Deck 6: The Purchase Method: Postacquisition Periods and Partial Ownerships

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

_____ When a parent company uses the equity method in accounting for its investment in a subsidiary, which of the following affects the parent's reported investment income?

Question

_____ When a parent company uses the cost method in accounting for its investment in a subsidiary, which of the following affects the parent's reported investment income?

Question

_____ A subsidiary declares a liquidating cash dividend. The Investment in Subsidiary account would be credited under which of the following accounting methods?

Question

_____ A subsidiary declares a nonliquidating cash dividend. What is the effect of this declaration on the parent's Retained Earnings account under each of the following accounting methods?

Question

Question

Question

Question

Question

Question

_____ On 4/1/06, Pullco acquired 100% of Strapco's outstanding common stock for $500,000 cash. For 2006, Strapco reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

Question

_____ On 4/1/06, Pullco acquired 100% of Strapco's outstanding common stock for $500,000 cash. For 2006, Strapco reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?.

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?.

A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?.A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

Question

_____ On 3/31/06, Ponzico acquired 100% of the outstanding common stock of Schemex for $700,000 cash. For 2006, Schemex reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

Question

_____ On 3/31/06, Ponzico acquired 100% of the outstanding common stock of Schemex for $700,000 cash. For 2006, Schemex reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?

A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

Question

Question

Question

_____ On 9/30/06, Punn issued shares of its voting common stock in exchange for all the outstanding common stock of Sunn in a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company is as follows:

What is the parent's net income for 2006 under the equity method?

What is the parent's net income for 2006 under the equity method?

A) $6,140,000

B) $6,200,000

C) $6,740,000

D) $6,800,000

E) None of the above.

What is the parent's net income for 2006 under the equity method?A) $6,140,000

B) $6,200,000

C) $6,740,000

D) $6,800,000

E) None of the above.

Question

_____ On 9/30/06, Punn issued shares of its voting common stock in exchange for all the outstanding common stock of Sunn in a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company is as follows:

What is the increase in the parent's Retained Earnings account during 2006 as a result of acquiring Sunn?

What is the increase in the parent's Retained Earnings account during 2006 as a result of acquiring Sunn?

A) $140,000

B) $200,000

C) $240,000

D) $300,000

E) None of the above.

What is the increase in the parent's Retained Earnings account during 2006 as a result of acquiring Sunn?A) $140,000

B) $200,000

C) $240,000

D) $300,000

E) None of the above.

Question

_____On 1/1/06, Pylex acquired 100% of Sylex's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional information:

Additional information:

A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

What is the carrying value of the investment at 12/31/06?

A) $500,000

B) $505,000

C) $515,000

D) $530,000

E) None of the above.

Additional information:A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

What is the carrying value of the investment at 12/31/06?

A) $500,000

B) $505,000

C) $515,000

D) $530,000

E) None of the above.

Question

_____ On 1/1/06, Pylex acquired 100% of Sylex's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional information:

Additional information:

A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

The general ledger balance in the Equity in Net Income of Subsidiary account at year-end should be

A)$50,000

B)$55,000

C)$75,000

D)$80,000

E)None of the above.

Additional information:A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

The general ledger balance in the Equity in Net Income of Subsidiary account at year-end should be

A)$50,000

B)$55,000

C)$75,000

D)$80,000

E)None of the above.

Question

_____ On 1/1/06, Pylex acquired 100% of Sylex's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional information:

Additional information:

A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

In preparing the consolidation worksheet at 12/31/06, the Accumulated Depreciation account will be adjusted in total by the following amount:

A)Downward by $44,000.

B)Downward by $39,000.

C)Upward by $5,000.

D)$-0- (no adjustment required).

E)None of the above.

Additional information:A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

In preparing the consolidation worksheet at 12/31/06, the Accumulated Depreciation account will be adjusted in total by the following amount:

A)Downward by $44,000.

B)Downward by $39,000.

C)Upward by $5,000.

D)$-0- (no adjustment required).

E)None of the above.

Question

Question

Question

Question

_____ At a goodwill impairment testing date, the following information exists for an acquired subsidiary that is a reporting unit:

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $700,000. What is the impairment loss to be recognized?

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $700,000. What is the impairment loss to be recognized?

A) $50,000

B) $130,000

C) $150,000

D) $280,000

E) None of the above.

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $700,000. What is the impairment loss to be recognized?A) $50,000

B) $130,000

C) $150,000

D) $280,000

E) None of the above.

Question

_____ At a goodwill impairment testing date, the following information exists for an acquired subsidiary that is a reporting unit:

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $1,000,000. What is the impairment loss to be recognized?

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $1,000,000. What is the impairment loss to be recognized?

A) $ -0-

B) $80,000

C) $180,000

D) $280,000

E) None of the above.

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $1,000,000. What is the impairment loss to be recognized?A) $ -0-

B) $80,000

C) $180,000

D) $280,000

E) None of the above.

Question

Question

Question

Question

Question

Question

_____ On 4/1/06, Pax acquired 80% of Sax's outstanding common stock for $700,000 cash. For 2006, Sax reported the following items:

In addition, Pax recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Invest-ment account at 12/31/06?

In addition, Pax recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Invest-ment account at 12/31/06?

A) $780,000

B) $784,000

C) $800,000

D) $805,000

E) $808,000

In addition, Pax recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Invest-ment account at 12/31/06?A) $780,000

B) $784,000

C) $800,000

D) $805,000

E) $808,000

Question

_____ On 9/30/06, Pittco acquired 75% of Stoneco's outstanding common stock for $600,000 cash. For 2006, Stoneco reported the following items:

In addition, Pittco recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

In addition, Pittco recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

A) $605,000

B) $610,000

C) $620,000

D) $630,000

E) $745,000

In addition, Pittco recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?A) $605,000

B) $610,000

C) $620,000

D) $630,000

E) $745,000

Question

_____ On 5/1/06, Pixco issued shares of its voting common stock in exchange for 60% of Stixco's outstanding common stock as a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company follows:

What is the parent's net income for 2006 under the equity method?

What is the parent's net income for 2006 under the equity method?

A) $8,230,000

B) $8,350,000

C) $8.410,000

D) $8,480,000

E) None of the above.

What is the parent's net income for 2006 under the equity method?A) $8,230,000

B) $8,350,000

C) $8.410,000

D) $8,480,000

E) None of the above.

Question

_____ On 5/1/06, Pixco issued shares of its voting common stock in exchange for 60% of Stixco's outstanding common stock as a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company follows:

What is the increase in the parent's Retained Earnings account during 2006 as a result of owning Stixco?

What is the increase in the parent's Retained Earnings account during 2006 as a result of owning Stixco?

A) $210,000

B) $230,000

C) $280,000

D) $300,000

E) None of the above.

What is the increase in the parent's Retained Earnings account during 2006 as a result of owning Stixco?A) $210,000

B) $230,000

C) $280,000

D) $300,000

E) None of the above.

Question

_____ On 1/1/06, Platt acquired 75% of Slatt's outstanding common stock. The analysis of the Investment account (in thousands) as of that date under the parent company concept follows:

Additional information:

Additional information:

A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the carrying value of the investment at 12/31/06?

A)$896,000

B)$897,000

C)$926,000

D)$927,000

E)None of the above.

Additional information:A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the carrying value of the investment at 12/31/06?

A)$896,000

B)$897,000

C)$926,000

D)$927,000

E)None of the above.

Question

_____ On 1/1/06, Platt acquired 75% of Slatt's outstanding common stock. The analysis of the Investment account (in thousands) as of that date under the parent company concept follows:

Additional information:

Additional information:

A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the parent's general ledger balance in the Equity in Net Income of Subsidiary account at year-end?

A)$72,000

B)$75,000

C)$222,000

D)$225,000

E)None of the above.

Additional information:A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the parent's general ledger balance in the Equity in Net Income of Subsidiary account at year-end?

A)$72,000

B)$75,000

C)$222,000

D)$225,000

E)None of the above.

Question

_____ On 1/1/06, Platt acquired 75% of Slatt's outstanding common stock. The analysis of the Investment account (in thousands) as of that date under the parent company concept follows:

Additional information:

Additional information:

A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

Under the parent company concept, what is the noncontrolling interest reported in the consolidated balance sheet at 12/31/06?

A)$200,000

B)$240,000

C)$249,000

D)$250,000

E)None of the above.

Additional information:A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

Under the parent company concept, what is the noncontrolling interest reported in the consolidated balance sheet at 12/31/06?

A)$200,000

B)$240,000

C)$249,000

D)$250,000

E)None of the above.

Question

_____ On 7/1/06, Pablex acquired 75% of Sablex's outstanding common stock for $180,000 cash. Selected data pertaining to Sablex as of the acquisition date follow:

In the consolidated balance sheet prepared at the acquisition date under the parent company concept, the Patent account would be reported at

In the consolidated balance sheet prepared at the acquisition date under the parent company concept, the Patent account would be reported at

A) $87,000

B) $100,000

C) $112,000

D) $116,000

E) None of the above.

In the consolidated balance sheet prepared at the acquisition date under the parent company concept, the Patent account would be reported atA) $87,000

B) $100,000

C) $112,000

D) $116,000

E) None of the above.

Question

_____ On 7/1/06, Pablex acquired 75% of Sablex's outstanding common stock for $180,000 cash. Selected data pertaining to Sablex as of the acquisition date follow:

The amount reported for goodwill under the parent company concept is

The amount reported for goodwill under the parent company concept is

A) $3,000

B) $15,000

C) $21,000

D) $28,000

E) None of the above.

The amount reported for goodwill under the parent company concept isA) $3,000

B) $15,000

C) $21,000

D) $28,000

E) None of the above.

Question

Question

Question

On 5/1/06, Podex acquired 100% of Sodex's outstanding common stock in a business combination. Both companies have a December 31 year-end. Selected information for each company follows:

Required:

Required:

a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Required:a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Question

On 10/1/06, Plyco issued shares of its voting common stock in exchange for 100% of Slyco's outstanding common stock in a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company follows:

Required:

Required:

a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Required:a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Question

On 1/1/06, Podcom acquired 100% of Sodcom's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional Information:

Additional Information:

a. The subsidiary had net income of $80,000 in 2006.

b. The subsidiary declared dividends of $50,000 in 2006.

c. The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

d. The building has a remaining life of 12 years.

e. The subsidiary's accumulated depreciation at the acquisition date was $44,000.

Required:

Prepare all consolidation entries as of 12/31/06.

Additional Information:a. The subsidiary had net income of $80,000 in 2006.

b. The subsidiary declared dividends of $50,000 in 2006.

c. The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

d. The building has a remaining life of 12 years.

e. The subsidiary's accumulated depreciation at the acquisition date was $44,000.

Required:

Prepare all consolidation entries as of 12/31/06.

Question

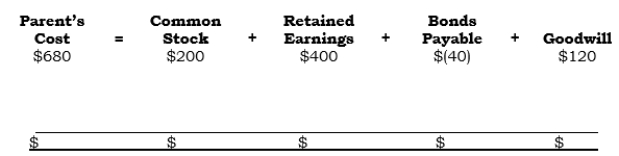

On 1/1/06, Penn acquired 100% of Senn's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional Information:

Additional Information:

a. The subsidiary had net income of $70,000 in 2006.

b. The subsidiary declared dividends of $30,000 in 2006.

c. The subsidiary paid dividends of $20,000 on 10/19/06. (The remaining $10,000 of dividends declared in 2006 was paid on 1/20/07.)

d. The bonds have a remaining life of 5 years.

e. The subsidiary's accumulated depreciation at the acquisition date was $55,000.

Required:

Prepare all consolidation entries as of 12/31/06.

Additional Information:a. The subsidiary had net income of $70,000 in 2006.

b. The subsidiary declared dividends of $30,000 in 2006.

c. The subsidiary paid dividends of $20,000 on 10/19/06. (The remaining $10,000 of dividends declared in 2006 was paid on 1/20/07.)

d. The bonds have a remaining life of 5 years.

e. The subsidiary's accumulated depreciation at the acquisition date was $55,000.

Required:

Prepare all consolidation entries as of 12/31/06.

Question

COMPREHENSIVE

On 7/1/06, PBM Company acquired 100% of the outstanding common stock of Sapple Company by issuing 6,000 shares of its $10 par value common stock (which was trading at $70 per share on that date). In addition, PBM incurred direct costs of $90,000 relating to the acquisition, $40,000 of which was for the registration of the shares issued with the SEC. Selected relevant data follows:

Required:

Required:

a. Prepare the entry to record the business combination on 7/1/06.

b. Complete the PBM Company and Sapple Company columns of the consolidation worksheet on the following page.

c. Prepare the consolidation entries at 12/31/06.

d. Post the consolidation entries in Requirement c to the following consolidation worksheet, and complete the worksheet.

On 7/1/06, PBM Company acquired 100% of the outstanding common stock of Sapple Company by issuing 6,000 shares of its $10 par value common stock (which was trading at $70 per share on that date). In addition, PBM incurred direct costs of $90,000 relating to the acquisition, $40,000 of which was for the registration of the shares issued with the SEC. Selected relevant data follows:

Required:a. Prepare the entry to record the business combination on 7/1/06.

b. Complete the PBM Company and Sapple Company columns of the consolidation worksheet on the following page.

c. Prepare the consolidation entries at 12/31/06.

d. Post the consolidation entries in Requirement c to the following consolidation worksheet, and complete the worksheet.

Question

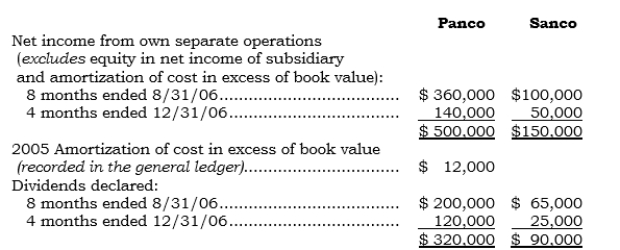

On 9/1/06, Panco acquired 80% of Sanco's outstanding common stock. Both entities have December 31 year-ends. Selected data for each of the companies for 2006 follow:

Required:

Required:

a. Determine the consolidated net income to be reported for 2006 under the parent company concept.

b. Compute the noncontrolling interest deduction for 2006 under the parent company concept.

c. Determine the amount of dividends to be reported in the consolidated statement of retained earnings for 2006.

d. Determine the consolidated net income for 2006 under the economic unit concept.

Required:a. Determine the consolidated net income to be reported for 2006 under the parent company concept.

b. Compute the noncontrolling interest deduction for 2006 under the parent company concept.

c. Determine the amount of dividends to be reported in the consolidated statement of retained earnings for 2006.

d. Determine the consolidated net income for 2006 under the economic unit concept.

Question

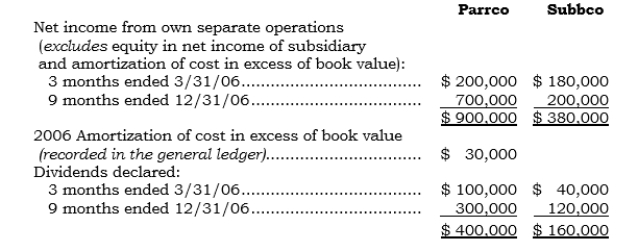

On 4/1/06, Parrco acquired 60% of Subbco's outstanding common stock. Both entities have December 31 year-ends. Selected data for each company for 2006 follow:

Required:

Required:

a. Determine the consolidated net income to be reported for 2006 under the parent company concept.

b. Compute the noncontrolling interest deduction for 2006 under the parent company concept.

c. Determine the amount of dividends to be reported in the consolidated statement of retained earnings for 2006.

d. Determine the consolidated net income for 2006 under the economic unit concept.

Required:a. Determine the consolidated net income to be reported for 2006 under the parent company concept.

b. Compute the noncontrolling interest deduction for 2006 under the parent company concept.

c. Determine the amount of dividends to be reported in the consolidated statement of retained earnings for 2006.

d. Determine the consolidated net income for 2006 under the economic unit concept.

Question

Pyna acquired 75% of Syna's outstanding common stock for $180,000 cash. Selected data pertaining to Syna as of the acquisition date follow:

Required:

Required:

Prepare an analysis of the Investment account by the components of the major conceptual elements using the parent company concept.

Required:Prepare an analysis of the Investment account by the components of the major conceptual elements using the parent company concept.

Question

Pimex acquired 80% of Simex's outstanding common stock for $250,000 cash. Selected data pertaining to Simex as of the acquisition date follow:

Required:

Required:

Prepare an analysis of the Investment account by the individual components of the major conceptual elements using the parent company concept.

Required:Prepare an analysis of the Investment account by the individual components of the major conceptual elements using the parent company concept.

Question

On 5/1/06, Pozco acquired 75% of Sozco's outstanding common stock for $550,000 cash. (On 4/30/06, Sozco's assets and liabilities had book values of $2,000,000 and $1,560,000 respectively.) A conceptual analysis of the Invest-ment account as of 5/1/06 under the parent company concept follows:

Required:

a. Determine the amounts at which the land and goodwill would be reported in the consolidated financial statements under the parent company concept.

a. Determine the amounts at which the land and goodwill would be reported in the consolidated financial statements under the parent company concept.

b. Determine the amounts at which the land and goodwill would be reported in the consolidated financial statements under the economic unit concept.

c. Determine the dollar amount differences between the noncontrolling interest reported in the balance sheet under the parent company concept versus under the economic unit concept.

Required:

a. Determine the amounts at which the land and goodwill would be reported in the consolidated financial statements under the parent company concept.b. Determine the amounts at which the land and goodwill would be reported in the consolidated financial statements under the economic unit concept.

c. Determine the dollar amount differences between the noncontrolling interest reported in the balance sheet under the parent company concept versus under the economic unit concept.

Question

Question

Question

Punda purchased two blocks of stock of Sunda. Information concerning these purchases follows:

Required:

Required:

a. Analyze the Investment account as of 1/1/05, and update it through 5/1/05. Use the parent company concept.

b. Prepare all consolidation entries at 5/1/05.

Required:a. Analyze the Investment account as of 1/1/05, and update it through 5/1/05. Use the parent company concept.

b. Prepare all consolidation entries at 5/1/05.

Question

On 7/1/06, PDQ acquired 80% of Sprint's outstanding common stock by issuing 8,000 shares of its $5 par value common stock (which was trading at $60 per share on that date). In addition, PDQ incurred direct costs of $100,000 relating to the acquisition, $60,000 of which was for the registration of the shares issued with the SEC. Selected relevant data follow:

Additional Information:

Additional Information:

Additional Information:

a. The non-push-down basis of accounting was selected.

b. The equity method of accounting is to be used.

c. During 2006, PDQ declared and paid $80,000 of dividends each quarter. Also, PDQ reported a net income of $200,000 for the 6 months ended 6/30/06.

d. For 2006, Sprint had the following earnings and dividends:

Required:

Required:

a. Prepare the entry to record the business combination on 7/1/06.

b. Complete the PDQ and Sprint Company columns of the following consolidation worksheet.

c. Prepare all the consolidation entries.

d. Post the consolidation entries in Requirement c to the consolidation worksheet and complete the worksheet.

Additional Information:Additional Information:

a. The non-push-down basis of accounting was selected.

b. The equity method of accounting is to be used.

c. During 2006, PDQ declared and paid $80,000 of dividends each quarter. Also, PDQ reported a net income of $200,000 for the 6 months ended 6/30/06.

d. For 2006, Sprint had the following earnings and dividends:

Required:a. Prepare the entry to record the business combination on 7/1/06.

b. Complete the PDQ and Sprint Company columns of the following consolidation worksheet.

c. Prepare all the consolidation entries.

d. Post the consolidation entries in Requirement c to the consolidation worksheet and complete the worksheet.

Question

At a postacquisition impairment evaluation date, the following information exists for an acquired subsidiary that is a reporting unit:

Required

Required

a. What is the implied fair value of goodwill?

b. What is the impairment loss to be recognized, if any?

c. Prepare the parent's appropriate adjusting entry, if necessary. (Assume that the parent had acquired common stock and used non-push-down accounting.)

d. If an impairment evaluation is performed one year later and the goodwill's implied fair value is $200,000 at that date, what adjusting entry would be made by the parent?

Requireda. What is the implied fair value of goodwill?

b. What is the impairment loss to be recognized, if any?

c. Prepare the parent's appropriate adjusting entry, if necessary. (Assume that the parent had acquired common stock and used non-push-down accounting.)

d. If an impairment evaluation is performed one year later and the goodwill's implied fair value is $200,000 at that date, what adjusting entry would be made by the parent?

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/74

Play

Full screen (f)

Deck 6: The Purchase Method: Postacquisition Periods and Partial Ownerships

1

When an acquired subsidiary declares dividends in excess of the subsidiary's retained earnings balance at the acquisition date, the excess amount is called a ______________________________ dividend.

liquidating

2

When testing goodwill for possible impairment, the goodwill's book value is compared with the goodwill's _____________________________ fair value.

implied

3

Under the _____________________________________ concept, assets of an acquired subsidiary are revalued in consolidation to their current values only to the extent that such undervaluation is paid for by the parent company.

parent company

4

Under the _____________________________________ concept, assets of an acquired subsidiary are revalued in consolidation to 100% of their current values at the combination date.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

5

The equity method would not be used when the target company's assets were acquired.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

6

Under the equity method, amortization of cost in excess of book value is recorded in the consolidation process.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

7

Under the equity method, amortization of cost in excess of book value is recorded in the parent's general ledger.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

8

Under the equity method, no distinction need be made as to whether an acquired subsidiary's dividends are liquidating or nonliquidating.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

9

From the parent's perspective, the true earnings of an acquired subsidiary can be determined using the equity method-the push-down basis of accounting is not needed to make this determination.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

10

In testing goodwill for possible impairment, the fair value of the reporting unit's unrecognized intangible assets is ignored.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

11

In testing goodwill for possible impairment, the goodwill's book value is compared with the goodwill's implied fair value-but only if the reporting unit's carrying value exceeds the reporting unit's estimated fair value.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

12

In testing goodwill for possible impairment, the goodwill's book value is compared with the goodwill's implied fair value-regardless whether the reporting unit's estimated fair value exceeds the reporting unit's carrying value.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

13

In periods subsequent to a goodwill impairment write-down, the goodwill may be written back up up to the goodwill's initially recorded amount if the goodwill has recovered in value.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

14

In periods subsequent to a goodwill impairment write-down, the goodwill may not be written back up up to the goodwill's initially recorded amount if the goodwill has recovered in value.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

15

Under the parent company concept, the subsidiary's undervalued assets are revalued to 100% of their current values for consolidated reporting purposes.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

16

Under the economic unit concept, the subsidiary's undervalued assets are revalued upward only to the extent that such undervaluation was bought and paid for by the parent.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

17

Under the parent company concept, goodwill is reported at an imputed amount.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

18

Under the "pure" form of the economic unit concept, goodwill is reported at an imputed amount-not at the amount bought and paid for by the parent.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

19

_____ When a parent company uses the equity method in accounting for its investment in a subsidiary, which of the following affects the parent's reported investment income?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

20

_____ When a parent company uses the cost method in accounting for its investment in a subsidiary, which of the following affects the parent's reported investment income?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

21

_____ A subsidiary declares a liquidating cash dividend. The Investment in Subsidiary account would be credited under which of the following accounting methods?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

22

_____ A subsidiary declares a nonliquidating cash dividend. What is the effect of this declaration on the parent's Retained Earnings account under each of the following accounting methods?

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

23

_____ The consolidated income statement amounts are the same

A) Whether the cost method or the equity method is used by the parent company.

B) Whether all of the target company's common stock is acquired or all of the target company' assets are acquired.

C) In both a and b.

D) In neither a nor b.

A) Whether the cost method or the equity method is used by the parent company.

B) Whether all of the target company's common stock is acquired or all of the target company' assets are acquired.

C) In both a and b.

D) In neither a nor b.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

24

_____ For a 60% ownership situation in which the parent paid an amount for goodwill, which of the following methods would report the highest amount for goodwill?

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

A) The parent company concept.

B) The economic unit concept.

C) Proportional consolidation.

D) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

25

_____ Which of the following concepts or approaches assigns a portion of the parent's amortization of cost in excess of book value (as recorded on the parent's books under the equity method) against the NCI in the subsidiary's net income?

A) The parent company concept.

B) The economic unit concept.

C) The proportional consolidation approach.

D) None of the above.

A) The parent company concept.

B) The economic unit concept.

C) The proportional consolidation approach.

D) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

26

_____ On 7/1/06, Payco acquired 100% of Sayco's outstanding common stock when its Retained Earnings were $200,000. For the six months ended 12/31/06, Sayco reported net income of $50,000 and declared dividends of $60,000. Under the equity method, what amount should the parent report in its 2006 income statement?

A) $ -0-

B) $10,000

C) $50,000

D) $60,000

A) $ -0-

B) $10,000

C) $50,000

D) $60,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

27

On 7/1/06, Pynco acquired 100% of Synco's outstanding common stock when its retained earnings were $200,000. For the six months ended 12/31/06, Synco reported net income of $50,000 and declared dividends of $60,000. Under the cost method, what amount should the parent report in its 2006 income statement?

A) $ -0-

B) $10,000

C)$50,000

D) $60,000

A) $ -0-

B) $10,000

C)$50,000

D) $60,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

28

_____ On 4/1/06, Pullco acquired 100% of Strapco's outstanding common stock for $500,000 cash. For 2006, Strapco reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

29

_____ On 4/1/06, Pullco acquired 100% of Strapco's outstanding common stock for $500,000 cash. For 2006, Strapco reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?.

A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

In addition, amortization of cost in excess of book value for 2006 was $20,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?.A) $500,000

B) $540,000

C) $550,000

D) $570,000

E) $630,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

30

_____ On 3/31/06, Ponzico acquired 100% of the outstanding common stock of Schemex for $700,000 cash. For 2006, Schemex reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

31

_____ On 3/31/06, Ponzico acquired 100% of the outstanding common stock of Schemex for $700,000 cash. For 2006, Schemex reported the following items:

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?

A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

In addition, amortization of cost in excess of book value for 2006 was $30,000. Assume non-push-down accounting is used. Under the cost method, what is the carrying value of the Investment account at 12/31/06?A) $660,000

B) $670,000

C) $690,000

D) $700,000

E) $870,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

32

_____ On 1/1/06, Pax acquired 100% of Sax's outstanding common stock. For 2005, Sax reported $200,000 of net income and declared dividends of $150,000. Amortization of cost in excess of book value for 2006 was $20,000. Pax opted to use (1) the equity method of accounting and (2) non-push-down accounting. What are Sax's true earnings for 2006 from Pax's perspective?

A) $130,000

B) $150,000

C) $180,000

D) $200,000

E) $330,000

A) $130,000

B) $150,000

C) $180,000

D) $200,000

E) $330,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

33

_____ On 1/1/06, Poxx acquired 100% of Soxx's outstanding common stock. For 2006, Soxx reported $200,000 of net income and declared dividends of $150,000. Amortization of cost in excess of book value for 2006 was $20,000. Poxx opted to use (1) the cost method and (2) non-push-down accounting. What are Soxx's true earnings for 2006 from Poxx's perspective?

A) $130,000

B) $150,000

C) $180,000

D) $200,000

E) $330,000

A) $130,000

B) $150,000

C) $180,000

D) $200,000

E) $330,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

34

_____ On 9/30/06, Punn issued shares of its voting common stock in exchange for all the outstanding common stock of Sunn in a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company is as follows:

What is the parent's net income for 2006 under the equity method?

A) $6,140,000

B) $6,200,000

C) $6,740,000

D) $6,800,000

E) None of the above.

What is the parent's net income for 2006 under the equity method?A) $6,140,000

B) $6,200,000

C) $6,740,000

D) $6,800,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

35

_____ On 9/30/06, Punn issued shares of its voting common stock in exchange for all the outstanding common stock of Sunn in a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company is as follows:

What is the increase in the parent's Retained Earnings account during 2006 as a result of acquiring Sunn?

A) $140,000

B) $200,000

C) $240,000

D) $300,000

E) None of the above.

What is the increase in the parent's Retained Earnings account during 2006 as a result of acquiring Sunn?A) $140,000

B) $200,000

C) $240,000

D) $300,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

36

_____On 1/1/06, Pylex acquired 100% of Sylex's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional information:

A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

What is the carrying value of the investment at 12/31/06?

A) $500,000

B) $505,000

C) $515,000

D) $530,000

E) None of the above.

Additional information:A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

What is the carrying value of the investment at 12/31/06?

A) $500,000

B) $505,000

C) $515,000

D) $530,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

37

_____ On 1/1/06, Pylex acquired 100% of Sylex's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional information:

A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

The general ledger balance in the Equity in Net Income of Subsidiary account at year-end should be

A)$50,000

B)$55,000

C)$75,000

D)$80,000

E)None of the above.

Additional information:A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

The general ledger balance in the Equity in Net Income of Subsidiary account at year-end should be

A)$50,000

B)$55,000

C)$75,000

D)$80,000

E)None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

38

_____ On 1/1/06, Pylex acquired 100% of Sylex's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional information:

A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

In preparing the consolidation worksheet at 12/31/06, the Accumulated Depreciation account will be adjusted in total by the following amount:

A)Downward by $44,000.

B)Downward by $39,000.

C)Upward by $5,000.

D)$-0- (no adjustment required).

E)None of the above.

Additional information:A.The subsidiary had net income of $80,000 in 2006.

B.The subsidiary declared dividends of $50,000 in 2006.

C.The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

D.The building has a remaining life of 12 years.

E.The subsidiary's accumulated depreciation at the acquisition date was $44,000.

F.The parent uses the equity method of accounting.

In preparing the consolidation worksheet at 12/31/06, the Accumulated Depreciation account will be adjusted in total by the following amount:

A)Downward by $44,000.

B)Downward by $39,000.

C)Upward by $5,000.

D)$-0- (no adjustment required).

E)None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

39

_____ At a goodwill impairment testing date, a reporting unit's fair value (including unrecognized intangible assets of $90,000) is $1,000,000 ($200,000 below its carrying value). If goodwill's carrying value is $400,000 and its implied fair value is $330,000, what is the impairment loss to be recognized?

A) $ -0-

B) $70,000

C) $160,000

D) $200,000

E) $400,000

A) $ -0-

B) $70,000

C) $160,000

D) $200,000

E) $400,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

40

_____ At a goodwill impairment testing date, a reporting unit's fair value (including unrecognized intangible assets of $300,000) is $3,000,000 ($200,000 above its carrying value). If goodwill's carrying value is $1,000,000 and its implied fair value is $911,000, what is the impairment loss to be recognized?

A) $ -0-

B) $89,000

C) $189,000

D) $389,000

E) None of the above.

A) $ -0-

B) $89,000

C) $189,000

D) $389,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

41

_____ At a goodwill impairment testing date, a reporting unit's fair value (including unrecognized intangible assets of $100,000) is $5,000,000 ($60,000 below its carrying value). If goodwill's carrying value is $2,000,000 and its implied fair value is $1,800,000, what is the impairment loss to be recognized?

A) $ -0-

B) $60,000

C) $160,000

D) $200,000

E) None of the above.

A) $ -0-

B) $60,000

C) $160,000

D) $200,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

42

_____ At a goodwill impairment testing date, the following information exists for an acquired subsidiary that is a reporting unit:

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $700,000. What is the impairment loss to be recognized?

A) $50,000

B) $130,000

C) $150,000

D) $280,000

E) None of the above.

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $700,000. What is the impairment loss to be recognized?A) $50,000

B) $130,000

C) $150,000

D) $280,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

43

_____ At a goodwill impairment testing date, the following information exists for an acquired subsidiary that is a reporting unit:

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $1,000,000. What is the impairment loss to be recognized?

A) $ -0-

B) $80,000

C) $180,000

D) $280,000

E) None of the above.

The reporting unit's estimated fair value (determined by discounting estimated future cash inflows) is $1,000,000. What is the impairment loss to be recognized?A) $ -0-

B) $80,000

C) $180,000

D) $280,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

44

_____ On 4/1/06, Patz acquired 90% of Satz's outstanding common stock for $500,000 cash. For 2006, Satz reported $30,000 of net income each quarter and declared dividends of $10,000 each quarter. Also for 2006, Patz recorded $10,000 of amortization of cost in excess of book value in its general ledger.

What should be the carrying value of Patz's investment under the equity method at 12/31/06?

A) $544,000

B) $545,000

C) $562,000

D) $563,000

E) $571,000

What should be the carrying value of Patz's investment under the equity method at 12/31/06?

A) $544,000

B) $545,000

C) $562,000

D) $563,000

E) $571,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

45

_____ On 4/1/06, Patz acquired 90% of Satz's outstanding common stock for $500,000 cash. For 2006, Satz reported $30,000 of net income each quarter and declared dividends of $10,000 each quarter. Also for 2006, Patz recorded $10,000 of amortization of cost in excess of book value in its general ledger.

What amount appears in Patz's 2006 income statement if it accounts for its investment in Satz under the equity method?

A) $17,000

B) $27,000

C) $71,000

D) $72,000

E) $81,000

What amount appears in Patz's 2006 income statement if it accounts for its investment in Satz under the equity method?

A) $17,000

B) $27,000

C) $71,000

D) $72,000

E) $81,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

46

_____ On 6/1/06, Piner acquired 80% of Siner's outstanding common stock for $800,000 cash. On this date, Siner had (a) net assets that had book value of $750,000 and (b) land that had a book value of $300,000 and a current value of $400,000. Goodwill paid for was calculated to be $120,000. At what amount would Siner's land be reported in the consolidated balance sheet at 6/1/06 under the parent company concept?

A) $300,000

B) $320,000

C) $340,000

D) $380,000

E) $400,000

A) $300,000

B) $320,000

C) $340,000

D) $380,000

E) $400,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

47

_____ On 7/1/06, Pane acquired 60% of Sill's outstanding common stock for $480,000 cash. The book value of Sill's net assets is $500,000. Sill's only over-or undervalued asset or liability is a building that has a book value of $700,000 and a current value of $900,000. The building has a remaining life of 10 years.

Under the parent company concept, at what amount would the noncontrolling interest be reported in the consolidated balance sheet at 7/1/06?

A) $200,000

B) $240,000

C) $280,000

D) $320,000

E) None of the above.

Under the parent company concept, at what amount would the noncontrolling interest be reported in the consolidated balance sheet at 7/1/06?

A) $200,000

B) $240,000

C) $280,000

D) $320,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

48

_____ On 7/1/06, Pane acquired 60% of Sill's outstanding common stock for $480,000 cash. The book value of Sill's net assets is $500,000. Sill's only over-or undervalued asset or liability is a building that has a book value of $700,000 and a current value of $900,000. The building has a remaining life of 10 years. Sill reported $150,000 of postacquisition net income for 2006 and declared dividends of $100,000 in 2006 after the acquisition date.

Under the parent company concept, at what amount would the noncontrolling interest be reported in the consolidated balance sheet at 12/31/06?

A) $200,000

B) $212,000

C) $216,000

D) $220,000

E) None of the above.

Under the parent company concept, at what amount would the noncontrolling interest be reported in the consolidated balance sheet at 12/31/06?

A) $200,000

B) $212,000

C) $216,000

D) $220,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

49

_____ On 4/1/06, Pax acquired 80% of Sax's outstanding common stock for $700,000 cash. For 2006, Sax reported the following items:

In addition, Pax recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Invest-ment account at 12/31/06?

A) $780,000

B) $784,000

C) $800,000

D) $805,000

E) $808,000

In addition, Pax recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Invest-ment account at 12/31/06?A) $780,000

B) $784,000

C) $800,000

D) $805,000

E) $808,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

50

_____ On 9/30/06, Pittco acquired 75% of Stoneco's outstanding common stock for $600,000 cash. For 2006, Stoneco reported the following items:

In addition, Pittco recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?

A) $605,000

B) $610,000

C) $620,000

D) $630,000

E) $745,000

In addition, Pittco recorded amortization of cost in excess of book value in its general ledger for 2006 of $20,000. Assume non-push-down accounting is used. Under the equity method, what is the carrying value of the Investment account at 12/31/06?A) $605,000

B) $610,000

C) $620,000

D) $630,000

E) $745,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

51

_____ On 5/1/06, Pixco issued shares of its voting common stock in exchange for 60% of Stixco's outstanding common stock as a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company follows:

What is the parent's net income for 2006 under the equity method?

A) $8,230,000

B) $8,350,000

C) $8.410,000

D) $8,480,000

E) None of the above.

What is the parent's net income for 2006 under the equity method?A) $8,230,000

B) $8,350,000

C) $8.410,000

D) $8,480,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

52

_____ On 5/1/06, Pixco issued shares of its voting common stock in exchange for 60% of Stixco's outstanding common stock as a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company follows:

What is the increase in the parent's Retained Earnings account during 2006 as a result of owning Stixco?

A) $210,000

B) $230,000

C) $280,000

D) $300,000

E) None of the above.

What is the increase in the parent's Retained Earnings account during 2006 as a result of owning Stixco?A) $210,000

B) $230,000

C) $280,000

D) $300,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

53

_____ On 1/1/06, Platt acquired 75% of Slatt's outstanding common stock. The analysis of the Investment account (in thousands) as of that date under the parent company concept follows:

Additional information:

A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the carrying value of the investment at 12/31/06?

A)$896,000

B)$897,000

C)$926,000

D)$927,000

E)None of the above.

Additional information:A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the carrying value of the investment at 12/31/06?

A)$896,000

B)$897,000

C)$926,000

D)$927,000

E)None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

54

_____ On 1/1/06, Platt acquired 75% of Slatt's outstanding common stock. The analysis of the Investment account (in thousands) as of that date under the parent company concept follows:

Additional information:

A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the parent's general ledger balance in the Equity in Net Income of Subsidiary account at year-end?

A)$72,000

B)$75,000

C)$222,000

D)$225,000

E)None of the above.

Additional information:A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

What is the parent's general ledger balance in the Equity in Net Income of Subsidiary account at year-end?

A)$72,000

B)$75,000

C)$222,000

D)$225,000

E)None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

55

_____ On 1/1/06, Platt acquired 75% of Slatt's outstanding common stock. The analysis of the Investment account (in thousands) as of that date under the parent company concept follows:

Additional information:

A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

Under the parent company concept, what is the noncontrolling interest reported in the consolidated balance sheet at 12/31/06?

A)$200,000

B)$240,000

C)$249,000

D)$250,000

E)None of the above.

Additional information:A.Slatt had net income of $300,000 in 2006.

B.Slatt declared dividends of $100,000 in 2006.

C.Slatt paid dividends of $60,000 on 12/23/06. (The remaining $40,000 of dividends declared in 2006 was paid on 1/10/07.)

D.Platt uses the equity method of accounting.

E.The undervalued equipment has a 10-yr. remaining life.

Under the parent company concept, what is the noncontrolling interest reported in the consolidated balance sheet at 12/31/06?

A)$200,000

B)$240,000

C)$249,000

D)$250,000

E)None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

56

_____ On 7/1/06, Pablex acquired 75% of Sablex's outstanding common stock for $180,000 cash. Selected data pertaining to Sablex as of the acquisition date follow:

In the consolidated balance sheet prepared at the acquisition date under the parent company concept, the Patent account would be reported at

A) $87,000

B) $100,000

C) $112,000

D) $116,000

E) None of the above.

In the consolidated balance sheet prepared at the acquisition date under the parent company concept, the Patent account would be reported atA) $87,000

B) $100,000

C) $112,000

D) $116,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

57

_____ On 7/1/06, Pablex acquired 75% of Sablex's outstanding common stock for $180,000 cash. Selected data pertaining to Sablex as of the acquisition date follow:

The amount reported for goodwill under the parent company concept is

A) $3,000

B) $15,000

C) $21,000

D) $28,000

E) None of the above.

The amount reported for goodwill under the parent company concept isA) $3,000

B) $15,000

C) $21,000

D) $28,000

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

58

_____ Use the information in the second preceding question. Assume that for 2006, the subsidiary reported postacquisition net income of $40,000 and postacquisition dividends declared of $12,000. Also, the parent charged $3,000 of amortization of cost in excess of book value to its Equity in Net Income account in 2006. In the 12/31/06 consolidated balance sheet, the noncontrolling interest under the parent company concept would be reported at

A) $35,000

B) $42,000

C) $47,000

D) $59,000

E) $66,000

A) $35,000

B) $42,000

C) $47,000

D) $59,000

E) $66,000

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

59

_____ On 1/1/06, Pongo acquired 66 2/3% of Songo's outstanding common stock for $500,000 cash. On 1/2/06 (one day later), Songo declared and paid a cash dividend of $150,000 (as instructed by Pongo). For 2006, Songo reported $240,000 of net income. For 2006, Pongo had no amortization of cost in excess of book value. What did the parent earn on its investment in 2006?

A) 20% ($100,000/$500,000)

B) 32% ($160,000/$500,000)

C) 25% ($100,000/$400,000)

D) 40% ($160,000/$400,000)

E) None of the above.

A) 20% ($100,000/$500,000)

B) 32% ($160,000/$500,000)

C) 25% ($100,000/$400,000)

D) 40% ($160,000/$400,000)

E) None of the above.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

60

On 5/1/06, Podex acquired 100% of Sodex's outstanding common stock in a business combination. Both companies have a December 31 year-end. Selected information for each company follows:

Required:

a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Required:a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

61

On 10/1/06, Plyco issued shares of its voting common stock in exchange for 100% of Slyco's outstanding common stock in a business combination appropriately accounted for under the purchase method. Both companies have a December 31 year-end. Selected information for each company follows:

Required:

a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Required:a. Determine the parent's net income for 2006 under the equity method.

b. Determine the parent's net income for 2006 under the cost method.

c. Determine the consolidated net income for 2006.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

62

On 1/1/06, Podcom acquired 100% of Sodcom's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional Information:

a. The subsidiary had net income of $80,000 in 2006.

b. The subsidiary declared dividends of $50,000 in 2006.

c. The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

d. The building has a remaining life of 12 years.

e. The subsidiary's accumulated depreciation at the acquisition date was $44,000.

Required:

Prepare all consolidation entries as of 12/31/06.

Additional Information:a. The subsidiary had net income of $80,000 in 2006.

b. The subsidiary declared dividends of $50,000 in 2006.

c. The subsidiary paid dividends of $35,000 on 11/11/06. (The remaining $15,000 of dividends declared in 2006 was paid on 1/15/07.)

d. The building has a remaining life of 12 years.

e. The subsidiary's accumulated depreciation at the acquisition date was $44,000.

Required:

Prepare all consolidation entries as of 12/31/06.

Unlock Deck

Unlock for access to all 74 flashcards in this deck.

Unlock Deck

k this deck

63

On 1/1/06, Penn acquired 100% of Senn's outstanding common stock. The analysis of the Investment account (in thousands) as of that date follows:

Additional Information:

a. The subsidiary had net income of $70,000 in 2006.

b. The subsidiary declared dividends of $30,000 in 2006.

c. The subsidiary paid dividends of $20,000 on 10/19/06. (The remaining $10,000 of dividends declared in 2006 was paid on 1/20/07.)

d. The bonds have a remaining life of 5 years.

e. The subsidiary's accumulated depreciation at the acquisition date was $55,000.

Required:

Prepare all consolidation entries as of 12/31/06.

Additional Information:a. The subsidiary had net income of $70,000 in 2006.

b. The subsidiary declared dividends of $30,000 in 2006.