Deck 1: Certified Regulatory Compliance Manager

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

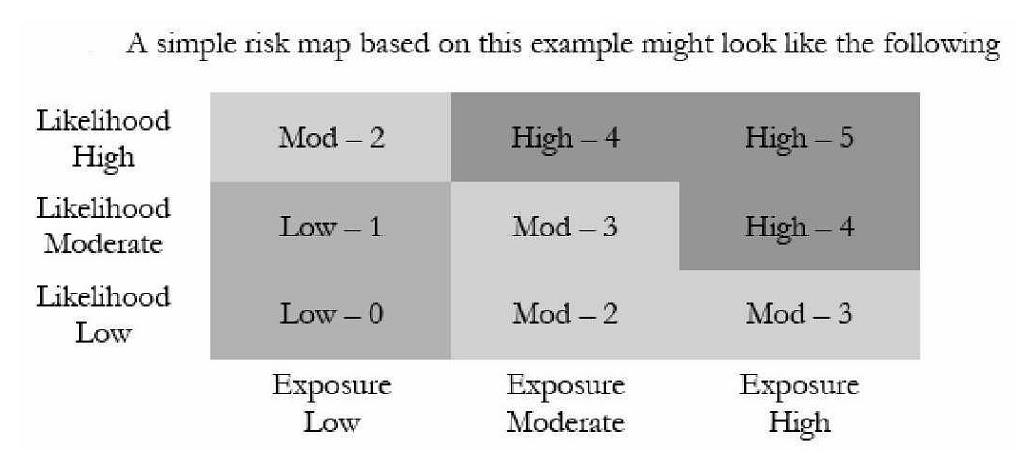

For example on a 0-5 scale:  The risk trend shows the direction of risk and probable change to risk over the next 12 months. A trend toward increasing risk means that

The risk trend shows the direction of risk and probable change to risk over the next 12 months. A trend toward increasing risk means that

A) Management may want to take additional action through more controls or increased reviews

B) Risk may prompt a decrease in controls and improved efficiencies

C) Controls currently in place are appropriate to succeed in keeping risks within management's established risk-tolerance level

D) Risk measurements exceed management's tolerance for risk

The risk trend shows the direction of risk and probable change to risk over the next 12 months. A trend toward increasing risk means thatA) Management may want to take additional action through more controls or increased reviews

B) Risk may prompt a decrease in controls and improved efficiencies

C) Controls currently in place are appropriate to succeed in keeping risks within management's established risk-tolerance level

D) Risk measurements exceed management's tolerance for risk

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/418

Play

Full screen (f)

Deck 1: Certified Regulatory Compliance Manager

1

Subprime borrowers are those with weakened credit histories or reduced repayment capacity. Loans to these borrowers historically have had a higher delinquency rate. Many lenders have expanded their lending programs and added subprime products as a method of meeting their _______________ by providing greater credit access to lower-income consumers.

A) Community Reinvestment Act (CRA) responsibilities

B) Fraudulent marketing tactics

C) FTC Act

D) Predatory Lending

A) Community Reinvestment Act (CRA) responsibilities

B) Fraudulent marketing tactics

C) FTC Act

D) Predatory Lending

A

2

In Compliance regulation and risk assessment key performance indicators usually include:

A) Fines or penalties

B) Customer complaints

C) Regulatory criticism from a regulator or internal or external auditors

D) None of these

A) Fines or penalties

B) Customer complaints

C) Regulatory criticism from a regulator or internal or external auditors

D) None of these

A,B,C

3

Compliance professionals have a duty to keep senior management and the board apprised of the state of compliance within the bank through which of the following:

A) Self-monitoring and audit results

B) Proactive compliance controls

C) Timely and accurate regulatory reporting

D) All of the options mentioned above

A) Self-monitoring and audit results

B) Proactive compliance controls

C) Timely and accurate regulatory reporting

D) All of the options mentioned above

D

4

There is no established template for documenting compliance risk. Each institution should develop a risk assessment that fits its risk profile. The components that are commonly used throughout the industry are as follows EXCEPT:

A) Risk assessment

B) Measuring key risk indicators

C) Identifying key performance indicators

D) Training the leadership of compliance regulation program

A) Risk assessment

B) Measuring key risk indicators

C) Identifying key performance indicators

D) Training the leadership of compliance regulation program

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

5

______________ should include basic elements designed to understand and mitigate risk. It usually includes: Written program Compliance-related policies and procedures

A) Tactical Compliance procedure

B) Rank solution

C) Compliance program

D) None of these

A) Tactical Compliance procedure

B) Rank solution

C) Compliance program

D) None of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

6

A compliance professional's responsibilities include all of the following EXCEPT:

A) Understanding the business units operating environment and risk tolerance

B) Performing risk assessments with the assistance of business units to determine current risk levels and risks associated with the bank's products, lines of business, customers, and locations, among other factors

C) Working with business units to ensure prompt corrective action for any detected errors

D) Assisting business lines with compliance training for employees, as needed

A) Understanding the business units operating environment and risk tolerance

B) Performing risk assessments with the assistance of business units to determine current risk levels and risks associated with the bank's products, lines of business, customers, and locations, among other factors

C) Working with business units to ensure prompt corrective action for any detected errors

D) Assisting business lines with compliance training for employees, as needed

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

7

In a compliance program, tactical compliance procedures should be integrated into business line procedures, such as how to deliver an Adverse Action Notice when an application is declined. In this case:

A) Regulations should be applied consistently to procedures throughout the bank

B) Revisions to procedures should be based on compliance expertise and not mere editing

C) Providing solutions to mitigate any identified risk

D) Assisting business units in developing or revising policies and procedures to reflect current regulatory requirements

A) Regulations should be applied consistently to procedures throughout the bank

B) Revisions to procedures should be based on compliance expertise and not mere editing

C) Providing solutions to mitigate any identified risk

D) Assisting business units in developing or revising policies and procedures to reflect current regulatory requirements

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

8

Which one of the following is out of the FIRREA penalties included in the enforcement section of Adjusted Mortgage Regulation (12 CFR 34)?

A) Penalties up to $7,500 per day for violations of laws and regulations

B) Penalties up to $47,500 per day if violations or unsafe or unsound practices are engaged in recklessly or are part of a pattern of misconduct that causes more than a minimal loss to the bank or any pecuniary gain to the parties involved

C) Penalties up to $1,375,000 per day against persons who knowingly commit a violation and knowingly or recklessly cause a substantial loss to the bank or a substantial benefit to the party

D) Penalties up to $6,500 per day for violations of laws and regulations

A) Penalties up to $7,500 per day for violations of laws and regulations

B) Penalties up to $47,500 per day if violations or unsafe or unsound practices are engaged in recklessly or are part of a pattern of misconduct that causes more than a minimal loss to the bank or any pecuniary gain to the parties involved

C) Penalties up to $1,375,000 per day against persons who knowingly commit a violation and knowingly or recklessly cause a substantial loss to the bank or a substantial benefit to the party

D) Penalties up to $6,500 per day for violations of laws and regulations

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

9

Under Interagency Guidance on Subprime Lending (1999) lending policy must:

A) Be appropriate to the size and complexity of the operation

B) Address the types of products offers and those not authorized

C) Require credit file documentation

D) All of these

A) Be appropriate to the size and complexity of the operation

B) Address the types of products offers and those not authorized

C) Require credit file documentation

D) All of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

10

The purpose of guidelines for National Banks to Guard against Predatory and Abusive Lending Practices- AL-2003-2 includes all of the following EXCEPT:

A) Provide examples to national banks of practices that may be abusive

B) Advise banks on how they should avoid abusive practices

C) Banks should consider appropriate discount rates, credit loss rates, and prepayment rates when valuing these assets

D) Show how some abusive lending can involve unfair or deceptive practices and therefore violate the Federal Trade Commission Act

A) Provide examples to national banks of practices that may be abusive

B) Advise banks on how they should avoid abusive practices

C) Banks should consider appropriate discount rates, credit loss rates, and prepayment rates when valuing these assets

D) Show how some abusive lending can involve unfair or deceptive practices and therefore violate the Federal Trade Commission Act

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

11

To be effective, compliance risk management professionals must design a framework to ensure that bank management understands the risks and the steps that must be taken to mitigate them. The many roles compliance professionals fill incorporate risk management aspects including:

A) Coordinating regulatory exams to explain risks to examiners

B) Overseeing compliance training targeting higher risk areas

C) Tracking regulatory proposals and final rules to understand new risks

D) All of these

A) Coordinating regulatory exams to explain risks to examiners

B) Overseeing compliance training targeting higher risk areas

C) Tracking regulatory proposals and final rules to understand new risks

D) All of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

12

The compliance program should address plans to verify adherence to applicable regulations through:

A) Ongoing monitoring to evaluate the program, self monitoring and corrective action

B) Self monitoring

C) Periodic reviews

D) Ongoing monitoring to evaluate the program, self monitoring and periodic reviews

A) Ongoing monitoring to evaluate the program, self monitoring and corrective action

B) Self monitoring

C) Periodic reviews

D) Ongoing monitoring to evaluate the program, self monitoring and periodic reviews

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

13

In the mid-1980s a movement began among the federal supervisory agencies to produce a uniform ARM regulation. In 1988, the Federal Reserve Board added the uniform ARM disclosure requirements to a regulation. Therefore, most of the original OCC ARM consumer protection requirements are now found in this new regulation. Adjustable rate mortgage loans made by national banks may be subject to the OCC's ARM regulation or the requirements of this new regulation, or both. This new regulation is:

A) Regulation Z

B) Truth in Lending

C) CFR 34.21, 34.22 and 34.23

D) FIRREA penalty

A) Regulation Z

B) Truth in Lending

C) CFR 34.21, 34.22 and 34.23

D) FIRREA penalty

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

14

They also embrace the concept of risk-based compliance management. They expect compliance management to be tailored to the bank, be it large or small, offering standard or specialty financial services, simple or complex products lines, and adjusted as appropriate for the customer base as that issued for the Bank Secrecy Act, also establishes their expectations that a bank's program be risk based. Who are they?

A) Outsourcing firms

B) Foreign financial service providers

C) Bank regulatory agencies

D) Risk management organizations

A) Outsourcing firms

B) Foreign financial service providers

C) Bank regulatory agencies

D) Risk management organizations

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

15

For example on a 0-5 scale: The risk trend shows the direction of risk and probable change to risk over the next 12 months. A trend toward increasing risk means that

A) Management may want to take additional action through more controls or increased reviews

B) Risk may prompt a decrease in controls and improved efficiencies

C) Controls currently in place are appropriate to succeed in keeping risks within management's established risk-tolerance level

D) Risk measurements exceed management's tolerance for risk

The risk trend shows the direction of risk and probable change to risk over the next 12 months. A trend toward increasing risk means thatA) Management may want to take additional action through more controls or increased reviews

B) Risk may prompt a decrease in controls and improved efficiencies

C) Controls currently in place are appropriate to succeed in keeping risks within management's established risk-tolerance level

D) Risk measurements exceed management's tolerance for risk

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following should be done during research and interpreting regulations Compliance professionals in mitigating compliance risk?

A) Track regulatory proposals

B) Implementing final regulatory rules

C) Understanding the business units' operating environment and risk tolerance

D) Ranking solutions as high, moderate and low risk

A) Track regulatory proposals

B) Implementing final regulatory rules

C) Understanding the business units' operating environment and risk tolerance

D) Ranking solutions as high, moderate and low risk

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

17

In Requirements section of Adjusted Mortgage Regulation (12 CFR 34), for loans subject to both the OCC ARM regulation and to Regulation Z, 12 CFR 226.19(b)-that is, loans made to an individual, for personal purposes, secured by the borrower's principal dwelling, and having a term longer than one year- the index to which the interest rate is tied must be:

A) Specified in loan documents

B) Readily available to and verifiable by the browser

C) Multiple values of a chosen measure or a moving average of the chosen measure calculated over a specified period

D) A and B only

A) Specified in loan documents

B) Readily available to and verifiable by the browser

C) Multiple values of a chosen measure or a moving average of the chosen measure calculated over a specified period

D) A and B only

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

18

After a compliance officer develops a base of knowledge of regulations, he or she must begin the art of applying regulations in a risk management environment. Which of the following is NOT out of a few things to be kept in mind when determining what to do FIRST?

A) Think practically about your role as an advisor. Involve the business units in the decision process rather than making decisions for them

B) Calculate the institution's consolidated risk profile

C) Make sure you understand the level of risk the bank will tolerate, so decisions do not exceed this limit

D) Add value by analyzing regulatory requirements for the business units before you present proposed or final rules or solutions

A) Think practically about your role as an advisor. Involve the business units in the decision process rather than making decisions for them

B) Calculate the institution's consolidated risk profile

C) Make sure you understand the level of risk the bank will tolerate, so decisions do not exceed this limit

D) Add value by analyzing regulatory requirements for the business units before you present proposed or final rules or solutions

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

19

The banking agencies issued two guidances to caution depository institutions about risks involved in funding non-depository lenders that engage in predatory lending. Predatory and abusive practices include:

A) High-pressure sales

B) Excessive fees and interest rate including fees for unnecessary products

C) Balloon payments that may never cause foreclosures

D) Excessive refinancing with fees included in the new loan

A) High-pressure sales

B) Excessive fees and interest rate including fees for unnecessary products

C) Balloon payments that may never cause foreclosures

D) Excessive refinancing with fees included in the new loan

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following usually comes under the heading of abusive lending?

A) Abusive lending usually is defined by a variety of lending practices

B) It is the excessive and hidden fees in the amount financed

C) A fundamental characteristic is aggressive marketing of credit to prospective borrowers who cannot repay it on the terms offered

D) Typically, such loans are underwritten on the liquidation value of the collateral rather than the creditworthiness of the borrower

A) Abusive lending usually is defined by a variety of lending practices

B) It is the excessive and hidden fees in the amount financed

C) A fundamental characteristic is aggressive marketing of credit to prospective borrowers who cannot repay it on the terms offered

D) Typically, such loans are underwritten on the liquidation value of the collateral rather than the creditworthiness of the borrower

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

21

The act limited balloon payments in consumer leases and enabled consumers to compare lease terms with credit terms where appropriate. The act was implemented by Regulation M (Consumer Leasing). It requires disclosures to consumers before consummation of the lease agreement. This act is:

A) Consumer leasing act

B) Risk disclosure act

C) ALLL

D) None of these

A) Consumer leasing act

B) Risk disclosure act

C) ALLL

D) None of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

22

Which one of the following should be included in an early termination notice in case of the termination from consumer leasing agreement?

A) A warning to the consumer that a substantial charge may result from early termination (required only in a motor vehicle lease)

B) A statement of the conditions under which the lessee or lessor may terminate the lease prior to the end of the lease term

C) The purchase option at the end of the lease term

D) The amount of any penalty or other charge for early termination (the penalty must be reasonable)

A) A warning to the consumer that a substantial charge may result from early termination (required only in a motor vehicle lease)

B) A statement of the conditions under which the lessee or lessor may terminate the lease prior to the end of the lease term

C) The purchase option at the end of the lease term

D) The amount of any penalty or other charge for early termination (the penalty must be reasonable)

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

23

Content of segregated disclosures in Consumer Leasing Act include all of the following EXCEPT:

A) Amount due at lease signing or delivery, itemized by type and amount, including: Refundable security deposit Advance monthly or other periodic payment Capitalized cost reduction An itemization of how the amount due will be paid, by type and amount (only required in a motor vehicle lease), using the model form

B) Number, amount, and due date of payments scheduled and the total amount of periodic payments

C) In an open-end lease, the descriptive statement "You will owe an additional amount if the actual value of the vehicle is less than the residual value"

D) If there are multiple items of property, the property description may be separate

A) Amount due at lease signing or delivery, itemized by type and amount, including: Refundable security deposit Advance monthly or other periodic payment Capitalized cost reduction An itemization of how the amount due will be paid, by type and amount (only required in a motor vehicle lease), using the model form

B) Number, amount, and due date of payments scheduled and the total amount of periodic payments

C) In an open-end lease, the descriptive statement "You will owe an additional amount if the actual value of the vehicle is less than the residual value"

D) If there are multiple items of property, the property description may be separate

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

24

If the institution offers both full and reduced documentation loans and there is a pricing premium attached to the reduced documentation loan, the consumer should:

A) Be alerted to this fact

B) Not be alerted to this fact

C) Provide consumers with a clear statement of the options available

D) Not lead consumers with payment option ARMs to choose a non-amortizing or negatively amortizing payment

A) Be alerted to this fact

B) Not be alerted to this fact

C) Provide consumers with a clear statement of the options available

D) Not lead consumers with payment option ARMs to choose a non-amortizing or negatively amortizing payment

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

25

Compliance issues related to payday lending are all of the following EXCEPT:

A) Payday lending may adversely affect a bank's CRA rating. Any illegal or questionable practices will negatively affect a bank's CRA performance. A payday lending program may be inconsistent with helping to meet the community's credit needs

B) The bank (or its third-party partner) must properly disclose all finance charges and fees to payday lending customers. Advertisements of the program are also subject to Truth-in-Lending requirements

C) Adverse action disclosures must be provided to applicants of payday loans that are denied if a consumer report (including check tracking services) was used in the credit decision

D) The bank may be subject to the FOC's unfair or deceptive practices rules.

A) Payday lending may adversely affect a bank's CRA rating. Any illegal or questionable practices will negatively affect a bank's CRA performance. A payday lending program may be inconsistent with helping to meet the community's credit needs

B) The bank (or its third-party partner) must properly disclose all finance charges and fees to payday lending customers. Advertisements of the program are also subject to Truth-in-Lending requirements

C) Adverse action disclosures must be provided to applicants of payday loans that are denied if a consumer report (including check tracking services) was used in the credit decision

D) The bank may be subject to the FOC's unfair or deceptive practices rules.

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

26

Predatory lending practices can adversely affect:

A) A bank's CRA rating

B) Equity shipping

C) Loan quality control reviews

D) Truth in Lending Act

A) A bank's CRA rating

B) Equity shipping

C) Loan quality control reviews

D) Truth in Lending Act

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

27

Banks must maintain an ____________ adequate to absorb estimated credit losses from payday loans. Banks should evaluate the collectability of accrued fees and finance charges on payday loans and ensure that this income is appropriately measured.

A) TILA

B) FCRA

C) ALLL

D) A and B both

A) TILA

B) FCRA

C) ALLL

D) A and B both

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

28

Guidelines for National Banks to Guard against Predatory and Abusive Lending Practices-AL-2003-2 says that refusing to purchase the following types of loans can reduce the possibility of purchasing abusive mortgage loans EXCEPT:

A) Loans in which the lender has not adequately determined the borrower's ability to repay the debt

B) Loans subject to the Home Ownership and Equity Protection Act (HOEPA)

C) Loans with points and fees in excess of 5 percent of the loan amount, except in cases where the higher amount was to prevent the loan from being unprofitable

D) Loans in which a prepaid multiple-premium credit insurance policy was included in the amount financed

A) Loans in which the lender has not adequately determined the borrower's ability to repay the debt

B) Loans subject to the Home Ownership and Equity Protection Act (HOEPA)

C) Loans with points and fees in excess of 5 percent of the loan amount, except in cases where the higher amount was to prevent the loan from being unprofitable

D) Loans in which a prepaid multiple-premium credit insurance policy was included in the amount financed

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

29

Below mentioned is the necessary information that should be included in the ___________. Risk of payment shock-potential payment increases; how the new payment will be calculated when the introductory rate expires Ramifications of prepayment penalties-how they will be calculated, when they will be imposed Ramifications of balloon payments Ramifications of the lack of escrowing for taxes and insurance-who is responsible for paying taxes and insurance and the fact that their costs may be substantial Cost of reduced documentation loans-whether there is a pricing premium required

A) Consumer protection principles

B) Underwriting standards

C) Workout arrangements

D) None of these

A) Consumer protection principles

B) Underwriting standards

C) Workout arrangements

D) None of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

30

In a motor vehicle lease, a mathematical progression showing how the periodic payment is derived, containing the following information:

A) Gross capitalized cost (including the agreed-on value of the vehicle)

B) Rent charge (the difference between the total of base payment over the lease term minus the depreciation and any amortized amounts)

C) Itemization of other charges that are part of the periodic payment

D) All of the above

A) Gross capitalized cost (including the agreed-on value of the vehicle)

B) Rent charge (the difference between the total of base payment over the lease term minus the depreciation and any amortized amounts)

C) Itemization of other charges that are part of the periodic payment

D) All of the above

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

31

In Guidance on Nontraditional Mortgage Product Risks, if the institution has a concentration in a nontraditional mortgage portfolio, the institution should:

A) Have well-developed monitoring systems and risk management practices

B) Monitor by originator and key borrower and portfolio characteristics

C) Not understand the risk of payment shock and negative amortization

D) A and B

A) Have well-developed monitoring systems and risk management practices

B) Monitor by originator and key borrower and portfolio characteristics

C) Not understand the risk of payment shock and negative amortization

D) A and B

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

32

The purpose of advisory letter in Avoiding Predatory and Abusive Lending Practices in Brokered and Purchased Loans- AL-2003-3 is to:

A) Adopt sound credit underwriting policies

B) Alert national banks to the risks they take if they make loans through brokers or purchase loans that contain or reflect abusive or predatory terms or practices

C) Adopt policies that address the circumstances under which the bank would make loans that have features associated with abusive lending practices

D) Make loans secured by the consumer's home but with high, up-front fees that are financed and secured by the home

A) Adopt sound credit underwriting policies

B) Alert national banks to the risks they take if they make loans through brokers or purchase loans that contain or reflect abusive or predatory terms or practices

C) Adopt policies that address the circumstances under which the bank would make loans that have features associated with abusive lending practices

D) Make loans secured by the consumer's home but with high, up-front fees that are financed and secured by the home

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

33

Underwriting standards in Subprime Mortgage Lending include:

A) The borrower's debt-to-income ratio should include the borrower's total yearly housing-related payments as a percentage of gross monthly income

B) Institutions should have a clear policy governing the use of risk-layering features, such as reduced documentation loans or simultaneous second lien mortgages

C) Stated income and reduced documentation loans to subprime borrowers should be made only if there are clear, documented mitigating factors

D) Mitigating factors should be present when risk layering features are combined in order to support the underwriting decision and the borrower's repayment capacity

A) The borrower's debt-to-income ratio should include the borrower's total yearly housing-related payments as a percentage of gross monthly income

B) Institutions should have a clear policy governing the use of risk-layering features, such as reduced documentation loans or simultaneous second lien mortgages

C) Stated income and reduced documentation loans to subprime borrowers should be made only if there are clear, documented mitigating factors

D) Mitigating factors should be present when risk layering features are combined in order to support the underwriting decision and the borrower's repayment capacity

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

34

Supervisory review should also be the part of Subprime Mortgage Lending. It should review:

A) Regulatory agencies will continue to focus on risk management review and consumer compliance processes

B) Hiring and Training of personnel

C) Agencies will continue to take action against institutions that violate consumer protection laws or fair lending laws or that engages in unfair or deceptive acts or practices or in unsafe or unsound lending practices

D) Applicability of prepayment penalties

A) Regulatory agencies will continue to focus on risk management review and consumer compliance processes

B) Hiring and Training of personnel

C) Agencies will continue to take action against institutions that violate consumer protection laws or fair lending laws or that engages in unfair or deceptive acts or practices or in unsafe or unsound lending practices

D) Applicability of prepayment penalties

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

35

Below mentioned list shows the significant risks of _______________. Borrowers with cash-flow difficulties Borrowers with no lower-cost credit alternatives Minimal analysis of borrower's ability to repay the loan Minimal review of borrower's credit history Credit is usually unsecured

A) Payday lending

B) Loan flipping

C) Equity stripping

D) None of these

A) Payday lending

B) Loan flipping

C) Equity stripping

D) None of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

36

Examples of unfair practices mentioned in guidelines against Predatory and Abusive Lending includes loan flipping and loan equity stripping. It is said that:

A) Loan flipping may be unfair because it increases the chances of foreclosure by decreasing home equity and increasing debt burden

B) Equity stripping is the practice of making loans secured by the consumer's home but with high, up-front fees that are financed and secured by the home

C) Loan flipping is the practice of making loans secured by the consumer's home but with high, up-front fees that are financed and secured by the home

D) Equity stripping may be unfair because it increases the chances of foreclosure by decreasing home equity and increasing debt burden

A) Loan flipping may be unfair because it increases the chances of foreclosure by decreasing home equity and increasing debt burden

B) Equity stripping is the practice of making loans secured by the consumer's home but with high, up-front fees that are financed and secured by the home

C) Loan flipping is the practice of making loans secured by the consumer's home but with high, up-front fees that are financed and secured by the home

D) Equity stripping may be unfair because it increases the chances of foreclosure by decreasing home equity and increasing debt burden

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

37

______________ is frequent refinancing that do not benefit the borrower. This practice can result in borrower injury from the fees imposed and from the fact that it decreases home equity and increases the consumer's debt burden, thus increasing the chance of foreclosure.

A) Loan flipping

B) Loan refinancing

C) Securitization

D) Subprime loans

A) Loan flipping

B) Loan refinancing

C) Securitization

D) Subprime loans

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

38

Safety and soundness concerns in FDIC Payday Lending Guidance clearly mention that there should be adequate capital as Minimum capital requirements are not enough to offset the risks of payday loans. Banks should hold capital against its subprime portfolio in amounts:

A) That are 1½ to 5 times greater than normal

B) That are 1½ to 3 times greater than normal

C) That are 1½ to 3 times lower than normal

D) That should be between 2-5 in comparison to normal

A) That are 1½ to 5 times greater than normal

B) That are 1½ to 3 times greater than normal

C) That are 1½ to 3 times lower than normal

D) That should be between 2-5 in comparison to normal

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

39

Institutions that offer nontraditional mortgage products should make sure they comply with the following, as applicable, EXCEPT:

A) Truth in Lending Act

B) FTC Act (i.e., Unfair and Deceptive Acts and Practices)

C) RESTA

D) State laws prohibiting deceptive trade practices

A) Truth in Lending Act

B) FTC Act (i.e., Unfair and Deceptive Acts and Practices)

C) RESTA

D) State laws prohibiting deceptive trade practices

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

40

Which of the following are recommended practices in Avoiding Predatory and Abusive Lending Practices in Brokered and Purchased Loans-AL-2003-3?

A) Have written agreements with third-party brokers that specifically and clearly address the rights and responsibilities of each party. Written agreements should 1. Ensure that no inappropriate compensation exists 2. Provide for indemnification to the bank 3. Enable banks to exit the arrangement through a termination procedure 4. Provide for the bank's and the OCC's ability to access all records of the third party and to audit the third party's operations

B) Verify that brokers and originators have established policies to ensure that loans will comply with all applicable laws

C) Establish an effective management information system to monitor the performance of third-party brokers and originators

D) All of the above

A) Have written agreements with third-party brokers that specifically and clearly address the rights and responsibilities of each party. Written agreements should 1. Ensure that no inappropriate compensation exists 2. Provide for indemnification to the bank 3. Enable banks to exit the arrangement through a termination procedure 4. Provide for the bank's and the OCC's ability to access all records of the third party and to audit the third party's operations

B) Verify that brokers and originators have established policies to ensure that loans will comply with all applicable laws

C) Establish an effective management information system to monitor the performance of third-party brokers and originators

D) All of the above

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

41

Practice/s addressed in the guidance of OCC advisory on credit card practices-AL-2004- 10 is/are:

A) "Up-to" marketing

B) Promotional rate marketing

C) Repricing of accounts and other changes in credit terms

D) Lending to insiders

A) "Up-to" marketing

B) Promotional rate marketing

C) Repricing of accounts and other changes in credit terms

D) Lending to insiders

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

42

OCC advisory on credit card practice-AL-2004-10 in credit card practices covers:

A) Finance and credit management practices that may be unfair or deceptive and expose a bank to compliance and reputation risk

B) Marketing and account management practices that may be unfair or deceptive and expose a bank to compliance and reputation risk

C) Marketing and account management practices

D) Marketing and account management practices that may be fair and can't expose a bank to compliance and reputation risk

A) Finance and credit management practices that may be unfair or deceptive and expose a bank to compliance and reputation risk

B) Marketing and account management practices that may be unfair or deceptive and expose a bank to compliance and reputation risk

C) Marketing and account management practices

D) Marketing and account management practices that may be fair and can't expose a bank to compliance and reputation risk

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

43

Under Consumer Leasing Act Enforcement-15 USC 1667d section FIRREA penalties include:

A) Penalties up to $8,500 per day for violations of laws and regulations

B) Penalties up to $37,500 per day if violations or unsafe or unsound practices are engaged in recklessly or are part of a pattern of misconduct that causes more than a minimal loss to the bank or any pecuniary gain to the parties involved

C) Penalties up to $1,375,000 per day against persons who knowingly commit a violation and knowingly or recklessly cause a substantial loss to the bank or a substantial benefit to the party

D) Penalties up to $9,500 per day for violations of laws and regulations

A) Penalties up to $8,500 per day for violations of laws and regulations

B) Penalties up to $37,500 per day if violations or unsafe or unsound practices are engaged in recklessly or are part of a pattern of misconduct that causes more than a minimal loss to the bank or any pecuniary gain to the parties involved

C) Penalties up to $1,375,000 per day against persons who knowingly commit a violation and knowingly or recklessly cause a substantial loss to the bank or a substantial benefit to the party

D) Penalties up to $9,500 per day for violations of laws and regulations

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

44

_____________ requires that a statement of purpose be obtained from borrowers whose loans are to be greater than $100,000 and that will be secured by margin stock. Loans made for the purpose of purchasing margin stock are subject to additional limitations

A) Regulation U

B) Regulation V

C) Regulation Z

D) Regulation X

A) Regulation U

B) Regulation V

C) Regulation Z

D) Regulation X

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

45

Which one of the following types of credit may be extended in Requirements case-12 CFR 221.3, 221.7:

A) Temporary advances in payment against delivery transactions

B) Capital contribution leases

C) Credit to clearing banking authorities

D) Underwriter loans

A) Temporary advances in payment against delivery transactions

B) Capital contribution leases

C) Credit to clearing banking authorities

D) Underwriter loans

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

46

Regulation O both restricts lending to insiders and requires that certain loans to insiders be disclosed. Each banking agency has adopted the provisions of Regulation O for administrative enforcement purposes. These were not found to be useful in preventing insider lending abuse. Regulation O governs which of the following areas major areas:

A) Lending to insiders

B) Disclosures of loans made to insiders

C) Both of these

D) None of these

A) Lending to insiders

B) Disclosures of loans made to insiders

C) Both of these

D) None of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

47

What is actually a Single credit rule-12 CFR 221.3(d)?

A) All purpose credit extended to a customer will be considered to be a single credit for purposes of Regulation U

B) The value of all collateral securing all-purpose loans will be aggregated to determine if it is sufficient

C) If unsecured purpose credit is extended before secured purpose credit, the loans need only be combined for purposes of applying the withdrawal and substitution rules

D) All of the above

A) All purpose credit extended to a customer will be considered to be a single credit for purposes of Regulation U

B) The value of all collateral securing all-purpose loans will be aggregated to determine if it is sufficient

C) If unsecured purpose credit is extended before secured purpose credit, the loans need only be combined for purposes of applying the withdrawal and substitution rules

D) All of the above

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

48

Under collateral requirements-12CFR 221.7, maximum loan value of margin stock is:

A) Currently 50 percent of the current market value

B) Currently 70 percent of the current market value

C) Subject to change by the Federal Reserve

D) Subject to change by the Equity Reserve

A) Currently 50 percent of the current market value

B) Currently 70 percent of the current market value

C) Subject to change by the Federal Reserve

D) Subject to change by the Equity Reserve

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

49

Banks may extend and maintain purpose credit without complying with Regulation U if the credit is extended:

A) To a bank auditor

B) To a qualified employee stock ownership plan running previously but not now

C) To any customer, other than a broker or dealer, to temporarily finance the purchase or sale of securities for prompt delivery, if the credit is to be repaid in the ordinary course of business on the completion of the transaction

D) To enable a customer to meet emergency expenses not reasonably foreseen and if the bank obtains a good faith statement from the customer. Emergency expenses are ones related to unforeseen death or disability, not a chance to make a profit.

A) To a bank auditor

B) To a qualified employee stock ownership plan running previously but not now

C) To any customer, other than a broker or dealer, to temporarily finance the purchase or sale of securities for prompt delivery, if the credit is to be repaid in the ordinary course of business on the completion of the transaction

D) To enable a customer to meet emergency expenses not reasonably foreseen and if the bank obtains a good faith statement from the customer. Emergency expenses are ones related to unforeseen death or disability, not a chance to make a profit.

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

50

The maximum amount of credit that a bank may extend to all of its insiders is known as the ______________and is equal to 100 percent of its unimpaired capital and surplus.

A) Aggregate lending limit

B) Loan filliping

C) Equity stripping

D) Tangible economic benefit

A) Aggregate lending limit

B) Loan filliping

C) Equity stripping

D) Tangible economic benefit

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

51

It is an extension of credit will be deemed to be made to an insider if the proceeds are transferred to the insider or used for the insider's benefit. This rule does not apply if the credit is made on substantially the same terms and conditions as those made to a noninsider and if the proceeds are used in a bona fide transaction involving the acquisition of property, goods, or services from the insider. What is it?

A) Tangible economic benefit rule012 CFR 215.3(f)

B) Extension of credit-12 CFR 215.3

C) Lending restrictions

D) Intangible economic-benefit rule

A) Tangible economic benefit rule012 CFR 215.3(f)

B) Extension of credit-12 CFR 215.3

C) Lending restrictions

D) Intangible economic-benefit rule

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

52

Margin stock includes:

A) Equity securities registered or having delisted trading privileges on a national securities exchange:

B) Over-the-counter (OTC) securities that do not qualify for trading in the National Market System

C) Warrants or rights to subscribe to or purchase a common stock

D) Securities issued by an investment company registered under the Investment Company Act, except for: A company licensed under the Small Business Investment Company Act A company that has at least 95 percent of its assets continuously invested in exempted securities; or A company that issues face-amount certificates; or A company that is considered a money market fund under the SEC Rules

A) Equity securities registered or having delisted trading privileges on a national securities exchange:

B) Over-the-counter (OTC) securities that do not qualify for trading in the National Market System

C) Warrants or rights to subscribe to or purchase a common stock

D) Securities issued by an investment company registered under the Investment Company Act, except for: A company licensed under the Small Business Investment Company Act A company that has at least 95 percent of its assets continuously invested in exempted securities; or A company that issues face-amount certificates; or A company that is considered a money market fund under the SEC Rules

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

53

____________ is any company of which the bank is a subsidiary or any other subsidiary of the same company of which the bank is a subsidiary.

A) Brokerage House

B) Treasury

C) FDIC

D) Affiliates

A) Brokerage House

B) Treasury

C) FDIC

D) Affiliates

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

54

Under Renegotiations, extensions, and assumptions-12 CFR 213.5; any lease that is renegotiated or extended by longer than six months is considered to be a new lease, subject to new disclosure requirements, except when:

A) One or more payments are deferred, whether or not there is a charge for the deferral

B) Lease property is substituted with property of substantially equivalent or greater value, if no other lease terms are changed

C) In a multiple-item lease, property is added, deleted, or substituted provided the average periodic payment does not change by more than 35 percent

D) There is an agreement resulting from a pre-order

A) One or more payments are deferred, whether or not there is a charge for the deferral

B) Lease property is substituted with property of substantially equivalent or greater value, if no other lease terms are changed

C) In a multiple-item lease, property is added, deleted, or substituted provided the average periodic payment does not change by more than 35 percent

D) There is an agreement resulting from a pre-order

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

55

Unless excluded by a board resolution or the bylaws, the following officers will be considered to be executive officers EXCEPT:

A) Chairman of the board

B) President

C) Each vice-president and above (for example, senior vice-president, executive vice-president, and so on)

D) Brokerage house's vice president

A) Chairman of the board

B) President

C) Each vice-president and above (for example, senior vice-president, executive vice-president, and so on)

D) Brokerage house's vice president

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

56

Lending restrictions under requirements 12 CFR 215; 12 CFR 337, 12 CFR 349 are all of the following EXCEPT:

A) Banks may not lend to executive officers, directors, principal shareholders, or any of their related interests unless the credit is made on substantially the same terms and following credit underwriting standards that are not less stringent than those on loans to persons who are not insiders; however, if the bank has a benefit program widely available to its employees, it may lend to insiders on the same terms and conditions as it lends to its other employees, pursuant to its employee benefit program

B) Banks may not lend to any executive officer, director, or principal shareholder, and to any of their related interests, amounts that exceed the higher of $25,000 or 5 percent of the bank's capital and unimpaired surplus (up to a maximum of $500,000) in the aggregate unless The credit is approved in advance by the board of directors The interested party has abstained from voting

C) Prior approval is not needed for each draw against a line of credit provided the line of credit was approved within the preceding 14 months, based on the then-current financial statement

D) None of these

A) Banks may not lend to executive officers, directors, principal shareholders, or any of their related interests unless the credit is made on substantially the same terms and following credit underwriting standards that are not less stringent than those on loans to persons who are not insiders; however, if the bank has a benefit program widely available to its employees, it may lend to insiders on the same terms and conditions as it lends to its other employees, pursuant to its employee benefit program

B) Banks may not lend to any executive officer, director, or principal shareholder, and to any of their related interests, amounts that exceed the higher of $25,000 or 5 percent of the bank's capital and unimpaired surplus (up to a maximum of $500,000) in the aggregate unless The credit is approved in advance by the board of directors The interested party has abstained from voting

C) Prior approval is not needed for each draw against a line of credit provided the line of credit was approved within the preceding 14 months, based on the then-current financial statement

D) None of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

57

In Consumer Leasing Act Content of non-segregated disclosures may be made separately or as part of another document (such as the lease agreement); however, other information cannot be stated, used, or placed so as to mislead or confuse the consumer. Other disclosures include all of the following EXCEPT:

A) A statement of the conditions under which the lessee or lessor may terminate the lease before the end of the lease term, along with the amount (or a description of the method of how the amount is determined) of any penalty or other charge for early termination

B) Whether the lessee has the option to purchase the leased property during the lease term and, if applicable, the purchase price (or method for determining it) and when the lessee may exercise it

C) The lessee's right to an independent appraisal of the property if the lessee's liability at the end of the lease is based on the realized value of the leased property, and that the appraisal will be binding on all parties

D) A statement of maintenance responsibilities including the counter bank responsible and a description of the responsibility

A) A statement of the conditions under which the lessee or lessor may terminate the lease before the end of the lease term, along with the amount (or a description of the method of how the amount is determined) of any penalty or other charge for early termination

B) Whether the lessee has the option to purchase the leased property during the lease term and, if applicable, the purchase price (or method for determining it) and when the lessee may exercise it

C) The lessee's right to an independent appraisal of the property if the lessee's liability at the end of the lease is based on the realized value of the leased property, and that the appraisal will be binding on all parties

D) A statement of maintenance responsibilities including the counter bank responsible and a description of the responsibility

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

58

Purpose credit is credit for all of the following EXCEPT:

A) Immediate purpose of purchasing or carrying margin stock

B) Incidental purpose of purchasing or carrying margin stock

C) Ultimate purpose of purchasing or carrying margin stock

D) Accidental purpose of purchasing or carrying margin stock

A) Immediate purpose of purchasing or carrying margin stock

B) Incidental purpose of purchasing or carrying margin stock

C) Ultimate purpose of purchasing or carrying margin stock

D) Accidental purpose of purchasing or carrying margin stock

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

59

An exempted borrower is a member of a national securities exchange or a registered broker or dealer who:

A) Maintains at least 1,000 active accounts annually for persons other than brokers, dealers, and persons associated with brokers and dealers

B) Earns at least $10 million in gross revenues on an annual basis from transactions with persons other than brokers, dealers, and persons associated with brokers and dealers, or

C) Earns at least 10 percent of its gross revenues on an annual basis from transactions with persons other than brokers, dealers, and persons associated with brokers and dealers

D) None of these

A) Maintains at least 1,000 active accounts annually for persons other than brokers, dealers, and persons associated with brokers and dealers

B) Earns at least $10 million in gross revenues on an annual basis from transactions with persons other than brokers, dealers, and persons associated with brokers and dealers, or

C) Earns at least 10 percent of its gross revenues on an annual basis from transactions with persons other than brokers, dealers, and persons associated with brokers and dealers

D) None of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

60

In Advertising-12 CFR 213.7, if a percentage rate is used in an advertisement, it cannot be more prominent than any other disclosure, EXCEPT:

A) For the warning regarding the limitation of the rate as a measurement of cost

B) For beginning at least 3 days before and ending at least 10 days after the broadcast

C) For required disclosures in advertisements

D) For an advertisement accessed in electronic form

A) For the warning regarding the limitation of the rate as a measurement of cost

B) For beginning at least 3 days before and ending at least 10 days after the broadcast

C) For required disclosures in advertisements

D) For an advertisement accessed in electronic form

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

61

Under content of disclosures long term disclosures may include the following, as applicable EXCLUDING:

A) Notification that the product is optional

B) Explanation of debt-suspension agreement

C) Lump-sum payment of fee with no refund

D) Refund of fee paid in lump sum

A) Notification that the product is optional

B) Explanation of debt-suspension agreement

C) Lump-sum payment of fee with no refund

D) Refund of fee paid in lump sum

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

62

________________is defined as every aspect of an applicant's dealing with a creditor, beginning with information gathering and continuing through to the servicing and collection of the loan.

A) Credit terms

B) Credit rating

C) Credit transaction

D) Credit application

A) Credit terms

B) Credit rating

C) Credit transaction

D) Credit application

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

63

These are the definitions of _____________: The refusal to grant credit in substantially the amount or on substantially the terms requested in an application (and the applicant uses or expressly accepts the credit offered) A termination of the account or an unfavorable change in the terms of an account, unless the change affects substantially all of the lender's accounts of that type. A refusal to increase the amount of credit available to an applicant who has made an application for an increase

A) Adverse action-12 CFR 202.2(c)

B) Special-purpose credit-12 CFR 202.8

C) Refusals- 12 CFR 202.8

D) security agreements-12 CFR 202.2(c)

A) Adverse action-12 CFR 202.2(c)

B) Special-purpose credit-12 CFR 202.8

C) Refusals- 12 CFR 202.8

D) security agreements-12 CFR 202.2(c)

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

64

In Processing and evaluating applications-12 CFR 202.6, protected income part is also under discussion. Which of the following considerations is NOT its part?

A) Public assistance income may not consider whether an applicant's income is from a public assistance source

B) Public assistance income may consider as it relates to another pertinent element of creditworthiness

C) May consider length of time public assistance income will be received, whether the applicant will continue to qualify for the income, and whether the income can be garnished

D) Can discount or refuse to consider the following: Part-time income Annuities Pensions Retirement benefits Alimony, child support, and separate maintenance payments to the extent they are likely to be consistently made

A) Public assistance income may not consider whether an applicant's income is from a public assistance source

B) Public assistance income may consider as it relates to another pertinent element of creditworthiness

C) May consider length of time public assistance income will be received, whether the applicant will continue to qualify for the income, and whether the income can be garnished

D) Can discount or refuse to consider the following: Part-time income Annuities Pensions Retirement benefits Alimony, child support, and separate maintenance payments to the extent they are likely to be consistently made

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

65

The Equal Credit Opportunity Act (ECOA) was enacted in 1974 to prevent discrimination in credit transactions. In 1975 the act was amended. Which of the following prohibited base/s are now included in it?

A) National origin

B) Exercise of rights under the Consumer Credit Protection Act

C) Receipt of public assistance income

D) All of these

A) National origin

B) Exercise of rights under the Consumer Credit Protection Act

C) Receipt of public assistance income

D) All of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

66

Securities credit covers credit subject to Section 7 of the Securities Exchange Act of 1934 or credit by a broker or dealer subject to regulation under the act. The following requirements of Regulation B do not apply EXCEPT:

A) Restrictions regarding information about a spouse or former spouse, marital status, or sex of the applicant

B) It is not payable by agreement in more than four installments

C) Provisions relating to furnishing credit information

D) Records retention requirements

A) Restrictions regarding information about a spouse or former spouse, marital status, or sex of the applicant

B) It is not payable by agreement in more than four installments

C) Provisions relating to furnishing credit information

D) Records retention requirements

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

67

Short-form disclosures are required in advertisements and promotional materials unless the advertisements and promotional materials are of:

A) A general nature describing or listing the products or services offered by the bank

B) A specific nature describing or listing the products or services offered by the bank

C) A general nature describing or special services offered by the bank

D) A general nature describing competitive advantage of the bank

A) A general nature describing or listing the products or services offered by the bank

B) A specific nature describing or listing the products or services offered by the bank

C) A general nature describing or special services offered by the bank

D) A general nature describing competitive advantage of the bank

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

68

On a written request from a member of the public, the bank must disclose the names of each of its executive officers and principal shareholders to whom the bank had aggregate credit outstanding at the end of the latest quarter that equaled or exceeded:

A) 10 percent of the bank's capital, and unimpaired surplus or $500,000, whichever is less; no disclosure is required if the aggregate credit was $30,000 or less. Disclosure of individual loan amounts is not required

B) 5 percent of the bank's capital, and unimpaired surplus or $500,000, whichever is less; no disclosure is required if the aggregate credit was $25,000 or less. Disclosure of individual loan amounts is not required

C) 6 percent of the bank's capital, and unimpaired surplus or $100,000, whichever is less; no disclosure is required if the aggregate credit was $25,000 or less. Disclosure of individual loan amounts is not required

D) 5 percent of the bank's capital, and unimpaired surplus or $100,000, whichever is less; no disclosure is required if the aggregate credit was $35,000 or less. Disclosure of individual loan amounts is not required

A) 10 percent of the bank's capital, and unimpaired surplus or $500,000, whichever is less; no disclosure is required if the aggregate credit was $30,000 or less. Disclosure of individual loan amounts is not required

B) 5 percent of the bank's capital, and unimpaired surplus or $500,000, whichever is less; no disclosure is required if the aggregate credit was $25,000 or less. Disclosure of individual loan amounts is not required

C) 6 percent of the bank's capital, and unimpaired surplus or $100,000, whichever is less; no disclosure is required if the aggregate credit was $25,000 or less. Disclosure of individual loan amounts is not required

D) 5 percent of the bank's capital, and unimpaired surplus or $100,000, whichever is less; no disclosure is required if the aggregate credit was $35,000 or less. Disclosure of individual loan amounts is not required

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

69

Banks must establish and maintain effective risk management and control processes over its DCCs and DSAs, including:

A) Appropriate recognition and financial reporting of income, expenses, assets, and liabilities

B) Appropriate treatment of losses associated with these products

C) Assessment of the adequacy of its internal controls and risk mitigation activities

D) Before entering into a contract, the bank must obtain the customer's written affirmative election to enter into the contract and written acknowledgement of the receipt of the disclosures

A) Appropriate recognition and financial reporting of income, expenses, assets, and liabilities

B) Appropriate treatment of losses associated with these products

C) Assessment of the adequacy of its internal controls and risk mitigation activities

D) Before entering into a contract, the bank must obtain the customer's written affirmative election to enter into the contract and written acknowledgement of the receipt of the disclosures

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

70

This is a loan term or an arrangement that modifies a loan term under which a bank agrees to cancel all or part of a customer's loan obligation on the occurrence of a specified event. It may be included as a part of the loan documents, or it may be a separate agreement. What is it?

A) Debt suspension agreement (DSA)

B) Anti-dying

C) Debt cancellation contract (DCC)

D) ALLL

A) Debt suspension agreement (DSA)

B) Anti-dying

C) Debt cancellation contract (DCC)

D) ALLL

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

71

Government credit

A) It is credit extended to governments or government agencies, instrumentalities, or subdivisions

B) It has no finance charge

C) It has Records retention requirements

D) Only the general rule against discrimination applies to government credit

A) It is credit extended to governments or government agencies, instrumentalities, or subdivisions

B) It has no finance charge

C) It has Records retention requirements

D) Only the general rule against discrimination applies to government credit

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

72

This is a loan term or an arrangement that modifies a loan term under which a bank agrees to suspend all or part of a customer's loan obligation on the occurrence of a specified event. It May be a part of the loan itself or a separate agreement. Does not include a loan payment deferral arrangement where the borrower or the bank can unilaterally defer a payment. What is it?

A) Debt suspension agreement (DSA)

B) Anti-dying

C) Debt cancellation contract (DCC)

D) ALLL

A) Debt suspension agreement (DSA)

B) Anti-dying

C) Debt cancellation contract (DCC)

D) ALLL

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

73

Record keeping requirements-12 CFR 215.8 elaborates that:

A) Each bank must establish a recordkeeping system to keep records necessary for compliance with Regulation O

B) Banks may use any alternative recordkeeping method for insiders of affiliates if the bank's regulatory agency determines the bank's method is at least as effective as that required by Regulation O

C) All recordkeeping systems must Include either an annual survey of insiders to identify related interests, or a requirement as part of each extension of credit that the borrower indicates whether he or she is an insider. Provide for the maintenance of records of all credit to insiders, including the amounts and terms

D) All of these

A) Each bank must establish a recordkeeping system to keep records necessary for compliance with Regulation O

B) Banks may use any alternative recordkeeping method for insiders of affiliates if the bank's regulatory agency determines the bank's method is at least as effective as that required by Regulation O

C) All recordkeeping systems must Include either an annual survey of insiders to identify related interests, or a requirement as part of each extension of credit that the borrower indicates whether he or she is an insider. Provide for the maintenance of records of all credit to insiders, including the amounts and terms

D) All of these

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

74

Debt Cancellation Contracts and Debt Suspension Agreements coverage includes:

A) National banks that issue debt cancellation contracts and debt suspension agreements with borrowers in connection with loans for personal, family, or household purposes

B) A national bank may not engage in any practice, including advertising, which would cause a reasonable person to be misled with respect to DSAs and DCCs

C) A bank must provide the long-form disclosures in writing before the customer completes the purchase of a contract. If the solicitation occurs in person, the long-form disclosures must be provided at that time

D) A bank must make the short-form disclosures orally at the time the bank first solicits the contract

A) National banks that issue debt cancellation contracts and debt suspension agreements with borrowers in connection with loans for personal, family, or household purposes

B) A national bank may not engage in any practice, including advertising, which would cause a reasonable person to be misled with respect to DSAs and DCCs

C) A bank must provide the long-form disclosures in writing before the customer completes the purchase of a contract. If the solicitation occurs in person, the long-form disclosures must be provided at that time

D) A bank must make the short-form disclosures orally at the time the bank first solicits the contract

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

75

FDIC guidance lists three requirements to ensure compliance with spousal signature rules include all of the following EXCEPT:

A) Review and revise policies Eliminate policies or procedures that are inconsistent with the requirements Expand loan policies and procedures to provide loan staff with specific guidance on state law(s) regarding requiring signatures Cover the laws of all states where the creditor institution does business Create checklists to address situations when spousal signatures can be required

B) Provide training to consumer and commercial loan staff

C) Implement monitoring and auditing programs to check for spousal signature violations

D) Must allow an applicant to designate a birth-given first name and a birth-given, surname, spouse's surname, or combination

A) Review and revise policies Eliminate policies or procedures that are inconsistent with the requirements Expand loan policies and procedures to provide loan staff with specific guidance on state law(s) regarding requiring signatures Cover the laws of all states where the creditor institution does business Create checklists to address situations when spousal signatures can be required

B) Provide training to consumer and commercial loan staff

C) Implement monitoring and auditing programs to check for spousal signature violations

D) Must allow an applicant to designate a birth-given first name and a birth-given, surname, spouse's surname, or combination

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

76

Requirements-12 CFR 202.2, 202.4, 202.5, 202.6, and 202.13 say that a creditor may not request information about an application's race, color, religion, national origin, or gender except as specifically permitted by ____________or another statute such as the Home Mortgage Disclosure Act.

A) Regulation B

B) Regulation U

C) Regulation Z

D) Regulation A

A) Regulation B

B) Regulation U

C) Regulation Z

D) Regulation A

Unlock Deck

Unlock for access to all 418 flashcards in this deck.

Unlock Deck

k this deck

77

Federal regulations define special-purpose credit-12 CFR 202.8 to include:

A) Any credit assistance program authorized by federal or state law for the benefit of an economically disadvantaged class of persons

B) Any credit assistance program offered by a not-for-profit organization for the benefit of its members or for the benefit of an economically disadvantaged class of person

C) A special-purpose credit program must not discriminate on a prohibited basis; however, it can require its participants to share a particular characteristic (such as race or sex) provided the requirement was not established to evade the requirements of the ECOA. If the participants must share a common characteristic, the bank may collect information on that characteristic to determine eligibility

D) If the program includes financial need as a criterion, the creditor can never request and consider information regarding the applicant

A) Any credit assistance program authorized by federal or state law for the benefit of an economically disadvantaged class of persons

B) Any credit assistance program offered by a not-for-profit organization for the benefit of its members or for the benefit of an economically disadvantaged class of person

C) A special-purpose credit program must not discriminate on a prohibited basis; however, it can require its participants to share a particular characteristic (such as race or sex) provided the requirement was not established to evade the requirements of the ECOA. If the participants must share a common characteristic, the bank may collect information on that characteristic to determine eligibility