Deck 9: Accounting Quality

Full screen (f)

Question

Question

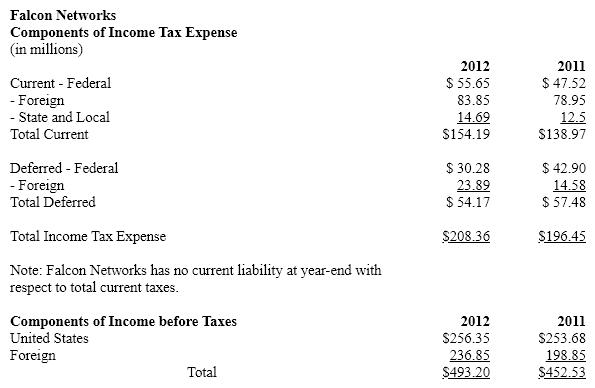

Falcon Networks

Falcon Networks is a leading semiconductor company with operations in 17 different countries. Information about the company's taxes appears below:

Based on the information provided by Falcon Networks how much cash did income taxes use during 2012?

A) $154.19 million

B) $54.17 million

C) $208.36 million

D) $284.84 million

Falcon Networks is a leading semiconductor company with operations in 17 different countries. Information about the company's taxes appears below:

Based on the information provided by Falcon Networks how much cash did income taxes use during 2012?

A) $154.19 million

B) $54.17 million

C) $208.36 million

D) $284.84 million

Question

Gorilla, Corp. implemented a defined-benefit pension plan for its employees on January 2, 2012. The following data are provided for year 2012, as of December 31:

What amount should Gorilla record as additional minimum pension liability at December 31, 2012?

What amount should Gorilla record as additional minimum pension liability at December 31, 2012?

A) $0

B) $5,000

C) $20,000

D) $45,000

What amount should Gorilla record as additional minimum pension liability at December 31, 2012?A) $0

B) $5,000

C) $20,000

D) $45,000

Question

Question

Question

Presented below is pension information related to Roberts Corp. for the year 2012:

The amount of pension expense to be reported for 2012 is:

The amount of pension expense to be reported for 2012 is:

A) $46,000

B) $48,000

C) $54,000

D) $40,000

The amount of pension expense to be reported for 2012 is:A) $46,000

B) $48,000

C) $54,000

D) $40,000

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

At the end of 2012 Playtime provided the following information about the project:

What percentage is the playground complete?

What percentage is the playground complete?

A) 62.5%

B) 66.7%

C) 55.6%

D) 50.0%

What percentage is the playground complete?A) 62.5%

B) 66.7%

C) 55.6%

D) 50.0%

Question

Question

Upton Company has consistently used the percentage-of-completion method of recognizing income. In 2010, Upton started on an $18,000,000 construction contract that was completed in 2012. The following information was taken from Upton's 2010 accounting records:

What amount of revenue should Upton recognize on the contract in 2010?

A) $6,000,000

B) $5,400,000

C) $9,000,000

D) $0

What amount of revenue should Upton recognize on the contract in 2010?

A) $6,000,000

B) $5,400,000

C) $9,000,000

D) $0

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Playtime Corporation

Assume that Playtime Corp. has agreed to construct a new playground for Surrey County for $2,450,000. Construction of the new playground will begin on March 17, 2012 and is expected to be completed in August 2013. At the signing of the contract Playtime Corp. estimates that it will cost $1,750,000 to build the playground.

At the end of 2012 Playtime provided the following information about the project:

If Playtime uses the percentage of completion to recognize revenue on the long-term contract, how much gross margin should Playtime recognize in 2012?

If Playtime uses the percentage of completion to recognize revenue on the long-term contract, how much gross margin should Playtime recognize in 2012?

A) $389,200

B) $278,000

C) $556,000

D) $433,550

Assume that Playtime Corp. has agreed to construct a new playground for Surrey County for $2,450,000. Construction of the new playground will begin on March 17, 2012 and is expected to be completed in August 2013. At the signing of the contract Playtime Corp. estimates that it will cost $1,750,000 to build the playground.

At the end of 2012 Playtime provided the following information about the project:

If Playtime uses the percentage of completion to recognize revenue on the long-term contract, how much gross margin should Playtime recognize in 2012?A) $389,200

B) $278,000

C) $556,000

D) $433,550

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

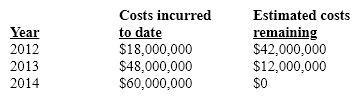

Assume that Madison Corp. has agreed to construct a new basketball arena for Gator Town for $70 million dollars. Construction of the new arena begins in July, 2012 and is expected to be completed in March 2009. At the signing of the contract Madison Corp. estimates that the new arena will cost $60 million dollars to build. Given the following cost and building schedule determine the cumulative degree of completion and how much revenue and gross margin Madison Corp. should recognize in years 2012, 2013 and 2014.

Question

Question

Question

Question

Question

Question

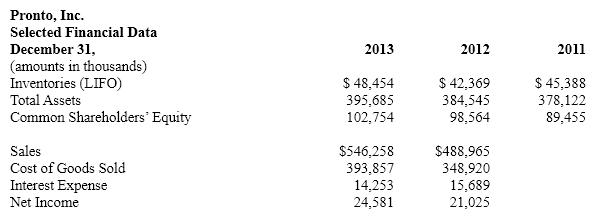

Pronto, Inc. is a major producer of printing equipment. Pronto uses a LIFO cost-flow assumption for inventories. The company's tax rate is 35%. Below is selected financial data for the company.

a. The excess of FIFO over LIFO inventories was $25 million on December 31, 2013, $28.5 million on December 31, 2012 and $22 million on December 31, 2011. Compute the cost of goods sold for Pronto, Inc. for years 2013 and 2012 assuming that it had used a FIFO assumption.

b. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a LIFO cost-flow assumption.

c. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a FIFO cost-flow assumption.

d. Compute the rate of return on assets for years 2013 and 2012 based on the reported amounts. Disaggregate ROA into profit margin and asset turnover components.

e. Compute the rate of return on assets for years 2013 and 2012 assuming that Pronto, Inc. had used the FIFO method of accounting for inventories. Disaggregate ROA into profit margin and asset turnover components.

a. The excess of FIFO over LIFO inventories was $25 million on December 31, 2013, $28.5 million on December 31, 2012 and $22 million on December 31, 2011. Compute the cost of goods sold for Pronto, Inc. for years 2013 and 2012 assuming that it had used a FIFO assumption.

b. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a LIFO cost-flow assumption.

c. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a FIFO cost-flow assumption.

d. Compute the rate of return on assets for years 2013 and 2012 based on the reported amounts. Disaggregate ROA into profit margin and asset turnover components.

e. Compute the rate of return on assets for years 2013 and 2012 assuming that Pronto, Inc. had used the FIFO method of accounting for inventories. Disaggregate ROA into profit margin and asset turnover components.

Question

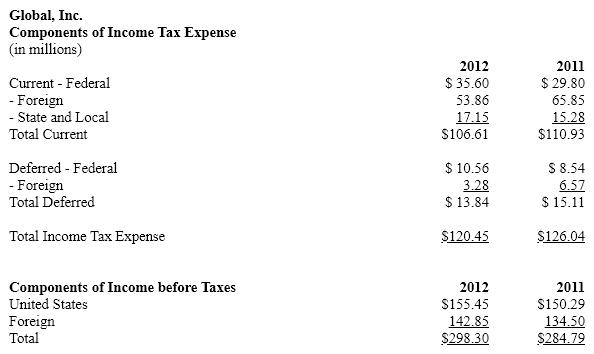

Global, Inc. provides consulting services throughout the world. The company pays taxes to the nation where revenues are earned. Information about the company's taxes is presented below:

a. Using the information provided for Global, prepare the company's journal entry to record income taxes for 2012 and 2011.

b. Using the information provided for Global, determine the company's effective tax rate for 2012 and 2011.

a. Using the information provided for Global, prepare the company's journal entry to record income taxes for 2012 and 2011.

b. Using the information provided for Global, determine the company's effective tax rate for 2012 and 2011.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/68

Play

Full screen (f)

Deck 9: Accounting Quality

1

To calculate a company's average tax rate an analyst would:

A) Divide income tax payable by income before taxes

B) Divide income tax expense by income before taxes

C) Multiply the statutory income tax rate by income before tax

D) Average a firm's Federal, State, Local and Foreign tax rates.

A) Divide income tax payable by income before taxes

B) Divide income tax expense by income before taxes

C) Multiply the statutory income tax rate by income before tax

D) Average a firm's Federal, State, Local and Foreign tax rates.

B

2

Falcon Networks

Falcon Networks is a leading semiconductor company with operations in 17 different countries. Information about the company's taxes appears below:

Based on the information provided by Falcon Networks how much cash did income taxes use during 2012?

A) $154.19 million

B) $54.17 million

C) $208.36 million

D) $284.84 million

Falcon Networks is a leading semiconductor company with operations in 17 different countries. Information about the company's taxes appears below:

Based on the information provided by Falcon Networks how much cash did income taxes use during 2012?

A) $154.19 million

B) $54.17 million

C) $208.36 million

D) $284.84 million

A

3

Gorilla, Corp. implemented a defined-benefit pension plan for its employees on January 2, 2012. The following data are provided for year 2012, as of December 31:

What amount should Gorilla record as additional minimum pension liability at December 31, 2012?

A) $0

B) $5,000

C) $20,000

D) $45,000

What amount should Gorilla record as additional minimum pension liability at December 31, 2012?A) $0

B) $5,000

C) $20,000

D) $45,000

B

4

Which of the following calculations is used to determine the amount of the liability reported on the balance sheet for underfunding?

A) Plan assets less projected benefit obligation.

B) Projected benefit obligation less plan assets.

C) Plan assets less accumulated benefit obligation.

D) Accumulated benefit obligation less plan assets.

A) Plan assets less projected benefit obligation.

B) Projected benefit obligation less plan assets.

C) Plan assets less accumulated benefit obligation.

D) Accumulated benefit obligation less plan assets.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

5

All of the following conditions signal that revenue recognition may have been recorded too early except :

A) large and volatile amounts of uncollectible accounts receivable.

B) a decrease in the number of days accounts receivable are outstanding.

C) unusually large amounts of returned goods.

D) excessive warranty expenditures.

A) large and volatile amounts of uncollectible accounts receivable.

B) a decrease in the number of days accounts receivable are outstanding.

C) unusually large amounts of returned goods.

D) excessive warranty expenditures.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

6

Presented below is pension information related to Roberts Corp. for the year 2012:

The amount of pension expense to be reported for 2012 is:

A) $46,000

B) $48,000

C) $54,000

D) $40,000

The amount of pension expense to be reported for 2012 is:A) $46,000

B) $48,000

C) $54,000

D) $40,000

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

7

Which of the following will most likely help identify an increasing proportion of uncollectible sales?

A) accounts receivable turnover

B) the ratio of bad debt expense to sales

C) the ratio of sales returns to sales

D) the ratio of cost of sales to sales

A) accounts receivable turnover

B) the ratio of bad debt expense to sales

C) the ratio of sales returns to sales

D) the ratio of cost of sales to sales

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

8

All of the following are considered by analysts when assessing the quality of accounting except :

A) Price variation and the speed at which inventory turns over

B) Any liquidation of FIFO inventory layers

C) Any physical deterioration or obsolescence of inventory

D) The inventory cost-flow assumption chosen by management

A) Price variation and the speed at which inventory turns over

B) Any liquidation of FIFO inventory layers

C) Any physical deterioration or obsolescence of inventory

D) The inventory cost-flow assumption chosen by management

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

9

The accumulated benefit obligation measures:

A) the pension obligation on the basis of the plan formula applied to years of service to date and based on existing salary levels.

B) an estimated total benefit at retirement and then computes the level cost that will be sufficient, together with interest expected to accumulate at the assumed rate, to provide the total benefits at retirement.

C) the pension obligation on the basis of the plan formula applied to years of service to date and based on future salary levels.

D) the shortest possible period for funding to maximize the tax deduction.

A) the pension obligation on the basis of the plan formula applied to years of service to date and based on existing salary levels.

B) an estimated total benefit at retirement and then computes the level cost that will be sufficient, together with interest expected to accumulate at the assumed rate, to provide the total benefits at retirement.

C) the pension obligation on the basis of the plan formula applied to years of service to date and based on future salary levels.

D) the shortest possible period for funding to maximize the tax deduction.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

10

The major difference between accounting for pensions and the accounting for other postretirement benefits is that firms:

A) do not need to report an excess of the accumulated benefits obligations over assets in a postretirement benefits fund as a liability on the balance sheet.

B) do not need to disclose any estimates used in calculating projected benefits.

C) postretirement benefits are normally not material for most companies and do not need to be disclosed.

D) do not need to set aside funds for future postretirement benefits as they do for pension benefits.

A) do not need to report an excess of the accumulated benefits obligations over assets in a postretirement benefits fund as a liability on the balance sheet.

B) do not need to disclose any estimates used in calculating projected benefits.

C) postretirement benefits are normally not material for most companies and do not need to be disclosed.

D) do not need to set aside funds for future postretirement benefits as they do for pension benefits.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

11

Using the information provided by Falcon Networks , determine the foreign effective tax rate for 2012.

A) 33.52%

B) 35.00%

C) 42.25%

D) 45.49%

A) 33.52%

B) 35.00%

C) 42.25%

D) 45.49%

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements best describes the difference between U.S. GAAP and IFRS with respect to revenue recognition?

A) IFRS has a substantial amount of industry specific guidance for revenue recognition.

B) IFRS revenue recognition is not consistent with U.S. GAAP in principle.

C) There are subtle differences in the wording of U.S. GAAP as compared with IFRS.

D) IFRS has four criteria and U.S. GAAP has five conditions for revenue recognition.

A) IFRS has a substantial amount of industry specific guidance for revenue recognition.

B) IFRS revenue recognition is not consistent with U.S. GAAP in principle.

C) There are subtle differences in the wording of U.S. GAAP as compared with IFRS.

D) IFRS has four criteria and U.S. GAAP has five conditions for revenue recognition.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

13

Using the information provided by Falcon Networks , determine the federal effective tax rate for 2012.

A) 33.52%

B) 35.00%

C) 42.25%

D) 45.49%

A) 33.52%

B) 35.00%

C) 42.25%

D) 45.49%

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

14

The projected benefit obligation measures:

A) the pension obligation on the basis of the plan formula applied to years of service to date and based on existing salary levels.

B) an estimated total benefit at retirement and then computes the level cost that will be sufficient, together with interest expected to accumulate at the assumed rate, to provide the total benefits at retirement.

C) the pension obligation on the basis of the plan formula applied to years of service to date and based on future salary levels.

D) the shortest possible period for funding to maximize the tax deduction.

A) the pension obligation on the basis of the plan formula applied to years of service to date and based on existing salary levels.

B) an estimated total benefit at retirement and then computes the level cost that will be sufficient, together with interest expected to accumulate at the assumed rate, to provide the total benefits at retirement.

C) the pension obligation on the basis of the plan formula applied to years of service to date and based on future salary levels.

D) the shortest possible period for funding to maximize the tax deduction.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

15

Analysts concerns with postretirement benefits include all of the following except:

A) Should the underfunded postretirement benefit obligation be added to liabilities in assessing risk?

B) How reasonable are the firms' assumptions regarding health care cost increases?

C) Is the postretirement benefit fund adequately paying benefits?

D) Is the postretirement benefit fund generating returns consistent with the expected rate of return?

A) Should the underfunded postretirement benefit obligation be added to liabilities in assessing risk?

B) How reasonable are the firms' assumptions regarding health care cost increases?

C) Is the postretirement benefit fund adequately paying benefits?

D) Is the postretirement benefit fund generating returns consistent with the expected rate of return?

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

16

All of the following are true regarding accrual accounting except :

A) Accrual basis measures operating success by the extent to which accomplishments exceed efforts.

B) Accrual basis measures operating success by the extent to which revenues exceed expenses.

C) Accrual basis reports operating activities in terms of their success in generating value.

D) Accrual basis for the recognition of expenses is not required under IFRS.

A) Accrual basis measures operating success by the extent to which accomplishments exceed efforts.

B) Accrual basis measures operating success by the extent to which revenues exceed expenses.

C) Accrual basis reports operating activities in terms of their success in generating value.

D) Accrual basis for the recognition of expenses is not required under IFRS.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following accounts would not be considered a reserve account?

A) Allowance for Doubtful Accounts

B) Estimated Warranty Liability

C) Prepaid Expense

D) Accumulated Depreciation

A) Allowance for Doubtful Accounts

B) Estimated Warranty Liability

C) Prepaid Expense

D) Accumulated Depreciation

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

18

A minimum liability for pension expense is reported when:

A) the projected benefit obligation exceeds the fair value of pension plan assets.

B) the pension expense reported for the period is greater than the funding amount for the same period.

C) the accumulated benefit obligation exceeds the fair value of pension plan assets.

D) vested benefits exceed the fair value of pension plan assets.

A) the projected benefit obligation exceeds the fair value of pension plan assets.

B) the pension expense reported for the period is greater than the funding amount for the same period.

C) the accumulated benefit obligation exceeds the fair value of pension plan assets.

D) vested benefits exceed the fair value of pension plan assets.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

19

All of the following are conditions for revenue recognition outlined by SAB 104 except :

A) There is pervasive evidence that an arrangement exists.

B) Delivery has occurred or services have been performed.

C) The seller's price to the buyer can be variable.

D) Collectability is reasonably assured.

A) There is pervasive evidence that an arrangement exists.

B) Delivery has occurred or services have been performed.

C) The seller's price to the buyer can be variable.

D) Collectability is reasonably assured.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

20

Using the information provided by Falcon Networks determine the combined effective tax rate for 2012.

A) 33.52%

B) 35.00%

C) 42.25%

D) 45.49%

A) 33.52%

B) 35.00%

C) 42.25%

D) 45.49%

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following would not be suggestive of a company recognizing sales too early?

A) large and volatile amounts of uncollectible accounts receivable

B) excessive warranty expenditures

C) large growth in accounts receivable

D) unusually large amount of returned goods

A) large and volatile amounts of uncollectible accounts receivable

B) excessive warranty expenditures

C) large growth in accounts receivable

D) unusually large amount of returned goods

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

22

A typical defined benefit pension plan formula includes all of the following except :

A) the number of years of employee service

B) the fair market value of pension plan assets

C) a credit for each year of annual service

D) the final salary at retirement date

A) the number of years of employee service

B) the fair market value of pension plan assets

C) a credit for each year of annual service

D) the final salary at retirement date

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

23

A LIFO liquidation during periods when prices are increasing results in a company:

A) recording a large inventory write down.

B) recording higher earnings than it would have if it had used FIFO.

C) recording lower earnings than it would have if it had used FIFO.

D) having operational problems, but no financial statement effects.

A) recording a large inventory write down.

B) recording higher earnings than it would have if it had used FIFO.

C) recording lower earnings than it would have if it had used FIFO.

D) having operational problems, but no financial statement effects.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is not part of the balance sheet approach when computing income tax expense?

A) Identifying at each balance sheet date all differences between the book basis of assets, liabilities, and tax loss carryforwards

B) Eliminating permanent differences between book and tax basis.

C) Eliminating deferred tax assets.

D) Assessing the likelihood that the firm will realize the benefits of deferred tax assets in the future.

A) Identifying at each balance sheet date all differences between the book basis of assets, liabilities, and tax loss carryforwards

B) Eliminating permanent differences between book and tax basis.

C) Eliminating deferred tax assets.

D) Assessing the likelihood that the firm will realize the benefits of deferred tax assets in the future.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

25

All of the following examples represent complex revenue generation models except :

A) Point-of-sale transactions

B) Uncertain revenue timing

C) Bundled service deliverables

D) Bundled deliverables in leases

A) Point-of-sale transactions

B) Uncertain revenue timing

C) Bundled service deliverables

D) Bundled deliverables in leases

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

26

When input prices are increasing, companies that use the LIFO method of accounting for inventory will report:

A) Lower cost of goods sold amounts in comparison to the FIFO method

B) Higher sales amounts in comparison to the FIFO method

C) Higher ending inventory amounts in comparison to the FIFO method

D) Lower gross profit margins in comparison to the FIFO method

A) Lower cost of goods sold amounts in comparison to the FIFO method

B) Higher sales amounts in comparison to the FIFO method

C) Higher ending inventory amounts in comparison to the FIFO method

D) Lower gross profit margins in comparison to the FIFO method

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

27

At the end of 2012 Playtime provided the following information about the project:

What percentage is the playground complete?

A) 62.5%

B) 66.7%

C) 55.6%

D) 50.0%

What percentage is the playground complete?A) 62.5%

B) 66.7%

C) 55.6%

D) 50.0%

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

28

Regarding actuarial assumptions, firms must disclose in notes to the financial statements all of the following except :

A) the discount rate used to compute the pension benefit obligation.

B) the expected rate of return on pension investments.

C) estimates of the number of retirees over the future 10 years.

D) the rate of compensation increase.

A) the discount rate used to compute the pension benefit obligation.

B) the expected rate of return on pension investments.

C) estimates of the number of retirees over the future 10 years.

D) the rate of compensation increase.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

29

Upton Company has consistently used the percentage-of-completion method of recognizing income. In 2010, Upton started on an $18,000,000 construction contract that was completed in 2012. The following information was taken from Upton's 2010 accounting records:

What amount of revenue should Upton recognize on the contract in 2010?

A) $6,000,000

B) $5,400,000

C) $9,000,000

D) $0

What amount of revenue should Upton recognize on the contract in 2010?

A) $6,000,000

B) $5,400,000

C) $9,000,000

D) $0

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

30

All of the following are events that can change the projected benefit obligation (PBO) during a period except :

A) The payment of retirement benefits.

B) Amendments to the pension plan agreement

C) The interest accumulated on the liability.

D) All of these can change the PBO.

A) The payment of retirement benefits.

B) Amendments to the pension plan agreement

C) The interest accumulated on the liability.

D) All of these can change the PBO.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is not a disclosure for derivatives required under SFAS No. 133?

A) Firms must describe their risk management strategy and how particular derivatives help accomplish their hedging objectives.

B) For fair value and cash flow hedges, firms must disclose the net gain or loss recognized in earnings resulting from the hedges' ineffectiveness and the line item on the income statement that includes this net gain or loss.

C) For cash flow hedges, firms must describe the transactions or events that will result in reclassifying gains and losses from other comprehensive income to net income and the estimated amount of such reclassifications during the next 12 months.

D) The specifics of a model that simulates with a 95 percent or other confidence level the minimum, maximum, or average amount of loss that a firm would incur.

A) Firms must describe their risk management strategy and how particular derivatives help accomplish their hedging objectives.

B) For fair value and cash flow hedges, firms must disclose the net gain or loss recognized in earnings resulting from the hedges' ineffectiveness and the line item on the income statement that includes this net gain or loss.

C) For cash flow hedges, firms must describe the transactions or events that will result in reclassifying gains and losses from other comprehensive income to net income and the estimated amount of such reclassifications during the next 12 months.

D) The specifics of a model that simulates with a 95 percent or other confidence level the minimum, maximum, or average amount of loss that a firm would incur.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

32

If the portions of the firm's foreign operations in higher-tax-rate countries grew more rapidly than foreign operations in lower-tax-rate countries, the company may seek out more tax effective ways of operating abroad through all of the following means except :

A) Assess whether transfer prices or cost allocations can be adjusted to shift income from high-tax-rate to low-tax-rate jurisdictions.

B) Shift from domestic to foreign borrowing to increase deductions for interest against foreign-source income.

C) Shift from debt to equity financing of foreign operations to increase interest deductions against foreign-source income.

D) Shift some operations, like marketing, to the United States where the average tax rate is lower.

A) Assess whether transfer prices or cost allocations can be adjusted to shift income from high-tax-rate to low-tax-rate jurisdictions.

B) Shift from domestic to foreign borrowing to increase deductions for interest against foreign-source income.

C) Shift from debt to equity financing of foreign operations to increase interest deductions against foreign-source income.

D) Shift some operations, like marketing, to the United States where the average tax rate is lower.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

33

Dividing a company's income tax expense by its book income before income taxes provides the company's ___________________________________.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

34

All of the following are most likely to change the FMV of pension plan assets during a given period except :

A) Employer cash payments are made to the plan trustee.

B) Changes in Internal Revenue Service regulations for future tax deductible amounts of contributions.

C) Actual returns on invested plan assets.

D) Retirement benefits paid.

A) Employer cash payments are made to the plan trustee.

B) Changes in Internal Revenue Service regulations for future tax deductible amounts of contributions.

C) Actual returns on invested plan assets.

D) Retirement benefits paid.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

35

Typical U.S. GAAP disclosures for deferred income taxes include all of the following except :

A) Components of income tax expense

B) Components of income before taxes

C) Reconciliation of income taxes at statutory rate with income tax expense

D) Components of permanent tax differences

A) Components of income tax expense

B) Components of income before taxes

C) Reconciliation of income taxes at statutory rate with income tax expense

D) Components of permanent tax differences

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

36

An inventory pricing procedure in which the current costs have a direct impact on the inventory is:

A) FIFO

B) LIFO

C) Base stock

D) Weighted-average

A) FIFO

B) LIFO

C) Base stock

D) Weighted-average

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

37

Under the completed contract method:

A) revenue and cost are recognized during the production cycle, but gross profit recognition is deferred until the contract is completed.

B) revenue, cost, and gross profit are recognized during the production cycle.

C) revenue, cost, and gross profit are recognized at the time the contract is completed.

D) None of these are correct.

A) revenue and cost are recognized during the production cycle, but gross profit recognition is deferred until the contract is completed.

B) revenue, cost, and gross profit are recognized during the production cycle.

C) revenue, cost, and gross profit are recognized at the time the contract is completed.

D) None of these are correct.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

38

The _____________________________________________ is equal to the actuarial present value of amounts that the employer expects to pay to retired employees, based on the employees' service to date and using expected future salary amounts.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

39

Deferred tax assets result in future tax ____________________ when temporary differences reverse.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

40

Playtime Corporation

Assume that Playtime Corp. has agreed to construct a new playground for Surrey County for $2,450,000. Construction of the new playground will begin on March 17, 2012 and is expected to be completed in August 2013. At the signing of the contract Playtime Corp. estimates that it will cost $1,750,000 to build the playground.

At the end of 2012 Playtime provided the following information about the project:

If Playtime uses the percentage of completion to recognize revenue on the long-term contract, how much gross margin should Playtime recognize in 2012?

A) $389,200

B) $278,000

C) $556,000

D) $433,550

Assume that Playtime Corp. has agreed to construct a new playground for Surrey County for $2,450,000. Construction of the new playground will begin on March 17, 2012 and is expected to be completed in August 2013. At the signing of the contract Playtime Corp. estimates that it will cost $1,750,000 to build the playground.

At the end of 2012 Playtime provided the following information about the project:

If Playtime uses the percentage of completion to recognize revenue on the long-term contract, how much gross margin should Playtime recognize in 2012?A) $389,200

B) $278,000

C) $556,000

D) $433,550

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

41

Under the accrual method of accounting, when a firm has substantially completed its value-adding activities it should recognize ____________________.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

42

____________________ differences result from including revenues and expenses in income before taxes in a different period than those items affect taxable income.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

43

The difference between the economic resources received from customers and the economic resources paid to suppliers, employees and other providers of goods and services is called ____________________.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

44

Companies that engage in long-term contracts can recognize income using either the _____________________________________________ method or the ________________________________________ method.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

45

The statement of cash flows allows the accountant to agree the net cash provided to the _________________________ general ledger

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

46

A company that uses FIFO will find that its ___________________________________ account tends to be somewhat out of date.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

47

Recording municipal bond interest received in the general ledger will generate a(n) _________________ difference

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

48

The process of allocating the historical cost of certain assets to the periods of their use in a reasonably systematic manner is referred to as ____________________.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

49

___________________________________ is primarily a question of timing.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

50

Differences between income before taxes and taxable income are either ____________________ or ____________________.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

51

Please answer the following questions about defined benefit pension plans:

1. Companies with defined benefit pension plans must recognize pension expense each period. What are the five components of pension expense? Briefly describe each component.

2. How does each component of pension expense effect pension expense during the period (increase, decrease, or uncertain)?

3. What is the difference between the accumulated pension obligation and the projected pension obligation?

4. What determines whether a pension plan is underfunded or overfunded?

1. Companies with defined benefit pension plans must recognize pension expense each period. What are the five components of pension expense? Briefly describe each component.

2. How does each component of pension expense effect pension expense during the period (increase, decrease, or uncertain)?

3. What is the difference between the accumulated pension obligation and the projected pension obligation?

4. What determines whether a pension plan is underfunded or overfunded?

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

52

U.S. GAAP requires firms to report the assets and liabilities of defined benefit plans _______________________________________________________.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

53

Deferred tax liabilities result in future tax ____________________ when temporary differences reverse.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

54

One sign that a company may be recognizing sales too early is that it has unusually large amounts of ______________________________.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

55

A company that uses LIFO will experience a(n) ______________________________ during a period it sells more units than it purchases.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

56

Although LIFO generally provides higher quality earnings measures, FIFO generally provides higher _____________________________________________ measures.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

57

Income tax expense consists of two components, the ____________________ portion and the ____________________ portion.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

58

Accountants use reserve accounts for various reasons, for each of the scenarios below describe a specific account example that matches the scenario.

1. The use of a reserve account in order to match expense with revenues.

2. The use of a reserve account in order to keep expense out of the income statement.

3. The use of a reserve account in order to revalue an asset, but delay the income recognition effect.

1. The use of a reserve account in order to match expense with revenues.

2. The use of a reserve account in order to keep expense out of the income statement.

3. The use of a reserve account in order to revalue an asset, but delay the income recognition effect.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

59

A contractor would not use ________________________________________ method of income recognition when there is substantial uncertainty regarding the total costs it will incur in completing the project.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

60

A company that uses LIFO will find that its ______________________________ account will be somewhat out of date.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

61

Assume that Madison Corp. has agreed to construct a new basketball arena for Gator Town for $70 million dollars. Construction of the new arena begins in July, 2012 and is expected to be completed in March 2009. At the signing of the contract Madison Corp. estimates that the new arena will cost $60 million dollars to build. Given the following cost and building schedule determine the cumulative degree of completion and how much revenue and gross margin Madison Corp. should recognize in years 2012, 2013 and 2014.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

62

Explain the difference between a temporary and a permanent timing difference for income tax purposes"

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

63

What are the four disclosures required by U.S. GAAP relating to income taxes?

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

64

Under U.S. GAAP, application of the LIFO and FIFO inventory methods result in differences in the balance sheet, income statement and cash flow statement. Compare and contrast the effect of the two methods on each financial statement and determine the advantages and disadvantages of each method.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

65

What are the five steps to apply the core principles of revenue recognition?

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

66

A company may try to paint a favorable picture of itself by accelerating the timing of revenues or estimating the collectible amounts too aggressively. In these cases the quality of accounting information declines because it does not represent the company's true economic condition and may not be sustainable. List four conditions that might suggest that a company is recognizing revenues too early?

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

67

Pronto, Inc. is a major producer of printing equipment. Pronto uses a LIFO cost-flow assumption for inventories. The company's tax rate is 35%. Below is selected financial data for the company.

a. The excess of FIFO over LIFO inventories was $25 million on December 31, 2013, $28.5 million on December 31, 2012 and $22 million on December 31, 2011. Compute the cost of goods sold for Pronto, Inc. for years 2013 and 2012 assuming that it had used a FIFO assumption.

b. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a LIFO cost-flow assumption.

c. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a FIFO cost-flow assumption.

d. Compute the rate of return on assets for years 2013 and 2012 based on the reported amounts. Disaggregate ROA into profit margin and asset turnover components.

e. Compute the rate of return on assets for years 2013 and 2012 assuming that Pronto, Inc. had used the FIFO method of accounting for inventories. Disaggregate ROA into profit margin and asset turnover components.

a. The excess of FIFO over LIFO inventories was $25 million on December 31, 2013, $28.5 million on December 31, 2012 and $22 million on December 31, 2011. Compute the cost of goods sold for Pronto, Inc. for years 2013 and 2012 assuming that it had used a FIFO assumption.

b. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a LIFO cost-flow assumption.

c. Compute the inventory turnover ratio for Pronto, Inc. for years 2013 and 2012 using a FIFO cost-flow assumption.

d. Compute the rate of return on assets for years 2013 and 2012 based on the reported amounts. Disaggregate ROA into profit margin and asset turnover components.

e. Compute the rate of return on assets for years 2013 and 2012 assuming that Pronto, Inc. had used the FIFO method of accounting for inventories. Disaggregate ROA into profit margin and asset turnover components.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

68

Global, Inc. provides consulting services throughout the world. The company pays taxes to the nation where revenues are earned. Information about the company's taxes is presented below:

a. Using the information provided for Global, prepare the company's journal entry to record income taxes for 2012 and 2011.

b. Using the information provided for Global, determine the company's effective tax rate for 2012 and 2011.

a. Using the information provided for Global, prepare the company's journal entry to record income taxes for 2012 and 2011.

b. Using the information provided for Global, determine the company's effective tax rate for 2012 and 2011.

Unlock Deck

Unlock for access to all 68 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 68 flashcards in this deck.