Deck 10: Monopolistic Competition and Oligopoly

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

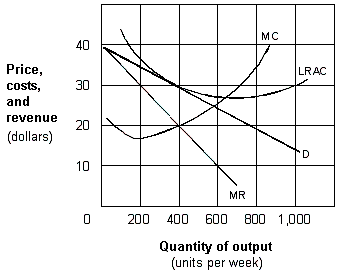

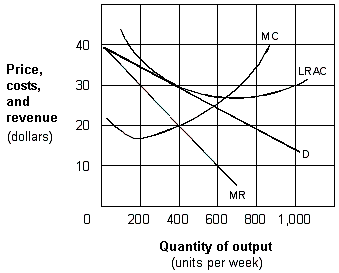

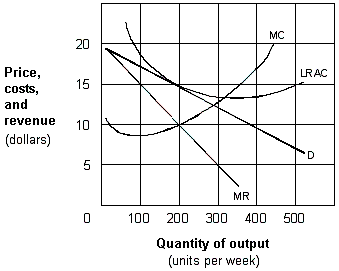

Exhibit 10-3 A monopolistic competitive firm in the long run

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-3 will charge a price per unit of:

A) zero.

B) $10

C) $20.

D) $30.

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-3 will charge a price per unit of:

A) zero.

B) $10

C) $20.

D) $30.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

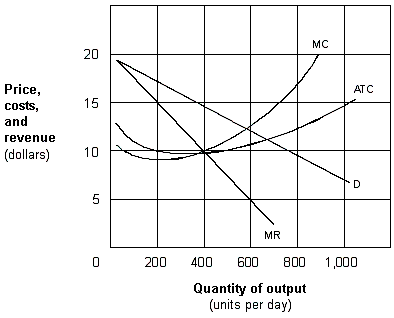

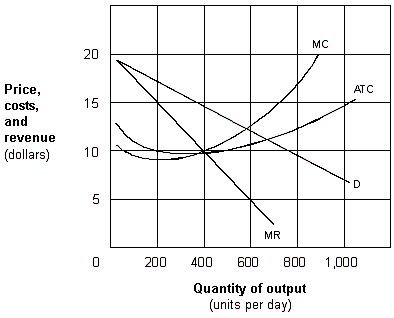

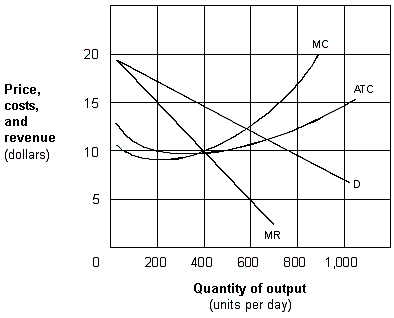

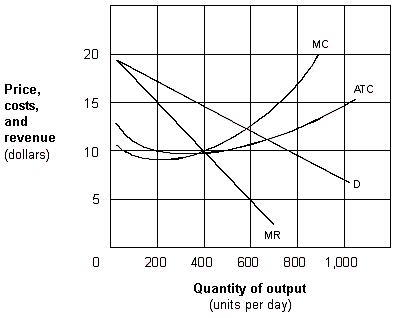

Exhibit 10-1 A monopolistic competitive firm

As presented in Exhibit 10-1, the short-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per day.

B) 200 units per day.

C) 400 units per day.

D) 600 units per day.

As presented in Exhibit 10-1, the short-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per day.

B) 200 units per day.

C) 400 units per day.

D) 600 units per day.

Question

Exhibit 10-1 A monopolistic competitive firm

In the long run, the demand curve for the monopolistic competitive firm shown in Exhibit 10-1:

A) shifts leftward.

B) remains the same.

C) shifts rightward.

D) becomes more inelastic.

In the long run, the demand curve for the monopolistic competitive firm shown in Exhibit 10-1:

A) shifts leftward.

B) remains the same.

C) shifts rightward.

D) becomes more inelastic.

Question

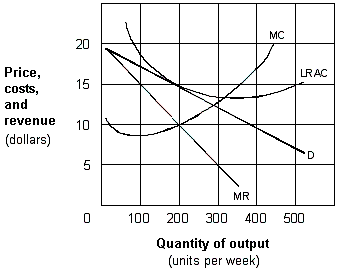

Exhibit 10-3 A monopolistic competitive firm in the long run

As presented in Exhibit 10-3, the long-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per week.

B) 200 units per week.

C) 400 units per week.

D) 600 units per week.

As presented in Exhibit 10-3, the long-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per week.

B) 200 units per week.

C) 400 units per week.

D) 600 units per week.

Question

Question

Exhibit 10-2 A monopolistic competitive firm

As represented in Exhibit 10-2, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per week.

C) $1,000 per week.

D) $20,000 per week.

As represented in Exhibit 10-2, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per week.

C) $1,000 per week.

D) $20,000 per week.

Question

Exhibit 10-1 A monopolistic competitive firm

As represented in Exhibit 10-1, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per day.

C) $1,000 per day.

D) $20,000 per day.

As represented in Exhibit 10-1, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per day.

C) $1,000 per day.

D) $20,000 per day.

Question

Exhibit 10-2 A monopolistic competitive firm

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-2 will charge a price per unit of:

A) zero.

B) $5.

C) $10.

D) $15.

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-2 will charge a price per unit of:

A) zero.

B) $5.

C) $10.

D) $15.

Question

Exhibit 10-2 A monopolistic competitive firm

Comparing the monopolistically competitive firm in Exhibit 10-2 to the long-run profit-maximizing outcome for a perfectly competitive firm with a price of $15 per unit and a quantity of 600,

A) the quantity produced by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

B) the profit earned by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

C) the marginal revenue of the monopolistically competitive firm is lower than that of the perfectly competitive firm at the profit-maximizing quantity.

D) the long run average cost of the monopolistically competitive firm is higher than that of the perfectly competitive firm at the profit-maximizing quantity.

Comparing the monopolistically competitive firm in Exhibit 10-2 to the long-run profit-maximizing outcome for a perfectly competitive firm with a price of $15 per unit and a quantity of 600,

A) the quantity produced by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

B) the profit earned by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

C) the marginal revenue of the monopolistically competitive firm is lower than that of the perfectly competitive firm at the profit-maximizing quantity.

D) the long run average cost of the monopolistically competitive firm is higher than that of the perfectly competitive firm at the profit-maximizing quantity.

Question

Question

Question

Question

Exhibit 10-2 A monopolistic competitive firm

If all firms in a monopolistic competitive industry have demand and cost curves like those shown in Exhibit 10-2, we would expect that in the long run:

A) all firms will leave the industry.

B) some firms will leave the industry.

C) firms in the industry earn zero economic profits.

D) a number of new firms will enter the industry.

If all firms in a monopolistic competitive industry have demand and cost curves like those shown in Exhibit 10-2, we would expect that in the long run:

A) all firms will leave the industry.

B) some firms will leave the industry.

C) firms in the industry earn zero economic profits.

D) a number of new firms will enter the industry.

Question

Question

Question

Question

Exhibit 10-1 A monopolistic competitive firm

If all firms in the industry are the same as the monopolistic competitive firm shown in this Exhibit 10-1, firms in the long run will:

A) leave the industry.

B) earn positive economic profits.

C) experience less competition because firms will exit the industry.

D) experience competition from new firms that enter the industry.

If all firms in the industry are the same as the monopolistic competitive firm shown in this Exhibit 10-1, firms in the long run will:

A) leave the industry.

B) earn positive economic profits.

C) experience less competition because firms will exit the industry.

D) experience competition from new firms that enter the industry.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Exhibit 10-2 A monopolistic competitive firm

Comparing the firms in a monopolistic competitive industry shown in Exhibit 10-2 to a perfectly competitive firm in long-run equilibrium, we find that both firms

A) choose a price equal to the marginal cost at the profit-maximizing quantity.

B) will experience entry of new firms into the industry.

C) earn zero economic profits.

D) minimize cost per unit at their profit-maximizing quantity.

Comparing the firms in a monopolistic competitive industry shown in Exhibit 10-2 to a perfectly competitive firm in long-run equilibrium, we find that both firms

A) choose a price equal to the marginal cost at the profit-maximizing quantity.

B) will experience entry of new firms into the industry.

C) earn zero economic profits.

D) minimize cost per unit at their profit-maximizing quantity.

Question

Question

Question

Question

Question

Question

Question

Question

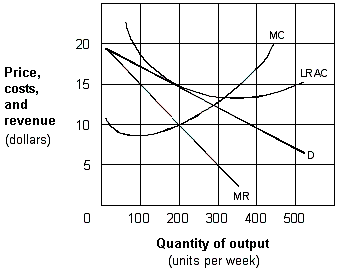

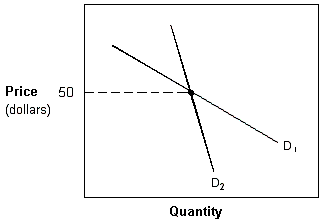

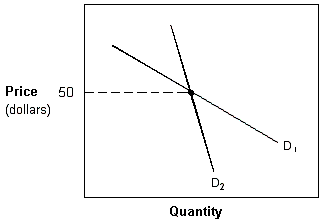

Exhibit 10-4 Kinked demand curves

In Exhibit 10-4, the exhibit represents a kinked-demand oligopoly model. Suppose the current price is $50. If one firm in the oligopoly now attempts to raise price, all firms will:

A) follow along demand curve D1.

B) follow along demand curve D2.

C) ignore this price increase and cause the price-raising firm to move along D1.

D) ignore this price increase and cause the price-raising firm to move along D2.

In Exhibit 10-4, the exhibit represents a kinked-demand oligopoly model. Suppose the current price is $50. If one firm in the oligopoly now attempts to raise price, all firms will:

A) follow along demand curve D1.

B) follow along demand curve D2.

C) ignore this price increase and cause the price-raising firm to move along D1.

D) ignore this price increase and cause the price-raising firm to move along D2.

Question

Question

Question

Exhibit 10-4 Kinked demand curves

In Exhibit 10-4, in a kinked-demand oligopoly model, D2 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

In Exhibit 10-4, in a kinked-demand oligopoly model, D2 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Exhibit 10-4 Kinked demand curves

In Exhibit 10-4, in a kinked-demand oligopoly model, D1 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

In Exhibit 10-4, in a kinked-demand oligopoly model, D1 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/97

Play

Full screen (f)

Deck 10: Monopolistic Competition and Oligopoly

1

Which of the following is the best example of a firm operating in a monopolistically competitive market?

A) A Kansas wheat farmer.

B) TGI Fridays, a family restaurant.

C) U.S. Postal Service.

D) Boeing, an aircraft manufacturer

A) A Kansas wheat farmer.

B) TGI Fridays, a family restaurant.

C) U.S. Postal Service.

D) Boeing, an aircraft manufacturer

B

2

The demand curve in monopolistic competition slopes downward because of:

A) strong barriers to entry.

B) product differentiation.

C) the small number of firms.

D) government regulation.

A) strong barriers to entry.

B) product differentiation.

C) the small number of firms.

D) government regulation.

B

3

What are the characteristics of monopolistic competition?

Monopolistic competition is characterized by a large number of sellers selling a differentiated product. There are relatively weak barriers to entry and firms compete aggressively on a nonprice basis.

4

Which of the following is the result of competing through advertising for a monopolistically competitive firm?

A) Long-run average costs shift downward.

B) The firm's demand curve become flatter and shifts inward.

C) The firm's demand curve keeps the same slope and shifts inward.

D) Long-run average costs shift upward.

A) Long-run average costs shift downward.

B) The firm's demand curve become flatter and shifts inward.

C) The firm's demand curve keeps the same slope and shifts inward.

D) Long-run average costs shift upward.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

5

Because a monopolistically competitive market is characterized by

A) many small sellers selling a differentiated product, each seller has some influence over its own price.

B) a single seller of a product that has few suitable substitutes, the seller is a price maker.

C) many small sellers selling a differentiated product, one seller's change in price has a large effect on the market price.

D) a few sellers selling a differentiated product, each seller bases its decisions on the expected decisions of its rivals.

A) many small sellers selling a differentiated product, each seller has some influence over its own price.

B) a single seller of a product that has few suitable substitutes, the seller is a price maker.

C) many small sellers selling a differentiated product, one seller's change in price has a large effect on the market price.

D) a few sellers selling a differentiated product, each seller bases its decisions on the expected decisions of its rivals.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

6

Which of the following is true about advertising?

A) Firms spend money on advertising in an attempt to make the demand curve more elastic.

B) Advertising may be the only way that a new entrant can penetrate a market dominated by long-established firms.

C) Advertising has no impact on entry costs or market structure.

D) Firms consider advertising to be successful if it succeeds in lowering the long-run average cost.

A) Firms spend money on advertising in an attempt to make the demand curve more elastic.

B) Advertising may be the only way that a new entrant can penetrate a market dominated by long-established firms.

C) Advertising has no impact on entry costs or market structure.

D) Firms consider advertising to be successful if it succeeds in lowering the long-run average cost.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

7

The monopolistic competition market structure is characterized by:

A) few firms and similar products.

B) many firms and differentiated products.

C) many firms and a homogeneous product.

D) few firms and a homogeneous product.

A) few firms and similar products.

B) many firms and differentiated products.

C) many firms and a homogeneous product.

D) few firms and a homogeneous product.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is always associated with monopolistic competition?

A) identical products

B) economic profits in the short run

C) product differentiation

D) Demand curves become more inelastic as new entry occurs.

A) identical products

B) economic profits in the short run

C) product differentiation

D) Demand curves become more inelastic as new entry occurs.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

9

The marginal revenue curve of a monopolistically competitive firm will always lie:

A) below the firm's demand curve.

B) parallel to the firm's demand curve.

C) parallel to the firm's quantity axis.

D) above the firm's demand curve.

A) below the firm's demand curve.

B) parallel to the firm's demand curve.

C) parallel to the firm's quantity axis.

D) above the firm's demand curve.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is true about advertising by a firm?

A) It is always successful in increasing demand for a firm's product.

B) It attempts to increase demand and to make demand more inelastic.

C) It reduces barriers to entry in a market.

D) It is only used in the monopolistic competition market structure.

A) It is always successful in increasing demand for a firm's product.

B) It attempts to increase demand and to make demand more inelastic.

C) It reduces barriers to entry in a market.

D) It is only used in the monopolistic competition market structure.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

11

Exhibit 10-3 A monopolistic competitive firm in the long run

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-3 will charge a price per unit of:

A) zero.

B) $10

C) $20.

D) $30.

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-3 will charge a price per unit of:

A) zero.

B) $10

C) $20.

D) $30.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

12

Critics of advertising argue that it:

A) lowers price by increasing competition.

B) results in more variety of products.

C) establishes brand loyalty, which promotes competition.

D) serves as a barrier to entry for new firms.

A) lowers price by increasing competition.

B) results in more variety of products.

C) establishes brand loyalty, which promotes competition.

D) serves as a barrier to entry for new firms.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

13

The theory of monopolistic competition predicts that in long-run equilibrium a monopolistically competitive firm will:

A) produce the output level at which price equals long-run marginal cost.

B) operate at minimum long-run average cost.

C) overutilize its insufficient capacity.

D) produce the output level at which price equals long-run average cost.

A) produce the output level at which price equals long-run marginal cost.

B) operate at minimum long-run average cost.

C) overutilize its insufficient capacity.

D) produce the output level at which price equals long-run average cost.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

14

A profit-maximizing monopolistically competitive firm will expand output to the point where:

A) total revenue equals total cost.

B) marginal revenue equals marginal cost.

C) price equals average total cost.

D) price equals marginal cost.

A) total revenue equals total cost.

B) marginal revenue equals marginal cost.

C) price equals average total cost.

D) price equals marginal cost.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

15

Product differentiation makes the demand for a monopolistically competitive firm's product:

A) perfectly elastic.

B) more elastic than for a monopoly.

C) more inelastic than for a monopoly.

D) perfectly inelastic.

A) perfectly elastic.

B) more elastic than for a monopoly.

C) more inelastic than for a monopoly.

D) perfectly inelastic.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following is characteristic of a monopolistically competitive firm?

A) The firm faces an upward-sloping demand curve.

B) The firm faces an inelastic demand curve.

C) The firm faces a horizontal demand curve.

D) The firm produces a differentiated product.

A) The firm faces an upward-sloping demand curve.

B) The firm faces an inelastic demand curve.

C) The firm faces a horizontal demand curve.

D) The firm produces a differentiated product.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following statements best describes firms under monopolistic competition?

A) There is little price or quality competition.

B) The firms compete, using quality, location, advertising, and price.

C) Firms do not compete using advertising.

D) There is only one firm so there is no competition.

A) There is little price or quality competition.

B) The firms compete, using quality, location, advertising, and price.

C) Firms do not compete using advertising.

D) There is only one firm so there is no competition.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

18

Which of the following is not true of a monopolistically competitive firm?

A) The firm will maximize profits by producing where MR = MC.

B) The firm will not likely earn an economic profit in the long run.

C) The firm will shut down if price is less than average variable cost.

D) The firm will produce an efficient quantity where average total cost is minimized.

A) The firm will maximize profits by producing where MR = MC.

B) The firm will not likely earn an economic profit in the long run.

C) The firm will shut down if price is less than average variable cost.

D) The firm will produce an efficient quantity where average total cost is minimized.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following most closely approximates the conditions of a monopolistically competitive market?

A) The market for Grade A eggs, which is characterized by a large number of firms producing a homogeneous product.

B) The restaurant industry, which is characterized by firms producing a differentiated product in a market with low entry barriers.

C) Local cable television service, where a licensed supplier competes with firms offering satellite service.

D) The market for jumbo aircraft, where one major domestic firm competes with one major foreign firm.

A) The market for Grade A eggs, which is characterized by a large number of firms producing a homogeneous product.

B) The restaurant industry, which is characterized by firms producing a differentiated product in a market with low entry barriers.

C) Local cable television service, where a licensed supplier competes with firms offering satellite service.

D) The market for jumbo aircraft, where one major domestic firm competes with one major foreign firm.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

20

Nonprice competition in monopolistically competitive markets results in

A) consumers buying the product with the lowest price in a differentiated market.

B) less advertising and product differentiation than in markets without nonprice competition.

C) rivalry among competing firms based on the characteristics that differentiate their products.

D) price equaling the minimum average total cost in long run equilibrium.

A) consumers buying the product with the lowest price in a differentiated market.

B) less advertising and product differentiation than in markets without nonprice competition.

C) rivalry among competing firms based on the characteristics that differentiate their products.

D) price equaling the minimum average total cost in long run equilibrium.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

21

Costume jewelry is produced in a monopolistically competitive market. One producer finds that MR = MC = $3 when output is 700 necklaces. An economist studying this information can conclude that:

A) the producer is charging a price of $3.

B) economic profit is $2,100.

C) the producer charges a price greater than $3.

D) new firms will want to enter.

A) the producer is charging a price of $3.

B) economic profit is $2,100.

C) the producer charges a price greater than $3.

D) new firms will want to enter.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

22

The short-run equilibrium for a monopolistically competitive firm is at P = $28.47, ATC = $22.13, and MC = MR = $17.47. Which of the following is true ?

A) Average cost must be rising.

B) Additional firms will be attracted into the industry.

C) The firm could raise price and increase profits.

D) The firm could lower price and increase profits.

A) Average cost must be rising.

B) Additional firms will be attracted into the industry.

C) The firm could raise price and increase profits.

D) The firm could lower price and increase profits.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

23

Exit of existing firms will occur in a monopolistic competitive industry until:

A) marginal cost equals zero.

B) marginal revenue equals zero.

C) marginal revenue equals marginal cost.

D) economic profit equals zero.

A) marginal cost equals zero.

B) marginal revenue equals zero.

C) marginal revenue equals marginal cost.

D) economic profit equals zero.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

24

Exhibit 10-1 A monopolistic competitive firm

As presented in Exhibit 10-1, the short-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per day.

B) 200 units per day.

C) 400 units per day.

D) 600 units per day.

As presented in Exhibit 10-1, the short-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per day.

B) 200 units per day.

C) 400 units per day.

D) 600 units per day.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

25

Exhibit 10-1 A monopolistic competitive firm

In the long run, the demand curve for the monopolistic competitive firm shown in Exhibit 10-1:

A) shifts leftward.

B) remains the same.

C) shifts rightward.

D) becomes more inelastic.

In the long run, the demand curve for the monopolistic competitive firm shown in Exhibit 10-1:

A) shifts leftward.

B) remains the same.

C) shifts rightward.

D) becomes more inelastic.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

26

Exhibit 10-3 A monopolistic competitive firm in the long run

As presented in Exhibit 10-3, the long-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per week.

B) 200 units per week.

C) 400 units per week.

D) 600 units per week.

As presented in Exhibit 10-3, the long-run profit-maximizing output for the monopolistic competitive firm is:

A) zero units per week.

B) 200 units per week.

C) 400 units per week.

D) 600 units per week.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

27

As new firms enter a monopolistic competitive industry, it can be expected that:

A) market price will increase.

B) the output of existing firms will increase.

C) profits of existing firms will increase.

D) profits of existing firms will decrease.

A) market price will increase.

B) the output of existing firms will increase.

C) profits of existing firms will increase.

D) profits of existing firms will decrease.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

28

Exhibit 10-2 A monopolistic competitive firm

As represented in Exhibit 10-2, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per week.

C) $1,000 per week.

D) $20,000 per week.

As represented in Exhibit 10-2, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per week.

C) $1,000 per week.

D) $20,000 per week.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

29

Exhibit 10-1 A monopolistic competitive firm

As represented in Exhibit 10-1, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per day.

C) $1,000 per day.

D) $20,000 per day.

As represented in Exhibit 10-1, the maximum long-run economic profit earned by this monopolistic competitive firm is:

A) zero.

B) $200 per day.

C) $1,000 per day.

D) $20,000 per day.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

30

Exhibit 10-2 A monopolistic competitive firm

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-2 will charge a price per unit of:

A) zero.

B) $5.

C) $10.

D) $15.

To maximize long-run profits, the monopolistically competitive firm shown in Exhibit 10-2 will charge a price per unit of:

A) zero.

B) $5.

C) $10.

D) $15.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

31

Exhibit 10-2 A monopolistic competitive firm

Comparing the monopolistically competitive firm in Exhibit 10-2 to the long-run profit-maximizing outcome for a perfectly competitive firm with a price of $15 per unit and a quantity of 600,

A) the quantity produced by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

B) the profit earned by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

C) the marginal revenue of the monopolistically competitive firm is lower than that of the perfectly competitive firm at the profit-maximizing quantity.

D) the long run average cost of the monopolistically competitive firm is higher than that of the perfectly competitive firm at the profit-maximizing quantity.

Comparing the monopolistically competitive firm in Exhibit 10-2 to the long-run profit-maximizing outcome for a perfectly competitive firm with a price of $15 per unit and a quantity of 600,

A) the quantity produced by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

B) the profit earned by the monopolistically competitive firm is higher than that of the perfectly competitive firm.

C) the marginal revenue of the monopolistically competitive firm is lower than that of the perfectly competitive firm at the profit-maximizing quantity.

D) the long run average cost of the monopolistically competitive firm is higher than that of the perfectly competitive firm at the profit-maximizing quantity.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

32

In monopolistic competition if there is profit, there is:

A) a signal for new firms to enter.

B) a motive for existing firms to increase prices.

C) proof that advertising works.

D) a motive for existing firms to decrease prices.

A) a signal for new firms to enter.

B) a motive for existing firms to increase prices.

C) proof that advertising works.

D) a motive for existing firms to decrease prices.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

33

Which of the following statements best describes the price, output, and profit conditions of monopolistic competition?

A) Price will equal marginal cost at the profit-maximizing level of output; profits will be positive in the long-run.

B) Price will always equal average variable cost in the short run and either profits or losses may result in the long run.

C) Marginal revenue will equal marginal cost at the short run, profit-maximizing level of output; in the long run, economic profit will be zero.

D) Marginal revenue will equal average total cost in the short run; long-run economic profits will be zero.

A) Price will equal marginal cost at the profit-maximizing level of output; profits will be positive in the long-run.

B) Price will always equal average variable cost in the short run and either profits or losses may result in the long run.

C) Marginal revenue will equal marginal cost at the short run, profit-maximizing level of output; in the long run, economic profit will be zero.

D) Marginal revenue will equal average total cost in the short run; long-run economic profits will be zero.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

34

Entry of new firms into a monopolistically competitive market causes a(n)

A) decrease in the existing firms' demand curves.

B) increase in the existing firms' demand curves.

C) decrease in the existing firms' cost curves.

D) increase in the existing firms' cost curves.

A) decrease in the existing firms' demand curves.

B) increase in the existing firms' demand curves.

C) decrease in the existing firms' cost curves.

D) increase in the existing firms' cost curves.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

35

Exhibit 10-2 A monopolistic competitive firm

If all firms in a monopolistic competitive industry have demand and cost curves like those shown in Exhibit 10-2, we would expect that in the long run:

A) all firms will leave the industry.

B) some firms will leave the industry.

C) firms in the industry earn zero economic profits.

D) a number of new firms will enter the industry.

If all firms in a monopolistic competitive industry have demand and cost curves like those shown in Exhibit 10-2, we would expect that in the long run:

A) all firms will leave the industry.

B) some firms will leave the industry.

C) firms in the industry earn zero economic profits.

D) a number of new firms will enter the industry.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

36

Tombstones are produced in a monopolistic competitive market. One producer, Rolling Stones, sells 20 tombstones a week at a price of $500 each. Its average total cost is $600. From this information, we can tell:

A) new tombstone firms will want to enter.

B) this producer is losing $2,000 a week.

C) this producer is making an economic profit of $400.

D) this producer should increase production.

A) new tombstone firms will want to enter.

B) this producer is losing $2,000 a week.

C) this producer is making an economic profit of $400.

D) this producer should increase production.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

37

A picture frame company operates in a monopolistically competitive market. Its short-run equilibrium price is $80 and its ATC is $65. It sells 100 picture frames a week. From this we can tell:

A) this firm is making a normal profit.

B) other picture frame companies will want to exit the market.

C) there are no other picture frame companies in the area.

D) economic profits are $1,500.

A) this firm is making a normal profit.

B) other picture frame companies will want to exit the market.

C) there are no other picture frame companies in the area.

D) economic profits are $1,500.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

38

In the long run, the economic profits of Hoot's Chicken 'n' Ribs, a monopolistic competitor, are:

A) not eliminated, because competition is not perfect.

B) not eliminated, because the demand curve slopes downward.

C) eliminated due to firms entering the industry.

D) eliminated due to firms leaving the industry.

A) not eliminated, because competition is not perfect.

B) not eliminated, because the demand curve slopes downward.

C) eliminated due to firms entering the industry.

D) eliminated due to firms leaving the industry.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

39

Exhibit 10-1 A monopolistic competitive firm

If all firms in the industry are the same as the monopolistic competitive firm shown in this Exhibit 10-1, firms in the long run will:

A) leave the industry.

B) earn positive economic profits.

C) experience less competition because firms will exit the industry.

D) experience competition from new firms that enter the industry.

If all firms in the industry are the same as the monopolistic competitive firm shown in this Exhibit 10-1, firms in the long run will:

A) leave the industry.

B) earn positive economic profits.

C) experience less competition because firms will exit the industry.

D) experience competition from new firms that enter the industry.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

40

Compared to monopoly, the market results with monopolistic competition are usually expected to be:

A) worse because consumers get fewer choices.

B) worse because consumers pay a higher price.

C) better because consumers pay a lower price.

D) better because consumers get less output.

A) worse because consumers get fewer choices.

B) worse because consumers pay a higher price.

C) better because consumers pay a lower price.

D) better because consumers get less output.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

41

The automobile, steel, and oil markets are all examples of:

A) perfectly competitive markets.

B) monopolies.

C) monopolistically competitive markets.

D) oligopolies.

A) perfectly competitive markets.

B) monopolies.

C) monopolistically competitive markets.

D) oligopolies.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

42

In the long run, monopolistically competitive firms have:

A) excess capacity.

B) positive profits.

C) minimal average costs.

D) homogeneous production.

A) excess capacity.

B) positive profits.

C) minimal average costs.

D) homogeneous production.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

43

Suppose the Tidy Laundry Detergent Company, which sells 40% of all detergent, is thinking about raising its price. Before Tidy makes the change, they analyze the likely responses of the All-Clean Detergent Company, which sells 35% of all detergent, and Cheerful Detergent Company, which sells 20% of all detergent. Tidy's behavior shows

A) mutual interdependence in pricing decisions.

B) nonprice competition.

C) difficult entry in oligopolies.

D) collusion.

A) mutual interdependence in pricing decisions.

B) nonprice competition.

C) difficult entry in oligopolies.

D) collusion.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

44

The industry that most closely approximates the conditions of the oligopoly model is:

A) restaurants.

B) retail clothing.

C) home construction.

D) tires.

A) restaurants.

B) retail clothing.

C) home construction.

D) tires.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following is true in long-run equilibrium for both perfect competition and monopolistic competition?

A) Accounting profit is zero.

B) Marginal cost equals price.

C) Long-run average cost is at a minimum.

D) Economic profit is zero.

A) Accounting profit is zero.

B) Marginal cost equals price.

C) Long-run average cost is at a minimum.

D) Economic profit is zero.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

46

A monopolistic competitive firm is inefficient because the firm:

A) earns positive economic profit in the long run.

B) is producing at an output corresponding to the condition that marginal cost equals price.

C) is not maximizing its profit.

D) produces an output where average total cost is not minimum.

A) earns positive economic profit in the long run.

B) is producing at an output corresponding to the condition that marginal cost equals price.

C) is not maximizing its profit.

D) produces an output where average total cost is not minimum.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

47

Product differentiation:

A) refers to the attempt of firms to make their products look like those of the other firms in the industry and is used in a perfectly competitive market structure.

B) refers to the attempt of firms to make real or apparent differences in essentially substitutable products look different in the minds of the consumers and is used in a monopolistically competitive market structure.

C) leads to nonprice competition in a perfectly competitive market structure.

D) leads to price equaling the minimum average total cost in the long run in a monopolistically competitive market structure.

A) refers to the attempt of firms to make their products look like those of the other firms in the industry and is used in a perfectly competitive market structure.

B) refers to the attempt of firms to make real or apparent differences in essentially substitutable products look different in the minds of the consumers and is used in a monopolistically competitive market structure.

C) leads to nonprice competition in a perfectly competitive market structure.

D) leads to price equaling the minimum average total cost in the long run in a monopolistically competitive market structure.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

48

Suppose ABC Dairy is one firm competing in the perfectly competitive market for milk. Now suppose ABC Dairy decides to produce only organic milk. Which of the following best describes the effects of this change in the market?

A) ABC Dairy is differentiating its product and will likely be able to charge a higher price than before.

B) ABC Dairy will still be a price taker because it is still operating in a perfectly competitive market.

C) ABC Dairy will have a monopoly on organic milk due to very high entry barriers.

D) The other dairy firms will produce with excess capacity, but ABC Dairy will be efficient.

A) ABC Dairy is differentiating its product and will likely be able to charge a higher price than before.

B) ABC Dairy will still be a price taker because it is still operating in a perfectly competitive market.

C) ABC Dairy will have a monopoly on organic milk due to very high entry barriers.

D) The other dairy firms will produce with excess capacity, but ABC Dairy will be efficient.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

49

When the price and output decisions of one firm include the possible price and output reactions of the firm's rivals, the market is

A) a monopoly characterized by differentiated products.

B) an oligopoly characterized by mutual interdependence.

C) perfectly competitive characterized by collusion.

D) monopolistically competitive characterized by nonprice competition.

A) a monopoly characterized by differentiated products.

B) an oligopoly characterized by mutual interdependence.

C) perfectly competitive characterized by collusion.

D) monopolistically competitive characterized by nonprice competition.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

50

What is the key feature shared by all oligopoly markets?

A) a large number of sellers

B) mutual interdependence

C) product differentiation

D) easy entry and exit

A) a large number of sellers

B) mutual interdependence

C) product differentiation

D) easy entry and exit

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

51

When Pepsi is considering a price hike, it needs to consider how Coke may react. This situation is called:

A) mutual interdependence.

B) price leadership.

C) collusion.

D) monopolistic competition.

A) mutual interdependence.

B) price leadership.

C) collusion.

D) monopolistic competition.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

52

The market for Product A has many sellers, selling identical products, each earning an economic profit of zero in the long run. The market for Product B has many sellers, selling differentiated products, each earning an economics profit of zero in the long run. Given this information, one can conclude that

A) The markets for Product A and Product B are perfectly competitive.

B) The markets for Product A and Product B are monopolistically competitive.

C) The market for Product A is monopolistically competitive and the market for Product B is perfectly competitive.

D) The market for Product A is perfectly competitive and the market for Product B is monopolistically competitive.

A) The markets for Product A and Product B are perfectly competitive.

B) The markets for Product A and Product B are monopolistically competitive.

C) The market for Product A is monopolistically competitive and the market for Product B is perfectly competitive.

D) The market for Product A is perfectly competitive and the market for Product B is monopolistically competitive.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

53

While there is no specific number of firms that must dominate an industry before it is an oligopoly, the number of sellers characterizes an oligopoly when

A) there are more firms than a monopolistically competitive market.

B) there is a sufficient number of firms to satisfy the market demand.

C) the firms are so large relative to the total market that they can affect the market price.

D) the firms are so small relative to the total market that they cannot affect the market price.

A) there are more firms than a monopolistically competitive market.

B) there is a sufficient number of firms to satisfy the market demand.

C) the firms are so large relative to the total market that they can affect the market price.

D) the firms are so small relative to the total market that they cannot affect the market price.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

54

When a perfectly competitive firm or a monopolistically competitive firm is making zero economic profit,

A) no firms will want to enter or exit.

B) some firms will want to leave.

C) some firms will want to enter.

D) market demand shifts to the left.

A) no firms will want to enter or exit.

B) some firms will want to leave.

C) some firms will want to enter.

D) market demand shifts to the left.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

55

A market situation where a small number of sellers dominate the entire industry is called:

A) monopolistic competition.

B) monopsony.

C) monopoly.

D) oligopoly.

A) monopolistic competition.

B) monopsony.

C) monopoly.

D) oligopoly.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

56

The markets for Products X and Y both have many sellers, each earning an economic profit of zero in the long run. One of the markets is perfectly competitive while the other is monopolistically competitive. Which of the following information can help you determine which operates in a monopolistically competitive market structure?

A) There is easy entry into the market for Product X.

B) The firms selling product Y choose the profit-maximizing quantity where MR = MC.

C) The price for Product X is higher than the marginal cost at the profit-maximizing quantity.

D) The price for Product Y is equal to the average total cost at the long-run equilibrium quantity.

A) There is easy entry into the market for Product X.

B) The firms selling product Y choose the profit-maximizing quantity where MR = MC.

C) The price for Product X is higher than the marginal cost at the profit-maximizing quantity.

D) The price for Product Y is equal to the average total cost at the long-run equilibrium quantity.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

57

Exhibit 10-2 A monopolistic competitive firm

Comparing the firms in a monopolistic competitive industry shown in Exhibit 10-2 to a perfectly competitive firm in long-run equilibrium, we find that both firms

A) choose a price equal to the marginal cost at the profit-maximizing quantity.

B) will experience entry of new firms into the industry.

C) earn zero economic profits.

D) minimize cost per unit at their profit-maximizing quantity.

Comparing the firms in a monopolistic competitive industry shown in Exhibit 10-2 to a perfectly competitive firm in long-run equilibrium, we find that both firms

A) choose a price equal to the marginal cost at the profit-maximizing quantity.

B) will experience entry of new firms into the industry.

C) earn zero economic profits.

D) minimize cost per unit at their profit-maximizing quantity.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

58

One key characteristic that is distinctive of an oligopoly market is that:

A) the demand curve facing each firm is downward sloping, with a marginal revenue curve that lies below the firm's demand curve.

B) the decisions of one seller often influences the price of products, the output, and the profits of rival firms.

C) there is only one firm that produces a product for which there are no good substitutes.

D) there are many sellers in the market and each is small relative to the total market.

A) the demand curve facing each firm is downward sloping, with a marginal revenue curve that lies below the firm's demand curve.

B) the decisions of one seller often influences the price of products, the output, and the profits of rival firms.

C) there is only one firm that produces a product for which there are no good substitutes.

D) there are many sellers in the market and each is small relative to the total market.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

59

Monopolistic competition is inefficient because:

A) firms earn positive economic profits.

B) the firms' marginal costs and marginal revenues are not equal.

C) firms have excess capacity in the long run.

D) entry is difficult.

A) firms earn positive economic profits.

B) the firms' marginal costs and marginal revenues are not equal.

C) firms have excess capacity in the long run.

D) entry is difficult.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

60

Perfect competition and monopolistic competition are similar because under both market structures,

A) there are many firms.

B) production takes place at the least-cost combination.

C) differentiated products are produced.

D) entry is difficult.

A) there are many firms.

B) production takes place at the least-cost combination.

C) differentiated products are produced.

D) entry is difficult.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

61

Suppose Ford, GM, and Dodge make the majority of pick-up trucks sold in the United States If they all sell for approximately the same price, and Ford offers a $2,000 rebate on new truck sales, what can Ford expect to see?

A) an unprecedented increase in truck sales

B) an immediate response by GM and Dodge

C) a visit from the antitrust authorities of the government

D) a revolution from Ford stockholders

A) an unprecedented increase in truck sales

B) an immediate response by GM and Dodge

C) a visit from the antitrust authorities of the government

D) a revolution from Ford stockholders

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

62

The two tendencies of a firm in a cartel are the incentive to:

A) cheat to maximize joint profits and the incentive to raise prices.

B) cheat and avoid collusion and the incentive to raise price to maximize the firm's share of profits.

C) increase output in order to minimize per-unit cost and the incentive to reduce price in order to maximize joint profit.

D) cooperate to maximize joint profits and to cheat on the agreement in order to increase the firm's share of the profit.

A) cheat to maximize joint profits and the incentive to raise prices.

B) cheat and avoid collusion and the incentive to raise price to maximize the firm's share of profits.

C) increase output in order to minimize per-unit cost and the incentive to reduce price in order to maximize joint profit.

D) cooperate to maximize joint profits and to cheat on the agreement in order to increase the firm's share of the profit.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

63

Suppose an oil cartel has an agreement to restrict members' production in order to maintain a price of $30 per barrel. A single cartel member may want to cheat and exceed its quota so that it can:

A) reduce its costs.

B) charge higher prices.

C) make demand more inelastic.

D) earn a bigger profit.

A) reduce its costs.

B) charge higher prices.

C) make demand more inelastic.

D) earn a bigger profit.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

64

In a price leadership oligopoly model,

A) a cartel of leading firms determines price and industry output.

B) the industry in consortium with the government determines price and output.

C) one firm is the price leader and all other firms follow.

D) the firms abandon a profit-maximizing goal.

A) a cartel of leading firms determines price and industry output.

B) the industry in consortium with the government determines price and output.

C) one firm is the price leader and all other firms follow.

D) the firms abandon a profit-maximizing goal.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

65

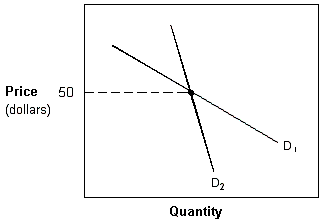

Exhibit 10-4 Kinked demand curves

In Exhibit 10-4, the exhibit represents a kinked-demand oligopoly model. Suppose the current price is $50. If one firm in the oligopoly now attempts to raise price, all firms will:

A) follow along demand curve D1.

B) follow along demand curve D2.

C) ignore this price increase and cause the price-raising firm to move along D1.

D) ignore this price increase and cause the price-raising firm to move along D2.

In Exhibit 10-4, the exhibit represents a kinked-demand oligopoly model. Suppose the current price is $50. If one firm in the oligopoly now attempts to raise price, all firms will:

A) follow along demand curve D1.

B) follow along demand curve D2.

C) ignore this price increase and cause the price-raising firm to move along D1.

D) ignore this price increase and cause the price-raising firm to move along D2.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

66

A kink in the demand curve facing an oligopolist is caused by:

A) rapidly rising marginal revenues.

B) excessive advertising.

C) the belief that competitors will follow price increases but not match price decreases.

D) the tendency of competitors to follow price reductions but not price increases.

A) rapidly rising marginal revenues.

B) excessive advertising.

C) the belief that competitors will follow price increases but not match price decreases.

D) the tendency of competitors to follow price reductions but not price increases.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

67

Which of the following is the best example of an oligopoly?

A) area restaurants

B) the automobile industry

C) agricultural markets free of government support

D) local utilities

A) area restaurants

B) the automobile industry

C) agricultural markets free of government support

D) local utilities

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

68

Exhibit 10-4 Kinked demand curves

In Exhibit 10-4, in a kinked-demand oligopoly model, D2 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

In Exhibit 10-4, in a kinked-demand oligopoly model, D2 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

69

Assume that an oligopolist has a kinked demand curve. Suppose that the marginal cost curve passes through the gap in the marginal revenue curve. This means price and output will be shown by a point:

A) above the curve.

B) below the curve.

C) at the kink.

D) on the upper part of the curve.

A) above the curve.

B) below the curve.

C) at the kink.

D) on the upper part of the curve.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

70

As a result of a kinked demand curve, the price:

A) fluctuates.

B) falls below the kink.

C) settles at the kink.

D) rises above the kink.

A) fluctuates.

B) falls below the kink.

C) settles at the kink.

D) rises above the kink.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

71

In order to make oil profits as large as possible, OPEC meets to set oil production quotas for its members. OPEC is best classified as a:

A) monopoly.

B) cartel.

C) kinked demand industry.

D) price-leadership industry.

A) monopoly.

B) cartel.

C) kinked demand industry.

D) price-leadership industry.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

72

Cartel members have an incentive to cheat on the cartel because:

A) the industry profit would be higher under competitive conditions.

B) the cartel price is the competitive price.

C) each member's output quota is too high.

D) each member's MR is not equal to the cartel's MC.

A) the industry profit would be higher under competitive conditions.

B) the cartel price is the competitive price.

C) each member's output quota is too high.

D) each member's MR is not equal to the cartel's MC.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

73

The kinked demand theory attempts to explain why an oligopolistic firm:

A) has relatively large advertising expenditures.

B) fails to invest in research and development.

C) infrequently changes its price.

D) engages in excessive brand proliferation.

A) has relatively large advertising expenditures.

B) fails to invest in research and development.

C) infrequently changes its price.

D) engages in excessive brand proliferation.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

74

A kinked demand curve is perceived by the firm as being:

A) more elastic to the right of the kink

B) more inelastic to the right of the kink

C) more inelastic to the left of the kink

D) present when there is a monopoly

A) more elastic to the right of the kink

B) more inelastic to the right of the kink

C) more inelastic to the left of the kink

D) present when there is a monopoly

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

75

Pricing and output determination under an oligopoly is more complicated than pricing and output determinations in other industries. The primary reason for the complication is the:

A) fewness of firms.

B) brand loyalty of consumers.

C) powerful effect of advertising.

D) mutual interdependence of firms.

A) fewness of firms.

B) brand loyalty of consumers.

C) powerful effect of advertising.

D) mutual interdependence of firms.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

76

What are the characteristics of an oligopoly?

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

77

If OPEC is an effective cartel,

A) price changes are dictated by changes in demand.

B) output changes are dictated by changes in demand.

C) members agree on output quotas.

D) oil prices will be lower than if the market functioned competitively.

A) price changes are dictated by changes in demand.

B) output changes are dictated by changes in demand.

C) members agree on output quotas.

D) oil prices will be lower than if the market functioned competitively.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

78

Suppose that R. J. Reynolds raises the price of cigarettes by 10 percent. Although they have no requirement or agreement to do so, the other cigarette firms decide to raise their prices accordingly. This situation is best described as:

A) price leadership.

B) a cartel.

C) monopolistic competition.

D) a market with kinked demand.

A) price leadership.

B) a cartel.

C) monopolistic competition.

D) a market with kinked demand.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

79

Suppose Kellogg's, General Mills, and Post make the majority of breakfast cereal sold in the United States. If Kellogg's decides to decrease its prices by 10%,

A) General Mills and Post will immediately respond because of mutual interdependence.

B) Kellogg's will also decrease the variety of cereals it offers because of nonprice competition.

C) the other firms in the industry will not change their pricing strategy because of the kinked demand curve.

D) more firms will enter the market due to low barriers to entry.

A) General Mills and Post will immediately respond because of mutual interdependence.

B) Kellogg's will also decrease the variety of cereals it offers because of nonprice competition.

C) the other firms in the industry will not change their pricing strategy because of the kinked demand curve.

D) more firms will enter the market due to low barriers to entry.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

80

Exhibit 10-4 Kinked demand curves

In Exhibit 10-4, in a kinked-demand oligopoly model, D1 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

In Exhibit 10-4, in a kinked-demand oligopoly model, D1 represents the demand curve

A) applicable to any price increase above $50.

B) applicable to any price decrease below $50.

C) facing firms when a cartel is formed.

D) facing the price leader.

Unlock Deck

Unlock for access to all 97 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 97 flashcards in this deck.