bank 25 in capital for the banks troubled assets, it would be purchasing the securitized assets. This occurs because the securitized assets are those whose value is uncertain. By paying 25 in capital for troubled assets, the bank is essentially purchasing the low end of this valuation. This means that the previous valuation of between 25 and 45 is no longer applicable. The government is guaranteeing that these assets will be worth 25 no matter what. However, the risk that the value of these assets is only 25 poses the risk of leaving the bank insolvent. If these assets are only worth 25, the bank would still be 5 short on its liabilities. If this happens, the government would likely have to commit more money for purchasing bad assets to ensure the bank remains solvent.

(d) Below is the new balance sheet of the bank as per the given information:

Assets Liabilities + Equity

Since total assets, which are now 100, must equal total equity plus total liabilities, the new value of the bank's capital is 20 now. Although there is a possibility that the bank could become insolvent because short-term liabilities are 5 more than untroubled assets, this would mean that the default rate on troubled assets is 80%, which is highly unlikely. (e) Given these answers, recapitalization might be a better policy than buying the troubled assets because there is less risk that the government might lose money due to bad valuations. If the government just purchases assets, it could wind up purchasing too little based on bad valuations, which would still leave the bank insolvent. If this happens, the government would need to step in and recapitalize the bank itself. By having the bank recapitalize itself, the government decreases the risk of the bank becoming insolvent.

2

The Ted spread

The text described the fluctuations in the Ted spread that occurred during the financial crisis. Do an interne: search and find the recent history of the Ted spread. You can find this information easily from various sources.

a. Consult Figure 28-5 to compare the current value of the Ted spread to its value before and during the financial crisis. How does the current value of the Ted Spread compare to Its highest values during the crisis How does the current value of the ted spread compare to its value at the beginning of 2007 (Note that the Ted spread is often quoted in basis points. One hundred basis points equals one percentage point.)

b. Has the Ted spread been relatively stable in recent months In what range of values has the spread fluctuated

c. What do you conclude about the willingness of banks to lend to one another now as compared to the beginning of 2007 as compared to the fall of 2008 Explain.

The text described the fluctuations in the Ted spread that occurred during the financial crisis. Do an interne: search and find the recent history of the Ted spread. You can find this information easily from various sources.

a. Consult Figure 28-5 to compare the current value of the Ted spread to its value before and during the financial crisis. How does the current value of the Ted Spread compare to Its highest values during the crisis How does the current value of the ted spread compare to its value at the beginning of 2007 (Note that the Ted spread is often quoted in basis points. One hundred basis points equals one percentage point.)

b. Has the Ted spread been relatively stable in recent months In what range of values has the spread fluctuated

c. What do you conclude about the willingness of banks to lend to one another now as compared to the beginning of 2007 as compared to the fall of 2008 Explain.

(a) Current, the Ted spread is at 0.35%. This tells us how much banks charge to lend to each other. Thus, to lend to another bank, a bank would expect a return of 0.35%. This tells us that banks do not perceive lending to others banks to be risky.

The current value of the Ted spread, 0.35%, is significantly lower than it was during the peak of the financial crisis. During the financial crisis, banks perceived lending to other banks to be very risky which caused the Ted spread to increase to over 4%. This is a staggeringly high Ted spread and it demonstrates the uncertainty of how risky lending to a bank was thought to be.

Right before the financial crisis, the Ted spread was at a very low value of 0.17%. At this point, banks perceived lending to other banks to be very safe. This value is not much different than the current Ted spread. However, we must note that the current value is still twice as high as the Ted spread right before the financial crisis.

(b) In the past 6 months the Ted spread has barely moved at all. During December of 2011, the Ted spread was at a high of 0.56% but has since decreased, remaining stable at about 0.37%. In the past 6 months the spread has been between 0.35% and 0.4%, a very narrow range.

(c) Compared to the beginning of 2007, banks are only slightly more hesitant to lend to each other. Although 0.35% is still low, 0.17% is very low. In the beginning of 2007, lending between banks was perceived as riskless. Now, lending between banks is still perceived as very safe, but the higher Ted spread demonstrates that banks do acknowledge that some risk does exist.

Compared to the fall of 2008, the Ted spread is tiny. At a value of over 4%, the Ted spread was enormous in the fall of 2008 and banks perceived lending to each other to be very risky. In fact, this Ted spread is one of the highest ever. Currently, as the Ted spread is very low, lending between banks is perceived as safe again and is a very different situation than in the fall of 2008.

The current value of the Ted spread, 0.35%, is significantly lower than it was during the peak of the financial crisis. During the financial crisis, banks perceived lending to other banks to be very risky which caused the Ted spread to increase to over 4%. This is a staggeringly high Ted spread and it demonstrates the uncertainty of how risky lending to a bank was thought to be.

Right before the financial crisis, the Ted spread was at a very low value of 0.17%. At this point, banks perceived lending to other banks to be very safe. This value is not much different than the current Ted spread. However, we must note that the current value is still twice as high as the Ted spread right before the financial crisis.

(b) In the past 6 months the Ted spread has barely moved at all. During December of 2011, the Ted spread was at a high of 0.56% but has since decreased, remaining stable at about 0.37%. In the past 6 months the spread has been between 0.35% and 0.4%, a very narrow range.

(c) Compared to the beginning of 2007, banks are only slightly more hesitant to lend to each other. Although 0.35% is still low, 0.17% is very low. In the beginning of 2007, lending between banks was perceived as riskless. Now, lending between banks is still perceived as very safe, but the higher Ted spread demonstrates that banks do acknowledge that some risk does exist.

Compared to the fall of 2008, the Ted spread is tiny. At a value of over 4%, the Ted spread was enormous in the fall of 2008 and banks perceived lending to each other to be very risky. In fact, this Ted spread is one of the highest ever. Currently, as the Ted spread is very low, lending between banks is perceived as safe again and is a very different situation than in the fall of 2008.

3

Prospects for the future

The test described net exports as a needed avenue of growth for the United States to be able to sustain a recovery. The text also noted that possibilities for improvement in net exports depend in part on policy measures in the countries with large trade surpluses. Do some Internet research and find out whether surplus countries have been raking the necessity policy measures Focus on Chin, and consider the issues described in parts (a) and (In a. At the time of this writing, U.S. policymakers had for several years been asking the Chinese government to stop its policy of maintaining a low (undervalued) value of its currency. Absent this policy, it is widely believed that the dollar would depreciate sharply against the Chinese currency. How would such a depreciation affect U.S. net exports Is there any evidence that China is changing (or has changed) its currency policy

b. Some economists point to the high private saving rate in China as related to a lack of social insurance. In effect, individuals have to insure themselves. If the Chinese government were to provide more social insurance (say in the areas of health care and education financing, and retirement), individuals might reduce their saving and increase their consumption. Some of this increased consumption would fall on U.S. goods. Is there any evidence of a change in Chinese policy with respect to social insurance Is there any evidence of a decrease in the Chinese saving rate

The test described net exports as a needed avenue of growth for the United States to be able to sustain a recovery. The text also noted that possibilities for improvement in net exports depend in part on policy measures in the countries with large trade surpluses. Do some Internet research and find out whether surplus countries have been raking the necessity policy measures Focus on Chin, and consider the issues described in parts (a) and (In a. At the time of this writing, U.S. policymakers had for several years been asking the Chinese government to stop its policy of maintaining a low (undervalued) value of its currency. Absent this policy, it is widely believed that the dollar would depreciate sharply against the Chinese currency. How would such a depreciation affect U.S. net exports Is there any evidence that China is changing (or has changed) its currency policy

b. Some economists point to the high private saving rate in China as related to a lack of social insurance. In effect, individuals have to insure themselves. If the Chinese government were to provide more social insurance (say in the areas of health care and education financing, and retirement), individuals might reduce their saving and increase their consumption. Some of this increased consumption would fall on U.S. goods. Is there any evidence of a change in Chinese policy with respect to social insurance Is there any evidence of a decrease in the Chinese saving rate

(a) A sharp depreciation of the U.S. dollar would increase net exports for the United States and decrease net exports for China. This would occur because a Chinese currency appreciation would make Chinese imports to the United States relatively more expensive, thus causing consumers to buy less of them. This would then lead less Chinese exports coming into the United States.

A depreciation of the U.S. dollar relative to the Chinese currency would make U.S. goods relatively cheaper relative to Chinese goods, both at home and abroad. Instead of buying cheap Chinese made goods, consumers would choose between Chinese goods and United States goods that are now priced at similar prices. This would allow U.S. goods to be more competitively priced with Chinese goods, leading to an increase in net exportation of U.S. goods.

There is some evidence that China is allowing its currency to depreciate. Politicians have been accusing China of continuing to manipulate its currency still. While China has not allowed its currency to appreciate to the full extent it normally would, inflation has been putting pressure on its currency. To combat inflationary pressure, China has had to allow its currency to appreciate somewhat.

(b) There is not much evidence that China's social insurance is changing. In fact, China's savings rate has actually increased over the past decade. China has actually decreased its social insurance by decreasing the provision of education, health care, retirement planning, etc. This has been the main driver of the increased savings rate, as young Chinese workers are beginning to save early for their retirement and future expenditures.

A depreciation of the U.S. dollar relative to the Chinese currency would make U.S. goods relatively cheaper relative to Chinese goods, both at home and abroad. Instead of buying cheap Chinese made goods, consumers would choose between Chinese goods and United States goods that are now priced at similar prices. This would allow U.S. goods to be more competitively priced with Chinese goods, leading to an increase in net exportation of U.S. goods.

There is some evidence that China is allowing its currency to depreciate. Politicians have been accusing China of continuing to manipulate its currency still. While China has not allowed its currency to appreciate to the full extent it normally would, inflation has been putting pressure on its currency. To combat inflationary pressure, China has had to allow its currency to appreciate somewhat.

(b) There is not much evidence that China's social insurance is changing. In fact, China's savings rate has actually increased over the past decade. China has actually decreased its social insurance by decreasing the provision of education, health care, retirement planning, etc. This has been the main driver of the increased savings rate, as young Chinese workers are beginning to save early for their retirement and future expenditures.

4

Using information in this chapter, label each of the following statements true, false, or uncertain. Explain briefly

a. The loss in output that has and will result from the financial crisis is many times larger than the losses on mortgages held by U.S. financial institutions.

b. An increase in a firm's leverage ratio tends to increase both the expected profit of the firm and the risk of the firm going bankrupt.

c. The high degree of securitization in the U.S. financial system helped to diversify risk and probably lessened the economic effect of the fall in housing prices.

d. Since the financial crisis ultimately led to a global recession, the policy measures (adopted in many countries) that provided substantial liquidity to financial institutions and that recapitalized banks (through the purchase of shares by governments) failed.

e. The fiscal stimulus programs adopted by many countries in response to the financial crisis helped offset the decline in aggregate demand and reduce the size of the recession.

a. The loss in output that has and will result from the financial crisis is many times larger than the losses on mortgages held by U.S. financial institutions.

b. An increase in a firm's leverage ratio tends to increase both the expected profit of the firm and the risk of the firm going bankrupt.

c. The high degree of securitization in the U.S. financial system helped to diversify risk and probably lessened the economic effect of the fall in housing prices.

d. Since the financial crisis ultimately led to a global recession, the policy measures (adopted in many countries) that provided substantial liquidity to financial institutions and that recapitalized banks (through the purchase of shares by governments) failed.

e. The fiscal stimulus programs adopted by many countries in response to the financial crisis helped offset the decline in aggregate demand and reduce the size of the recession.

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

5

Traditional monetary and fiscal policy (a refresher)

Consider an economy described by Figure 28-12, with output lower than the natural level of output and the nominal interest rate at zero.

a. Draw Figure 28-12.

b. If the Federal Reserve increases the money supply, what will happen to the IS-LM diagram you drew in part (a) Will equilibrium output move closer to the natural level

c. Given your answer to part (b), what policy options are available to the government to try to increase output Consider traditional policy options only, and not financial policies. How does your answer relate to the policy decisions of the Obama administration and the U.S. Congress in February 2009 Dig Deeper

Consider an economy described by Figure 28-12, with output lower than the natural level of output and the nominal interest rate at zero.

a. Draw Figure 28-12.

b. If the Federal Reserve increases the money supply, what will happen to the IS-LM diagram you drew in part (a) Will equilibrium output move closer to the natural level

c. Given your answer to part (b), what policy options are available to the government to try to increase output Consider traditional policy options only, and not financial policies. How does your answer relate to the policy decisions of the Obama administration and the U.S. Congress in February 2009 Dig Deeper

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

6

Nontraditional macroeconomic policy: financial policy and quantitative easing

Interpret the interest rate as the federal funds rate, the pol-icy interest rate of the Federal Reserve. Assume that there is an unusually high premium added to the federal funds rate when firms borrow to invest.

a. Suppose that the government takes action to improve the solvency of the financial system. If the government's action is successful, and banks become more willing to lend-both to one another and to nonfinancial firms-what is likely to happen to the premium What will happen to the IS-LM diagram Can we con-sider financial policy a kind of macroeconomic policy

b. Faced with a zero nominal interest rate, suppose the Fed decides to purchase securities directly to facilitate the flow of credit in the financial markets. This policy is called quantitative easing. If quantitative easing is successful, so that it becomes easier for financial and nonfinancial firms to obtain credit, what is likely to hap-pen to the premium What effect will this have on the 1S-LM diagram If quantitative easing has some effect, is it true that the Fed has no policy options to stimulate the economy when the federal funds rate is zero

Interpret the interest rate as the federal funds rate, the pol-icy interest rate of the Federal Reserve. Assume that there is an unusually high premium added to the federal funds rate when firms borrow to invest.

a. Suppose that the government takes action to improve the solvency of the financial system. If the government's action is successful, and banks become more willing to lend-both to one another and to nonfinancial firms-what is likely to happen to the premium What will happen to the IS-LM diagram Can we con-sider financial policy a kind of macroeconomic policy

b. Faced with a zero nominal interest rate, suppose the Fed decides to purchase securities directly to facilitate the flow of credit in the financial markets. This policy is called quantitative easing. If quantitative easing is successful, so that it becomes easier for financial and nonfinancial firms to obtain credit, what is likely to hap-pen to the premium What effect will this have on the 1S-LM diagram If quantitative easing has some effect, is it true that the Fed has no policy options to stimulate the economy when the federal funds rate is zero

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

7

Modem bank runs

Consider a simple bank that has assets of 100, capital of 20, and checking deposits of 80. Recall from Chapter 4 that checking deposits are liabilities of a bank.

a. Set up the banks' balance sheet.

b. Now suppose that the perceived value of the bank's assets falls by 10. What is the new value of the bank's capital

c. Suppose the deposits are insured by the government. Despite the decline in the value of bank capital, Is there any immediate mason for depositors to withdraw their funds from the bank Would your answer change if the perceived value of the bank's assets fell by 15 20 25 Explain.

Now consider a different sort of bank, still with assets of 100 and capital of 20,but now with short-term credit of 80 instead of checkable deposits. Short-term credit must be repaid or roiled over (borrowed again) when it comes due.

d. Set up this bank's balance sheet.

e. Again suppose the perceived value of the bank's assets falls. If lenders are nervous about the solvency of the bank, will they be willing to continue to provide short-term credit to the bank at low interest rates

f. Assuming that the bank cannot raise additional capital how can It raise the funds necessary to repay its debt coming due If many banks are in this position at the same time (and if banks hold similar kinds of assets). What will likely happen to the value of the assets of these banks How will this affect the willingness of lenders to provide short-term credit

Consider a simple bank that has assets of 100, capital of 20, and checking deposits of 80. Recall from Chapter 4 that checking deposits are liabilities of a bank.

a. Set up the banks' balance sheet.

b. Now suppose that the perceived value of the bank's assets falls by 10. What is the new value of the bank's capital

c. Suppose the deposits are insured by the government. Despite the decline in the value of bank capital, Is there any immediate mason for depositors to withdraw their funds from the bank Would your answer change if the perceived value of the bank's assets fell by 15 20 25 Explain.

Now consider a different sort of bank, still with assets of 100 and capital of 20,but now with short-term credit of 80 instead of checkable deposits. Short-term credit must be repaid or roiled over (borrowed again) when it comes due.

d. Set up this bank's balance sheet.

e. Again suppose the perceived value of the bank's assets falls. If lenders are nervous about the solvency of the bank, will they be willing to continue to provide short-term credit to the bank at low interest rates

f. Assuming that the bank cannot raise additional capital how can It raise the funds necessary to repay its debt coming due If many banks are in this position at the same time (and if banks hold similar kinds of assets). What will likely happen to the value of the assets of these banks How will this affect the willingness of lenders to provide short-term credit

Unlock Deck

Unlock for access to all 7 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 7 flashcards in this deck.