Deck 8: Costing

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

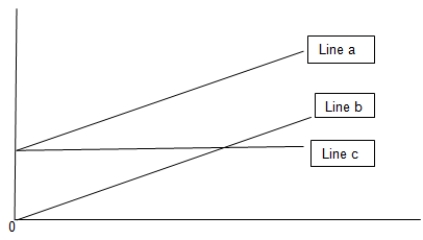

What does line a on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

Question

What does line b on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

Question

What does line c on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

Question

What does line a on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Total revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Total revenue

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/40

Play

Full screen (f)

Deck 8: Costing

1

Which one of the following statements is not true?

A) Financial accounting reports are aimed at internal users of accounting information while management accounting reports are aimed at external users of accounting information

B) Financial accounting summarizes accounting data while management accounting breaks down costs into their detailed components.

C) Financial accounting reports report on what has happened while management accounting reports focus on current activity and future projections.

D) Financial accounting reports are used by investors to make investment decisions while management accounting reports are used by managers to make business decisions.

A) Financial accounting reports are aimed at internal users of accounting information while management accounting reports are aimed at external users of accounting information

B) Financial accounting summarizes accounting data while management accounting breaks down costs into their detailed components.

C) Financial accounting reports report on what has happened while management accounting reports focus on current activity and future projections.

D) Financial accounting reports are used by investors to make investment decisions while management accounting reports are used by managers to make business decisions.

A

2

Which of the following are descriptions of management accounting? Please select all that apply.

A) Future focus

B) Expected v actual comparisons

C) External parties reporting

D) Accounting data at the micro level

A) Future focus

B) Expected v actual comparisons

C) External parties reporting

D) Accounting data at the micro level

A,B,D

3

Which one of the following is the odd one out?

A) Not designed for planning purposes.

B) Information with a historical perspective.

C) Presents summarised accounting information.

D) A focus on the future.

A) Not designed for planning purposes.

B) Information with a historical perspective.

C) Presents summarised accounting information.

D) A focus on the future.

D

4

Which one of the following is the odd one out?

A) Information prepared for internal users.

B) Information summarising annual accounting data.

C) Information that is used to make business decisions.

D) Information that has a forward looking perspective.

A) Information prepared for internal users.

B) Information summarising annual accounting data.

C) Information that is used to make business decisions.

D) Information that has a forward looking perspective.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

5

Which one of the following statements does not describe a feature of management accounting?

A) Used to guide and control operations.

B) Used to guide an organization to the fulfilment of both long and short term objectives.

C) Used by external users for investment decision making purposes.

D) Monitors actual outcomes against budgets.

A) Used to guide and control operations.

B) Used to guide an organization to the fulfilment of both long and short term objectives.

C) Used by external users for investment decision making purposes.

D) Monitors actual outcomes against budgets.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

6

Which one of the following statements is not true?

A) At zero levels of production, total costs = fixed costs.

B) Variable costs are zero when no production takes place.

C) As the number of products produced decreases, the average total cost per product decreases.

D) The cost of salaried production workers is both a direct and a fixed cost that will not vary directly in line with production.

A) At zero levels of production, total costs = fixed costs.

B) Variable costs are zero when no production takes place.

C) As the number of products produced decreases, the average total cost per product decreases.

D) The cost of salaried production workers is both a direct and a fixed cost that will not vary directly in line with production.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

7

Which one of the following is the odd one out?

A) Direct labour

B) Direct material

C) Factory overhead.

D) Direct expense

A) Direct labour

B) Direct material

C) Factory overhead.

D) Direct expense

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

8

In a book printing business, which one of the following would not be classified as a direct labour cost?

A) Proof reading

B) Editing

C) Printers' salaries

D) Sales representatives' salaries

A) Proof reading

B) Editing

C) Printers' salaries

D) Sales representatives' salaries

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

9

Direct costs are

A) The costs directly attributable to producing a product or delivering a service.

B) The variable costs of producing a product or service.

C) The marginal cost of a product or service.

D) The costs incurred in producing one more unit of product or service.

A) The costs directly attributable to producing a product or delivering a service.

B) The variable costs of producing a product or service.

C) The marginal cost of a product or service.

D) The costs incurred in producing one more unit of product or service.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

10

Direct costs:

Please select all that apply.

A) Can be both fixed and variable.

B) Can be traced to specific units of production.

C) Vary directly in line with production.

D) Are incurred only as a result of producing goods and services.

Please select all that apply.

A) Can be both fixed and variable.

B) Can be traced to specific units of production.

C) Vary directly in line with production.

D) Are incurred only as a result of producing goods and services.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

11

Direct costs are the marginal cost of production of goods and services.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

12

All indirect costs are fixed costs.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

13

All direct costs of production are variable costs.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following statements describe fixed costs? Please select all that apply.

A) These costs remain the same for a given period of time.

B) These costs are still incurred even when production is zero.

C) These costs can form part of the direct costs of production.

D) These costs vary in line with production.

A) These costs remain the same for a given period of time.

B) These costs are still incurred even when production is zero.

C) These costs can form part of the direct costs of production.

D) These costs vary in line with production.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements describe variable costs? Please select all that apply.

A) These costs change in line with changes in production.

B) These costs are absorbed into products on the basis of labour or machine hours in a traditional costing system.

C) These costs are £nil when no production takes place.

D) These costs can be direct costs of production or indirect costs.

A) These costs change in line with changes in production.

B) These costs are absorbed into products on the basis of labour or machine hours in a traditional costing system.

C) These costs are £nil when no production takes place.

D) These costs can be direct costs of production or indirect costs.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

16

Acme Manufacturing produces a standard sized radiator for central heating systems. Parts for each radiator cost £20 and direct labour of £10 is incurred in the production of each radiator along with direct expenses of £5. Annual factory overheads total up to £200,000 for the year. The directors of Acme Manufacturing expect to produce 25,000 radiators each year but due to difficulties in the manufacturing process in the financial year to 31 December 2019, only 20,000 radiators were produced. The selling price of each radiator is £55. At 31 December 2019, there were 1,000 radiators held in inventory. What is the total value of this closing inventory on an absorption costing basis?

A) £35,000

B) £43,000

C) £45,000

D) £55,000

A) £35,000

B) £43,000

C) £45,000

D) £55,000

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

17

Miller Limited manufactures television sets. The marketing department is setting a selling price for each television set and has received the following details of costs from the accounting department. Direct costs per television set: £80; total departmental overheads: £600,000; total number of departmental labour hours: 25,000; number of departmental labour hours taken to produce each television set: 5. The selling price for television sets has been set at total absorption cost + 25%. What is the selling price that the marketing department should set for each television set?

A) £100

B) £130

C) £150

D) £250

A) £100

B) £130

C) £150

D) £250

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

18

Omega Manufacturing has three production departments, milling, finishing and painting. The painting department has allocated overheads of £120,000 and a normal level of activity of 10,000 labour hours per annum. The repairs and maintenance service department has allocated overheads of £100,000 and the painting department's usage of the repairs and maintenance department is 30% of the total capacity of that department. Of the 28 employees in the firm, 7 are in the painting department. Canteen costs for Omega Manufacturing are £80,000 per annum. What is the painting department's hourly overhead absorption rate on a labour-hour basis?

A) £12

B) £17

C) £20

D) £22

A) £12

B) £17

C) £20

D) £22

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

19

The production department at Geneva Manufacturing incurs annual production overheads of £250,000. There are three support departments for the business, stores, set up and maintenance. The maintenance department's resources are used as follows: 20% by production, 10% by stores, 15% by set up. The other 55% of the maintenance department's resources are used by other departments in the business. In addition, the production department uses 40% of the resources of the stores department and 40% of the resources in the set up department. Support department overheads total up as follows: stores: £100,000, set up: £150,000, maintenance: £80,000. What are the total overheads that will be allocated to the production department?

A) £250,000

B) £358,000

C) £366,000

D) £374,000

A) £250,000

B) £358,000

C) £366,000

D) £374,000

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

20

Modigliani Limited manufactures large speaker cabinets. Each speaker cabinet has material costs of £50, direct labour cost of £25 and direct expenses of £15. Each speaker requires 5 hours of machining department time and 6 hours of finishing department time. Total overheads in the machining department are £300,000 per annum while the finishing department incurs total overheads of £150,000. The finishing department's employees work 25,000 labour hours each year while the machining department machines run for 30,000 hours during the year. What is the absorption cost of each large speaker cabinet?

A) £90

B) £126

C) £140

D) £176

A) £90

B) £126

C) £140

D) £176

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

21

Production overheads for a year are totalled up and then absorbed into the cost of products on a labour or machine hour basis. Which one of the following expenses will not be classified as a production overhead?

A) Machinery depreciation

B) Factory rent

C) Product advertising

D) Maintenance department costs

A) Machinery depreciation

B) Factory rent

C) Product advertising

D) Maintenance department costs

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

22

The St Godwen Wine Cooperative runs a vineyard and winery. The direct costs of producing one bottle of wine are £5.50. The expected level of production in a year is 250,000 bottles of wine. In the year ended 31 January 2020, only 200,000 bottles of wine were produced due to unfavourable weather conditions in the summer of 2019. Fixed production costs for the year total up to £450,000. At 31 January 2020, the St Godwen Wine Cooperative has 20,000 bottles of wine from the 2019 vintage in its cellars. What is the total value of this wine on an absorption costing basis?

A) £36,000

B) £110,000

C) £146,000

D) £155,000

A) £36,000

B) £110,000

C) £146,000

D) £155,000

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

23

The actual level of production is used as the basis for allocating indirect costs to products and services.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

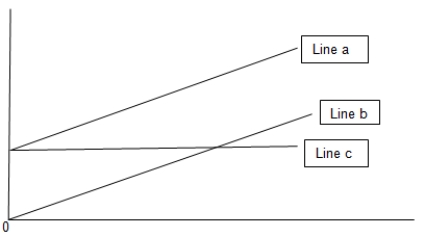

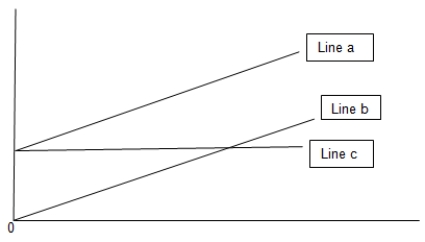

24

What does line a on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

25

What does line b on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

26

What does line c on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Revenue

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

27

What does line a on the graph represent?

A) Variable cost

B) Fixed cost

C) Total cost

D) Total revenue

A) Variable cost

B) Fixed cost

C) Total cost

D) Total revenue

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

28

The variable cost line on the total costs graph starts at zero and rises in a linear fashion in line with the production of goods and services.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

29

The fixed costs line on the total costs graph is a horizontal line starting at the level of fixed costs on the y axis.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

30

Which one of the following is not a limitation of traditional absorption costing?

A) Under- or over-allocates overheads to products on machine or labour hour allocation bases.

B) Allocates costs on the basis of labour or machine hours rather than on the basis of the number of activities consumed by each product.

C) Assumes that costs can be determined with the required precision to enable overhead cost to be allocated to products on the basis of labour or machine hours.

D) Recognizes that variable costs do not necessarily remain the same for all units of production.

A) Under- or over-allocates overheads to products on machine or labour hour allocation bases.

B) Allocates costs on the basis of labour or machine hours rather than on the basis of the number of activities consumed by each product.

C) Assumes that costs can be determined with the required precision to enable overhead cost to be allocated to products on the basis of labour or machine hours.

D) Recognizes that variable costs do not necessarily remain the same for all units of production.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following statements do not describe absorption costing? Please select all that apply.

A) Subsidises products through the misallocation of overheads on a labour or machine hour basis.

B) Takes into account the unique costs attributable to each product.

C) Recognises the complexity of modern manufacturing environments and the ways in which costs are driven by activity levels.

D) Suitable for allocating costs to individually designed and manufactured products.

A) Subsidises products through the misallocation of overheads on a labour or machine hour basis.

B) Takes into account the unique costs attributable to each product.

C) Recognises the complexity of modern manufacturing environments and the ways in which costs are driven by activity levels.

D) Suitable for allocating costs to individually designed and manufactured products.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

32

Which one of the following statements is not a criticism of traditional absorption costing?

A) Assumes costs are incurred in a steady, easy to allocate way.

B) Fails to recognise the demands made by particular products on an entity's resources.

C) Able to allocate unique costs to specific units of production.

D) Results in the calculation of inaccurate selling prices.

A) Assumes costs are incurred in a steady, easy to allocate way.

B) Fails to recognise the demands made by particular products on an entity's resources.

C) Able to allocate unique costs to specific units of production.

D) Results in the calculation of inaccurate selling prices.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

33

Activity-based costing allocates overheads to products on the basis of:

A) Expected levels of production

B) Labour or machine hours used

C) Costs consumed by a product

D) Services consumed on the basis of departmental usage

A) Expected levels of production

B) Labour or machine hours used

C) Costs consumed by a product

D) Services consumed on the basis of departmental usage

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

34

Which of the following will be required to determine selling prices for products and services when using an activity based costing (ABC) system?

Please select all that apply.

A) Costs allocated to cost pools.

B) Cost drivers for each cost pool.

C) The direct costs of products and services.

D) Total machine or labour hours for the period of operations.

Please select all that apply.

A) Costs allocated to cost pools.

B) Cost drivers for each cost pool.

C) The direct costs of products and services.

D) Total machine or labour hours for the period of operations.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

35

In an activity based costing system, overheads are allocated to products on the basis of activities consumed by each product.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

36

DEF produces a component, G4H125. The company has annual set up costs for 200 set ups a year of £100,000; annual materials handling costs are £75,000 with 10,000 materials handling operations taking place each year; the company deals with 4,000 orders with suppliers each year at a total cost of £80,000. Component G4H125 accounts for 80 set ups each year, 5,000 materials handling operations and 625 supplier orders. Total annual machine hours are 30,000 and component G4H125 uses 6 machine hours for each component. Total annual labour hours are 15,000 and component G4H125 uses 5 labour hours per component. 2,500 G4H125 components are produced each year. What would be the overhead to allocate to each G4H125 component using an activity-based costing approach to overhead allocation?

A) £36

B) £51

C) £85

D) £102

A) £36

B) £51

C) £85

D) £102

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

37

KLM produces a component, N1P442. The company has total annual overheads of £660,000. These are made up of quality inspection costs of £120,000, design costs of £200,000, materials handling costs of £160,000 and set up costs of £180,000. During the financial year there are 3,600 set ups, 6,000 quality inspections, 6,400 materials handling operations and 2,500 design hours. Component N1P442 accounts for 2,400 set ups each year, 2,000 materials handling operations and 1,500 quality inspections. 500 design hours are allocated to the N1P442 component during the year. Total annual machine hours are 50,000 and component N1P442 uses 30 machine hours for each component. Total annual labour hours are 120,000 and component N1P442 uses 64 labour hours per component. 600 N1P442 components are produced each year. What would be the overhead to allocate to each N1P442 component using an activity-based costing approach to overhead allocation?

A) £352

B) £396

C) £400

D) £1,100

A) £352

B) £396

C) £400

D) £1,100

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

38

Fixed costs remain fixed over a given time period and over all levels of production.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

39

Variable costs remain the same for all units of production.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

40

Costing relies heavily on estimation and the costs allocated to a product or service are a best guess, not an absolutely correct figure.

Unlock Deck

Unlock for access to all 40 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 40 flashcards in this deck.