Deck 7: Proprietary Type Fundsenterprise and Internal Service Funds

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

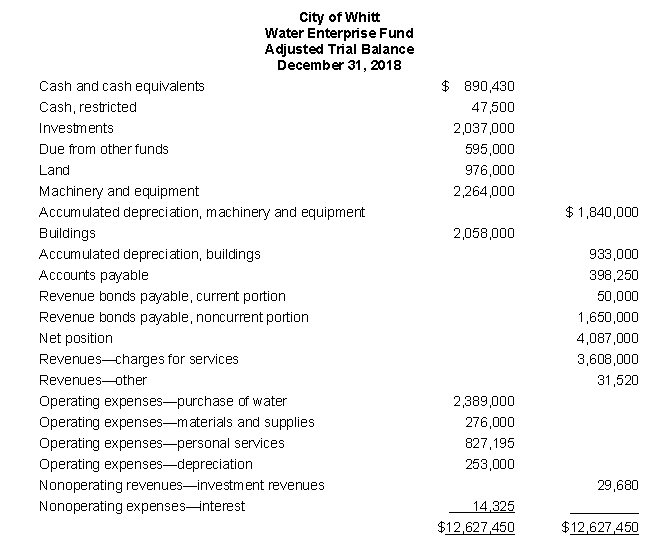

Presented on the following page is the adjusted trial balance for the Water Enterprise Fund of the City of Whitt at December 31, 2018, the end of its fiscal year. Based on this information:

a. Prepare the entry necessary to close the accounts

b. Compute the ending fund net position balances for (1) net investment in capital assets, (2) restricted net position, and (3) unrestricted net position

(Note: Debt related to the capital assets consists solely of the City's revenue bonds payable.)

a. Prepare the entry necessary to close the accounts

b. Compute the ending fund net position balances for (1) net investment in capital assets, (2) restricted net position, and (3) unrestricted net position

(Note: Debt related to the capital assets consists solely of the City's revenue bonds payable.)

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/42

Play

Full screen (f)

Deck 7: Proprietary Type Fundsenterprise and Internal Service Funds

1

Internal Service Funds may only provide services to individuals or entities outside the government.

False

2

In Proprietary Fund accounting, transactions related to operating costs are recognized as expenditures when purchased.

False

3

Capital assets are not recorded in proprietary fund accounting.

False

4

Only the GASB's standards for proprietary funds apply to Enterprise and Internal Service Funds.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

5

Proprietary funds are required to present four basic financial statements-a Statement of Net Position, a Statement of Changes in Fund Net Position, a Statement of Cash Flows, and a Budgetary Comparison Statement.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

6

An Enterprise Fund must be used if the activity it reports issues debt secured solely by a pledge of its own revenues.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

7

An Internal Service Fund typically provides services to the other funds and departments of a government, such as a motor pool or a data processing service.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

8

Internal Service Fund expenses are generally controlled by the budgetary constraints of the funds and departments who use their services.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

9

When Internal Service Funds [ISFs] bill the government's other funds or departments for the services they provide, ISFs report the amount billed as revenues.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

10

When Internal Service Funds [ISFs] present net position in their financial statements, they can use up to three line items, including net investment in capital assets, restricted, and unrestricted.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

11

When governments establish an activity that must use Enterprise Fund accounting and reporting, many also create a separate legal entity, like a public authority or public corporation.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

12

An Enterprise Fund must be used whenever a government charges fees to external users for goods or services.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

13

Revenue bonds are debt that is secured exclusively by the revenues generated by an activity accounted for in a specific fund, generally an Enterprise Fund.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

14

Accounts receivable that an Enterprise Fund estimates won't be collectible are reported as bad debt expense in its statement of revenues, expenses, and changes in fund net position.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

15

The Enterprise Fund net position component called, Net Investment in Capital Assets, is equal to the sum of all capital assets net of accumulated depreciation reported on those assets.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

16

Only Enterprise Funds may use the modified approach to report infrastructure assets.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

17

In governmental accounting and reporting, all leases are classified as either short-term or long-term.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

18

Because all capital assets may become impaired-because of changes in technology or other reasons-the FASB and GASB both require impaired assets to be written down using the same criteria.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

19

Both the FASB and the GASB, respectively, require companies and governments to record some form of a net pension or other postemployment benefit (OPEB) liability on the face of the entity's financial statements.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

20

Neither the FASB nor any of its predecessor standards-setting bodies have ever considered whether fiduciary activities should be reported in GAAP financial reports.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

21

GASB requires governments to report deferred outflows and deferred inflows of assets separate from assets and liabilities.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

22

The Weber County Printing Internal Service Fund (ISF) spent $82,000 in cash provided by contributions from the County's General Fund to purchase a commercial quality offset printer. Assuming the printer has an expected useful life of 10 years with no salvage value, which of the following entries should be used to record the printer when acquired and related depreciation at year end?

a. Two entries:

b. Two entries:

c. One entry:

d. One entry:

a. Two entries:

b. Two entries:

c. One entry:

d. One entry:

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following accounts would not appear in an Enterprise Fund statement of net position?

A) Accumulated depreciation

B) Retained earnings

C) Net position, unrestricted

D) Inventory

A) Accumulated depreciation

B) Retained earnings

C) Net position, unrestricted

D) Inventory

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

24

A Water Enterprise Fund (EF) issues $4 million of 5% revenue bonds on October 1, 2018. The EF will make its first payment of interest on March 31, 2019, together with a principal payment of $200,000. What amount, if any, should the EF report in its fund statement of revenues, expenses, and changes in net position for the year ended December 31, 2018?

A) Zero

B) Interest expense of $100,000

C) Interest expense of $50,000 and principal expense of $100,000

D) Interest expense of $50,000

A) Zero

B) Interest expense of $100,000

C) Interest expense of $50,000 and principal expense of $100,000

D) Interest expense of $50,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

25

A City accounts for its hospital in an Enterprise Fund. An individual brings a malpractice suit against the hospital in 2017. City lawyers are concerned about losing the case if it goes to court, but estimate that it is probable they can settle it out of court for $50,000. In any event, the City does not expect any cash outflows on the claim for several years. How should the Enterprise Fund report this item in its statements for the year ended December 31, 2017?

A) No reporting is necessary

B) The situation should be reported only by means of note disclosure

C) The Enterprise Fund should report a claims expense and a current liability of $50,000

D) The Enterprise Fund should report a claims expense and a noncurrent liability of $50,000

A) No reporting is necessary

B) The situation should be reported only by means of note disclosure

C) The Enterprise Fund should report a claims expense and a current liability of $50,000

D) The Enterprise Fund should report a claims expense and a noncurrent liability of $50,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

26

At December 31, 2018, a Water Enterprise Fund has outstanding revenue bonds payable of $1 million, of which $40,000 is due to be paid on February 15, 2019, and $50,000 is due to be paid on August 15, 2019. How should it report this liability in its fund statement of net position as of December 31, 2018?

A) It should report $40,000 as a current liability and disclose $960,000 in a note

B) It should report $40,000 as a current liability and $960,000 as a noncurrent liability

C) It should report $90,000 as a current liability and $910,000 as a noncurrent liability

D) It should report no liability for this obligation on the fund statement of net position

A) It should report $40,000 as a current liability and disclose $960,000 in a note

B) It should report $40,000 as a current liability and $960,000 as a noncurrent liability

C) It should report $90,000 as a current liability and $910,000 as a noncurrent liability

D) It should report no liability for this obligation on the fund statement of net position

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

27

An Enterprise Fund (EF) issued bonds in the amount of $100,000 and immediately acquired capital assets from the bond proceeds at a cost of $100,000. As of December 31, 2018, accumulated depreciation on the assets was $10,000. Also, as of December 31, 2018, the EF had paid back $15,000 of the debt principal. In its December 31, 2018, statement of net position, how much should the EF report as its net investment in capital assets?

A) $90,000

B) $85,000

C) $15,000

D) $5,000

A) $90,000

B) $85,000

C) $15,000

D) $5,000

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

28

Governments control their Enterprise Fund revenues and expenses in what way?

A) By using encumbrance accounting

B) By using flexible budgets; however, they are not recorded in the accounts of the fund.

C) By gaining approval of their budget at required public hearings

D) By issuing hedge contracts on all projected purchases for the year

A) By using encumbrance accounting

B) By using flexible budgets; however, they are not recorded in the accounts of the fund.

C) By gaining approval of their budget at required public hearings

D) By issuing hedge contracts on all projected purchases for the year

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

29

Some Enterprise Funds report special assessments as a revenue source. Which of the following is most descriptive of those assessments or fees?

A) Special assessments are charged when the services provided benefit one group of citizens

More than the general public

B) Special assessments replace capital grants

C) Special assessments can only be used to purchase or construct capital assets

D) Special assessments can only be used to pay for noncapital assets

A) Special assessments are charged when the services provided benefit one group of citizens

More than the general public

B) Special assessments replace capital grants

C) Special assessments can only be used to purchase or construct capital assets

D) Special assessments can only be used to pay for noncapital assets

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

30

The Potomac River Electricity Enterprise Fund (PREEF) has a limited group of customers who receive special street lighting designed to provide higher security than for its regular customers. PREEF uses special assessments to finance the services it provides to this limited group. What effect does this have on PREEF's financial reporting?

A) EFs are required to report special assessment revenues on the modified accrual basis

B) Special assessment revenues are reported using the same accounting used for other EF

Revenues, except that the revenues and receivables are described as special assessments.

C) EF special assessments are reported on the cash basis

D) EF special assessments must be separately reported in Special Revenue Funds

A) EFs are required to report special assessment revenues on the modified accrual basis

B) Special assessment revenues are reported using the same accounting used for other EF

Revenues, except that the revenues and receivables are described as special assessments.

C) EF special assessments are reported on the cash basis

D) EF special assessments must be separately reported in Special Revenue Funds

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

31

Which of the following is true about activities that are reported both by governments and by commercial and nonprofit entities?

A) Colleges and universities that are operated by state governments use the same accounting

Standards as those operated as private colleges by nonprofits

B) Electric utilities are reported using the same methods because, regardless of ownership, all

Are rate-regulated entities within in their respective states

C) Hospitals and colleges and universities apply the same reporting standards, regardless of

Ownership

D) None of the above

A) Colleges and universities that are operated by state governments use the same accounting

Standards as those operated as private colleges by nonprofits

B) Electric utilities are reported using the same methods because, regardless of ownership, all

Are rate-regulated entities within in their respective states

C) Hospitals and colleges and universities apply the same reporting standards, regardless of

Ownership

D) None of the above

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

32

In some circumstances, Enterprise Funds are permitted to report capital assets using the modified approach? What is one reason why the GASB permits this method versus simple depreciation accounting required by the FASB for businesses?

A) Businesses do not invest in infrastructure assets

B) It would not be possible for businesses to meet the record-keeping requirements of the

Modified approach

C) Governments are expected to exist in perpetuity, unlike businesses, which may be sold or

Simply close

D) Businesses must answer to stockholders; governments do not sell shares of stock

A) Businesses do not invest in infrastructure assets

B) It would not be possible for businesses to meet the record-keeping requirements of the

Modified approach

C) Governments are expected to exist in perpetuity, unlike businesses, which may be sold or

Simply close

D) Businesses must answer to stockholders; governments do not sell shares of stock

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

33

One significant difference between how the GASB and the FASB report retiree benefits, such as pensions, is that businesses report the difference between actuarial projections versus actual results immediately in comprehensive income. Actuarial differences calculated by governmental entities are deferred and amortized. What reason does the GASB give for this treatment?

A) Governments rarely go out of business, while a company could be sold at any time

B) Actuarial projections generally aren't reliable; this softens the effect of mismeasurement

C) Governments will be able to cover the cost of retiree benefits with property taxes, which will

Always be available

D) Governments do not like the "lumpiness" that immediate recognition causes in retiree benefit expenses

A) Governments rarely go out of business, while a company could be sold at any time

B) Actuarial projections generally aren't reliable; this softens the effect of mismeasurement

C) Governments will be able to cover the cost of retiree benefits with property taxes, which will

Always be available

D) Governments do not like the "lumpiness" that immediate recognition causes in retiree benefit expenses

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

34

The FASB and GASB both have standards for reporting capital asset impairment but with different results. Which of the following is not one of the three methods required by the GASB or the FASB for calculating the impairment of capital assets?

A) Cost to restore the service utility of an asset

B) Difference between the sums of discounted cash flows that are expected to be received

From using an impaired asset compared to that asset's fair value

C) Comparing the service units the asset could have provided before its impairment compared

To after its impairment

D) Difference between the estimated costs to buy an impaired asset in its current condition versus the entity's carrying cost of the asset before impairment

A) Cost to restore the service utility of an asset

B) Difference between the sums of discounted cash flows that are expected to be received

From using an impaired asset compared to that asset's fair value

C) Comparing the service units the asset could have provided before its impairment compared

To after its impairment

D) Difference between the estimated costs to buy an impaired asset in its current condition versus the entity's carrying cost of the asset before impairment

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

35

The GASB and FASB accounting requirements for reporting leases are similar because:

A) Both standards distinguish operating leases from finance leases

B) Both had the overarching goal of reporting a transaction that conveys the right to use another entity's asset for an agreed-upon period

C) Both standards distinguish between short- and long-term leases

D) Both standards address leasing capital assets

A) Both standards distinguish operating leases from finance leases

B) Both had the overarching goal of reporting a transaction that conveys the right to use another entity's asset for an agreed-upon period

C) Both standards distinguish between short- and long-term leases

D) Both standards address leasing capital assets

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

36

Jockey City operates FUNaquatic Park that meets the GASB definition of an Enterprise Fund (EF). In 2018, the EF enters into a 20-year agreement with Coco's Cabanas to lease shower facilities and changing rooms for the park. If the City were to buy the equipment, it would cost $320,000. Assuming that the present value of the lease payments is $281,526, how should the EF initially report the lease?

A) As a debit to Capital asset-cabanas and shower facilities for $281,526 and a credit to Lease notes payable for the same amount

B) As a debit to Intangible asset-lease for $281,526 and a credit to Lease payable for the same amount

C) The leased asset and present value of the lease payments should be reported in Jockey City's General Fund

D) As a debit to Capital assets-cabanas and shower facilities for $320,000 and a credit for $281,526 to Lease payable and a credit for $38,474 to Deferred interest expense-leases

A) As a debit to Capital asset-cabanas and shower facilities for $281,526 and a credit to Lease notes payable for the same amount

B) As a debit to Intangible asset-lease for $281,526 and a credit to Lease payable for the same amount

C) The leased asset and present value of the lease payments should be reported in Jockey City's General Fund

D) As a debit to Capital assets-cabanas and shower facilities for $320,000 and a credit for $281,526 to Lease payable and a credit for $38,474 to Deferred interest expense-leases

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

37

The City of Casa Cortez uses an Internal Service Fund (ISF) to provide centralized printing services for all City agencies. City agencies are billed on a per-page basis (number of pages in a document times the number of documents printed). The City requires the ISF to develop its billing rate that it recovers all costs on the accrual basis of accounting, plus the cost of repaying a $400,000 start-up loan made by the City to the ISF. Compute the rate per page to be charged by the ISF, based on the following factors:

a. Start-up loan from City to ISF - $400,000 non-interest bearing loan, to be

repaid in equal payments over 10 years

b. Printing equipment - estimated to cost $300,000 and to have an average life of

10 years

c. Personnel costs - Estimated salaries of $500,000, plus contribution to Pension

Trust Fund of 10% of salaries

d. Paper- Opening inventory of $16,000; expected purchases of $72,000;

expected ending inventory of $12,000

e. Occupancy costs - Estimated at $50,000 per year

f. Expected number of pages to be printed - 20 million.

a. Start-up loan from City to ISF - $400,000 non-interest bearing loan, to be

repaid in equal payments over 10 years

b. Printing equipment - estimated to cost $300,000 and to have an average life of

10 years

c. Personnel costs - Estimated salaries of $500,000, plus contribution to Pension

Trust Fund of 10% of salaries

d. Paper- Opening inventory of $16,000; expected purchases of $72,000;

expected ending inventory of $12,000

e. Occupancy costs - Estimated at $50,000 per year

f. Expected number of pages to be printed - 20 million.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

38

Twizzle City establishes an Internal Service Fund (ISF) to account for the costs of printing services that it will provide to the various City departments. Make journal entries to record the following transactions in the ISF only.

a. The General Fund transfers $425,000 to the ISF as a contribution to start the printing activity.

b. The ISF immediately uses $400,000 of the cash to purchase printing equipment. (The printing equipment is estimated to have an average useful life of 8 years.)

c. On various occasions during the year, the ISF buys paper and other supplies in the amount of $90,000 on open account. The supplies are put into inventory.

d. Invoices for the supplies purchased in c., above are paid.

e. Employee salaries for the year amounting to $345,000 are paid.

f. The ISF makes a payment of $41,000 for defined contribution pensions for its personnel.

g. The ISF receives an invoice of $28,000 from the General Fund for occupancy costs, which includes space and utility costs.

h. The ISF sends invoices throughout the year to several City agencies for printing services, as follows:

(1) To General Fund departments $575,000

(2) To the Water Enterprise Fund 9,500

i. The ISF receives payments of $555,000 from General Fund agencies and $9,500 from the Water Enterprise Fund.

To prepare its financial statements, the ISF must make adjusting entries to account for the following:

j. To record one-year's depreciation on the equipment purchased in b., above.

k. To record the expense of paper and supplies consumed during the year. A year-end inventory showed unused paper and supplies amounting to $8,000. (See c., above.)

l. To record unpaid salaries of $13,500.

a. The General Fund transfers $425,000 to the ISF as a contribution to start the printing activity.

b. The ISF immediately uses $400,000 of the cash to purchase printing equipment. (The printing equipment is estimated to have an average useful life of 8 years.)

c. On various occasions during the year, the ISF buys paper and other supplies in the amount of $90,000 on open account. The supplies are put into inventory.

d. Invoices for the supplies purchased in c., above are paid.

e. Employee salaries for the year amounting to $345,000 are paid.

f. The ISF makes a payment of $41,000 for defined contribution pensions for its personnel.

g. The ISF receives an invoice of $28,000 from the General Fund for occupancy costs, which includes space and utility costs.

h. The ISF sends invoices throughout the year to several City agencies for printing services, as follows:

(1) To General Fund departments $575,000

(2) To the Water Enterprise Fund 9,500

i. The ISF receives payments of $555,000 from General Fund agencies and $9,500 from the Water Enterprise Fund.

To prepare its financial statements, the ISF must make adjusting entries to account for the following:

j. To record one-year's depreciation on the equipment purchased in b., above.

k. To record the expense of paper and supplies consumed during the year. A year-end inventory showed unused paper and supplies amounting to $8,000. (See c., above.)

l. To record unpaid salaries of $13,500.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

39

These transactions relate to Metro Bus, which provides transportation services to residents of Parker County. Metro Bus is accounted for as a County Enterprise Fund. Make journal entries to account for the following 2018 transactions in the Enterprise Fund.

a. On April 1, 2018, Metro borrows $3,000,000 by issuing 10-year revenue bonds. Bond principal is to be paid back in 20 equal semi-annual installments, starting October 1, 2018, together with interest of 6% a year on the unpaid principal.

b. On July 1, Metro pays cash for 10 buses costing $150,000 each. Metro also pays cash for land costing $100,000 and a building costing $900,000 to house its repair activity.

c. On July 1, Metro invests $200,000 of unused cash in a Certificate of Deposit (CD).

d. Metro pays cash of $50,000 to acquire an inventory of repair parts.

e. Metro collects bus fares of $900,000, which it deposits in the bank.

f. Metro sends an invoice for $10,000 to the County Social Services Agency for taking senior citizens on bus tours. That Agency receives appropriations from the General Fund.

g. Metro pays salaries of $500,000 to its bus operators, mechanics, and administrative staff.

h. The CD (transaction c.) matures and Metro receives a check for $203,000.

i. On October 1, 2018, Metro pays the first installment of principal and interest on the revenue bonds in transaction a.

To prepare its financial statements at December 31, 2018, Metro must make adjusting journal entries for the following items:

j. To record six months' depreciation on the buses and building bought in transaction b. Estimated lives are: buses - 10 years; building - 30 years.

k. To record consumption of repair parts. A year-end physical inventory shows repair parts on hand amounting to $8,000. (See transaction d.)

l. To accrue for unpaid salaries of $12,000.

m. To accrue interest on the revenue bonds outstanding at December 31, 2018. (See transactions a. and i.)

a. On April 1, 2018, Metro borrows $3,000,000 by issuing 10-year revenue bonds. Bond principal is to be paid back in 20 equal semi-annual installments, starting October 1, 2018, together with interest of 6% a year on the unpaid principal.

b. On July 1, Metro pays cash for 10 buses costing $150,000 each. Metro also pays cash for land costing $100,000 and a building costing $900,000 to house its repair activity.

c. On July 1, Metro invests $200,000 of unused cash in a Certificate of Deposit (CD).

d. Metro pays cash of $50,000 to acquire an inventory of repair parts.

e. Metro collects bus fares of $900,000, which it deposits in the bank.

f. Metro sends an invoice for $10,000 to the County Social Services Agency for taking senior citizens on bus tours. That Agency receives appropriations from the General Fund.

g. Metro pays salaries of $500,000 to its bus operators, mechanics, and administrative staff.

h. The CD (transaction c.) matures and Metro receives a check for $203,000.

i. On October 1, 2018, Metro pays the first installment of principal and interest on the revenue bonds in transaction a.

To prepare its financial statements at December 31, 2018, Metro must make adjusting journal entries for the following items:

j. To record six months' depreciation on the buses and building bought in transaction b. Estimated lives are: buses - 10 years; building - 30 years.

k. To record consumption of repair parts. A year-end physical inventory shows repair parts on hand amounting to $8,000. (See transaction d.)

l. To accrue for unpaid salaries of $12,000.

m. To accrue interest on the revenue bonds outstanding at December 31, 2018. (See transactions a. and i.)

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

40

Cottenec Memorial Golf Course is reported as an Enterprise Fund (EF) of LeCorre City. In 2018, the EF leased professional restaurant equipment based on a 20-year lease agreement with French Cooks, Inc. The City has determined that the present value of the lease payments (at 5%) is $443,000.

Provide entries to:

a. Record the long-term equipment lease.

b. Record a required initial lease payment of $150,000 that must be paid at the time the

equipment is installed.

Provide entries to:

a. Record the long-term equipment lease.

b. Record a required initial lease payment of $150,000 that must be paid at the time the

equipment is installed.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

41

Presented on the following page is the adjusted trial balance for the Water Enterprise Fund of the City of Whitt at December 31, 2018, the end of its fiscal year. Based on this information:

a. Prepare the entry necessary to close the accounts

b. Compute the ending fund net position balances for (1) net investment in capital assets, (2) restricted net position, and (3) unrestricted net position

(Note: Debt related to the capital assets consists solely of the City's revenue bonds payable.)

a. Prepare the entry necessary to close the accounts

b. Compute the ending fund net position balances for (1) net investment in capital assets, (2) restricted net position, and (3) unrestricted net position

(Note: Debt related to the capital assets consists solely of the City's revenue bonds payable.)

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

42

The City of Deshields establishes an Internal Service Fund (ISF) to provide limousine services to all City agencies. The Mayor's office activity is recorded in the City's General Fund. The ISF has concluded that each of its limousines should be billed out to the City at a rate of $150 per hour. Based on this information, prepare journal entries to record the following transactions in all of the appropriate City funds.

a. The City's General Fund contributes $300,000 to the ISF to allow it to purchase limousines and set up operations.

b. The ISF purchases two used limousines for $190,000 in cash.

c. The Mayor spends the day at the state capitol representing the City in property tax hearings. Limousine A was used for 10 hours. The ISF bills the Mayor's office for the service.

d. The head of the City's Electric Utility Enterprise Fund and the City Controller attend a ribbon cutting ceremony celebrating the opening of the new electric plant. Both limousines were used for 7 hours each. The ISF bills the Mayor's office and the EF for the service.

e. The Mayor's office pays for the services billed to the General Fund in transactions c. and d.

f. The ISF pays $3,000 to its drivers for their services for the month.

a. The City's General Fund contributes $300,000 to the ISF to allow it to purchase limousines and set up operations.

b. The ISF purchases two used limousines for $190,000 in cash.

c. The Mayor spends the day at the state capitol representing the City in property tax hearings. Limousine A was used for 10 hours. The ISF bills the Mayor's office for the service.

d. The head of the City's Electric Utility Enterprise Fund and the City Controller attend a ribbon cutting ceremony celebrating the opening of the new electric plant. Both limousines were used for 7 hours each. The ISF bills the Mayor's office and the EF for the service.

e. The Mayor's office pays for the services billed to the General Fund in transactions c. and d.

f. The ISF pays $3,000 to its drivers for their services for the month.

Unlock Deck

Unlock for access to all 42 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 42 flashcards in this deck.