Deck 3: Social Security Taxes

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Instruction 3-1  *Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Dee is paid $2,345 on November 8, 20--. Dee had cumulative gross earnings, including overtime pay, of $131,600 prior to this pay.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed. Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Dee is paid $2,345 on November 8, 20--. Dee had cumulative gross earnings, including overtime pay, of $131,600 prior to this pay.

Question

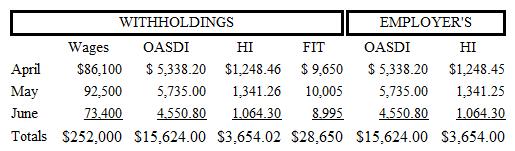

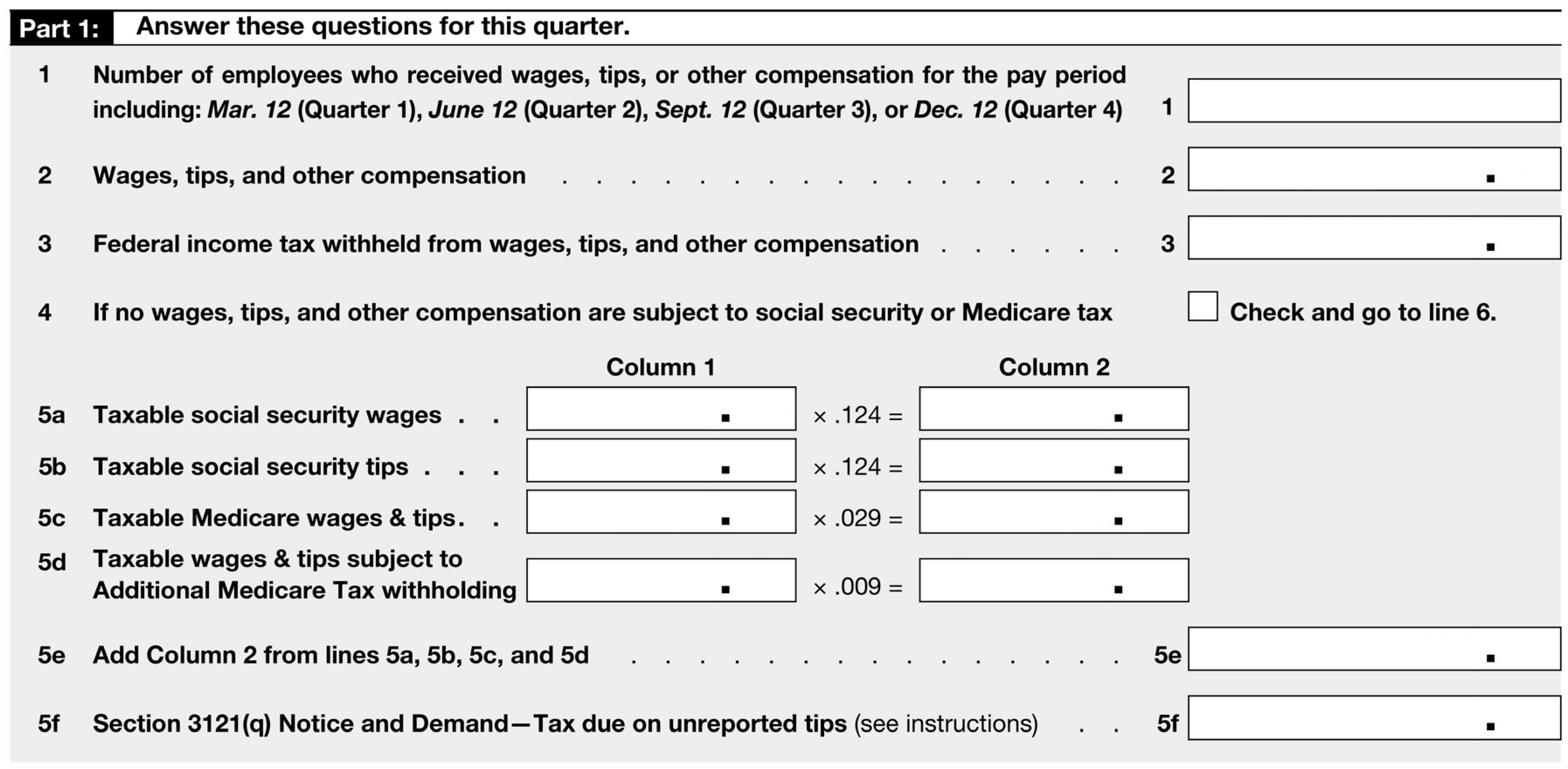

Lidge Company of Texas (TX) is classified as a monthly depositor and pays its employees monthly. The following payroll information is for the second quarter of 20--.

The number of employees on June 12, 20-- was 11.

a. Complete the following portion of Form 941.

Source: Internal Revenue Service

b. Complete the following portion of Form 941.

Source: Internal Revenue Service

c. Complete Part 2 of Form 941.

Source: Internal Revenue Service

d. What are the payment due dates of each of the monthly liabilities assuming all

deposits were made on time, and the due date of the filing of Form 941 (year 20--)?

The number of employees on June 12, 20-- was 11.

a. Complete the following portion of Form 941.

Source: Internal Revenue Service

b. Complete the following portion of Form 941.

Source: Internal Revenue Service

c. Complete Part 2 of Form 941.

Source: Internal Revenue Service

d. What are the payment due dates of each of the monthly liabilities assuming all

deposits were made on time, and the due date of the filing of Form 941 (year 20--)?

Question

Question

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . In this pay, Moss Company deducted OASDI taxes of $5,276.24 and HI taxes of $1,233.95 from the $85,100.90 of taxable wages paid. What is Moss Company's portion of the social security taxes for:

a) OASDI

b) HI

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . In this pay, Moss Company deducted OASDI taxes of $5,276.24 and HI taxes of $1,233.95 from the $85,100.90 of taxable wages paid. What is Moss Company's portion of the social security taxes for:

a) OASDI

b) HI

Question

Instruction 3-1  *Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Jax Company's (a monthly depositor) tax liability (amount withheld from employees' wages for federal income tax and FICA tax plus the company's portion of the FICA tax) for July was $1,210.

No deposit was made by the company until August 24, 20-- (9 days late). Determine:

a) The date by which the deposit should have been made

b) The penalty for failure to make timely deposit

c) The penalty for failure to fully pay tax when due

d) The interest on taxes due and unpaid (assume a 5% interest rate)

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed. Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Jax Company's (a monthly depositor) tax liability (amount withheld from employees' wages for federal income tax and FICA tax plus the company's portion of the FICA tax) for July was $1,210.

No deposit was made by the company until August 24, 20-- (9 days late). Determine:

a) The date by which the deposit should have been made

b) The penalty for failure to make timely deposit

c) The penalty for failure to fully pay tax when due

d) The interest on taxes due and unpaid (assume a 5% interest rate)

Question

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On August 1, Huff (part-time waitress) reported on Form 4070 the cash tips of $158.50 that she received in July. During August, Huff was paid wages of $550 by her employer. Determine:

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On August 1, Huff (part-time waitress) reported on Form 4070 the cash tips of $158.50 that she received in July. During August, Huff was paid wages of $550 by her employer. Determine:

Question

Question

Question

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Eager, a tipped employee, reported to his employer that he had received $320 in tips during March. On the next payday, April 6, he was paid his regular salary of $400.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Eager, a tipped employee, reported to his employer that he had received $320 in tips during March. On the next payday, April 6, he was paid his regular salary of $400.

Question

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On the last weekly pay of the first quarter, Lorenz is paid her current pay of $90 per day for four days worked and one day sick pay (total-$450). She is also paid her first quarter commission of $1,200 in this pay. How much will be deducted for:

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On the last weekly pay of the first quarter, Lorenz is paid her current pay of $90 per day for four days worked and one day sick pay (total-$450). She is also paid her first quarter commission of $1,200 in this pay. How much will be deducted for:

Question

Question

Question

Question

Question

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Crow earned $585.15 during the week ended March 1, 20--. Prior to payday, Crow had cumulative gross earnings of $4,733.20.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Crow earned $585.15 during the week ended March 1, 20--. Prior to payday, Crow had cumulative gross earnings of $4,733.20.

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/94

Play

Full screen (f)

Deck 3: Social Security Taxes

1

Each year, the FICA (OASDI portion) taxable wage base is automatically adjusted whenever a cost of living raise in social security benefits becomes available.

True

2

Exempt educational assistance includes payments for tools that employees keep after they complete a course of instruction.

False

3

Payments made to a worker's spouse for hospital expenses in connection with an accident disability are not considered wages under FICA.

True

4

OASDI taxes are levied when the wages are earned by , rather than when paid to , employees.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

5

FICA defines wages as including the cash value of meals provided for the convenience of the employees.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

6

The Federal Insurance Contributions Act levies a tax upon the gross earnings of self-employed persons.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

7

Employer payments made directly to employees in lieu of health insurance coverage are taxable wages.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

8

The FICA tax rates and taxable wage bases are exactly the same for the employee and employer when the employee makes $200,000 or less.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

9

Employees of a state government hired before January 1, 1986, and covered by a public retirement plan, are exempt from FICA coverage.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

10

Employees may use Form 4070 to report the amount of their tips to their employers.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

11

Under FICA only, cash tips of more than $100 in a month are defined as taxable wages.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

12

A worker hired by the federal government after 1983 is covered under FICA.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

13

Severance pay is considered taxable wages under FICA.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

14

In its definition of employee , FICA clearly distinguishes between classes or grades of employees.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

15

Peter, age 17 and employed by his family-owned corporation, is covered under FICA.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

16

The highest paid executives of a firm are excluded from coverage under the Federal Insurance Contributions Act (FICA).

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

17

FICA does not consider the first six months of sick pay as taxable wages.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

18

In computing their own FICA taxes, employers may exclude the total amount of tips reported to them by their tipped employees.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

19

Employers do not pay payroll taxes on payments made to independent contractors.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

20

FICA includes partnerships in its definition of employer .

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

21

Form 941 is used by employers to make their quarterly return of FICA taxes and withheld income taxes.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

22

The requirements for depositing FICA taxes and income taxes withheld from nonagricultural employees' wages vary according to the amount of such taxes reported during a "lookback period."

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

23

The Social Security Act requires workers to obtain a new account number each time they change jobs.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

24

If an employee, who works two or more separate jobs, pays OASDI taxes on wages in excess of the taxable wage base, the employee is entitled to a refund of the overpayment.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

25

If the accumulated employment taxes during a quarter are less than $2,500, no deposits are required.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

26

Self-employed persons include their self-employment taxes in their quarterly payment of estimated federal income taxes.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

27

All employers of one or more persons must file an application for an identification number.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

28

The Social Security Act does not require self-employed persons to have an account number.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

29

On Schedule B of Form 941, the employer does not show the date of each tax deposit during the quarter.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

30

Noncash items given to household employees by their employers are subject to FICA tax.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

31

State and local government employers must make their tax deposits according to a different schedule than private employers.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

32

Businesses with $2,500 or less in quarterly tax liabilities can pay the taxes when they file Form 941.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

33

Nonagricultural employers who withhold income taxes and are liable for social security taxes must file a monthly tax and information return.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

34

Employees are liable for their FICA taxes only until the taxes have been collected from their pay by their employer.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

35

A monthly depositor is one who reported employment taxes of $50,000 or more for the four quarters in the lookback period.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

36

Under SECA, all of an individual's self-employment income is counted in determining the HI tax.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

37

The employees of a semiweekly depositor are paid every Tuesday. The accumulated payroll taxes must be deposited on or before the following Friday.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

38

Monthly depositors are required to deposit their taxes by the 15th day of the following month.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

39

An employer's portion of social security and withheld income taxes for the quarter are less than $2,500. The employer must deposit the taxes at its bank at the time of filing the fourth quarter Form 941.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

40

Under the safe harbor rule, when employers deposit their tax liabilities, they may have a shortfall of no more than $200 without incurring any penalty.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

41

Which of the following deposit requirements pertains to a monthly depositor who has accumulated employment taxes of $2,900 at the end of October?

A) No deposit is required.

B) The undeposited taxes should be carried over to the end of November.

C) The taxes must be deposited on or before November 15.

D) The taxes must be deposited on or before the next banking day.

E) None of the above.

A) No deposit is required.

B) The undeposited taxes should be carried over to the end of November.

C) The taxes must be deposited on or before November 15.

D) The taxes must be deposited on or before the next banking day.

E) None of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

42

The OASDI taxable wage base is correctly defined as:

A) all amounts earned by an employee during a calendar year.

B) the maximum amount of wages during a calendar year that is subject to the OASDI tax.

C) all amounts paid an employee during a calendar year.

D) all amounts either earned by, or paid to, an employee during a calendar year.

E) none of the above.

A) all amounts earned by an employee during a calendar year.

B) the maximum amount of wages during a calendar year that is subject to the OASDI tax.

C) all amounts paid an employee during a calendar year.

D) all amounts either earned by, or paid to, an employee during a calendar year.

E) none of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

43

FICA excludes from coverage all of the following kinds of employment except :

A) domestic service performed in a college sorority by a student.

B) service performed by a 16-year-old child in the employ of the mother.

C) babysitting service performed by a 35-year-old person who receives $40 in cash during the calendar quarter.

D) federal government secretaries hired in 1990.

E) services performed by a railroad worker for an employer covered by the Railroad Retirement Tax Act.

A) domestic service performed in a college sorority by a student.

B) service performed by a 16-year-old child in the employ of the mother.

C) babysitting service performed by a 35-year-old person who receives $40 in cash during the calendar quarter.

D) federal government secretaries hired in 1990.

E) services performed by a railroad worker for an employer covered by the Railroad Retirement Tax Act.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

44

Each of the following items is accurately defined under FICA as taxable wages except :

A) value of meals furnished employees for the employer's convenience.

B) value of meals furnished employees for the employees' convenience.

C) commissions.

D) severance pay.

E) $500 award for productivity improvement suggestion.

A) value of meals furnished employees for the employer's convenience.

B) value of meals furnished employees for the employees' convenience.

C) commissions.

D) severance pay.

E) $500 award for productivity improvement suggestion.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

45

Which of the following statements does not describe an employee's FICA taxes and withholdings?

A) The employee's taxes are collected by the employer and paid to the IRS along with the employer's taxes.

B) The employee's taxes are deducted from the employee's wages at the time of payment.

C) The employee's liability for the FICA taxes continues even after the employer has withheld them.

D) The amount of tax to be withheld is computed by multiplying the employee's taxable wages by the current tax rate.

E) The employee is entitled to a refund for overpayment of FICA taxes resulting from having worked for more than one employer.

A) The employee's taxes are collected by the employer and paid to the IRS along with the employer's taxes.

B) The employee's taxes are deducted from the employee's wages at the time of payment.

C) The employee's liability for the FICA taxes continues even after the employer has withheld them.

D) The amount of tax to be withheld is computed by multiplying the employee's taxable wages by the current tax rate.

E) The employee is entitled to a refund for overpayment of FICA taxes resulting from having worked for more than one employer.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

46

Form 941 is due on or before the 15th day of the month following the close of the calendar quarter for which the return is made.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

47

Employers who fail to file employment tax returns are subject to both civil and criminal penalties.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

48

Form 944 (annual form) can be used by all new employers instead of Form 941.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

49

To be designated a semiweekly depositor, how much in employment taxes would an employer have reported for the four quarters in the lookback period?

A) More than $50,000.

B) More than $100,000.

C) Less than $50,000.

D) More than $2,500.

E) None of the above.

A) More than $50,000.

B) More than $100,000.

C) Less than $50,000.

D) More than $2,500.

E) None of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

50

Which of the following deposit requirements pertains to a semiweekly depositor who has accumulated employment taxes of $17,500 on payday, Saturday, May 16, 20--?

A) No deposit is required until May 18, the next banking day.

B) The undeposited taxes should be carried over to the next payday on May 23.

C) The taxes must be deposited on or before Tuesday, May 19.

D) The taxes must be deposited on or before Friday, May 22.

E) None of the above.

A) No deposit is required until May 18, the next banking day.

B) The undeposited taxes should be carried over to the next payday on May 23.

C) The taxes must be deposited on or before Tuesday, May 19.

D) The taxes must be deposited on or before Friday, May 22.

E) None of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

51

If an employer fails to file an employment tax return on the due date, a penalty based on a certain percentage of the amount of tax required to be reported may be added to the tax.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

52

The FICA tax rates for the self-employed are:

A) 6.2% (OASDI) and 1.45% (HI).

B) 12.4% (OASDI) and 1.45% (HI).

C) 6.2% (OASDI) and 2.9% (HI).

D) 10.0% (OASDI) and 1.0% (HI).

E) none of the above.

A) 6.2% (OASDI) and 1.45% (HI).

B) 12.4% (OASDI) and 1.45% (HI).

C) 6.2% (OASDI) and 2.9% (HI).

D) 10.0% (OASDI) and 1.0% (HI).

E) none of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

53

The taxes imposed under the Social Security Act consist of:

A) two taxes on employers.

B) two taxes on employees.

C) OASDI and HI taxes.

D) taxes on the net earnings of the self-employed.

E) all of the above.

A) two taxes on employers.

B) two taxes on employees.

C) OASDI and HI taxes.

D) taxes on the net earnings of the self-employed.

E) all of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

54

Ashe, an employer, has made timely deposits of FICA taxes and withheld income taxes during the first quarter of 20--. The latest date on which Ashe may file Form 941 (without incurring penalty) is:

A) April 10.

B) April 30.

C) May 1.

D) May 10.

E) May 15.

A) April 10.

B) April 30.

C) May 1.

D) May 10.

E) May 15.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

55

Barr fails to make a timely deposit of FICA taxes and withheld income taxes until five days after the due date. The penalty facing Barr is:

A) 2% of the undeposited taxes.

B) 5% of the undeposited taxes.

C) 10% of the undeposited taxes.

D) 25% of the undeposited taxes.

E) none of the above.

A) 2% of the undeposited taxes.

B) 5% of the undeposited taxes.

C) 10% of the undeposited taxes.

D) 25% of the undeposited taxes.

E) none of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

56

Which of the following payments are not taxable for FICA?

A) Back-pay awards.

B) Wage supplements to cover difference between employees' salaries and their military pay.

C) Severance pay.

D) Difference between employees' regular wages and the amount received for jury duty.

E) Retroactive wage increase.

A) Back-pay awards.

B) Wage supplements to cover difference between employees' salaries and their military pay.

C) Severance pay.

D) Difference between employees' regular wages and the amount received for jury duty.

E) Retroactive wage increase.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

57

FICA defines all of the following as wages except :

A) year-end bonuses.

B) standby payments.

C) total cash tips of $15 received by a tipped employee in May.

D) employees' social security taxes paid for by the employer.

E) first six months of sick pay.

A) year-end bonuses.

B) standby payments.

C) total cash tips of $15 received by a tipped employee in May.

D) employees' social security taxes paid for by the employer.

E) first six months of sick pay.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

58

Employers file Form 941 with the IRS center of the region in which the employer's principal place of business is located.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

59

FICA defines all of the following as employees except :

A) vice presidents.

B) partners.

C) superintendents.

D) full-time life insurance salespersons.

E) payroll managers.

A) vice presidents.

B) partners.

C) superintendents.

D) full-time life insurance salespersons.

E) payroll managers.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following deposit requirements pertains to a nonagricultural employer who has employer FICA taxes and withheld employee FICA taxes and income taxes of $125,000 at the end of payday on Friday, August 14, 20--?

A) No deposit is required until Tuesday, August 18.

B) The taxes must be deposited by the close of the next banking day.

C) The taxes must be deposited on or before August 31.

D) The undeposited taxes should be carried over to the end of September.

E) None of the above.

A) No deposit is required until Tuesday, August 18.

B) The taxes must be deposited by the close of the next banking day.

C) The taxes must be deposited on or before August 31.

D) The undeposited taxes should be carried over to the end of September.

E) None of the above.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

61

Employees and independent contractors pay different FICA tax rates.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

62

Instruction 3-1

Use the following tax rates, ceiling and maximum taxes:

Employee and Employer OASDI: 6.20% $132,900 $8,239.80

Employee* and Employer HI: 1.45% No limit No maximum

Self-employed OASDI: 12.4% $132,900 $16,479.60

Self-employed HI: 2.9% No limit No maximum

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Ralston is the sole proprietor of Cut & Curl. During the year, his net earnings were $79,700. What are his self-employment taxes (OASDI and HI) on these earnings?

Use the following tax rates, ceiling and maximum taxes:

Employee and Employer OASDI: 6.20% $132,900 $8,239.80

Employee* and Employer HI: 1.45% No limit No maximum

Self-employed OASDI: 12.4% $132,900 $16,479.60

Self-employed HI: 2.9% No limit No maximum

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Ralston is the sole proprietor of Cut & Curl. During the year, his net earnings were $79,700. What are his self-employment taxes (OASDI and HI) on these earnings?

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

63

Instruction 3-1 *Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Dee is paid $2,345 on November 8, 20--. Dee had cumulative gross earnings, including overtime pay, of $131,600 prior to this pay.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed. Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Dee is paid $2,345 on November 8, 20--. Dee had cumulative gross earnings, including overtime pay, of $131,600 prior to this pay.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

64

Lidge Company of Texas (TX) is classified as a monthly depositor and pays its employees monthly. The following payroll information is for the second quarter of 20--.

The number of employees on June 12, 20-- was 11.

a. Complete the following portion of Form 941.

Source: Internal Revenue Service

b. Complete the following portion of Form 941.

Source: Internal Revenue Service

c. Complete Part 2 of Form 941.

Source: Internal Revenue Service

d. What are the payment due dates of each of the monthly liabilities assuming all

deposits were made on time, and the due date of the filing of Form 941 (year 20--)?

The number of employees on June 12, 20-- was 11.

a. Complete the following portion of Form 941.

Source: Internal Revenue Service

b. Complete the following portion of Form 941.

Source: Internal Revenue Service

c. Complete Part 2 of Form 941.

Source: Internal Revenue Service

d. What are the payment due dates of each of the monthly liabilities assuming all

deposits were made on time, and the due date of the filing of Form 941 (year 20--)?

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

65

If on any day during a deposit period an employer has accumulated $100,000 or more in undeposited employment taxes, the taxes must be deposited on the next banking day.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

66

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . In this pay, Moss Company deducted OASDI taxes of $5,276.24 and HI taxes of $1,233.95 from the $85,100.90 of taxable wages paid. What is Moss Company's portion of the social security taxes for:

a) OASDI

b) HI

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . In this pay, Moss Company deducted OASDI taxes of $5,276.24 and HI taxes of $1,233.95 from the $85,100.90 of taxable wages paid. What is Moss Company's portion of the social security taxes for:

a) OASDI

b) HI

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

67

Instruction 3-1 *Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Jax Company's (a monthly depositor) tax liability (amount withheld from employees' wages for federal income tax and FICA tax plus the company's portion of the FICA tax) for July was $1,210.

No deposit was made by the company until August 24, 20-- (9 days late). Determine:

a) The date by which the deposit should have been made

b) The penalty for failure to make timely deposit

c) The penalty for failure to fully pay tax when due

d) The interest on taxes due and unpaid (assume a 5% interest rate)

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed. Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Jax Company's (a monthly depositor) tax liability (amount withheld from employees' wages for federal income tax and FICA tax plus the company's portion of the FICA tax) for July was $1,210.

No deposit was made by the company until August 24, 20-- (9 days late). Determine:

a) The date by which the deposit should have been made

b) The penalty for failure to make timely deposit

c) The penalty for failure to fully pay tax when due

d) The interest on taxes due and unpaid (assume a 5% interest rate)

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

68

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On August 1, Huff (part-time waitress) reported on Form 4070 the cash tips of $158.50 that she received in July. During August, Huff was paid wages of $550 by her employer. Determine:

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On August 1, Huff (part-time waitress) reported on Form 4070 the cash tips of $158.50 that she received in July. During August, Huff was paid wages of $550 by her employer. Determine:

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

69

Employer contributions for retirement plan payments for employees are defined as wages and are thus subject to FICA taxes.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

70

Under FICA, each partner in a partnership is defined as an employee of that organization.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

71

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Eager, a tipped employee, reported to his employer that he had received $320 in tips during March. On the next payday, April 6, he was paid his regular salary of $400.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Eager, a tipped employee, reported to his employer that he had received $320 in tips during March. On the next payday, April 6, he was paid his regular salary of $400.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

72

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On the last weekly pay of the first quarter, Lorenz is paid her current pay of $90 per day for four days worked and one day sick pay (total-$450). She is also paid her first quarter commission of $1,200 in this pay. How much will be deducted for:

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . On the last weekly pay of the first quarter, Lorenz is paid her current pay of $90 per day for four days worked and one day sick pay (total-$450). She is also paid her first quarter commission of $1,200 in this pay. How much will be deducted for:

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

73

Part-time employees pay a FICA tax at half the tax rate of full-time employees.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

74

Instruction 3-1

Use the following tax rates, ceiling and maximum taxes:

Employee and Employer OASDI: 6.20% $132,900 $8,239.80

Employee* and Employer HI: 1.45% No limit No maximum

Self-employed OASDI: 12.4% $132,900 $16,479.60

Self-employed HI: 2.9% No limit No maximum

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Beginning with the first pay of the year, Carson will make $2,700 each week. In which numbered pay of the year will Carson hit the OASDI taxable limit?

Use the following tax rates, ceiling and maximum taxes:

Employee and Employer OASDI: 6.20% $132,900 $8,239.80

Employee* and Employer HI: 1.45% No limit No maximum

Self-employed OASDI: 12.4% $132,900 $16,479.60

Self-employed HI: 2.9% No limit No maximum

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Beginning with the first pay of the year, Carson will make $2,700 each week. In which numbered pay of the year will Carson hit the OASDI taxable limit?

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

75

Once a person reaches the age of 65, social security taxes are not taken out of his or her paycheck.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

76

Year-end bonuses paid to employees are not subject to the hospital insurance (HI) part of the FICA tax.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

77

Instruction 3-1

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Crow earned $585.15 during the week ended March 1, 20--. Prior to payday, Crow had cumulative gross earnings of $4,733.20.

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Crow earned $585.15 during the week ended March 1, 20--. Prior to payday, Crow had cumulative gross earnings of $4,733.20.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

78

A child working for his father's corporation is not exempt from coverage under FICA.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

79

Under FICA, employers must collect the employee's FICA taxes on tips reported by each employee.

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

80

Instruction 3-1

Use the following tax rates, ceiling and maximum taxes:

Employee and Employer OASDI: 6.20% $132,900 $8,239.80

Employee* and Employer HI: 1.45% No limit No maximum

Self-employed OASDI: 12.4% $132,900 $16,479.60

Self-employed HI: 2.9% No limit No maximum

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Fess receives wages totaling $75,700 and has net earnings from self-employment amounting to $61,300. In determining her taxable self-employment income for the OASDI tax, how much of her net self-employment earnings must Fess count?

Use the following tax rates, ceiling and maximum taxes:

Employee and Employer OASDI: 6.20% $132,900 $8,239.80

Employee* and Employer HI: 1.45% No limit No maximum

Self-employed OASDI: 12.4% $132,900 $16,479.60

Self-employed HI: 2.9% No limit No maximum

*Employee HI: Plus an additional 0.9% on wages over $200,000. Also applicable to self-employed.

Rounding Rules: Unless instructed otherwise compute hourly rate and overtime rates as follows:

1. Carry the hourly rate and the overtime rate to 3 decimal places and then round off to 2 decimals places (round the hourly rate to 2 decimal places

before multiplying by one and one-half to determine the overtime rate).

2. If the third decimal place is 5 or more, round to the next higher cent.

3. If the third decimal place is less than 5, drop the third decimal place.

Also, use the minimum hourly wage of $7.25 in solving these problems and all that follow.

Refer to Instruction 3-1 . Fess receives wages totaling $75,700 and has net earnings from self-employment amounting to $61,300. In determining her taxable self-employment income for the OASDI tax, how much of her net self-employment earnings must Fess count?

Unlock Deck

Unlock for access to all 94 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 94 flashcards in this deck.