Deck 8: Perfect Competition

Full screen (f)

Question

Question

Question

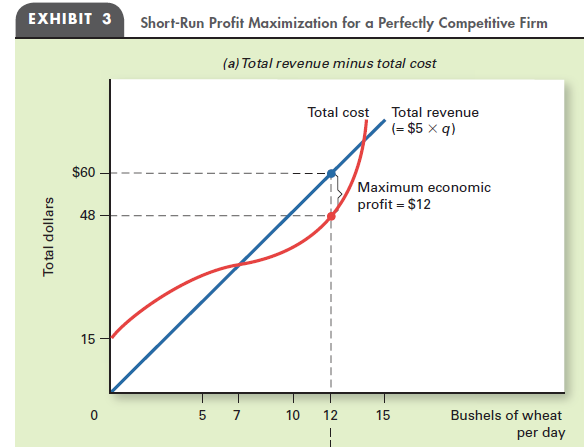

Total Revenue Look back at Exhibit 3, panel (a), in this chapter. Explain why the total revenue curve is a straight line from the origin, whereas the slope of the total cost curve changes

Question

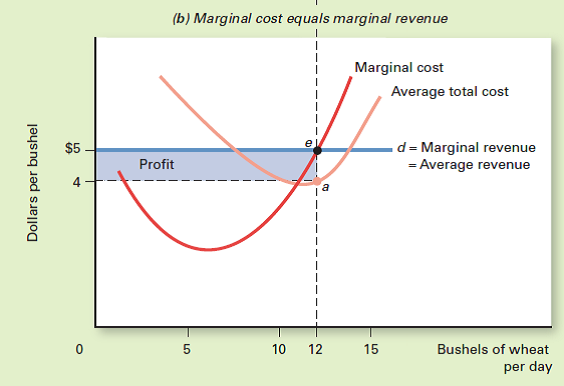

Profit in the Short Run Look back at Exhibit 3, panel (b), in this chapter. Why doesn't the firm choose the output that maximizes average profit (i.e., the output where average cost is the lowest)?

Question

Question

Question

Question

Question

Question

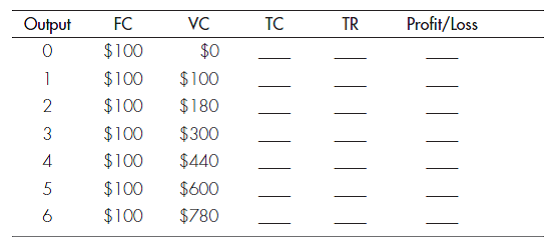

SHORT-RUN PROFIT MAXIMIZATION A perfectly competitive firm has the following fixed and variable costs in the short run. The market price for the firm's product is $150.

a. Complete the table.

b. At what output rate does the firm maximize profit or minimize loss?

c. What is the firm's marginal revenue at each positive rate of output? Its average revenue?

d. What can you say about the relationship between marginal revenue and marginal cost for output rates below the profit-maximizing (or loss-minimizing) rate? For output rates above the profit-maximizing (or loss-minimizing) rate?

a. Complete the table.

b. At what output rate does the firm maximize profit or minimize loss?

c. What is the firm's marginal revenue at each positive rate of output? Its average revenue?

d. What can you say about the relationship between marginal revenue and marginal cost for output rates below the profit-maximizing (or loss-minimizing) rate? For output rates above the profit-maximizing (or loss-minimizing) rate?

Question

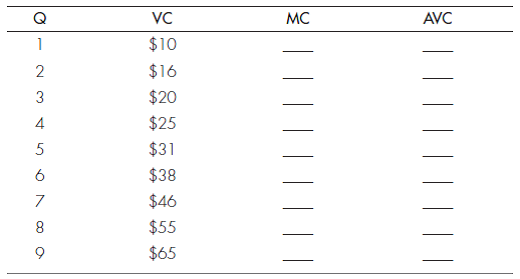

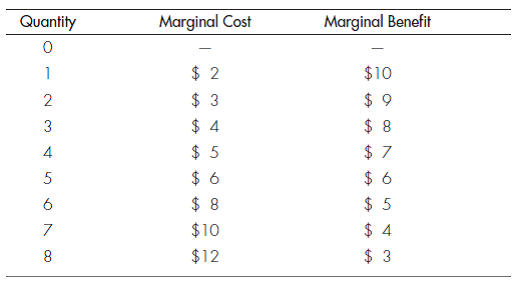

THE SHORT-RUN FIRM SUPPLY CURVE Use the following data to answer the questions below:

a. Calculate the marginal cost and average variable cost for each rate of output.

b. How much would the firm produce if it could sell its product for $5? For $7? For $10?

c. Explain your answers.

d. Assuming that its fixed cost is $3, calculate the firm's economic profit at each output rate determined in part (b).

a. Calculate the marginal cost and average variable cost for each rate of output.

b. How much would the firm produce if it could sell its product for $5? For $7? For $10?

c. Explain your answers.

d. Assuming that its fixed cost is $3, calculate the firm's economic profit at each output rate determined in part (b).

Question

Question

Question

Question

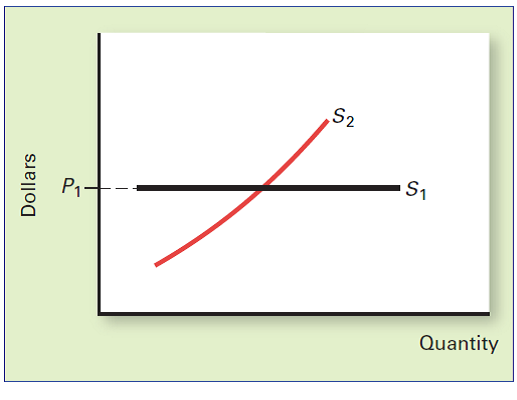

THE LONG-RUN INDUSTRY SUPPLY CURVE The following graph shows possible long-run market supply curves for a perfectly competitive industry. Determine which supply curve indicates a constant-cost industry and which an increasing-cost industry.

a. Explain the difference between a constant-cost industry and an increasing-cost industry.

b. Distinguish between the long-run impact of an increase of market demand in a constant-cost industry and the impact in an increasing-cost industry.

a. Explain the difference between a constant-cost industry and an increasing-cost industry.

b. Distinguish between the long-run impact of an increase of market demand in a constant-cost industry and the impact in an increasing-cost industry.

Question

WHAT'S SO PERFECT ABOUT PERFECT COMPETITION Use the following data to answer the questions.

a. For the product shown, assume that the minimum point of each firm's average variable cost curve is at $2. Construct a demand and supply diagram for the product and indicate the equilibrium price and quantity.

b. On the graph, label the area of consumer surplus as f. Label the area of producer surplus as g.

c. If the equilibrium price were $2, what would be the amount of producer surplus?

a. For the product shown, assume that the minimum point of each firm's average variable cost curve is at $2. Construct a demand and supply diagram for the product and indicate the equilibrium price and quantity.

b. On the graph, label the area of consumer surplus as f. Label the area of producer surplus as g.

c. If the equilibrium price were $2, what would be the amount of producer surplus?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/16

Play

Full screen (f)

Deck 8: Perfect Competition

1

MARKET STRUCTURE Define market structure. What factors are considered in determining the market structure of a particular industry?

Market structure:

Market refers to a place or medium where buyers and sellers trade their goods. Market structure refers to the characteristic features of the market that is determined by the behavior of the market.

• Perfect competition refers to the market structure with the features of more number of sellers and buyers in the market. Firms sell homogenous products. Price is fixed by the market demand and supply. Individual firm cannot change the price. Firms can easily enter or exit from the market. Firms and consumers are well informed about the market. Firms are competing with each other.

• Monopoly refers to the market structure with the features of a single seller and more buyers. Firms have full control over the market. Price is fixed by the monopoly producer. There is a restriction for entry of a firm.

• Oligopoly refers to the market structure with the features of a few sellers and more buyers. Firms are producing homogenous goods. Firms are competing with themselves. There is no easy entry into the market due to the huge investment. Information about the market is not available.• Monopolistic competition refers to the market structure with the features of more buyers and more sellers. Each firm sells the homogenous product with a different brand name. Firms can easily enter or exit from the market.

Following are the factors to determine the market structure:

• Number of buyers and sellers.

• Degree of uniformity.

• Easy entry into and exit from the market.

• Competition among the firms.

Market refers to a place or medium where buyers and sellers trade their goods. Market structure refers to the characteristic features of the market that is determined by the behavior of the market.

• Perfect competition refers to the market structure with the features of more number of sellers and buyers in the market. Firms sell homogenous products. Price is fixed by the market demand and supply. Individual firm cannot change the price. Firms can easily enter or exit from the market. Firms and consumers are well informed about the market. Firms are competing with each other.

• Monopoly refers to the market structure with the features of a single seller and more buyers. Firms have full control over the market. Price is fixed by the monopoly producer. There is a restriction for entry of a firm.

• Oligopoly refers to the market structure with the features of a few sellers and more buyers. Firms are producing homogenous goods. Firms are competing with themselves. There is no easy entry into the market due to the huge investment. Information about the market is not available.• Monopolistic competition refers to the market structure with the features of more buyers and more sellers. Each firm sells the homogenous product with a different brand name. Firms can easily enter or exit from the market.

Following are the factors to determine the market structure:

• Number of buyers and sellers.

• Degree of uniformity.

• Easy entry into and exit from the market.

• Competition among the firms.

2

DEMAND UNDER PERFECT COMPETITION What type of demand curve does a perfectly competitive firm face? Why?

Perfect competition:

Perfect competition refers to the market structure with the features of more number of sellers and buyers in the market. Firms sell homogenous products. Price is fixed by the market demand and supply.

Individual firm cannot change the price. Firms can easily enter or exit from the market. Firms and consumers are well informed about the market. Firms are competing with each other.

Demand refers to the desire and ability of the consumer to buy goods and services at the prevailing price.Demand Curve:

Demand curve refers to the graph that illustrates the amount of goods and services demanded at various levels of price. Since , demand curve is negatively related to price, it falls from left to right.

Shape of demand curve in the perfect competition:

In the perfect competition, prices of goods and services are determined by the market demand and supply. Therefore, firms are price takers. Firms are selling their product as much as they can sell in the market at the prevailing price. If a particular firm increases the price slightly, then consumers do not buy the product from that particular seller. Hence, the demand curve is horizon tal.

Perfect competition refers to the market structure with the features of more number of sellers and buyers in the market. Firms sell homogenous products. Price is fixed by the market demand and supply.

Individual firm cannot change the price. Firms can easily enter or exit from the market. Firms and consumers are well informed about the market. Firms are competing with each other.

Demand refers to the desire and ability of the consumer to buy goods and services at the prevailing price.Demand Curve:

Demand curve refers to the graph that illustrates the amount of goods and services demanded at various levels of price. Since , demand curve is negatively related to price, it falls from left to right.

Shape of demand curve in the perfect competition:

In the perfect competition, prices of goods and services are determined by the market demand and supply. Therefore, firms are price takers. Firms are selling their product as much as they can sell in the market at the prevailing price. If a particular firm increases the price slightly, then consumers do not buy the product from that particular seller. Hence, the demand curve is horizon tal.

3

Total Revenue Look back at Exhibit 3, panel (a), in this chapter. Explain why the total revenue curve is a straight line from the origin, whereas the slope of the total cost curve changes

Revenue generated from total sales of goods and services is called total revenue. Total cost refers to costs that are involved (incurred) in the production of goods and services. It would vary with the quantity of production.

Price in the perfect competition is fixed. Hence, firms can sell any amount of goods at the prevailing market price. Cost of the product does not have any impact on the total revenue. Therefore, the total revenue is a straight line.Perfect competition refers to the market structure with the features of more number of sellers and buyers in the market.

The production involves both diminishing returns and increasing returns due to economies of scale. Therefore, the cost of production varies throughout production. Hence, the slope of the total cost curve changes.

Price in the perfect competition is fixed. Hence, firms can sell any amount of goods at the prevailing market price. Cost of the product does not have any impact on the total revenue. Therefore, the total revenue is a straight line.Perfect competition refers to the market structure with the features of more number of sellers and buyers in the market.

The production involves both diminishing returns and increasing returns due to economies of scale. Therefore, the cost of production varies throughout production. Hence, the slope of the total cost curve changes.

4

Profit in the Short Run Look back at Exhibit 3, panel (b), in this chapter. Why doesn't the firm choose the output that maximizes average profit (i.e., the output where average cost is the lowest)?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

5

THE SHORT-RUN FIRM SUPPLY CURVE An individual competitive firm's short-run supply curve is the portion of its marginal cost curve that equals and rises above the average variable cost. Explain why.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

6

ZERO ECONOMIC PROFITS IN THE LONG RUN Why would firms choose to operate in a perfectly competitive market even though they earn no economic profit in the long run?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

7

LONG-RUN INDUSTRY SUPPLY Why does the long-run industry supply curve for an increasing-cost industry slope up to the right? What increases costs in an increasing-cost industry?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

8

PERFECT COMPETITION AND EFFICIENCY Define productive efficiency and allocative efficiency. What conditions must be met to achieve them?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

9

Case Study: Experimental Economics

In Professor Vernon Smith's experiment, which "buyers" ended up with a surplus at the market-clearing price of $2? Which "sellers" had a surplus? Which "buyers" or "sellers" did not engage in transactions?

In Professor Vernon Smith's experiment, which "buyers" ended up with a surplus at the market-clearing price of $2? Which "sellers" had a surplus? Which "buyers" or "sellers" did not engage in transactions?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

10

SHORT-RUN PROFIT MAXIMIZATION A perfectly competitive firm has the following fixed and variable costs in the short run. The market price for the firm's product is $150.

a. Complete the table.

b. At what output rate does the firm maximize profit or minimize loss?

c. What is the firm's marginal revenue at each positive rate of output? Its average revenue?

d. What can you say about the relationship between marginal revenue and marginal cost for output rates below the profit-maximizing (or loss-minimizing) rate? For output rates above the profit-maximizing (or loss-minimizing) rate?

a. Complete the table.

b. At what output rate does the firm maximize profit or minimize loss?

c. What is the firm's marginal revenue at each positive rate of output? Its average revenue?

d. What can you say about the relationship between marginal revenue and marginal cost for output rates below the profit-maximizing (or loss-minimizing) rate? For output rates above the profit-maximizing (or loss-minimizing) rate?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

11

THE SHORT-RUN FIRM SUPPLY CURVE Use the following data to answer the questions below:

a. Calculate the marginal cost and average variable cost for each rate of output.

b. How much would the firm produce if it could sell its product for $5? For $7? For $10?

c. Explain your answers.

d. Assuming that its fixed cost is $3, calculate the firm's economic profit at each output rate determined in part (b).

a. Calculate the marginal cost and average variable cost for each rate of output.

b. How much would the firm produce if it could sell its product for $5? For $7? For $10?

c. Explain your answers.

d. Assuming that its fixed cost is $3, calculate the firm's economic profit at each output rate determined in part (b).

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

12

THE SHORT-RUN FIRM SUPPLY CURVE Each of the following situations could exist for a perfectly competitive firm in the short run. In each case, indicate whether the firm should produce in the short run or shut down in the short run, or whether additional information is needed to determine what it should do in the short run.

a. Total cost exceeds total revenue at all output levels.

b. Total variable cost exceeds total revenue at all output levels.

c. Total revenue exceeds total fixed cost at all output levels.

d. Marginal revenue exceeds marginal cost at the current output level.

e. Price exceeds average total cost at all output levels.

f. Average variable cost exceeds price at all output levels.

g. Average total cost exceeds price at all output levels.

a. Total cost exceeds total revenue at all output levels.

b. Total variable cost exceeds total revenue at all output levels.

c. Total revenue exceeds total fixed cost at all output levels.

d. Marginal revenue exceeds marginal cost at the current output level.

e. Price exceeds average total cost at all output levels.

f. Average variable cost exceeds price at all output levels.

g. Average total cost exceeds price at all output levels.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

13

PERFECT COMPETITION IN THE LONG RUN Draw the short-and long-run cost curves for a competitive firm in long-run equilibrium. Indicate the long-run equilibrium price and quantity.

a. Discuss the firm's short-run response to a reduction in the price of a variable resource.

b. Assuming that this is a constant-cost industry, describe the process by which the industry returns to long-run equilibrium following an increase of market demand.

a. Discuss the firm's short-run response to a reduction in the price of a variable resource.

b. Assuming that this is a constant-cost industry, describe the process by which the industry returns to long-run equilibrium following an increase of market demand.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

14

THE LONG-RUN INDUSTRY SUPPLY CURVE A normal good is being produced in a constant-cost, perfectly competitive industry. Initially, each firm is in long-run equilibrium.

a. Graphically illustrate and explain the short-run adjustments for the market and the firm to a decrease in consumer incomes. Be sure to discuss any changes in output levels, prices, profits, and the number of firms.

b. Next, show on your graph and explain the long-run adjustment to that income change. Be sure to discuss any changes in output levels, prices, profits, and the number of firms.

a. Graphically illustrate and explain the short-run adjustments for the market and the firm to a decrease in consumer incomes. Be sure to discuss any changes in output levels, prices, profits, and the number of firms.

b. Next, show on your graph and explain the long-run adjustment to that income change. Be sure to discuss any changes in output levels, prices, profits, and the number of firms.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

15

THE LONG-RUN INDUSTRY SUPPLY CURVE The following graph shows possible long-run market supply curves for a perfectly competitive industry. Determine which supply curve indicates a constant-cost industry and which an increasing-cost industry.

a. Explain the difference between a constant-cost industry and an increasing-cost industry.

b. Distinguish between the long-run impact of an increase of market demand in a constant-cost industry and the impact in an increasing-cost industry.

a. Explain the difference between a constant-cost industry and an increasing-cost industry.

b. Distinguish between the long-run impact of an increase of market demand in a constant-cost industry and the impact in an increasing-cost industry.

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

16

WHAT'S SO PERFECT ABOUT PERFECT COMPETITION Use the following data to answer the questions.

a. For the product shown, assume that the minimum point of each firm's average variable cost curve is at $2. Construct a demand and supply diagram for the product and indicate the equilibrium price and quantity.

b. On the graph, label the area of consumer surplus as f. Label the area of producer surplus as g.

c. If the equilibrium price were $2, what would be the amount of producer surplus?

a. For the product shown, assume that the minimum point of each firm's average variable cost curve is at $2. Construct a demand and supply diagram for the product and indicate the equilibrium price and quantity.

b. On the graph, label the area of consumer surplus as f. Label the area of producer surplus as g.

c. If the equilibrium price were $2, what would be the amount of producer surplus?

Unlock Deck

Unlock for access to all 16 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 16 flashcards in this deck.