Deck 8: Cost Curves

Full screen (f)

Question

Question

Question

Question

Question

Question

A)The slope of the isocost line becomes flatter.

B)The slope of the isocost line becomes steeper.

C)The slope of the isocost line is unchanged.

D)We cannot determine whether the slope becomes flatter or steeper.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A)The slope of the isocost line becomes flatter.

B)The slope of the isocost line becomes steeper.

C)The slope of the isocost line is unchanged.

D)We cannot determine whether the slope becomes flatter or steeper.

Question

Suppose that a firm's production function can be specified as  Which of the following accurately describes this firm's long run total cost function?

Which of the following accurately describes this firm's long run total cost function?

Which of the following accurately describes this firm's long run total cost function? Question

Which of the following is not an accurate specification of a firm's long-run total cost curve? FC stands for fixed cost, VC stands for variable cost, and AC stands for average cost, below.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

When the production function is given by Q = L, which of the following statements is true?

Question

Question

Question

Question

Question

Question

Suppose  . Short run marginal cost is:

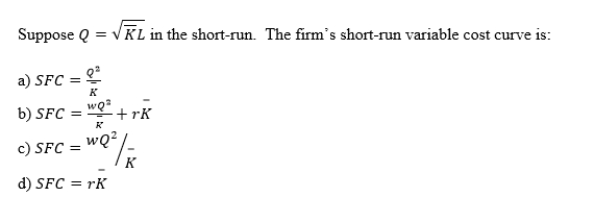

. Short run marginal cost is:

A)indeterminate, since we don't know the level of .

B)22

C)20

D)2

. Short run marginal cost is:A)indeterminate, since we don't know the level of .

B)22

C)20

D)2

Question

Question

Question

Question

Question

Question

Question

Question

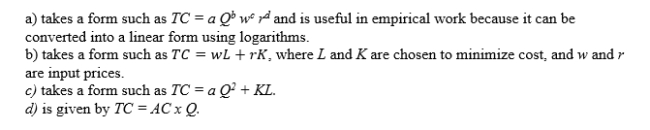

For a production process that involves two inputs, capital and labor, the constant elasticity long-run total cost function defined in linear relationship using logarithms is:

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

A constant elasticity cost function:

Question

Question

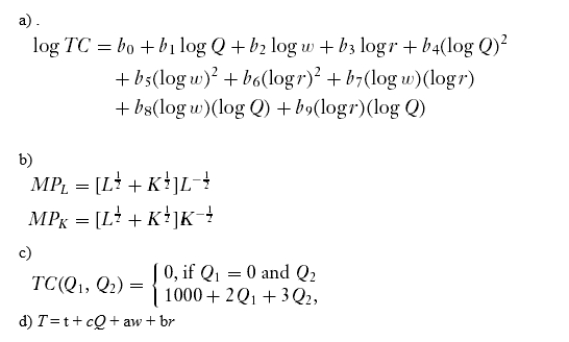

The equation of translog cost function is

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/91

Play

Full screen (f)

Deck 8: Cost Curves

1

When the prices of all inputs increase by a proportionate amount:

A)the firm's total cost curve will remain unchanged since the cost-minimizing combination of inputs is unchanged.

B)the firm's total cost curve may rotate upward or may leave the long-run total cost curve unchanged.

C)will always rotate the long-run total cost curve upward.

D)could actually rotate the long-run total cost downward if the firm chooses to produce a lower level of output.

A)the firm's total cost curve will remain unchanged since the cost-minimizing combination of inputs is unchanged.

B)the firm's total cost curve may rotate upward or may leave the long-run total cost curve unchanged.

C)will always rotate the long-run total cost curve upward.

D)could actually rotate the long-run total cost downward if the firm chooses to produce a lower level of output.

C

2

The relationship between the long-run total cost curve and the marginal and average cost curves is best described by which of the following statements?

A)The slope of the total cost curve from the origin to a point on the total cost curve is how you derive the marginal cost curve while the average cost is given by TC/Q.

B)Marginal cost is MC/Q while average cost is TC/Q.

C)Marginal cost is derived by dividing total cost by a constant as is average cost.

D)The slope of the total cost curve at each point is how you derive the marginal cost curve while the slope from the origin to a point on the total cost curve is how you derive the average cost curve.

A)The slope of the total cost curve from the origin to a point on the total cost curve is how you derive the marginal cost curve while the average cost is given by TC/Q.

B)Marginal cost is MC/Q while average cost is TC/Q.

C)Marginal cost is derived by dividing total cost by a constant as is average cost.

D)The slope of the total cost curve at each point is how you derive the marginal cost curve while the slope from the origin to a point on the total cost curve is how you derive the average cost curve.

D

3

The long-run total cost curve shows:

A)the various combinations of capital and labor that will produce different levels of output at the same cost.

B)the various combinations of capital and labor that will produce the same level of output.

C)the minimum total cost to produce any level of output, holding input prices fixed, and choosing all inputs to minimize cost.

D)for a fixed level of capital, the minimum cost to produce a given level of output.

A)the various combinations of capital and labor that will produce different levels of output at the same cost.

B)the various combinations of capital and labor that will produce the same level of output.

C)the minimum total cost to produce any level of output, holding input prices fixed, and choosing all inputs to minimize cost.

D)for a fixed level of capital, the minimum cost to produce a given level of output.

C

4

When average cost is "u-shaped" (neither always rising nor always falling), the marginal cost curve will

A)cross through (intersect)the average cost curve at its maximum.

B)not intersect with the average cost curve at all.

C)be a fixed distance above the average cost curve.

D)cross through (intersect)the average cost curve at its minimum.

A)cross through (intersect)the average cost curve at its maximum.

B)not intersect with the average cost curve at all.

C)be a fixed distance above the average cost curve.

D)cross through (intersect)the average cost curve at its minimum.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

5

A long-run total cost curve:

A)must be equal to zero when the level of output is zero.

B)may be greater than or equal to zero when the level of output is zero.

C)must be decreasing when the level of output is zero.

D)will be equal to fixed cost, which is greater than zero, when the level of output is zero.

A)must be equal to zero when the level of output is zero.

B)may be greater than or equal to zero when the level of output is zero.

C)must be decreasing when the level of output is zero.

D)will be equal to fixed cost, which is greater than zero, when the level of output is zero.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

6

A)The slope of the isocost line becomes flatter.

B)The slope of the isocost line becomes steeper.

C)The slope of the isocost line is unchanged.

D)We cannot determine whether the slope becomes flatter or steeper.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

7

A firm's long-run average cost curve is comprised of:

A)the minimum points of each of the firm's short-run average cost curves.

B)the lower envelope of the firm's short-run average cost curves.

C)the minimum points of each of the firm's short-run marginal cost curves.

D)the series of points where the short-run marginal cost curves intersect the short-run average cost curves.

A)the minimum points of each of the firm's short-run average cost curves.

B)the lower envelope of the firm's short-run average cost curves.

C)the minimum points of each of the firm's short-run marginal cost curves.

D)the series of points where the short-run marginal cost curves intersect the short-run average cost curves.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

8

When the price of all inputs increase by the same percentage:

A)the firm's total cost curve will rotate upward by a higher percentage if the firm's production technology exhibits decreasing returns to scale.

B)the firm's total cost curve will rotate upward by the same percentage.

C)the firm's total cost curve will rotate upward by a higher percentage if the firm's production technology exhibits increasing returns to scale.

D)the firm's total cost curve will remain unchanged since the cost-minimizing combination of inputs is unchanged.

A)the firm's total cost curve will rotate upward by a higher percentage if the firm's production technology exhibits decreasing returns to scale.

B)the firm's total cost curve will rotate upward by the same percentage.

C)the firm's total cost curve will rotate upward by a higher percentage if the firm's production technology exhibits increasing returns to scale.

D)the firm's total cost curve will remain unchanged since the cost-minimizing combination of inputs is unchanged.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

9

The long-run total cost curve tends to:

A)rotate upward when input prices fall.

B)rotate upward when input prices rise.

C)shift vertically upward by a fixed amount.

D)shift vertically downward by a fixed amount.

A)rotate upward when input prices fall.

B)rotate upward when input prices rise.

C)shift vertically upward by a fixed amount.

D)shift vertically downward by a fixed amount.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

10

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

11

A long-run total cost curve:

A)always has a constant slope.

B)is always upward sloping.

C)never has a constant slope.

D)is always downward sloping.

A)always has a constant slope.

B)is always upward sloping.

C)never has a constant slope.

D)is always downward sloping.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

12

The cost of producing a good in a single-product firm is:

A)additional cost

B)stand-alone cost

C)variable cost

D)average cost

A)additional cost

B)stand-alone cost

C)variable cost

D)average cost

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

13

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

14

An increase in the price of one input:

A)will always rotate the long-run total cost curve upward.

B)may rotate the long-run total cost curve upward or may leave the long-run total cost unchanged.

C)could actually rotate the long-run total cost downward.

D)will have no effect on the long-run total cost curve as long as long as the firm is using positive amounts of both inputs.

A)will always rotate the long-run total cost curve upward.

B)may rotate the long-run total cost curve upward or may leave the long-run total cost unchanged.

C)could actually rotate the long-run total cost downward.

D)will have no effect on the long-run total cost curve as long as long as the firm is using positive amounts of both inputs.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

15

The output elasticity of total cost is defined as:

A)the percentage change in output per one percent change in total cost.

B)the percentage change in total cost per one percent change in output.

C)output divided by total cost.

D)total cost divided by output.

A)the percentage change in output per one percent change in total cost.

B)the percentage change in total cost per one percent change in output.

C)output divided by total cost.

D)total cost divided by output.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

16

Cost driver is:

A)a mathematical relationship that shows how total costs vary with the factors that influence total costs

B)a factor that influences or "drives" total or average costs

C)a factor that influences quality of output and prices of inputs

D)a cost level.

A)a mathematical relationship that shows how total costs vary with the factors that influence total costs

B)a factor that influences or "drives" total or average costs

C)a factor that influences quality of output and prices of inputs

D)a cost level.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

17

A)The slope of the isocost line becomes flatter.

B)The slope of the isocost line becomes steeper.

C)The slope of the isocost line is unchanged.

D)We cannot determine whether the slope becomes flatter or steeper.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

18

Suppose that a firm's production function can be specified as Which of the following accurately describes this firm's long run total cost function?

Which of the following accurately describes this firm's long run total cost function? Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is not an accurate specification of a firm's long-run total cost curve? FC stands for fixed cost, VC stands for variable cost, and AC stands for average cost, below.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

20

An indivisible input is:

A)an input that cannot be seen by the naked eye.

B)an important input that the firm cannot identify.

C)an input that can only be obtained in a certain minimum size.

D)an input the firm cannot stop using.

A)an input that cannot be seen by the naked eye.

B)an important input that the firm cannot identify.

C)an input that can only be obtained in a certain minimum size.

D)an input the firm cannot stop using.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

21

Suppose that a firm's total costs of production are 0 at an output of zero, 10 at an output of 1, 20 at an output of 2 units, 30 at an output of three units, 35 at an output of four units and 37 at an output of five units. At which number of units are marginal and average costs equal?

A)The first unit.

B)The fifth unit.

C)The third unit.

D)At the first, second and third units.

A)The first unit.

B)The fifth unit.

C)The third unit.

D)At the first, second and third units.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

22

Marginal cost is:

A)the cost per unit of output.

B)the increase in total cost from producing an additional unit of output.

C)the same thing as total variable cost.

D)is only relevant in the long-run.

A)the cost per unit of output.

B)the increase in total cost from producing an additional unit of output.

C)the same thing as total variable cost.

D)is only relevant in the long-run.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

23

Suppose a firm produces 50,000 units of output, and determines that its marginal cost is $0.72 and its average total cost is $0.72. At this quantity of output, what is the slope of this firm's long run average total cost curve?

A)Upward-sloping.

B)Downward-sloping.

C)Horizontal.

D)Vertical.

A)Upward-sloping.

B)Downward-sloping.

C)Horizontal.

D)Vertical.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

24

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

25

Economies of scale exist when firms have:

A)increasing returns to scale.

B)constant returns to scale.

C)decreasing returns to scale.

D)constant marginal cost.

A)increasing returns to scale.

B)constant returns to scale.

C)decreasing returns to scale.

D)constant marginal cost.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

26

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following factors may explain diseconomies of scale?

A)Increasing returns to scale of inputs.

B)Specialization of labor.

C)Indivisible inputs.

D)Managerial diseconomies.

A)Increasing returns to scale of inputs.

B)Specialization of labor.

C)Indivisible inputs.

D)Managerial diseconomies.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

28

Suppose that a firm's total costs of production are 0 at an output of zero, 10 at an output of 1, 20 at an output of 2 units, 30 at an output of three units, 35 at an output of four units and 37 at an output of five units. At which number of units is average cost minimized?

A)The first unit.

B)The fifth unit.

C)The third unit.

D)At the first, second and third units.

A)The first unit.

B)The fifth unit.

C)The third unit.

D)At the first, second and third units.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

29

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

30

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

31

The output elasticity of total cost is equal to:

A)the slope of the isocost line.

B)the ratio of marginal cost to average cost.

C)the ratio of average cost to marginal cost.

D)the ratio of average cost to total cost.

A)the slope of the isocost line.

B)the ratio of marginal cost to average cost.

C)the ratio of average cost to marginal cost.

D)the ratio of average cost to total cost.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

32

If average cost is constant for all levels of output:

A)the marginal cost curve will intersect the average cost at a single point, the minimum of average cost.

B)marginal cost will be equal to average cost for all levels of output.

C)marginal cost will be above average cost when average cost is increasing and marginal cost will be below average cost when average cost is decreasing.

D)marginal cost will have a region of diminishing marginal cost.

A)the marginal cost curve will intersect the average cost at a single point, the minimum of average cost.

B)marginal cost will be equal to average cost for all levels of output.

C)marginal cost will be above average cost when average cost is increasing and marginal cost will be below average cost when average cost is decreasing.

D)marginal cost will have a region of diminishing marginal cost.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

33

Minimum efficient scale is:

A)the lowest level of efficiency the firm can achieve.

B)the highest level of output the firm can achieve.

C)the lowest level of long-run average cost.

D)the smallest quantity at which the long-run average cost achieves a minimum.

A)the lowest level of efficiency the firm can achieve.

B)the highest level of output the firm can achieve.

C)the lowest level of long-run average cost.

D)the smallest quantity at which the long-run average cost achieves a minimum.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

34

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

35

When the production function is given by Q = L, which of the following statements is true?

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

36

Marginal cost:

A)is equal to average cost at the minimum point of the marginal cost curve.

B)is equal to average cost at the maximum point of the average cost curve.

C)is decreasing whenever average cost is decreasing.

D)is equal to average cost at the minimum point of the average cost curve.

A)is equal to average cost at the minimum point of the marginal cost curve.

B)is equal to average cost at the maximum point of the average cost curve.

C)is decreasing whenever average cost is decreasing.

D)is equal to average cost at the minimum point of the average cost curve.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

37

When the output elasticity of total cost is less than one,

A)Marginal cost is less than average cost and average cost decreases as Q increases.

B)Marginal cost is less than average cost and average cost increases as Q increases.

C)Marginal cost is greater than average cost and average cost decreases as Q increases.

D)Marginal cost is greater than average cost and average cost increases as Q increases.

A)Marginal cost is less than average cost and average cost decreases as Q increases.

B)Marginal cost is less than average cost and average cost increases as Q increases.

C)Marginal cost is greater than average cost and average cost decreases as Q increases.

D)Marginal cost is greater than average cost and average cost increases as Q increases.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

38

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

39

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

40

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

41

Suppose . Short run marginal cost is:

A)indeterminate, since we don't know the level of .

B)22

C)20

D)2

. Short run marginal cost is:A)indeterminate, since we don't know the level of .

B)22

C)20

D)2

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

42

The percentage change in average variable cost for every 1 percent increase in cumulative volume is referred to as:

A)experience elasticity

B)experience curve

C)experience output

D)experience slope

A)experience elasticity

B)experience curve

C)experience output

D)experience slope

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

43

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

44

Diseconomies of scale exist when:

A)the firm's total cost falls as the level of output increases.

B)the firm's total cost increases as the level of output increases.

C)the firm's average cost decreases as the level of output decreases.

D)the firm's average cost decreases as the level of output increases.

A)the firm's total cost falls as the level of output increases.

B)the firm's total cost increases as the level of output increases.

C)the firm's average cost decreases as the level of output decreases.

D)the firm's average cost decreases as the level of output increases.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

45

Suppose the output elasticity of total cost is 1.5. This implies the average cost curve exhibits:

A)increasing returns to scale.

B)economies of scale.

C)neither economies nor diseconomies of scale.

D)diseconomies of scale.

A)increasing returns to scale.

B)economies of scale.

C)neither economies nor diseconomies of scale.

D)diseconomies of scale.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

46

Economies of experience are exhibited when:

A)it takes a professor a smaller quantity of time to prepare a lesson for a new class than for the first class he taught.

B)an older professor is more intelligent than a younger professor.

C)a professor goes into business as a consultant.

D)a professor reaches age 65 and begins to get a senior citizen discount.

A)it takes a professor a smaller quantity of time to prepare a lesson for a new class than for the first class he taught.

B)an older professor is more intelligent than a younger professor.

C)a professor goes into business as a consultant.

D)a professor reaches age 65 and begins to get a senior citizen discount.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

47

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

48

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

49

For a production process that involves two inputs, capital and labor, the constant elasticity long-run total cost function defined in linear relationship using logarithms is:

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

50

Let the average variable cost of production be $20 when 10 units are produced in the first year. In the second year, after the second 10 units have been produced, the average variable cost of production is $12. The slope of the experience curve for this firm is:

A)85%

B)60%

C)175%

D)12%

A)85%

B)60%

C)175%

D)12%

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

51

If the output elasticity of total cost is less than one, then the long-run average cost curve experiences:

A)economies of scale.

B)diseconomies of scale.

C)decreasing returns to scale.

D)the minimum efficient scale.

A)economies of scale.

B)diseconomies of scale.

C)decreasing returns to scale.

D)the minimum efficient scale.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

52

Economies of scope:

A)are related to the average cost of producing a good when you double the scale of output.

B)are higher the more specialized a firm is in production.

C)means the rotation of the long-run total cost curve in a downward direction.

D)are a production characteristic in which the total cost of producing given quantities of two goods in the same firm is less than the total cost of producing those quantities in two single-product firms.

A)are related to the average cost of producing a good when you double the scale of output.

B)are higher the more specialized a firm is in production.

C)means the rotation of the long-run total cost curve in a downward direction.

D)are a production characteristic in which the total cost of producing given quantities of two goods in the same firm is less than the total cost of producing those quantities in two single-product firms.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

53

The experience curve (also called the learning curve)shows the relationship between:

A)average total cost and output.

B)average variable cost and returns to scale.

C)output and marginal cost.

D)average variable cost and cumulative production volume.

A)average total cost and output.

B)average variable cost and returns to scale.

C)output and marginal cost.

D)average variable cost and cumulative production volume.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following factors would not explain economies of scale?

A)Increasing returns to scale of inputs.

B)Specialization of labor.

C)Indivisible inputs.

D)Managerial diseconomies

A)Increasing returns to scale of inputs.

B)Specialization of labor.

C)Indivisible inputs.

D)Managerial diseconomies

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

55

The short-run total cost curve:

A)shows the minimized total cost of producing a given quantity of output.

B)shows the outputs that correspond to minimized total cost when at least one input is fixed.

C)shows the minimized total cost of producing a given quantity of output when at least one input is fixed.

D)shows the minimized total cost of producing a given quantity of output when all inputs are fixed.

A)shows the minimized total cost of producing a given quantity of output.

B)shows the outputs that correspond to minimized total cost when at least one input is fixed.

C)shows the minimized total cost of producing a given quantity of output when at least one input is fixed.

D)shows the minimized total cost of producing a given quantity of output when all inputs are fixed.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

56

The short-run total cost curve is the sum of which two components?

A)Short-run and long-run

B)Total variable cost curve and total fixed cost curve

C)Average cost curve and marginal cost curve

D)Economies of scale and economies of scope

A)Short-run and long-run

B)Total variable cost curve and total fixed cost curve

C)Average cost curve and marginal cost curve

D)Economies of scale and economies of scope

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

57

Suppose a firm's production technology exhibits constant returns to scale. The firm's long-run average cost curve will:

A)be U-shaped

B)exhibit economies of scale.

C)exhibit diseconomies of scale.

D)be a horizontal straight line.

A)be U-shaped

B)exhibit economies of scale.

C)exhibit diseconomies of scale.

D)be a horizontal straight line.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

58

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

59

Economies of ______ occur when a single firm can produce two products together for a lower total cost than two firms could produce those same products separately, one at each firm.

A)scale.

B)scope.

C)efficiency.

D)output.

A)scale.

B)scope.

C)efficiency.

D)output.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

60

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

61

The following is not a property of the translog cost function:

A)The constant elasticity cost function is a special case of it.

B)The average cost may be U-shaped.

C)It is a good approximation for almost any production function.

D)It only applies to long run total costs.

A)The constant elasticity cost function is a special case of it.

B)The average cost may be U-shaped.

C)It is a good approximation for almost any production function.

D)It only applies to long run total costs.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

62

When the price of all inputs increase by the same percentage, the firm's total cost curve will remain unchanged since the cost-minimizing combination of inputs is unchanged.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

63

Consider the relationship between the long-run total cost curve and the marginal and average cost curve. Marginal cost is MC/Q while average cost is TC/Q.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

64

Let a firm's long run total cost be described by the constant elasticity total cost function. The coefficient of the log of output in this function is interpreted as the:

A)average cost.

B)marginal cost.

C)output elasticity of total cost.

D)cost driver.

A)average cost.

B)marginal cost.

C)output elasticity of total cost.

D)cost driver.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

65

Consider the relationship between the long-run total cost curve and the marginal and average cost curve. Marginal cost is derived by dividing total cost by a constant as is average cost.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

66

A constant elasticity cost function:

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

67

Consider the relationship between the long-run total cost curve and the marginal and average cost curve. The slope of the total cost curve at each point is how you derive the marginal cost curve while the slope from the origin to a point on the total cost curve is how you derive the average cost curve.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

68

The equation of translog cost function is

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

69

When the price of all inputs increase by the same percentage, the firm's total cost curve will rotate upward by a higher percentage if the firm's production technology exhibits decreasing returns to scale.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

70

Let a firm's long run total cost be described by the constant elasticity total cost function. The coefficients of the log of the wage and the log of capital in this function should:

A)add up to one.

B)be negative.

C)be of opposite sign.

D)of indeterminate sign.

A)add up to one.

B)be negative.

C)be of opposite sign.

D)of indeterminate sign.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

71

Marginal cost can be measured as the slope of the total cost curve.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

72

When average cost is "u-shaped" (neither always rising nor always falling), the marginal cost curve will cross through (intersect)the average cost curve at its maximum.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

73

Consider the relationship between the long-run total cost curve and the marginal and average cost curve. The slope of the total cost curve from the origin to a point on the total cost curve is how you derive the marginal cost curve while the average cost is given by TC/Q.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

74

When the price of all inputs increase by the same percentage, the firm's total cost curve will rotate upward by a higher percentage if the firm's production technology exhibits increasing returns to scale.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

75

When average cost is "u-shaped" (neither always rising nor always falling), the marginal cost curve will not intersect with the average cost curve at all.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

76

When average cost is "u-shaped" (neither always rising nor always falling), the marginal cost curve will cross through (intersect)the average cost curve at its minimum.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

77

When marginal cost is rising, average total cost is rising.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

78

When average cost is "u-shaped" (neither always rising nor always falling), the marginal cost curve will be a fixed distance above the average cost curve.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

79

Average total cost can be measured as the slope of the ray from the origin to the total cost curve.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

80

When the price of all inputs increase by the same percentage, the firm's total cost curve will rotate upward by the same percentage.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 91 flashcards in this deck.