Deck 2: Wholly Owned Subsidiaries: Postcreation Periods

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

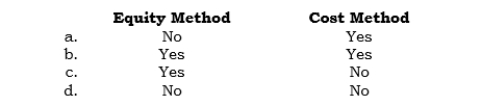

_____ The Dividend Income account would be used in which of the following accounting methods?

Question

Question

Question

Question

Question

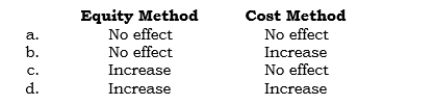

_____ A subsidiary declared a cash dividend. What is the ultimate effect of this declaration on the parent's retained earnings account-not the consolidated retained earnings-under each of the following methods?

Question

Question

Question

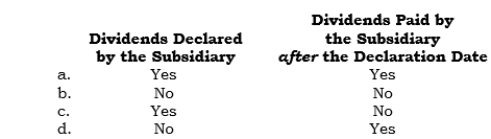

_____ When a parent company uses the equity method of accounting for its investment in a subsidiary, which of the following affects the parent's retained earnings?

Question

_____ When a parent company uses the cost method of accounting for its investment in a subsidiary, which of the following affects the parent's retained earnings?

Question

Question

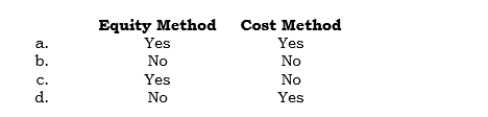

Question

Question

Question

Question

Question

Question

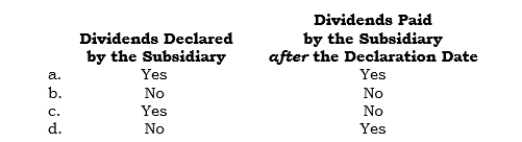

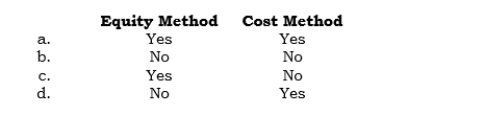

_____ When a parent-subsidiary relationship exists, the Dividend Income account is reported in the consolidated income statement under which of the following accounting methods?

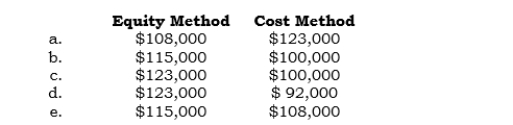

Question

_____ Dividends declared by a subsidiary are reported currently in the parent's separate income statement and in the consolidated income statement under the

Question

Question

Question

Question

Question

Question

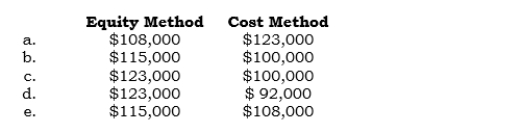

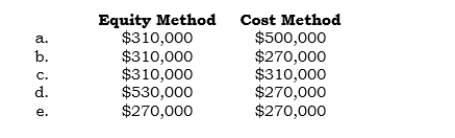

_____ On 4/1/06, Pix Inc. formed Stix Inc., investing $100,000 cash. For 2004, Stix reported net income of $23,000 and declared and paid cash dividends of $8,000. What is Pix's carrying value of its investment in Stix at 12/31/06 under each of the following methods?

Question

_____ On 4/1/06, Pix Inc. formed Stix Inc., investing $100,000 cash. For 2006, Stix reported net income of $23,000 and declared cash dividends of $8,000 (which were paid 1/2/07). What is Pix's carrying value of its investment in Stix at 12/31/06?

Question

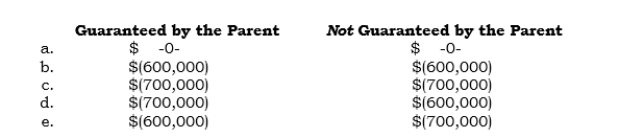

_____ On 5/1/05, Pax Inc. created Sax Inc., investing $500,000 cash. Sax reported a highly unexpected $230,000 loss for 2005 and a $40,000 profit for 2006. The 2005 loss created substantial doubt as to (a) the ability of the subsidiary to survive and (b) the ability of the parent to sell the subsidiary at other than an amount substantially below its initial investment. What should the carrying value of Pax's investment in Sax be at 12/31/06 under each of the following methods?

Question

_____ On 1/1/06, the carrying value of Plano Company's investment in its 100%-owned created subsidiary, Slano, was $600,000. During 2006, Slano reported a loss of $700,000. Under the equity method, what amount should be reported in Plano's separate income statement for 2006, relating to its investment in Slano, if Slano's debt is

Question

Question

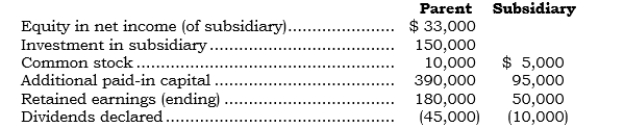

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at the end of 2006?

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at the end of 2006?

A) Debit of $17,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at the end of 2006?A) Debit of $17,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

Question

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (2001) at the end of 2006:

The subsidiary's retained earnings at 12/31/05 were $27,000. What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

The subsidiary's retained earnings at 12/31/05 were $27,000. What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

A) Debit of $10,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

The subsidiary's retained earnings at 12/31/05 were $27,000. What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?A) Debit of $10,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

Question

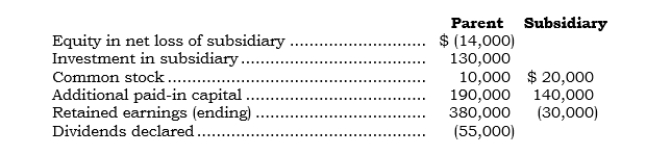

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

Question

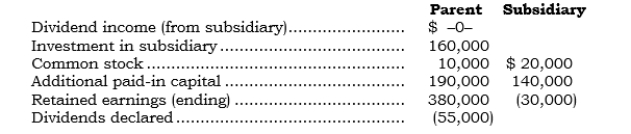

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

The subsidiary's retained earnings at 12/31/05 were $(16,000). What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

The subsidiary's retained earnings at 12/31/05 were $(16,000). What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

The subsidiary's retained earnings at 12/31/05 were $(16,000). What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

Question

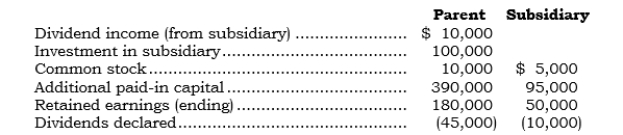

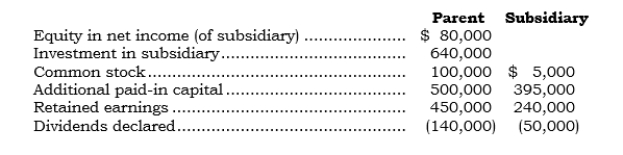

_____ The following accounts were taken from the separate company financial statements of a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

What amount should be reported for consolidated retained earnings at the end of 2006?

What amount should be reported for consolidated retained earnings at the end of 2006?

A) $450,000

B) $480,000

C) $530,000

D) $690,000

E) None of the above.

What amount should be reported for consolidated retained earnings at the end of 2006?A) $450,000

B) $480,000

C) $530,000

D) $690,000

E) None of the above.

Question

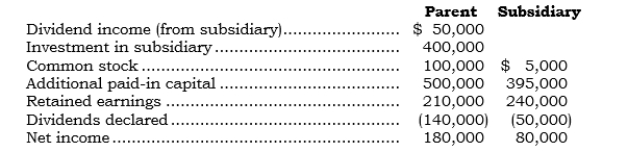

_____ The following accounts or amounts were taken from the separate company financial statements of a parent and its 100%-owned subsidiary (created in 2006) at the end of 2006:

What amount should be reported for consolidated retained earnings at the end of 2006?

What amount should be reported for consolidated retained earnings at the end of 2006?

A) $210,000

B) $240,000

C) $290,000

D) $450,000

E) None of the above.

What amount should be reported for consolidated retained earnings at the end of 2006?A) $210,000

B) $240,000

C) $290,000

D) $450,000

E) None of the above.

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/110

Play

Full screen (f)

Deck 2: Wholly Owned Subsidiaries: Postcreation Periods

1

The two methods of accounting for an investment in a subsidiary are the _______________________ method and the ______________________________ method.

equity, cost

2

The conceptually correct method of accounting for an investment in a subsidiary is the ___________________________________________________ method.

equity

3

A parent that uses the accrual basis for income tax-reporting purposes will pay U.S. income taxes on a subsidiary's earnings when the subsidiary ________________________________________.

declares dividends

4

Under the equity method of accounting, the parent's investment income is appropriately described in the parent's income statement using the account ________________________________________.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

5

Under the cost method of accounting, the parent's investment income is appropriately described in the parent's income statement using the account ________________________________________.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

6

Under the equity method, all dividends declared by the subsidiary are treated as a(n) ________________________________________ of the parent's investment.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

7

The equity method reflects the _________________________________________ of the subsidiary.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

8

The difference between the carrying value of the investment under the equity method and under the cost method pertains to the subsidiary's _______________________________________.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

9

A company that has no operations of its own-only investments in other companies that have operations-is called a(n) ________________________________.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

10

Financial statements of the parent that are presented in certain circumstances in notes to the consolidated statements are called ___________________________ statements.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

11

To use the equity method of accounting for an unconsolidated subsidiary, the parent must have __________________________________.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

12

The equity method is sometimes referred to as a(n) __________________________.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

13

Under the equity method, a subsidiary's earnings are effectively treated as an additional capital investment by the parent.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

14

Under the equity method, all dividends (except stock dividends) declared by the subsidiary are treated as a liquidation of the investment.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

15

Under the equity method, the declaration of dividends-not the cash payment of dividends-results in changing the carrying value of the investment.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

16

Under the equity method, the carrying value of the investment represents the market value of the common stock holding.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

17

When a subsidiary declares a dividend that is more than the subsidiary's net income for that year, the consolidated net income will not equal the parent's net income under the equity method.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

18

When the parent is not obligated to invest additional funds in a subsidiary that is reporting losses, the parent stops applying the equity method when the subsidiary's retained earnings becomes negative.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

19

When the parent is not obligated to invest additional funds in a subsidiary that is reporting losses, the parent stops applying the equity method when the subsidiary's equity becomes negative.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

20

When the parent is obligated to invest additional funds in a subsidiary that is reporting losses, the parent stops applying the equity method when the subsidiary's retained earnings becomes negative.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

21

When the parent is obligated to invest additional funds in a subsidiary that is reporting losses, the parent stops applying the equity method when the subsidiary's equity becomes negative.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

22

When the parent has temporarily discontinued applying the equity method because of the subsidiary's substantial operating losses, the parent resumes application of the equity method when the subsidiary's retained earnings becomes positive.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

23

When the parent has temporarily discontinued applying the equity method because of the subsidiary's substantial operating losses, the parent resumes application of the equity method when the subsidiary's equity becomes positive.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

24

When a parent accounts for its investment in a subsidiary using the equity method, only the subsidiary's undistributed retained earnings is added to the parent's retained earnings in the consolidation process.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

25

To properly calculate the return on its investment in a subsidiary, the parent must use as the denominator the carrying value produced under the equity method.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

26

Whether the equity method or the cost method is used to account for an investment in a subsidiary, the consolidated statements are identical.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

27

Under the cost method, the investment account is not reduced for dividends declared by the subsidiary.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

28

Under the cost method, the investment account is reduced for dividends when they are received-not when they are paid.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

29

Under the cost method, the investment account is reduced for the subsidiary's cumulative reported losses that exceed its cumulative reported profits.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

30

The cost method has a built-in checking feature that is useful in preparing consolidated statements.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

31

If a write-down has been made to the parent's investment under the cost method, the investment account can be written back up, but only to the original cost amount, if the subsidiary later becomes profitable.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

32

If a write-down has been made to the parent's investment under the cost method, the investment account cannot be written back up to the original cost amount if the subsidiary later becomes profitable.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

33

The consolidated net income equals the parent's net income only if the parent accounts for its investment in the subsidiary using the cost method.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

34

When a subsidiary is reporting profits, the consolidated net income can never equal the parent's net income under the cost method.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

35

Under the cost method, the subsidiary's retained earnings is added to the parent's retained earnings in the consolidation process.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

36

Under FAS 94, parent-company-only statements must be included in notes to the consolidated statements.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

37

When parent-company-only statements are presented in the notes to the consolidated statements, the net income and retained earnings amounts in such statements agree with the corresponding amounts in the consolidated statements only if the equity method is used.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

38

Parent-company-only statements are required by the Securities and Exchange Commission when the restricted net assets of all subsidiaries of a bank holding company exceed 25% of consolidated net assets.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

39

Parent-company-only statements are required by the Securities and Exchange Commission when the restricted net assets of all subsidiaries of a bank holding company exceed 25% of the consolidated retained earnings.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

40

_____ Which of the following statements is not an argument in support of the equity method?

A) It reflects economic substance.

B) It keeps track of the amount invested.

C) It enables parent company financial statements to be used meaningfully internally.

D) It is the same as the accrual basis of accounting.

E) None of the above.

A) It reflects economic substance.

B) It keeps track of the amount invested.

C) It enables parent company financial statements to be used meaningfully internally.

D) It is the same as the accrual basis of accounting.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

41

_____ Which statement is correct concerning the equity method?

A) It is used exclusively instead of consolidation.

B) It is based on the historical cost concept.

C) It does not have a built-in self-checking feature in the consolidation process.

D) Cash dividends declared by the subsidiary are always treated as a partial liquidation (reduction) of the parent's investment in the subsidiary.

E) None of the above.

A) It is used exclusively instead of consolidation.

B) It is based on the historical cost concept.

C) It does not have a built-in self-checking feature in the consolidation process.

D) Cash dividends declared by the subsidiary are always treated as a partial liquidation (reduction) of the parent's investment in the subsidiary.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

42

_____ Under the equity method, which account is not used?

A) Dividends Receivable.

B) Dividends Income.

C) Investment in Subsidiary.

D) Equity in Net Income of Subsidiary.

E) None of the above.

A) Dividends Receivable.

B) Dividends Income.

C) Investment in Subsidiary.

D) Equity in Net Income of Subsidiary.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

43

_____ Under the cost method, which account does not have any general ledger entries made to it when the subsidiary has been profitable each year since its creation?

A) Dividends Receivable.

B) Dividends Income.

C) Investment in Subsidiary.

D) Cash.

E) None of the above.

A) Dividends Receivable.

B) Dividends Income.

C) Investment in Subsidiary.

D) Cash.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

44

_____ The Dividend Income account would be used in which of the following accounting methods?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

45

_____ When a parent uses the equity method of accounting for its investment in a 100%-owned subsidiary, the Investment account will be increased when the parent recognizes

A) Cash dividends declared by the subsidiary.

B) The receipt of cash in payment of dividends declared by the subsidiary.

C) The subsidiary's reported net income.

D) The subsidiary's reported net loss.

E) None of the above.

A) Cash dividends declared by the subsidiary.

B) The receipt of cash in payment of dividends declared by the subsidiary.

C) The subsidiary's reported net income.

D) The subsidiary's reported net loss.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

46

_____ When a parent uses the cost method to account for its investment in a 100%-owned subsidiary, cash dividends declared by the subsidiary should be recorded by the parent as

A) Dividend income when declared.

B) Dividend income when the cash is received.

C) A deduction from the parent's Investment account.

D) An addition to the parent's Investment account.

E) None of the above.

A) Dividend income when declared.

B) Dividend income when the cash is received.

C) A deduction from the parent's Investment account.

D) An addition to the parent's Investment account.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

47

_____ On 12/29/05, a subsidiary declared a cash dividend that was paid on 1/2/06. Under the equity method, what is the effect of this declaration on the parent's retained earnings-not the consolidated retained earnings?

A) Increase.

B) Decrease.

C) No effect.

A) Increase.

B) Decrease.

C) No effect.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

48

_____ On 12/29/05, a subsidiary declared a cash dividend that was paid on 1/2/06. Under the cost method, what is the effect of this declaration on the parent's retained earnings-not the consolidated retained earnings?

A) Increase.

B) Decrease.

C) No effect.

A) Increase.

B) Decrease.

C) No effect.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

49

_____ A subsidiary declared a cash dividend. What is the ultimate effect of this declaration on the parent's retained earnings account-not the consolidated retained earnings-under each of the following methods?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

50

_____ On 1/4/06, a subsidiary paid a cash dividend that had been declared on 12/30/05. Under the equity method, what is the effect of this payment on the parent's retained earnings-not the consolidated retained earnings?

A) Increase.

B) Decrease

C) No effect.

A) Increase.

B) Decrease

C) No effect.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

51

_____ On 1/4/06, a subsidiary paid a cash dividend that had been declared on 12/30/05. Under the cost method, what is the effect of this payment on the parent's retained earnings-not the consolidated retained earnings?

A) Increase.

B) Decrease.

C) No effect.

A) Increase.

B) Decrease.

C) No effect.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

52

_____ When a parent company uses the equity method of accounting for its investment in a subsidiary, which of the following affects the parent's retained earnings?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

53

_____ When a parent company uses the cost method of accounting for its investment in a subsidiary, which of the following affects the parent's retained earnings?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

54

_____ In the absence of knowing whether the parent has guaranteed any of the subsidiary's debt, a parent company using the equity method will consider when it is absolutely necessary to temporarily discontinue application of the equity method when the

A) Subsidiary reports losses but still has positive retained earnings.

B) Subsidiary's retained earnings becomes negative.

C) Subsidiary's equity becomes negative.

D) Subsidiary no longer declares dividends.

E) None of the above.

A) Subsidiary reports losses but still has positive retained earnings.

B) Subsidiary's retained earnings becomes negative.

C) Subsidiary's equity becomes negative.

D) Subsidiary no longer declares dividends.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

55

_____ Which of the following statements is false?

A) Consolidation entries are never posted to the general ledger.

B) Any balance in the Equity in Net Income (of subsidiary) account is always eliminated in the consolidation process.

C) Under the equity method, the parent's net income always equals consolidated net income when the subsidiary has always been profitable.

D) In consolidation, dividends declared by a 100%-owned subsidiary are always eliminated.

E) None of the above.

A) Consolidation entries are never posted to the general ledger.

B) Any balance in the Equity in Net Income (of subsidiary) account is always eliminated in the consolidation process.

C) Under the equity method, the parent's net income always equals consolidated net income when the subsidiary has always been profitable.

D) In consolidation, dividends declared by a 100%-owned subsidiary are always eliminated.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

56

_____ Under the equity method, a parent company that has guaranteed all of its subsidiary's debt would

A) Discontinue applying the equity method when the subsidiary's retained earnings becomes negative.

B) Discontinue applying the equity method when the subsidiary's equity becomes negative.

C) Not discontinue applying the equity method regardless of the subsidiary's losses.

D) Switch to the cost method when the subsidiary's equity becomes zero.

E) None of the above.

A) Discontinue applying the equity method when the subsidiary's retained earnings becomes negative.

B) Discontinue applying the equity method when the subsidiary's equity becomes negative.

C) Not discontinue applying the equity method regardless of the subsidiary's losses.

D) Switch to the cost method when the subsidiary's equity becomes zero.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

57

_____ If a subsidiary has always been profitable (and dividends never equaled net income), the consolidated net income amount is the same as the parent's net income amount

A) Only under the equity method.

B) Only under the cost method.

C) Under both the equity method and the cost method.

D) Under neither the equity method nor the cost method.

A) Only under the equity method.

B) Only under the cost method.

C) Under both the equity method and the cost method.

D) Under neither the equity method nor the cost method.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

58

_____ Dividends declared by a subsidiary as shown in its analysis of retained earnings on the consolidation worksheet are

A) Added to the dividends declared by the parent in arriving at dividends declared to be reported in the consolidated analysis of retained earnings.

B) Eliminated in consolidation only if the parent uses the equity method.

C) Eliminated in consolidation only if the parent uses the cost method.

D) Eliminated in consolidation regardless of whether the parent uses the equity method or the cost method.

A) Added to the dividends declared by the parent in arriving at dividends declared to be reported in the consolidated analysis of retained earnings.

B) Eliminated in consolidation only if the parent uses the equity method.

C) Eliminated in consolidation only if the parent uses the cost method.

D) Eliminated in consolidation regardless of whether the parent uses the equity method or the cost method.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

59

_____ When a parent uses the equity method and consolidates a subsidiary that has never reported a loss, consolidated retained earnings will always be

A) More than the parent's retained earnings.

B) Less than the parent's retained earnings.

C) Equal to the parent's retained earnings.

D) More than or less than the parent's retained earnings, depending on whether the parent has a positive or negative balance in its Retained Earnings account.

E) None of the above.

A) More than the parent's retained earnings.

B) Less than the parent's retained earnings.

C) Equal to the parent's retained earnings.

D) More than or less than the parent's retained earnings, depending on whether the parent has a positive or negative balance in its Retained Earnings account.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

60

_____ In the consolidated statement of retained earnings for a parent and a 100%-owned subsidiary, dividends declared by the subsidiary are

A) Shown.

B) Not shown.

C) Shown only under the equity method.

D) Shown only under the cost method.

A) Shown.

B) Not shown.

C) Shown only under the equity method.

D) Shown only under the cost method.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

61

_____ When a parent-subsidiary relationship exists, the Dividend Income account is reported in the consolidated income statement under which of the following accounting methods?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

62

_____ Dividends declared by a subsidiary are reported currently in the parent's separate income statement and in the consolidated income statement under the

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

63

_____ Under the cost method, the parent's net income equals the consolidated net income only if

A) The subsidiary reports no loss.

B) The subsidiary reports a loss.

C) The subsidiary declares dividends equal to or greater than its net income.

D) The subsidiary declares dividends equal to its net income.

E) None of the above.

A) The subsidiary reports no loss.

B) The subsidiary reports a loss.

C) The subsidiary declares dividends equal to or greater than its net income.

D) The subsidiary declares dividends equal to its net income.

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

64

_____ On 1/1/06, Parco created a 100%-owned subsidiary, Sarco, with a $100,000 cash investment. During 2006, Sarco reported net income of $35,000, declared cash dividends of $15,000, and paid $10,000 of the $15,000 to the parent. What is the carrying value of the investment at 12/31/06 under the equity method?

A) $100,000

B) $115,000

C) $120,000

D) $135,000

E) $145,000

A) $100,000

B) $115,000

C) $120,000

D) $135,000

E) $145,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

65

_____ On 1/1/06, Parco created a 100%-owned subsidiary, Sarco, with a $100,000 cash investment. During 2006, Sarco reported net income of $35,000, declared cash dividends of $15,000, and paid $10,000 of the $15,000 to the parent. What is the carrying value of the investment at 12/31/06 under the cost method?

A) $100,000

B) $115,000

C) $120,000

D) $135,000

E) $145,000

A) $100,000

B) $115,000

C) $120,000

D) $135,000

E) $145,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

66

_____ On 5/1/06, Pyne Inc. formed Syne Inc., investing $500,000 cash. For 2004, Syne reported net income of $65,000 and declared and paid cash dividends of $25,000. Under the equity method, what amount appears in the parent's separate 2006 income statement-not the consolidated income statement?

A) $25,000

B) $40,000

C) $65,000

D) $90,000

A) $25,000

B) $40,000

C) $65,000

D) $90,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

67

_____ On 5/1/06, Pyne Inc. formed Syne Inc., investing $500,000 cash. For 2006, Syne reported net income of $65,000 and declared and paid cash dividends of $25,000. Under the cost method, what amount appears in the parent's separate 2006 income statement-not the consolidated income statement?

A) $25,000 c. $65,000

B) $40,000 d. $90,000

A) $25,000 c. $65,000

B) $40,000 d. $90,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

68

_____ On 4/1/06, Pix Inc. formed Stix Inc., investing $100,000 cash. For 2004, Stix reported net income of $23,000 and declared and paid cash dividends of $8,000. What is Pix's carrying value of its investment in Stix at 12/31/06 under each of the following methods?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

69

_____ On 4/1/06, Pix Inc. formed Stix Inc., investing $100,000 cash. For 2006, Stix reported net income of $23,000 and declared cash dividends of $8,000 (which were paid 1/2/07). What is Pix's carrying value of its investment in Stix at 12/31/06?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

70

_____ On 5/1/05, Pax Inc. created Sax Inc., investing $500,000 cash. Sax reported a highly unexpected $230,000 loss for 2005 and a $40,000 profit for 2006. The 2005 loss created substantial doubt as to (a) the ability of the subsidiary to survive and (b) the ability of the parent to sell the subsidiary at other than an amount substantially below its initial investment. What should the carrying value of Pax's investment in Sax be at 12/31/06 under each of the following methods?

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

71

_____ On 1/1/06, the carrying value of Plano Company's investment in its 100%-owned created subsidiary, Slano, was $600,000. During 2006, Slano reported a loss of $700,000. Under the equity method, what amount should be reported in Plano's separate income statement for 2006, relating to its investment in Slano, if Slano's debt is

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

72

_____ On 5/1/05, Platt created a 100%-owned subsidiary, Switt, with a cash investment of $500,000. Switt reported a net loss of $600,000 for 2005 and net income of $140,000 for 2006. Platt has not guaranteed any of the subsidiary's debt. Under the equity method, what should be the amount reported in Platt's income statement for 2006-not 2005-relating to its investment in Switt?

A) $ -0-

B) $(40,000)

C) $40,000

D) $(140,000)

E) $140,000

A) $ -0-

B) $(40,000)

C) $40,000

D) $(140,000)

E) $140,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

73

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at the end of 2006?

A) Debit of $17,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at the end of 2006?A) Debit of $17,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

74

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (2001) at the end of 2006:

The subsidiary's retained earnings at 12/31/05 were $27,000. What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

A) Debit of $10,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

The subsidiary's retained earnings at 12/31/05 were $27,000. What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?A) Debit of $10,000.

B) Debit of $27,000.

C) Debit of $37,000.

D) Debit of $50,000.

E) No amount is posted.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

75

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

76

_____ The following accounts are as they appear in the consolidation worksheet for a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

The subsidiary's retained earnings at 12/31/05 were $(16,000). What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?

A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

The subsidiary's retained earnings at 12/31/05 were $(16,000). What amount appears as a separate line item posting to the Retained Earnings account in the basic elimination entry at 12/31/06?A) Debit of $16,000.

B) Credit of $16,000.

C) Debit of $44,000.

D) Credit of $44,000.

E) No amount is posted.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

77

_____ The following accounts were taken from the separate company financial statements of a parent and its 100%-owned subsidiary (created in 2001) at the end of 2006:

What amount should be reported for consolidated retained earnings at the end of 2006?

A) $450,000

B) $480,000

C) $530,000

D) $690,000

E) None of the above.

What amount should be reported for consolidated retained earnings at the end of 2006?A) $450,000

B) $480,000

C) $530,000

D) $690,000

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

78

_____ The following accounts or amounts were taken from the separate company financial statements of a parent and its 100%-owned subsidiary (created in 2006) at the end of 2006:

What amount should be reported for consolidated retained earnings at the end of 2006?

A) $210,000

B) $240,000

C) $290,000

D) $450,000

E) None of the above.

What amount should be reported for consolidated retained earnings at the end of 2006?A) $210,000

B) $240,000

C) $290,000

D) $450,000

E) None of the above.

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

79

_____ For 2006, a 100%-owned subsidiary reported (a) net income of $75,000 and (b) dividends declared of $15,000 ($10,000 of which was paid in 2006). What amount appears in the parent's separate income statement for 2006 under the equity method of accounting?

A) $10,000

B) $15,000

C) $60,000

D) $65,000

E) $75,000

A) $10,000

B) $15,000

C) $60,000

D) $65,000

E) $75,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

80

_____ For 2006, a 100%-owned subsidiary reported (a) net income of $75,000 and (b) dividends declared of $15,000 ($10,000 of which was paid in 2006). What amount appears in the parent's separate income statement for 2006 under the cost method of accounting?

A) $10,000

B) $15,000

C) $60,001

D) $65,000

E) $75,000

A) $10,000

B) $15,000

C) $60,001

D) $65,000

E) $75,000

Unlock Deck

Unlock for access to all 110 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 110 flashcards in this deck.