Deck 6: Activity-Based Costing, Customer Profitability, and Activity-Based Management

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

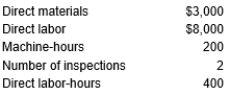

Doggle, Inc. has two categories of overhead: maintenance and inspection. Costs expected for these categories for the coming year are as follows:

The following data have been assembled for use in developing a bid for a proposed job:

The following data have been assembled for use in developing a bid for a proposed job:

The practical capacity of machine-hours for all jobs during the year is 12,500, and for inspections is 400. These are the cost drivers for maintenance and inspection costs, respectively.

The practical capacity of machine-hours for all jobs during the year is 12,500, and for inspections is 400. These are the cost drivers for maintenance and inspection costs, respectively.

Using the appropriate cost drivers, the total cost of the potential job is:

A) $11,000

B) $18,400

C) $16,300

D) $36,800

The following data have been assembled for use in developing a bid for a proposed job: The practical capacity of machine-hours for all jobs during the year is 12,500, and for inspections is 400. These are the cost drivers for maintenance and inspection costs, respectively.Using the appropriate cost drivers, the total cost of the potential job is:

A) $11,000

B) $18,400

C) $16,300

D) $36,800

Question

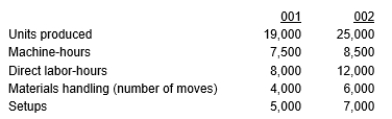

Joshua, Inc. uses activity-based costing. The company produces two products, 001 and 002. Information relating to the two products is as follows:

The following costs are reported:

The following costs are reported:

Setup costs assigned to 002 are:

Setup costs assigned to 002 are:

A) $140,000

B) $112,000

C) $175,000

D) $144,000

The following costs are reported: Setup costs assigned to 002 are:A) $140,000

B) $112,000

C) $175,000

D) $144,000

Question

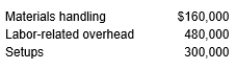

Hanna, Inc. uses activity-based costing. The company produces X and Y. Information relating to the two products is as follows:

The following costs are reported:

The following costs are reported:

Labor-related overhead costs assigned to product X are:

Labor-related overhead costs assigned to product X are:

A) $192,000

B) $232,000

C) $112,000

D) $224,000

The following costs are reported: Labor-related overhead costs assigned to product X are:A) $192,000

B) $232,000

C) $112,000

D) $224,000

Question

Question

Question

Question

Question

The following information is available pertaining to Evan Division that uses a plantwide overhead rate based on machine hours:

Production information pertaining to Job 501:

Production information pertaining to Job 501:

What are the total overhead costs assigned to Job 501?

What are the total overhead costs assigned to Job 501?

A) $240

B) $207

C) $360

D) $180

Production information pertaining to Job 501: What are the total overhead costs assigned to Job 501?A) $240

B) $207

C) $360

D) $180

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Ace, Inc. has three activity pools which have the following costs:

The activity cost drivers (and driver quantity) for the three pools are, respectively, number of setups (100), number of material moves (220), and number of machine hours (175).

The activity cost drivers (and driver quantity) for the three pools are, respectively, number of setups (100), number of material moves (220), and number of machine hours (175).

Product G10 used the following quantity of activity drivers to produce 100 units of final product:

?12 setups

?20 material moves, and

?32 machine hours.

The total ABC cost and unit ABC cost assigned to Product G10 is:

A) $ 3,630 total ABC cost and $ 36.30 unit ABC cost

B) $10,300 total ABC cost and $103.00 unit ABC cost

C) $ 6,360 total ABC cost and $ 63.60 unit ABC cost

D) $ 3,300 total ABC cost and $330.00 unit ABC cost

The activity cost drivers (and driver quantity) for the three pools are, respectively, number of setups (100), number of material moves (220), and number of machine hours (175).Product G10 used the following quantity of activity drivers to produce 100 units of final product:

?12 setups

?20 material moves, and

?32 machine hours.

The total ABC cost and unit ABC cost assigned to Product G10 is:

A) $ 3,630 total ABC cost and $ 36.30 unit ABC cost

B) $10,300 total ABC cost and $103.00 unit ABC cost

C) $ 6,360 total ABC cost and $ 63.60 unit ABC cost

D) $ 3,300 total ABC cost and $330.00 unit ABC cost

Question

Question

Question

Question

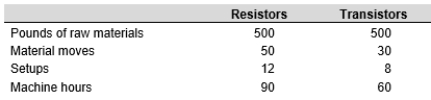

Jasmine Electronics Company produces two products, Resistors and Transistors in a small manufacturing plant. During June, Jasmine Electronics produced 100 units of Resistors and 100 units of Transistors incurring a total manufacturing overhead cost of $21,000. Assume Jasmine Electronics uses Activity Based Costing and that its total manufacturing overhead costs of $21,000 were assigned to the following:

ABC cost pools:

Resistors and Transistors used the following quantities of the four activity drivers:

Resistors and Transistors used the following quantities of the four activity drivers:

The overhead costs assigned to each unit of Resistors and Transistors using the Activity based costing were:

The overhead costs assigned to each unit of Resistors and Transistors using the Activity based costing were:

A) $93.50 for Resistors and $116.50 for Transistors

B) $116.50 for Resistors and $93.50 for Transistors

C) $11,650 for Resistors and $9,350 for Transistors

D) $225 for Resistors and $225 for Transistors

ABC cost pools:

Resistors and Transistors used the following quantities of the four activity drivers: The overhead costs assigned to each unit of Resistors and Transistors using the Activity based costing were:A) $93.50 for Resistors and $116.50 for Transistors

B) $116.50 for Resistors and $93.50 for Transistors

C) $11,650 for Resistors and $9,350 for Transistors

D) $225 for Resistors and $225 for Transistors

Question

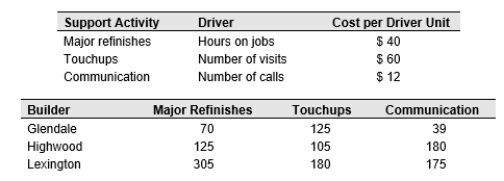

Premier Painting Services, Inc. provides residential painting services for three home building companies, Glendale, Highwood, and Lexington, and it uses a job costing system for determining the costs for completing each job. The job cost system does not capture any cost incurred by Premier for return touchups and refinishes after the homeowner occupies the home. Premier paints each house on a square footage contract price, which includes painting as well as all refinishes and touchups required after the homes are occupied.

Each year, the company generates about one-third of its total revenues and gross profits from each of the three builders. The Premier owner has observed that the builders, however, require substantially different levels of support following the completion of jobs.

The following data have been gathered:

Assume that each of the three customers produces Gross Profit of $50,000.

Assume that each of the three customers produces Gross Profit of $50,000.

The profitability from each builder after taking into account the support activity required for each builder is:

A) $39,232 Glendale, $36,540 Highwood, $24,900 Lexington

B) $35,540 Glendale, $40,140 Highwood, $36,040 Lexington

C) $40,140 Glendale, $35,540 Highwood, $36,540 Lexington

D) $40,000 Glendale, $35,000 Highwood, $38,000 Lexington

Each year, the company generates about one-third of its total revenues and gross profits from each of the three builders. The Premier owner has observed that the builders, however, require substantially different levels of support following the completion of jobs.

The following data have been gathered:

Assume that each of the three customers produces Gross Profit of $50,000.The profitability from each builder after taking into account the support activity required for each builder is:

A) $39,232 Glendale, $36,540 Highwood, $24,900 Lexington

B) $35,540 Glendale, $40,140 Highwood, $36,040 Lexington

C) $40,140 Glendale, $35,540 Highwood, $36,540 Lexington

D) $40,000 Glendale, $35,000 Highwood, $38,000 Lexington

Question

Jason Company manufactures two products: A and B. The overhead costs have been divided into four activity pools that use the following cost drivers:

Required:

Required:

a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Required:a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Question

Farrow Corporation manufactures two products: A and B. The total indirect manufacturing overhead resource costs of $100,350 have been assigned to four activity cost pools that use the following cost drivers:

Required:

Required:

a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Required:a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Question

Question

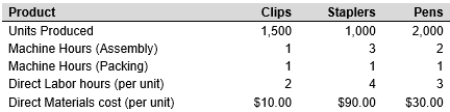

Chester Corp. produces three products: Clips, Staples, and Pens. Chester uses a plantwide overhead rate based on machine hours. The following information is available for the next period:  Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $250,000 for the Packing Department.Calculate the total product cost per unit of Pens.

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $250,000 for the Packing Department.Calculate the total product cost per unit of Pens.

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $250,000 for the Packing Department.Calculate the total product cost per unit of Pens. Question

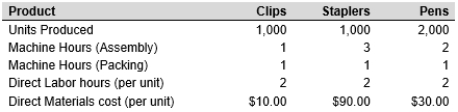

Chester Corp. produces three products: Clips, Staples, and Pens. Chester uses department overhead rates for Assembly and Packing, both of which are based on machine hours. The following information is available for the next period:  Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the total product cost per unit of Pens.

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the total product cost per unit of Pens.

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the total product cost per unit of Pens. Question

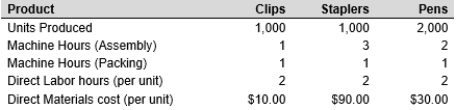

Chester Corp. produces three products: Clips, Staples, and Pens. Chester uses department overhead rates for Assembly and Packing, both of which are based on machine hours. The following information is available for the next period:  Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $420,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the effect of using a plantwide rate as opposed to departmental overhead rates on the three products. (Round to two decimal places, when necessary.)

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $420,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the effect of using a plantwide rate as opposed to departmental overhead rates on the three products. (Round to two decimal places, when necessary.)

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $420,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the effect of using a plantwide rate as opposed to departmental overhead rates on the three products. (Round to two decimal places, when necessary.) Question

Question

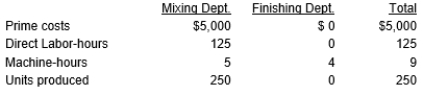

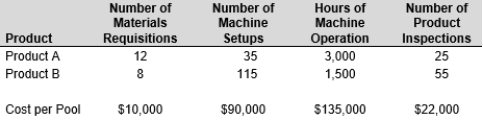

Tiger Company has identified the following overhead costs and cost drivers for next year:

The following are two of the jobs completed during the year:

The following are two of the jobs completed during the year:

Determine the unit cost for each job using the four cost drivers. (Round amounts to 2 decimal places.)

Determine the unit cost for each job using the four cost drivers. (Round amounts to 2 decimal places.)

The following are two of the jobs completed during the year: Determine the unit cost for each job using the four cost drivers. (Round amounts to 2 decimal places.) Question

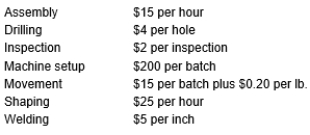

Angel Manufacturing Company has developed the following activity cost information for its manufacturing activities:

Filling a batch order for 45 units with a combined weight of 200 pounds required:

Filling a batch order for 45 units with a combined weight of 200 pounds required:

●Three sets of inspections per unit

●Drilling four holes in each unit

●Completing 20 inches of welds on each unit

●0.6 hour of shaping for each unit

●One hour of assembly per unit

Calculate the total cost to produce a batch of 45 units.

Filling a batch order for 45 units with a combined weight of 200 pounds required:●Three sets of inspections per unit

●Drilling four holes in each unit

●Completing 20 inches of welds on each unit

●0.6 hour of shaping for each unit

●One hour of assembly per unit

Calculate the total cost to produce a batch of 45 units.

Question

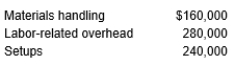

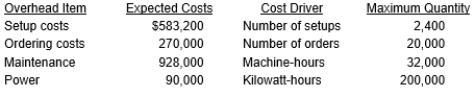

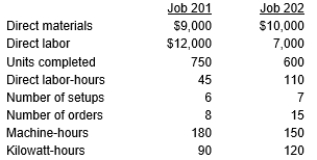

Stanford Corporation has four categories of overhead. The expected overhead costs for each category for next year are as follows:

The company has been asked to submit a bid for a proposed job. The plant manager believes that obtaining this job would result in new business in future years. Bids are usually based upon full manufacturing cost plus 30 percent. Estimates for the proposed job are as follows:

The company has been asked to submit a bid for a proposed job. The plant manager believes that obtaining this job would result in new business in future years. Bids are usually based upon full manufacturing cost plus 30 percent. Estimates for the proposed job are as follows:

Expected activity for the four activity-based cost drivers that would be used is:

Expected activity for the four activity-based cost drivers that would be used is:

Required:

Required:

a. Determine the amount of overhead that would be allocated to the proposed job if 20,000 direct labor-hours are used as the volume-based cost driver. Determine the total costs of the proposed job. Determine the company's bid, if the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

b. Determine the amount of overhead that would be applied to the proposed project if activity-based costing is used. Determine the total costs of the proposed job if activity-based costing is used. Determine the company's bid if activity-based costing is used and the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

c. Which product costing method produces the more competitive bid?

The company has been asked to submit a bid for a proposed job. The plant manager believes that obtaining this job would result in new business in future years. Bids are usually based upon full manufacturing cost plus 30 percent. Estimates for the proposed job are as follows: Expected activity for the four activity-based cost drivers that would be used is: Required:a. Determine the amount of overhead that would be allocated to the proposed job if 20,000 direct labor-hours are used as the volume-based cost driver. Determine the total costs of the proposed job. Determine the company's bid, if the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

b. Determine the amount of overhead that would be applied to the proposed project if activity-based costing is used. Determine the total costs of the proposed job if activity-based costing is used. Determine the company's bid if activity-based costing is used and the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

c. Which product costing method produces the more competitive bid?

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/50

Play

Full screen (f)

Deck 6: Activity-Based Costing, Customer Profitability, and Activity-Based Management

1

The twentieth century saw an accelerating shift from traditional manufacturing activities to production procedures requiring large investments in raw materials and labor.

False

2

Over the past century, overhead costs have increased as a percentage of total product cost.

True

3

Activity-based costing determines the cost of activities and traces their costs to cost objects on the basis of the cost object's utilization of units of activity.

True

4

The number of purchase orders is a reasonable basis for allocating to jobs the purchasing department costs.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

5

The plantwide rate approach is the simplest to apply, but it is also the most costly to implement, compared to a departmental or activity-based cost allocation system.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

6

ABC is useful for product costing, but traditional costing is superior for customer profitability.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

7

If products are being sold to customers A and B above costs and the company is earning a profit, then customers A and B must both be profitable.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

8

Activity-based management (ABM) focuses on reducing costs and maximizing value to consumers.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

9

The most appropriate cost driver for the activity of cleaning (bussing) tables in a restaurant is:

A) The number of cooks in the kitchen

B) The number of tables cleaned

C) The number of employees assigned to the job of cleaning tables

D) The amount of money deposited to the bank each day

A) The number of cooks in the kitchen

B) The number of tables cleaned

C) The number of employees assigned to the job of cleaning tables

D) The amount of money deposited to the bank each day

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following statements about activity based costing is true?

A) The most widely used approach to activity-based costing involves the use of a two-stage model.

B) Activity-based costing involves tracing the cost of activities used by the various cost objects.

C) Activity-based costing involves determining the cost of activities.

D) All of the above

A) The most widely used approach to activity-based costing involves the use of a two-stage model.

B) Activity-based costing involves tracing the cost of activities used by the various cost objects.

C) Activity-based costing involves determining the cost of activities.

D) All of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

11

An object to which costs are assigned is called:

A) A value chain

B) A cost object

C) A cost pool

D) Overhead

A) A value chain

B) A cost object

C) A cost pool

D) Overhead

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following procedures best describes activity-based costing?

A) All overhead costs are recorded as expenses as incurred.

B) Overhead costs are assigned directly to products.

C) Overhead costs are assigned to activities; then costs are assigned to products.

D) Overhead costs are assigned to departments; then costs are assigned to products.

A) All overhead costs are recorded as expenses as incurred.

B) Overhead costs are assigned directly to products.

C) Overhead costs are assigned to activities; then costs are assigned to products.

D) Overhead costs are assigned to departments; then costs are assigned to products.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

13

Which of the following tasks is not required when using a two-stage activity-based costing model?

A) Identifying activities

B) Assigning costs to activities

C) Determining how much direct labor each cost object consumes

D) Determining the cost per unit of activity

A) Identifying activities

B) Assigning costs to activities

C) Determining how much direct labor each cost object consumes

D) Determining the cost per unit of activity

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

14

In a two-stage activity-based costing model, stage one involves:

A) Assigning activity costs to cost objects

B) Measuring the various indirect resource costs and determining resource drivers

C) Assigning indirect resource costs to activity pools

D) Assigning direct costs to cost objects

A) Assigning activity costs to cost objects

B) Measuring the various indirect resource costs and determining resource drivers

C) Assigning indirect resource costs to activity pools

D) Assigning direct costs to cost objects

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

15

In an activity-based costing model, total costs assigned to cost objects may include:

A) Only direct costs

B) Both direct costs and resource costs

C) Both activity costs and resource costs

D) Both direct costs and activity costs

A) Only direct costs

B) Both direct costs and resource costs

C) Both activity costs and resource costs

D) Both direct costs and activity costs

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

16

Doggle, Inc. has two categories of overhead: maintenance and inspection. Costs expected for these categories for the coming year are as follows:

The following data have been assembled for use in developing a bid for a proposed job:

The practical capacity of machine-hours for all jobs during the year is 12,500, and for inspections is 400. These are the cost drivers for maintenance and inspection costs, respectively.

Using the appropriate cost drivers, the total cost of the potential job is:

A) $11,000

B) $18,400

C) $16,300

D) $36,800

The following data have been assembled for use in developing a bid for a proposed job: The practical capacity of machine-hours for all jobs during the year is 12,500, and for inspections is 400. These are the cost drivers for maintenance and inspection costs, respectively.Using the appropriate cost drivers, the total cost of the potential job is:

A) $11,000

B) $18,400

C) $16,300

D) $36,800

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

17

Joshua, Inc. uses activity-based costing. The company produces two products, 001 and 002. Information relating to the two products is as follows:

The following costs are reported:

Setup costs assigned to 002 are:

A) $140,000

B) $112,000

C) $175,000

D) $144,000

The following costs are reported: Setup costs assigned to 002 are:A) $140,000

B) $112,000

C) $175,000

D) $144,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

18

Hanna, Inc. uses activity-based costing. The company produces X and Y. Information relating to the two products is as follows:

The following costs are reported:

Labor-related overhead costs assigned to product X are:

A) $192,000

B) $232,000

C) $112,000

D) $224,000

The following costs are reported: Labor-related overhead costs assigned to product X are:A) $192,000

B) $232,000

C) $112,000

D) $224,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is a true characteristic of activity-based costing?

A) Activity-based costing uses a smaller number of cost pools than does organizational-based costing.

B) Relative to traditional costing methods, activity-based costing is more concerned with identifying processes and less concerned with causal factors of overhead costs.

C) Activity-based costing removes the use of judgment from the allocation process.

D) Activity-based costing cannot be used to assign costs unless the activity cost drivers of those costs are identified.

A) Activity-based costing uses a smaller number of cost pools than does organizational-based costing.

B) Relative to traditional costing methods, activity-based costing is more concerned with identifying processes and less concerned with causal factors of overhead costs.

C) Activity-based costing removes the use of judgment from the allocation process.

D) Activity-based costing cannot be used to assign costs unless the activity cost drivers of those costs are identified.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

20

The second stage of an activity-based costing two-stage product costing model includes:

A) Assignment of cost pools to products

B) Assignment of cost pools to cost centers

C) Assignment of resource costs to cost pools

D) All of the above

A) Assignment of cost pools to products

B) Assignment of cost pools to cost centers

C) Assignment of resource costs to cost pools

D) All of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

21

Assume that total costs assigned to the setup activity cost pool in June are $60,000 and 50 setups were completed in June. Further, assume that during June machines were setup 10 times to make product G10.

The total setup cost that would be assigned to product G10 would be:

A) $ 1,600

B) $12,000

C) Cannot be determined

D) $24,000

The total setup cost that would be assigned to product G10 would be:

A) $ 1,600

B) $12,000

C) Cannot be determined

D) $24,000

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

22

The practical capacity for a particular production facility is best described as:

A) The highest level of activity possible allowing for normal repairs and maintenance

B) The highest level of activity possible under any circumstance

C) The highest level of activity at which average costs are minimized

D) The level of activity that makes the most practical sense within the framework of a given situation

A) The highest level of activity possible allowing for normal repairs and maintenance

B) The highest level of activity possible under any circumstance

C) The highest level of activity at which average costs are minimized

D) The level of activity that makes the most practical sense within the framework of a given situation

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

23

The following information is available pertaining to Evan Division that uses a plantwide overhead rate based on machine hours:

Production information pertaining to Job 501:

What are the total overhead costs assigned to Job 501?

A) $240

B) $207

C) $360

D) $180

Production information pertaining to Job 501: What are the total overhead costs assigned to Job 501?A) $240

B) $207

C) $360

D) $180

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following product costing methods produces the most precise product costing information?

A) Activity-based costing

B) Departmental overhead rate methods

C) Organization-based costing

D) Plantwide overhead rates

A) Activity-based costing

B) Departmental overhead rate methods

C) Organization-based costing

D) Plantwide overhead rates

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

25

Activity-based costing is a technique for more precisely measuring the cost and profitability of:

A) Products

B) Customers

C) Distribution channels

D) All of the above

A) Products

B) Customers

C) Distribution channels

D) All of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

26

Which of the following aspects of manufacturing must be understood in order to implement activity based costing in a production setting?

A) The production process

B) The activities that occur in the production process must be known

C) The cost drivers that generate activities within the production process

D) All of the above

A) The production process

B) The activities that occur in the production process must be known

C) The cost drivers that generate activities within the production process

D) All of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

27

Which of the following statements describes the typical effect of creating a large number of refined activity cost pools for a given costing application?

A) A complex ABC system with numerous cost pools provides substantial cost improvement over a smaller system with only seven to ten cost pools.

B) A system containing a large number of cost pools will not tend to exhibit substantial cost accuracy over a system containing seven to ten cost pools.

C) With the aid of a computer, every public company should strive to develop as many cost pools as possible because there is virtually no disadvantage of so doing.

D) Employees normally develop a deep appreciation for the complexity of a large, tedious ABC system.

A) A complex ABC system with numerous cost pools provides substantial cost improvement over a smaller system with only seven to ten cost pools.

B) A system containing a large number of cost pools will not tend to exhibit substantial cost accuracy over a system containing seven to ten cost pools.

C) With the aid of a computer, every public company should strive to develop as many cost pools as possible because there is virtually no disadvantage of so doing.

D) Employees normally develop a deep appreciation for the complexity of a large, tedious ABC system.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

28

Activity-based costing systems tend to _____________________ high-volume, low-complexity products.

A) Undercost

B) Overcost

C) Accurately cost

D) None of the above

A) Undercost

B) Overcost

C) Accurately cost

D) None of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

29

Activity-based costing's primary benefit is that it provides:

A) Absolutely accurate product costing information

B) Data for external financial reporting purposes

C) More precise cost data for internal decision-making purposes

D) All of the above

A) Absolutely accurate product costing information

B) Data for external financial reporting purposes

C) More precise cost data for internal decision-making purposes

D) All of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following statements concerning activity-based management is true?

A) Activity-based management is concerned with maximizing the value of activities.

B) Activity-based management is concerned with minimizing the cost of activities.

C) Activity-based management is concerned with improving processes.

D) All of the above statements are true.

A) Activity-based management is concerned with maximizing the value of activities.

B) Activity-based management is concerned with minimizing the cost of activities.

C) Activity-based management is concerned with improving processes.

D) All of the above statements are true.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

31

_____________________ is defined as the identification and selection of activities to maximize the value of the activities while minimizing their cost from the perspective of the final consumer.

A) Activity-based costing

B) Activity-based management

C) Strategic cost management

D) None of the above

A) Activity-based costing

B) Activity-based management

C) Strategic cost management

D) None of the above

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following statements about activity-based management (ABM) is/are true?

A) ABM is concerned with how to effectively and efficiently manage activities and processes to provide value to the final consumer.

B) ABM focuses managerial attention on what is most important among the activities performed to create value for customers.

C) Defining processes and identifying key activities helps management better understand the business and to evaluate whether activities performed add value to the customer.

D) All of the above are true.

A) ABM is concerned with how to effectively and efficiently manage activities and processes to provide value to the final consumer.

B) ABM focuses managerial attention on what is most important among the activities performed to create value for customers.

C) Defining processes and identifying key activities helps management better understand the business and to evaluate whether activities performed add value to the customer.

D) All of the above are true.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

33

Ace, Inc. has three activity pools which have the following costs:

The activity cost drivers (and driver quantity) for the three pools are, respectively, number of setups (100), number of material moves (220), and number of machine hours (175).

Product G10 used the following quantity of activity drivers to produce 100 units of final product:

?12 setups

?20 material moves, and

?32 machine hours.

The total ABC cost and unit ABC cost assigned to Product G10 is:

A) $ 3,630 total ABC cost and $ 36.30 unit ABC cost

B) $10,300 total ABC cost and $103.00 unit ABC cost

C) $ 6,360 total ABC cost and $ 63.60 unit ABC cost

D) $ 3,300 total ABC cost and $330.00 unit ABC cost

The activity cost drivers (and driver quantity) for the three pools are, respectively, number of setups (100), number of material moves (220), and number of machine hours (175).Product G10 used the following quantity of activity drivers to produce 100 units of final product:

?12 setups

?20 material moves, and

?32 machine hours.

The total ABC cost and unit ABC cost assigned to Product G10 is:

A) $ 3,630 total ABC cost and $ 36.30 unit ABC cost

B) $10,300 total ABC cost and $103.00 unit ABC cost

C) $ 6,360 total ABC cost and $ 63.60 unit ABC cost

D) $ 3,300 total ABC cost and $330.00 unit ABC cost

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

34

Nano Electronics Company produces two products, Resistors and Transistors in a small manufacturing plant which had total manufacturing overhead of $21,000 in June and used 300 direct labor hours. The factory has two departments, Design, which incurred $10,000 of manufacturing overhead, and Production which incurred $11,000 of manufacturing overhead. Design used 200 hours of direct labor and Production used 80 machine hours.

During June, 150 direct labor hours were used in making 100 units of Resistors, and 150 direct labor hours were used in making 100 units of Transmitters.

If Nano Electronics Company uses a plantwide rate based on direct labor hours to assign manufacturing costs to products, the total manufacturing overhead assigned to each unit of Resistors and Transistors in June were:

A) $105 for Resistors and $105 for Transistors

B) $225 for Resistors and $225 for Transistors

C) $250 for Resistors and $200 for Transistors

D) $107.14 for Resistors, and $42.86 for Transistors

During June, 150 direct labor hours were used in making 100 units of Resistors, and 150 direct labor hours were used in making 100 units of Transmitters.

If Nano Electronics Company uses a plantwide rate based on direct labor hours to assign manufacturing costs to products, the total manufacturing overhead assigned to each unit of Resistors and Transistors in June were:

A) $105 for Resistors and $105 for Transistors

B) $225 for Resistors and $225 for Transistors

C) $250 for Resistors and $200 for Transistors

D) $107.14 for Resistors, and $42.86 for Transistors

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

35

Malta Electric Company produces two products, Resistors and Transistors in a small manufacturing plant which had total manufacturing overhead of $21,000 in June. The factory has two departments, Design, which incurred $10,000 of manufacturing overhead, and Production which incurred $11,000 of manufacturing overhead. Design used 200 hours of direct labor and Production used 80 machine hours.

During June, 150 direct labor hours were used in making 100 units of Resistors, and 150 direct labor hours were used in making 100 units of Transistors.

If Malta Electric Company uses a department rate based on direct labor hours for the Design Department and machine hours for the Production Department, the department overhead rates for the Design and Production Departments in June were:

A) $ 50 per direct labor hour for both Design and Production

B) $ 62.50 per direct labor hour for Design, and $125 per machine hour for Production

C) $125 per direct labor hour for Design, and $62.50 per machine hour for Production

D) $ 50 per direct labor hour for Design, and $137.50 per machine hour for Production

During June, 150 direct labor hours were used in making 100 units of Resistors, and 150 direct labor hours were used in making 100 units of Transistors.

If Malta Electric Company uses a department rate based on direct labor hours for the Design Department and machine hours for the Production Department, the department overhead rates for the Design and Production Departments in June were:

A) $ 50 per direct labor hour for both Design and Production

B) $ 62.50 per direct labor hour for Design, and $125 per machine hour for Production

C) $125 per direct labor hour for Design, and $62.50 per machine hour for Production

D) $ 50 per direct labor hour for Design, and $137.50 per machine hour for Production

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

36

Zion Electronics Company produces two products, Resistors and Transistors in a small manufacturing plant which had total manufacturing overhead of $21,000 in June. The factory has two departments, Design, which incurred $10,000 of manufacturing overhead, and Production which incurred $11,000 of manufacturing overhead. Design used 250 hours of direct labor and Production used 80 machine hours.

Assume that Resistors used 100 direct labor hours to make 100 units and Transistors used 150 direct labor hours to make 100 units in the Design Department. Also, assume that Resistors used 50 machine hours and Transistors used 30 machine hours in the Production Department.

The overhead costs assigned to each unit of Resistors and Transistors using department overhead rate were:

A) $ 40 for Resistors and $137.50 for Transistors

B) $177.50 for Resistors and $177.50 for Transistors

C) $108.75 for Resistors and $101.25 for Transistors

D) $234.30 for Resistors and $215.60 for Transistors

Assume that Resistors used 100 direct labor hours to make 100 units and Transistors used 150 direct labor hours to make 100 units in the Design Department. Also, assume that Resistors used 50 machine hours and Transistors used 30 machine hours in the Production Department.

The overhead costs assigned to each unit of Resistors and Transistors using department overhead rate were:

A) $ 40 for Resistors and $137.50 for Transistors

B) $177.50 for Resistors and $177.50 for Transistors

C) $108.75 for Resistors and $101.25 for Transistors

D) $234.30 for Resistors and $215.60 for Transistors

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

37

Jasmine Electronics Company produces two products, Resistors and Transistors in a small manufacturing plant. During June, Jasmine Electronics produced 100 units of Resistors and 100 units of Transistors incurring a total manufacturing overhead cost of $21,000. Assume Jasmine Electronics uses Activity Based Costing and that its total manufacturing overhead costs of $21,000 were assigned to the following:

ABC cost pools:

Resistors and Transistors used the following quantities of the four activity drivers:

The overhead costs assigned to each unit of Resistors and Transistors using the Activity based costing were:

A) $93.50 for Resistors and $116.50 for Transistors

B) $116.50 for Resistors and $93.50 for Transistors

C) $11,650 for Resistors and $9,350 for Transistors

D) $225 for Resistors and $225 for Transistors

ABC cost pools:

Resistors and Transistors used the following quantities of the four activity drivers: The overhead costs assigned to each unit of Resistors and Transistors using the Activity based costing were:A) $93.50 for Resistors and $116.50 for Transistors

B) $116.50 for Resistors and $93.50 for Transistors

C) $11,650 for Resistors and $9,350 for Transistors

D) $225 for Resistors and $225 for Transistors

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

38

Premier Painting Services, Inc. provides residential painting services for three home building companies, Glendale, Highwood, and Lexington, and it uses a job costing system for determining the costs for completing each job. The job cost system does not capture any cost incurred by Premier for return touchups and refinishes after the homeowner occupies the home. Premier paints each house on a square footage contract price, which includes painting as well as all refinishes and touchups required after the homes are occupied.

Each year, the company generates about one-third of its total revenues and gross profits from each of the three builders. The Premier owner has observed that the builders, however, require substantially different levels of support following the completion of jobs.

The following data have been gathered:

Assume that each of the three customers produces Gross Profit of $50,000.

The profitability from each builder after taking into account the support activity required for each builder is:

A) $39,232 Glendale, $36,540 Highwood, $24,900 Lexington

B) $35,540 Glendale, $40,140 Highwood, $36,040 Lexington

C) $40,140 Glendale, $35,540 Highwood, $36,540 Lexington

D) $40,000 Glendale, $35,000 Highwood, $38,000 Lexington

Each year, the company generates about one-third of its total revenues and gross profits from each of the three builders. The Premier owner has observed that the builders, however, require substantially different levels of support following the completion of jobs.

The following data have been gathered:

Assume that each of the three customers produces Gross Profit of $50,000.The profitability from each builder after taking into account the support activity required for each builder is:

A) $39,232 Glendale, $36,540 Highwood, $24,900 Lexington

B) $35,540 Glendale, $40,140 Highwood, $36,040 Lexington

C) $40,140 Glendale, $35,540 Highwood, $36,540 Lexington

D) $40,000 Glendale, $35,000 Highwood, $38,000 Lexington

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

39

Jason Company manufactures two products: A and B. The overhead costs have been divided into four activity pools that use the following cost drivers:

Required:

a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Required:a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

40

Farrow Corporation manufactures two products: A and B. The total indirect manufacturing overhead resource costs of $100,350 have been assigned to four activity cost pools that use the following cost drivers:

Required:

a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Required:a. Compute the unit activity costs for each of the cost drivers listed.

b. Assign the overhead costs to products A and B using activity-based costing.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

41

Silver Streak Company manufactures two products, A and B, and incurs overhead costs in two production departments, Mixing and Filling. The annual overhead costs in each production department are as follows:

●Mixing Dept. overhead = $155,000 + $25 per machine-hour

●Filling Dept. overhead = $280,000 + $60 per machine-hour

●Each unit of Product A requires 1 machine-hour in the Mixing Department and 3 hours in the Filling Department.

●Each unit of Product B requires 5 hours in the Mixing Department and 2 hours in the Filling Department.

During 2017, 30,000 units of A and 25,000 units of B were produced.

Calculate the total overhead costs assigned to a unit of Product B, assuming departmental overhead rates based on machine-hours are used.

●Mixing Dept. overhead = $155,000 + $25 per machine-hour

●Filling Dept. overhead = $280,000 + $60 per machine-hour

●Each unit of Product A requires 1 machine-hour in the Mixing Department and 3 hours in the Filling Department.

●Each unit of Product B requires 5 hours in the Mixing Department and 2 hours in the Filling Department.

During 2017, 30,000 units of A and 25,000 units of B were produced.

Calculate the total overhead costs assigned to a unit of Product B, assuming departmental overhead rates based on machine-hours are used.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

42

Chester Corp. produces three products: Clips, Staples, and Pens. Chester uses a plantwide overhead rate based on machine hours. The following information is available for the next period: Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $250,000 for the Packing Department.Calculate the total product cost per unit of Pens.

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $250,000 for the Packing Department.Calculate the total product cost per unit of Pens. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

43

Chester Corp. produces three products: Clips, Staples, and Pens. Chester uses department overhead rates for Assembly and Packing, both of which are based on machine hours. The following information is available for the next period: Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the total product cost per unit of Pens.

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $400,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the total product cost per unit of Pens. Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

44

Chester Corp. produces three products: Clips, Staples, and Pens. Chester uses department overhead rates for Assembly and Packing, both of which are based on machine hours. The following information is available for the next period: Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $420,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the effect of using a plantwide rate as opposed to departmental overhead rates on the three products. (Round to two decimal places, when necessary.)

Note that the direct labor wage rate is a flat $25 per hour with no overtime incurred. Also, total overhead costs are $420,000 for the Assembly Department and $240,000 for the Packing Department.Calculate the effect of using a plantwide rate as opposed to departmental overhead rates on the three products. (Round to two decimal places, when necessary.) Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

45

Silver Company manufactures two products, A and B, and incurs overhead costs in two production departments, Mixing and Filling. The annual overhead costs in each production department are as follows:

●Mixing Dept. overhead = $175,000 + $25 per machine-hour

●Filling Dept. overhead = $235,000 + $60 per machine-hour

●Each unit of Product A requires 1 machine-hour in the Mixing Department and 3 hours in the Filling Department.

●Each unit of Product B requires 5 hours in the Mixing Department and 2 hours in the Filling Department.

During 2017, 30,000 units of A and 25,000 units of B were produced.

Calculate the total overhead costs assigned to a unit of Product A, assuming plantwide overhead rates based on machine-hours are used. (Round to two decimal places, when necessary.)

●Mixing Dept. overhead = $175,000 + $25 per machine-hour

●Filling Dept. overhead = $235,000 + $60 per machine-hour

●Each unit of Product A requires 1 machine-hour in the Mixing Department and 3 hours in the Filling Department.

●Each unit of Product B requires 5 hours in the Mixing Department and 2 hours in the Filling Department.

During 2017, 30,000 units of A and 25,000 units of B were produced.

Calculate the total overhead costs assigned to a unit of Product A, assuming plantwide overhead rates based on machine-hours are used. (Round to two decimal places, when necessary.)

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

46

Tiger Company has identified the following overhead costs and cost drivers for next year:

The following are two of the jobs completed during the year:

Determine the unit cost for each job using the four cost drivers. (Round amounts to 2 decimal places.)

The following are two of the jobs completed during the year: Determine the unit cost for each job using the four cost drivers. (Round amounts to 2 decimal places.) Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

47

Angel Manufacturing Company has developed the following activity cost information for its manufacturing activities:

Filling a batch order for 45 units with a combined weight of 200 pounds required:

●Three sets of inspections per unit

●Drilling four holes in each unit

●Completing 20 inches of welds on each unit

●0.6 hour of shaping for each unit

●One hour of assembly per unit

Calculate the total cost to produce a batch of 45 units.

Filling a batch order for 45 units with a combined weight of 200 pounds required:●Three sets of inspections per unit

●Drilling four holes in each unit

●Completing 20 inches of welds on each unit

●0.6 hour of shaping for each unit

●One hour of assembly per unit

Calculate the total cost to produce a batch of 45 units.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

48

Stanford Corporation has four categories of overhead. The expected overhead costs for each category for next year are as follows:

The company has been asked to submit a bid for a proposed job. The plant manager believes that obtaining this job would result in new business in future years. Bids are usually based upon full manufacturing cost plus 30 percent. Estimates for the proposed job are as follows:

Expected activity for the four activity-based cost drivers that would be used is:

Required:

a. Determine the amount of overhead that would be allocated to the proposed job if 20,000 direct labor-hours are used as the volume-based cost driver. Determine the total costs of the proposed job. Determine the company's bid, if the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

b. Determine the amount of overhead that would be applied to the proposed project if activity-based costing is used. Determine the total costs of the proposed job if activity-based costing is used. Determine the company's bid if activity-based costing is used and the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

c. Which product costing method produces the more competitive bid?

The company has been asked to submit a bid for a proposed job. The plant manager believes that obtaining this job would result in new business in future years. Bids are usually based upon full manufacturing cost plus 30 percent. Estimates for the proposed job are as follows: Expected activity for the four activity-based cost drivers that would be used is: Required:a. Determine the amount of overhead that would be allocated to the proposed job if 20,000 direct labor-hours are used as the volume-based cost driver. Determine the total costs of the proposed job. Determine the company's bid, if the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

b. Determine the amount of overhead that would be applied to the proposed project if activity-based costing is used. Determine the total costs of the proposed job if activity-based costing is used. Determine the company's bid if activity-based costing is used and the bid is based upon full manufacturing cost plus 30 percent. (Round amounts to 2 decimal places.)

c. Which product costing method produces the more competitive bid?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

49

Comment on cost distortions commonly observed in traditional costing systems.

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

50

How can ABC used to improve customer profitability analysis?

Unlock Deck

Unlock for access to all 50 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 50 flashcards in this deck.