Deck 15: Fundamentals of Accounting

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

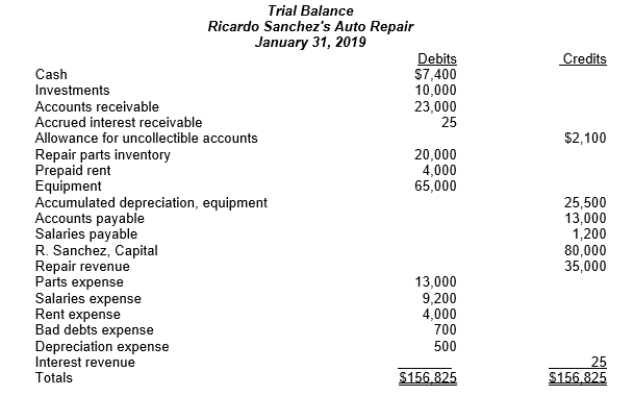

Following is a trial balance for Ricardo Sanchez's Auto Repair as of January 31, 2019.

Required:

Required:

a. Prepare an income statement.

b.Prepare a statement of changes in owner's equity for the month ended January 31, 2019.

c. Prepare balance sheet as of January 31, 2019.

d. Prepare the entry to close the books, as if Ricardo's financial year end is January 31.

Required: a. Prepare an income statement.

b.Prepare a statement of changes in owner's equity for the month ended January 31, 2019.

c. Prepare balance sheet as of January 31, 2019.

d. Prepare the entry to close the books, as if Ricardo's financial year end is January 31.

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/45

Play

Full screen (f)

Deck 15: Fundamentals of Accounting

1

An asset can be created by incurring a liability.

True

2

If a transaction causes an asset to increase, another asset cannot simultaneously decrease.

False

3

Most nonprofit entities now refer to their balance sheets as the statement of financial position.

True

4

When assets are used by a company, they reduce the owner's equity.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

5

The purpose of accounting in most cases is to be able to measure net income or profitability.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

6

Accruals, deferrals, and amortizations are the three processes that make up accrual accounting.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

7

The notion of relating revenues to periods of time is called "matching."

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

8

The process of recording transactions in a journal is referred to as making a trial balance.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

9

Revenues and expenses are temporary subsets of assets and liabilities, respectively.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

10

The two components of a journal entry are the date and the amount.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

11

As expenses increase, the equity of an entity will decrease.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

12

The first step toward preparing financial statements-after recording journal entries-is to prepare a trial balance.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

13

Adjusting entries are only needed if there is a mistake in the journal entries that is not caught before the end of each year.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

14

Companies typically prepare three separate financial statements-a balance sheet, an operating statement, and a statement of change in owner's equity.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

15

The purpose of preparing an entry to close the books is so that a company can start over with zero revenues and zero expenses at the beginning of a new year.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

16

After a company closes its books at the end of the year, the revenue and expense accounts are no longer relevant.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

17

"Matching" also means recording bad debts expense with the revenues to which the bad debts relate.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

18

When the owner of a company withdraws cash from the company, the journal entry shows a debit to cost of sales and a credit to cash.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

19

Veronica Lodge borrowed $15,000 from a bank on January 1, 2019 to finance her new business. She agrees to repay the bank on December 31, 2019, with $750 interest on the loan. In addition to increasing cash, what else should Veronica record on January 1, 2019?

A) An increase in a liability of $15,000

B) An increase in a liability of $15,750

C) An increase in equity of $15,000

D) An increase in a liability of $15,750, and a decrease in equity of $750

A) An increase in a liability of $15,000

B) An increase in a liability of $15,750

C) An increase in equity of $15,000

D) An increase in a liability of $15,750, and a decrease in equity of $750

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

20

At the end of the month, Samantha's Shoes received a bill for electricity that her business used during the month, but Samantha didn't pay the bill. What is the effect on Samantha's Shoes' assets, liabilities, and equity?

A) Assets increased and liabilities increased.

B) Liabilities increased and equity decreased.

C) Assets increased and equity decreased.

D) Liabilities increased and liabilities decreased.

A) Assets increased and liabilities increased.

B) Liabilities increased and equity decreased.

C) Assets increased and equity decreased.

D) Liabilities increased and liabilities decreased.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

21

In accounting, the term "matching" refers to

A) Relating debits to credits

B) Relating assets to liabilities

C) Relating accruals to deferrals

D) Relating expenses to the same period of time that revenues are recognized

A) Relating debits to credits

B) Relating assets to liabilities

C) Relating accruals to deferrals

D) Relating expenses to the same period of time that revenues are recognized

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

22

The Cardiel Car Company purchased a passenger van to use to transport customers when they leave their car for repairs. If the van is expected to last 7 years and costs $56,000, what effect would that have on income on the accrual basis each year?

A) The van's cost would need to be amortized/depreciated to recognize an expense equal to $10,000 each year.

B) Both the van and depreciation would be reduced by $8,000 each year.

C) No effect.

D) The van's cost would need to be amortized/depreciated to recognize an expense of $8,000 ($56,000 ÷ 7) in each year.

A) The van's cost would need to be amortized/depreciated to recognize an expense equal to $10,000 each year.

B) Both the van and depreciation would be reduced by $8,000 each year.

C) No effect.

D) The van's cost would need to be amortized/depreciated to recognize an expense of $8,000 ($56,000 ÷ 7) in each year.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

23

A business owns an automobile that has an estimated useful life of five years. What is the effect on the accounting equation of recording the using up of the auto for one year?

A) Assets are decreased and equity is decreased.

B) Assets are decreased and liabilities are increased.

C) There is no effect, provided the automobile was paid for at the time of purchase.

D) Assets are increased and equity is increased.

A) Assets are decreased and equity is decreased.

B) Assets are decreased and liabilities are increased.

C) There is no effect, provided the automobile was paid for at the time of purchase.

D) Assets are increased and equity is increased.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

24

Because of recent E. coli outbreaks at nearby farms, the Flora Brothers Farm decided to purchase product liability insurance. Because they expect that the cost of this insurance to rise dramatically if outbreaks continue, they find an insurer willing to enter into a 10-year contract. Assuming that the Flora Brothers paid cash of $120,000 total in exchange for ten years of insurance, how should the Flora Brothers record this contract and cost?

A) Record prepaid insurance of $120,000 (an asset) and then report a $10,000 expense in each year that the contract covers, reducing the prepaid insurance asset by the same amount.

B) Record the entire cost of the contract as a current period expense.

C) Record prepaid insurance of $120,000 (an asset) and then charge $12,000 to each year that the

Contract covers, reducing the prepaid insurance asset by the same amount.

D) Record insurance cost each year of $12,000.

A) Record prepaid insurance of $120,000 (an asset) and then report a $10,000 expense in each year that the contract covers, reducing the prepaid insurance asset by the same amount.

B) Record the entire cost of the contract as a current period expense.

C) Record prepaid insurance of $120,000 (an asset) and then charge $12,000 to each year that the

Contract covers, reducing the prepaid insurance asset by the same amount.

D) Record insurance cost each year of $12,000.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

25

A business borrows $100,000 from a bank on July 1, 2018. Under the agreement with the bank, the loan must be repaid in full on June 30, 2019, with interest at 6% a year. The business wants to prepare financial statements for the year ended December 31, 2018. How much interest expense should it report for that year?

A) $0

B) $3,000

C) $6,000

D) $12,000

A) $0

B) $3,000

C) $6,000

D) $12,000

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

26

When an accountant uses T-accounts, the debit side is always the left side and the credit side is always the right side. Which of the following describes increases and decreases in assets and liabilities?

A) Debits increase liabilities and credits increase assets.

B) Debits increase assets and debits decrease liabilities.

C) Debits increase assets and debits increase liabilities.

D) Credits increase assets and credits increase liabilities.

A) Debits increase liabilities and credits increase assets.

B) Debits increase assets and debits decrease liabilities.

C) Debits increase assets and debits increase liabilities.

D) Credits increase assets and credits increase liabilities.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

27

A company's payroll for the period ended March 15 totaled $12,000. The salaries, however, were subject to federal withholding taxes, so the company withheld $1,500 from the employees' checks. The employees were paid on March 15, but the company was not required to remit the withheld taxes to the government until April 10. What journal entry did the company make on March 15?

A) Debit salaries expense for $10,500 and credit cash for $10,500.

B) Debit salaries expense for $12,000 and credit cash for $12,000.

C) Debit salaries expense for $12,000, credit cash for $10,500, and credit salaries payable for $1,500.

D) Debit salaries expense for $12,000, credit cash for $10,500, and credit withholding taxes payable for $1,500.

A) Debit salaries expense for $10,500 and credit cash for $10,500.

B) Debit salaries expense for $12,000 and credit cash for $12,000.

C) Debit salaries expense for $12,000, credit cash for $10,500, and credit salaries payable for $1,500.

D) Debit salaries expense for $12,000, credit cash for $10,500, and credit withholding taxes payable for $1,500.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

28

At the beginning of the year, a business had office supplies on hand in the amount of $35,000. During the year, the business acquired additional supplies in the amount of $27,000. At year-end, in anticipation of preparing financial statements, the business took an inventory of its office supplies and found that the amount on hand was $19,000. What journal must be made to record the business' use of office supplies during the year?

A) Debit office supplies and credit office supplies expense for $19,000.

B) Debit office supplies and credit office supplies expense for $43,000.

C) Debit office supplies expense and credit office supplies for $43,000.

D) Debit office supplies expense and credit office supplies for $8,000.

A) Debit office supplies and credit office supplies expense for $19,000.

B) Debit office supplies and credit office supplies expense for $43,000.

C) Debit office supplies expense and credit office supplies for $43,000.

D) Debit office supplies expense and credit office supplies for $8,000.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

29

What assurance do you have if you prepare a trial balance and the sum of the debits equals the sum of the credits?

A) That all journal entries have been posted to the ledger accounts

B) That all journal entries have been posted to the correct ledger account

C) That both a. and b. have occurred

D) You cannot be assured that either a. or b. have occurred.

A) That all journal entries have been posted to the ledger accounts

B) That all journal entries have been posted to the correct ledger account

C) That both a. and b. have occurred

D) You cannot be assured that either a. or b. have occurred.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

30

A balance sheet is used to report the year-end balances of which accounts?

A) Revenues and expenses and owner's equity

B) Net income and owner's equity

C) Assets, liabilities, and capital accounts

D) Assets, liabilities, and net income

A) Revenues and expenses and owner's equity

B) Net income and owner's equity

C) Assets, liabilities, and capital accounts

D) Assets, liabilities, and net income

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

31

An income statement or operating statement compares which accounts for the year?

A) Revenues to expenses resulting in net income or loss

B) Net income to owner's equity

C) Assets to liabilities, and owner's equity

D) Assets and liabilities to net income

A) Revenues to expenses resulting in net income or loss

B) Net income to owner's equity

C) Assets to liabilities, and owner's equity

D) Assets and liabilities to net income

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

32

Eddie Howard's bookkeeper prepared a trial balance of the accounts at December 31, 2020 in order to prepare financial statements. Following is a summary of the trial balance. Based on the trial balance, how much was Eddie Howard's net income on the income statement and how much was Eddie Howard's Capital on the balance sheet?

A) Net income - $8,700; Capital - $14,900

B) Net income - $62,000; Capital - $68,200

C) Net income - $22,300; Capital - $22,300

D) Net income - $84,300; Capital - $6,200

A) Net income - $8,700; Capital - $14,900

B) Net income - $62,000; Capital - $68,200

C) Net income - $22,300; Capital - $22,300

D) Net income - $84,300; Capital - $6,200

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

33

Of the four financial statements prepared by companies, which of the following is an accurate statement about the relationship between those statements?

A) Only revenues and expenses increase the owner's capital account.

B) The ending balance in the owner's capital account is used to balance the balance sheet.

C) Adjusting journal entries all create contra-asset accounts.

D) Net income for the period is taken from the income statement and is used to determine the ending balance for capital assets.

A) Only revenues and expenses increase the owner's capital account.

B) The ending balance in the owner's capital account is used to balance the balance sheet.

C) Adjusting journal entries all create contra-asset accounts.

D) Net income for the period is taken from the income statement and is used to determine the ending balance for capital assets.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

34

Accountants may use a worksheet that starts with a company's trial balance and then spreads that information across 4 more columns before creating the financial statements. What four columns (debit and credit) would appear after the unadjusted trial balance?

A) Revenues (two columns-debit and credit) and expenses (two columns-debit and credit).

B) Adjusting entries (two columns-debit and credit) and adjusted trial balance (two columns-debit

And credit)

C) Net income and changes in owner's equity.

D) Net income for the period is taken from the income statement and is used to determine the ending balance for capital assets.

A) Revenues (two columns-debit and credit) and expenses (two columns-debit and credit).

B) Adjusting entries (two columns-debit and credit) and adjusted trial balance (two columns-debit

And credit)

C) Net income and changes in owner's equity.

D) Net income for the period is taken from the income statement and is used to determine the ending balance for capital assets.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

35

When closing the books, accountants refer to certain accounts as "permanent or real" accounts-assets, liabilities, and equity. Why are they given this label?

A) These accounts record real, permanent assets and liabilities.

B) These accounts are useful for evaluating a company's operations for the current year.

C) They are called permanent accounts because their balances carry forward from year to year.

D) Only these entries are reflected in the owner's equity account.

A) These accounts record real, permanent assets and liabilities.

B) These accounts are useful for evaluating a company's operations for the current year.

C) They are called permanent accounts because their balances carry forward from year to year.

D) Only these entries are reflected in the owner's equity account.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

36

What would be the effect of making closing entries before making adjusting entries?

A) Revenues and expenses would be higher than they should be.

B) Net income would still be correct.

C) Capital assets would be reported as assets.

D) Net income would not be recorded on the accrual basis. .

A) Revenues and expenses would be higher than they should be.

B) Net income would still be correct.

C) Capital assets would be reported as assets.

D) Net income would not be recorded on the accrual basis. .

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

37

What is the underlying purpose of establishing an allowance for uncollectible accounts?

A) It allows management to reduce the net profit for the year and, therefore, to pay less income tax.

B) It provides a means for adjusting the accounts receivable control account to be equal to the total of the individual accounts receivable.

C) It enables the expense of bad debts to be matched with the revenues of the year in which the sale was recorded.

D) It gives management the ability to manipulate the amount reported as net profit from year to year.

A) It allows management to reduce the net profit for the year and, therefore, to pay less income tax.

B) It provides a means for adjusting the accounts receivable control account to be equal to the total of the individual accounts receivable.

C) It enables the expense of bad debts to be matched with the revenues of the year in which the sale was recorded.

D) It gives management the ability to manipulate the amount reported as net profit from year to year.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

38

Tony's Tool Shed specializes in selling small farm tractors. Tony's starts the year with an inventory of $140,000. During the year, the manufacturer delivered $220,000 more inventory. At year-end, Tony's counts his inventory and finds that he has tractors costing a total of $100,000 on hand. During the year, Tony's sales totaled $300,000. What was his gross profit on the sales for the year?

A) $54,000

B) $40,000

C) $74,000

D) $82,000

A) $54,000

B) $40,000

C) $74,000

D) $82,000

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

39

When customers buy goods on credit and are allowed a certain period of time to pay for their purchases, companies need to consider that some customers may not pay their bills. When a company estimates that some purchases will go unpaid, the company should:

A) Credit Bad debt expense and debit Allowance for uncollectible accounts

B) Debit Bad debt expense and a credit a contra-asset account called Allowance for uncollectible

Accounts

C) Debit Bad debt expense and credit Accounts receivable

D) Debit revenues and credit Costs of goods sold

A) Credit Bad debt expense and debit Allowance for uncollectible accounts

B) Debit Bad debt expense and a credit a contra-asset account called Allowance for uncollectible

Accounts

C) Debit Bad debt expense and credit Accounts receivable

D) Debit revenues and credit Costs of goods sold

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

40

Companies may have thousands of customers and thousands of accounts receivable. How do companies use subsidiary accounts to manage their accounts receivable?

A) Subsidiary accounts are used for each subsidiary a company owns.

B) It establishes a subsidiary account page for each customer. Totals for all these pages must equal

The control account contained in the company's general ledger.

C) It establishes a subsidiary account for each customer that result in a separate balance sheet and

Income statement for each customer.

D) Companies record the transactions they have with each individual customer as if no other customers exist.

A) Subsidiary accounts are used for each subsidiary a company owns.

B) It establishes a subsidiary account page for each customer. Totals for all these pages must equal

The control account contained in the company's general ledger.

C) It establishes a subsidiary account for each customer that result in a separate balance sheet and

Income statement for each customer.

D) Companies record the transactions they have with each individual customer as if no other customers exist.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

41

The Jacob Company keeps its accounts on a calendar-year basis. On January 1, 2019, there is a balance of $2,800 in the Prepaid insurance account. The insurance represented by that amount expires on March 31, 2019, but the business makes no entry to record the expiration of the insurance until its year-end. On April 1, 2019, the Company pays $16,000 for an insurance policy covering the period April 1, 2019 - March 31, 2020. Prepare the journal entry at December 31, 2019, to record the full amount of insurance expense for the year.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

42

Ricardo's Garage wants to prepare financial statements for his company at the end of the January. But first, his accountant needs to make the following adjusting journal entries:

a. To recognize one month's depreciation on $60,000 of equipment on hand at the

beginning of the month. Ricardo assumes the equipment will have a 10-year life.

b. To recognize estimated bad debts. Ricardo wants to provide for additional bad debts

at the rate of 2% of the month's billings, which were $35,000 in January.

c. To recognize unpaid salaries of $1,200 for the last few days in January.

d. To recognize 3% interest earned for one-month on a $100,000 CD purchased on

December 31.

e. To recognize the expiration of one month's rent from three months' worth of rent of

$12,000 paid at the end of December

Required:

Prepare journal entries to record all of the adjustments.

a. To recognize one month's depreciation on $60,000 of equipment on hand at the

beginning of the month. Ricardo assumes the equipment will have a 10-year life.

b. To recognize estimated bad debts. Ricardo wants to provide for additional bad debts

at the rate of 2% of the month's billings, which were $35,000 in January.

c. To recognize unpaid salaries of $1,200 for the last few days in January.

d. To recognize 3% interest earned for one-month on a $100,000 CD purchased on

December 31.

e. To recognize the expiration of one month's rent from three months' worth of rent of

$12,000 paid at the end of December

Required:

Prepare journal entries to record all of the adjustments.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

43

Regina's Dry Cleaning had a great year. It reported net income of $186,600 in 2018. Now Regina Arter needs to close the books and get ready to open on January 1.

Required:

Using the Regina's 2018 Income Statement, prepare the entry needed to close the books as of December 31, 2018.

Required:

Using the Regina's 2018 Income Statement, prepare the entry needed to close the books as of December 31, 2018.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

44

Lillian Rose opened a facility to provide day care for children. The following transactions occurred during the month of July 2019, the first month of business.

a. Lillian Rose invested $10,000 of her personal funds in a business, to be known as LilyRose Day

Care.

b. To provide additional funds for her business, she borrowed $20,000 from a bank. The loan must be

repaid at the end of year with interest at 8% per annum.

c. She rented a large house for one year. She paid rent of $5,000 in advance for the months of Julyand August.

d. She bought furniture at a cost of $6,000, receiving an invoice that had to be paid in 10 days. Sheexpected the equipment to last five years.

e. She paid $1,000 cash for food, toys and other operating supplies. (Because these

items are likely to be consumed in a few months, treat them as Operating Expenses.)

f. She paid the invoice for $6,000, received in transaction d.

g. She paid her helper at the rate of $400 a week, a total of $1,600 for the month.

h. She billed her clients $11,500 for day care services provided during the month.

i. She received checks totaling $11,000 against the bills sent out in transaction h.

j. She received a bill for utilities in the amount of $300.

Lillian wanted to prepare financial statements at the end of the month, so she made adjusting journal entries for the following items.

k. To record interest for one month on the amount borrowed from the bank in

transaction b.

l. To recognize the expiration of rent for the month of July (transaction c).

m. To recognize one month's depreciation on the equipment purchased in transaction d.

n. To recognize salary of $240 owed to her helper for the last three days of July.

Required:

A. Analyze the above transactions on a worksheet. The worksheet should show columns for

individual accounts classified as assets, liabilities, and equity.

B. Prepare journal entries to record the above transactions.

a. Lillian Rose invested $10,000 of her personal funds in a business, to be known as LilyRose Day

Care.

b. To provide additional funds for her business, she borrowed $20,000 from a bank. The loan must be

repaid at the end of year with interest at 8% per annum.

c. She rented a large house for one year. She paid rent of $5,000 in advance for the months of Julyand August.

d. She bought furniture at a cost of $6,000, receiving an invoice that had to be paid in 10 days. Sheexpected the equipment to last five years.

e. She paid $1,000 cash for food, toys and other operating supplies. (Because these

items are likely to be consumed in a few months, treat them as Operating Expenses.)

f. She paid the invoice for $6,000, received in transaction d.

g. She paid her helper at the rate of $400 a week, a total of $1,600 for the month.

h. She billed her clients $11,500 for day care services provided during the month.

i. She received checks totaling $11,000 against the bills sent out in transaction h.

j. She received a bill for utilities in the amount of $300.

Lillian wanted to prepare financial statements at the end of the month, so she made adjusting journal entries for the following items.

k. To record interest for one month on the amount borrowed from the bank in

transaction b.

l. To recognize the expiration of rent for the month of July (transaction c).

m. To recognize one month's depreciation on the equipment purchased in transaction d.

n. To recognize salary of $240 owed to her helper for the last three days of July.

Required:

A. Analyze the above transactions on a worksheet. The worksheet should show columns for

individual accounts classified as assets, liabilities, and equity.

B. Prepare journal entries to record the above transactions.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

45

Following is a trial balance for Ricardo Sanchez's Auto Repair as of January 31, 2019.

Required:

a. Prepare an income statement.

b.Prepare a statement of changes in owner's equity for the month ended January 31, 2019.

c. Prepare balance sheet as of January 31, 2019.

d. Prepare the entry to close the books, as if Ricardo's financial year end is January 31.

Required: a. Prepare an income statement.

b.Prepare a statement of changes in owner's equity for the month ended January 31, 2019.

c. Prepare balance sheet as of January 31, 2019.

d. Prepare the entry to close the books, as if Ricardo's financial year end is January 31.

Unlock Deck

Unlock for access to all 45 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 45 flashcards in this deck.