Deck 5: Internal Control and Cash

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

The following information pertains to Rodriguez Company:

Rodriguez should show the following reconciled cash balance from the bank reconciliation on its balance sheet:

A) $6,770

B) $8,445

C) $7,420

D) $8,055

E) None of the above

Rodriguez should show the following reconciled cash balance from the bank reconciliation on its balance sheet:

A) $6,770

B) $8,445

C) $7,420

D) $8,055

E) None of the above

Question

Williams Inc.'s June bank statement shows a June 30 balance of $9,050. Prior to reconciliation, its books show a cash balance of $9,210. The information below pertains to Williams:

The reconciled cash balance at June 30 on the bank reconciliation should be:

A) $10,100

B) $ 9,520

C) $ 9,340

D) $ 9,270

E) None of the above

The reconciled cash balance at June 30 on the bank reconciliation should be:

A) $10,100

B) $ 9,520

C) $ 9,340

D) $ 9,270

E) None of the above

Question

In preparing its bank reconciliation at March 31, Chioda Company has the following information:

What is the proper cash balance at March 31 for balance sheet purposes?

What is the proper cash balance at March 31 for balance sheet purposes?

A) $35,750

B) $36,750

C) $36,800

D) $37,050

E) None of the above

What is the proper cash balance at March 31 for balance sheet purposes?A) $35,750

B) $36,750

C) $36,800

D) $37,050

E) None of the above

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/43

Play

Full screen (f)

Deck 5: Internal Control and Cash

1

Fraud refers to any act by the management or employees of a business involving an intentional deception for personal gain.

True

2

Three elements of the fraud triangle include perceived pressure; a way to rationalize the fraudulent act; and a perceived opportunity.

True

3

A company implements internal controls to improve the chances that employee will function according to the plans and standard operating procedures developed by the management team.

True

4

Requiring employees to take vacations is an example of a good internal accounting control feature.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

5

Good internal accounting control requires that the person handling cash should also make any related journal entries so that responsibility for cash can be assigned to one person.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

6

A control activity can be either a prevention control or a monitoring control.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

7

A detection control is generally more desirable than a prevention control.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

8

Certain highly liquid, short-term investments of 90 days maturity or less are often combined with Cash and presented as a single amount called Cash and Cash Equivalents on the balance sheet.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

9

At the end of an accounting period, the "cash balance per bank statement" on that date is usually the proper cash amount to show on the balance sheet.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

10

It is efficient, less costly, and a good internal accounting control procedure to pay small bills each day with cash available from daily cash receipts.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

11

Good internal accounting control over cash includes depositing all cash receipts in the bank each day.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

12

Disbursements from a petty cash fund should be made with checks that are prenumbered.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

13

The most effective tool for external parties to monitor a company's cash is the income statement.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

14

An operational audit is an examination of a company's annual financial statements by a firm of independent certified public accountants.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

15

Outstanding checks are checks a company has written and recorded as cash disbursements that have not yet been presented to the bank for payment.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

16

Journal entries are required for all adjustments to the "cash balance per bank statement" in a bank reconciliation,

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not an element of the fraud triangle?

A) Perceived pressure

B) Internal audits

C) Opportunity

D) Rationalization

A) Perceived pressure

B) Internal audits

C) Opportunity

D) Rationalization

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

18

The COSO framework is designed to help companies structure and evaluate their internal controls. Which of the following is not an internal control component under COSO?

A) Risk assessment

B) Monitoring activities

C) Rationalization

D) Control environment

E) All above are internal control components under COSO

A) Risk assessment

B) Monitoring activities

C) Rationalization

D) Control environment

E) All above are internal control components under COSO

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following is desirable in a good system of internal accounting controls?

A) Develop plans and budgets

B) Encourage employee collusion

C) Maintain adequate accounting records

D) Two of the above

E) None of the above

A) Develop plans and budgets

B) Encourage employee collusion

C) Maintain adequate accounting records

D) Two of the above

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

20

Which of the following is desirable in a good system of internal accounting control?

A) Responsibility and authority for a given function should be shared among several employees

B) Appropriate forms, such as checks and sales invoices, should have preprinted control numbers

C) All accounting personnel in a firm should be bonded

D) To obtain the benefit of specialization, employees should not be rotated among similar jobs

E) None of the above

A) Responsibility and authority for a given function should be shared among several employees

B) Appropriate forms, such as checks and sales invoices, should have preprinted control numbers

C) All accounting personnel in a firm should be bonded

D) To obtain the benefit of specialization, employees should not be rotated among similar jobs

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

21

Which of the following is a poor internal accounting control feature?

A) Segregation of duties.

B) Combining authorization with custodianship.

C) Rotation of personnel.

D) Internal auditing.

E) None of the above

A) Segregation of duties.

B) Combining authorization with custodianship.

C) Rotation of personnel.

D) Internal auditing.

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

22

Procedures requiring that the recording of asset transactions be separated from the custody of those assets:

A) Will uncover collusion among employees

B) Are important only in very large businesses

C) Are especially important in handling cash

D) Make it easy for an employee to cover up the theft of an asset

E) None of the above

A) Will uncover collusion among employees

B) Are important only in very large businesses

C) Are especially important in handling cash

D) Make it easy for an employee to cover up the theft of an asset

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

23

In establishing an effective internal control structure, management should:

A) Establish a good control environment.

B) Provide an effective accounting system.

C) Integrate control procedures into the control environment and accounting system.

D) All of the above.

E) None of the above

A) Establish a good control environment.

B) Provide an effective accounting system.

C) Integrate control procedures into the control environment and accounting system.

D) All of the above.

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

24

The Sarbanes-Oxley Act (SOX) mandates that all publicly traded US corporations must:

A) Maintain an adequate system of internal controls

B) Top management must ensure the reliability of the controls

C) Outside independent auditors must attest to the adequacy of the controls

D) All of the above.

A) Maintain an adequate system of internal controls

B) Top management must ensure the reliability of the controls

C) Outside independent auditors must attest to the adequacy of the controls

D) All of the above.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

25

Internal auditing is a company function that:

A) Audits the firm's financial statements and expresses an opinion on them

B) Provides independent appraisals of the company's financial statements, its internal control, and its operations

C) Prepares the firm's income tax returns

D) All of the above

E) None of the above

A) Audits the firm's financial statements and expresses an opinion on them

B) Provides independent appraisals of the company's financial statements, its internal control, and its operations

C) Prepares the firm's income tax returns

D) All of the above

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

26

A compensating balance refers to:

A) The minimum balance established for a petty cash fund

B) A minimum balance that a financial institution requires a firm to maintain in its account as part of a borrowing arrangement

C) The final cash balance achieved in a bank reconciliation

D) The amount of cash invested temporarily in highly marketable securities

E) None of the above

A) The minimum balance established for a petty cash fund

B) A minimum balance that a financial institution requires a firm to maintain in its account as part of a borrowing arrangement

C) The final cash balance achieved in a bank reconciliation

D) The amount of cash invested temporarily in highly marketable securities

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

27

From the viewpoint of good internal accounting control, which of the following individuals would be the proper person to prepare bank reconciliations for a company that receives cash payments both through the mail and from customers in person?

A) The individual who opens the company's mail and lists the payments received

B) The individual who works in the customer service department and receives payments from customers who pay in person

C) The individual who deposits the daily cash receipts in the bank

D) Any of the above individuals would be appropriate

E) None of the above

A) The individual who opens the company's mail and lists the payments received

B) The individual who works in the customer service department and receives payments from customers who pay in person

C) The individual who deposits the daily cash receipts in the bank

D) Any of the above individuals would be appropriate

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following features should not be included in a good system of internal accounting control over cash?

A) All receipts are deposited daily in the bank.

B) All major disbursements are made by check, and an imprest fund is used for petty cash disbursements.

C) Cash handling is separated from the recording of cash transactions.

D) Monthly bank reconciliations are prepared by the person who makes the daily bank deposits.

E) All of the above are part of a good system of internal accounting control over cash.

A) All receipts are deposited daily in the bank.

B) All major disbursements are made by check, and an imprest fund is used for petty cash disbursements.

C) Cash handling is separated from the recording of cash transactions.

D) Monthly bank reconciliations are prepared by the person who makes the daily bank deposits.

E) All of the above are part of a good system of internal accounting control over cash.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

29

Which of the following is not a feature of good internal accounting control over cash?

A) All cash receipts are deposited in the bank each day.

B) Most bills are paid with paper currency and coins to minimize the bank service charges.

C) A bank reconciliation is prepared when each bank statement is received.

D) Cash is handled separately from the recording of cash transactions.

E) All of the above are part of a good system of internal accounting control over cash.

A) All cash receipts are deposited in the bank each day.

B) Most bills are paid with paper currency and coins to minimize the bank service charges.

C) A bank reconciliation is prepared when each bank statement is received.

D) Cash is handled separately from the recording of cash transactions.

E) All of the above are part of a good system of internal accounting control over cash.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

30

The Cash amount properly shown on the year-end balance sheet is the

A) Balance in the general ledger account before the year-end bank reconciliation

B) Balance per the year-end bank statement

C) Balance per the year-end bank statement less deposits in transit and plus outstanding checks

D) Balance in the general ledger account after entries from the year-end bank reconciliation have been posted

E) None of the above

A) Balance in the general ledger account before the year-end bank reconciliation

B) Balance per the year-end bank statement

C) Balance per the year-end bank statement less deposits in transit and plus outstanding checks

D) Balance in the general ledger account after entries from the year-end bank reconciliation have been posted

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

31

Identify the principle of internal control that is violated in the following situation: Marvin Company is a very small business. Sam Jones, one of the two office clerks, opens the mail each day and removes the cash receipts that come in the mail. Sam then records the receipts in the cash records and the customer's account and deposits the cash in the bank.

A) Insure assets and bond key employee

B) Maintain adequate records

C) Divide responsibility for related transactions.

D) Perform regular and independent reviews

A) Insure assets and bond key employee

B) Maintain adequate records

C) Divide responsibility for related transactions.

D) Perform regular and independent reviews

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

32

The following adjustment is necessary upon discovery of a "NSF" check during a bank reconciliation:

A) Increase Accounts Receivable; decrease cash

B) Increase Not Sufficient Funds Expense; decrease Cash

C) Increase Miscellaneous Expense; decrease Cash

D) No adjustment is necessary because the bank makes the entry.

E) None of the above

A) Increase Accounts Receivable; decrease cash

B) Increase Not Sufficient Funds Expense; decrease Cash

C) Increase Miscellaneous Expense; decrease Cash

D) No adjustment is necessary because the bank makes the entry.

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

33

At May 31, Robinson Company has outstanding checks totaling $9,800. The bank reconciliation for May should show these checks as a(n):

A) Deduction from balance per bank statement

B) Addition to balance per bank statement

C) Addition to balance per general ledger

D) Deduction from balance per general ledger

E) None of the above

A) Deduction from balance per bank statement

B) Addition to balance per bank statement

C) Addition to balance per general ledger

D) Deduction from balance per general ledger

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

34

First State Bank collected a note for Smith Company. This collection, not yet recorded in Smith's books, appears on the bank reconciliation as a(n):

A) Addition to balance per general ledger

B) Deduction from balance per bank statement

C) Addition to balance per bank statement

D) Deduction from balance per general ledger

E) None of the above

A) Addition to balance per general ledger

B) Deduction from balance per bank statement

C) Addition to balance per bank statement

D) Deduction from balance per general ledger

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

35

In reconciling the July bank statement, the vice president discovered that the bookkeeper had recorded a check written for $353 as $533 in the cash disbursements journal. For the bank reconciliation, the $180 error should be:

A) Added to balance per bank statement

B) Added to balance per general ledger

C) Deducted from balance per bank statement

D) Deducted from balance per general ledger

E) None of the above

A) Added to balance per bank statement

B) Added to balance per general ledger

C) Deducted from balance per bank statement

D) Deducted from balance per general ledger

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

36

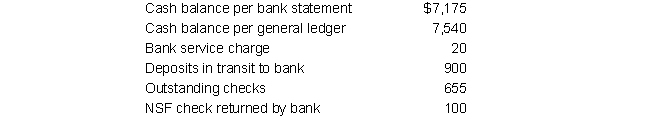

The following information pertains to Rodriguez Company:

Rodriguez should show the following reconciled cash balance from the bank reconciliation on its balance sheet:

A) $6,770

B) $8,445

C) $7,420

D) $8,055

E) None of the above

Rodriguez should show the following reconciled cash balance from the bank reconciliation on its balance sheet:

A) $6,770

B) $8,445

C) $7,420

D) $8,055

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

37

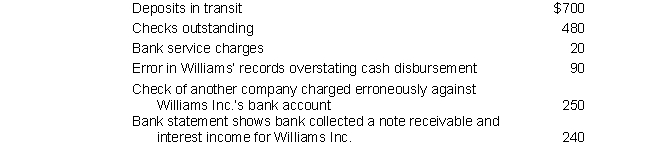

Williams Inc.'s June bank statement shows a June 30 balance of $9,050. Prior to reconciliation, its books show a cash balance of $9,210. The information below pertains to Williams:

The reconciled cash balance at June 30 on the bank reconciliation should be:

A) $10,100

B) $ 9,520

C) $ 9,340

D) $ 9,270

E) None of the above

The reconciled cash balance at June 30 on the bank reconciliation should be:

A) $10,100

B) $ 9,520

C) $ 9,340

D) $ 9,270

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

38

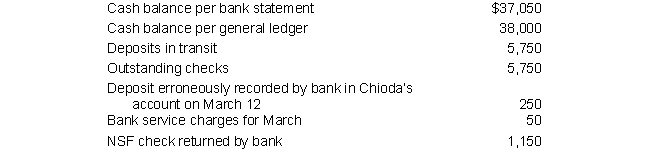

In preparing its bank reconciliation at March 31, Chioda Company has the following information:

What is the proper cash balance at March 31 for balance sheet purposes?

A) $35,750

B) $36,750

C) $36,800

D) $37,050

E) None of the above

What is the proper cash balance at March 31 for balance sheet purposes?A) $35,750

B) $36,750

C) $36,800

D) $37,050

E) None of the above

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

39

The bank statement reported an ending balance of $14,620 after deducting $220 in service charges and an addition of $4,500 for a note collected by the bank on the company's behalf. The company books reported an ending balance of $9,690, and determined that deposits in transit equal $5,600 and outstanding checks equal $6,250.

What is the adjusted cash balance?

A) $13,970

B) $ 5,600

C) $11,970

D) $ 7,040

What is the adjusted cash balance?

A) $13,970

B) $ 5,600

C) $11,970

D) $ 7,040

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

40

Discuss and differentiate between prevention control and detection control. Provide an example of each.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

41

Identify and discuss the four primary activities of effective cash management.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

42

Use the following information to prepare a bank reconciliation for Larkin Company at August 31, 2019:

(1) Cash account balance, August 31, $10,335.30.

(2) Bank statement balance, August 31, $12,380.50.

(3) Deposits in transit, $960.00.

(4) Outstanding checks, August 31, $3,190.20.

(5) Service charge on bank statement not recorded in books, $25.00.

(6) Bank error--another company's check charged on Larkin Company's bank statement, $250.00.

(7) Check for repairs expense, $670.00, incorrectly recorded in books as $760.00.

(1) Cash account balance, August 31, $10,335.30.

(2) Bank statement balance, August 31, $12,380.50.

(3) Deposits in transit, $960.00.

(4) Outstanding checks, August 31, $3,190.20.

(5) Service charge on bank statement not recorded in books, $25.00.

(6) Bank error--another company's check charged on Larkin Company's bank statement, $250.00.

(7) Check for repairs expense, $670.00, incorrectly recorded in books as $760.00.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

43

Use the following information to prepare a bank reconciliation for Forrester Company at April 30, 2019:

(1) Cash account balance, April 30, $9,786.40.

(2) Bank statement balance, April 30, $10,758.20.

(3) Service charge on bank statement not recorded in books, $70.00.

(4) Deposits in transit, $1,438.60.

(5) Outstanding checks, April 30, $946.80.

(6) The bank statement included a charge of $466.40 for N. Ryan's NSF check. The check, returned with the bank statement, had been received by Forrester in payment on account.

(7) The bank collected a $2,000.00 note in April for Forrester. This amount was included in the bank statement, but Forrester had not yet recorded the collection. The bank's $70.00 service charge for April [see (3) above] included collection charge for the note.

(1) Cash account balance, April 30, $9,786.40.

(2) Bank statement balance, April 30, $10,758.20.

(3) Service charge on bank statement not recorded in books, $70.00.

(4) Deposits in transit, $1,438.60.

(5) Outstanding checks, April 30, $946.80.

(6) The bank statement included a charge of $466.40 for N. Ryan's NSF check. The check, returned with the bank statement, had been received by Forrester in payment on account.

(7) The bank collected a $2,000.00 note in April for Forrester. This amount was included in the bank statement, but Forrester had not yet recorded the collection. The bank's $70.00 service charge for April [see (3) above] included collection charge for the note.

Unlock Deck

Unlock for access to all 43 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 43 flashcards in this deck.