Deck : 4 Acquisition Costs of Unproved Propertysuccessful Efforts

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

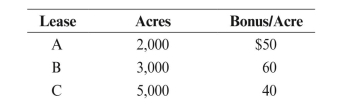

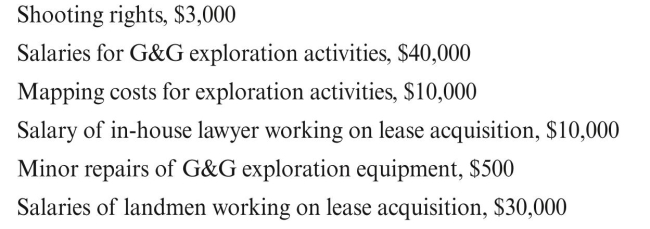

During 2015, Prosperity Oil Company acquired the following leases:  In acquiring and exploring these leases, Prosperity Oil Company incurred the following

In acquiring and exploring these leases, Prosperity Oil Company incurred the following

additional costs: Prosperity Oil allocates internal costs relating to lease acquisition to specific leases.

Prosperity Oil allocates internal costs relating to lease acquisition to specific leases.

Assuming Lease A was abandoned at the end of the year, answer the following

questions:

a. What was the total nondrilling exploration expense for all three leases for the year?

b. What was the surrendered lease expense?

c. How much was capitalized as unproved property for Lease B?

Hint: Some of these costs must be allocated to the individual leases on some

reasonable basis.

In acquiring and exploring these leases, Prosperity Oil Company incurred the followingadditional costs:

Prosperity Oil allocates internal costs relating to lease acquisition to specific leases.Assuming Lease A was abandoned at the end of the year, answer the following

questions:

a. What was the total nondrilling exploration expense for all three leases for the year?

b. What was the surrendered lease expense?

c. How much was capitalized as unproved property for Lease B?

Hint: Some of these costs must be allocated to the individual leases on some

reasonable basis.

Question

Question

Railway Oil and Gas Company owned the following unproved property as of the end

of 2010: Although no activity took place on Lease A during the year, Railway decided that

Although no activity took place on Lease A during the year, Railway decided that

Lease A was not impaired, because there were still three years left in that lease's

primary term. Two dry holes were drilled on Lease B during the year; but because

Railway intended to drill one more well on Lease B in the coming year, it decided that

Lease B was only 40% impaired. With respect to the individually insignificant leases,

past experience indicates that 70% of all unproved properties assessed on a group basis

will eventually be abandoned. Railway's policy is to provide at year-end an allowance

equal to 70% of the gross cost of these properties. The allowance account had a

balance of $20,000 at year-end. Give the entries to record impairment.

of 2010:

Although no activity took place on Lease A during the year, Railway decided thatLease A was not impaired, because there were still three years left in that lease's

primary term. Two dry holes were drilled on Lease B during the year; but because

Railway intended to drill one more well on Lease B in the coming year, it decided that

Lease B was only 40% impaired. With respect to the individually insignificant leases,

past experience indicates that 70% of all unproved properties assessed on a group basis

will eventually be abandoned. Railway's policy is to provide at year-end an allowance

equal to 70% of the gross cost of these properties. The allowance account had a

balance of $20,000 at year-end. Give the entries to record impairment.

Question

Question

Question

Sauer Energy purchased land in fee for $100,000. The fair market values of the surface

and mineral rights were determined by a qualified appraiser as follows: Prepare a journal entry to record the purchase.

Prepare a journal entry to record the purchase.

and mineral rights were determined by a qualified appraiser as follows:

Prepare a journal entry to record the purchase. Question

Question

Critic Oil Company purchased three leases as follows:  All the leases are classified as individually significant.

All the leases are classified as individually significant.

a. On December 31, 2014, Lease A is determined to be 25% impaired. Lease B and

Lease C are not impaired.

b. On December 31, 2015, Lease A is determined to be impaired a total of 75%, and

Lease C, 60%. Lease B is not impaired.

c. On December 31, 2016, Lease A is considered to be 100% impaired and is

abandoned. Lease B is 30% impaired, and a well on Lease C found proved reserves.

Prepare journal entries for all of the transactions except the initial purchase.

All the leases are classified as individually significant.a. On December 31, 2014, Lease A is determined to be 25% impaired. Lease B and

Lease C are not impaired.

b. On December 31, 2015, Lease A is determined to be impaired a total of 75%, and

Lease C, 60%. Lease B is not impaired.

c. On December 31, 2016, Lease A is considered to be 100% impaired and is

abandoned. Lease B is 30% impaired, and a well on Lease C found proved reserves.

Prepare journal entries for all of the transactions except the initial purchase.

Question

Question

Question

Question

Question

Question

Ernest Oil Company's balance sheet, at 12/31/14, included account balances as follows:  During 2015, the following events related to the above unproved properties occurred:

During 2015, the following events related to the above unproved properties occurred:

a. Lease A is abandoned.

b. Lease B is surrendered.

c. Leases G & F (individually insignificant) in the amounts of $2,000 and $3,000,

respectively, are abandoned.

Prepare the necessary entries.

During 2015, the following events related to the above unproved properties occurred:a. Lease A is abandoned.

b. Lease B is surrendered.

c. Leases G & F (individually insignificant) in the amounts of $2,000 and $3,000,

respectively, are abandoned.

Prepare the necessary entries.

Question

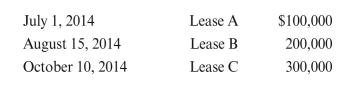

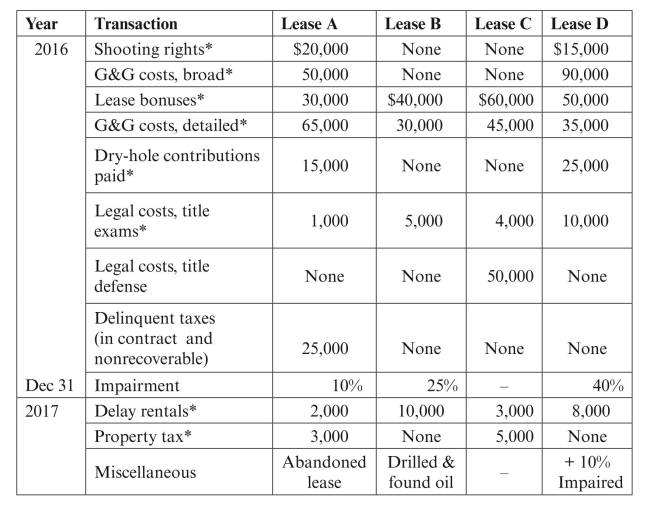

Rock Petroleum began operations in 2016 with the acquisition of four undeveloped

leases, all individually significant. Give the entries assuming the following transactions.

For simplicity, you may combine entries for the different leases for all items marked

with an asterisk (*).

leases, all individually significant. Give the entries assuming the following transactions.

For simplicity, you may combine entries for the different leases for all items marked

with an asterisk (*).

Question

Monarch Energy Corporation owned the following unproved property at 12/31/14:  Prepare journal entries for 2015, assuming the following events:

Prepare journal entries for 2015, assuming the following events:

a. Found proved reserves on Leases A & B.

b. Found proved reserves on Lease D.

c. Found proved reserves on Lease C.

Prepare journal entries for 2015, assuming the following events:a. Found proved reserves on Leases A & B.

b. Found proved reserves on Lease D.

c. Found proved reserves on Lease C.

Question

Question

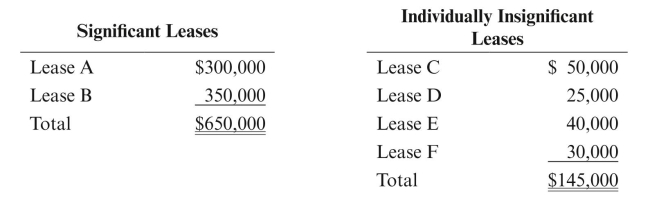

Dwight Corporation has the following groups of individually insignificant leases at

12/31/15. Prepare journal entries to record impairment for each of the groups at 12/31/15.

Prepare journal entries to record impairment for each of the groups at 12/31/15.

12/31/15.

Prepare journal entries to record impairment for each of the groups at 12/31/15. Question

Given the following data for Float Energy:  a. Give the entries to record the abandonment of both Lease A and Lease B.

a. Give the entries to record the abandonment of both Lease A and Lease B.

b. Give the entries assuming instead that both Lease A and Lease B were proved, i.e.,

oil or gas was discovered on the leases.

a. Give the entries to record the abandonment of both Lease A and Lease B.b. Give the entries assuming instead that both Lease A and Lease B were proved, i.e.,

oil or gas was discovered on the leases.

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/26

Play

Full screen (f)

Deck : 4 Acquisition Costs of Unproved Propertysuccessful Efforts

1

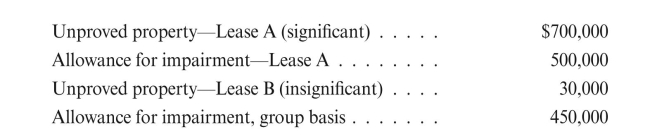

Guarantee Oil Company's internal land department incurred costs of $150,000 in

acquiring leases. Of the 1 million acres of prospects, only 450,000 acres were leased.

a. How much, if any, of the $150,000 incurred by the land department should be

capitalized?

b. If capitalized, what account(s) should be debited?

acquiring leases. Of the 1 million acres of prospects, only 450,000 acres were leased.

a. How much, if any, of the $150,000 incurred by the land department should be

capitalized?

b. If capitalized, what account(s) should be debited?

G Oil Company's internal land department incurred cost of $150,000 in acquiring lease. 450,000 acres were leased out of 1,000,000 acres of prospects.

a.Following amount should be capitalized by the land department. Hence the amount should be capitalized

Hence the amount should be capitalized  Capitalize amount is $ 67,500. The remaining amount $82,500

Capitalize amount is $ 67,500. The remaining amount $82,500  will be expensed out as it is not related to lease prospects.

will be expensed out as it is not related to lease prospects.

b.Unproved property account should be debited.

a.Following amount should be capitalized by the land department.

Hence the amount should be capitalized Capitalize amount is $ 67,500. The remaining amount $82,500 will be expensed out as it is not related to lease prospects.b.Unproved property account should be debited.

2

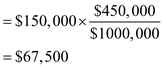

Opaque Corporation purchased land in fee for $420,000. The land was located in a

remote area in Oklahoma. An appraiser estimated the fair market value of the surface

rights to be $200,000. The appraiser was not able to make an estimate of the value of

the mineral rights.

Prepare a journal entry to record the purchase.

remote area in Oklahoma. An appraiser estimated the fair market value of the surface

rights to be $200,000. The appraiser was not able to make an estimate of the value of

the mineral rights.

Prepare a journal entry to record the purchase.

O corporation purchased land in fee for $ 420,000. Fair market value of surface rights is $200,000 which is debited to land account. As fair market value of mineral rights is not possible to determine, difference amount of $220,000  should be debited to unproved property account. Cash account will be credited by $420,000.

should be debited to unproved property account. Cash account will be credited by $420,000.

should be debited to unproved property account. Cash account will be credited by $420,000. 3

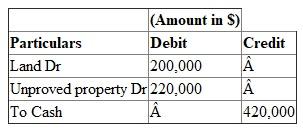

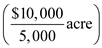

Gusher Oil Corporation obtained shooting rights only for $10,000 on 5,000 acres

owned by Mr. Q and shooting rights coupled with an option to lease for $12,000 on

4,000 acres owned by Mr. S. The 4,000 acres owned by Mr. S are located adjacent to the

5,000 acres owned by Mr. Q. Ignore any other acquisition costs.

a. Give the entries to record the rights obtained, assuming there is no apportionment

of the cost between the option and the shooting rights.

b. Give the entry to record the rights obtained from Mr. S, assuming instead that the

$12,000 was apportioned between the option and the shooting rights.

c. Give the entry to record the leasing of all 4,000 of Mr. S's acres, assuming that the

original cost of $12,000 was not apportioned between the option and the shooting

rights.

d. Give the entry to record the leasing of only 1,000 acres from Mr. S, again assuming

that the original cost of $12,000 was not apportioned. Also assume Gusher did not

apportion the amount in the suspense account based on the acreage leased.

e. Give the entry to record the leasing of 1,000 acres from Mr. S, assuming that the

original cost of $12,000 was not apportioned. Assume that Gusher Oil Corporation

apportioned the amount in the suspense account based on relative acreage leased.

owned by Mr. Q and shooting rights coupled with an option to lease for $12,000 on

4,000 acres owned by Mr. S. The 4,000 acres owned by Mr. S are located adjacent to the

5,000 acres owned by Mr. Q. Ignore any other acquisition costs.

a. Give the entries to record the rights obtained, assuming there is no apportionment

of the cost between the option and the shooting rights.

b. Give the entry to record the rights obtained from Mr. S, assuming instead that the

$12,000 was apportioned between the option and the shooting rights.

c. Give the entry to record the leasing of all 4,000 of Mr. S's acres, assuming that the

original cost of $12,000 was not apportioned between the option and the shooting

rights.

d. Give the entry to record the leasing of only 1,000 acres from Mr. S, again assuming

that the original cost of $12,000 was not apportioned. Also assume Gusher did not

apportion the amount in the suspense account based on the acreage leased.

e. Give the entry to record the leasing of 1,000 acres from Mr. S, assuming that the

original cost of $12,000 was not apportioned. Assume that Gusher Oil Corporation

apportioned the amount in the suspense account based on relative acreage leased.

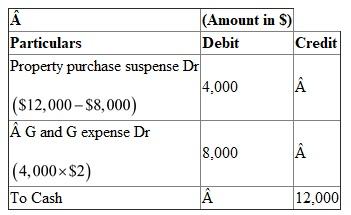

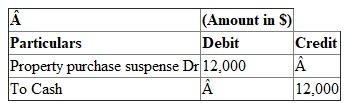

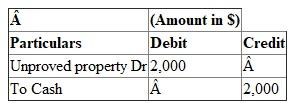

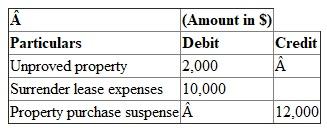

G Oil Company obtained shooting rights.

a.Journal entry of acquiring shooting right by assuming there is no allocation of cost between the option and shooting right. Property purchase suspense account will be debited as it is real account and cash account will be credited as cash goes out. b.Assuming rights obtained from Mr. S for 4,000 acres were apportioned between the options and shooting right. Shooting right per acre is $2

b.Assuming rights obtained from Mr. S for 4,000 acres were apportioned between the options and shooting right. Shooting right per acre is $2  .

.  c.Assuming original cost of $ 12,000 was not apportioned between the options and shooting right then entire amount will be capitalized. Hence property purchase suspense account will be debited.

c.Assuming original cost of $ 12,000 was not apportioned between the options and shooting right then entire amount will be capitalized. Hence property purchase suspense account will be debited.  d.Following journal entry showing the leasing of only 1,000 acres from Mr. S by assuming original cost of $ 12,000 was not apportioned between the options and shooting rights. Hence 1,000 acre will be multiplied by $2. As this amount will not be suspense this will be debited to unproved property because property is giving on lease.

d.Following journal entry showing the leasing of only 1,000 acres from Mr. S by assuming original cost of $ 12,000 was not apportioned between the options and shooting rights. Hence 1,000 acre will be multiplied by $2. As this amount will not be suspense this will be debited to unproved property because property is giving on lease.  e.

e.

Following journal entry showing the leasing of only 1,000 acres from Mr. S by assuming original cost of $ 12,000 was not apportioned. G Oil Corporation apportioned the amount in the suspense account based on relative acreage leased. Hence 1,000 acre will be multiplied by $2. As this amount will account to suspense account as this will be debited to property purchase suspense because property is giving on lease.

a.Journal entry of acquiring shooting right by assuming there is no allocation of cost between the option and shooting right. Property purchase suspense account will be debited as it is real account and cash account will be credited as cash goes out.

b.Assuming rights obtained from Mr. S for 4,000 acres were apportioned between the options and shooting right. Shooting right per acre is $2 . c.Assuming original cost of $ 12,000 was not apportioned between the options and shooting right then entire amount will be capitalized. Hence property purchase suspense account will be debited. d.Following journal entry showing the leasing of only 1,000 acres from Mr. S by assuming original cost of $ 12,000 was not apportioned between the options and shooting rights. Hence 1,000 acre will be multiplied by $2. As this amount will not be suspense this will be debited to unproved property because property is giving on lease. e.Following journal entry showing the leasing of only 1,000 acres from Mr. S by assuming original cost of $ 12,000 was not apportioned. G Oil Corporation apportioned the amount in the suspense account based on relative acreage leased. Hence 1,000 acre will be multiplied by $2. As this amount will account to suspense account as this will be debited to property purchase suspense because property is giving on lease.

4

On January 1, 2010, Local Petroleum entered into a concession agreement with the

government of Egypt and paid a $3,000,000 signing bonus. The agreement covers

20,000 acres, has a term of five years, and requires that exploration begin immediately.

At the end of the first three years, Local is required to begin relinquishing acreage at a

rate of 25% of the contract area per year. However, Local is not required to relinquish

proved acreage. On July 16, 2012, Local makes a commercial discovery and determines

that a 1,000 acre block is proved. On December 31, 2012, 25% of the initial contract

area is relinquished. Local estimates that only another 25% of the original contract

acreage will be relinquished.

Prepare all journal entries that would be required to account for the concession area

from January 1, 2010 through December 31, 2012.

government of Egypt and paid a $3,000,000 signing bonus. The agreement covers

20,000 acres, has a term of five years, and requires that exploration begin immediately.

At the end of the first three years, Local is required to begin relinquishing acreage at a

rate of 25% of the contract area per year. However, Local is not required to relinquish

proved acreage. On July 16, 2012, Local makes a commercial discovery and determines

that a 1,000 acre block is proved. On December 31, 2012, 25% of the initial contract

area is relinquished. Local estimates that only another 25% of the original contract

acreage will be relinquished.

Prepare all journal entries that would be required to account for the concession area

from January 1, 2010 through December 31, 2012.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

5

The following transactions relate to one lease:

a. On March 10, 2017, Axis Petroleum paid delinquent property taxes of $2,000 on

an undeveloped lease. Assume that these taxes are recoverable out of future delay

rental or royalty payments. Give the entry to record payment.

b. On February 15, 2018, a delay rental payment of $800 is due. Determine the

amount of cash actually paid and give the entry to record payment.

c. On July 21, 2018, Axis Petroleum decided to surrender the lease. Give the entry

to record abandonment with respect to the delinquent property taxes. Ignore

acquisition costs of the property.

d. Assume instead that the $2,000 payment of delinquent taxes was not recoverable

and was made at the time Axis Petroleum was acquiring the lease. Give the entry to

record the payment.

e. Assume instead that the $2,000 payment was not recoverable and was made by Axis

Petroleum six months after acquiring the lease in order to protect Axis' investment.

Give the entry to record the payment.

a. On March 10, 2017, Axis Petroleum paid delinquent property taxes of $2,000 on

an undeveloped lease. Assume that these taxes are recoverable out of future delay

rental or royalty payments. Give the entry to record payment.

b. On February 15, 2018, a delay rental payment of $800 is due. Determine the

amount of cash actually paid and give the entry to record payment.

c. On July 21, 2018, Axis Petroleum decided to surrender the lease. Give the entry

to record abandonment with respect to the delinquent property taxes. Ignore

acquisition costs of the property.

d. Assume instead that the $2,000 payment of delinquent taxes was not recoverable

and was made at the time Axis Petroleum was acquiring the lease. Give the entry to

record the payment.

e. Assume instead that the $2,000 payment was not recoverable and was made by Axis

Petroleum six months after acquiring the lease in order to protect Axis' investment.

Give the entry to record the payment.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

6

Lomax Company typically acquires a large number of individually insignificant

properties each year. In computing impairment, Lomax groups these properties by

year of acquisition. During 2015, Lomax acquired individually insignificant unproved

property costing a total of $400,000. In the past, Lomax has abandoned 30% of all

individually insignificant unproved properties without ever finding oil or gas. It takes

Lomax an average of three years to determine whether a property will be proved or

surrendered.

Give the entry to record impairment.

properties each year. In computing impairment, Lomax groups these properties by

year of acquisition. During 2015, Lomax acquired individually insignificant unproved

property costing a total of $400,000. In the past, Lomax has abandoned 30% of all

individually insignificant unproved properties without ever finding oil or gas. It takes

Lomax an average of three years to determine whether a property will be proved or

surrendered.

Give the entry to record impairment.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

7

During 2015, Prosperity Oil Company acquired the following leases: In acquiring and exploring these leases, Prosperity Oil Company incurred the following

additional costs: Prosperity Oil allocates internal costs relating to lease acquisition to specific leases.

Assuming Lease A was abandoned at the end of the year, answer the following

questions:

a. What was the total nondrilling exploration expense for all three leases for the year?

b. What was the surrendered lease expense?

c. How much was capitalized as unproved property for Lease B?

Hint: Some of these costs must be allocated to the individual leases on some

reasonable basis.

In acquiring and exploring these leases, Prosperity Oil Company incurred the followingadditional costs:

Prosperity Oil allocates internal costs relating to lease acquisition to specific leases.Assuming Lease A was abandoned at the end of the year, answer the following

questions:

a. What was the total nondrilling exploration expense for all three leases for the year?

b. What was the surrendered lease expense?

c. How much was capitalized as unproved property for Lease B?

Hint: Some of these costs must be allocated to the individual leases on some

reasonable basis.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

8

Bryant Oil Corporation acquired a lease on October 15, 2015, for $200,000 cash. No

drilling was done on the lease during the first year. Since Bryant wished to retain the

lease, a delay rental of $10,000 was paid on October 15, 2016. During November and

December of 2016, three dry holes were drilled on surrounding leases. Based on the

dry holes, Bryant's management decided that the lease was 75% impaired. Bryant had

still not started drilling operations by the end of the second year and so paid a second

delay rental. During November 2017, with less than one year of the primary term

left, Bryant drilled a dry hole on the lease and decided to abandon the lease. Because

the end of Bryant's accounting period is December 31 and for income tax purposes,

Bryant executed a quit claim deed and relinquished all rights to the lease the last day of

November 2017. Give the entries.

drilling was done on the lease during the first year. Since Bryant wished to retain the

lease, a delay rental of $10,000 was paid on October 15, 2016. During November and

December of 2016, three dry holes were drilled on surrounding leases. Based on the

dry holes, Bryant's management decided that the lease was 75% impaired. Bryant had

still not started drilling operations by the end of the second year and so paid a second

delay rental. During November 2017, with less than one year of the primary term

left, Bryant drilled a dry hole on the lease and decided to abandon the lease. Because

the end of Bryant's accounting period is December 31 and for income tax purposes,

Bryant executed a quit claim deed and relinquished all rights to the lease the last day of

November 2017. Give the entries.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

9

Railway Oil and Gas Company owned the following unproved property as of the end

of 2010: Although no activity took place on Lease A during the year, Railway decided that

Lease A was not impaired, because there were still three years left in that lease's

primary term. Two dry holes were drilled on Lease B during the year; but because

Railway intended to drill one more well on Lease B in the coming year, it decided that

Lease B was only 40% impaired. With respect to the individually insignificant leases,

past experience indicates that 70% of all unproved properties assessed on a group basis

will eventually be abandoned. Railway's policy is to provide at year-end an allowance

equal to 70% of the gross cost of these properties. The allowance account had a

balance of $20,000 at year-end. Give the entries to record impairment.

of 2010:

Although no activity took place on Lease A during the year, Railway decided thatLease A was not impaired, because there were still three years left in that lease's

primary term. Two dry holes were drilled on Lease B during the year; but because

Railway intended to drill one more well on Lease B in the coming year, it decided that

Lease B was only 40% impaired. With respect to the individually insignificant leases,

past experience indicates that 70% of all unproved properties assessed on a group basis

will eventually be abandoned. Railway's policy is to provide at year-end an allowance

equal to 70% of the gross cost of these properties. The allowance account had a

balance of $20,000 at year-end. Give the entries to record impairment.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

10

Latitude Energy decided to explore some acreage in Texas before acquiring any leases.

Latitude acquired shooting rights only on 15,000 acres owned by Mr. T for $0.10/acre.

Latitude obtained shooting rights coupled with an option to lease on 10,000 acres

owned by Mr. H for $0.25/acre. After completing G&G surveys at a cost of $85,000,

Latitude decided to lease 5,000 acres from Mr. T, paying a bonus of $35/acre. Latitude

also decided to lease 5,000 acres from Mr. H, paying the same bonus of $35/acre.

Latitude's income statement has seen better days, and although it will not help much,

Latitude decides to capitalize every possible cost. Give the entries.

Latitude acquired shooting rights only on 15,000 acres owned by Mr. T for $0.10/acre.

Latitude obtained shooting rights coupled with an option to lease on 10,000 acres

owned by Mr. H for $0.25/acre. After completing G&G surveys at a cost of $85,000,

Latitude decided to lease 5,000 acres from Mr. T, paying a bonus of $35/acre. Latitude

also decided to lease 5,000 acres from Mr. H, paying the same bonus of $35/acre.

Latitude's income statement has seen better days, and although it will not help much,

Latitude decides to capitalize every possible cost. Give the entries.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

11

Bear Oil Incorporated has two unproved leases with the following capitalized costs:

Lease C (600 acres) $20,000

Lease D (1,200 acres) $50,000

Bear Oil Incorporated negotiated a new lease on Lease C immediately following the end

of the primary term. The lease bonus was $60/acre on the new lease. Before the end of

the primary term, Bear Oil also obtained a new lease on Lease D at a lease bonus rate

of $40/acre. This lease was to take effect prior to the end of the primary term. Prepare

journal entries for the two leases.

Lease C (600 acres) $20,000

Lease D (1,200 acres) $50,000

Bear Oil Incorporated negotiated a new lease on Lease C immediately following the end

of the primary term. The lease bonus was $60/acre on the new lease. Before the end of

the primary term, Bear Oil also obtained a new lease on Lease D at a lease bonus rate

of $40/acre. This lease was to take effect prior to the end of the primary term. Prepare

journal entries for the two leases.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

12

Sauer Energy purchased land in fee for $100,000. The fair market values of the surface

and mineral rights were determined by a qualified appraiser as follows: Prepare a journal entry to record the purchase.

and mineral rights were determined by a qualified appraiser as follows:

Prepare a journal entry to record the purchase. Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

13

Define the following:

top lease

bonus

option to lease

purchase in fee

delinquent taxes paid by the lessee

impairment

internal costs

top lease

bonus

option to lease

purchase in fee

delinquent taxes paid by the lessee

impairment

internal costs

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

14

Critic Oil Company purchased three leases as follows: All the leases are classified as individually significant.

a. On December 31, 2014, Lease A is determined to be 25% impaired. Lease B and

Lease C are not impaired.

b. On December 31, 2015, Lease A is determined to be impaired a total of 75%, and

Lease C, 60%. Lease B is not impaired.

c. On December 31, 2016, Lease A is considered to be 100% impaired and is

abandoned. Lease B is 30% impaired, and a well on Lease C found proved reserves.

Prepare journal entries for all of the transactions except the initial purchase.

All the leases are classified as individually significant.a. On December 31, 2014, Lease A is determined to be 25% impaired. Lease B and

Lease C are not impaired.

b. On December 31, 2015, Lease A is determined to be impaired a total of 75%, and

Lease C, 60%. Lease B is not impaired.

c. On December 31, 2016, Lease A is considered to be 100% impaired and is

abandoned. Lease B is 30% impaired, and a well on Lease C found proved reserves.

Prepare journal entries for all of the transactions except the initial purchase.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

15

On December 31, 2016, Dill Oil Company recognized impairment of $100,000 on an

individually significant lease. Before the financial statements were issued early the next

year, a well was drilled and proved reserves were found. Dill easily revised their financial

statements so that no impairment was recognized on the property. Please comment.

individually significant lease. Before the financial statements were issued early the next

year, a well was drilled and proved reserves were found. Dill easily revised their financial

statements so that no impairment was recognized on the property. Please comment.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

16

Seaside Oil Corporation has an offshore lease that cost $4,000,000. The total acreage

is 40,000 acres. Proved reserves are found on a 10,000 acre tract that is included in the

40,000 acres. Management decides to reclassify only the proved area acreage.

Prepare the entry to reclassify the acreage.

is 40,000 acres. Proved reserves are found on a 10,000 acre tract that is included in the

40,000 acres. Management decides to reclassify only the proved area acreage.

Prepare the entry to reclassify the acreage.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

17

Tharp Energy Company, which uses the successful efforts method of accounting, owns

an individually significant lease, with a cost of $200,000. On December 31, 2017, the

lease is not considered impaired. However, prior to completion of the audit, a well on

adjacent property is abandoned as a dry hole, and the lease is now considered to be

40% impaired. Prepare any necessary adjusting entry.

an individually significant lease, with a cost of $200,000. On December 31, 2017, the

lease is not considered impaired. However, prior to completion of the audit, a well on

adjacent property is abandoned as a dry hole, and the lease is now considered to be

40% impaired. Prepare any necessary adjusting entry.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

18

Bartz Corporation leased 10,000 acres with a lease bonus of $80/acre. Delay rentals are

to be at a rate of $5/acre. The lease specified that Bartz Corporation could abandon the

lease in 1,000 acre portions. At the end of year 1, Bartz Corporation abandoned 4,000

acres and paid a delay rental on the remainder.

Prepare journal entries for the activities.

to be at a rate of $5/acre. The lease specified that Bartz Corporation could abandon the

lease in 1,000 acre portions. At the end of year 1, Bartz Corporation abandoned 4,000

acres and paid a delay rental on the remainder.

Prepare journal entries for the activities.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

19

Decade Oil Corporation paid $500/acre for a lease with a three-year primary term.

During the next two years, Decade drilled three dry holes on the property. With one

more year of the primary term left, Decade still intends to try one more time. Should

any impairment be recognized on the property?

During the next two years, Decade drilled three dry holes on the property. With one

more year of the primary term left, Decade still intends to try one more time. Should

any impairment be recognized on the property?

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

20

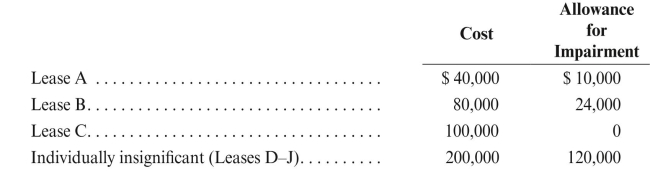

Ernest Oil Company's balance sheet, at 12/31/14, included account balances as follows: During 2015, the following events related to the above unproved properties occurred:

a. Lease A is abandoned.

b. Lease B is surrendered.

c. Leases G & F (individually insignificant) in the amounts of $2,000 and $3,000,

respectively, are abandoned.

Prepare the necessary entries.

During 2015, the following events related to the above unproved properties occurred:a. Lease A is abandoned.

b. Lease B is surrendered.

c. Leases G & F (individually insignificant) in the amounts of $2,000 and $3,000,

respectively, are abandoned.

Prepare the necessary entries.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

21

Rock Petroleum began operations in 2016 with the acquisition of four undeveloped

leases, all individually significant. Give the entries assuming the following transactions.

For simplicity, you may combine entries for the different leases for all items marked

with an asterisk (*).

leases, all individually significant. Give the entries assuming the following transactions.

For simplicity, you may combine entries for the different leases for all items marked

with an asterisk (*).

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

22

Monarch Energy Corporation owned the following unproved property at 12/31/14: Prepare journal entries for 2015, assuming the following events:

a. Found proved reserves on Leases A & B.

b. Found proved reserves on Lease D.

c. Found proved reserves on Lease C.

Prepare journal entries for 2015, assuming the following events:a. Found proved reserves on Leases A & B.

b. Found proved reserves on Lease D.

c. Found proved reserves on Lease C.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

23

On December 31, 2015, Launch Oil Company's unproved property account for leases

that are not individually significant had a balance of $800,000. The impairment

allowance account had a balance of $75,000. Give the entries for each of the following

transactions occurring in 2015, 2016, and 2017. (All transactions concern individually

insignificant unproved leases.)

a. Assuming Launch has a policy of maintaining a 55% allowance, i.e., 55% of gross

unproved properties, give the entry to record impairment on December 31, 2015.

b. During 2016, Launch surrendered leases that cost $300,000.

c. During 2016, leases that cost $50,000 were proved.

d. During 2016, leases costing $310,000 were acquired.

e. Give the entry to record impairment on December 31, 2006.

f. During 2017, leases costing $428,000 were surrendered.

that are not individually significant had a balance of $800,000. The impairment

allowance account had a balance of $75,000. Give the entries for each of the following

transactions occurring in 2015, 2016, and 2017. (All transactions concern individually

insignificant unproved leases.)

a. Assuming Launch has a policy of maintaining a 55% allowance, i.e., 55% of gross

unproved properties, give the entry to record impairment on December 31, 2015.

b. During 2016, Launch surrendered leases that cost $300,000.

c. During 2016, leases that cost $50,000 were proved.

d. During 2016, leases costing $310,000 were acquired.

e. Give the entry to record impairment on December 31, 2006.

f. During 2017, leases costing $428,000 were surrendered.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

24

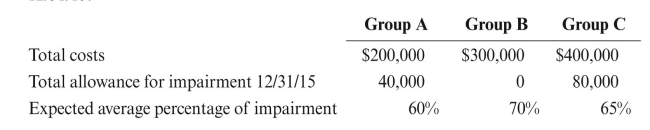

Dwight Corporation has the following groups of individually insignificant leases at

12/31/15. Prepare journal entries to record impairment for each of the groups at 12/31/15.

12/31/15.

Prepare journal entries to record impairment for each of the groups at 12/31/15. Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

25

Given the following data for Float Energy: a. Give the entries to record the abandonment of both Lease A and Lease B.

b. Give the entries assuming instead that both Lease A and Lease B were proved, i.e.,

oil or gas was discovered on the leases.

a. Give the entries to record the abandonment of both Lease A and Lease B.b. Give the entries assuming instead that both Lease A and Lease B were proved, i.e.,

oil or gas was discovered on the leases.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

26

Give the entry to record abandonment in each of the following cases.

a. Gaylene Energy Company abandoned an unproved property that cost $150,000.

The property was considered significant and had been impaired $100,000 on an

individual basis.

b. Gaylene also abandoned an unproved property that was not considered individually

significant. The property cost $10,000, and the group allowance account had a

balance of $400,000 at the time of the abandonment.

a. Gaylene Energy Company abandoned an unproved property that cost $150,000.

The property was considered significant and had been impaired $100,000 on an

individual basis.

b. Gaylene also abandoned an unproved property that was not considered individually

significant. The property cost $10,000, and the group allowance account had a

balance of $400,000 at the time of the abandonment.

Unlock Deck

Unlock for access to all 26 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 26 flashcards in this deck.