Deck 1: The Demand for Audit, Cpa Profession, Audit Reports and Other Assurance Services

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

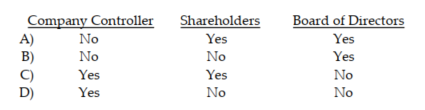

To emphasize the fact that the auditor is independent, a typical addressee of the audit report could be:

Question

Question

An auditor determines the financial statements include a material departure from IFRS. Which type of opinion may be issued?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Which of the following representations does an auditor make explicitly and which implicitly when issuing an unmodified opinion?

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/108

Play

Full screen (f)

Deck 1: The Demand for Audit, Cpa Profession, Audit Reports and Other Assurance Services

1

In the audit of historical financial statements, which of the following accounting bases is the most common?

A) International Financial Reporting Standards.

B) Liquidation basis of accounting.

C) Regulatory accounting principles.

D) Cash basis of accounting.

A) International Financial Reporting Standards.

B) Liquidation basis of accounting.

C) Regulatory accounting principles.

D) Cash basis of accounting.

International Financial Reporting Standards.

2

The _________ interest rate may be defined as approximately the rate a bank could earn by investing in government treasury notes for the same length as the length of a business loan.

A) risk- free

B) prevailing

C) nominal

D) stated

A) risk- free

B) prevailing

C) nominal

D) stated

risk- free

3

In the Arab world, requirements for the formal education, practice experience, and continuing education of public accounts are set by:

A) national associations of accountants and auditors.

B) government ministries.

C) either of A and B.

D) neither A or B.

A) national associations of accountants and auditors.

B) government ministries.

C) either of A and B.

D) neither A or B.

either of A and B.

4

Which of the following is a type of audit evidence?

A) Observations made by an auditor.

B) Written communications from company employees or outsiders.

C) Oral responses to the auditor from employees of the company under audit.

D) Evidence may take any of the above forms.

A) Observations made by an auditor.

B) Written communications from company employees or outsiders.

C) Oral responses to the auditor from employees of the company under audit.

D) Evidence may take any of the above forms.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

5

Which of the following is not a Trust Services principle as defined by the AICPA or CICA?

A) Availability.

B) Operational integrity.

C) Online privacy.

D) Processing integrity.

A) Availability.

B) Operational integrity.

C) Online privacy.

D) Processing integrity.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

6

Which one of the following is more difficult to evaluate objectively?

A) Efficiency and effectiveness of operations.

B) Compliance with government regulations.

C) Presentation of financial statements in accordance with IFRS.

D) All three of the above are equally difficult.

A) Efficiency and effectiveness of operations.

B) Compliance with government regulations.

C) Presentation of financial statements in accordance with IFRS.

D) All three of the above are equally difficult.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

7

Publicly traded companies in the Arab world:

A) are not required to produce audited financial statements.

B) are only required to produce financial statements checked by internal auditors.

C) must have an audit of their financial statements.

D) must have an audit of their financial statements and their internal controls.

A) are not required to produce audited financial statements.

B) are only required to produce financial statements checked by internal auditors.

C) must have an audit of their financial statements.

D) must have an audit of their financial statements and their internal controls.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

8

Discuss the four primary requirements for becoming a licensed accountant in Kuwait.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

9

Discuss the reasons why auditors of financial statements must be both competent and independent.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

10

Discuss the role of the forensic auditor and give some examples of situations that they might investigate.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

11

Match each of the definition with the following terms

-An independent professional service that improves the quality of information for decision makers.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-An independent professional service that improves the quality of information for decision makers.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

12

Match each of the definition with the following terms

-The concept that the manager generally has more information about the True financial position, results of operations, and cash flow of the company than the absentee owner.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-The concept that the manager generally has more information about the True financial position, results of operations, and cash flow of the company than the absentee owner.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

13

Match each of the definition with the following terms

-A law passed in 2002 that provides for additional regulation of public companies and their auditors; and also requires auditors to audit the effectiveness of internal control over financial reporting

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-A law passed in 2002 that provides for additional regulation of public companies and their auditors; and also requires auditors to audit the effectiveness of internal control over financial reporting

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

14

Match each of the definition with the following terms

-Any information used by the auditor to determine whether the information being audited is stated in accordance with established criteria.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-Any information used by the auditor to determine whether the information being audited is stated in accordance with established criteria.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

15

Match each of the definition with the following terms

-The recording, classifying, and summarizing of economic events in a logical manner for the purpose of providing financial information for decision making.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-The recording, classifying, and summarizing of economic events in a logical manner for the purpose of providing financial information for decision making.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

16

Match each of the definition with the following terms

-The risk that information upon which a business decision is made is inaccurate

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-The risk that information upon which a business decision is made is inaccurate

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

17

Match each of the definition with the following terms

-A type of assurance service in which an auditing firm issues a report about the reliability of an assertion that is the responsibility of another party.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-A type of assurance service in which an auditing firm issues a report about the reliability of an assertion that is the responsibility of another party.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

18

Match each of the definition with the following terms

-The process of investigating cases of fraud in the company's financial statements, accounting books and records, and any other documents used in the company's operations that may be used in white- collar crime.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

-The process of investigating cases of fraud in the company's financial statements, accounting books and records, and any other documents used in the company's operations that may be used in white- collar crime.

A) Accounting

B) Assurance service

C) Attestation service

D) Audit evidence

E) Audit of historical financial statements

F) Audit report

G) Compliance audit

H) Forensic audit

I) Independent auditors

J) Information asymmetry

K) Information risk

L) Internal auditors

M) Internal control over financial reporting

N) Operational audit

O) Review of historical financial statements

P) Sarbanes-Oxley Act

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

19

Companies that file annual statements with a capital market authority are required to have an audit of the effectiveness of their internal controls.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

20

Working as a GAO auditor or as an internal auditor fulfils the experience requirement for becoming a licensed accountant in many Arab countries.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

21

The use of assurance and attestation services for online information and other IT services is widespread in the Arab world.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

22

The organization providing guidelines and licenses for forensic auditors is the International Auditing and Assurance Standards Board.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

23

A review of a company's wage rates for compliance with minimum wage legislation is an operational audit.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

24

An auditor provides a moderate level of assurance for reviews of interim financial statements so the same level of evidence is needed as for a full audit.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

25

External users such as stockholders and lenders who rely on those financial statements to make business decisions look to the auditor's report as an indication of the statements' reliability.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

26

For the audit of tax returns by a local tax authority, the criteria for evaluating the information are found in the international tax law.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

27

Which one of these following is not covered in the general principles and responsibilities section of the International Standards on Auditing?

A) Agreeing the terms of audit engagements.

B) Communication with those charged with governance.

C) Audit documentation.

D) Planning an audit of financial statements.

A) Agreeing the terms of audit engagements.

B) Communication with those charged with governance.

C) Audit documentation.

D) Planning an audit of financial statements.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

28

Which one of the following is not one of the three general standards in the GAAS framework?

A) Maintain independence of mental attitude.

B) Have adequate training and proficiency.

C) Ensure proper planning and supervision.

D) Exercise due professional care.

A) Maintain independence of mental attitude.

B) Have adequate training and proficiency.

C) Ensure proper planning and supervision.

D) Exercise due professional care.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

29

Which one of these following is not covered in the audit evidence section of the International Standards on Auditing?

A) Communication with those charged with governance.

B) Going concern.

C) Analytical procedures.

D) External confirmations.

A) Communication with those charged with governance.

B) Going concern.

C) Analytical procedures.

D) External confirmations.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

30

Which one of the following is not a field work standard in the GAAS framework?

A) Understand the entity and its environment including internal control.

B) Exercise due professional care.

C) Adequate planning and supervision.

D) Sufficient appropriate audit evidence.

A) Understand the entity and its environment including internal control.

B) Exercise due professional care.

C) Adequate planning and supervision.

D) Sufficient appropriate audit evidence.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

31

The GAAS general standards stress the:

A) evidence accumulation process.

B) need to communicate the auditor's findings to the user.

C) important personal qualities the auditor should possess.

D) general supervision of the audit.

A) evidence accumulation process.

B) need to communicate the auditor's findings to the user.

C) important personal qualities the auditor should possess.

D) general supervision of the audit.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

32

The generally accepted auditing standard that requires 'adequate technical training and proficiency' is normally interpreted as requiring the auditor to have:

A) a graduate degree in a business field.

B) worked for an entity similar to the entity being audited.

C) independence in mental attitude.

D) formal education in auditing and accounting.

A) a graduate degree in a business field.

B) worked for an entity similar to the entity being audited.

C) independence in mental attitude.

D) formal education in auditing and accounting.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

33

The generally accepted auditing standard that requires 'adequate technical training and proficiency' is normally interpreted as requiring the auditor to have:

A) worked for an entity similar to the entity being audited.

B) formal education in auditing and accounting.

C) independence in mental attitude.

D) a graduate degree in a business field.

A) worked for an entity similar to the entity being audited.

B) formal education in auditing and accounting.

C) independence in mental attitude.

D) a graduate degree in a business field.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

34

The Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) prepares accounting, auditing, governance, ethics and Shari'a standards for Islamic financial institutions. The AAOIFI:

A) only operates within Arab countries.

B) is a division of the International Auditing and Assurance Standards Board.

C) was established by the Islamic Financial Services Board.

D) is an independent international organization.

A) only operates within Arab countries.

B) is a division of the International Auditing and Assurance Standards Board.

C) was established by the Islamic Financial Services Board.

D) is an independent international organization.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

35

Which of the following statements most accurately captures the intent of the standards of field work?

A) Field work standards are primarily concerned with personal attributes necessary during the conduct of the audit.

B) Field work standards are primarily concerned with preparing a report on a company's financial statements.

C) Field work standards are primarily concerned with evidence accumulation and other activities during the conduct of the audit.

D) Field work standards are primarily concerned with the conduct of substantive testing as opposed to testing of internal controls.

A) Field work standards are primarily concerned with personal attributes necessary during the conduct of the audit.

B) Field work standards are primarily concerned with preparing a report on a company's financial statements.

C) Field work standards are primarily concerned with evidence accumulation and other activities during the conduct of the audit.

D) Field work standards are primarily concerned with the conduct of substantive testing as opposed to testing of internal controls.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

36

GAAS, SASs, and ISAs should be looked on by practitioners as _ _________ standards of performance.

A) minimum

B) prescriptive

C) professional

D) maximum

A) minimum

B) prescriptive

C) professional

D) maximum

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

37

Which of the following is the least likely form of business structure for a CPA firm?

A) General corporation.

B) Proprietorship.

C) General partnership.

D) Limited liability partnership.

A) General corporation.

B) Proprietorship.

C) General partnership.

D) Limited liability partnership.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

38

The Statements on Auditing Standards issued by the Auditing Standards Board:

A) are the equivalent of laws for audit practitioners.

B) are optional guidelines which an auditor may choose to follow or not follow when conducting an audit.

C) must be followed in all situations.

D) are interpretations of GAAS.

A) are the equivalent of laws for audit practitioners.

B) are optional guidelines which an auditor may choose to follow or not follow when conducting an audit.

C) must be followed in all situations.

D) are interpretations of GAAS.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

39

Which of these international standards are published by the International Auditing and Assurance Standards Board?

A) International Standards on Review Engagements.

B) International Standards on Related Services.

C) International Standards on Quality Control.

D) All of the above.

A) International Standards on Review Engagements.

B) International Standards on Related Services.

C) International Standards on Quality Control.

D) All of the above.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

40

International Standards on Review Engagements are issued by the:

A) Financial Accounting Standards Board.

B) International Auditing and Assurance Standards Board.

C) Islamic Financial Services Board.

D) Securities and Exchange Commission.

A) Financial Accounting Standards Board.

B) International Auditing and Assurance Standards Board.

C) Islamic Financial Services Board.

D) Securities and Exchange Commission.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

41

The auditor's judgment concerning the overall presentation of the audit entity's financial position is applied within the framework of:

A) the auditor's evaluation of the audited company's internal control.

B) auditing standards-either International Standards on Auditing, generally accepted auditing standards, or local auditing standards-which include the concept of materiality.

C) quality control.

D) accounting standards-either International Financial Reporting Standards, generally accepted accounting principles, or local accounting standards.

A) the auditor's evaluation of the audited company's internal control.

B) auditing standards-either International Standards on Auditing, generally accepted auditing standards, or local auditing standards-which include the concept of materiality.

C) quality control.

D) accounting standards-either International Financial Reporting Standards, generally accepted accounting principles, or local accounting standards.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

42

Williams & Co., a U.S. audit firm, is to have a 'peer review.' The peer review can be performed by:

A) another audit firm selected by Williams & Co.

B) a review team selected by the state society.

C) internal auditors.

D) either A or B.

A) another audit firm selected by Williams & Co.

B) a review team selected by the state society.

C) internal auditors.

D) either A or B.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

43

Which of these statements about quality reviews undertaken by international CPA networks in the Arab world is not True?

A) The review includes an evaluation of the internal system of the member, including the firm's working papers and audit manual.

B) The member being reviewed selects partners and managers of other member firms within the network to conduct the review.

C) Each CPA network carries out an interim review of its members' quality of services using standard practices applied within the network.

D) Those carrying out reviews of other firms must be located in the same geographical area where there are common features relating to the accounting and auditing profession.

A) The review includes an evaluation of the internal system of the member, including the firm's working papers and audit manual.

B) The member being reviewed selects partners and managers of other member firms within the network to conduct the review.

C) Each CPA network carries out an interim review of its members' quality of services using standard practices applied within the network.

D) Those carrying out reviews of other firms must be located in the same geographical area where there are common features relating to the accounting and auditing profession.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

44

ISAs, GAAS, and SASs should be looked upon by practitioners as:

A) minimum standards of performance that must be achieved on each audit engagement.

B) benchmarks to be used on all audits, reviews, and compilations.

C) maximum standards that denote excellent work.

D) ideals to work towards, but which are not achievable.

A) minimum standards of performance that must be achieved on each audit engagement.

B) benchmarks to be used on all audits, reviews, and compilations.

C) maximum standards that denote excellent work.

D) ideals to work towards, but which are not achievable.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

45

Distinguish between International Standards on Auditing (ISAs) and International Financial Reporting Standards (IFRS). What organization establishes ISAs? What organization establishes IFRS? What are the equivalent standards called in the U.S.?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

46

There are ten generally accepted auditing standards, divided into three categories. List, by category, each of these ten standards.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

47

The International Standards on Auditing are organized into six main parts. List these parts.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

48

In the context of auditing, explain what is meant by an independent mental attitude. Discuss how internal auditors can have an independent mental attitude when they are employed by the company they audit.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

49

Explain the concept of Islamic accounting and discuss the purpose of the Accounting and Auditing Organization for Islamic Institutions and its influence on setting generally accepted accounting principles.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

50

Discuss the quality control measures introduced for audit firms in Saudi Arabia by the Saudi Organization for Certified Public Accountants (SOCPA)?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

51

There is a joint partnership between the International CPA networks and local accountant(s) in every Arab country

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

52

CPA firms in most countries in the Arab world are permitted to be general corporations.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

53

To be a member of the Egyptian Society of Accountants and Auditors (ESAA) accountants must pass three levels of examination.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

54

In the United Arab Emirates, accountants are not allowed to work as auditors unless their names are listed in the register of practicing auditors maintained by the Ministry of Economy and Commerce.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

55

Any graduate wishing to join the AICPA needs to travel to U.S. to take the AICPA exams.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

56

Most CPA firms have specialists who spend a large portion of their time ensuring that their clients satisfy all SEC requirements.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

57

When auditing a public company, the International Standards on Auditing override a country's regulations governing the audit of financial or other information.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

58

The Egyptian Standards on Auditing (ESA) are based on the ISAs and translated into Arabic.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

59

The Auditing Standards Board (ASB) has no plans to converge U.S. GAAS with the ISAs and align its agenda with the IAASB.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

60

Statements on Auditing Standards (SASs) are considered to be interpretations of the ten generally accepted auditing standards.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

61

Any CPA firm in the U.S. that audits more than 100 public companies is required to have an annual inspection by the PCAOB.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

62

In the Arab world, the review of the quality of the audit provided by auditing firms is undertaken by the international CPA networks.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

63

In Egypt, the Egyptian Society of Accountants and Auditors has established a unit responsible for monitoring the quality of services provided by registered audit firms with the Capital Market Authority.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

64

To emphasize the fact that the auditor is independent, a typical addressee of the audit report could be:

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

65

The purpose of the introductory paragraph in the standard unmodified report is:

A) to identify the financial statements audited and the dates and time periods covered by the report.

B) to indicate the auditor followed applicable audit standards.

C) to identify that the type of opinion issued is unmodified.

D) to indicate all the financial statements are in accordance with IFRS or local accounting standards.

A) to identify the financial statements audited and the dates and time periods covered by the report.

B) to indicate the auditor followed applicable audit standards.

C) to identify that the type of opinion issued is unmodified.

D) to indicate all the financial statements are in accordance with IFRS or local accounting standards.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

66

An auditor determines the financial statements include a material departure from IFRS. Which type of opinion may be issued?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

67

When the auditor evaluates the effect of a change in accounting principle, the materiality of the change should be evaluated based on:

A) the effect on total assets.

B) the prior years presented.

C) guidelines included in auditing standards.

D) the current year effect of the change.

A) the effect on total assets.

B) the prior years presented.

C) guidelines included in auditing standards.

D) the current year effect of the change.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

68

Conditions requiring a departure from an unmodified audit report include all but which of the following?

A) Management refused to allow the auditor to confirm significant accounts receivable for which there were no alternative procedures performed.

B) Management has determined that fixed assets should be reported in the balance sheet at their replacement values rather than historical costs. The auditors do not concur.

C) Management decided not to allow the auditor to confirm significant accounts receivable, but the auditor obtained sufficient appropriate evidence by examining subsequent cash receipts.

D) The audit partner's dependent child received a gift of 100 shares of a client's stock for her birthday from a grandparent.

A) Management refused to allow the auditor to confirm significant accounts receivable for which there were no alternative procedures performed.

B) Management has determined that fixed assets should be reported in the balance sheet at their replacement values rather than historical costs. The auditors do not concur.

C) Management decided not to allow the auditor to confirm significant accounts receivable, but the auditor obtained sufficient appropriate evidence by examining subsequent cash receipts.

D) The audit partner's dependent child received a gift of 100 shares of a client's stock for her birthday from a grandparent.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

69

PCAOB Auditing Standard 5 requires the audit of internal control over financial reporting to be integrated with:

A) the review of annual financial statements.

B) the audit of the financial statements.

C) the quarterly review of financial information.

D) none of the above.

A) the review of annual financial statements.

B) the audit of the financial statements.

C) the quarterly review of financial information.

D) none of the above.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

70

The audit report indicates that (1) management is responsible for the content of the financial statements and (2) the auditor is responsible for evaluating the appropriateness of the accounting principles chosen by management. Which paragraph contains those statements?

A) Both are in the opinion paragraph.

B) Both are in the management's responsibility paragraph.

C) Both are in the introductory paragraph.

D) None of the above are true.

A) Both are in the opinion paragraph.

B) Both are in the management's responsibility paragraph.

C) Both are in the introductory paragraph.

D) None of the above are true.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

71

Whenever an auditor issues a qualified opinion, the implication is that the auditor:

A) believes the financial statements are presented fairly 'except for' a specific aspect of them.

B) does not know if the financial statements are presented fairly.

C) does not believe the financial statements are presented fairly.

D) believes the financial statements are presented fairly.

A) believes the financial statements are presented fairly 'except for' a specific aspect of them.

B) does not know if the financial statements are presented fairly.

C) does not believe the financial statements are presented fairly.

D) believes the financial statements are presented fairly.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

72

The necessity to issue a disclaimer of opinion may arise because of:

A) a lack of independence between the auditor and client.

B) a severe limitation on the scope of the audit.

C) either A or B.

D) neither A nor B.

A) a lack of independence between the auditor and client.

B) a severe limitation on the scope of the audit.

C) either A or B.

D) neither A nor B.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

73

Whenever there is a scope restriction, the appropriate response is to issue a(n):

A) qualified opinion.

B) adverse opinion.

C) unmodified report, a qualification of scope and opinion, or a disclaimer, depending on materiality.

D) disclaimer of opinion.

A) qualified opinion.

B) adverse opinion.

C) unmodified report, a qualification of scope and opinion, or a disclaimer, depending on materiality.

D) disclaimer of opinion.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

74

Which of the following is least likely to cause uncertainty about the ability of an entity to continue as a going concern?

A) Working capital deficiencies.

B) Significant recurring operating losses.

C) Loss of major customers.

D) A client's lawsuit against another company which claims the other company has infringed on its patent.

A) Working capital deficiencies.

B) Significant recurring operating losses.

C) Loss of major customers.

D) A client's lawsuit against another company which claims the other company has infringed on its patent.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

75

When a client has not applied IFRS consistently from the prior year to the current year, the auditor does not concur with the appropriateness of the change, and the change in IFRS has a material effect on the financial statements, the auditor should issue a(n):

A) unmodified opinion.

B) disclaimer.

C) qualified opinion.

D) adverse opinion.

A) unmodified opinion.

B) disclaimer.

C) qualified opinion.

D) adverse opinion.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

76

Which of the following is not a change that affects consistency and, therefore, does not require an emphasis of matter paragraph?

A) Change in an estimate, such as a decrease in the life of an asset for depreciation purposes.

B) Correction of errors by changing from non- IFRS to IFRS.

C) Change in accounting principle, such as a change from LIFO to FIFO.

D) Change in reporting entity, such as the inclusion of an additional company in combined financial statements.

A) Change in an estimate, such as a decrease in the life of an asset for depreciation purposes.

B) Correction of errors by changing from non- IFRS to IFRS.

C) Change in accounting principle, such as a change from LIFO to FIFO.

D) Change in reporting entity, such as the inclusion of an additional company in combined financial statements.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

77

When a company's financial statements contain a departure from IFRS with which the auditor concurs, the departure should be explained in:

A) the opinion paragraph.

B) the management's responsibility paragraph.

C) an emphasis of a matter paragraph that appears before the opinion paragraph.

D) an emphasis of a matter paragraph after the opinion paragraph.

A) the opinion paragraph.

B) the management's responsibility paragraph.

C) an emphasis of a matter paragraph that appears before the opinion paragraph.

D) an emphasis of a matter paragraph after the opinion paragraph.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

78

Which of the following representations does an auditor make explicitly and which implicitly when issuing an unmodified opinion?

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

79

Auditors issue several types of 'special audit reports.' Which of the following circumstances wouldnot require the issuance of a special audit report?

A) The auditor has been retained to audit only the current assets.

B) The auditor has been retained to review the internal control system, not the financial statements.

C) The client's financial statements are prepared using the accrual basis.

D) The client's financial statements are prepared using the cash basis.

A) The auditor has been retained to audit only the current assets.

B) The auditor has been retained to review the internal control system, not the financial statements.

C) The client's financial statements are prepared using the accrual basis.

D) The client's financial statements are prepared using the cash basis.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following will not cause the auditor to issue a standard unmodified report with an emphasis of matter paragraph or modified wording?

A) Auditor disagrees with client's departure from IFRS.

B) Reports involving other auditors.

C) Matters presented in the financial statements are of such importance that they are fundamental to users' understanding of the financial statements.

D) Lack of consistent application of IFRS.

A) Auditor disagrees with client's departure from IFRS.

B) Reports involving other auditors.

C) Matters presented in the financial statements are of such importance that they are fundamental to users' understanding of the financial statements.

D) Lack of consistent application of IFRS.

Unlock Deck

Unlock for access to all 108 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 108 flashcards in this deck.