Deck 5: Audit Evidence

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

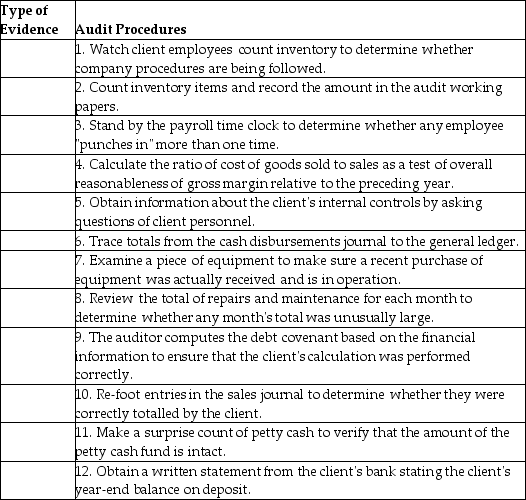

Below are 12 audit procedures.Classify each procedure according to the following types of audit evidence: 1)inspection,2)external confirmation,3)recalculation,4)observation,5)inquiry of the client,6)reperformance,and 7)analytical procedure.

Question

Question

Question

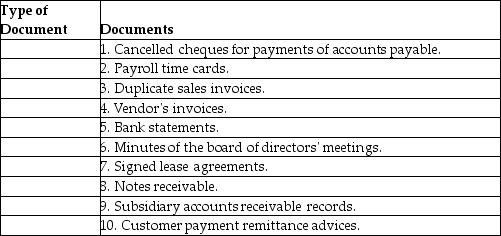

A)Distinguish between internal documentation and external documentation as types of audit evidence.Give two examples of each.Which type is considered more reliable? B)Below are 10 documents typically examined by auditors.Classify each document as either internal or external.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/91

Play

Full screen (f)

Deck 5: Audit Evidence

1

List the various judgments and conclusions that auditors make with the help of evidence gathered in all phases of the audit process.-to accept (or continue with)the client.

-to plan the audit.

-to decide where there could be a risk of material misstatement in the financial statements.

-to develop an appropriate risk response.

-to conclude on the type of audit report to be issued.

-to plan the audit.

-to decide where there could be a risk of material misstatement in the financial statements.

-to develop an appropriate risk response.

-to conclude on the type of audit report to be issued.

Judgments and conclusions that auditors make with the help of evidence gathered in all phases of the audit process are:

2

List the purposes and types of audit procedures used by auditors in all phases of the audit process.

Purposes of audit procedures used by auditors in all phases of the audit process are:

-to conduct risk assessment.

-to conduct test of controls.

-to conduct substantive procedures.

Types of audit procedures used by auditors in all phases of the audit process are:

-inspection.

-observation.

-inquiry.

-confirmation.

-recalculation.

-reperformance.

-analytical procedures.

-to conduct risk assessment.

-to conduct test of controls.

-to conduct substantive procedures.

Types of audit procedures used by auditors in all phases of the audit process are:

-inspection.

-observation.

-inquiry.

-confirmation.

-recalculation.

-reperformance.

-analytical procedures.

3

Evidence is generally considered appropriate when

A)it has the qualities of being relevant,objective,and free from known bias.

B)there is enough of it to afford a reasonable basis for an opinion on financial statements.

C)it has been obtained by random selection.

D)it consists of written statements made by managers of the enterprise under audit.

A)it has the qualities of being relevant,objective,and free from known bias.

B)there is enough of it to afford a reasonable basis for an opinion on financial statements.

C)it has been obtained by random selection.

D)it consists of written statements made by managers of the enterprise under audit.

A

4

Gina is performing the audit of the payables section of Reno Inc.She wants to confirm the payables from an independent source.Which of the following actions would achieve this?

A)Confirm an interco payable with the CEO of the US branch of Reno Inc.

B)Confirm the account payable with Clarkson Corp.The CFO of Clarkson is the wife of the controller of Reno.

C)Confirm the line of credit balance with Citizen Bank.Reno does all its banking with Citizen and it also has a long-term loan there.

D)Confirm the account payable to Suco Inc.The CEO of Reno owns 30% of the outstanding shares of Suco.

A)Confirm an interco payable with the CEO of the US branch of Reno Inc.

B)Confirm the account payable with Clarkson Corp.The CFO of Clarkson is the wife of the controller of Reno.

C)Confirm the line of credit balance with Citizen Bank.Reno does all its banking with Citizen and it also has a long-term loan there.

D)Confirm the account payable to Suco Inc.The CEO of Reno owns 30% of the outstanding shares of Suco.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

5

An audit program is

A)a set of specifications of audit standards relevant to the financial statements being audited.

B)a set of documentation of the assertions under audit,the evidence obtained,and the conclusions reached.

C)a set of reconciliations of the account balances in the financial statements with the account balances in the auditee's general ledger

D)a set of detailed instructions for the entire collection of evidence for an audit area.

A)a set of specifications of audit standards relevant to the financial statements being audited.

B)a set of documentation of the assertions under audit,the evidence obtained,and the conclusions reached.

C)a set of reconciliations of the account balances in the financial statements with the account balances in the auditee's general ledger

D)a set of detailed instructions for the entire collection of evidence for an audit area.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

6

In determining the quantity and quality of evidence to gather,the auditor will be satisfied when the evidence is

A)irrefutable.

B)conclusive.

C)highly persuasive.

D)sufficiently convincing.

A)irrefutable.

B)conclusive.

C)highly persuasive.

D)sufficiently convincing.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

7

Those procedures specifically outlined in an audit program are primarily designed to

A)prevent litigation.

B)detect errors or irregularities.

C)test internal controls.

D)collect evidence.

A)prevent litigation.

B)detect errors or irregularities.

C)test internal controls.

D)collect evidence.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

8

"The detailed instructions for the collection of a particular type of audit evidence" is the definition of a(n)

A)sampling plan.

B)audit procedure.

C)audit plan.

D)audit program.

A)sampling plan.

B)audit procedure.

C)audit plan.

D)audit program.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

9

Last year,the client's internal controls were weak.This year,the internal controls are stronger.This means that information recorded on internal documentation is

A)more timely.

B)less reliable.

C)more reliable.

D)less timely.

A)more timely.

B)less reliable.

C)more reliable.

D)less timely.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

10

The auditor is tracing from the duplicate sales invoices to related shipping documents with respect to the occurrence transaction-related audit objective.This type of evidence is

A)independent.

B)relevant.

C)timely.

D)related to external documentation.

A)independent.

B)relevant.

C)timely.

D)related to external documentation.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

11

Which is the essence of professional skepticism?

A)The auditor has interviewed client management for any changes in the business and industry.

B)The auditor has performed a critical evaluation of audit evidence.

C)The auditor has reviewed prior-year working papers and permanent file documents.

D)The auditor has taken a tour of a client's physical facilities,noting obvious inventory obsolescence or equipment maintenance issues.

A)The auditor has interviewed client management for any changes in the business and industry.

B)The auditor has performed a critical evaluation of audit evidence.

C)The auditor has reviewed prior-year working papers and permanent file documents.

D)The auditor has taken a tour of a client's physical facilities,noting obvious inventory obsolescence or equipment maintenance issues.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

12

The Bank of New Haven relies heavily on computers to calculate the settlements of amounts due to other banks.Given that the process is highly automated,the auditor would not be able to obtain sufficient evidence with substantive procedures.The auditors of the Bank of New Haven should

A)design and perform tests of controls.

B)qualify the opinion for the section on settlements.

C)hire a specialist to give an opinion on the proper functioning of the system.

D)perform a walkthrough of the system.

A)design and perform tests of controls.

B)qualify the opinion for the section on settlements.

C)hire a specialist to give an opinion on the proper functioning of the system.

D)perform a walkthrough of the system.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

13

How frequently does the auditor make a decision with respect to the sample size to be selected?

A)once for the entire audit

B)for each transaction cycle

C)once for each type of audit procedure

D)for each audit procedure

A)once for the entire audit

B)for each transaction cycle

C)once for each type of audit procedure

D)for each audit procedure

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following audit techniques would the auditor use to test the completeness of sales (i.e. ,test whether shipments have been billed to customers)?

A)trace shipping documents to duplicate sales invoices

B)trace duplicate sales invoices to shipping documents

C)match data file versions of sales invoices to paper records

D)look at subsequent payments after the year end for payments for outstanding invoices

A)trace shipping documents to duplicate sales invoices

B)trace duplicate sales invoices to shipping documents

C)match data file versions of sales invoices to paper records

D)look at subsequent payments after the year end for payments for outstanding invoices

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

15

"The detailed instructions for the entire collection of evidence for an audit area" is the definition of a(n)

A)sampling plan.

B)audit procedure.

C)audit plan.

D)audit program.

A)sampling plan.

B)audit procedure.

C)audit plan.

D)audit program.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

16

The two most important factors that determine the appropriate sample size in audits are

A)the auditor's expectation of errors and the effectiveness of the client's internal controls.

B)the auditor's expectation of errors and materiality.

C)the effectiveness of the client's internal controls and materiality.

D)materiality and the type of audit procedure to be applied to the population.

A)the auditor's expectation of errors and the effectiveness of the client's internal controls.

B)the auditor's expectation of errors and materiality.

C)the effectiveness of the client's internal controls and materiality.

D)materiality and the type of audit procedure to be applied to the population.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

17

The auditor's decisions regarding evidence accumulation can be broken into various decisions.One decision relates to determining the nature of the audit procedure to be used to collect the evidence;i.e. ,"which audit procedures to use." Identify and discuss the remaining audit evidence decisions that the auditor makes.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following types of evidence would be considered most reliable in the audit of accounts payable?

A)review of internal budgets for the period under audit

B)inquiry of management with respect to recent purchases

C)inspection of client purchase orders

D)inspection of supplier invoices

A)review of internal budgets for the period under audit

B)inquiry of management with respect to recent purchases

C)inspection of client purchase orders

D)inspection of supplier invoices

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following types of evidence is most appropriate in the audit of fixed assets?

A)recalculation of the amortization schedule provided by the client

B)auditor inspection of recently acquired fixed assets

C)reperformance of the posting of depreciation expenses to the general ledger

D)analytical review to assess the reasonableness of depreciation expense

A)recalculation of the amortization schedule provided by the client

B)auditor inspection of recently acquired fixed assets

C)reperformance of the posting of depreciation expenses to the general ledger

D)analytical review to assess the reasonableness of depreciation expense

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

20

To improve the appropriateness of audit evidence,the auditor should

A)be sure to select a larger sample size for the items being tested.

B)add additional population items into the sample to improve sample variety.

C)select audit procedures that improve the reliability of the evidence.

D)select a smaller sample size that is statistically valid.

A)be sure to select a larger sample size for the items being tested.

B)add additional population items into the sample to improve sample variety.

C)select audit procedures that improve the reliability of the evidence.

D)select a smaller sample size that is statistically valid.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is an example of subjective evidence?

A)a positive confirmation of an account receivable

B)a bank confirmation

C)inquiries of the credit manager about the collectability of noncurrent accounts receivable

D)the physical count of securities and cash

A)a positive confirmation of an account receivable

B)a bank confirmation

C)inquiries of the credit manager about the collectability of noncurrent accounts receivable

D)the physical count of securities and cash

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

22

Inspection of assets is not a sufficient form of evidence when the auditor wants to determine the

A)existence of the asset.

B)quantity and description of the asset.

C)condition or quality of the asset.

D)ownership of the asset.

A)existence of the asset.

B)quantity and description of the asset.

C)condition or quality of the asset.

D)ownership of the asset.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

23

Reperformance is often conducted using computer-assisted audit techniques.The most effective use of generalized audit software for reperformance would be to

A)recalculate a whole class of transactions,helping to quantify dollar errors.

B)determine on a test basis whether posting and summarization is performed accurately.

C)confirm whether evidence has been recorded for the entire period under audit.

D)select a sample of transactions for recalculation.

A)recalculate a whole class of transactions,helping to quantify dollar errors.

B)determine on a test basis whether posting and summarization is performed accurately.

C)confirm whether evidence has been recorded for the entire period under audit.

D)select a sample of transactions for recalculation.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

24

Identify and explain the three determinants of the persuasiveness of evidence.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

25

For each of the following audit procedures,state and describe the type of audit evidence,state the audit assertion that it applies to,and describe the reliability of the evidence (with reasons).

A)Watch staff scan products and enter cash received.

B)Reconcile daily cash drawer receipts (cash,debit card sales,credit card sales)with daily sales for one week.

C)Calculate daily gross profit and gross profit by product line.

D)Account for a sequence of sales documents.

A)Watch staff scan products and enter cash received.

B)Reconcile daily cash drawer receipts (cash,debit card sales,credit card sales)with daily sales for one week.

C)Calculate daily gross profit and gross profit by product line.

D)Account for a sequence of sales documents.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following characteristics of samples would make the sample more sufficient?

A)Samples that contain at least one of each type of transaction that is in the population and have a high number of sample items.

B)Samples that contain items with a high likelihood of error and have large dollar values as well as being representative of the population.

C)Samples that contain multiple items from different layers of the population (strata)as well as all items that are above the materiality threshold.

D)Samples that contain items that have a high likelihood of error as well as being related to the audit assertions that are being tested.

A)Samples that contain at least one of each type of transaction that is in the population and have a high number of sample items.

B)Samples that contain items with a high likelihood of error and have large dollar values as well as being representative of the population.

C)Samples that contain multiple items from different layers of the population (strata)as well as all items that are above the materiality threshold.

D)Samples that contain items that have a high likelihood of error as well as being related to the audit assertions that are being tested.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

27

Evidence is usually more persuasive for balance sheet accounts when it is obtained

A)from various time periods throughout the client's year.

B)only from transactions occurring on the balance sheet date.

C)as close to the balance sheet date as possible.

D)from the time period when transactions in that account were most numerous during the fiscal period.

A)from various time periods throughout the client's year.

B)only from transactions occurring on the balance sheet date.

C)as close to the balance sheet date as possible.

D)from the time period when transactions in that account were most numerous during the fiscal period.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

28

Audit evidence is generally considered sufficient when

A)it is appropriate.

B)there is enough of it to afford a reasonable basis for an opinion on financial statements.

C)it has the qualities of being relevant,objective,and free from known bias.

D)it has been obtained by random selection.

A)it is appropriate.

B)there is enough of it to afford a reasonable basis for an opinion on financial statements.

C)it has the qualities of being relevant,objective,and free from known bias.

D)it has been obtained by random selection.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

29

Mary is entering a fictitious transaction in the sales data entry system to see if the system will reject the order for a client that is already exceeding its credit limit.Mary is using

A)observation.

B)analytical procedures.

C)test data.

D)generalized audit software.

A)observation.

B)analytical procedures.

C)test data.

D)generalized audit software.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

30

For income statement accounts,evidence is more persuasive if there is a sample from

A)the entire period under audit.

B)the period closest to the end of the fiscal period.

C)at least three months of the fiscal year.

D)December,since this would include large holiday sales.

A)the entire period under audit.

B)the period closest to the end of the fiscal period.

C)at least three months of the fiscal year.

D)December,since this would include large holiday sales.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

31

A PA is planning the audit of Lowden's Company.Lowden verbally asserts to the PA that all the expenses for the year have been recorded in the accounts.Lowden's representation

A)should be disregarded because it is not in writing.

B)can enable the PA to minimize his work during control testing for the completeness of expenses.

C)is sufficient evidence for the PA to conclude that the completeness assertion is supported for the expenses.

D)is not considered a sufficient basis for the PA to conclude that all expenses have been recorded.

A)should be disregarded because it is not in writing.

B)can enable the PA to minimize his work during control testing for the completeness of expenses.

C)is sufficient evidence for the PA to conclude that the completeness assertion is supported for the expenses.

D)is not considered a sufficient basis for the PA to conclude that all expenses have been recorded.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

32

Evidence can be obtained from others or provided by the auditor who has good knowledge of each industry but is not an expert.Which of the following types of evidence is considered to be most reliable?

A)examination of diamond inventory by the auditor

B)external confirmations from individual owners of condominium units

C)examination of oil and gas reserves by the auditor

D)external confirmations from financial institutions

A)examination of diamond inventory by the auditor

B)external confirmations from individual owners of condominium units

C)examination of oil and gas reserves by the auditor

D)external confirmations from financial institutions

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

33

The decision of how many items to test must be made by the auditor for each audit procedure.The sample size for any given procedure

A)will be the same if the same level of assurance is required.

B)must cover the entire period under audit.

C)is focused on high-dollar-value items only.

D)is likely to vary from audit to audit.

A)will be the same if the same level of assurance is required.

B)must cover the entire period under audit.

C)is focused on high-dollar-value items only.

D)is likely to vary from audit to audit.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

34

Audit evidence can come in different forms with different degrees of persuasiveness.Which of the following is the least persuasive type of evidence?

A)bank statement obtained from the client

B)computations made by the auditor

C)prenumbered client sales invoices

D)a vendor's invoice

A)bank statement obtained from the client

B)computations made by the auditor

C)prenumbered client sales invoices

D)a vendor's invoice

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

35

There are six factors that affect the reliability of audit evidence.One factor is the independence of the provider (i.e. ,evidence obtained from a source outside the client company is more reliable than that obtained within).Identify and discuss the remaining five factors that affect the reliability of evidence.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

36

Confirmations from outside organizations such as banks and law firms are

A)a highly regarded and often-used type of evidence.

B)expensive and rarely used during the audit.

C)difficult to obtain and infrequently required.

D)internal documents that provide low-quality evidence.

A)a highly regarded and often-used type of evidence.

B)expensive and rarely used during the audit.

C)difficult to obtain and infrequently required.

D)internal documents that provide low-quality evidence.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is the best example of objective evidence?

A)a letter written by a client's lawyer discussing the likely outcome of outstanding lawsuits

B)the physical count of securities and cash by the auditor

C)inquiries of the credit manager about the collectability of noncurrent accounts receivable

D)observation of cobwebs on some inventory bins

A)a letter written by a client's lawyer discussing the likely outcome of outstanding lawsuits

B)the physical count of securities and cash by the auditor

C)inquiries of the credit manager about the collectability of noncurrent accounts receivable

D)observation of cobwebs on some inventory bins

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

38

Observation is an important audit technique where the auditor can use sight,hearing,touch,and smell.Observation needs to be used together with other audit techniques because

A)employees will often perform their procedures consistently over time.

B)it is a high-cost technique that is rarely used by auditors.

C)it is a point-in-time technique limited to the time of the observation.

D)auditors may not accurately observe and interpret what is happening.

A)employees will often perform their procedures consistently over time.

B)it is a high-cost technique that is rarely used by auditors.

C)it is a point-in-time technique limited to the time of the observation.

D)auditors may not accurately observe and interpret what is happening.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

39

Which one of the following forms of evidence would be least reliable?

A)monthly bank statement

B)positive confirmation of customer's balance

C)a letter from client's lawyer stating that there are no known lawsuits pending against client

D)client's file copy of a purchase requisition

A)monthly bank statement

B)positive confirmation of customer's balance

C)a letter from client's lawyer stating that there are no known lawsuits pending against client

D)client's file copy of a purchase requisition

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

40

Although considerable evidence is obtained from the client through inquiry,it usually cannot be regarded as conclusive because

A)the client may not have sufficient knowledge to answer the question.

B)it is not from an independent source and may be biased.

C)there is a risk that the auditor will misinterpret what the client said.

D)the client cannot be trusted to provide persuasive information.

A)the client may not have sufficient knowledge to answer the question.

B)it is not from an independent source and may be biased.

C)there is a risk that the auditor will misinterpret what the client said.

D)the client cannot be trusted to provide persuasive information.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

41

Most auditors prefer to replace external confirmation with analytical procedures whenever possible because the

A)analytical procedures are more reliable.

B)external confirmations are more expensive.

C)analytical procedures are more persuasive.

D)tests of details are more difficult to interpret.

A)analytical procedures are more reliable.

B)external confirmations are more expensive.

C)analytical procedures are more persuasive.

D)tests of details are more difficult to interpret.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

42

An example of vouching would be to trace from

A)receiving reports to the acquisitions journal.

B)the acquisitions journal to supporting vendor invoices.

C)duplicate bank deposit slips to the cash receipts journal.

D)cancelled cheques to the cash disbursement journal.

A)receiving reports to the acquisitions journal.

B)the acquisitions journal to supporting vendor invoices.

C)duplicate bank deposit slips to the cash receipts journal.

D)cancelled cheques to the cash disbursement journal.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

43

To provide reliable evidence,confirmations should be

A)created and sent to the third parties by the client to be returned to the client.

B)created and sent to the third parties by the auditors to be returned to the client.

C)created and sent to the third parties by the client to be returned to the auditor.

D)created and sent to the third parties by the auditors to be returned to the auditor.

A)created and sent to the third parties by the client to be returned to the client.

B)created and sent to the third parties by the auditors to be returned to the client.

C)created and sent to the third parties by the client to be returned to the auditor.

D)created and sent to the third parties by the auditors to be returned to the auditor.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

44

An aspect of analytical procedures is referred to as "attention-directing" when it highlights

A)errors.

B)irregularities.

C)areas of improvement.

D)areas that need more detailed procedures.

A)errors.

B)irregularities.

C)areas of improvement.

D)areas that need more detailed procedures.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

45

When the auditor examines the client's documents and records to support recorded transactions or amounts,it is commonly referred to as

A)inquiry.

B)confirmation.

C)vouching.

D)physical examination.

A)inquiry.

B)confirmation.

C)vouching.

D)physical examination.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

46

An example of a document that the auditor receives from the client,but which was prepared by someone outside the client's organization,is a(n)

A)external confirmation.

B)copy of sales invoice.

C)copy of a bank note payable.

D)inventory receiving report.

A)external confirmation.

B)copy of sales invoice.

C)copy of a bank note payable.

D)inventory receiving report.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

47

Which of the following forms of evidence would be least persuasive in forming the auditor's opinion?

A)the auditor's count of marketable securities

B)correspondence with a stockbroker regarding the quantity of the client's investments held in street name by the broker

C)minutes of the board of directors meeting authorizing the purchase of stock as an investment

D)responses to auditor's questions by the president and controller regarding the investments account

A)the auditor's count of marketable securities

B)correspondence with a stockbroker regarding the quantity of the client's investments held in street name by the broker

C)minutes of the board of directors meeting authorizing the purchase of stock as an investment

D)responses to auditor's questions by the president and controller regarding the investments account

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

48

Identify and define the seven methods of audit evidence collection.Which two types of evidence are the most expensive? Which three types of evidence are the least expensive? Which type of evidence would be most persuasive when testing the existence objective for long-term assets?

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

49

An abnormal fluctuation in gross profit that might suggest the need for extended audit procedures for sales and inventories would most likely be identified in the planning phase of the audit by the use of

A)tests of details of balances.

B)procedures to obtain an understanding of internal controls.

C)specialized audit programs.

D)analytical procedures.

A)tests of details of balances.

B)procedures to obtain an understanding of internal controls.

C)specialized audit programs.

D)analytical procedures.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

50

Inquiry is a valuable technique during the planning phase of the audit because it

A)involves the rechecking of controls to ensure that they are conducted accurately.

B)is a type of audit evidence that provides a very high level of assurance.

C)is conclusive evidence from an independent source.

D)helps obtain information about how procedures and internal controls operate.

A)involves the rechecking of controls to ensure that they are conducted accurately.

B)is a type of audit evidence that provides a very high level of assurance.

C)is conclusive evidence from an independent source.

D)helps obtain information about how procedures and internal controls operate.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

51

An example of an external document is

A)a cancelled cheque.

B)employees' time reports.

C)inventory receiving reports.

D)the minutes of the board of directors' meetings.

A)a cancelled cheque.

B)employees' time reports.

C)inventory receiving reports.

D)the minutes of the board of directors' meetings.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

52

"Use of comparisons and relationships to determine whether account balances or other data appear reasonable" is a definition of

A)auditing.

B)tests of balances.

C)tests of controls.

D)analytical procedures.

A)auditing.

B)tests of balances.

C)tests of controls.

D)analytical procedures.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

53

Below are 12 audit procedures.Classify each procedure according to the following types of audit evidence: 1)inspection,2)external confirmation,3)recalculation,4)observation,5)inquiry of the client,6)reperformance,and 7)analytical procedure.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

54

The following are audit procedures in the sales and collection cycle.

1.Inspect a sample of shipping documents to determine if each has a sales invoice number included on it.

2.Discuss with the sales manager whether any sales allowances have been granted after the balance sheet date that may apply to the current period.

3.Add the columns on the aged trial balance and compare the total with the general ledger.

4.Observe whether the controller makes an independent comparison of the total in the general ledger with the trial balance of accounts receivable.

5.For the month of May,count the approximate number of shipping documents filed in the shipping department and compare the total with the number of sales invoices in the sales journal.

6.Compare the date on a sample of shipping documents throughout the year with related duplicate sales invoices and the accounts receivable master file.

7.Examine a sample of customer orders and see if each has a credit authorization.

8.Send letters directly to former customers whose accounts have been written off as uncollectible to determine if any have actually been paid.

9.Examine the master file of accounts receivable to see if each has an indication of "C" for a regular customer,"N" for interest-bearing receivables,and "R" for related parties.

10.Compare the date on a sample of shipping documents a few days before and after the balance sheet date with related sales journal transactions.

Required:

For each procedure,identify the type of evidence being used.For each procedure,identify either the transaction-related audit objective(s)being met or the balance-related audit objective(s)being met.

1.Inspect a sample of shipping documents to determine if each has a sales invoice number included on it.

2.Discuss with the sales manager whether any sales allowances have been granted after the balance sheet date that may apply to the current period.

3.Add the columns on the aged trial balance and compare the total with the general ledger.

4.Observe whether the controller makes an independent comparison of the total in the general ledger with the trial balance of accounts receivable.

5.For the month of May,count the approximate number of shipping documents filed in the shipping department and compare the total with the number of sales invoices in the sales journal.

6.Compare the date on a sample of shipping documents throughout the year with related duplicate sales invoices and the accounts receivable master file.

7.Examine a sample of customer orders and see if each has a credit authorization.

8.Send letters directly to former customers whose accounts have been written off as uncollectible to determine if any have actually been paid.

9.Examine the master file of accounts receivable to see if each has an indication of "C" for a regular customer,"N" for interest-bearing receivables,and "R" for related parties.

10.Compare the date on a sample of shipping documents a few days before and after the balance sheet date with related sales journal transactions.

Required:

For each procedure,identify the type of evidence being used.For each procedure,identify either the transaction-related audit objective(s)being met or the balance-related audit objective(s)being met.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

55

The audit evidence gathering technique of recalculation refers to

A)sending bank confirmation to validate bank balances.

B)rechecking prices as per price list.

C)counting inventory.

D)checking the calculation of amortization expense.

A)sending bank confirmation to validate bank balances.

B)rechecking prices as per price list.

C)counting inventory.

D)checking the calculation of amortization expense.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

56

A)Distinguish between internal documentation and external documentation as types of audit evidence.Give two examples of each.Which type is considered more reliable? B)Below are 10 documents typically examined by auditors.Classify each document as either internal or external.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

57

An example of an internal document is

A)a cancelled cheque.

B)a bank statement.

C)a bill of lading for purchases.

D)employees' time reports.

A)a cancelled cheque.

B)a bank statement.

C)a bill of lading for purchases.

D)employees' time reports.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

58

When comparing the reliability of external versus internal documents,the external documents are generally considered

A)more reliable.

B)less reliable.

C)equally reliable.

D)unreliable.

A)more reliable.

B)less reliable.

C)equally reliable.

D)unreliable.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

59

Following are examples of evidence that could be collected during an audit of financial statements.

1.Duplicate copies of sales invoices

2.Inspection of new $100 000 cutting machine

3.Bank confirmation

4.Remittance advices

5.Vendors' invoices

6.Standard letter from lawyer to auditor

7.Auditor inventory count sheets

8.Shipping documents

9.Payroll cheques

10.Long-term debt agreements review notes

11.Auditor interest expense calculation worksheet

12.Observation by auditor of computer error message (invalid supplier number)

13.Gross margin calculation

14.Interview notes from interview with credit manager

Required:

Classify each type of evidence as to its reliability (1 - high,2 - moderate,3 - low).Justify your classification.

1.Duplicate copies of sales invoices

2.Inspection of new $100 000 cutting machine

3.Bank confirmation

4.Remittance advices

5.Vendors' invoices

6.Standard letter from lawyer to auditor

7.Auditor inventory count sheets

8.Shipping documents

9.Payroll cheques

10.Long-term debt agreements review notes

11.Auditor interest expense calculation worksheet

12.Observation by auditor of computer error message (invalid supplier number)

13.Gross margin calculation

14.Interview notes from interview with credit manager

Required:

Classify each type of evidence as to its reliability (1 - high,2 - moderate,3 - low).Justify your classification.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

60

An auditor is conducting the audit of the financial statements of a retail department store.The auditor is aware that he must obtain sufficient appropriate evidence with respect to various audit assertions associated with management assertions and thus with material financial statement amounts.

The following is a list of specific audit procedures the auditor plans to perform:

1.Send negative external confirmation requests to a large sample of the store's customers who have balances due on account at year end.

2.Perform test counts of goods on hand during the company's normal physical inventory taking,one month prior to the year end.

3.Examine receiving reports dated prior to the year end that have not been matched to vendor invoices.

4.Review paid invoices and supporting documents for amounts classified as repair and maintenance expense for large or unusual items.

5.Examine audited financial statements of several foreign companies in which the client owns shares,and which are being held as temporary investments.

Required:

For each of the five audit procedures listed,describe only the PRIMARY management assertion being tested,the PRIMARY audit assertion being tested,and the quality of evidence (high,medium,low)obtained,explaining WHY the evidence is the quality level you specify.

The following is a list of specific audit procedures the auditor plans to perform:

1.Send negative external confirmation requests to a large sample of the store's customers who have balances due on account at year end.

2.Perform test counts of goods on hand during the company's normal physical inventory taking,one month prior to the year end.

3.Examine receiving reports dated prior to the year end that have not been matched to vendor invoices.

4.Review paid invoices and supporting documents for amounts classified as repair and maintenance expense for large or unusual items.

5.Examine audited financial statements of several foreign companies in which the client owns shares,and which are being held as temporary investments.

Required:

For each of the five audit procedures listed,describe only the PRIMARY management assertion being tested,the PRIMARY audit assertion being tested,and the quality of evidence (high,medium,low)obtained,explaining WHY the evidence is the quality level you specify.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

61

When a higher than normal ratio of long-term debt to net worth is coupled with a lower than average ratio of profits to total assets,the company

A)is highly successful.

B)is comparable with industry standards.

C)has a high risk of financial failure.

D)has a liquidity problem.

A)is highly successful.

B)is comparable with industry standards.

C)has a high risk of financial failure.

D)has a liquidity problem.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

62

An important benefit of industry comparisons is as

A)an aid to understanding the client's performance.

B)an indicator of errors.

C)an indicator of irregularities.

D)a least-cost indicator for audit procedures.

A)an aid to understanding the client's performance.

B)an indicator of errors.

C)an indicator of irregularities.

D)a least-cost indicator for audit procedures.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

63

The audit working papers serve as a record of the evidence accumulated and the results of the audit tests.This helps to demonstrate that the audit was

A)kept properly confidential;information was held secure.

B)completed using Canadian generally accepted accounting principles.

C)organized effectively with no mistakes in calculations.

D)conducted in accordance with Canadian generally accepted auditing standards.

A)kept properly confidential;information was held secure.

B)completed using Canadian generally accepted accounting principles.

C)organized effectively with no mistakes in calculations.

D)conducted in accordance with Canadian generally accepted auditing standards.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

64

Renaldo compared shipping reports to sales documents,checking to see that the sales invoice dates matched the shipping dates,and that quantities invoiced matched quantities shipped.On his working paper,he said that he vouched invoices.What else should his working paper include with respect to the audit procedure conducted?

A)details of tests conducted,with results

B)results of analytical review procedures on the aging of accounts receivable

C)employee numbers and wage rates of the employees he spoke to

D)a statement that the information will be held confidential

A)details of tests conducted,with results

B)results of analytical review procedures on the aging of accounts receivable

C)employee numbers and wage rates of the employees he spoke to

D)a statement that the information will be held confidential

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

65

Which of the following would you expect to find in a corporation's bylaws?

A)The kinds and amounts of capital stock authorized.

B)The date of incorporation.

C)The rules and procedures adopted by the shareholders of the corporation.

D)The types of business activities that the corporation is authorized to conduct.

A)The kinds and amounts of capital stock authorized.

B)The date of incorporation.

C)The rules and procedures adopted by the shareholders of the corporation.

D)The types of business activities that the corporation is authorized to conduct.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

66

Each working paper should include enough information to fulfill the objectives for which it was designed.For example,if a working paper is designed to list the detail and show the verification of support of a balance sheet account such as prepaid insurance,it is essential that the detail on the working paper

A)reconcile the change in costs from last year to this year.

B)use analytical review to consider the reasonableness of the account.

C)reconcile with the associated general ledger account.

D)use observation to identify controls in place over the transactions.

A)reconcile the change in costs from last year to this year.

B)use analytical review to consider the reasonableness of the account.

C)reconcile with the associated general ledger account.

D)use observation to identify controls in place over the transactions.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

67

List and describe the process of developing substantive analytical procedures as per CAS 520.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

68

For some audit objectives and in some circumstances,analytical procedures may be the most effective procedure to apply.The objectives that most likely would benefit from the use of analytical review with respect to the allowance for uncollectible accounts would be

A)validity of sales transactions recorded for individual customer accounts.

B)classification and completeness of transactions,accuracy of judgments and estimates.

C)collectability of individual customer account balances.

D)allocation of transactions to the proper accounting period.

A)validity of sales transactions recorded for individual customer accounts.

B)classification and completeness of transactions,accuracy of judgments and estimates.

C)collectability of individual customer account balances.

D)allocation of transactions to the proper accounting period.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

69

During final review of working papers and financial statements,possible oversights in the audit can be identified by

A)the partner's knowledge of the client's business combined with effective analytical procedures.

B)conducting a closing interview with management of the client.

C)conducting a meeting with the audit team.

D)reviewing the minutes from the board meetings.

A)the partner's knowledge of the client's business combined with effective analytical procedures.

B)conducting a closing interview with management of the client.

C)conducting a meeting with the audit team.

D)reviewing the minutes from the board meetings.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

70

A)There are four important purposes of analytical procedures.Identify each of these four purposes and for each purpose give a specific example of an analytical procedure that an auditor might perform.B)Identify each of the five major types of analytical procedures and give an example of each.C)One purpose of performing analytical procedures in the planning phase of an audit is to assess the client's financial condition.Explain how the assessment of a client's financial condition can affect the auditor's decisions concerning evidence accumulation in later phases of the audit.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

71

The working papers contain data useful for evaluating the adequacy of the audit scope and the fairness of the financial statements.These data help the auditor to conclude whether

A)control risks were accurately identified and tested.

B)inherent risks were set as low as possible.

C)an unmodified audit report can be issued.

D)the current files properly contain copies of client contracts and agreements.

A)control risks were accurately identified and tested.

B)inherent risks were set as low as possible.

C)an unmodified audit report can be issued.

D)the current files properly contain copies of client contracts and agreements.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

72

When the current year's unaudited trial balance amounts are compared to the prior year's audited trial balance amounts,

A)errors are identified.

B)discrepancies are discovered.

C)irregularities become apparent.

D)significant changes in balances are highlighted.

A)errors are identified.

B)discrepancies are discovered.

C)irregularities become apparent.

D)significant changes in balances are highlighted.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

73

When an auditor calculates the gross margin as a percent of sales and compares it with previous periods,this type of evidence is called

A)physical examination.

B)analytical procedures.

C)observation.

D)enquiries of client.

A)physical examination.

B)analytical procedures.

C)observation.

D)enquiries of client.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

74

The new Canadian Auditing Standards require the auditor to complete the audit working papers within how many days of the audit report date?

A)45

B)60

C)90

D)183

A)45

B)60

C)90

D)183

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

75

A common comparison occurs when the auditor calculates the expected balance and compares it with the actual balance.The auditor's expected account balance may be determined by

A)using industry standards.

B)using credit bureau reports.

C)relating it to some other balance sheet or income statement account or accounts.

D)inquiring with the client.

A)using industry standards.

B)using credit bureau reports.

C)relating it to some other balance sheet or income statement account or accounts.

D)inquiring with the client.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

76

If most companies in the industry use FIFO inventory valuation and straight-line depreciation,and the audit client uses weighted-average cost inventory valuation and double-declining balance,comparisons of client and industry data

A)will be a meaningful highlight of the result of these differences in accounting methods.

B)will enable the auditor to spot errors but not irregularities.

C)will enable the auditor to spot irregularities but not errors.

D)may not be meaningful,affecting the comparability of data.

A)will be a meaningful highlight of the result of these differences in accounting methods.

B)will enable the auditor to spot errors but not irregularities.

C)will enable the auditor to spot irregularities but not errors.

D)may not be meaningful,affecting the comparability of data.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

77

List and explain the three times during an audit engagement the auditor performs analytical procedures.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

78

The working papers are

A)the property of the client.

B)prepared by the client's internal auditors.

C)the primary means of documenting that an adequate audit was conducted in accordance with GAAS.

D)used primarily as a basis for the partners to review and reward the work of the managers,seniors,and staff.

A)the property of the client.

B)prepared by the client's internal auditors.

C)the primary means of documenting that an adequate audit was conducted in accordance with GAAS.

D)used primarily as a basis for the partners to review and reward the work of the managers,seniors,and staff.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

79

At the first day of work at a PA firm,staff are given their own laptop computer for use in working with clients and other data.

Required:A)What is the typical structure of client working paper files? B)How is client data protected from unauthorized change?

Required:A)What is the typical structure of client working paper files? B)How is client data protected from unauthorized change?

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

80

The auditor will obtain a copy of the client's articles of incorporation (if applicable)and retain a copy in the permanent file.Important information in the articles of incorporation includes

A)the interest rates currently being paid for bonds that have been issued.

B)voting rights of each class of shares issued by the company.

C)which shares have been redeemed by the company in the current year.

D)the interest rates that are being received on long-term notes invested.

A)the interest rates currently being paid for bonds that have been issued.

B)voting rights of each class of shares issued by the company.

C)which shares have been redeemed by the company in the current year.

D)the interest rates that are being received on long-term notes invested.

Unlock Deck

Unlock for access to all 91 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 91 flashcards in this deck.