Deck 8: Audit of the Capital Acquisition, Repayment, Audit of Cash and Financial Instruments, and Completing the Audit

Full screen (f)

Question

Question

Question

Question

Question

Question

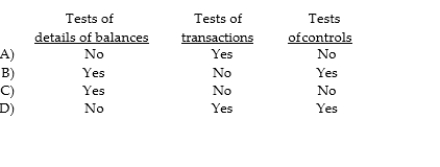

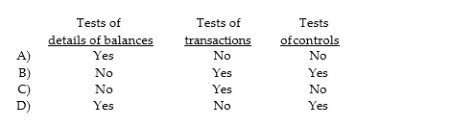

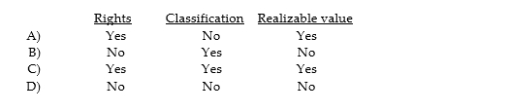

What type of audit test will auditors use when testing to see if existing capital stock transactions are recorded?

Question

What type of audit test will auditors use when testing to see if the amounts of capital stock transactions are accurately recorded?

Question

Question

Question

Question

Question

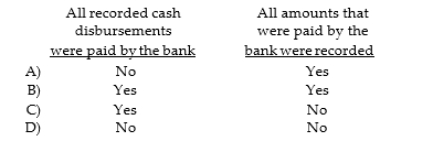

The auditor uses a proof of cash to determine whether:

Question

Question

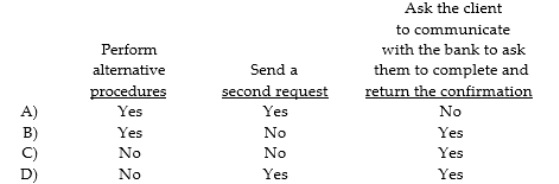

If a bank does not respond to a bank confirmation request, an auditor may:

Question

The most important controls for petty cash relate to:

Question

Which of the following balance- related objectives applies to auditing the general cash account?

Question

Question

Question

Question

Question

Question

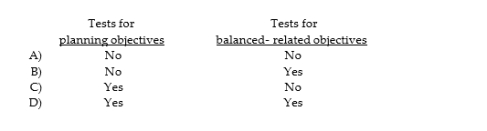

Auditors often integrate procedures for presentation and disclosure objectives with:

Question

Question

Which of the following is a contingent liability with which an auditor is particularly concerned?

Question

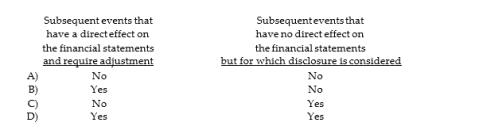

Which type of subsequent event requires consideration by management and evaluation by the auditor?

Question

Who may identify matters to be included in a letter of inquiry sent to a client's legal counsel?

Question

Question

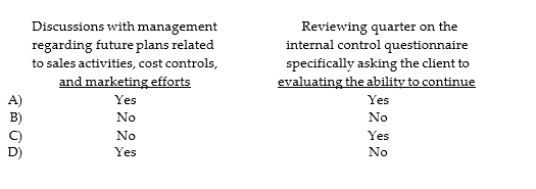

Which of the following procedures and methods are important in assessing a company's ability to continue as a going concern?

Question

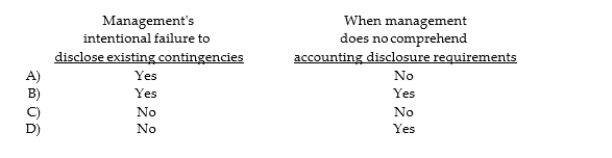

Inquiries of management regarding the possibility of unrecorded contingencies will be useful in uncovering:

Question

Question

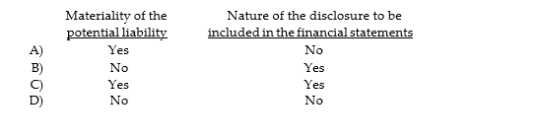

If an auditor concludes there are contingent liabilities, then he or she must evaluate the:

Question

Question

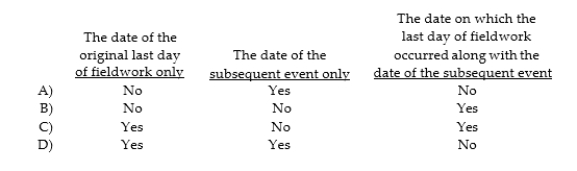

If the auditor determines that a subsequent event that affects the current period financial statements occurred after field work was completed but before the audit report was issued, what date(s) may the auditor use on the report?

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/49

Play

Full screen (f)

Deck 8: Audit of the Capital Acquisition, Repayment, Audit of Cash and Financial Instruments, and Completing the Audit

1

The primary focuses of the audit of debt are:

A) accuracy and completeness.

B) accuracy and existence.

C) completeness and valuation.

D) accuracy and valuation.

A) accuracy and completeness.

B) accuracy and existence.

C) completeness and valuation.

D) accuracy and valuation.

accuracy and completeness.

2

Which of the following accounts is not audited within the capital acquisition and repayment cycle?

A) Interest expense.

B) Accounts payable.

C) Notes payable.

D) Bonds payable.

A) Interest expense.

B) Accounts payable.

C) Notes payable.

D) Bonds payable.

Accounts payable.

3

Which of the following accounts would not normally be seen in the equity section of the balance sheet?

A) Donated capital.

B) Accrued revenue.

C) Common stock.

D) Dividends declared.

A) Donated capital.

B) Accrued revenue.

C) Common stock.

D) Dividends declared.

Accrued revenue.

4

Which of the following is an auditor least likely to consider in determining the appropriate tests of details of balances for notes payable?

A) Business risk.

B) Inherent risk.

C) Acceptable audit risk.

D) Results of analytical procedures.

A) Business risk.

B) Inherent risk.

C) Acceptable audit risk.

D) Results of analytical procedures.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

5

When there are numerous transactions involving notes payable during the year, the auditor will likely:

A) request the client to prepare a schedule of only those notes with unpaid balances at the end of the year.

B) review a schedule of notes payable and accrued interest obtained from the client.

C) perform some other procedure.

D) prepare a schedule of notes payable and accrued interest prepared.

A) request the client to prepare a schedule of only those notes with unpaid balances at the end of the year.

B) review a schedule of notes payable and accrued interest obtained from the client.

C) perform some other procedure.

D) prepare a schedule of notes payable and accrued interest prepared.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

6

What type of audit test will auditors use when testing to see if existing capital stock transactions are recorded?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

7

What type of audit test will auditors use when testing to see if the amounts of capital stock transactions are accurately recorded?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

8

What is a note payable?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

9

Public companies whose stock is listed on a stock exchange must employ a stock transfer agent.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

10

Which of the following is the focus of an audit of cash for most companies?

A) Petty cash account.

B) Money market account.

C) Payroll cash account.

D) General cash account.

A) Petty cash account.

B) Money market account.

C) Payroll cash account.

D) General cash account.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

11

Cash is important to auditors primarily because of the potential for:

A) fraud.

B) errors.

C) liquidity.

D) expenditures.

A) fraud.

B) errors.

C) liquidity.

D) expenditures.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

12

The auditor uses a proof of cash to determine whether:

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

13

The concern in a monthly proof of cash is with:

A) reconciling the amounts per books and bank.

B) identifying cash transfers.

C) adjusting account balances.

D) determining the month- end balance.

A) reconciling the amounts per books and bank.

B) identifying cash transfers.

C) adjusting account balances.

D) determining the month- end balance.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

14

If a bank does not respond to a bank confirmation request, an auditor may:

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

15

The most important controls for petty cash relate to:

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

16

Which of the following balance- related objectives applies to auditing the general cash account?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

17

What is the most important internal control over petty cash?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

18

Discuss the circumstances in which an auditor would prepare a proof of cash.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

19

Do companies usually have significant client business risks affecting cash balances?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

20

It is acceptable for petty cash funds to be mingled with other receipts if circumstances require it.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

21

When auditing the general cash account, receipt of a standard bank confirmation satisfies the completeness objective for unrecorded bank balances and loans from the bank.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

22

Auditors often integrate procedures for presentation and disclosure objectives with:

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

23

Which of the following is an incorrect combination of the 'likelihood of occurrence' and financial statement treatment?

A) Probable (amount is estimable): financial statements are adjusted.

B) Remote: no disclosure.

C) Probable (amount is not estimable): footnote disclosure is required.

D) Reasonably possible (amount is estimable): financial statements are adjusted.

A) Probable (amount is estimable): financial statements are adjusted.

B) Remote: no disclosure.

C) Probable (amount is not estimable): footnote disclosure is required.

D) Reasonably possible (amount is estimable): financial statements are adjusted.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

24

Which of the following is a contingent liability with which an auditor is particularly concerned?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

25

Which type of subsequent event requires consideration by management and evaluation by the auditor?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

26

Who may identify matters to be included in a letter of inquiry sent to a client's legal counsel?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

27

At what stages of the audit must analytical procedures be used?

A) Testing and completion.

B) Planning and testing.

C) Planning, testing, and completion.

D) Planning and completion.

A) Testing and completion.

B) Planning and testing.

C) Planning, testing, and completion.

D) Planning and completion.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

28

Which of the following procedures and methods are important in assessing a company's ability to continue as a going concern?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

29

Inquiries of management regarding the possibility of unrecorded contingencies will be useful in uncovering:

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

30

Which of the following items would ordinarily not be included in the standard letter of inquiry to the client's attorney?

A) A request that the attorney confirm the amount of outstanding fees which client owes for legal services.

B) A request that the attorney furnish an estimate of the amount or range of the potential loss.

C) A request that the attorney furnish information or comment about the likelihood of an unfavorable outcome of litigation.

D) A list, prepared by management, of pending threatened litigation of material amounts.

A) A request that the attorney confirm the amount of outstanding fees which client owes for legal services.

B) A request that the attorney furnish an estimate of the amount or range of the potential loss.

C) A request that the attorney furnish information or comment about the likelihood of an unfavorable outcome of litigation.

D) A list, prepared by management, of pending threatened litigation of material amounts.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

31

If an auditor concludes there are contingent liabilities, then he or she must evaluate the:

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

32

Which of the following determines the sufficiency of evidence?

A) Capital market authority regulations.

B) Adherence to the audit program.

C) Auditing standards.

D) Auditor judgment.

A) Capital market authority regulations.

B) Adherence to the audit program.

C) Auditing standards.

D) Auditor judgment.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

33

If the auditor determines that a subsequent event that affects the current period financial statements occurred after field work was completed but before the audit report was issued, what date(s) may the auditor use on the report?

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

34

Why must audit documentation be reviewed?

A) To evaluate the performance of inexperienced personnel.

B) To ensure that the audit meets the auditing firm's standard of performance.

C) To counteract bias that often enters into the auditor's judgment.

D) All of the above are reasons for review of audit documentation.

A) To evaluate the performance of inexperienced personnel.

B) To ensure that the audit meets the auditing firm's standard of performance.

C) To counteract bias that often enters into the auditor's judgment.

D) All of the above are reasons for review of audit documentation.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

35

List four contingent liabilities that auditors are concerned about in most instances.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

36

Characterize the auditor's role in preparing the financial statements.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

37

The field work for the December 31, 2012 audit of Medina Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On April 5, 2013, you discovered that, on February 16, 2013, a flood destroyed the entire uninsured inventory in one of Medina's warehouses.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

-On April 5, 2013, you discovered that, on February 16, 2013, a flood destroyed the entire uninsured inventory in one of Medina's warehouses.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

38

The field work for the December 31, 2012 audit of Medina Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On February 17, 2013, you discovered that, on February 16, 2013, a flood destroyed the entire uninsured inventory in one of Medina's warehouses.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

-On February 17, 2013, you discovered that, on February 16, 2013, a flood destroyed the entire uninsured inventory in one of Medina's warehouses.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

39

The field work for the December 31, 2012 audit of Medina Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On February 17, 2013, you discovered that, on November 30, 2012, a flood destroyed the entire uninsured inventory in one of Medina's warehouses.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

-On February 17, 2013, you discovered that, on November 30, 2012, a flood destroyed the entire uninsured inventory in one of Medina's warehouses.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

40

The field work for the December 31, 2012 audit of Medina Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On April 5, 2013, you discovered that, on March 30, 2013, a fire destroyed one of Medina's 13 plants.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

-On April 5, 2013, you discovered that, on March 30, 2013, a fire destroyed one of Medina's 13 plants.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

41

The field work for the December 31, 2012 audit of Medina Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On April 7, 2013, you discovered that a debtor of Schmidt went bankrupt on January 6, 2013, due to gradual declining financial health.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

-On April 7, 2013, you discovered that a debtor of Schmidt went bankrupt on January 6, 2013, due to gradual declining financial health.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

42

The field work for the December 31, 2012 audit of Alfa Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On January 16, 2013, a lawsuit was filed against Alfa for a patent infringement action that allegedly took place in early 2005. In the opinion of Alfa's attorneys, there is a reasonable (but not probable) danger of a significant loss to Alfa.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

-On January 16, 2013, a lawsuit was filed against Alfa for a patent infringement action that allegedly took place in early 2005. In the opinion of Alfa's attorneys, there is a reasonable (but not probable) danger of a significant loss to Alfa.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

43

The field work for the December 31, 2012 audit of Alfa Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On February 19, 2013, Alfa settled a lawsuit out of court that had originated in 2002 and is currently listed as a contingent liability.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

-On February 19, 2013, Alfa settled a lawsuit out of court that had originated in 2002 and is currently listed as a contingent liability.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

44

The field work for the December 31, 2012 audit of Alfa Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On March 30, 2013, Alfa settled a lawsuit out of court that had originated in 2004 and is currently listed as a contingent liability.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

-On March 30, 2013, Alfa settled a lawsuit out of court that had originated in 2004 and is currently listed as a contingent liability.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

45

The field work for the December 31, 2012 audit of Alfa Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On February 2, 2013, you discovered an uninsured lawsuit against Alfa that had originated on August 30, 2012.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

-On February 2, 2013, you discovered an uninsured lawsuit against Alfa that had originated on August 30, 2012.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

46

The field work for the December 31, 2012 audit of Alfa Corporation ended on March 17, 2013. The financial statements and auditor's report were issued and mailed to stockholders on March 29, 2013. In each of the material situations below, select the appropriate action.

-On April 7, 2013, you discovered that a debtor of Alfa went bankrupt on January 22, 2013, due to a major uninsured fire that occurred on January 2, 2013.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

-On April 7, 2013, you discovered that a debtor of Alfa went bankrupt on January 22, 2013, due to a major uninsured fire that occurred on January 2, 2013.

A) Adjust the December 31, 2012 financial statements.

B) Disclose the information in a footnote in the December 31, 2012 financial statements.

C) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve an adjustment to the December 31, 2012 financial statements.

D) Request the client revise and reissue the December 31, 2012 financial statements. The revision should involve the addition of a footnote, but no adjustment, to the December 31, 2012 financial statements.

E) No action is required

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

47

ISA 560 and ISA 570 directs the auditor's assessment of going- concern issues.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

48

Auditors are not required to evaluate the going concern assumption as part of each audit.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

49

If an attorney refuses to provide the auditor with information about material existing lawsuits or unasserted claims, auditing standards require that the auditor issue an adverse opinion to reflect the lack of available evidence.

Unlock Deck

Unlock for access to all 49 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 49 flashcards in this deck.