Deck 17: Accounting for Leases

Full screen (f)

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

Question

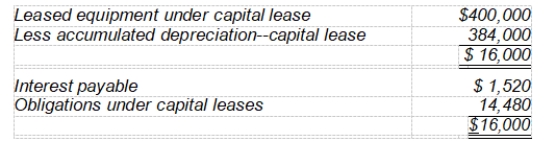

Estes Co. leased a machine to Dains Co. Assume the lease payments were made on the basis that the residual value was guaranteed and Estes gets to recognize all the profits, and at the end of the lease term, before the lessee transfers the asset to the lessor, the leased asset and obligation accounts have the following balances:

If, at the end of the lease, the fair market value of the residual value is $8,800, what gain or loss should Estes record?

If, at the end of the lease, the fair market value of the residual value is $8,800, what gain or loss should Estes record?

A) $6,480 gain

B) $7,120 loss

C) $7,200 loss

D) $8,800 gain

If, at the end of the lease, the fair market value of the residual value is $8,800, what gain or loss should Estes record?A) $6,480 gain

B) $7,120 loss

C) $7,200 loss

D) $8,800 gain

Question

Question

Question

Question

Question

Question

Bohl Co. purchases land and constructs a service station and car wash for a total of $360,000. At January 2, 2007, when construction is completed, the facility and land on which it was constructed are sold to a major oil company for $400,000 and immediately leased from the oil company by Bohl. Fair value of the land at time of the sale was $40,000. The lease is a 10-year, noncancelable lease. Bohl uses straight-line depreciation for its other various business holdings. The economic life of the facility is 15 years with zero salvage value. Title to the facility and land will pass to Bohl at termination of the lease. A partial amortization schedule for this lease is as follows:

-From the viewpoint of the lessor, what type of lease is involved above?

A) Sales-type lease

B) Operating lease

C) Direct-financing lease

D) None of these

-From the viewpoint of the lessor, what type of lease is involved above?

A) Sales-type lease

B) Operating lease

C) Direct-financing lease

D) None of these

Question

Bohl Co. purchases land and constructs a service station and car wash for a total of $360,000. At January 2, 2007, when construction is completed, the facility and land on which it was constructed are sold to a major oil company for $400,000 and immediately leased from the oil company by Bohl. Fair value of the land at time of the sale was $40,000. The lease is a 10-year, noncancelable lease. Bohl uses straight-line depreciation for its other various business holdings. The economic life of the facility is 15 years with zero salvage value. Title to the facility and land will pass to Bohl at termination of the lease. A partial amortization schedule for this lease is as follows:

-What is the amount of the lessee's liability to the lessor after the December 31, 2009 payment? (Rounded to the nearest dollar.)

A) $400,000

B) $374,902

C) $347,294

D) $316,925

-What is the amount of the lessee's liability to the lessor after the December 31, 2009 payment? (Rounded to the nearest dollar.)

A) $400,000

B) $374,902

C) $347,294

D) $316,925

Question

Question

Question

Unlock Deck

Sign up to unlock the cards in this deck!

Unlock Deck

Unlock Deck

1/59

Play

Full screen (f)

Deck 17: Accounting for Leases

1

An essential element of the lease agreement is that the lessor conveys less than the total interest in the property.

True

2

An operating lease refers to a lease agreement for property used in the operations of the lessee's business.

False

3

If a lease is noncancelable and contains a bargain purchase option, the lessee shall classify and account for the arrangement as a capital lease.

True

4

Under the operating method, the lessee assigns rent to the periods benefiting from the use of the asset and does not record the commitment to make future payments.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

5

Under the capital lease method, the lessee treats the lease transaction as if an asset were being purchased on an installment payment basis.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

6

The lessee records a capital lease as an asset, using the fair market value of the leased asset on the date of the lease as the asset's cost.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

7

When the lessor accounts for minimum lease payments, the basis for capitalization includes the guaranteed residual value but excludes the unguaranteed residual value.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

8

A lessee would treat guaranteed residual value as an additional lease payment that will be paid in property or cash, or both, at the end of the lease term.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

9

One of the major distinctions between an operating lease and a capital lease is the fact that annual rental payments under a capital lease are higher than rental payments under an operating lease.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

10

A lessor must be a manufacturer or dealer to realize a profit (or loss) at the inception of a lease that requires application of sales-type lease accounting.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

11

All leases that do not qualify as direct financing or sales-type leases are classified and accounted for by the lessors as capital leases.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

12

The interest revenue related to a lease transaction accounted for under the direct financing method should be reported as income over the lease term by use of the effective interest method.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

13

Companies that use sales-type leases recognize income later than if a direct-financing lease is used.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

14

During the term of the lease, assets recorded under capital leases are separately identified in the lessee's balance sheet.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

15

Lease disclosure requirements on the part of the lessor apply only to lessors whose predominant business activity is leasing.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

16

While only certain leases are currently accounted for as a sale or purchase, there is theoretic justification for considering all leases to be sales or purchases. The principal reason that supports this idea is that

A) all leases are generally for the economic life of the property and the residual value of the property at the end of the lease is minimal.

B) at the end of the lease the property usually can be purchased by the lessee.

C) a lease reflects the purchase or sale of a quantifiable right to the use of property.

D) during the life of the lease the lessee can effectively treat the property as if it were owned by the lessee.

A) all leases are generally for the economic life of the property and the residual value of the property at the end of the lease is minimal.

B) at the end of the lease the property usually can be purchased by the lessee.

C) a lease reflects the purchase or sale of a quantifiable right to the use of property.

D) during the life of the lease the lessee can effectively treat the property as if it were owned by the lessee.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

17

Which of the following is not one of the commonly discussed advantages of leasing?

A) Leasing permits 100% financing versus 60 to 80% when purchasing an asset.

B) Leasing permits rapid changes in equipment, thus reducing the risk of obsolescence.

C) Leasing improves financial ratios by increasing assets without a corresponding increase in debt.

D) Leasing permits write-off of the full cost of the asset.

A) Leasing permits 100% financing versus 60 to 80% when purchasing an asset.

B) Leasing permits rapid changes in equipment, thus reducing the risk of obsolescence.

C) Leasing improves financial ratios by increasing assets without a corresponding increase in debt.

D) Leasing permits write-off of the full cost of the asset.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

18

The accounting principles used in lease accounting attempt to provide symmetry between the lessee and lessor. With respect to lease rental payments in a capital lease, they are considered to consist of both interest and principal by the

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

19

Which of the following lease arrangements would most likely be accounted for as an operating lease by the lessee?

A) The lease agreement runs for 15 years and the economic life of the leased property is 20 years.

B) The present value of the minimum lease payments is $55,600 and the fair value of the leased property is $60,000.

C) The lease agreement allows the lessee the right to purchase the leased asset for $1.00 when half of the asset's economic useful life has expired.

D) The lessee may renew the two-year lease for an additional two years at the same rental.

A) The lease agreement runs for 15 years and the economic life of the leased property is 20 years.

B) The present value of the minimum lease payments is $55,600 and the fair value of the leased property is $60,000.

C) The lease agreement allows the lessee the right to purchase the leased asset for $1.00 when half of the asset's economic useful life has expired.

D) The lessee may renew the two-year lease for an additional two years at the same rental.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

20

If the lease term is equal to 75% or more of the estimated economic life of the leased property, the asset should be capitalized by the lessee. The one exception to this rule is when the

A) lease term is for 5 years or less.

B) lessee does not intend to exercise its option to purchase the asset at the conclusion of the lease term.

C) lessor refuses to offer a bargain purchase option and the leased property will revert to the lessor at the end of the lease term.

D) inception of the lease occurs during the last 25% of the life of the asset.

A) lease term is for 5 years or less.

B) lessee does not intend to exercise its option to purchase the asset at the conclusion of the lease term.

C) lessor refuses to offer a bargain purchase option and the leased property will revert to the lessor at the end of the lease term.

D) inception of the lease occurs during the last 25% of the life of the asset.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

21

Minimum lease payments are payments the lessee is obligated to make or can be expected to make in connection with the leased property. In computing minimum lease payments, all of the following would be included except the

A) present value of the cost of the leased asset.

B) penalty for failure to renew or extend the lease.

C) bargain purchase option.

D) minimum rental payments.

A) present value of the cost of the leased asset.

B) penalty for failure to renew or extend the lease.

C) bargain purchase option.

D) minimum rental payments.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

22

Under an operating lease, a rent expense accrues day by day to the lessee as the property is used. This amount of rent expense is

A) capitalized in an asset account and charged against income as the asset depreciates.

B) capitalized in an asset account and netted against the corresponding lease liability each time a balance sheet is prepared.

C) charged against income in the periods benefiting from the use of the asset.

D) charged against income at the same rate as the reduction in the corresponding lease liability.

A) capitalized in an asset account and charged against income as the asset depreciates.

B) capitalized in an asset account and netted against the corresponding lease liability each time a balance sheet is prepared.

C) charged against income in the periods benefiting from the use of the asset.

D) charged against income at the same rate as the reduction in the corresponding lease liability.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

23

What impact does a bargain purchase option have on the present value of the minimum lease payments computed by the lessee?

A) No impact as the option does not enter into the transaction until the end of the lease term.

B) The lessee must increase the present value of the minimum lease payments by the present value of the option price.

C) The lessee must decrease the present value of the minimum lease payments by the present value of the option price.

D) The minimum lease payments would be increased by the present value of the option price if, at the time of the lease agreement, it appeared certain that the lessee would exercise the option at the end of the lease and purchase the asset at the option price.

A) No impact as the option does not enter into the transaction until the end of the lease term.

B) The lessee must increase the present value of the minimum lease payments by the present value of the option price.

C) The lessee must decrease the present value of the minimum lease payments by the present value of the option price.

D) The minimum lease payments would be increased by the present value of the option price if, at the time of the lease agreement, it appeared certain that the lessee would exercise the option at the end of the lease and purchase the asset at the option price.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

24

If a lease transaction is accorded capital lease treatment rather than operating lease treatment, it would have what impact on the following financial items of the lessee?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

25

In addition to the four criteria that a lessee must assess in deciding whether to classify a lease transaction as a capital lease, a lessor must meet two additional criteria. These include (1) the collectibility of the payments required from the lessee is reasonably predictable, and (2)

A) the lease includes an element of manufacturer or dealer profit.

B) the lessee has the ability to meet the requirements of the guaranteed residual value.

C) executory costs are provided for in a manner which makes their ultimate payment virtually a certainty.

D) no important uncertainties surround the amount of unreimbursable costs yet to be incurred by the lessor under the lease.

A) the lease includes an element of manufacturer or dealer profit.

B) the lessee has the ability to meet the requirements of the guaranteed residual value.

C) executory costs are provided for in a manner which makes their ultimate payment virtually a certainty.

D) no important uncertainties surround the amount of unreimbursable costs yet to be incurred by the lessor under the lease.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

26

Based solely upon the following sets of circumstances indicated below, which set gives rise to a sales-type or direct-financing lease of a lessor?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

27

In order to properly record a direct-financing lease, the lessor needs to know how to calculate the lease receivable. The lease receivable in a direct-financing lease is best defined as

A) the amount of funds the lessor has tied up in the asset which is the subject of the direct-financing lease.

B) the difference between the lease payments receivable and the fair market value of the leased property.

C) the present value of minimum lease payments.

D) the total book value of the asset less any accumulated depreciation recorded by the lessor prior to the lease agreement.

A) the amount of funds the lessor has tied up in the asset which is the subject of the direct-financing lease.

B) the difference between the lease payments receivable and the fair market value of the leased property.

C) the present value of minimum lease payments.

D) the total book value of the asset less any accumulated depreciation recorded by the lessor prior to the lease agreement.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

28

A lessor with a sales-type lease involving an unguaranteed residual value available to the lessor at the end of the lease term will report sales revenue in the period of inception of the lease at which of the following amounts?

A) The minimum lease payments plus the unguaranteed residual value.

B) The present value of the minimum lease payments.

C) The cost of the asset to the lessor, less the present value of any unguaranteed residual value.

D) The present value of the minimum lease payments plus the present value of the unguaranteed residual value.

A) The minimum lease payments plus the unguaranteed residual value.

B) The present value of the minimum lease payments.

C) The cost of the asset to the lessor, less the present value of any unguaranteed residual value.

D) The present value of the minimum lease payments plus the present value of the unguaranteed residual value.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

29

With respect to the computation of minimum lease payments by the lessee, how are the following items handled in the computation?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

30

On January 1, 2008, Penn Corporation signed a ten-year noncancelable lease for certain machinery. The terms of the lease called for Penn to make annual payments of $100,000 at the end of each year for ten years with title to pass to Penn at the end of this period. The machinery has an estimated useful life of 15 years and no salvage value. Penn uses the straight-line method of depreciation for all of its fixed assets. Penn accordingly accounted for this lease transaction as a capital lease. The lease payments were determined to have a present value of $671,008 at an effective interest rate of 8%. With respect to this capitalized lease, Penn should record for 2008

A) lease expense of $100,000.

B) interest expense of $44,734 and depreciation expense of $38,068.

C) interest expense of $53,681 and depreciation expense of $44,734.

D) interest expense of $45,681 and depreciation expense of $67,101.

A) lease expense of $100,000.

B) interest expense of $44,734 and depreciation expense of $38,068.

C) interest expense of $53,681 and depreciation expense of $44,734.

D) interest expense of $45,681 and depreciation expense of $67,101.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

31

On January 1, 2008, Dexter, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Garr Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-What is the amount of the minimum annual lease payment? (Rounded to the nearest dollar.)

A) $188,237

B) $478,236

C) $488,236

D) $498,236

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-What is the amount of the minimum annual lease payment? (Rounded to the nearest dollar.)

A) $188,237

B) $478,236

C) $488,236

D) $498,236

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

32

On January 1, 2008, Dexter, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Garr Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-What is the amount of the total annual lease payment?

A) $188,237

B) $478,237

C) $488,237

D) $498,237

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-What is the amount of the total annual lease payment?

A) $188,237

B) $478,237

C) $488,237

D) $498,237

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

33

On January 1, 2008, Dexter, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Garr Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-From the lessor's viewpoint, what type of lease is involved?

A) Sales-type lease

B) Sale-leaseback

C) Direct-financing lease

D) Operating lease

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-From the lessor's viewpoint, what type of lease is involved?

A) Sales-type lease

B) Sale-leaseback

C) Direct-financing lease

D) Operating lease

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

34

On January 1, 2008, Dexter, Inc. signs a 10-year noncancelable lease agreement to lease a storage building from Garr Warehouse Company. Collectibility of lease payments is reasonably predictable and no important uncertainties surround the amount of costs yet to be incurred by the lessor. The following information pertains to this lease agreement.

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-From the lessee's viewpoint, what type of lease exists in this case?

A) Sales-type lease

B) Sale-leaseback

C) Capital lease

D) Operating lease

(a) The agreement requires equal rental payments at the end of each year.

(b) The fair value of the building on January 1, 2008 is $3,000,000; however, the book value to Garr is $2,500,000.

(c) The building has an estimated economic life of 10 years, with no residual value. Dexter depreciates similar buildings on the straight-line method.

(d) At the termination of the lease, the title to the building will be transferred to the lessee.

(e) Dexter's incremental borrowing rate is 11% per year. Garr Warehouse Co. set the annual rental to ensure a 10% rate of return. The implicit rate of the lessor is known by Dexter, Inc.

(f) The yearly rental payment includes $10,000 of executory costs related to taxes on the property.

-From the lessee's viewpoint, what type of lease exists in this case?

A) Sales-type lease

B) Sale-leaseback

C) Capital lease

D) Operating lease

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

35

Huffman Company leases a machine from Lincoln Corp. under an agreement which meets the criteria to be a capital lease for Huffman. The six-year lease requires payment of $102,000 at the beginning of each year, including $15,000 per year for maintenance, insurance, and taxes. The incremental borrowing rate for the lessee is 10%; the lessor's implicit rate is 8% and is known by the lessee. The present value of an annuity due of 1 for six years at 10% is 4.79079. The present value of an annuity due of 1 for six years at 8% is 4.99271. Huffman should record the leased asset at

A) $509,256.

B) $488,661.

C) $434,366.

D) $416,799.

A) $509,256.

B) $488,661.

C) $434,366.

D) $416,799.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

36

On December 31, 2007, Pool Corporation leased a ship from Renn Company for an eight-year period expiring December 30, 2015. Equal annual payments of $200,000 are due on December 31 of each year, beginning with December 31, 2007. The lease is properly classified as a capital lease on Pool's books. The present value at December 31, 2007 of the eight lease payments over the lease term discounted at 10% is $1,173,685. Assuming all payments are made on time, the amount that should be reported by Pool Corporation as the total obligation under capital leases on its December 31, 2008 balance sheet is

A) $1,091,054.

B) $1,000,159.

C) $871,054.

D) $1,200,000.

A) $1,091,054.

B) $1,000,159.

C) $871,054.

D) $1,200,000.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

37

On January 1, 2008, Dalton Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Dalton to make annual payments of $50,000 at the beginning of each year for five years with title to pass to Dalton at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Dalton uses the straight-line method of depreciation for all of its fixed assets. Dalton accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $208,493 at an effective interest rate of 10%.

-In 2008, Dalton should record interest expense of

A) $15,849.

B) $29,151.

C) $20,849.

D) $34,151.

-In 2008, Dalton should record interest expense of

A) $15,849.

B) $29,151.

C) $20,849.

D) $34,151.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

38

On January 1, 2008, Dalton Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Dalton to make annual payments of $50,000 at the beginning of each year for five years with title to pass to Dalton at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Dalton uses the straight-line method of depreciation for all of its fixed assets. Dalton accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $208,493 at an effective interest rate of 10%.

-In 2009, Dalton should record interest expense of

A) $10,849.

B) $12,434.

C) $15,849.

D) $17,434.

-In 2009, Dalton should record interest expense of

A) $10,849.

B) $12,434.

C) $15,849.

D) $17,434.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

39

On December 31, 2008, Dodd Corporation leased a plane from Aero Company for an eight-year period expiring December 30, 2016. Equal annual payments of $150,000 are due on December 31 of each year, beginning with December 31, 2008. The lease is properly classified as a capital lease on Dodd's books. The present value at December 31, 2008 of the eight lease payments over the lease term discounted at 10% is $880,264. Assuming the first payment is made on time, the amount that should be reported by Dodd Corporation as the lease liability on its December 31, 2008 balance sheet is

A) $880,264.

B) $818,290.

C) $792,238.

D) $730,264.

A) $880,264.

B) $818,290.

C) $792,238.

D) $730,264.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

40

On January 1, 2008, Carley Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Carley to make annual payments of $60,000 at the end of each year for five years with title to pass to Carley at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Carley uses the straight-line method of depreciation for all of its fixed assets. Carley accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $227,448 at an effective interest rate of 10%.

-With respect to this capitalized lease, for 2008 Carley should record

A) rent expense of $60,000.

B) interest expense of $22,745 and depreciation expense of $45,489.

C) interest expense of $22,745 and depreciation expense of $32,493.

D) interest expense of $30,000 and depreciation expense of $45,489.

-With respect to this capitalized lease, for 2008 Carley should record

A) rent expense of $60,000.

B) interest expense of $22,745 and depreciation expense of $45,489.

C) interest expense of $22,745 and depreciation expense of $32,493.

D) interest expense of $30,000 and depreciation expense of $45,489.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

41

On January 1, 2008, Carley Corporation signed a five-year noncancelable lease for equipment. The terms of the lease called for Carley to make annual payments of $60,000 at the end of each year for five years with title to pass to Carley at the end of this period. The equipment has an estimated useful life of 7 years and no salvage value. Carley uses the straight-line method of depreciation for all of its fixed assets. Carley accordingly accounts for this lease transaction as a capital lease. The minimum lease payments were determined to have a present value of $227,448 at an effective interest rate of 10%.

-With respect to this capitalized lease, for 2009 Carley should record

A) interest expense of $22,745 and depreciation expense of $32,493.

B) interest expense of $20,469 and depreciation expense of $32,493.

C) interest expense of $19,019 and depreciation expense of $32,493.

D) interest expense of $14,469 and depreciation expense of $32,493.

-With respect to this capitalized lease, for 2009 Carley should record

A) interest expense of $22,745 and depreciation expense of $32,493.

B) interest expense of $20,469 and depreciation expense of $32,493.

C) interest expense of $19,019 and depreciation expense of $32,493.

D) interest expense of $14,469 and depreciation expense of $32,493.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

42

Barkley Corporation is a lessee with a capital lease. The asset is recorded at $450,000 and has an economic life of 8 years. The lease term is 5 years. The asset is expected to have a market value of $150,000 at the end of 5 years, and a market value of $50,000 at the end of 8 years. The lease agreement provides for the transfer of title of the asset to the lessee at the end of the lease term. What amount of depreciation expense would the lessee record for the first year of the lease?

A) $90,000

B) $80,000

C) $60,000

D) $50,000

A) $90,000

B) $80,000

C) $60,000

D) $50,000

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

43

Hay Corporation enters into an agreement with Marly Rentals Co. on January 1, 2008 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $155,213 are due on December 31 of each year.

(b) The fair value of the machine on January 1, 2008, is $400,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Hay depreciates all machinery it owns on a straight-line basis.

(d) Hay's incremental borrowing rate is 10% per year. Hay does not have knowledge of the 8% implicit rate used by Marly.

(e) Immediately after signing the lease, Marly finds out that Hay Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

-What type of lease is this from Hay Corporation's viewpoint?

A) Operating lease

B) Capital lease

C) Sales-type lease

D) Direct-financing lease

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $155,213 are due on December 31 of each year.

(b) The fair value of the machine on January 1, 2008, is $400,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Hay depreciates all machinery it owns on a straight-line basis.

(d) Hay's incremental borrowing rate is 10% per year. Hay does not have knowledge of the 8% implicit rate used by Marly.

(e) Immediately after signing the lease, Marly finds out that Hay Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

-What type of lease is this from Hay Corporation's viewpoint?

A) Operating lease

B) Capital lease

C) Sales-type lease

D) Direct-financing lease

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

44

Hay Corporation enters into an agreement with Marly Rentals Co. on January 1, 2008 for the purpose of leasing a machine to be used in its manufacturing operations. The following data pertain to the agreement:

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $155,213 are due on December 31 of each year.

(b) The fair value of the machine on January 1, 2008, is $400,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Hay depreciates all machinery it owns on a straight-line basis.

(d) Hay's incremental borrowing rate is 10% per year. Hay does not have knowledge of the 8% implicit rate used by Marly.

(e) Immediately after signing the lease, Marly finds out that Hay Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

-From the viewpoint of Marly, what type of lease agreement exists?

A) Operating lease

B) Capital lease

C) Sales-type lease

D) Direct-financing lease

(a) The term of the noncancelable lease is 3 years with no renewal option. Payments of $155,213 are due on December 31 of each year.

(b) The fair value of the machine on January 1, 2008, is $400,000. The machine has a remaining economic life of 10 years, with no salvage value. The machine reverts to the lessor upon the termination of the lease.

(c) Hay depreciates all machinery it owns on a straight-line basis.

(d) Hay's incremental borrowing rate is 10% per year. Hay does not have knowledge of the 8% implicit rate used by Marly.

(e) Immediately after signing the lease, Marly finds out that Hay Corp. is the defendant in a suit which is sufficiently material to make collectibility of future lease payments doubtful.

-From the viewpoint of Marly, what type of lease agreement exists?

A) Operating lease

B) Capital lease

C) Sales-type lease

D) Direct-financing lease

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

45

Sele Company leased equipment to Snead Company on July 1, 2007, for a one-year period expiring June 30, 2008, for $60,000 a month. On July 1, 2008, Sele leased this piece of equipment to Quirk Company for a three-year period expiring June 30, 2011, for $75,000 a month. The original cost of the equipment was $4,800,000. The equipment, which has been continually on lease since July 1, 2003, is being depreciated on a straight-line basis over an eight-year period with no salvage value. Assuming that both the lease to Snead and the lease to Quirk are appropriately recorded as operating leases for accounting purposes, what is the amount of income (expense) before income taxes that each would record as a result of the above facts for the year ended December 31, 2008?

A)

B)

C)

D)

A)

B)

C)

D)

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

46

Eddy leased equipment to Hoyle Company on May 1, 2008. At that time the collectibility of the minimum lease payments was not reasonably predictable. The lease expires on May 1, 2009. Hoyle could have bought the equipment from Eddy for $3,200,000 instead of leasing it. Eddy's accounting records showed a book value for the equipment on May 1, 2008, of $2,800,000. Eddy's depreciation on the equipment in 2008 was $360,000. During 2008, Hoyle paid $720,000 in rentals to Eddy for the 8-month period. Eddy incurred maintenance and other related costs under the terms of the lease of $64,000 in 2008. After the lease with Hoyle expires, Eddy will lease the equipment to another company for two years.

-Ignoring income taxes, the amount of expense incurred by Hoyle from this lease for the year ended December 31, 2008, should be

A) $296,000.

B) $360,000.

C) $656,000.

D) $720,000.

-Ignoring income taxes, the amount of expense incurred by Hoyle from this lease for the year ended December 31, 2008, should be

A) $296,000.

B) $360,000.

C) $656,000.

D) $720,000.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

47

Eddy leased equipment to Hoyle Company on May 1, 2008. At that time the collectibility of the minimum lease payments was not reasonably predictable. The lease expires on May 1, 2009. Hoyle could have bought the equipment from Eddy for $3,200,000 instead of leasing it. Eddy's accounting records showed a book value for the equipment on May 1, 2008, of $2,800,000. Eddy's depreciation on the equipment in 2008 was $360,000. During 2008, Hoyle paid $720,000 in rentals to Eddy for the 8-month period. Eddy incurred maintenance and other related costs under the terms of the lease of $64,000 in 2008. After the lease with Hoyle expires, Eddy will lease the equipment to another company for two years.

-The income before income taxes derived by Eddy from this lease for the year ended December 31, 2008, should be

A) $296,000.

B) $360,000.

C) $656,000.

D) $720,000.

-The income before income taxes derived by Eddy from this lease for the year ended December 31, 2008, should be

A) $296,000.

B) $360,000.

C) $656,000.

D) $720,000.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

48

Hite Company has a machine with a cost of $400,000 which also is its fair market value on the date the machine is leased to Rich Company. The lease is for 6 years and the machine is estimated to have an unguaranteed residual value of $40,000. If the lessor's interest rate implicit in the lease is 12%, the six beginning-of-the-year lease payments would be

A) $92,361.

B) $82,465.

C) $78,180.

D) $66,667.

A) $92,361.

B) $82,465.

C) $78,180.

D) $66,667.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

49

Estes Co. leased a machine to Dains Co. Assume the lease payments were made on the basis that the residual value was guaranteed and Estes gets to recognize all the profits, and at the end of the lease term, before the lessee transfers the asset to the lessor, the leased asset and obligation accounts have the following balances:

If, at the end of the lease, the fair market value of the residual value is $8,800, what gain or loss should Estes record?

A) $6,480 gain

B) $7,120 loss

C) $7,200 loss

D) $8,800 gain

If, at the end of the lease, the fair market value of the residual value is $8,800, what gain or loss should Estes record?A) $6,480 gain

B) $7,120 loss

C) $7,200 loss

D) $8,800 gain

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

50

Durham Company leased machinery to Santi Company on July 1, 2008, for a ten-year period expiring June 30, 2018. Equal annual payments under the lease are $75,000 and are due on July 1 of each year. The first payment was made on July 1, 2008. The rate of interest used by Durham and Santi is 9%. The cash selling price of the machinery is $525,000 and the cost of the machinery on Durham's accounting records was $465,000. Assuming that the lease is appropriately recorded as a sale for accounting purposes by Durham, what amount of interest revenue would Durham record for the year ended December 31, 2008?

A) $47,250

B) $40,500

C) $20,250

D) $0

A) $47,250

B) $40,500

C) $20,250

D) $0

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

51

Eby Company leased equipment to the Mills Company on July 1, 2008, for a ten-year period expiring June 30, 2018. Equal annual payments under the lease are $80,000 and are due on July 1 of each year. The first payment was made on July 1, 2008. The rate of interest contemplated by Eby and Mills is 9%. The cash selling price of the equipment is $560,000 and the cost of the equipment on Eby's accounting records was $496,000. Assuming that the lease is appropriately recorded as a sale for accounting purposes by Eby, what is the amount of profit on the sale and the interest revenue that Eby would record for the year ended December 31, 2008?

A) $64,000 and $50,400

B) $64,000 and $43,200

C) $64,000 and $21,600

D) $0 and $0

A) $64,000 and $50,400

B) $64,000 and $43,200

C) $64,000 and $21,600

D) $0 and $0

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

52

Risen Company, a dealer in machinery and equipment, leased equipment to Foran, Inc., on July 1, 2008. The lease is appropriately accounted for as a sale by Risen and as a purchase by Foran. The lease is for a 10-year period (the useful life of the asset) expiring June 30, 2018. The first of 10 equal annual payments of $621,000 was made on July 1, 2008. Risen had purchased the equipment for $3,900,000 on January 1, 2008, and established a list selling price of $5,400,000 on the equipment. Assume that the present value at July 1, 2008, of the rent payments over the lease term discounted at 8% (the appropriate interest rate) was $4,500,000.

-Assuming that Foran, Inc. uses straight-line depreciation, what is the amount of deprecia-tion and interest expense that Foran should record for the year ended December 31, 2008?

A) $225,000 and $155,160

B) $225,000 and $180,000

C) $270,000 and $155,160

D) $270,000 and $180,000

-Assuming that Foran, Inc. uses straight-line depreciation, what is the amount of deprecia-tion and interest expense that Foran should record for the year ended December 31, 2008?

A) $225,000 and $155,160

B) $225,000 and $180,000

C) $270,000 and $155,160

D) $270,000 and $180,000

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

53

Risen Company, a dealer in machinery and equipment, leased equipment to Foran, Inc., on July 1, 2008. The lease is appropriately accounted for as a sale by Risen and as a purchase by Foran. The lease is for a 10-year period (the useful life of the asset) expiring June 30, 2018. The first of 10 equal annual payments of $621,000 was made on July 1, 2008. Risen had purchased the equipment for $3,900,000 on January 1, 2008, and established a list selling price of $5,400,000 on the equipment. Assume that the present value at July 1, 2008, of the rent payments over the lease term discounted at 8% (the appropriate interest rate) was $4,500,000.

-What is the amount of profit on the sale and the amount of interest income that Risen should record for the year ended December 31, 2008?

A) $0 and $155,160

B) $600,000 and $155,160

C) $600,000 and $180,000

D) $900,000 and $360,000

-What is the amount of profit on the sale and the amount of interest income that Risen should record for the year ended December 31, 2008?

A) $0 and $155,160

B) $600,000 and $155,160

C) $600,000 and $180,000

D) $900,000 and $360,000

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

54

Mayer Company leased equipment from Lennon Company on July 1, 2008, for an eight-year period expiring June 30, 2016. Equal annual payments under the lease are $300,000 and are due on July 1 of each year. The first payment was made on July 1, 2008. The rate of interest contemplated by Mayer and Lennon is 8%. The cash selling price of the equipment is $1,861,875 and the cost of the equipment on Lennon's accounting records was $1,650,000. Assuming that the lease is appropriately recorded as a sale for accounting purposes by Lennon, what is the amount of profit on the sale and the interest income that Lennon would record for the year ended December 31, 2008?

A) $0 and $0

B) $0 and $62,475

C) $211,875 and $62,475

D) $211,875 and $74,475

A) $0 and $0

B) $0 and $62,475

C) $211,875 and $62,475

D) $211,875 and $74,475

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

55

Bohl Co. purchases land and constructs a service station and car wash for a total of $360,000. At January 2, 2007, when construction is completed, the facility and land on which it was constructed are sold to a major oil company for $400,000 and immediately leased from the oil company by Bohl. Fair value of the land at time of the sale was $40,000. The lease is a 10-year, noncancelable lease. Bohl uses straight-line depreciation for its other various business holdings. The economic life of the facility is 15 years with zero salvage value. Title to the facility and land will pass to Bohl at termination of the lease. A partial amortization schedule for this lease is as follows:

-From the viewpoint of the lessor, what type of lease is involved above?

A) Sales-type lease

B) Operating lease

C) Direct-financing lease

D) None of these

-From the viewpoint of the lessor, what type of lease is involved above?

A) Sales-type lease

B) Operating lease

C) Direct-financing lease

D) None of these

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

56

Bohl Co. purchases land and constructs a service station and car wash for a total of $360,000. At January 2, 2007, when construction is completed, the facility and land on which it was constructed are sold to a major oil company for $400,000 and immediately leased from the oil company by Bohl. Fair value of the land at time of the sale was $40,000. The lease is a 10-year, noncancelable lease. Bohl uses straight-line depreciation for its other various business holdings. The economic life of the facility is 15 years with zero salvage value. Title to the facility and land will pass to Bohl at termination of the lease. A partial amortization schedule for this lease is as follows:

-What is the amount of the lessee's liability to the lessor after the December 31, 2009 payment? (Rounded to the nearest dollar.)

A) $400,000

B) $374,902

C) $347,294

D) $316,925

-What is the amount of the lessee's liability to the lessor after the December 31, 2009 payment? (Rounded to the nearest dollar.)

A) $400,000

B) $374,902

C) $347,294

D) $316,925

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

57

On December 31, 2008, Mendez, Inc. leased machinery with a fair value of $840,000 from Cey Rentals Co. The agreement is a six-year noncancelable lease requiring annual payments of $160,000 beginning December 31, 2008. The lease is appropriately accounted for by Mendez as a capital lease. Mendez's incremental borrowing rate is 11%. Mendez knows the interest rate implicit in the lease payments is 10%.

The present value of an annuity due of 1 for 6 years at 10% is 4.7908.

The present value of an annuity due of 1 for 6 years at 11% is 4.6959.

In its December 31, 2008 balance sheet, Mendez should report a lease liability of

A) $606,528.

B) $680,000.

C) $751,344.

D) $766,528.

The present value of an annuity due of 1 for 6 years at 10% is 4.7908.

The present value of an annuity due of 1 for 6 years at 11% is 4.6959.

In its December 31, 2008 balance sheet, Mendez should report a lease liability of

A) $606,528.

B) $680,000.

C) $751,344.

D) $766,528.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

58

On December 31, 2007, Patten Co. leased a machine from Bass, Inc. for a five-year period. Equal annual payments under the lease are $630,000 (including $30,000 annual executory costs) and are due on December 31 of each year. The first payment was made on December 31, 2007, and the second payment was made on December 31, 2008. The five lease payments are discounted at 10% over the lease term. The present value of minimum lease payments at the inception of the lease and before the first annual payment was $2,502,000. The lease is appropriately accounted for as a capital lease by Patten. In its December 31, 2008 balance sheet, Patten should report a lease liability of

A) $1,902,000.

B) $1,872,000.

C) $1,711,800.

D) $1,492,200.

A) $1,902,000.

B) $1,872,000.

C) $1,711,800.

D) $1,492,200.

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

59

Castro Co. manufactures equipment that is sold or leased. On December 31, 2008, Castro leased equipment to Ermler for a five-year period ending December 31, 2013, at which date ownership of the leased asset will be transferred to Ermler. Equal payments under the lease are $220,000 (including $20,000 executory costs) and are due on December 31 of each year. The first payment was made on December 31, 2008. Collectibility of the remaining lease payments is reasonably assured, and Castro has no material cost uncertainties. The normal sales price of the equipment is $770,000, and cost is $600,000. For the year ended December 31, 2008, what amount of income should Castro realize from the lease transaction?

A) $170,000

B) $220,000

C) $230,000

D) $330,000

A) $170,000

B) $220,000

C) $230,000

D) $330,000

Unlock Deck

Unlock for access to all 59 flashcards in this deck.

Unlock Deck

k this deck

Unlock Deck

Unlock for access to all 59 flashcards in this deck.