Deck 3: Audit Evidence, Audit Planning, Analytical Procedures, Materiality and Risk

Full screen (f)

Question

Auditors must make decisions regarding what evidence to gather and how much to accumulate. Which of the following is a decision that must be made by auditors related to evidence?

Question

Audit procedures may be performed:

Question

Question

Question

Question

Question

Often, auditor procedures result in significant differences being discovered by the auditor. The auditor should investigate further if:

Question

Question

Question

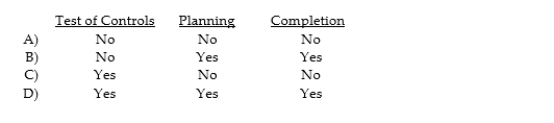

Analytical procedures must be used during which phase(s) of the audit?

Question

Question

Question

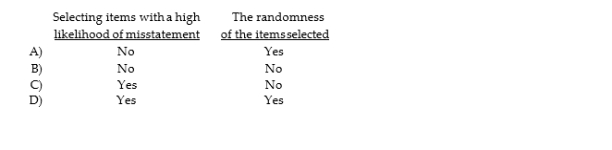

Which items affect the sufficiency of evidence when choosing a sample?

Question

Question

Question

Question

Question

Question

Audit documentation should provide support for:

Question

Question

Audit documentation should possess certain characteristics. Which of the following is one of the characteristics?

Question

Question

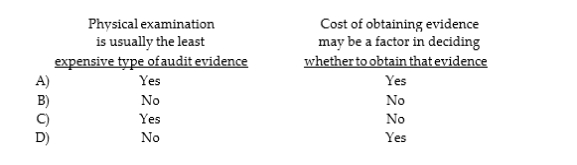

Which of the following statements is correct regarding the costs involved in obtaining evidence?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

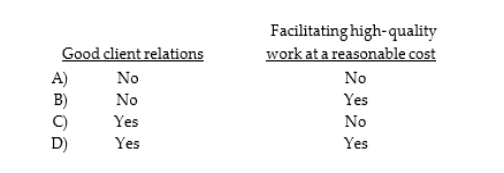

Avoiding misunderstandings with the client is important for:

Question

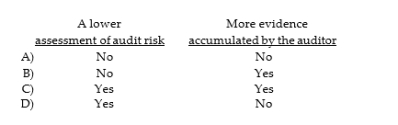

When inherent risk is high, there will need to be:

Question

The auditor is likely to accumulate more evidence when the audit is for a company:

Question

Question

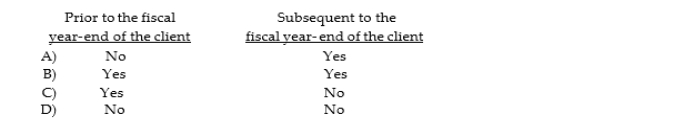

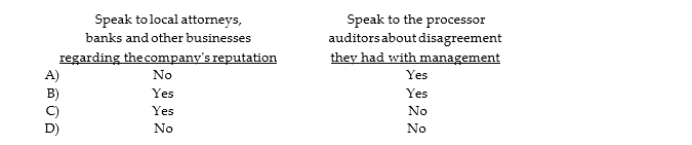

A successor auditor may perform which of the following for a new audit client?

Question

Question

Question

Question

Question

Question

The corporate minutes are the official record of the meetings of the board of directors and stockholders. The minutes typically include authorizations related to:

Question

Question

Question

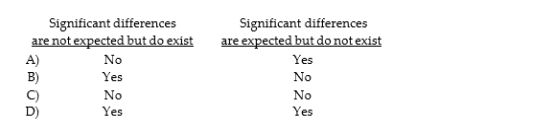

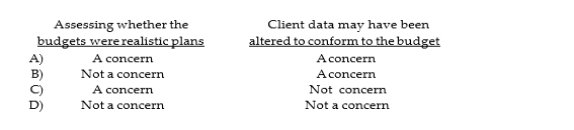

Whenever an auditor compares client data to client- prepared budgets, there are two special concerns. Indicate if the two items below are concerns.

Question

Which is usually included in an engagement letter?

Question

Which is usually included in an engagement letter?

Question

Which is usually included in an engagement letter?

Question

Which is usually included in the engagement letter?

Question

Which is usually included in the engagement letter?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/100

Play

Full screen (f)

Deck 3: Audit Evidence, Audit Planning, Analytical Procedures, Materiality and Risk

1

Auditors must make decisions regarding what evidence to gather and how much to accumulate. Which of the following is a decision that must be made by auditors related to evidence?

A

2

Audit procedures may be performed:

B

3

Which of the following forms of evidence is most reliable?

A) Internal memo explaining the issuance of a credit memo.

B) Confirmation of accounts receivable balance received from a customer.

C) Copy of month- end adjusting entries.

D) General ledger account balances.

A) Internal memo explaining the issuance of a credit memo.

B) Confirmation of accounts receivable balance received from a customer.

C) Copy of month- end adjusting entries.

D) General ledger account balances.

Confirmation of accounts receivable balance received from a customer.

4

Which of the following is not a characteristic of the reliability of evidence?

A) Qualifications of individuals providing information.

B) Degree of subjectivity.

C) Degree of objectivity.

D) Auditor's direct knowledge.

A) Qualifications of individuals providing information.

B) Degree of subjectivity.

C) Degree of objectivity.

D) Auditor's direct knowledge.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

5

Calculating the gross margin as a percent of sales and comparing it with previous periods is what type of evidence?

A) Analytical procedures.

B) Physical examination.

C) Observation.

D) Inquiries of the client.

A) Analytical procedures.

B) Physical examination.

C) Observation.

D) Inquiries of the client.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

6

When auditors use documents to support recorded transactions, the process is often called:

A) vouching.

B) physical examination.

C) confirmation.

D) inquiry.

A) vouching.

B) physical examination.

C) confirmation.

D) inquiry.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

7

Often, auditor procedures result in significant differences being discovered by the auditor. The auditor should investigate further if:

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

8

Which of the following is not a purpose of analytical procedures?

A) Understand the client's industry.

B) Reduce detailed audit tests.

C) Evaluate internal controls.

D) Assess the client's ability to continue as a going concern.

A) Understand the client's industry.

B) Reduce detailed audit tests.

C) Evaluate internal controls.

D) Assess the client's ability to continue as a going concern.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

9

Sarbanes- Oxley requires auditors of public companies to maintain audit documentation for what period of time?

A) Not less than 3 years.

B) Not less than 7 years.

C) Not less than 5 years.

D) Through the issuance of the financial statements.

A) Not less than 3 years.

B) Not less than 7 years.

C) Not less than 5 years.

D) Through the issuance of the financial statements.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

10

Analytical procedures must be used during which phase(s) of the audit?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

11

Which of the following statements is not correct?

A) The quantity of evidence obtained determines its sufficiency.

B) Evidence obtained directly by the auditor is ordinarily more reliable than evidence obtained from other sources.

C) Persuasiveness of evidence is partially determined by the reliability of evidence.

D) The auditor need not consider the independence of an information source when obtaining evidence.

A) The quantity of evidence obtained determines its sufficiency.

B) Evidence obtained directly by the auditor is ordinarily more reliable than evidence obtained from other sources.

C) Persuasiveness of evidence is partially determined by the reliability of evidence.

D) The auditor need not consider the independence of an information source when obtaining evidence.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

12

Which of the following statements regarding inspection is not correct?

A) Inspection includes examining client records such as general ledgers and supporting journals.

B) External documents are considered more reliable than internal documents.

C) Internal documents are documents that are generated within the company and used to communicate with external parties.

D) External documents are documents that are generated outside of the company and are used to communicate the results of a transaction.

A) Inspection includes examining client records such as general ledgers and supporting journals.

B) External documents are considered more reliable than internal documents.

C) Internal documents are documents that are generated within the company and used to communicate with external parties.

D) External documents are documents that are generated outside of the company and are used to communicate the results of a transaction.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

13

Which items affect the sufficiency of evidence when choosing a sample?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

14

Which of the following is an example of vouching?

A) Trace details of employee paychecks to the payroll journal.

B) Trace inventory purchases from the acquisitions journal to supporting invoices.

C) Trace selected sales invoices to the sales journal.

D) All of the above are examples of vouching.

A) Trace details of employee paychecks to the payroll journal.

B) Trace inventory purchases from the acquisitions journal to supporting invoices.

C) Trace selected sales invoices to the sales journal.

D) All of the above are examples of vouching.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

15

Which of the following statements about confirmations is True?

A) Confirmations are expensive and so are often not used.

B) Confirmations may inconvenience those asked to supply them, but they are widely used.

C) Confirmations are sometimes not reliable and so auditors use them only as necessary.

D) Confirmations are required for several balance sheet accounts but no income statement accounts.

A) Confirmations are expensive and so are often not used.

B) Confirmations may inconvenience those asked to supply them, but they are widely used.

C) Confirmations are sometimes not reliable and so auditors use them only as necessary.

D) Confirmations are required for several balance sheet accounts but no income statement accounts.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following statements regarding analytical procedures is not correct?

A) Analytical procedures are required on all audits.

B) For certain accounts with small balances, analytical procedures alone may be sufficient evidence.

C) Analytical tests emphasize a comparison of client internal controls to IFRS.

D) Analytical procedures can be used as substantive tests.

A) Analytical procedures are required on all audits.

B) For certain accounts with small balances, analytical procedures alone may be sufficient evidence.

C) Analytical tests emphasize a comparison of client internal controls to IFRS.

D) Analytical procedures can be used as substantive tests.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not a correct combination of terms and related type of audit evidence?

A) Vouch - inspection.

B) Compare - inspection.

C) Trace - analytical procedures.

D) Foot - recalculation.

A) Vouch - inspection.

B) Compare - inspection.

C) Trace - analytical procedures.

D) Foot - recalculation.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

18

Given the economic constraints in which auditors collect evidence, the auditor normally gathers evidence that is:

A) persuasive.

B) completely convincing.

C) conclusive.

D) irrefutable.

A) persuasive.

B) completely convincing.

C) conclusive.

D) irrefutable.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

19

Audit documentation should provide support for:

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

20

Relevance can be considered only in terms of:

A) balance- related audit objectives.

B) transaction- related audit objectives.

C) general audit objectives.

D) specific audit objectives.

A) balance- related audit objectives.

B) transaction- related audit objectives.

C) general audit objectives.

D) specific audit objectives.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

21

Audit documentation should possess certain characteristics. Which of the following is one of the characteristics?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

22

Which of the following statements is not correct concerning audit documentation?

A) Audit documentation is the primary frame of reference used by supervisory personnel to evaluate the sufficiency of evidence.

B) Audit documentation is acquired to defend against claims that the auditor performed a deficient audit.

C) The only time anyone has a legal right to examine audit documentation is when the documentation is subpoenaed by a court as legal evidence.

D) The auditor may deny requests by the client to review audit evidence.

A) Audit documentation is the primary frame of reference used by supervisory personnel to evaluate the sufficiency of evidence.

B) Audit documentation is acquired to defend against claims that the auditor performed a deficient audit.

C) The only time anyone has a legal right to examine audit documentation is when the documentation is subpoenaed by a court as legal evidence.

D) The auditor may deny requests by the client to review audit evidence.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following statements is correct regarding the costs involved in obtaining evidence?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

24

Identify the three common types of confirmations used by auditors. Indicate which type is most reliable and explain your answer. In addition, indicate which type is least reliable and explain your answer.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

25

Give two examples of relatively reliable documentation and two examples of less reliable documentation. What characteristics distinguish the two?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

26

Discuss the auditor's use of inspection as evidence.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

27

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Watch client employees count inventory to determine whether company procedures are being followed.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Watch client employees count inventory to determine whether company procedures are being followed.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

28

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Count inventory items and record the amount in the audit files.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Count inventory items and record the amount in the audit files.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

29

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Trace postings from the sales journal to the general ledger accounts.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Trace postings from the sales journal to the general ledger accounts.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

30

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Calculate the ratio of cost of goods sold to sales as a test of overall reasonableness of gross margin relative to the preceding year.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Calculate the ratio of cost of goods sold to sales as a test of overall reasonableness of gross margin relative to the preceding year.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

31

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Obtain information about the client's internal controls by asking questions of client personnel.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Obtain information about the client's internal controls by asking questions of client personnel.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

32

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Trace column totals from the cash disbursements journal to the general ledger.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Trace column totals from the cash disbursements journal to the general ledger.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

33

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Examine a piece of equipment to make sure a recent purchase of equipment was actually received and is in operation.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Examine a piece of equipment to make sure a recent purchase of equipment was actually received and is in operation.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

34

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Compute the total of repairs and maintenance for each month to determine whether any month's total was unusually large.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Compute the total of repairs and maintenance for each month to determine whether any month's total was unusually large.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

35

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Compare vendor names and amounts on purchases invoices with entries in the purchases journal.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Compare vendor names and amounts on purchases invoices with entries in the purchases journal.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

36

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Foot entries in the sales journal to determine whether they were correctly totaled by the client.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Foot entries in the sales journal to determine whether they were correctly totaled by the client.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

37

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Make a surprise count of petty cash to verify that the amount of the petty cash fund is intact.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Make a surprise count of petty cash to verify that the amount of the petty cash fund is intact.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

38

Below are 12 audit procedures. Classify each procedure according to the following types of audit evidence:

-Obtain a written statement from the client's bank stating the client's year- end balance on deposit.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

-Obtain a written statement from the client's bank stating the client's year- end balance on deposit.

A) physical examination

B) observation

C) confirmation

D) inspection

E) analytical procedures

F) inquiry of the client

G) recalculation

H) reperformance

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

39

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Canceled checks for payments of accounts payable.

-Canceled checks for payments of accounts payable.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

40

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Payroll time cards.

-Payroll time cards.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

41

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Duplicate sales invoices.

-Duplicate sales invoices.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

42

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Vendors' invoices

-Vendors' invoices

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

43

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Bank statements.

-Bank statements.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

44

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Minutes of the board of directors' meetings.

-Minutes of the board of directors' meetings.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

45

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Signed lease agreements.

-Signed lease agreements.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

46

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Subsidiary accounts receivable records.

-Subsidiary accounts receivable records.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

47

Below are 10 documents typically examined during an audit. Classify each document as either internal or external.

-Remittance advices.

-Remittance advices.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

48

Observation is normally more reliable than physical examination.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

49

One of the primary determinants of the reliability of audit evidence is the quantity of evidence.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

50

Of the three common types of confirmations used by auditors, the least reliable type is the negative confirmation.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

51

Avoiding misunderstandings with the client is important for:

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

52

When inherent risk is high, there will need to be:

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

53

The auditor is likely to accumulate more evidence when the audit is for a company:

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

54

Which of the following is not typically included in initial audit planning?

A) Determination of the purpose of the audit.

B) Client acceptance/continuation decisions.

C) Perform analytical procedures as substantive tests.

D) Obtain an understanding with the client.

A) Determination of the purpose of the audit.

B) Client acceptance/continuation decisions.

C) Perform analytical procedures as substantive tests.

D) Obtain an understanding with the client.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

55

A successor auditor may perform which of the following for a new audit client?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

56

It is easier and more common to implement increased evidence accumulation for inherent risk than for acceptable audit risk because:

A) inherent risk applies to the entire audit.

B) inherent risk can usually be isolated to specific accounts.

C) acceptable audit risk does not impact on the amount of evidence which must be accumulated.

D) acceptable audit risk and sample sizes are set statistically.

A) inherent risk applies to the entire audit.

B) inherent risk can usually be isolated to specific accounts.

C) acceptable audit risk does not impact on the amount of evidence which must be accumulated.

D) acceptable audit risk and sample sizes are set statistically.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

57

Investigating new clients with a focus on assessing the auditor's potential relationship with that new client is a critical element in determining:

A) financial risk.

B) inherent risk.

C) acceptable audit risk.

D) statistical risk.

A) financial risk.

B) inherent risk.

C) acceptable audit risk.

D) statistical risk.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

58

The least effective method of identifying related parties for a public company would be a(n):

A) distribution of the engagement letter to all stockholders.

B) inquiry of management.

C) review of filings to the appropriate capital market.

D) examination of stockholders' listings to identify principal stockholders.

A) distribution of the engagement letter to all stockholders.

B) inquiry of management.

C) review of filings to the appropriate capital market.

D) examination of stockholders' listings to identify principal stockholders.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

59

Which of the following is not likely to be a related party?

A) The chief executive officer.

B) A warehouse employee.

C) Affiliated companies.

D) A major stockholder of the company.

A) The chief executive officer.

B) A warehouse employee.

C) Affiliated companies.

D) A major stockholder of the company.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

60

Which of the following is most likely to occur at the beginning of an initial audit engagement?

A) Study and evaluate the system of internal administrative control.

B) Consult with and review the work of the predecessor auditor prior to discussing the engagement with the client management.

C) Prepare a rough draft of the financial statements and of the auditor's report.

D) Determine the client's reason for an audit.

A) Study and evaluate the system of internal administrative control.

B) Consult with and review the work of the predecessor auditor prior to discussing the engagement with the client management.

C) Prepare a rough draft of the financial statements and of the auditor's report.

D) Determine the client's reason for an audit.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

61

The corporate minutes are the official record of the meetings of the board of directors and stockholders. The minutes typically include authorizations related to:

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

62

Which of the following ratios is best used to assess a company's ability to meet its long- term debt obligations?

A) Debt to equity.

B) Return on common equity.

C) Quick ratio.

D) Current ratio.

A) Debt to equity.

B) Return on common equity.

C) Quick ratio.

D) Current ratio.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

63

Which of the following would not usually be included in the minutes of the board of directors?

A) Approval of executive bonuses.

B) The duties and powers of the corporate officers.

C) Declaration of dividends.

D) Authorization of long- term loans.

A) Approval of executive bonuses.

B) The duties and powers of the corporate officers.

C) Declaration of dividends.

D) Authorization of long- term loans.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

64

Whenever an auditor compares client data to client- prepared budgets, there are two special concerns. Indicate if the two items below are concerns.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

65

Which is usually included in an engagement letter?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

66

Which is usually included in an engagement letter?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

67

Which is usually included in an engagement letter?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

68

Which is usually included in the engagement letter?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

69

Which is usually included in the engagement letter?

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

70

Discuss the required communications between predecessor and successor auditors as outlined by ISA 300.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

71

Before accepting a new client, most audit firms investigate the company to determine its acceptability. However, confidentiality requirements prohibit audit firms from contacting certain parties-such as the company's attorneys and bankers-during this investigation.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

72

Auditors should obtain copies of the client's corporate charter (articles of incorporation), bylaws, and minutes of the meetings of the board of directors to help their understanding of the company's management and governance structure.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

73

Ordinarily, the auditor should review and abstract copies of contracts during the later stages of an audit.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

74

Two categories of audit- relevant information found in corporate charters and bylaws (memorandum and articles of association) are authorizations and discussions of matters affecting inherent risk.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

75

If the omission or misstatement of information, individually or in the aggregate, could reasonably be expected to influence the economic decisions of users of financial statements, then that information is, by definition of ISA 320:

A) insignificant.

B) material.

C) relevant.

D) significant.

A) insignificant.

B) material.

C) relevant.

D) significant.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

76

The FASB definition of materiality emphasizes what class of financial statement users?

A) Informed investors.

B) Potential investors.

C) Regulators.

D) Reasonable persons.

A) Informed investors.

B) Potential investors.

C) Regulators.

D) Reasonable persons.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

77

Auditors are ________ to decide on the combined amount of misstatements in the financial statements that they would consider material early in the audit.

A) permitted

B) required

C) strongly encouraged

D) not allowed

A) permitted

B) required

C) strongly encouraged

D) not allowed

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

78

After the preliminary judgment about materiality has been established, auditors may:

A) adjust it downward only.

B) adjust it either downward or upward.

C) not adjust it.

D) adjust it upward only.

A) adjust it downward only.

B) adjust it either downward or upward.

C) not adjust it.

D) adjust it upward only.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

79

In an audit area that has a lower inherent risk, it would be prudent to:

A) expand planning procedures.

B) increase the tolerable misstatement for the area.

C) assign more experienced staff to that area.

D) increase the amount of audit evidence gathered.

A) expand planning procedures.

B) increase the tolerable misstatement for the area.

C) assign more experienced staff to that area.

D) increase the amount of audit evidence gathered.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

80

Which of the following is least likely to be appropriate as the basis for determining the preliminary judgment about materiality in the audit of financial statements?

A) Owners' equity.

B) Current assets.

C) Net income before taxes.

D) Inventory.

A) Owners' equity.

B) Current assets.

C) Net income before taxes.

D) Inventory.

Unlock Deck

Unlock for access to all 100 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 100 flashcards in this deck.