Deck 15: Depreciation and Non-Current Assets

Full screen (f)

Question

Question

Question

Question

Question

Question

The balance at cost of an asset in the ledger is £500. The balance on the provision for depreciation account of the asset is £400. If the asset is sold for £50 the double entry should be:

A)

B)

C)

D)

A)

B)

C)

D)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

It is company policy to depreciate motor vehicles using a 25% reducing balance method. This year's

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

18)The following is an extract from the trial balance for an entity:

A) £14,062.50

B) £14,453.10

C) £10,546.90

D) £3,515.60

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

18)The following is an extract from the trial balance for an entity:

A) £14,062.50

B) £14,453.10

C) £10,546.90

D) £3,515.60

Question

It is company policy to depreciate motor vehicles using a 25% straight line method. This year's

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

The following is an extract from the trial balance for an entity:

A) £17,500

B) £22,500

C) £40,000

D) £47,500

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

The following is an extract from the trial balance for an entity:

A) £17,500

B) £22,500

C) £40,000

D) £47,500

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/20

Play

Full screen (f)

Deck 15: Depreciation and Non-Current Assets

1

Entities charge depreciation each year:

A) To ensure there is enough money in the firm to replace the asset

B) To spread the cost of the asset over its working life

C) To reduce the profit and thus the dividends they can pay to shareholders

D) Because the law states they must depreciate all assets held

A) To ensure there is enough money in the firm to replace the asset

B) To spread the cost of the asset over its working life

C) To reduce the profit and thus the dividends they can pay to shareholders

D) Because the law states they must depreciate all assets held

To spread the cost of the asset over its working life

2

An entity buys an asset for £1,000 and depreciates it using the reducing balance method. Which of the following amounts would be the second year's depreciation charge at 10% per annum?

A) £80

B) £81

C) £90

D) £100

A) £80

B) £81

C) £90

D) £100

£90

3

The net book value of a non-current asset represents:

A) The replacement value of that asset

B) Its market value on a going concern basis

C) Its realisable value in a forced sale

D) Its undepreciated cost

A) The replacement value of that asset

B) Its market value on a going concern basis

C) Its realisable value in a forced sale

D) Its undepreciated cost

Its undepreciated cost

4

Depreciation is:

A) A way of setting aside money to provide for the eventual replacement of non-current assets

B) A way of writing off the cost of non-current assets over their estimated revenue-generating period

C) The fall in value of non-current assets over their estimated useful economic lives

D) The writing off of the cost of non-current assets over their estimated useful economic lives in ever decreasing amounts.

A) A way of setting aside money to provide for the eventual replacement of non-current assets

B) A way of writing off the cost of non-current assets over their estimated revenue-generating period

C) The fall in value of non-current assets over their estimated useful economic lives

D) The writing off of the cost of non-current assets over their estimated useful economic lives in ever decreasing amounts.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

5

The sale of equipment costing £8,000, with accumulated depreciation of £6,700 and a sale price of £2,000, would result in a:

A) Gain of £2,000

B) Gain of £700

C) Loss of £700

D) Loss of £600

A) Gain of £2,000

B) Gain of £700

C) Loss of £700

D) Loss of £600

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

6

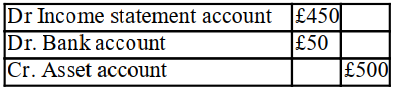

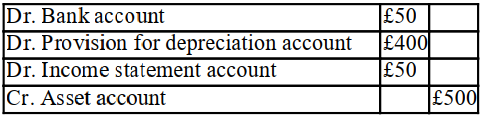

The balance at cost of an asset in the ledger is £500. The balance on the provision for depreciation account of the asset is £400. If the asset is sold for £50 the double entry should be:

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

7

The cost of an entity's assets three years ago was £24,000. Depreciation was charged at the rate of 10% per annum using the straight line method. The firm decided to change its method to reducing balance at 10% per annum with retrospective effect. The total difference in the profits over the three years would be:

A) £669

B) £696

C) £966

D) £969

A) £669

B) £696

C) £966

D) £969

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

8

A car cost £9,000. It has an expected useful life of 6 years, and an expected residual value £1,000. It is to be depreciated at 30% per annum on the reducing balance basis. During year four the car was sold for £3,000. A full year's depreciation is charged in the year of purchase, with none in the year of sale. The profit or loss on disposal is

A) Loss £87.

B) Loss £2,000.

C) Profit £256.

D) Profit £1,200.

A) Loss £87.

B) Loss £2,000.

C) Profit £256.

D) Profit £1,200.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

9

The balance on an entity's plant and machinery account on 1 January 20X2 was £5,000. During that year the following transactions took place on the dates shown:-

1 May 20X2 Plant which had originally cost £750, was sold

1 September 20X2 New machinery costing £3,000 was purchased

If depreciation is calculated at a rate of 10% per annum, on a strict time basis, using the straight line basis, the depreciation charge on plant and machinery for the year to 31 December 20X2, to the nearest pound is:

A) £525

B) £550

C) £600

D) £625

1 May 20X2 Plant which had originally cost £750, was sold

1 September 20X2 New machinery costing £3,000 was purchased

If depreciation is calculated at a rate of 10% per annum, on a strict time basis, using the straight line basis, the depreciation charge on plant and machinery for the year to 31 December 20X2, to the nearest pound is:

A) £525

B) £550

C) £600

D) £625

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

10

The cost of the non-current asset sold was:

A) £5,700

B) £8,300

C) £4,100

D) £5,000

A) £5,700

B) £8,300

C) £4,100

D) £5,000

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

11

The depreciation charge for the year ending 31/12/X0 was:

A) £500

B) £11,700

C) £7,300

D) £7,500

A) £500

B) £11,700

C) £7,300

D) £7,500

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

12

Amounts spent on non-current assets in the year to 31/12/X0 were:

A) £10,800

B) £13,100

C) £16,500

D) £22,200

A) £10,800

B) £13,100

C) £16,500

D) £22,200

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

13

Tom Ltd. bought a new machine. The cost of the machine was £10,000. The installation costs were £1,000 and the employees received specific training on how to use this particular machine, at a cost of £200. Before using the machine to make parts, a test was performed, and the oil and initial parts required for this test cost £50. It costs £100 to insure the machine for the year.

What should the cost of the machine be in the balance sheet?

A) £10,000.

B) £11,000.

C) £11,250.

D) £11,350.

What should the cost of the machine be in the balance sheet?

A) £10,000.

B) £11,000.

C) £11,250.

D) £11,350.

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

14

The net book value of this asset will now disappear from the register (£30,000 - £19,500) = £10,500 The new balance on the non-current asset register is £134,920 - £10,500 = £124,420

A non-current asset register showed a net book value of £134,920. A non-current asset costing £30,000 had been sold for £8,000, making a loss on disposal of £2,500. No entries had been made in the non-current asset register for this disposal.

The balance on the non-current asset register is:

A) £102,420

B) £107,420

C) £115,420

D) £124,420

A non-current asset register showed a net book value of £134,920. A non-current asset costing £30,000 had been sold for £8,000, making a loss on disposal of £2,500. No entries had been made in the non-current asset register for this disposal.

The balance on the non-current asset register is:

A) £102,420

B) £107,420

C) £115,420

D) £124,420

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

15

X Ltd bought a new printing machine. The machine cost £160,000. The installation costs were £10,000 and the employees received a training course on how to use the machine (cost £4,000). Before using the machine for normal day-to-day activities the installers undertook a test to ensure the machine worked, this test utilised paper and ink worth £2,000.

At what value will the machine be included in the statement of financial position?

A) £160,000

B) £170,000

C) £174,000

D) £176,000

At what value will the machine be included in the statement of financial position?

A) £160,000

B) £170,000

C) £174,000

D) £176,000

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

16

A car was purchased by a tile retailer in May 20W9 for £30,300 (including road tax for the year to 20X0 of £300). The business has a 31 December year end. The car was traded in on the 1st August 20X2 for £15,000.

The entity's accounting policy in respect of the depreciation of cars is to apply a 25% reducing balance method, with a full year's depreciation being charged in the year of purchase and none in the year of sale.

Given this information, what was the profit/loss on the trade-in during the year ended 31st December 20X2?

A) Profit of £2,154

B) Profit of £2,344

C) Profit of £5,364

D) Profit of £5,508

The entity's accounting policy in respect of the depreciation of cars is to apply a 25% reducing balance method, with a full year's depreciation being charged in the year of purchase and none in the year of sale.

Given this information, what was the profit/loss on the trade-in during the year ended 31st December 20X2?

A) Profit of £2,154

B) Profit of £2,344

C) Profit of £5,364

D) Profit of £5,508

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

17

Replacement shelving (£500) was recorded as fixtures and fittings. As a result:

A) Profit is overstated by £500 and non-current assets are overstated by £500

B) Profit is understated by £500 and non-current assets are understated by £500

C) Profit is understated by £500 and non-current assets are overstated by £500

D) Profit is overstated by £500 and non-current assets are understated by £500

A) Profit is overstated by £500 and non-current assets are overstated by £500

B) Profit is understated by £500 and non-current assets are understated by £500

C) Profit is understated by £500 and non-current assets are overstated by £500

D) Profit is overstated by £500 and non-current assets are understated by £500

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

18

It is company policy to depreciate motor vehicles using a 25% reducing balance method. This year's

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

18)The following is an extract from the trial balance for an entity:

A) £14,062.50

B) £14,453.10

C) £10,546.90

D) £3,515.60

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

18)The following is an extract from the trial balance for an entity:

A) £14,062.50

B) £14,453.10

C) £10,546.90

D) £3,515.60

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

19

It is company policy to depreciate motor vehicles using a 25% straight line method. This year's

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

The following is an extract from the trial balance for an entity:

A) £17,500

B) £22,500

C) £40,000

D) £47,500

Depreciation has not yet been adjusted for.

What is the balance on the provision for depreciation account after the depreciation adjustment has

Been made?

The following is an extract from the trial balance for an entity:

A) £17,500

B) £22,500

C) £40,000

D) £47,500

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

20

Accumulated depreciation

Year 1 20X8 £48,000 x 20% = £9,600

Year 2 20X9 (£48,000 - £9,600) x 20% = £7,680

Year 3 20Y0 (£48,000 - £9,600 - £7,680) x 20% = £6,144

Total depreciation = £23,424

A lorry was purchased in 20X8 for £48,000 and depreciated by 20% using the reducing balance method. It is the entity's policy to charge a full year's depreciation in the year of purchase and none in the year of sale. In the second month of 20Y1 it was sold for £24,000. This resulted in:

A) A loss on disposal of £4,800

B) A loss on disposal of £576

C) A profit on disposal of £4,800

D) A profit on disposal of £576

Year 1 20X8 £48,000 x 20% = £9,600

Year 2 20X9 (£48,000 - £9,600) x 20% = £7,680

Year 3 20Y0 (£48,000 - £9,600 - £7,680) x 20% = £6,144

Total depreciation = £23,424

A lorry was purchased in 20X8 for £48,000 and depreciated by 20% using the reducing balance method. It is the entity's policy to charge a full year's depreciation in the year of purchase and none in the year of sale. In the second month of 20Y1 it was sold for £24,000. This resulted in:

A) A loss on disposal of £4,800

B) A loss on disposal of £576

C) A profit on disposal of £4,800

D) A profit on disposal of £576

Unlock Deck

Unlock for access to all 20 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 20 flashcards in this deck.